Chapter 13

Confronting Uncertainty

IN THIS CHAPTER

![]() Seeing the dangers of ignoring change

Seeing the dangers of ignoring change

![]() Tracking economic, governmental, cultural, and technological trends

Tracking economic, governmental, cultural, and technological trends

![]() Looking ahead with trend forecasting, scenario planning, and hedging

Looking ahead with trend forecasting, scenario planning, and hedging

![]() Assessing the effects of change

Assessing the effects of change

Wasn’t it some ancient Greek wise man who said, “Change is the only constant in life”? Wise words indeed. Change defines life. All people expect change. At one time or another, no doubt, you’ve said, “I really need a change.” (Or was it the ex who said that? Never mind.) But you don’t often hear people say that they want a change or like change. People generally prefer stability in their lives. Change makes the future uncertain, and uncertainty makes planning difficult. But you can’t avoid change, so what are you going to do? For starters, keep reading this chapter (and this book) and learn to manage change.

But we must warn that you have the privilege of living in an era of unprecedented economic transition. If you’re one of those who has fresh ideas about market disruptions, that’s good — conditions are favorable. Yet the downside is that the old “rules” often no longer apply, so in many cases you will be flying blind — and might need a parachute. Measure your risks appropriately, whatever it is that you do.

We start by defining the elements of change, including economic, governmental, cultural, and technological trends. We look at ways in which you can anticipate change by forecasting trends and creating alternative scenarios. And we show you how to assess the possible effects of change and how to use innovation to take advantage of change.

Understanding the Dangers of Ignoring Change

Since companies are still run by people, they don’t want or like change either, and they come up with hundreds of excuses to try to keep business operations just the way they are. Here are some of the top excuses:

- Never been tried before. (Or we’ve tried it before.)

- Too radical. I don’t like radicals. If it ain’t broke, don’t fix it.

- We don’t have the time. (Or it’ll take too much time.)

- We’re not ready for it. Our company is different.

- It’s impossible. Now get back to work!

Many companies often try to avoid change, especially if they’ve been around awhile and seem to be successful in what they do. But denial is not a big river that runs through some other continent. Change needs to be both acknowledged and confronted by the business planner. It is what makes a market work. Change allows companies to form and grow, products and services to get better, competitors to emerge from everywhere, and customers to go on shopping. Small or new companies often champion this change, because they have little interest in maintaining the status quo. Disruption is their entry ticket to the game. In a competitive marketplace, if you stop changing, you die. This is a harsh but true reality.

Many companies often try to avoid change, especially if they’ve been around awhile and seem to be successful in what they do. But denial is not a big river that runs through some other continent. Change needs to be both acknowledged and confronted by the business planner. It is what makes a market work. Change allows companies to form and grow, products and services to get better, competitors to emerge from everywhere, and customers to go on shopping. Small or new companies often champion this change, because they have little interest in maintaining the status quo. Disruption is their entry ticket to the game. In a competitive marketplace, if you stop changing, you die. This is a harsh but true reality.

Good companies understand this fact but often have a hard time acting on it when they become successful — maybe because they have more at stake. The original Fortune 500 list, published in 1955, represented the biggest and best American companies of the era. Today, only a few of those original companies still appear on the list. Many operate in completely different businesses.

Across all industries, the list of companies whose stars have dimmed in the recent past continues to grow, if not glow:

- In the 1950s everyone looked up to General Motors, Sears Roebuck, and US Steel as exemplars of business leadership. “What was good for [America] was good for General Motors, and vice versa” was famously claimed.

- The 1960s and 1970s saw the rise of IBM and McKinsey & Co. as best in class.

- General Electric, Microsoft, and Goldman Sachs were deemed the role models of the 1980s. In Search of Excellence, published in 1982 and hailed as the best business book of all time, highlighted 43 American firms that succeeded in the face of fierce foreign competition. Later many declined, some fatally.

