OVERVIEW

Under both IFRS and ASPE, a complete set of basic financial statements includes a statement of cash flows for each period for which results of operations are provided. The primary purpose of a statement of cash flows is to provide relevant information about an entity's sources (receipts) and uses (payments) of cash during a period. When analyzed in conjunction with related disclosures and information contained in the other financial statements, the statement of cash flows helps investors, creditors, and others to assess: (a) the entity's ability to generate positive future net cash flows; (b) the entity's ability to meet its obligations and to pay dividends; (c) the entity's need for external financing; (d) the reasons for the difference between net income and cash flow from operating activities; and (e) the effects of both cash and noncash investing and financing transactions during the period on the entity's financial position. This chapter discusses preparation of a statement of cash flows, and related presentation, disclosure, and analysis issues.

STUDY STEPS

Understanding the Value of the Statement of Cash Flows

The primary objective of the statement of cash flows is to provide relevant information about a company's sources of cash (such as operating activities, sale of assets, and external financing) and uses of cash (such as operating activities, purchase of assets, and repaying debt). The statement of cash flows focuses on a company's liquidity and solvency. A company may report positive net income on the income statement, but have negative cash flow from operating activities. This relationship would be highlighted on the statement of cash flows.

A key number on the statement of cash flows is net cash flow from operating activities, or net cash provided by (used in) operating activities. In general, companies that perform better generate higher positive net cash flow from operating activities. These internally generated funds can be used to finance other activities such as business expansion, repayment of debt, and payment of dividends. If a company internally generates high positive net cash flow from operating activities, it may not have to rely heavily on external financing from creditors or shareholders. This is an advantage because external financing often carries with it commitments to pay a return to its providers (such as interest) and to repay principal, which can put an undue strain on the company's cash flows.

The statement of cash flows is valuable to users because it provides cash basis information, whereas measurement of net income on the income statement is affected by estimates and the preparers' choice of accounting principles and procedures.

Becoming Proficient in Related Calculations

In this section, we will discuss the preparation and interpretation of the statement of cash flows.

The statement of cash flows shows changes in cash and cash equivalents, sources of cash, and uses of cash during the period. On the statement of cash flows, this information is divided into the following three categories:

- Cash flow from operating activities

- Cash flow from investing activities

- Cash flow from financing activities

Operating activities are the enterprise's principal revenue-producing activities and all other activities that are not investing or financing activities.

Investing activities involve the acquisition and disposal of long-term assets and other investments that are not included in cash equivalents or acquired for trading purposes.

Financing activities result in changes in the size and composition of the enterprise's equity capital and borrowings.

There are two approaches to the preparation of the statement of cash flows:

- analysis of the Cash account (in the General Ledger)

- the work sheet approach

Since the statement of cash flows includes only transactions that involve cash (and cash equivalents), one way to identify relevant transactions is to analyze the cash account in the general ledger. The relevant transactions can then be classified by category (operating, investing, or financing), and analyzed individually to determine the effect on the statement of cash flows.

Note that in practice, cash transactions are often coded or sorted at the time of entry in the general ledger, in order to have sufficient information to produce the statement of cash flows at a later date. For example, a company may have separate general ledger accounts entitled Cash—Operating, Cash—Investing, and Cash—Financing.

The work sheet approach is an alternative way to perform the analysis required to produce a statement of cash flows. This approach involves:

- Determining the change in cash (and cash equivalents).

- Recording information from the income statement on the statement of cash flows. Most cash activities in this step are classified as cash flows from operating activities.

- Analyzing the change in each statement of financial position account, identifying all cash flows associated with changes in the account balance, and recording the effect on the statement of cash flows. Cash activities in this step may relate to cash flows from operating activities, investing activities, or financing activities.

- Completing the statement of cash flows.

Defining cash and cash equivalents

Cash includes cash on hand and demand deposits.

Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash and have an insignificant risk of change in value. Therefore, cash equivalents include short-term investments that are acquired with short maturities (generally less than three months from the date of acquisition). Under IFRS, preferred share investments acquired close to their maturity date may be included in cash equivalents. However, under ASPE, all equity investments are excluded from cash equivalents because they are not readily convertible to known amounts of cash, and because the risk of change in their value is significant.

Identifying transactions

Which transactions should be included on the statement of cash flows, and how do we know that all relevant transactions have been included? The work sheet (in the work sheet approach) is a particularly helpful tool in answering these questions.

Theoretically, all transactions ultimately affect the statement of financial position, because all income statement accounts are closed out to retained earnings at the end of each year, and retained earnings is a statement of financial position account. Therefore, analyzing the change in each statement of financial position account (from one period to the next), as suggested in step 3 of the work sheet approach, should ensure that all relevant transactions are identified and included in the statement of cash flows. Note that the net change in an account (for example, Land) usually does not provide enough information about individual transactions that affected the account. (For instance, an increase of $100,000 in the Land account may be due to one transaction, such as a purchase of land costing $100,000, or multiple transactions, including offsetting purchases and disposals of land.) Therefore, full analysis of the change in each statement of financial position account, together with analysis of other information including disclosures and the other financial statements, is required to ensure that all relevant transactions are identified and included on the statement of cash flows.

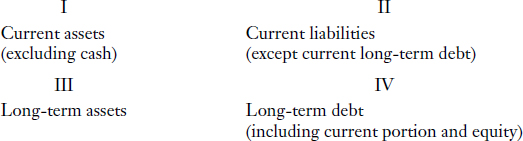

Classifying transactions

The definitions of operating activities, investing activities, and financing activities may be used to classify transactions. Another way to classify transactions is to divide the statement of financial position into quadrants as follows:

In general, transactions that affect quadrant I and quadrant II are classified as operating activities, transactions that affect quadrant III are classified as investing activities, and transactions that affect quadrant IV are classified as financing activities. Purchase of land affects quadrant III; therefore, it is an investing activity. Borrowing of money on a long-term basis affects quadrant IV; therefore, it is a financing activity. Intuitively, the process of earning net income is an operating activity; however, it can also be noted that sales and purchases affect current assets (such as Accounts Receivable and Inventory) and current liabilities (such as Accounts Payable), which affect quadrant I and quadrant II, respectively.

There are some exceptions to the quadrant approach described above, for instance:

- Current portion of long-term debt is included in current liabilities on the statement of financial position; however, current portion of long-term debt is classified as a financing cash flow since it relates to the company's borrowings.

- The effect of interest received may be included in an interest receivable account (typically a current asset). Under IFRS, interest received may be classified as either an operating or investing cash flow; however, under ASPE, interest received is classified as an operating cash flow.

- The effect of interest paid may be included in an interest payable account (typically a current liability). Under IFRS, interest paid may be classified as either an operating or financing cash flow; however, under ASPE, interest paid is classified as an operating cash flow if recognized in net income. (If charged directly to retained earnings, interest paid is classified as a financing cash flow.)

- The effect of dividends received may be included in a dividend receivable account (typically a current asset). Under IFRS, dividends received may be classified as either an operating or investing cash flow; however, under ASPE, dividends received are classified as an operating cash flow.

- The effect of dividends paid may be included in a dividend payable account (typically a current liability). Under IFRS, dividends paid may be classified as either an operating or financing cash flow; however, under ASPE, dividends paid are classified as an operating cash flow if recognized in net income. (If charged directly to retained earnings, dividends paid are classified as a financing cash flow.)

In summary, under IFRS, interest and dividends received may be classified as either operating or investing cash flows, and interest and dividends paid may be classified as either operating or financing cash flows. Note that under IFRS, once the choice of classification is made (for each of interest and dividends received and paid), it is applied consistently from period to period. Under ASPE, interest and dividends received and paid are generally classified as operating cash flows (unless interest and/or dividends paid are charged directly to retained earnings, in which case they are classified as financing cash flows).

A statement of cash flows that balances is not necessarily correct, for example:

- All transactions may not have been identified. (That is, there may be some transactions that offset each other that have not been identified.)

- Transactions may be classified incorrectly. (For example, an operating cash flow may have been classified as an investing cash flow in error.)

- The statement may not include sufficient detail, or may include presentation errors.

Presentation

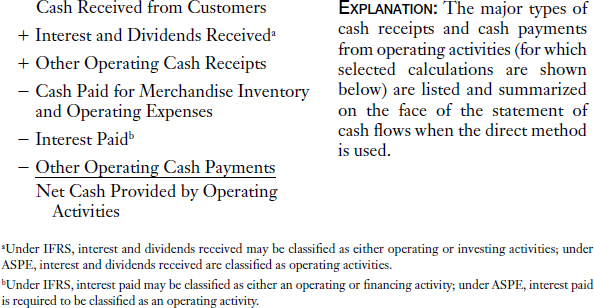

The direct method and the indirect (or reconciliation) method are two different ways of presenting cash flows from operating activities. Given the same information, both methods arrive at the same amount of net cash provided by (used in) operating activities. Both methods are acceptable, although IFRS and ASPE encourage (but do not require) use of the direct method. In practice, many companies use the indirect method.

The direct method The direct method shows the following amounts under “Cash flows from operating activities”:

Cash receipts from customers

Cash receipts from other revenue sources

Cash payments to suppliers for goods and services

Cash payments to and on behalf of employees

Cash interest paid

Cash dividends paid (if classified as operating cash flows under IFRS)

Cash payments of income tax

The indirect method The indirect method (also called the reconciliation method) adjusts for the same items included in cash flows from operating activities under the direct method. However, the indirect method begins with net income (per the income statement) and adds or deducts cash and noncash items and changes in working capital, resulting in reconciliation of net income to net cash provided by (used in) operating activities.

Interpreting the Statement of Cash Flows

The final, and perhaps the most important, study step is learning how to interpret a statement of cash flows. When analyzing a company's financial position, it may be best to start with the statement of cash flows, because its focus is on cash flow from operating activities (or cash from continuing operations). Analysis of cash flow from operating activities often reveals the strength of the company, whether or not the company's operating cash flow is sustainable, and whether or not the company will be able to pay dividends and interest and repay debt from internally generated funds. As previously discussed, the statement of cash flows also provides information regarding the company's sources and uses of cash during the period.

TIPS ON CHAPTER TOPICS

- Homework and examination problems related to the statement of cash flows very often involve comparative statement of financial position data. Although sometimes the earlier year's information is listed first (so that the data are shown in chronological order), it is also common to list the current year's information first. Before beginning work on a problem, carefully note the order of the data so that increases or decreases in accounts are correctly identified.

- Additional information is often provided with comparative statements of financial position. If no additional information is provided for a particular account, but the account balance has changed, assume that (1) only one transaction is responsible for the change in the account balance; (2) the most common transaction for the particular account occurred, which changed the account's balance; and (3) cash was involved in the transaction.

