OVERVIEW

Earnings per share (EPS) is a widely quoted financial ratio used by shareholders and potential investors in evaluating a company's profitability and value. Calculation of earnings per share is more complicated if the entity has potential common shares such as convertible securities, options, warrants, or other dilutive securities that could dilute earnings per share if they are converted or exercised. This chapter examines how basic and diluted earnings per share are calculated, and discusses their usefulness in financial analysis.

STUDY STEPS

Understanding the Calculations Required in Preparing Earnings per Share Information

Basic EPS

EPS is residual income available to common shareholders stated on a per-common-share basis, and is an indication of the amount of income that each common share earned during the year. Therefore, EPS allows common shareholders to determine how much of the company's available income can be attributed to the shares that they own. EPS is not necessarily related to the amount of dividends paid out. Rather, it represents the amount of net income attributed to each common share after paying operating costs (including interest) and paying or allocating a return to shareholders who rank higher in preference (for example, preferred shareholders).

Calculation of basic EPS is as follows:

![]()

Preferred dividends in the above formula include current year dividends on cumulative preferred shares, whether declared or not. This is because dividends on cumulative preferred shares are cumulative and will eventually have to be paid. However, dividends on non-cumulative preferred shares are only included in preferred dividends (and deducted from net income) if they were declared. This is because the rights to dividends on non-cumulative preferred shares do not accumulate if not declared in the year, and the company never has to make up a lost dividend on these shares.

Weighted average number of common shares outstanding is a calculation of the number of shares outstanding during the period, weighted by the fraction of the period that each number of shares was outstanding. Stock dividends and stock splits are treated as though they took place at the beginning of the year, even if they took place partway through the year or after year end (before issuing the financial statements). Calculation of the weighted average number of shares outstanding requires restatement of the number of shares outstanding before the stock dividend or stock split, so that earnings per share calculated before the stock dividend or stock split may be compared with earnings per share calculated after the stock dividend or stock split.

There are two types of EPS calculations:

- Basic EPS (discussed above)—an “actual” calculation, based on actual earnings and actual number of common shares outstanding

- Diluted EPS—a “what if” calculation, based on potential conversion of dilutive securities that might have a negative impact on EPS

Diluted EPS

Diluted EPS is what EPS would look like if dilutive potential common shares were actually converted to common shares, or exercised to purchase common shares, at the beginning of the period (or at the time of issuance if dilutive potential common shares were issued during the period). Dilutive potential common shares are securities or other contracts that may give holders the right to obtain common shares during or after the end of the reporting period, including convertible securities, options, and warrants that were outstanding during the period. In calculating diluted EPS, the numerator of basic EPS is adjusted to exclude the effect of preferred dividends and after-tax interest that would have been avoided if the dilutive potential common shares were converted or exercised at the beginning of the year (that is, if the extra common shares were outstanding for the whole year). The denominator of basic EPS is adjusted to include the increase in the number of common shares outstanding if the dilutive potential common shares were converted or exercised at the beginning of the year (that is, if the extra common shares were outstanding for the whole year).

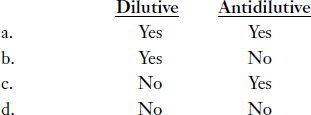

In general, the effect of dilutive potential common shares (potential common shares that would decrease EPS) is included in diluted EPS; the effect of antidilutive securities (potential common shares that would increase EPS) is not included in diluted EPS.

TIPS ON CHAPTER TOPICS

- An entity with a simple capital structure (with only common shares and preferred shares and/or debt without conversion rights) must report basic EPS amounts for income from continuing operations and for net income on the face of the income statement. An entity with a complex capital structure (with one or more securities outstanding that could have a dilutive effect) must report basic and diluted EPS for income from continuing operations and for net income on the face of the income statement with equal prominence. EPS related to discontinued operations (net of tax) may be reported either on the face of the income statement or in the notes to the financial statements.

- A dilutive security is a security that would reduce EPS (or increase net loss per share) if it was converted to common shares or exercised to purchase common shares. An antidilutive security is a security that would increase EPS (or decrease net loss per share).

- Antidilutive securities are excluded from the calculation of diluted EPS. This means that in calculating diluted EPS, a convertible bond is assumed to be converted to common shares only if the effect of that assumption is dilutive. If conversion of a convertible bond would be antidilutive, calculation of diluted EPS would assume that the bond would not be converted to common shares. Inclusion of antidilutive securities would increase diluted EPS, which would contradict the purpose of diluted EPS: to present the effects of what will likely occur and the worst-case dilutive situation.

- Securities such as convertible bonds, convertible preferred shares, options, warrants, mandatorily convertible instruments, and contingently issuable shares are referred to as “potential common shares,” “potential ordinary shares,” or “potentially dilutive securities.”

- Common shares are sometimes referred to as ordinary shares.

- Mandatorily convertible instruments are assumed to be converted for purposes of calculating basic EPS, because the issuance of common shares related to these securities will be required in future.

- Contingently issuable shares are potential common shares that are issuable in exchange for little or no consideration once a condition involving uncertainty has been resolved. For example, in an acquisition of another company, as part of the payment for the acquisition, the acquirer may promise to issue additional shares at a later date, if the acquired company earns profit above a certain amount in the year after acquisition. Contingently issuable shares that are issuable simply based on the passage of time are not considered contingently issuable since it is certain that time will pass; these shares are considered outstanding in the calculation of basic EPS. Contingently issuable shares that are issuable depending on the outcome of a condition (for example, future profit levels or performance targets) are considered outstanding in the calculation of basic EPS when the conditions are satisfied. See Illustration 17-1 for further discussion.