- Aggressive “new economy” firms like Blockbuster boomed in the 1990s. So did other tech companies like Hewlett-Packard, ITT Industries, Motorola, and Xerox.

Numerous articles and books have been written on these companies, on their industries, and on their times. In fact they are responsible for a thriving mini-industry within the publishing business. In each case, you can summarize the arguments by stating that these formerly successful companies failed because they didn’t or couldn’t change with the times. At some point, they each became frozen in the past, and that doomed them to extinction. And now the new century has brought us Facebook, Apple, Amazon, Netflix, and Google — the so-called FAANGs — as the role models for business excellence. Are they destined to suffer a similar fate at some point?

Defining the Dimensions of Change

Events and forces beyond your control continuously change the business conditions around you. You can’t fiddle with the laws of physics, but if you want your company to survive, you must keep track of changes as they take place. The experts call the practice environmental scanning — not the kind that the U.S. Environmental Protection Agency (EPA) does, but the kind that looks at anything that may affect your business situation. This approach is often called PEST analysis (or STEP if you rearrange the letters, because the first acronym reminds you of your little brother). This is a term that captures the four major categories of change that you need to monitor: political, economic, social/cultural, and technological.

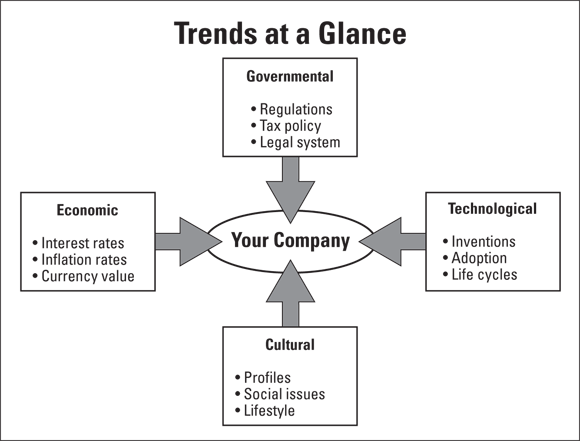

Although multiple factors can influence your business environment, you can simplify matters by looking at the major trends shown in Figure 13-1. (For the details, check out the following sections.) When radical changes threaten to reshape your industry and marketplace, you can bet that the underlying causes involve broad economic, governmental, cultural, or technological trends.

© John Wiley & Sons, Inc.

FIGURE 13-1: You can break a business environment scan into four major groups of trends.

Governmental trends

We won’t win any prizes by reminding you that the government has a profound effect on your company and your industry. From the rules and regulations that it issues to the tax policies and legal system that it supports, the government is a major player in your marketplace. Because of its sheer size and impact, the government sparks continuing national debate on how large, how wide, and how deeply involved it should be in the day-to-day running of the economy.

Some may desire a return to a mythical past in which small-town America could mind its own business without interference from “outsiders.” In that long-gone time, everything was small enough that local social pressure could keep the bad apples from spreading their rot. But that’s history. Today our massive national and global economy doesn’t allow for such intimacy. We often don’t know who supplies our products or where they’re located, let alone what individuals might be responsible for decisions. And who wants a world in which companies can sell products that endanger lives or tout benefits that are blatantly false? We also don’t want private business firms to be able to ride roughshod over the competition and become bloated monopolists just because they can.

We hope that business leaders realize they have social responsibilities beyond the bottom line. Nobody likes regulation, especially excessive rules and requirements that raise costs and prices for all without clear societal benefit. But when business folks, for whatever reason, do cross the line of responsibility and harm others, we need an active government that can protect consumers and competitors alike.

No matter which side of the more-or-less-government debate you stand on, be sure you do the right thing. You also need to keep track of where the discussion in your industry is heading. Governmental actions at any level — local, state, or federal — can rapidly and dramatically alter your business environment, and you should include a summary of the relevant governmental trends in the “Business Environment” section of your business plan (see Chapter 1).