- In studying this chapter and doing homework questions, you will encounter transactions for which you may not recall the proper accounting procedures. This chapter draws on your knowledge of all preceding chapters. Use this opportunity to look up accounting procedures you don't recall, and to refresh your memory. The accounting procedures you review will likely be easier to recall the next time you need to use them.

- Every transaction affecting the Cash account is reflected as either an inflow (receipt) or outflow (payment) on the statement of cash flows. Furthermore, receipts and payments are classified by activity. The three activity classifications are: (1) operating; (2) investing; and (3) financing.

- To determine if a cash transaction is related to an operating activity, investing activity, or financing activity, first determine if the transaction meets the definition of an investing activity. If not, determine if the transaction meets the definition of a financing activity. If not, then the transaction is related to an operating activity. (Refer to Illustration 22-1 for definitions and examples of operating activities, investing activities, and financing activities.)

- For investing activities and financing activities, cash receipts and payments are reported gross (not net). Thus, if issuance of long-term debt results in proceeds of $2 million, and principal repayments of the same long-term debt total $300,000 in the same period, the two amounts cannot be netted to show only a net cash inflow of $1.7 million. Instead, the cash inflow of $2 million and the cash outflow of $300,000 must be shown separately in the financing section of the statement of cash flows. Similarly, if there are acquisitions and disposals of plant assets in the same period, the related cash payments and receipts must be reported gross (not net).

- Cash includes currency on hand and demand deposits with banks or other financial institutions. Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash and have an insignificant risk of change in value. Examples of items that are cash equivalents include treasury bills, commercial paper, and money market funds. Cash equivalents may be included in the cash amount presented on the statement of financial position and on the statement of cash flows.

- Under IFRS, income taxes paid are required to be disclosed. However, under ASPE, income taxes paid are encouraged (but not required) to be disclosed.

- Cash flows related to investments and loans that are acquired specifically for trading purposes are operating cash flows, whereas investments and loans that are acquired for other purposes are investing cash flows.

- If a homework or exam problem requires use of the indirect method but does not give the net income figure, the amount of net income (or net loss) can usually be determined by analyzing the change in retained earnings (which will contain net income or net loss, in addition to other items).

Operating, Investing, and Financing Activities

DEFINITIONS:

Operating activities are the enterprise's principal revenue-producing activities and other activities that are not investing or financing activities. Operating cash flows generally involve the cash effects of transactions that determine net income.

Investing activities involve the acquisition and disposal of long-term assets and other investments that are not included in cash equivalents or acquired for trading purposes. Investing cash flows are generally the result of (a) making and collecting loans and (b) acquiring and disposing of investments and productive long-lived assets.

Financing activities result in changes in the size and composition of the enterprise's equity capital and borrowing. Financing cash flows are generally the result of (a) obtaining capital from owners and providing them with a return on, and a return of, their investment; and (b) obtaining cash from issuing debt and repaying amounts borrowed.

EXAMPLES:

Operating activities

Cash inflows:

From cash sales and collections from customers on account

From returns on loans (interest) and equity securities (dividends)a

From receipts for royalties, rents, and fees

Cash outflows:

To suppliers on account

To, and on behalf of, employees for services

To governments for taxes

To lenders for interestb

To others for expenses

Investing activities

Cash inflows:

From proceeds on sale of property, plant, and equipment

From proceeds on sale of debt or equity securities of other entities

From collection of principal on loans to other entities

Cash outflows:

For purchases of property, plant, and equipmentc

For purchases of debt or equity securities of other entities

For loans to other entities

Financing activities

Cash inflows:

From proceeds on issuance of equity securities (company's own shares)

From proceeds on issuance of debt (bonds and notes)

For payments of dividends to shareholdersd

For repayments of long-term debt or reacquisitions of share capital

For reductions of capital lease obligations

aUnder IFRS, interest and dividends received may be classified as either operating or investing cash inflows. Under ASPE, interest and dividends received are generally classified as operating cash inflows.

bUnder IFRS, interest paid may be classified as either operating or financing cash outflows. Under ASPE, interest paid is generally classified as an operating cash outflow.

cIf as part of a purchase of a plant asset, the company incurs debt owed directly to the seller, the transaction is considered a significant noncash transaction that will not appear on the statement of cash flows, but will be disclosed elsewhere in the financial statements.

dUnder IFRS, dividends paid may be classified as either operating or financing cash outflows. Under ASPE, dividends paid are classified as financing cash outflows.

The statement of cash flows summarizes all transactions that occurred during the period and had an impact on the cash balance.

PURPOSE: This exercise will give you practice in classifying transactions by activity category.

The Wolfson Corporation prepares financial statements in accordance with ASPE, and had the following transactions during 2014:

- Issued common shares for $100,000 in cash.

- Issued $22,000 worth of common shares in exchange for equipment.

- Sold services for $52,000 cash.

- Purchased securities as a long-term investment for $18,000 cash.

- Collected $9,000 of accounts receivable.

- Paid $14,000 of accounts payable.

- Declared and paid a cash dividend of $12,000.

- Sold a long-term investment in securities with a cost of $18,000 for $18,000 cash.

- Purchased a machine for $35,000 in exchange for a long-term note.

- Exchanged land costing $20,000 for equipment costing $20,000.

- Paid salaries and wages of $6,000.

- Paid $1,000 for advertising services.

- Paid $8,000 for insurance coverage for a future period.

- Borrowed $31,000 cash from the bank.

- Paid $11,000 interest.

- Paid $31,000 cash to the bank to repay loan principal.

- Issued $40,000 of common shares upon conversion of bonds payable having a face value of $40,000.

- Paid utilities of $4,000.

- Loaned a vendor $6,000 cash.

- Collected interest of $2,000.

- Collected $6,000 loan principal from a borrower.

- Purchased treasury shares for $4,000.

- Sold treasury shares for $6,000 (cost was $4,000).

- Paid taxes of $20,000.

Instructions

Analyze each transaction above and indicate whether it results in a(n):

(a) inflow of cash from operating activities,

(b) outflow of cash from operating activities,

(c) inflow of cash from investing activities,

(d) outflow of cash from investing activities,

(e) inflow of cash from financing activities,

(f) outflow of cash from financing activities, or

(g) noncash investing and/or financing activity.

Solution to Exercise 22-1

1. (e)

2. (g)

3. (a)

4. (d)

5. (a)

6. (b)

7. (f)

8. (c)

9. (g)

10. (g)

11. (b)

12. (b)

13. (b)

14. (e)

15. (b)

16. (f)

17. (g)

18. (b)

19. (d)

20. (a)

21. (c)

22. (f)

23. (e)

24. (b)

APPROACH: Write down the definitions for operating activities, investing activities, and financing activities. (Refer to Illustration 22-1.) Analyze each transaction to determine its classification. Watch for any transactions that do not result in cash flow; they are noncash items. Most noncash items are disclosed elsewhere in the financial statements.

EXPLANATION:

- Issuance of share capital for cash results in an inflow of cash from financing activities.

- Issuance of share capital in exchange for equipment (a plant asset) does not involve cash; the transaction is a noncash investing and financing activity.

- Sale of services is a revenue transaction. Sale of services for cash results in an inflow of cash from operating activities.

- Cash purchase of a long-term investment results in an outflow of cash from investing activities.

- Collection of accounts receivable is a cash inflow from customers for revenues already recorded. Cash inflow from customers is an inflow of cash from operating activities.

- Payment of accounts payable is a cash outflow to suppliers for inventory or expenses already recorded. Cash outflow to vendors is an outflow of cash from operating activities.

- Under ASPE, cash payment of dividends to shareholders is an outflow of cash from financing activities.

- Sale of a long-term investment results in an inflow of cash from investing activities.

- Acquisition of a machine (a plant asset) is an investing activity. Issuance of debt is a financing activity. Purchase of a machine plant asset by issuance of a note payable does not involve cash. Hence, the transaction is a noncash investing and financing activity.

- Acquisition of land (a plant asset) is an investing activity. Sale (disposal) of equipment (also a plant asset) is also an investing activity. Exchange of one plant asset for another plant asset does not involve cash; the transaction is a noncash investing activity.

- Payment of salaries and wages is payment to employees for services rendered, and results in an outflow of cash from operating activities.

- Payment for advertising services is payment to a supplier for services used in operations, and results in an outflow of cash from operating activities.

- Payment for insurance coverage for a future period is payment to a supplier for services to be used in operations, in a future period. The related expense will be recognized in the future period covered by the insurance; however, the payment (cash flow) occurred during 2014, and results in an outflow of cash from operating activities in 2014.

- Borrowing cash from a bank results in issuance of debt (that is, note payable), which is an inflow of cash from financing activities.

- Under ASPE, payment of interest is an outflow of cash from operating activities.

- Repayment of loan principal (debt) is an outflow of cash from financing activities.

- Issuance of common shares is a financing activity and liquidation (redemption) of bonds payable is a financing activity. Redemption of bonds by issuance of shares is a noncash financing activity because no cash is exchanged.

- Payment of utilities is payment to a supplier for services used in operations, and results in an outflow of cash from operating activities.

- Lending cash to another entity is an outflow of cash from investing activities.

- Under ASPE, cash interest received is an inflow of cash from operating activities.

- Collection of loan principal is an inflow of cash from investing activities.

- Cash payment to reacquire a company's own shares (treasury shares) is an outflow of cash from financing activities.

- Sale of treasury shares for cash results in an inflow of cash from financing activities.

- Payment of taxes is an outflow of cash from operating activities.

- To determine if a cash transaction should be classified as operating, investing, or financing, it is usually helpful to reconstruct the journal entry that recorded the transaction, and apply the following observations:

- The journal entry to record a cash transaction that is an operating activity will generally involve: (1) Cash and (2) a revenue account or an expense account; or, a prepaid expense account or an unearned revenue account; or, an account receivable or an account payable.

- The journal entry to record a cash transaction that is an investing activity will generally involve: (1) Cash and (2) an asset account other than Cash, such as Investments (that are not included in cash equivalents or acquired for trading purposes), Land, Building, Equipment, or Patent.

- The journal entry to record a cash transaction that is a financing activity will generally involve: (1) Cash and (2) a liability account (such as Bonds Payable, Notes Payable, or Dividends Payable), or a shareholders' equity account (such as Common Shares, Contributed Surplus, or Treasury Shares).

- If Wolfson prepares financial statements in accordance with IFRS, answers to items 7, 15, and 20 may differ. Item 7 involves dividends paid, which may be classified as either an operating or financing cash outflow under IFRS. Items 15 and 20 involve interest received and paid. Under IFRS, interest received may be classified as either an operating or investing cash inflow, and interest paid may be classified as either an operating or financing cash outflow.

