Chapter 8

Small Value: Diminutive Dazzlers

IN THIS CHAPTER

![]() Recognizing a small value stock

Recognizing a small value stock

![]() Praising the return king of all stock styles

Praising the return king of all stock styles

![]() Earmarking ETFs that track small value indexes

Earmarking ETFs that track small value indexes

![]() Knowing how much to allocate

Knowing how much to allocate

![]() Factoring in mid caps

Factoring in mid caps

Look at the list of some of the top companies represented in the Vanguard Small-Cap Value ETF: Devon Energy Corp., Index Corp., VICI Properties, Inc., L Brands, Inc., Nuance Communications. These are not household names. Nor are they especially fast-growing companies. Nor are they industry leaders. Nor is there much excitement to be seen in companies such as Index Corp. — a corporation that designs, produces, and distributes positive displacement pumps and flow meters, compressors, and injectors. As you go farther down the list of holdings, you’ll likely find some companies in financial distress. Others may be facing serious lawsuits, expiration of patents, or labor unrest. If you wanted to pick one of these companies to sink a wad of cash into, I would tell you that you’re crazy.

But if you want to sink that cash into the entire small value index, well, that’s another matter altogether. Assuming you could handle some risk, I’d tell you to go for it. By all means. Your odds of making money are pretty darned good — at least if history is your guide.

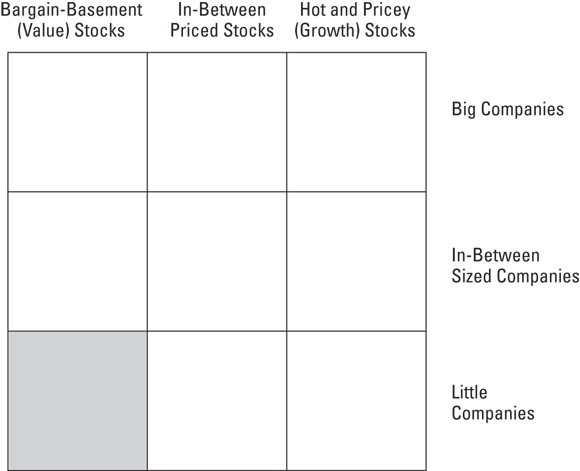

Don’t take my word for it; see Figure 8-2, which shows the enormous growth of value stocks over the past nine decades. On the way there, see Figure 8-1, which shows where small value fits into the investment style grid I introduce in Chapter 4. And then, follow me as I explain the importance of small value stocks in a poised-for-performance ETF portfolio.

FIGURE 8-1: Small value stocks occupy the southwest corner of the investment style grid.

Source: Colby Davis, RHS Financial, based on data provided by Ken French’s Data Library.

FIGURE 8-2: As you can see, small value has truly shined in the past nine decades.

It’s Been Quite a Ride

Small value stocks collectively have returned more to investors than have large value stocks or any kind of growth stocks. In fact, the difference in returns has been somewhat staggering: I’m talking about an annualized return of about 14 percent over the past 94 years for small value, versus 12 percent for large value, 10 for large growth, and 9 for small growth. Compounded over time, the outperformance of small value stocks has been HUGE.

Latching on for fun and profit

To be sure, small value stocks are risky little suckers. Even the entire index (available to you in neat ETF form) is more volatile than any conservative investor may feel comfortable with. But as part — a very handsome part — of a diversified portfolio, a small value ETF can be a beautiful thing indeed.

If you knew the past was going to repeat, such as it did in the movie Groundhog Day, there’d be no reason to have anything but small value in your portfolio. But, of course, you don’t know that the past will repeat. Bill Murray’s radio alarm clock may not go off at sunrise. And the small value premium, like Bill Murray’s hairline, may start to seriously recede. Still, the outperformance of small value has historically been so much greater than that of small growth that I favor a good tilt in the direction of value.

But keeping your balance

Whatever your total allocation to domestic small-cap stocks (see Chapter 21 for advice), I recommend that anywhere from 60 to 75 percent of that amount be allocated to small value. But no more than that, please. If the value premium disappears or becomes a value discount, I don’t want you left holding the bag. And even if small value continues to outperform, having both small value and small growth (along with their bigger cousins, all of which tend to rise and fall in different cycles) will help smooth out some of the inevitable volatility of holding stocks.