What kinds of issues should you watch for? Topics that arouse public opinion and finally lead to some sort of governmental reaction seem to have a predictable cycle of three stages. The timeline of the cycle, however, has become compressed with the rapid spread of online communications technologies. BSM (before social media) time is history, so you have to respond rapidly today:

- In stage 1 of the cycle, when some new problem or issue arose that was interpreted by some to be harmful, nothing much happened; it might have warranted an article here or an opinion poll there.

- But if the issue touched a nerve and could have serious consequences for many, stage 2 would kick in. It would begin to snowball with national media — ever on the prowl for stories that would attract readers or viewers — jumping on the bandwagon with exposés and accusations that drew attention.

- Finally, in stage 3, if threats to the public good posed by the issue at hand were serious enough, mounting public pressure finally got the political establishment to take action and pass some form of government legislation.

All three stages are still there today. But stage 1 has gone from taking months or even years to evolve to instant diffusion via social media. One perceived bad experience by an aggrieved customer becomes a viral wave on the web, complete with video or still pictures. If it’s your business that is alleged as the bad guy, you could be in deep doo-doo, right now. If it’s someone in your industry, you need to get the facts ASAP and ensure the stench doesn’t spread to your own organization. Stay alert so you can avoid the dirt.

At the federal level, government has three branches — executive, legislative, and judicial — and each branch can affect your company. You also need to think about local, state, and foreign governments.

You may need a little help in picking out the governmental activities and trends that can affect your business environment. Almost every industry has a trade association, along with an industry newsletter or two, most of which are conveniently online today. These organizations devote much of their time and resources to keeping tabs on — and influencing — current events at all levels of government. The larger ones also track relevant happenings abroad.

You may need a little help in picking out the governmental activities and trends that can affect your business environment. Almost every industry has a trade association, along with an industry newsletter or two, most of which are conveniently online today. These organizations devote much of their time and resources to keeping tabs on — and influencing — current events at all levels of government. The larger ones also track relevant happenings abroad.

Executive branch

The person who calls the White House home sets the general tone and direction of the U.S. government. When President Joe Biden took office in 2021, he quickly convinced Congress to pass legislation designed to counter the collapse of the economy caused by the COVID-19 pandemic that his administration inherited. Trillions of dollars began to flow into the bank accounts of millions of Americans, and these soon reverberated in ringing cash registers across the country. Certainly not all, but many business firms in numerous industries benefitted. Maybe yours, too.

On the other hand, if you have anything to do with the traditional fossil-fuel energy industry, it could be a different story; that ringing you hear in the distance could be the church bells tolling for thee. As evidence mounts that carbon contributes to global warming and environmental catastrophes, the Biden administration has called for significant curbs on the activities of oil and gas companies.

Think about this: How might the federal government’s agenda influence the future of your industry?

Legislative branch

Congress writes the laws of the land and holds the nation’s purse strings. Only the House and Senate, acting together, have the authority to spend your tax dollars. This can range from national security and defense expenditures to social programs such as Social Security and health benefits to enhance the lives of Americans.

More recently, Congress has been wrestling with how to provide oversight to financial market disruptions due to “fintech” innovations. New products and services enabled by technological change, such as cryptocurrencies from Bitcoin to Ethereum to altcoins, are revolutionizing financial markets. Until the dust settles, these markets will remain volatile. If your business is affected, will you discover new opportunities or see only threats?

Judicial branch

The federal courts interpret all the laws that Congress passes each year, so they have a profound effect on every industry in America.

Recent investigations for potential antitrust violations in industries as varied as sports, media, entertainment, airlines, education, and others are shaking up the status quo. Who knows, your little corner of commerce could be next if you don’t pay attention (or conversely, an industry breakup could be just the means by which your little firm can now get into the game and survive).