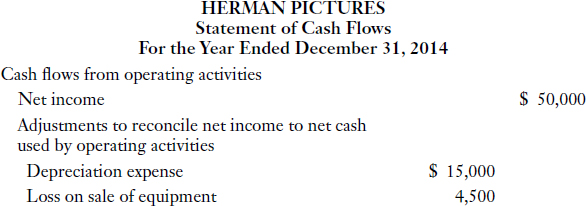

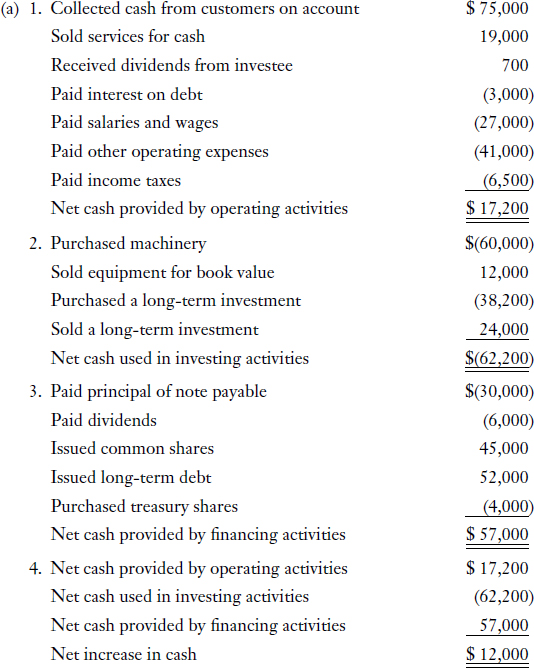

PURPOSE: This exercise will provide an opportunity to prepare a statement of cash flows using the indirect method.

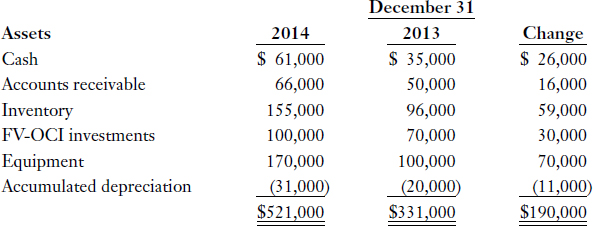

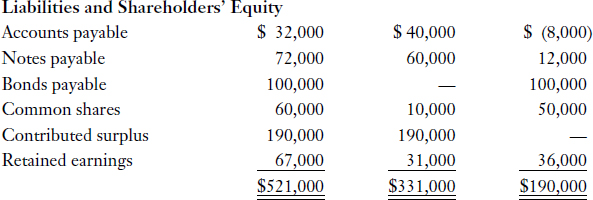

A comparative balance sheet for Herman Pictures appears below:

Additional information:

- New equipment costing $80,000 was purchased for cash.

- Old equipment was sold at a loss of $4,500.

- Bonds were issued for cash.

- An equity investment costing $30,000 was acquired in exchange for a long-term note payable. Herman Pictures intends to hold the equity investment for the long term. As at December 31, 2014, the fair value of the equity investment is $30,000.

- Cash dividends of $14,000 were declared and paid during the year.

- Depreciation expense for 2014 was $15,000.

- Accounts Payable relate to operating expenses.

Instructions

Prepare a statement of cash flows for 2014 using the indirect method, assuming Herman Pictures applies ASPE.

In this exercise, you must analyze the changes in the Retained Earnings account balance to determine the net income figure for 2014.

Solution to Exercise 22-2

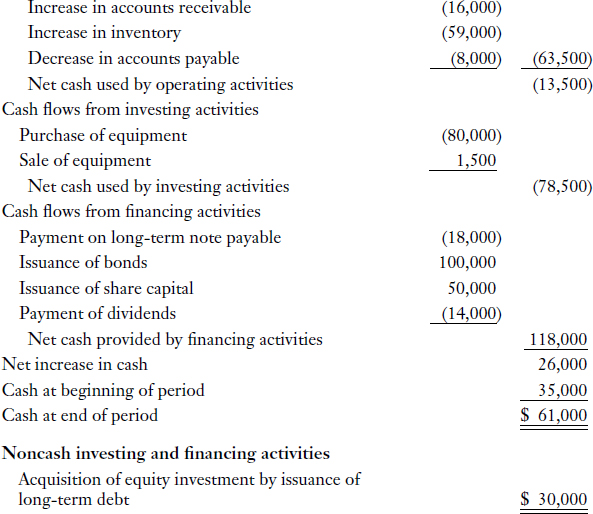

Examine the statement of cash flows and notice the major sources and uses of cash during the period.

APPROACH: Glance through the balance sheet data and additional information to get a sense of the facts given. Set up the format for the statement of cash flows by placing the major classification headings approximately where they should be. Leave space between the headings to fill in details later. (Allow about a one-half page for operating activities, one-quarter page for investing activities, and one-quarter page for financing activities.) Then take each fact in order and process it by placing it where it belongs on the statement of cash flows.

- Find the net change in cash by comparing the balance of Cash at the end of the period with the balance of Cash at the beginning of the period. Net change in cash should equal net increase in cash (or net decrease in cash), which should reconcile beginning and ending cash balances.

- Analyze every change in every balance sheet account other than Cash. Reconstruct the journal entries for the transactions that caused each balance sheet account to change. Examine each journal entry to identify (a) if there is an inflow of cash (debit to Cash) or an outflow of cash (credit to Cash) or no effect on cash; (b) if the transaction involves an operating, investing, or financing activity.

- To help identify the activity classification for each transaction, write down the definitions for operating activities, investing activities, and financing activities. Analyze each transaction to see if it meets one of these definitions. (Refer to Illustration 22-1.)

- To help identify transactions involving operating activities, recall that operating activities typically result in recording of revenues or expenses at some point in time. Thus, if the journal entry to record the transaction involves revenue earned, expense incurred, a receivable, a prepaid expense, a payable, or an unearned revenue, the transaction likely involves an operating activity. When the indirect method is used, the net income figure is used as a starting point for calculation of “net cash flows provided by operating activities.” The net income figure must then be converted from an accrual basis to a cash basis amount. To help identify the transactions requiring an adjustment to net income, find the transactions that affect an income statement account and a balance sheet account other than Cash (such as depreciation), or that affect Cash and result in accruals or deferrals of revenues or expenses (such as payment of expense in advance of consumption of related benefits).

- To help identify investing activities, recall that transactions involving investing activities typically cause changes in non-current asset accounts (or changes in certain current asset accounts such as short-term investments that are not included in cash equivalents and are not acquired specifically for trading purposes, and non-trade receivables).

- To help identify financing activities, recall that transactions involving financing activities typically cause changes in non-current liability accounts or shareholders' equity accounts (or changes in certain current liability accounts such as short-term non-trade notes payable, and current portion of long-term debt).

- If the reason for change in a balance sheet account is not fully explained in the additional information given, assume the most common reason for the change in the particular account. Assume purchases and sales of assets are for cash unless otherwise indicated.

- When more than one transaction is responsible for the net change in an account balance, it may be helpful to draw a T account for the account, and to include all transactions that occurred during the period.

EXPLANATION:

- There was an increase of $26,000 in the Cash account. This net increase in cash goes near the bottom of the statement of cash flows and reconciles the $35,000 beginning cash balance with the $61,000 ending cash balance.

- The journal entry to record the increase in Accounts Receivable is reconstructed as follows:

Net income increases but Cash is not affected; thus, under the indirect method, this increase in accounts receivable is deducted from net income to arrive at net cash provided by operating activities. An increase in accounts receivable indicates that sales revenue for the period exceeded cash collections from customers during the period; therefore, net income is greater than net cash provided by operating activities.

- The journal entry to record the increase in Inventory is reconstructed as follows:

Payments to suppliers are an operating cash outflow. This cash outflow is not reflected in the net income figure; thus, under the indirect method, this increase in inventory is deducted from net income to arrive at net cash provided by operating activities. An increase in inventory indicates that cost of goods sold expense was less than cash payments to suppliers; therefore, net income is greater than net cash provided by operating activities.

- The journal entry to record the increase in FV-OCI Investments is reconstructed as follows:

Acquisition of an equity investment is an investing activity, and issuance of debt is a financing activity; however, in this transaction, there is no effect on cash. This noncash investing and financing transaction is not reported in the body of the statement of cash flows, but must be disclosed elsewhere in the financial statements.

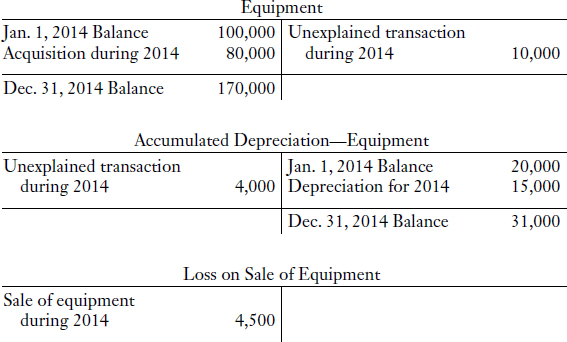

- The T accounts for Equipment, Accumulated Depreciation, and Loss on Sale of Equipment are reconstructed as follows:

The additional information given states that Equipment costing $80,000 was purchased. Depreciation expense amounted to $15,000, and old equipment was sold at a loss of $4,500. We can solve for the missing data (an unexplained credit of $10,000 to Equipment and an unexplained debit of $4,000 to Accumulated Depreciation—Equipment). The most common reason for a credit to the Equipment account is disposal of an asset. That transaction would also explain the $4,000 reduction in Accumulated Depreciation—Equipment and the $4,500 loss on sale of equipment. Thus, it appears that an asset with a cost of $10,000 and book value of $6,000 ($10,000 − $4,000 = $6,000) was sold at a loss of $4,500. This means cash proceeds on the disposal amounted to $1,500 ($6,000 book value − $4,500 loss = $1,500 cash proceeds).

The journal entries to record the transactions discussed above are reconstructed as follows:

Purchase of plant assets is an investing activity. Therefore, this cash outflow is reported as an investing activity.

This journal entry does not affect cash, but does reduce net income. Under the indirect method, depreciation expense is added back to net income to calculate net cash provided by operating activities.

Disposal of plant assets is an investing activity. Therefore, this inflow of cash is reported as an investing activity. Under the indirect method, the loss on sale of equipment must also be added back to net income, as there was no corresponding outflow of cash.

- The journal entry to record the decrease in Accounts Payable is reconstructed as follows:

Payment to suppliers for goods and services consumed in operations is an operating activity. Under the indirect method, this decrease in Accounts Payable must be deducted from net income because a decrease in Accounts Payable indicates that expenses incurred were less than cash payments to suppliers; therefore, net income was greater than the net cash provided by operating activities.