- ASPE does not prescribe standards for calculating EPS, or require EPS disclosure in financial statements, whereas IFRS does. Therefore, EPS standards apply only to those entities in Canada that present EPS and apply IFRS.

Calculation of Earnings Per Share

Step 1: Calculate weighted average number of common shares outstanding.

(a) If common shares were issued during the period, weight them according to the length of time in the period the shares were outstanding, relative to the total time in the period.

(b) If common shares were issued in connection with a stock dividend or a stock split declared during the period, treat these shares retroactively (assume they have been outstanding since the beginning of the year), even if the stock dividend or stock split is declared partway through the year or after the end of the period (but before financial statements are published). Also adjust prior periods' comparative EPS presented for the effects of the stock dividend or stock split.

See Illustration 17-2 for a shortcut method of calculating weighted average number of common shares outstanding.

Step 2: Calculate basic EPS (EPS before any assumptions or adjustments).

![]()

The numerator represents income available to common shareholders, or net income minus dividends on preferred shares, where dividends on preferred shares include dividends declared on non-cumulative preferred shares and current year dividends on cumulative preferred shares (whether declared or not). Dividends in arrears on cumulative preferred shares have no effect on current year basic EPS.

- Dividends declared and/or paid during the year on common shares have no effect on basic EPS.

- If there is a net loss rather than net income, preferred dividends are added to the net loss in the numerator of basic EPS.

- Mandatorily convertible instruments are assumed to be converted for purposes of calculating basic EPS, because the issuance of common shares related to these securities will be required in future.

Step 3: Calculate diluted EPS.

(a) Adjust the formula for basic EPS:

(b) Convertible securities

- Apply the if-converted method. For each convertible security, assume conversion to common shares if conversion to common shares would be dilutive.

- Conversion to common shares would be dilutive if it would result in a lower EPS. Conversion to common shares would be antidilutive if it would result in a higher EPS or a decrease in net loss per share.

- A quick test to determine if a convertible debt instrument is antidilutive is as follows: If the amount of interest (net of tax) that would have been avoided (if converted) per additional common share exceeds basic EPS, the convertible debt is antidilutive.

- A quick test to determine if a convertible preferred share is antidilutive is as follows: If the amount of preferred dividends that would have been avoided (if converted) per additional common share exceeds basic EPS, the effect is antidilutive.

- Assume that convertible debt was converted at the beginning of the period for which EPS is being calculated (or at the time of issuance, if convertible debt was issued during the period). Add back interest (net of tax savings on interest expense) that would have been avoided as a result of the conversion, which should increase the EPS numerator. Add the appropriate weighted average number of common shares outstanding to the EPS denominator, to reflect the additional common shares that are assumed to be issued.

- Assume that convertible preferred shares were converted at the beginning of the period for which EPS is being calculated (or at the time of issuance, if convertible preferred shares were issued during the period). Add back preferred dividends that were deducted in the calculation of basic EPS, thereby increasing the EPS numerator. Add the appropriate weighted average number of common shares outstanding, to reflect the additional common shares that are assumed to be issued.

In using the “if-converted” method for convertible debt, interest expense is added back to the EPS numerator and the related tax savings are deducted. In using the “if-converted” method for a convertible preferred share, preferred dividends are added back to the EPS numerator (because they were deducted in the calculation of basic EPS); however, there is no related tax effect to adjust for because preferred dividends are not tax deductible.

- If there is a scale of conversion rates, use the rate that is most advantageous from the security holder's standpoint.

(c) Options and warrants

- If exercising options or warrants would decrease EPS, include the effect of exercising the dilutive options or warrants in the calculation of EPS.

A written call option or warrant is dilutive if the average market price per common share during the period is greater than the exercise price of the option or warrant. A written put option or warrant is dilutive if the exercise price of the option or warrant is greater than the average market price per common share during the period.

- For dilutive written call options and warrants, apply the treasury stock method. If written call options and warrants are exercised, the option holder normally pays cash into the company to purchase the company's shares. The dilutive effect of written call options and warrants is calculated using the treasury stock method. This method assumes that (1) the options and warrants are exercised at the beginning of the period (or at the time of issuance, if options and warrants were issued during the period) resulting in issuance of the agreed-upon number of common shares (per option terms) and (2) the proceeds from the exercise would be used to purchase common shares in the open market at the average market price per share during the period, to return some shares to the treasury. Note that no adjustment to the EPS numerator is required to include the dilutive effect of written call options and warrants—only the EPS denominator is affected. In summary, the EPS denominator is adjusted to reflect the increase in the number of shares issued upon the exercise of options and warrants, less the number of shares purchasable in the open market (at average market price per share during the period) with the proceeds from the exercise.

- For dilutive written put options and forward purchase contracts, apply the reverse treasury stock method. If written put options and forward purchase contracts are exercised or settled, the holder would sell the company's shares to the company, normally requiring the company to pay cash to the holder. The dilutive effect of written put options and forward purchase contracts is calculated using the reverse treasury stock method. This method assumes that (1) the company would issue enough common shares in the open market at the beginning of the period (or at the time of issuance, if options and warrants were issued during the period) to generate enough cash to buy the agreed-upon number of common shares (per option or forward terms), with issuance calculated at the average market price per share during the period and (2) the number of shares received from the holder (per option or forward terms) would be returned to the treasury. In summary, the EPS denominator is adjusted to reflect the increase in the number of shares issued in the open market (at average market price per share during the period) to obtain enough proceeds to purchase the common shares from the holders (per option or forward terms), less the number of common shares received from the holders (per option or forward terms).