Local and state governments

You are also liable to be touched by the actions of local governmental agencies, from state government to a special purpose “district” in your immediate neighborhood. In many cases, especially if you’re a smaller business, these can be more intrusive than something from the feds. These apply to activities as varied as water consumption prohibitions to your proximity to certain types of structures. Some states prohibit the sale of alcoholic beverages within a minimum distance of schools or churches. Others allow or disallow the growing or distribution of cannabis products or paraphernalia. Depending on what you do, you may need a state or local permit or license just to open your doors for business each morning (and some even have restrictions on days and hours of operation).

Foreign governments

Globalization is a recurring theme in this book, and it applies to monitoring foreign government and public policy trends as much as domestic. We note earlier in this chapter that currency fluctuations can impact your ability to plan for your business, even if you don’t directly engage in exports or imports from international markets. Look at these recent examples:

- The government of China has taken steps to minimize the influence of foreign cultures on its citizens. This has resulted in problems for U.S. firms engaged in entertainment sectors as varied as movies and TV shows, theme parks, gambling casinos, and publishing that have China-based sales and operations. The same government also wants to clamp down on the online gaming industry in an attempt to get the millions of young Chinese boys and girls who spend hours a day on those obsessive sites to devote more time doing calculus, practicing violin, or something else. U.S.-based firms who compete in China’s vast market were caught off guard by these sudden public announcements.

- The upheaval caused by the COVID-19 pandemic wreaked havoc for countless U.S. businesses engaged in the travel and tourism industries. Constantly changing rules and regulations kept these firms in the dark regarding the ability of foreign guests from European nations to travel to the United States and fulfill reservations sometimes made months in advance. U.S.-based firms in manufacturing industries suddenly faced parts shortages as their Asian suppliers shut down as the virus reduced the able-bodied workforce there.

It can be a caveat emptor world when dealing in foreign markets. Exercise caution. (And in fairness to our global readers out there, this advice applies just as much to firms engaged in trade with the United States.)

Economic trends

At an individual level, people use bank accounts, home mortgages, car loans, and credit cards every day to navigate through the financial contingencies of their lives. We save, spend, borrow, dream. At the same time, public agencies responsible for economic oversight and the financial institutions they oversee are making their own calculations, based on mandates to stabilize the national economy and, for private financial actors such as CEOs of corporations, generate profit as they measure the risk and reward trade-offs they face. When combined, these zillions of micro financial decisions create the complex glue that holds our “macro” economy together.

It is a large, complex, and enormously critical task to keep everything rolling along without the economy going off the rails. But as we have seen all too tragically in the first decades of the 21st century global economy, our best and brightest who control the levers don’t always succeed. The Great Depression of the 1930s still defies a standard explanation of causality. The Great Recession of 2008–2009 continues to generate learned theories that all seem to contradict the one just published. Perhaps the biggest mystery in economics is why no one seems to understand the basic forces at work.

Economics certainly sounds like science. People in the know always talk about it in terms of numbers — inflation rates, growth rates, interest rates, exchange rates, productivity levels, unemployment figures, price indices, blah, blah, blah. By the early 20th century, economics became math, the purest of the sciences. But when it comes to predicting the future levels of these indicators today (and what they mean to consumers and companies), the science can become rather subjective, kind of science-y in fact rather than slam-dunk truth telling. Even worse, the fault lines of political division have also blurred agreement on the direction, magnitude, or significance of the numbers. It’s not astrology yet, but macroeconomics does seem to be a discipline in search of its very foundations.

However, economists do agree on some basic facts:

- Economic indicators constantly change.

- Indicators are sometimes predictable.

- Indicators somehow relate to the performance of the economy.

- The overall economy affects your business environment.

Obviously, economic uncertainty isn’t very satisfying. But economic trends are important enough that you need to keep track of them, even if your information is incomplete and the underlying theories sometimes questionable. The most important economic trends for your industry should be incorporated into the “Business Environment” and “Financial Review” sections of your business plan (see Chapter 1). What numbers should you keep your eyes on? It depends on your business.