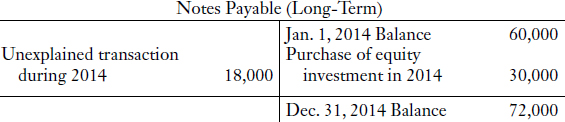

- The T account for Notes Payable (Long-Term) is reconstructed as follows:

The most common reason for a debit to a liability account is a payment. The journal entries to record these transactions are reconstructed as follows:

This transaction was discussed and analyzed in point 4 (above).

This cash outflow of $18,000 was due to payment of a non-trade note payable, which is a financing activity.

- The journal entry to record increase in Bonds Payable is reconstructed as follows:

This cash inflow of $100,000 was due to the issuance of bonds, which is a financing activity.

- The most common reason for an increase in Common Shares is the issuance of shares for cash. The journal entry to record this transaction is reconstructed as follows:

This cash inflow of $50,000 was due to the issuance of common shares, which is a financing activity.

- The Retained Earnings T account is reconstructed as follows:

The most common reason for a credit to Retained Earnings is net income. Since the indirect method is being applied in this exercise, the net income figure is needed as the starting point for calculation of net cash provided by operating activities.

The journal entries to record the declaration and payment of cash dividends are reconstructed as follows:

Providing owners with a return on their investment is classified as a financing activity (under ASPE, or as an operating or financing activity under IFRS). Declaration of dividends has no effect on cash; however, payment of a previously declared dividend reduces cash. Thus, payment of cash dividends is reported as a financing activity under ASPE, or as an operating or financing activity under IFRS.

The last step in the preparation of the statement of cash flows is to subtotal each of the three activity classifications. Inflows are shown as positive amounts; outflows are shown as negative amounts. An excess of inflows over outflows within a classification results in a net inflow; an excess of outflows over inflows within a classification results in a net outflow. Subtotals of the three activities are then totalled to determine net change in cash during the year. This net change must agree with your calculation of the change in the Cash account balance (Step 1); otherwise, one or more errors exist and must be corrected in order to balance the statement of cash flows.

CASE 22-1

PURPOSE: This case will help you practise classifying transactions as operating, investing, or financing.

Four different situations are described below:

- A company purchased a machine priced at $100,000 by issuing a cheque for $100,000.

- A company purchased a machine priced at $100,000 by giving a down payment of $20,000 and by issuing a note payable to the seller for $80,000. During the same year, the company made principal payments of $12,000 on the note and interest payments of $7,000.

- A company purchased a machine for $100,000. Of that amount, $80,000 was borrowed from a local bank. During the same year, principal payments of $12,000 and interest payments of $7,000 were paid to the bank for this loan.

- A company acquired a machine under a capital lease agreement. The present value of minimum lease payments at inception was $100,000. The first lease payment of $2,000 was paid on the date of lease inception. During the year, additional lease payments of $24,000 were made, which included interest of $15,000.

Instructions

Explain how each situation would be reflected in a statement of cash flows. For each situation, indicate the amount that would be included in the operating, investing, and/or financing section of the statement of cash flows, or indicate the amount that would be separately disclosed as a noncash investing and/or financing transaction.

Solution to Case 22-1

- Investing outflow of $100,000

- Investing outflow of $20,000

Financing outflow of $12,000

Operating outflow of $7,000. (Under IFRS, interest paid may be classified as either an operating or financing activity; under ASPE, interest paid is required to be classified as an operating activity.)

Disclosure of issuance of a note payable for $80,000 as part of this transaction to acquire machinery would be included elsewhere in the financial statements as a noncash investing and financing activity.

- Financing inflow of $80,000

Investing outflow of $100,000

Financing outflow of $12,000

Operating outflow of $7,000. (Under IFRS, interest paid may be classified as either an operating or financing activity; under ASPE, interest paid is required to be classified as an operating activity.)

- Financing outflow of $11,000 ($2,000 + $24,000 − $15,000)

Operating outflow of $15,000. (Under IFRS, interest paid may be classified as either an operating or financing activity; under ASPE, interest paid is required to be classified as an operating activity.)

Disclosure of the capital lease obligation related to this acquisition of machinery for $100,000 would be included elsewhere in the financial statements as a noncash investing and financing activity.

APPROACH: Refer to Illustration 22-1 for a description of the three classifications of activities.

Note that repayments of principal on seller-financed debt are classified as financing cash outflows.

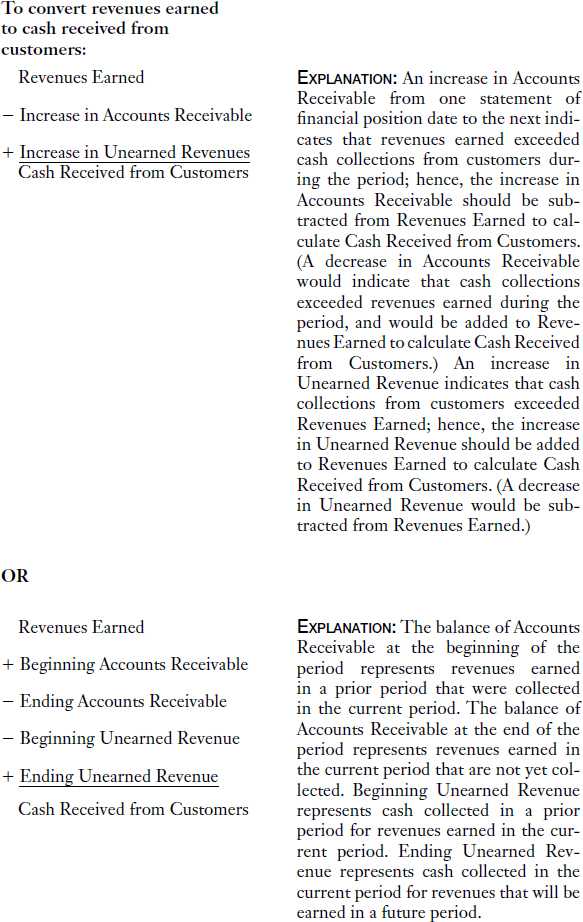

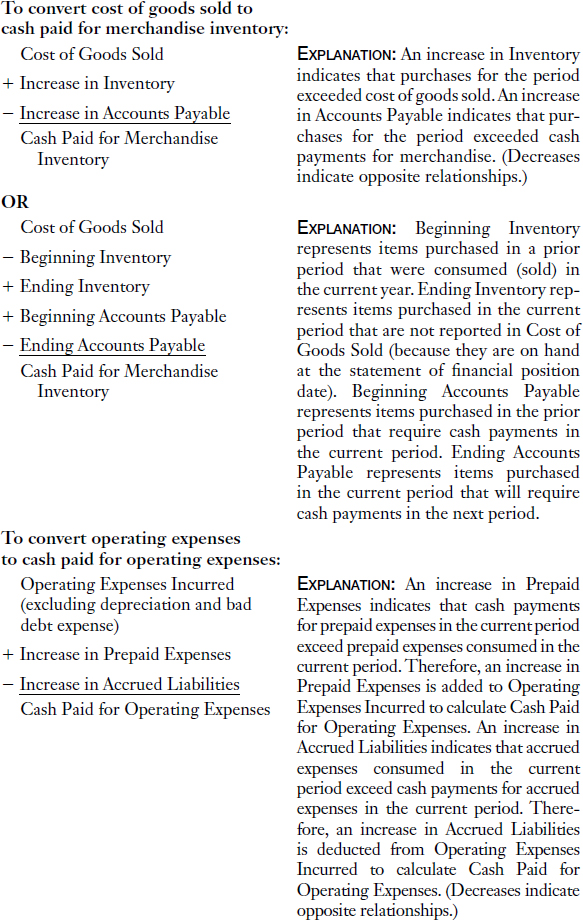

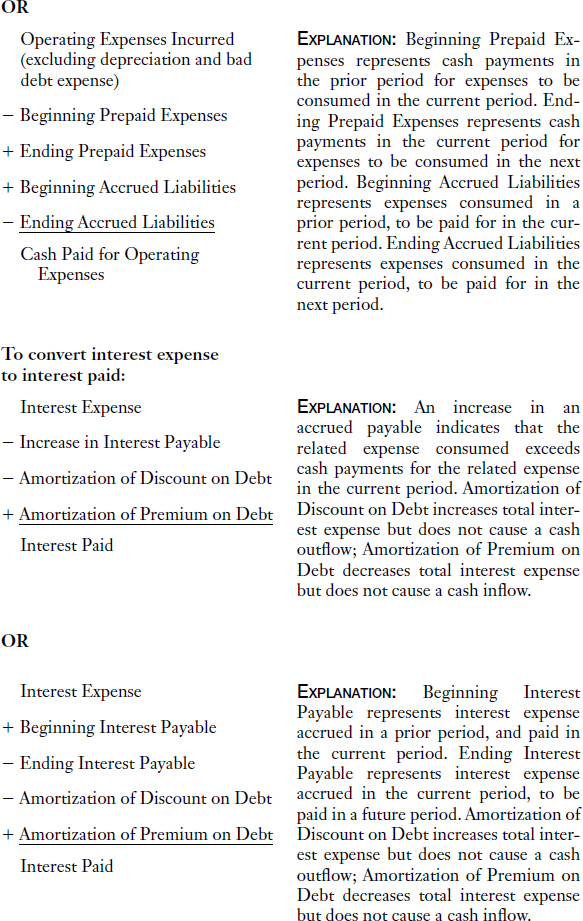

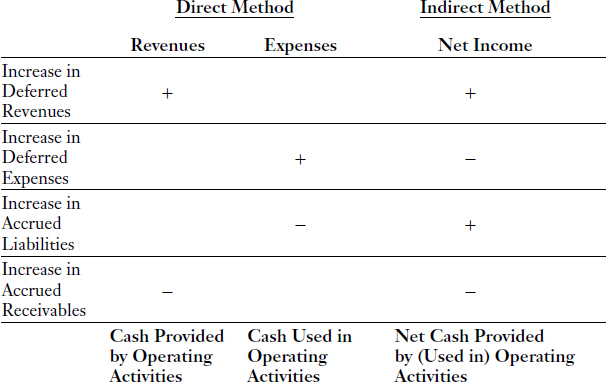

Conversion from Accrual Basis to Cash Basis

DIRECT METHOD

To calculate net cash provided by operating activities:

For all of the calculations above, a decrease in an account balance is treated in a manner opposite to the way an increase in an account balance is treated.

To calculate net cash provided by operating activities:

Treatment of Accruals and Deferrals

Treatment of increases in deferred (unearned) revenues, deferred (prepaid) expenses, accrued liabilities, and accrued receivables can be summarized as follows:

- In examining the summary above, notice the mathematical signs are the same for both the direct method and indirect method for changes in deferred revenues and changes in accrued receivables. This is because (1) changes in deferred revenues and accrued receivables explain the difference between revenues earned during the period and cash received from operating activities during the period; and (2) revenues earned are a positive component of net income, and cash received from operating activities is a positive component of net cash provided by operating activities.