- Purchased options and warrants will always be antidilutive, because it is assumed that the company will exercise the options or warrants only when they are in the money. Therefore, purchased options and warrants are not included in the calculation of diluted EPS.

(d) Contingently issuable shares

- Common shares that are issuable only after passage of a certain amount of time (in the future) are considered outstanding when calculating both basic and diluted EPS because it is certain that time will pass. They are not considered contingently issuable shares.

- Contingently issuable common shares that are issuable if a certain condition is met (for example, if a certain profit or market share price level is met) are considered outstanding from the beginning of the current period, if all conditions have been met as required. If the condition has not yet been met, but may be in the future, the contingently issuable common shares are included in diluted EPS only if the required condition to be met in the future (such as the share's market price or level of earnings) has reached the required level by the end of the current reporting period.

- Calculation of diluted EPS should not assume the conversion, exercise, or issuance of securities that would have an antidilutive effect on EPS. However, the actual conversion, exercise, or issuance of securities that had an antidilutive effect on EPS is included in the calculation of EPS, with an increase in the number of common shares outstanding weighted according to date of conversion, exercise, or satisfaction of conditions.

- In determining whether potential common shares are dilutive or antidilutive, each issue or series of issues of potential common shares should be considered separately rather than in aggregate.

- Convertible securities may be dilutive on their own but antidilutive if included with other potential common shares in the calculation of diluted EPS. To determine maximum potential dilution, each issue or series of issues of potential common shares is considered in sequence from most dilutive to least dilutive. That is, dilutive potential common shares with the lowest incremental effect per share are included in diluted EPS before those with a higher incremental effect per share. (Generally, options and warrants are included first because the treasury stock method does not affect the EPS numerator.)

- An entity that reports discontinued operations should use income before discontinued operations or income from continuing operations (adjusted for preferred dividends) as the “control number” in determining whether potential common shares are dilutive or antidilutive. That is, the same number of potential common shares used in calculating diluted EPS for income before discontinued operations should be used in calculating all other diluted EPS amounts even if those amounts will be antidilutive relative to their respective basic per-share amounts. For example, assume that Corporation A has income before discontinued operations of $2,400, loss from discontinued operations of $(3,600), net loss of $(1,200), and 1,000 common shares and 200 potential common shares outstanding. Corporation A's basic per-share amounts would be $2.40 for income before discontinued operations, $(3.60) for discontinued operations, and $(1.20) for net loss. Corporation A would include the 200 potential common shares in the denominator of its diluted per-share amount before discontinued operations because the resulting $2.00 per share is dilutive. (For illustrative purposes, assume no numerator effect on those 200 potential common shares.) Because income before discontinued operations is the control number, Corporation A must also include those 200 potential common shares in the calculation of the other diluted per-share amounts, even though the resulting per-share amounts [$(3.00) per share from discontinued operations and $(1.00) per share for net loss] are antidilutive relative to (resulting in a smaller loss per share compared with) their respective basic per-share amounts.

- If an entity has a loss from continuing operations or a loss from continuing operations available to common shareholders (after subtraction of preferred share dividends), including potential common shares in the diluted per-share calculation will always be antidilutive, and will result in a smaller per-share loss from continuing operations. Therefore, if an entity has a loss from continuing operations or a loss from continuing operations available to common shareholders (after subtraction of preferred share dividends), no potential common shares should be included in the calculation of any diluted per-share amounts. However, as noted above, if an entity has income from continuing operations, but a loss from discontinued operations and a net loss, calculation of all diluted per-share amounts should include potential common shares.

- If an entity has a complex capital structure, requiring presentation of both basic and diluted EPS, it must also disclose a reconciliation of the numerators and denominators of both basic and diluted EPS for income before discontinued operations, including individual income and share amounts for each class of securities that affects EPS.

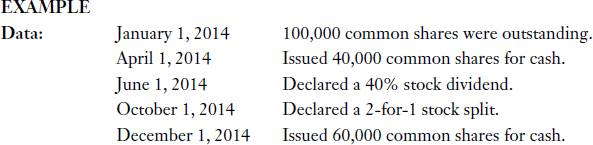

Shortcut Method for Calculating Weighted Average Number of Common Shares Outstanding

| Step 1: | Begin with the number of common shares outstanding at the beginning of the period and assume they were outstanding for the entire year. (Multiply or weight the number by |

| Step 2: | Find the first transaction that occurred during the year that changed the number of common shares outstanding, and adjust the balance in the Weighted Shares column accordingly.