There aren’t nearly the number of small-cap value ETFs as there are large-cap funds, but still, you have choices. The best choices among small value ETFs include offerings from iShares and Vanguard. I also review an option from Invesco, which isn’t terrible.

iShares Morningstar Small-Cap Value Index (ISCV)

Indexed to: Morningstar’s Small-Cap Value Index (about 1,300 companies of modest size and modest stock price)

Expense ratio: 0.06 percent

Average cap size: $4.0 billion

P/E ratio: 16.4

Top five holdings: AMC Entertainment Holdings, Inc., Ovintiv, Inc., Apartment Income REIT Corp., Tenet Healthcare Corp., Cimarex Energy Co.

Russell’s review: My only complaint with the Morningstar indexes is that they tend to be a bit too concentrated, at least in the large-cap arena where a company like Microsoft can hold too much sway. (It presently comprises almost 10 percent of the large-growth index.) In the Morningstar small-cap indexes, that isn’t a problem. The largest holding here, AMC Entertainment, gets only a 1.5 percent allocation, which is fine and dandy. The expense ratio is the lowest in this category. And I like that Morningstar promises no crossover between growth and value. If you own this ETF along with the iShares Morningstar Small-Cap Growth Index, you should get pleasantly modest correlation. (In lay terms, if one fund gets slammed, the other may not.)

Vanguard Small Cap Value ETF (VBR)

Indexed to: The CRSP U.S. Small Cap Value Index (about 930 small value domestic companies)

Expense ratio: 0.07 percent

Average cap size: $5.7 billion

P/E ratio: 20.2

Top five holdings: Index Corp., VICI Properties, Inc., Devon Energy Corp., L Brands Inc., Williams-Sonoma, Inc.

Russell’s review: This ETF has low cost, wide diversification, tax efficiency beyond compare, and a very definite value bias — what’s not to like? Um…the average market cap is larger than I would find ideal. For that reason, I’d say the Vanguard Small-Cap Value ETF offers a very good way to tap into this asset class, but I can’t call it great.

iShares S&P Small-Cap 600 Value Index (IJS)

Indexed to: 550 of the S&P Small Cap 600 Value Index companies

Expense ratio: 0.18 percent

Average cap size: $2.0 billion

P/E ratio: 20.1

Top five holdings: GameStop Corp. (Class A), Macy’s, Inc., PDC Energy, Inc., Resideo Technologies, Inc., Signet Jewelers Ltd.

Russell’s review: S&P indexes are a bit too subjective for me to want to marry them. Case in point is that the largest holding in this portfolio is GameStop. Yup, that’s the same GameStop that appears as a major holding in the iShares S&P Small Cap 600 Growth Index ETF (see Chapter 7). I find that confusing, and, as a rule, I don’t go out of my way to own investments that confuse.

Invesco S&P 600 SmallCap Pure Value (RZV)

Indexed to: S&P SmallCap 600 Pure Value Index (approximately 150 of the smallest and most valuey S&P 600 companies)

Expense ratio: 0.35

Average cap size: $1.2 billion

P/E ratio: 20.2

Top five holdings: Genworth Financial, Inc., Customers Bancorp, Inc., EZCORP, Inc., Boston Private Financial Holdings, Inc., Hanmi Financial Corporation.

Russell’s review: The price is higher than others in this category, and the promise of “purity” is a bit murky, especially if that quest for purity leads to high turnover, which can bleed profitability. The average market cap is quite small. When cap size gets too small (and small caps start looking like micro caps), liquidity becomes an issue, and index funds can sometimes get hurt.

What About the Mid Caps?

In a word, my take on mid-cap ETFs is…why? Yes, there are years when mid-cap stocks — investments in companies with roughly $2 to $10 billion in outstanding stock — have performed especially well. There are years where mid caps have done better than either large- or small-cap stocks. But there aren’t many such years. It’s a rarity.

If you look at the risk/return profile of mid caps over many years, you find that it generally falls right where you would expect it to fall: smack dab in between large and small cap. Owning both a large-cap and small-cap ETF, therefore, will give you an average return very similar to mid caps but with considerably less volatility because large- and small-cap stocks tend to move up and down at different times.

Other investment pros may disagree, but I really don’t see the point of shopping for mid-cap ETFs, even though there are many mid-cap offerings. Keep in mind, too, that most large-cap and small-cap funds are rather fluid: You will get some mid-cap exposure from both. Many sector funds — including real estate, materials, and utilities — are also chock-full of mid caps (see Chapter 10).