- Also notice that the mathematical signs are different for the direct method and the indirect method for changes in deferred expenses and changes in accrued liabilities. This is because (1) changes in deferred (prepaid) expenses and accrued liabilities explain the difference between expenses incurred during the period and cash paid for operating activities during the period; and (2) expenses incurred are a negative component of net income, and cash paid for operating activities is a negative component of net cash provided by operating activities.

- “(Net) cash provided by operating activities” (or “cash provided by operations”) is another name for “net income on a cash basis.”

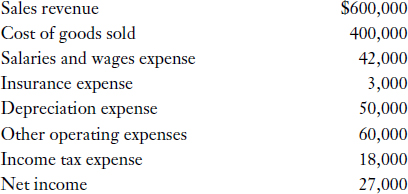

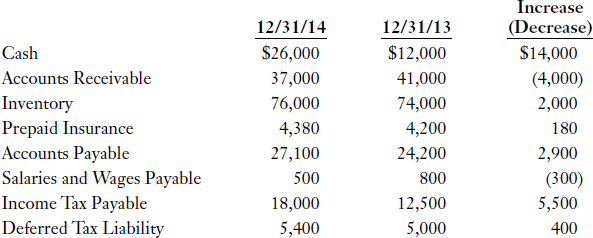

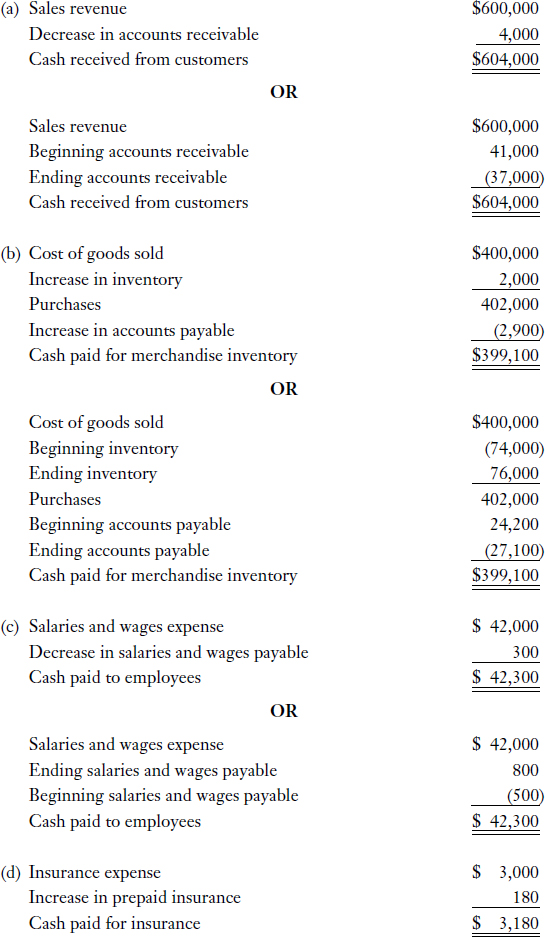

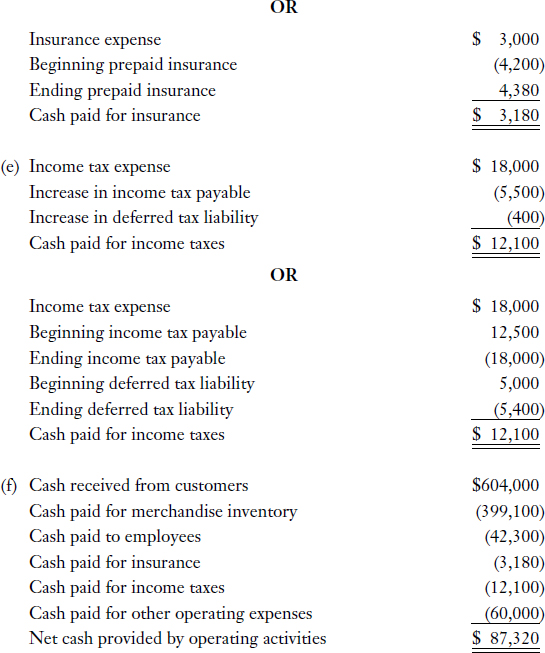

PURPOSE: This exercise will test your ability to convert accrual basis information to cash basis information.

The Fuller Corporation reported the following on its income statement for 2014:

The comparative statements of financial position reported the following selected information:

All of the operating expenses included in “other operating expenses” were paid in cash during 2014. Accounts payable relate to purchases of merchandise inventory.

Instructions

Calculate the following amounts for 2014:

(a) cash received from customers

(b) cash paid for merchandise inventory

(c) cash paid to employees

(d) cash paid for insurance

(e) cash paid for income taxes

(f) net cash provided by operating activities

Solution to Exercise 22-3

The change in the cash balance ($14,000 increase) had no effect on the calculations. Net cash provided by (used in) operating activities, plus net cash provided by (used in) investing activities, plus net cash provided by (used in) financing activities should net to the $14,000 increase in the cash balance.

Refer to Illustration 22-2 for explanations for the above calculations.

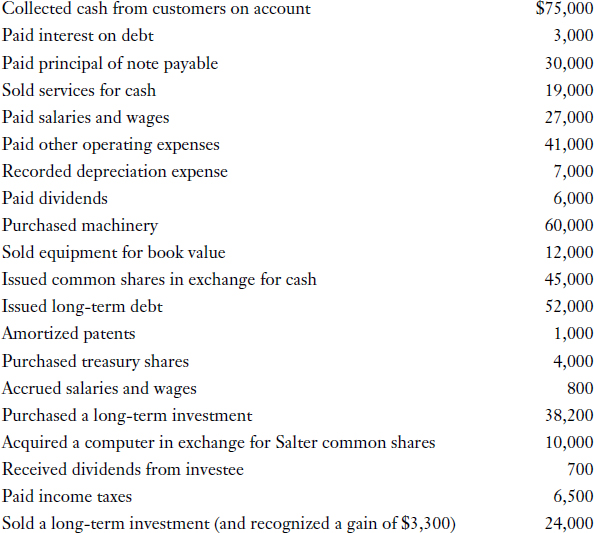

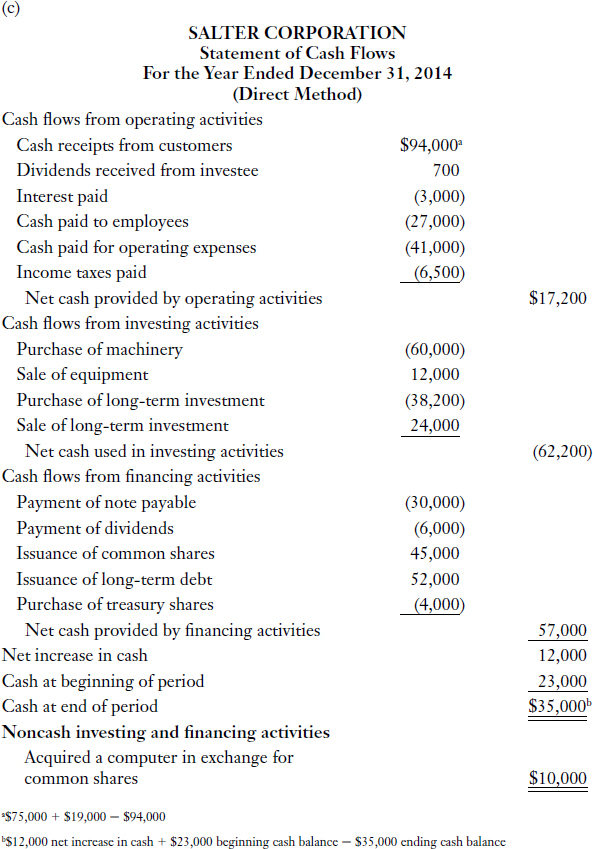

PURPOSE: This exercise will help you practise classifying transactions on a statement of cash flows using the direct method.

The Salter Corporation uses the direct method for preparation of the statement of cash flows. Salter prepares financial statements in accordance with IFRS, and classifies dividends paid as a financing activity, and interest paid and received and dividends received as operating activities. The following summarized transactions took place in 2014:

Instructions

(a) Calculate the following:

- net cash provided by (used in) operating activities

- net cash provided by (used in) investing activities

- net cash provided by (used in) financing activities

- net increase (decrease) in cash for the period

(b) If any transactions are not used in the required calculations in part (a), explain why.

(c) Based on the information given, prepare a statement of cash flows using the direct method. Assume the cash balance at the beginning of the year was $23,000.

Solution to Exercise 22-4

(b) 1. Recorded depreciation expense, $7,000, was not used because it is a noncash charge to income. It is an expense that did not require a cash payment this period. (The cash outlay occurred at time of payment for acquisition of the related depreciable assets.)

2. Amortized patents, $1,000, was not used because it is a noncash charge against income. It is an expense that did not require a cash payment in this period. (The cash outlay occurred at time of payment for acquisition of the related intangible assets.)

3. Accrued salaries and wages, $800, was not used because it relates to an expense recognized in this period, to be paid in the next period.

4. Acquired a computer in exchange for shares, $10,000, was not used because this is a noncash investing and financing activity.

If the indirect method were used: (1) the depreciation of $7,000 and the amortization of $1,000 would be added back to net income, (2) the increase of $800 in accrued salaries and wages would also be added to net income, and (3) the $3,300 gain on sale of long-term investment would be deducted from net income, in the process of reconciling net income to net cash provided by operating activities.

When using the direct method, an additional schedule reconciling net income to net cash provided by operating activities should be provided as a supplementary disclosure. The information given in this exercise is insufficient to prepare a similar reconciliation (for Salter Corporation).

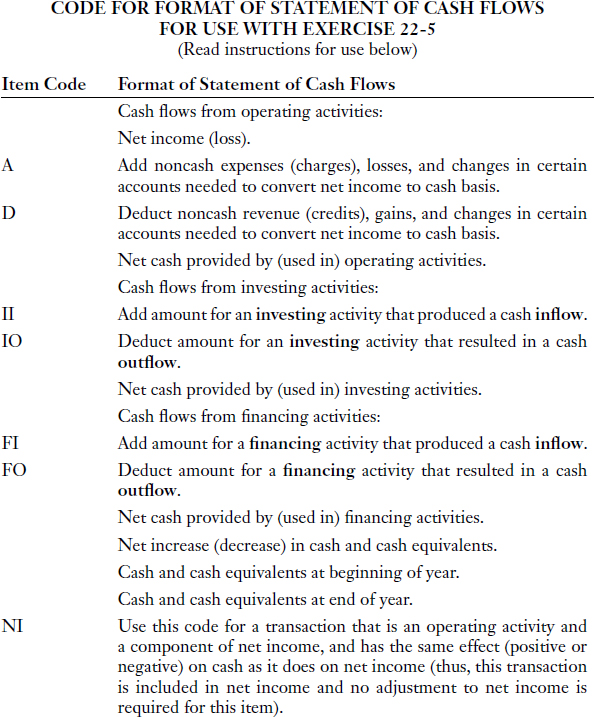

PURPOSE: This exercise will provide examples of transactions on a statement of cash flows using the indirect method.