(a) If shares were issued for cash or other assets, weight the number of new shares by multiplying the number of new shares by a fraction, where the numerator of the fraction is the number of months in the period the shares were outstanding and the denominator is the number of months in the period. Add the resulting amount to the Weighted Shares column to arrive at a new balance. (b) If shares were issued in a stock dividend or a stock split, adjust for these shares retroactively by taking an appropriate multiple of the balance in the Weighted Shares column to arrive at a new balance. Ignore the date of the stock dividend or stock split; the multiple is determined by the size of the stock dividend or stock split. (c) If shares were acquired as treasury shares or retired by the corporation, weight the shares to account for the time they were not outstanding, and deduct the amount from the Weighted Shares balance to arrive at a new balance. |

| Step 3: | In chronological order, analyze each of the other transactions that occurred during the year that changed the number of common shares outstanding. Adjust the balance in the Weighted Shares column accordingly (as discussed in Step 2 above). |

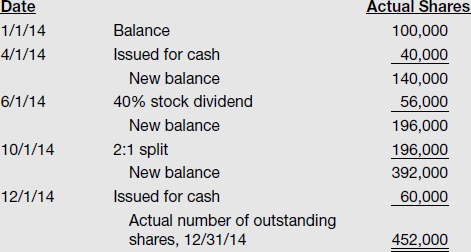

- Notice how the calculation of the weighted average number of common shares outstanding for the period differs from the calculation of the actual number of common shares outstanding at the end of the period. Actual number of common shares outstanding at December 31, 2014, is calculated as follows:

- Assume that in addition to the transactions listed above, a 10% stock dividend was declared on January 7, 2015, before the 2014 financial statements were issued. Weighted average number of common shares outstanding for purposes of calculating EPS for 2014 would be 405,900 (369,000 × 110% = 405,900). The actual number of common shares outstanding to be reported on the statement of financial position at December 31, 2014, however, would remain unchanged at 452,000.

PURPOSE: This exercise will apply the guidelines for calculating the weighted average number of common shares outstanding.

When the number of common shares outstanding varies during the year, the weighted average number of common shares outstanding must be calculated before EPS can be calculated.

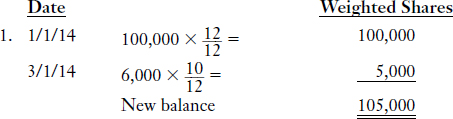

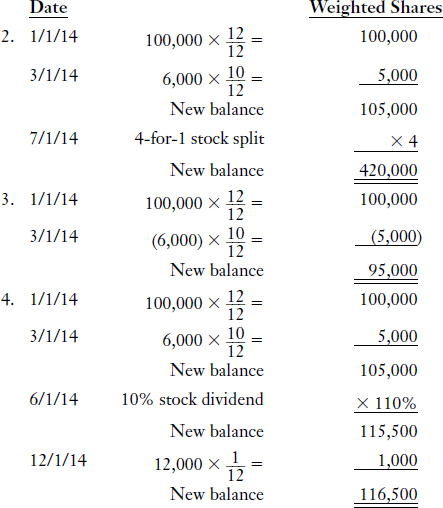

Listed below are details regarding common shares outstanding for four different companies:

- Jackson Corporation had 100,000 common shares outstanding on January 1, 2014. On March 1, 6,000 common shares were issued for cash.

- Buffet Corporation had 100,000 common shares outstanding on January 1, 2014. On March 1, 6,000 common shares were issued for cash. On July 1, a 4-for-1 stock split was declared.

- Harris Corporation had 100,000 common shares outstanding on January 1, 2014. On March 1, 6,000 common shares were reacquired by Harris.

- Van Kralingen Corporation had 100,000 common shares outstanding on January 1, 2014. On March 1, 6,000 common shares were issued for cash. On June 1, a 10% stock dividend was declared. On December 1, 12,000 common shares were issued for cash.

Instructions

(a) Calculate the weighted average number of common shares outstanding for 2014 (for the purposes of calculating EPS) for each of the independent situations above.

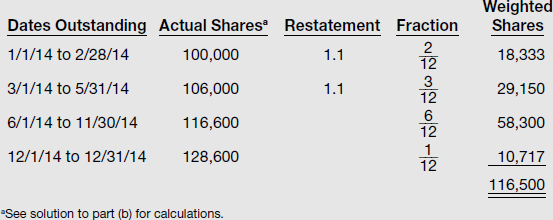

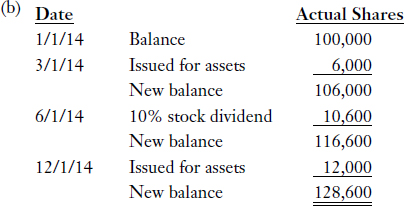

(b) Calculate the number of common shares outstanding to be reported on the statement of financial position at December 31, 2014, for Van Kralingen Corporation (situation 4).

Solution to Exercise 17-1

(a) Explanation: Use the shortcut method explained in Illustration 17-2.

Calculation of the weighted average number of common shares outstanding uses the same concept that is applied in the calculation of equivalent units of production for a manufacturing firm. In the situation above, the calculation indicates that having 6,000 shares outstanding for 10 months of the year is equivalent to having 5,000 shares outstanding for 12 months. Weighted average number of shares outstanding is sometimes referred to as “equivalent shares.”

Weighted average number of common shares outstanding for Van Kralingen Corporation can also be calculated as follows:

For calculation of EPS, a stock dividend or a stock split requires retroactive adjustment of the number of shares outstanding. A 10% stock dividend causes a 10% increase in the number of shares outstanding. Therefore, to retroactively adjust the number of shares outstanding, previous amounts of actual shares outstanding are multiplied by 110% (which is 1.1 in decimal form).