If you sell new cars, for example, most of your buyers finance their purchases with loans that have monthly payments tied to interest rates. So low interest rates are extremely important to the overall health of the auto industry. Interest rates make or break the home-building market for the same reasons, as well as the home-loan industry that supports it. If you’re a techie chasing the Next Big Thing, you need to know the specific pace of invention and innovation in your service or product niche. If you’re in a labor-intensive service business, like quick-service restaurants (fast-food restaurants to the rest of us), you need good, entry-level workers. Their ready availability hinges on wages and regional unemployment levels. As an exporter, you want to examine exchange rates and the current level of the dollar against the currencies of your international target markets.

No business is immune from economic forces, and that includes yours. The following sections highlight four key economic indicators reflective of major trends in the economy that you should watch closely.

GDP

The GDP (Gross Domestic Product) is the total value of a country’s annual production of goods and services. You should keep track of the change in GDP from year to year, because that change reflects the current overall economy. Moderate, consistent growth in the GDP generally produces a healthy economy with expanding opportunities for many businesses. A drop in the GDP, on the other hand, often leads to lower demand for products and services, an increase in competition as incumbent firms fight for survival, and lower profits for everyone.

You can’t always generalize based on the GDP, however; look at how your industry and your company performs within the larger economy.

Interest rates

Interest rates represent the cost of renting money — how much you have to pay a bank, for example, to use its cash for a certain period. Short-term rates apply when you borrow money for periods ranging from a month to two years (or even shorter times from “pay-day” lenders who extract exorbitant rates for those in need of cash right now, to be repaid the next pay day). Long-term rates apply to loans that extend all the way out to 30-year home mortgages. As you can imagine, the cost of money affects every facet of the economy, from consumer spending to business expansion.

In the United States, the Federal Reserve Bank in Washington (the Fed that holds the nation’s bank account) pretty much sets the short-term interest rates. With seemingly everyone now having access to a credit card (or four or five), short-term rates influence shopping habits: The lower the interest rates, the easier (and cheaper) it is for shoppers to buy on credit. So if you want to start a retail business, you have to pay special attention to how short-term interest rates might affect demand by your target customers.

And that also means you’re likely to have to accept credit as a form of payment. Have you noticed that even that tasty little taco and burrito truck who shows up at lunch time takes your card? Innovative e-commerce ecosystem lenders like Square came up with technology that lets the little guy use a smartphone to accept payment. Different card vendors, however, offer varying terms to small firms, so you need to be careful in finding one that’s best for your business.

Long-term interest rates rise and fall in the corporate and government bond markets. Bonds, as opposed to stocks, are fixed income investment products that yield a defined rate of return over a specified period of time to the lender. The value of stocks, of course, can rise or fall on a daily or even minute-by-minute basis. Long-term bond rates have a major impact on how easily consumers can afford houses, cars, and all other “big-ticket” (expensive) purchases, because consumers usually finance these items with long-term loans. Long-term rates, therefore, affect consumer demand for big-ticket items.

Inflation rates

Inflation, or a continuous rise in wages or prices, is a nasty habit that economies often suffer from. Consumers are the first to know when inflation rears its ugly head, because prices go up and money can’t buy as much as it used to. And lenders aren’t thrilled either: Under conditions of inflation, the payments made to repay their loans are worth less than the value of the loan when it was first handed over.

When inflation is high, companies find that resources and assets are more expensive for them as well. They have to pay more for everything from materials to employees’ wages and benefits. Investors turn their attention to products that have greater intrinsic value, such as gold, real estate, collectibles, and art — tangible or hard-to-replace goods that protect them against less valuable paper money that governments might simply print more of to pay bills (or fund popular new programs that keep voters happy and politicians in office). Consumers may borrow more money, partly to pay the higher prices and partly because they can pay back today’s cash with less valuable money. If the amount of goods produced remains static, but the amount of money out there increases, then the classic problem of “too much money chasing too few goods” drives up prices as customers bid more to get what they want. Lenders, including the Fed, sense the economic landscape, so interest rates go up.