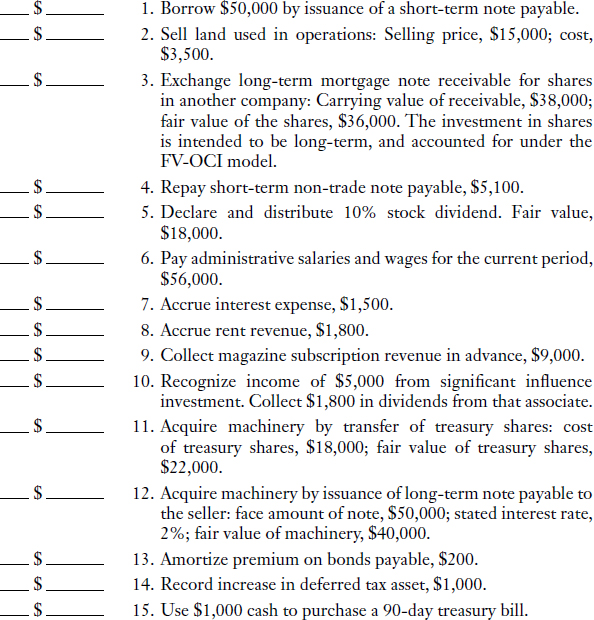

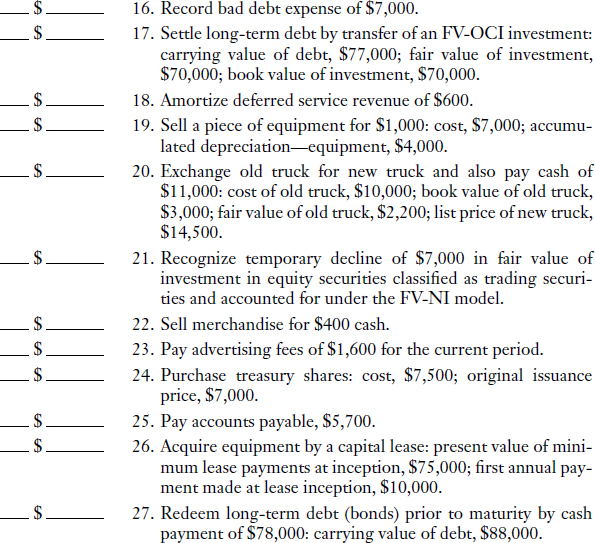

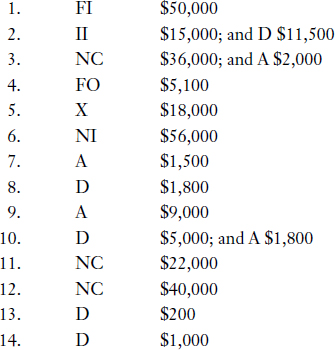

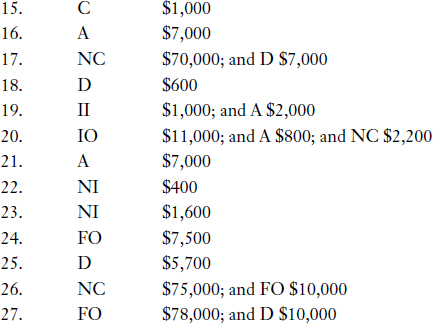

Instructions

For each of the following transactions and events, indicate how it should be reported in a statement of cash flows using the indirect approach. Use the code from the table above for shorthand notations for your responses. Include the appropriate dollar amount with each code. A transaction or event may require more than one code for a complete answer.

Solution to Exercise 22-5

APPROACH:

- Reconstruct the journal entry for each transaction. Examine each journal entry to determine if there is an inflow of cash, an outflow of cash, or no effect on cash.

- The journal entry to record a cash transaction that is an investing activity will generally involve: (1) Cash and (2) an asset account other than Cash, such as Investments, Land, Building, Equipment, or Patent.

- The journal entry to record a cash transaction that is a financing activity will generally involve: (1) Cash and (2) a liability account (such as Bonds Payable, Notes Payable, or Dividends Payable), or a shareholders' equity account (such as Common Shares, Contributed Surplus, or Treasury Shares).

- Write down the definitions for investing activities and financing activities (see below). Analyze each transaction to see if it fits one of these definitions:

Investing activities involve the acquisition and disposal of long-term assets and other investments that are not included in cash equivalents or acquired for trading purposes. Investing cash flows are generally the result of (a) making and collecting loans and (b) acquiring and disposing of investments and productive long-lived assets.

Financing activities result in changes in the size and composition of the enterprise's equity capital and borrowings. Financing cash flows are generally the result of (a) obtaining capital from owners and providing them with a return on, and a return of, their investment; and (b) obtaining cash from issuing debt and repaying amounts borrowed.

- Identify the items requiring adjustments to net income in order to convert net income to net cash provided by operating activities, by identifying the reconstructed journal entries that involve: (a) an income statement account and a statement of financial position account other than Cash (for example, the journal entry to record depreciation); or (b) the Cash account and a noncash asset or liability account that relates to operating activities (accounts receivable, inventory, accounts payable, etc.); or (c) a gain or loss that has no cash effect or a gain or loss from a transaction that is classified as an investing or financing activity.

- Identify the items that are noncash financing and investing activities by identifying transactions that fit the definitions of investing activities and/or financing activities, but do not affect Cash.

EXPLANATION: The journal entries for each transaction are reconstructed and analyzed below:

![]()

This is a cash inflow due to a financing activity.

Cash proceeds of $15,000 from sale of a plant asset should be reported as an investing cash inflow. The $15,000 represents recovery of the asset's book value of $3,500 and a gain of $11,500. The gain of $11,500 was included in net income. Using the indirect method, the gain must be deducted from net income in reconciling net income with net cash provided by operating activities, so that the $11,500 gain is not included in the statement of cash flows twice. (The entire $15,000 cash proceeds will be reported as an investing cash inflow.)

Cash is not affected. This exchange of one noncash asset for another noncash asset is a noncash investing activity that must be disclosed elsewhere in the financial statements. The loss on investment in mortgage note receivable was deducted from net income. Therefore, using the indirect method, the loss is added back to net income in reconciling net income with net cash provided by operating activities.

![]()

This is a cash outflow due to a financing activity.

Cash is not affected. A stock dividend is not a financing and/or investing activity, and therefore, is not required to be reported on the statement of cash flows. A stock dividend would be reflected on other financial statements or in notes to the financial statements, because it changes shareholders' equity.

![]()

This is a cash outflow due to an operating activity. This $56,000 salaries and wages expense amount was deducted from net income at the time of expense recognition. Therefore, using the indirect method, no adjustment is needed for this amount because it reduces both net income and cash.

![]()

Cash is not affected. Accrued interest expense was deducted from net income at the time of expense recognition. Therefore, using the indirect method, accrued interest expense is added back to net income in reconciling net income with net cash provided by operating activities.

![]()

Cash is not affected. Accrued rent revenue was added to net income at the time of revenue recognition. Therefore, using the indirect method, accrued rent revenue is deducted from net income in reconciling net income with net cash provided by operating activities.

![]()

This is a cash inflow due to an operating activity. This $9,000 unearned subscription revenue amount was not included in net income. Therefore, using the indirect method, unearned subscription revenue is added back to net income in reconciling net income with net cash provided by operating activities.

This transaction includes a noncash journal entry to record income from an investment in associate accounted for using the equity method, and an operating cash inflow of $1,800. (Under IFRS, dividends received are permitted to be classified as operating cash inflows; under ASPE, dividends received are classified as operating cash inflows.) The noncash journal entry increases net income, but not cash. The journal entry to record dividends received increases cash but does not affect net income. Therefore, using the indirect method, the $5,000 investment income amount is deducted from net income, and the $1,800 dividends received amount is added to net income, in reconciling net income with net cash provided by operating activities. On a net basis, $3,200 in undistributed earnings of the associate is deducted from net income.

Cash is not affected. This is a significant investing activity (acquisition of equipment) and financing activity (disposal of treasury shares) that must be disclosed elsewhere in the financial statements or in a schedule of noncash investing and financing activities.

![]()

A note payable is issued at an unreasonably low interest rate in exchange for a noncash asset; this transaction should be recorded at the fair value of the asset received. Cash is not affected. This is a significant investing and financing activity that must be disclosed elsewhere in the financial statements or in a schedule of noncash investing and financing activities.

![]()

Cash is not affected. A credit to interest expense was added to net income. Therefore, using the indirect method, the credit to interest expense is deducted from net income in reconciling net income with net cash provided by operating activities.

![]()

Cash is not affected. A credit to deferred tax benefit was deducted from net income. Therefore, using the indirect method, the credit to deferred tax expense is deducted from net income in reconciling net income with net cash provided by operating activities.

![]()

This is a decrease in cash and an increase in cash equivalents. Therefore, there is no change in total cash and cash equivalents.

![]()

Cash is not affected. Bad debt expense was deducted from net income at the time of expense recognition. Therefore, using the indirect method, bad debt expense is added back to net income in reconciling net income with net cash provided by operating activities.

Cash is not affected. This is a noncash investing and financing activity that must be disclosed elsewhere in the financial statements or in a schedule of noncash investing and financing activities. Using the indirect method, the gain on extinguishment of debt must be deducted from net income because it relates to a (noncash) financing activity.

![]()

Cash is not affected. Cash related to unearned revenue was collected in a previous period. Therefore, using the indirect method, a decrease in unearned revenue is deducted from net income in reconciling net income with net cash provided by operating activities.

This transaction includes a cash inflow of $1,000 related to an investing activity. Using the indirect method, the loss must be added back to net income in reconciling net income with net cash provided by operating activities. (The $1,000 cash proceeds will be reported as an investing cash inflow.)

This transaction includes a cash outflow of $11,000 related to an investing activity. Using the indirect method, the loss must be added back to net income in reconciling net income with net cash provided by operating activities. The exchange of one noncash asset (book value of $2,200 after the writedown for impairment) for another must be disclosed as a noncash investing activity.

![]()

Cash is not affected. The unrealized holding loss was deducted from net income at the time of recognition of the temporary decline in fair value of investment. Therefore, using the indirect method, the unrealized holding loss is added back to net income in reconciling net income with net cash provided by operating activities.