When shares are issued for cash or other assets, the shares are weighted by the number of months they are outstanding in the period relative to the number of months in the period for which EPS is being calculated. When shares are issued in a stock dividend or a stock split, they are not weighted; rather, the number of shares outstanding is retroactively adjusted. The reason for the difference in treatment is that when cash or other assets are received, the entity has more resources, and therefore, it has an opportunity to increase net income by earning a return on those new assets for the months that the new assets are available. When shares are issued in connection with a stock dividend or a stock split, the entity does not receive any new resources, and in order for the entity's EPS calculations in successive periods to be meaningful, all EPS calculations must be based on the entity's rearranged capital structure. As a result, stock dividends and stock splits must be treated retroactively. This retroactive treatment causes an adjustment to the weighted average number of common shares outstanding for any other comparative years presented. When comparative financial statements for a prior period are presented, EPS amounts for the prior period are also restated to reflect all stock dividends and stock splits that occurred in subsequent periods. Thus, a stock dividend declared in 2014 requires retroactive restatement of 2013 EPS amounts when the 2013 income statement is republished in 2014 for comparative purposes.

PURPOSE: This exercise will illustrate the application of the treasury stock method.

Sherman Corporation had 200,000 common shares outstanding during 2014. On January 1, 2014, 40,000 stock options were granted. Each option entitles the holder to purchase one common share at $40. The options become exercisable in 2016.

Net income for 2014 was $400,000. For 2014, the average market price per share during the year was $50; the closing market price per share at the end of the year was $54.

Instructions

(a) Calculate the amount(s) that Sherman Corporation should report for EPS for 2014.

(b) Explain how your answer(s) to part (a) would change if the options were issued on April 1, 2014, rather than January 1, 2014.

Solution to Exercise 17-2

(a) APPROACH: Follow the steps for calculating EPS as outlined in Illustration 17-1.

Step 1: Calculate weighted average number of common shares outstanding.

There were no changes in the 200,000 common shares outstanding during 2014. Therefore, the weighted average number of common shares outstanding is 200,000.

Step 2: Calculate basic EPS (EPS before any assumptions or adjustments).

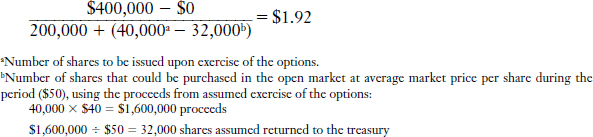

![]()

Step 3: Calculate diluted EPS.

- For the written call options, apply the treasury stock method.

- Use the quick test to determine if the options are dilutive. Compare average market price per share with exercise price of the option. The exercise price ($40) is less than average market price per share ($50), so the options are dilutive.

- Adjust the basic formula:

- Notice that the incremental number of shares calculated using the treasury stock method is 8,000 in this example (40,000 − 32,000). If average market price per share was less than the exercise price, the number of shares assumed to be returned to the treasury would exceed the number of shares issued upon exercise of the options, resulting in a decrease in the EPS denominator, which would have an antidilutive effect on EPS. Therefore, if the average market price per share was less than the exercise price, exercise of the options would not be assumed. In calculating diluted EPS, never make assumptions that are antidilutive.

- Notice why the treasury stock method is so named; proceeds from the assumed exercise of options are assumed to be used for purchase of treasury shares.

For 2014, Sherman Corporation should report dual presentation of EPS as follows:

$2.00 basic earnings per share, and

$1.92 diluted earnings per share.

(b) If the options were issued on April 1, 2014, exercise of the options would be assumed to take place on April 1 rather than on January 1. Therefore, adjustment to the EPS denominator would be weighted as follows: ![]() × (40,000 − 32,000) = 6,000.

× (40,000 − 32,000) = 6,000.

Diluted EPS would be calculated as follows:

![]()

PURPOSE: This exercise will illustrate the proper treatment of convertible securities in calculating EPS.

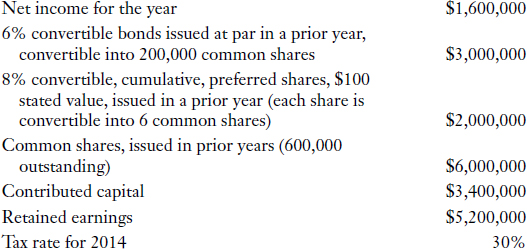

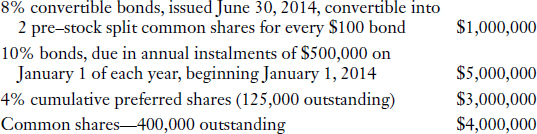

The following data pertain to the Trent Corporation at December 31, 2014:

During 2014, there were no changes in the number of common shares, preferred shares, or convertible bonds outstanding. There are no treasury shares held.

Instructions

(a) Calculate basic EPS for 2014.

(b) Calculate diluted EPS for 2014.

(c) Explain whether dual presentation of EPS (presentation of both basic and diluted EPS) is required for 2014.

Solution to Exercise 17-3

(a) $2.40. (See Step 2 below.)

(b) $1.88. (See Step 3 below.)

(c) Yes, dual presentation of EPS is required for 2014, because Trent has some dilutive securities outstanding.

For the calculation of EPS, follow the steps (in order) listed in Illustration 17-1. By following an organized approach to the calculation of EPS, you are less likely to overlook guidelines that may affect your solution.

EXPLANATION:

Step 1: Calculate weighted average number of common shares outstanding.

There was no change in the number of common shares outstanding during 2014. There are no treasury shares; thus, the weighted average number of common shares outstanding equals the number of shares issued, which is 600,000 (given).

Step 2: Calculate basic EPS (EPS before any assumptions or adjustments).

Recall that for cumulative preferred shares, the current year dividend is deducted from the EPS numerator, whether it was declared or not.