![]()

This is a cash inflow due to an operating activity. This $400 sales revenue amount was added to net income at the time of revenue recognition. Therefore, using the indirect method, no adjustment is needed for this amount because it increased both net income and cash.

![]()

This is a cash outflow due to an operating activity. This $1,600 advertising expense amount was deducted from net income at the time of expense recognition. Therefore, using the indirect method, no adjustment is needed for this amount because it reduced both net income and cash.

![]()

This is a cash outflow due to a financing activity (return of investment to owner).

![]()

This is a cash outflow due to an operating activity. This $5,700 decrease in accounts payable was not included in net income. Therefore, using the indirect method, the decrease in accounts payable paid is deducted from net income in reconciling net income with net cash provided by operating activities.

A capital lease is a transaction that qualifies as a noncash investing and financing activity that must be disclosed elsewhere in the financial statements or in a schedule of noncash investing and financing activities. The first lease payment results in a cash outflow due to a financing activity.

Payment of $78,000 to the creditor is a cash outflow due to a financing activity. Using the indirect method, the gain of $10,000 must be deducted from net income because it relates to a noncash financing activity.

ANALYSIS OF MULTIPLE-CHOICE QUESTIONS

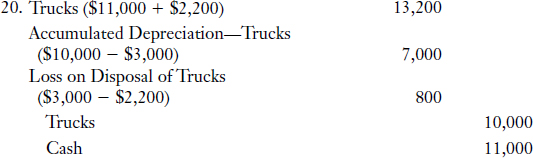

Question

1. At the end of 2014, a company acquired a hotel by paying a portion of the purchase price in cash and issuing a mortgage note payable to the seller for the balance. On the statement of cash flows for 2014, what amount is included in financing activities for this transaction?

- zero

- cash payment

- mortgage amount

- acquisition price

EXPLANATION: The cash down payment should be reported as a cash outflow due to an investing activity. Issuance of the mortgage note payable to the seller (that is, seller-financed debt) is a noncash investing and financing activity, which should be disclosed elsewhere in the financial statements. Payments of principal on the debt are financing cash outflows, although none have occurred yet because the purchase happened at the end of the period. (Solution = a.)

Question

2. Smith Corporation had the following transactions occur in the current year:

(1) Cash sale of merchandise inventory

(2) Sale of delivery truck at book value

(3) Sale of Smith Corporation common shares for cash

(4) Issuance of a note payable to a bank for cash

(5) Sale of a security held as a long-term investment

(6) Collection of a note receivable

In a statement of cash flows, how many of the above items are reported as a cash inflow from investing activities?

- all six items

- five items

- four items

- three items

EXPLANATION: Define “investing activities.” Compare each transaction above with the definition. Investing activities involve the acquisition and disposal of long-term assets and other investments that are not included in cash equivalents or those acquired for trading purposes. Investing cash flows are generally the result of (a) making and collecting loans and (b) acquiring and disposing of investments and productive long-lived assets. The sale of a delivery truck (regardless of the difference between selling price and carrying value), the sale of a long-term investment, and the collection of a note receivable are three items that produce cash inflows from investing activities. The cash sale of merchandise inventory results in a cash inflow from operating activities. The sale of the corporation's own common shares and the issuance of the note payable both produce cash inflows from financing activities. (Solution = d.)

Recall that transactions classified as investing activities involve assets (delivery truck, equity investments, and note receivable in this example), whereas transactions classified as financing activities involve liabilities (note payable in this example) or shareholders’ equity (common shares in this example).

Question

3. A corporation had the following transactions occur during the current year:

(1) Reclassification of debt from long-term liabilities to current liabilities

(2) Payment of principal on mortgage note payable

(3) Payment of interest on mortgage note payable

(4) Purchase of treasury shares

(5) Payment of cash dividend

(6) Payment of property dividend

(7) Distribution of stock dividend

Under ASPE, on a statement of cash flows, how many of the above items are reported as a cash outflow from financing activities?

- six items

- five items

- four items

- three items

EXPLANATION: The payment of principal on a note payable, the purchase of treasury shares, and the payment of a cash dividend are the three items that result in cash outflows from financing activities. Reclassification of debt does not affect cash. (It may be included in a schedule of noncash investing and financing activities.) Under ASPE, the payment of interest is reported as a cash outflow from operating activities. (Under IFRS, the payment of interest may be classified as either operating or financing activities.) Payment of a property dividend is a noncash activity to be disclosed elsewhere in the financial statements. Neither declaration nor distribution of a stock dividend affects cash. (Solution = d.)

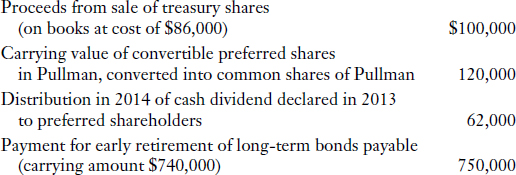

Question

Pullman prepares financial statements in accordance with ASPE. The amount of net cash provided by (used in) financing activities to appear in Pullman's statement of cash flows for 2014 should be:

- $716,000.

- $712,000.

- $592,000.

- $530,000.

EXPLANATION: Net cash used in financing activities is calculated as follows:

The conversion of preferred shares to common shares is a noncash transaction and would be disclosed elsewhere in the financial statements. (Solution = b.)

The $10,000 loss on retirement of bonds payable ($750,000 retirement price exceeds carrying value of $740,000 by $10,000) would be a component of net income. If the indirect method is used to present the net cash provided (used) by operations, the $10,000 loss would be added to net income in this calculation.

Question

5. During 2014, Vaudry Corporation had the following activities related to its financial operations:

(1) Purchased equipment for cash, which was borrowed from a bank.

(2) Acquired treasury shares for cash.

(3) Declared a cash dividend payable in 2015.

(4) Appropriated retained earnings for possible loss from a lawsuit.

(5) Purchased a two-month guaranteed investment certificate.

(6) Acquired a five-year guaranteed investment certificate from a bank.

(7) Made interest payments on bonds payable.

(8) Converted preferred shares to common shares.

(9) Received dividends from an investment in equity of another corporation.

In a statement of cash flows prepared under ASPE, how many of the above transactions would be reported as a cash outflow from investing activities?

- two

- three

- four

- five

EXPLANATION: Identify each transaction as one of the following:

- a cash inflow from operating activities

- a cash outflow from operating activities

- a cash inflow from investing activities

- a cash outflow from investing activities

- a cash inflow from financing activities

- a cash outflow from financing activities

- an investing and/or financing activity not affecting cash

Refer to the definitions in Illustration 22-1 if necessary.

Transactions 1 and 6 are reported as cash outflows from investing activities. (Solution = a.)

Question

6. Refer to the facts of Question 5 above. In a statement of cash flows prepared under ASPE, how many of the transactions would be reported as a cash outflow from financing activities?

- one

- two

- three

- four

EXPLANATION: Refer to the explanation for Question 5 above. Only Item 2 is reported as a cash outflow from financing activities. (Solution = a.)

Question

7. Which of the following may be classified as a financing activity on a statement of cash flows?

- Declaration and distribution of a stock dividend

- Deposit to a bond sinking fund

- Sale of a note receivable

- Payment of income taxes

EXPLANATION: Write down the definitions for operating, investing, and financing activities. Analyze each transaction and determine if it meets the definition of an operating, investing, or financing activity. Declaration and distribution of a stock dividend does not meet any of the definitions; it is not reported on a statement of cash flows. Although a journal entry to record a deposit to a bond sinking fund results in an increase in the fund, which is often classified as a long-term investment, a deposit to a sinking bond fund is usually classified as a financing activity because its purpose is to pay for amounts borrowed. Sale of a note receivable is an investing activity, and payment of income taxes is an operating activity. (Solution = b.)

Question

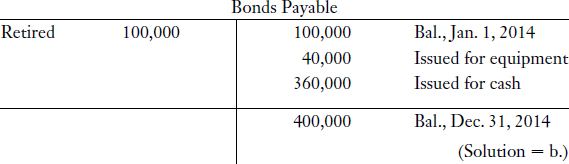

8. The following information was taken from the 2014 financial statements of the Laurel Corporation:

![]()

During 2014

- Bonds payable with a face amount of $40,000 were issued in exchange for equipment.

- A $90,000 payment was made to retire bonds payable with a carrying amount of $100,000.

In its statement of cash flows for the year ended December 31, 2014, what amount should Laurel report as proceeds from the issuance of bonds payable?

- $300,000

- $360,000

- $160,000

- $340,000

EXPLANATION: Draw a T account for Bonds Payable. Enter the data given and solve for the unknown.

Question

9. In a statement of cash flows, using the indirect method, which of the following are subtracted from net income to determine net cash provided by operating activities?

- Amortization of premium on bonds payable

- Loss on sale of equipment

- Depreciation expense

- I only

- II only

- I and II

- I and III

EXPLANATION: Think about how each item (1) affects net income and (2) affects cash. Determine the adjustment needed (if any) to reconcile net income to net cash provided by operating activities. Amortization of premium on bonds payable increases net income (because it reduces interest expense), but does not affect cash; thus it is deducted from net income in reconciling net income to net cash provided by operating activities. Loss on sale of equipment reduces net income but does not affect cash and is not an operating activity, and is therefore added to net income in reconciling net income to net cash provided by operating activities. Depreciation expense reduces net income but does not affect cash and is therefore added to net income in reconciling net income to net cash provided by operating activities. (Solution = a.)

Question

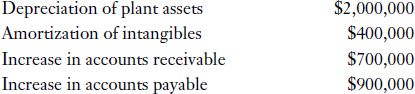

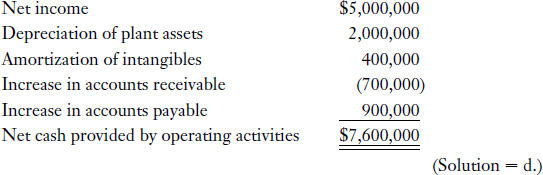

10. Alley Corporation had net income for 2014 of $5 million. Additional information is as follows:

Alley's net cash provided by operating activities for 2014 was:

- $2,800,000.

- $7,200,000.

- $7,400,000.

- $7,600,000.

EXPLANATION: The depreciation and amortization amounts are items that reduce net income but do not cause a decrease in cash. The increase in accounts receivable indicates that sales revenue earned for the period exceeded cash collected from customers, and therefore net income exceeded net cash provided by operating activities. The increase in accounts payable indicates that expenses incurred exceeded cash payments for expense-type items, which caused net income to be less than net cash provided by operating activities. The solution is as follows:

Question

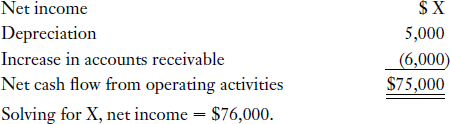

11. Net cash flow from operating activities for 2014 for Graham Corporation was $75,000. The following items are reported on the financial statements for 2014:

Graham prepares financial statements in accordance with ASPE. Based only on the information above, Graham's net income for 2014 was:

- $64,000.