Step 3: Calculate diluted EPS.

![]()

Notice why the “if-converted” method is so named; diluted EPS is calculated assuming the conversion of dilutive convertible securities.

When there is more than one potentially dilutive security outstanding, the steps for calculating diluted EPS are as follows:

- For each dilutive security, determine the incremental effect per additional share assuming exercise or conversion.

- Using the results from step 1, rank the dilutive securities from smallest to largest in terms of incremental effect per share; that is, rank the dilutive securities from most dilutive to least dilutive.

- Beginning with basic EPS (i.e., using the weighted average number of common shares outstanding or $2.40 in this problem), recalculate EPS by adding the effect of the most dilutive security (the security with the smallest incremental effect per share, according the calculations in step 2). If the result from the recalculation of EPS is less than $2.40, add the effect of the next most dilutive security and recalculate EPS again. Continue this process until recalculated EPS is no longer smaller than the previous recalculation of EPS, or there are no more dilutive securities to test.

This means that the most dilutive potential common shares are included in diluted EPS calculations before those that are less dilutive.

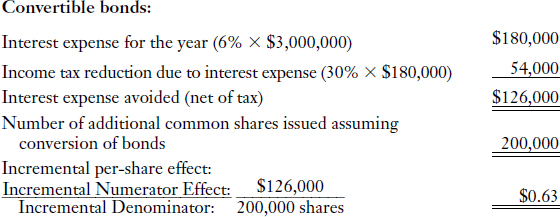

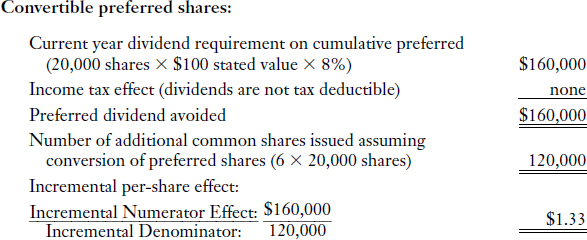

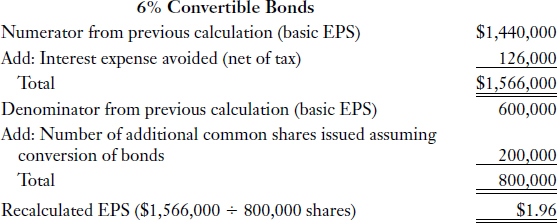

These three steps are now applied to Trent Corporation. Trent has two securities (6% convertible bonds and 8% convertible, cumulative, preferred shares) that could reduce EPS.

The first step in calculating diluted EPS is to determine the incremental effect per additional share of each potentially dilutive security.

Step 1: For each dilutive security, determine the incremental per-share effect on EPS assuming exercise or conversion.

Step 2: Rank the results from Step 1.

Ranking of the two potentially dilutive securities (from lowest to highest incremental effect per share) is as follows:

Step 3: Calculate diluted EPS.

The next step is to calculate diluted EPS based on the ranking above. Starting with basic EPS of $2.40 calculated previously, add the incremental effect of converting the bonds, as follows:

Since recalculated EPS is smaller compared with the previous calculation of EPS (EPS decreased from basic EPS of $2.40 to recalculated EPS of $1.96), the effect of converting the bonds is dilutive.

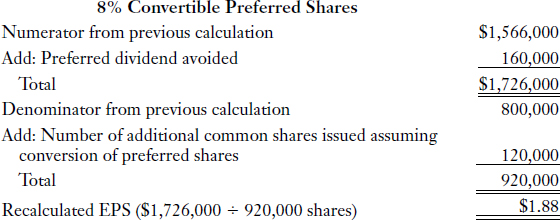

Because the incremental per-share effect of the convertible preferred shares (of $1.33) is lower than the recalculated $1.96, the next step is to recalculate EPS again, this time adding the incremental effect of converting the preferred shares:

Since the recalculated EPS amount is smaller than the previous recalculation of EPS (EPS decreased from $1.96 to $1.88), the effect of converting the preferred shares is dilutive. Therefore, diluted EPS is $1.88.

PURPOSE: This exercise will illustrate more complex EPS calculations.

EPS Limited (EL) has the following capital structure at December 31, 2014:

The following additional information is available:

- During the year, the entire $1 million of previously issued 6% convertible bonds were converted into 20,000 common shares on June 30, 2014. The 8% convertible bonds were issued at the same time.

- On March 31, 2013, 25,000 warrants were issued for $2 each, allowing holders to purchase one pre-split common share per warrant for $50. All warrants are still outstanding at December 31, 2014.

- On September 30, 2014, there was a 2-for-1 stock split.

- At year end, EL common shares were trading at $28 per share, a $4 increase over market price per share at the beginning of the year (including the effect of retroactive adjustment due to the stock split).

- The income tax rate for 2014 is 30%.

- Net income after tax for the year ended December 31, 2014, was $1.1 million.

- It is EL's company policy to update all agreements after a stock split such that arrangements made prior to the stock split are adjusted to reflect the split. For instance, if a bond was convertible into two pre-split shares, after the stock split, the bond would be convertible into four post-split shares.

Instructions

(a) Calculate basic EPS for the year ended December 31, 2014.

(b) Calculate diluted EPS.

Solution to Exercise 17-4

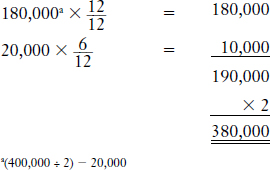

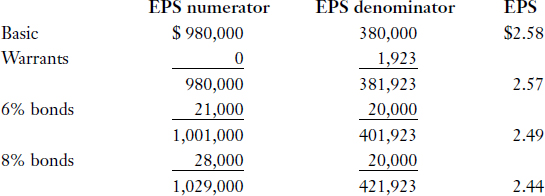

(a) Net income − preferred dividends = $1,100,000 − ($3,000,000 × .04) = $980,000

Weighted average number of common shares outstanding:

Basic EPS = $980,000 ÷ 380,000 = $2.58

(b) Diluted EPS should be calculated since there are dilutive securities outstanding.

First, identify the dilutive securities, and determine the incremental per-share effect on EPS assuming the exercise or conversion of each:

- 8% convertible bonds

- 6% convertible bonds

- Warrants

Second, rank the dilutive securities from lowest to highest incremental effect per share.

Third, calculate diluted EPS.

8% bonds

Impact on EPS numerator

![]()

Had the bonds been converted, $28,000 in interest expense would have been avoided. This is an after-tax amount since basic EPS is based on net income after tax. This is also a half-year amount since the bonds were issued on June 30.

Impact on EPS denominator

![]()

$1,000,000 ÷ 100 × 2 = 20,000 common shares would have been issued; however, this amount is weighted since the bonds were issued on June 30. (If the bonds had been outstanding since the beginning of the year, there would have been no need to weight the number of shares.) This amount also takes the 2-for-1 stock split into account (2 pre-split common shares for every $100 bond).

Incremental effect per additional share

![]()

Since the incremental effect per additional share is less than basic EPS, the 8% bonds are dilutive.

6% bonds

Impact on EPS numerator

![]()

We must consider the effect of these bonds even though they were already converted at year end. The objective is to consider all actual and potential dilutive conversions as though they took place at the beginning of the year (unless the dilutive securities were issued during the year).

Impact on EPS denominator

![]()

This amount is adjusted for the stock split, and weighted because conversion took place on June 30.

Incremental effect per additional share

![]()

Since the incremental effect per additional share is less than basic EPS, the 6% bonds are considered dilutive.

Warrants

Average market price per common share during the year is calculated as follows:

If the 25,000 warrants were exercised, the company would receive 25,000 × $50 = $1,250,000, which would be used to purchase shares in the open market (with purchase calculated at average market price per common share during the year).

![]()

Therefore, EL would have a net increase of 1,923 in common shares outstanding (50,000 − 48,077), and the warrants are considered dilutive.

The final step is to calculate diluted EPS, starting with the instrument that has the most dilutive effect first.

EPS information would be presented at the bottom of the income statement. If comparative financial statements are reported, basic and diluted EPS would be shown for the current year and the comparative year(s). Remember that comparative year(s') EPS calculations would be adjusted to reflect the stock split.

ANALYSIS OF MULTIPLE-CHOICE QUESTIONS

Question

- When calculating basic EPS, the numerator should be adjusted for:

EXPLANATION: Care should be taken to deduct current year undeclared dividends on cumulative preferred shares, as well as any other preferred share dividends declared in the year. (Solution = d.)

Question

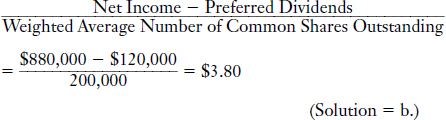

2. Wong Corporation reported net income of $880,000 for 2014. During 2014, a dividend of $120,000 was declared on preferred shares and another dividend of $200,000 was declared on common shares. There were no changes in shares outstanding during 2014 (200,000 common shares were outstanding and 40,000 preferred shares were outstanding). There were no potentially dilutive securities outstanding. EPS to be reported for 2014 is:

- $4.40.

- $3.80.

- $3.67.

- $2.80.

- none of the above.

EXPLANATION: Write down the formula for basic EPS. Solve using the data provided.

Question

3. Which of the following does not require retroactive adjustment when calculating the weighted average number of common shares outstanding for basic EPS?

- a stock split

- a reverse split

- a stock dividend

- a share conversion

EXPLANATION: If a transaction does not change each shareholder's relative interest in the company's earnings and net assets, retroactive adjustment is required when calculating the weighted average number of common shares outstanding for basic EPS. A share conversion would be accounted for prospectively since it would affect each shareholder's interest in earnings and net assets. (Solution = d.)

Question

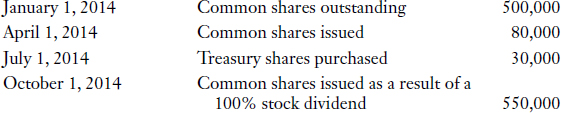

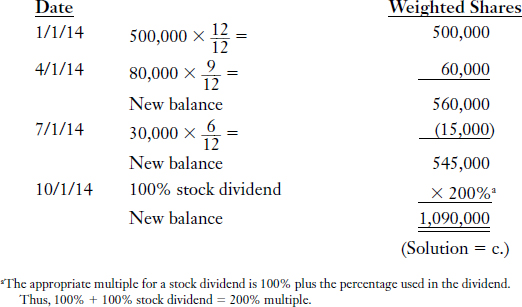

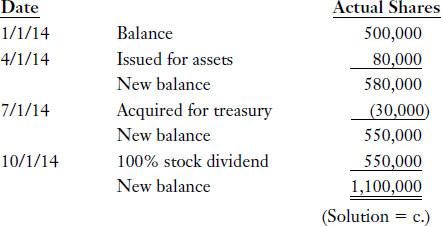

4. The Colby Corporation has the following data for 2014:

The number of shares to be used in calculating EPS for 2014 is:

- 1,130,000.