- $66,000.

- $74,000.

- $76,000.

EXPLANATION: Write down the format for reconciliation of net income to net cash flow from operating activities. Fill in the information given. Solve for the unknown.

Cash dividends paid on common shares have no effect on this calculation because cash dividends paid are not a component of net income and they are classified as financing cash outflows under ASPE. (Solution = d.)

Question

12. Change in accounts receivable is used to convert sales revenue to cash receipts from customers when the direct method is used. Change in accounts receivable is also used to convert net income to net cash from operating activities when the indirect method is used. Under each method, is change in gross accounts receivable or net accounts receivable used?

EXPLANATION: Change in net accounts receivable includes the change in the Accounts Receivable account and the change in the Allowance for Doubtful Accounts account. The Accounts Receivable account changes as a result of credit sales, writeoffs of individual accounts, cash collections, and reinstatement of accounts previously written off. The allowance account changes as a result of recognition of bad debt expense, writeoffs of individual accounts, and reinstatement of accounts previously written off.

When the direct method is used, only the change in gross receivables is used to convert sales revenue to cash receipts from customers. The change in the allowance account is not a factor because the related bad debt expense was not included in sales revenue. When the indirect method is used, the change in net receivables is used to convert net income to net cash provided by operating activities because it includes the effect of the bad debt expense that was recorded as well as the difference between the accrual basis revenue amount and cash collections from customers. (Solution = d.)

Question

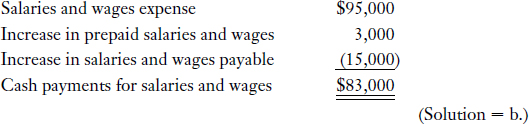

13. Ventresca Company reported salaries and wages expense of $95,000 for 2014. The following data were extracted from the company's financial records:

On a statement of cash flows for 2014, using the direct method, cash payments for salaries and wages should be:

- $77,000.

- $83,000.

- $107,000.

- $113,000.

EXPLANATION: Think of the relationship between salaries and wages expense and cash payments for salaries and wages when there is (1) an increase in prepaid salaries and wages, and (2) an increase in salaries and wages payable. Convert the expense amount to a cash-paid figure.

Question

14. The following information was taken from the 2014 financial statements of Gardner Corporation:

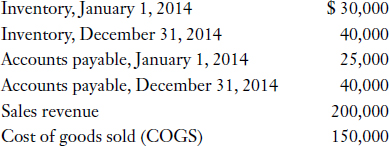

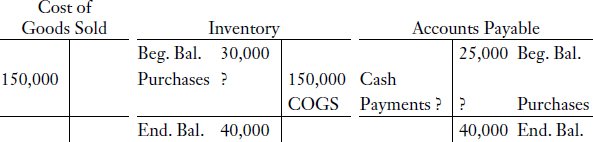

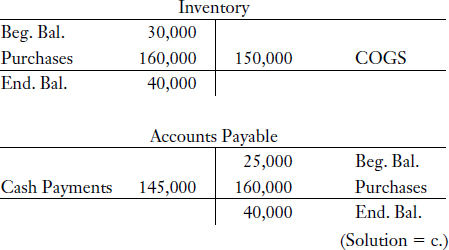

If the direct method is used in the 2014 statement of cash flows, what amount should Gardner report as cash payments for goods to be sold?

- $165,000

- $155,000

- $145,000

- $125,000

EXPLANATION:

Solve for the amount of purchases. Assume all purchases of inventory are on account and solve for the amount of cash payments for goods to be sold (assuming all accounts payable arise from purchases of inventory).

Question

15. Selected information for 2014 for Bharat Company follows:

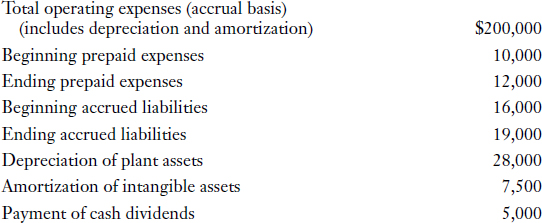

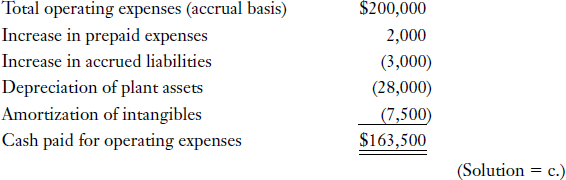

Bharat Company prepares financial statements in accordance with IFRS and classifies interest and dividends received as operating cash inflows, interest paid as operating cash outflows, and dividends paid as financing cash outflows. The amount of cash payments made during 2014 for operating expenses is:

- $234,500.

- $165,500.

- $163,500.

- $160,500.

EXPLANATION: Use one of the relevant formats in Illustration 22-2 to convert operating expenses to cash paid.

Notice that the amount given in the question for “total operating expenses” includes depreciation and amortization, whereas the format requires exclusion of these items. Depreciation expense and amortization expense are both expense items that do not require a cash outlay at the time the expense is recorded. Thus, they are deducted from total operating expenses to arrive at cash paid for operating expenses.

Question

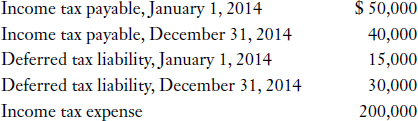

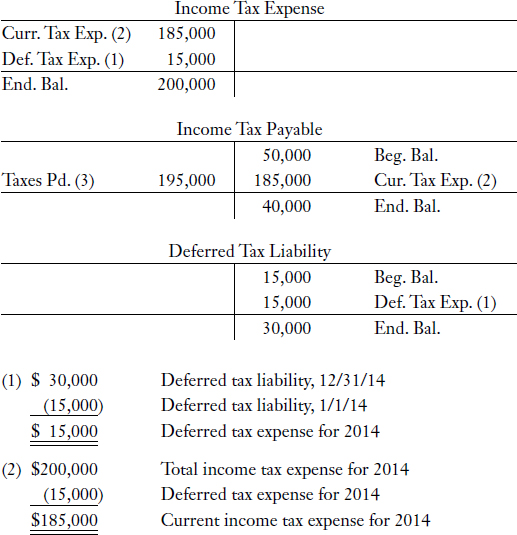

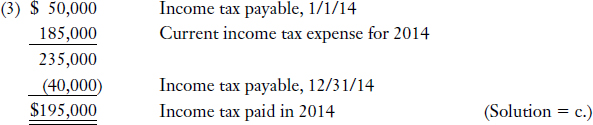

16. The following information was taken from the 2014 financial statements of Keewatinowi Corporation:

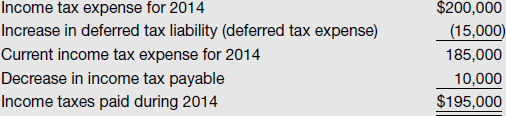

If the direct method is used to prepare the 2014 statement of cash flows, what amount should Keewatinowi report as cash payments for income taxes?

- $210,000

- $205,000

- $195,000

- $190,000

EXPLANATION: Draw T accounts. Enter the information given and solve for the missing amounts.

The use of T accounts is a good approach because it requires only that you recall the normal balance of relevant accounts and the transactions that affect those accounts. Picturing the accounts helps you determine the amounts of any debits or credits that affected each account. Another approach that requires more analysis of the relationship between the accounts appears as follows:

Question

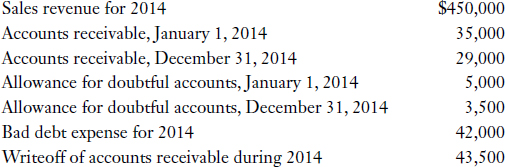

17. The following facts are available for the Pace Company:

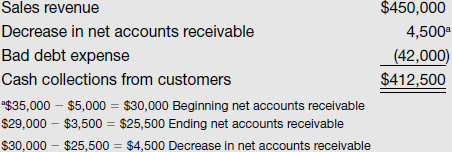

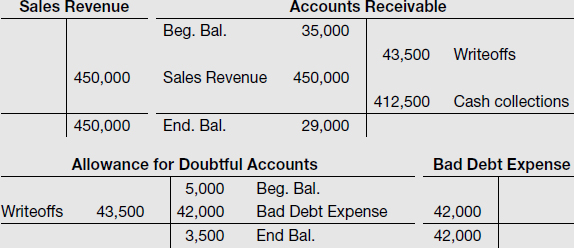

The amount of cash collections from customers during 2014 was:

- $498,000.

- $496,500.

- $487,500.

- $412,500.

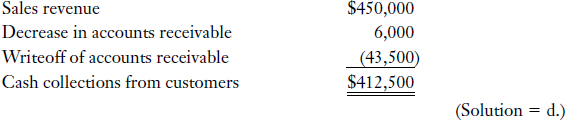

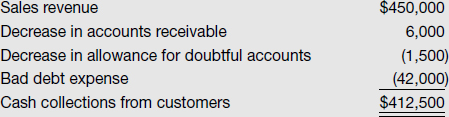

EXPLANATION: The amount of cash collections from customers is calculated as follows:

- An alternative solution is as follows:

- Another way of solving for the above is as follows:

- Draw T accounts for Sales Revenue, Accounts Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense. Enter the information given and solve for the missing amount. The T accounts would appear as follows:

- Assume all sales were on account. Even if some sales were cash sales, the answer would be the same for total cash collections.

Question

18. The activities of a discontinued operation should be presented on the face of a statement of cash flows as follows:

- in one net amount, under cash flows from operating activities.

- in one net amount, under cash flows from investing activities.

- in one net amount, under cash flows from financing activities.

- separately, with a net amount attributed to operating activities, a net amount attributed to investing activities, and a net amount attributed to financing activities.

EXPLANATION: Net cash flows attributable to operating, investing, and financing activities of a discontinued operation are presented separately on a statement of cash flows. (Solution = d.)

Question

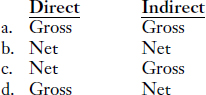

19. Both ASPE and IFRS allow either the direct or the indirect method of presenting the statement of cash flows; however, use of the direct method is preferred. Which of the following statements is true?

- Cash flow from operating activities is higher under the direct method than it is under the indirect method.

- Cash flow from operating activities is lower under the direct method than it is under the indirect method.

- Presentation of information under cash flow from investing activities and cash flow from financing activities is different under the direct method than it is under the indirect method.

- Under both the direct and indirect methods, the statement of cash flows is the same except for the presentation of information under cash flow from operating activities.

EXPLANATION: The only difference between the direct and indirect methods is the presentation of information under cash flow from operating activities. The direct method gives more detail about operating cash inflows and outflows, which is why it is the preferred method. (Solution = d.)