- 1,100,000.

- 1,090,000.

- 682,500.

EXPLANATION: Follow the steps listed in Illustration 17-2 to calculate the weighted average number of common shares outstanding for 2014.

Question

5. Refer to Question 4 above. The number of common shares actually outstanding at the end of 2014 is:

EXPLANATION:

Question

6. At December 31, 2013, Opal Company had 200,000 common shares and 5,000 8%, $100 stated value cumulative preferred shares outstanding. No dividends were declared on either preferred or common shares in 2013 or 2014. On February 10, 2015, prior to the issuance of financial statements for the year ended December 31, 2014, Opal declared a 100% stock split on its common shares. Net income for 2014 was $480,000. In its 2014 financial statements, Opal's 2014 EPS should read:

- $2.40.

- $2.20.

- $1.20.

- $1.10.

EXPLANATION:

![]()

Current year dividend on cumulative preferred shares is deducted in the EPS numerator, whether declared or not. However, dividends in arrears (prior years' dividends) do not affect calculation of EPS. Stock dividends and stock splits are treated retroactively for all periods presented, even if they occur partway through the year or after the end of the current year (but before the financial statements are issued). (Solution = d.)

Question

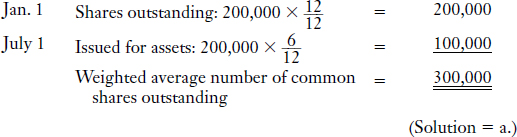

7. Tempo, Inc. had 200,000 common shares issued and outstanding at December 31, 2013. On July 1, 2014, an additional 200,000 common shares were issued for cash. Tempo also had stock options outstanding at the beginning and end of 2014, which allow the holders to purchase 60,000 common shares at $20 per share. Tempo's average market price per share was $15 during 2014. Tempo's market price per share was $25 at December 31, 2014. What is the number of shares that should be used in the denominator of diluted EPS for the year ended December 31, 2014?

- 300,000

- 360,000

- 400,000

- 415,000

EXPLANATION: Use the treasury stock method to determine the number of shares to be used in calculating diluted EPS. However, only make assumptions about the exercising of options when those assumptions are not antidilutive. A quick test to determine whether these options are dilutive or antidilutive is to compare average market price per share ($15) with exercise price ($20). Average market price per share is not higher; so in applying the treasury stock method, assumed exercise of the options would have an antidilutive effect. Therefore, the exercise of options should not be assumed. Only the weighted average number of common shares actually outstanding should be used in calculating EPS:

- You could calculate basic EPS, and calculate diluted EPS assuming exercise of the options and application of the treasury stock method. The $1.2 million in exercise proceeds would be assumed to be used to buy shares in the open market (at $15 average market price per share) for return to the treasury. This would result in the following adjustments to the EPS denominator:

- Add 60,000 shares due to the assumed exercise of options.

- Deduct 80,000 ($1.2 million ÷ $15 per share) shares due to the assumed purchase of shares in the open market for return to the treasury.

- The net result of these assumptions is a decrease in the number of shares used to calculate diluted EPS, which has an antidilutive effect on EPS. Thus, in this example, the exercise of options should not be assumed in calculating diluted EPS.

Question

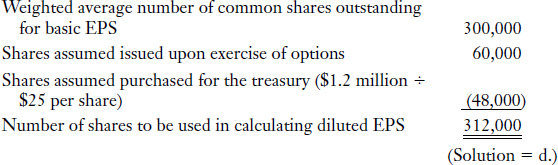

8. Refer to the facts of Question 7 above. If Tempo's average market price per share was $25 rather than $15 during 2014, what is the number of shares that should be used in calculating diluted EPS for the year ended December 31, 2014?

- 448,000

- 348,000

- 330,000

- 312,000

EXPLANATION: Use the treasury stock method to determine the number of shares to be used in calculating diluted EPS. The weighted average number of common shares actually outstanding is 300,000 (see the explanation to Question 7 above for this calculation). If the average market price per share was $25, the average market price per share ($25) would exceed the exercise price of the options ($20), and the assumed exercise of the options would have a dilutive effect on EPS. The number of shares to be used in calculating diluted EPS would be as follows:

A comparison of 312,000 shares (the number of shares to be used in calculating diluted EPS determined using the treasury stock method), with the weighted average number of common shares outstanding for basic EPS (300,000) also indicates a dilutive effect on EPS.

Question

9. A convertible bond issue should be included in calculating diluted EPS if the effect of its inclusion is:

EXPLANATION: A convertible security is a potentially dilutive security. All potentially dilutive securities that have a dilutive effect on EPS should be included in calculating diluted EPS. No potentially dilutive securities that have an antidilutive effect on EPS should be included in calculating diluted EPS. (Solution = b.)

Question

10. Which of the following are never considered dilutive securities?

- debt that is convertible into preferred shares

- convertible preferred shares

- stock options

- stock warrants

EXPLANATION: Dilution pertains to the effect on the number of potential common shares and the act of diluting individual common shareholders' proportionate interests in the entity, as well as in their share of the earnings. Therefore, convertible preferred shares, stock options, and stock warrants are potentially dilutive because if converted or exercised, they result in more common shares outstanding and (usually) lower earnings per common share. (Solution = a.)