Not all companies suffer equally from inflation, however. If you mine precious metal, pump oil, or sell real estate, for example, you can often do quite well during a period of inflation. If you operate any other business, however, you have to balance the broad economic trend against its effect on your industry.

All these factors are a real drag on the economy over time, and inflation can lead to a recession if the government and the Fed don’t attend to the problem. But let’s not forget what we note earlier in this chapter: Economists are struggling with understanding how the modern global economy works today. Huge injections of liquidity (cash) into the economy following the Great Recession of 2008 didn’t result in the surge of inflation that more conservative economists predicted. In fact, inflation came down to historic lows and stayed there. But then came the COVID-19 pandemic of 2020, subsequent governmental programs of cash handouts to prevent economic collapse — and inflationary surges in certain categories of goods. Go figure. No wonder they call it the dismal science.

Currency value

In today’s global economy, the rise or fall of the U.S. dollar against the Euro or other currencies can have an enormous impact on your entire industry. Your suppliers, competitors, and customers may be anywhere in the world, no matter what industry you’re in or how small your company is.

This has become especially acute with the rise of China as the “world’s factory.” Unlike most large economies in which the value of their currency “floats” according to market conditions (that is, rises or falls with global demand), that country’s government has maintained tight control over its economy, particularly by keeping the value of its currency low compared to other nation’s money. This was done to protect its manufacturers from foreign competition and to promote its products in world markets by keeping their costs (and prices) low when compared to local competitors. The result is that China became the world’s largest exporter of goods, and its success as a low-cost provider threatened competing producers almost everywhere. China’s currency manipulation policies have lessened in recent years, without question, but for many firms and industries it was too late as the damage was already done. (Ever heard of the Rust Belt?)

The lesson here for your business planning efforts is that you need to keep a sharp eye out on currency values. But wait, you say; “I don’t compete outside the shores of my own nation, so why would any of this economic gobbledygook affect me?” For good or bad, you do compete in the world today. Globalization has changed the playing field of commerce beyond recognition. Even with recent calls for the U.S. government to reign in free trade and impose protectionist economic policies, it is now clear that the tight weaving together of global supply chains won’t result in any quick-fix solutions. The bonds are too tight, and the benefits too good, for so many.

So stay vigilant. Short-term fluctuations in the value of the U.S. dollar are unpredictable. The effects of longer-term currency trends, on the other hand, are easier to predict. Be sure you understand how these might affect your own business planning.

Cultural trends

Take two frogs and a skillet. Place the skillet on the stove and bring a small amount of water to a boil. Drop one of the frogs into the skillet. The frog, no dummy that one, jumps out of the skillet, onto the floor, and out the door.

Place the skillet back on the stove, this time filled with cold water and the second frog (that first one’s long gone by now; think Pavlov). As the water slowly heats, the frog sits there agreeably, never noticing the rising temperature. (Don’t try this experiment at home unless you plan to have cuisse de grenouille for dinner.) The moral? When you ignore the slow changes that take place around you, you boil.

Cultural change doesn’t happen overnight. Yes, of course, we know there might be some hot new fad in fashion that’s here today and gone tomorrow (and maybe back again the day after tomorrow), but fashion is a special case. For most product or service categories, the glacial speed of these trends reflects the glacial forces that lie behind them. Most people, as we hint earlier in this chapter, really don’t like change that much; we’re creatures of habit who prefer the tried and true. The real danger lies in ignoring these slow-motion trend lines simply because you can always worry about them later.

Consider the cultural shifts we describe in the following sections.

Demographic changes

Demographic refers to the general profile of a specific population — anything from your company’s customers to the citizens of a nation. Demographic data includes attributes that you may find on a national census form, such as age, gender, and family size.

Changes in the profile of a nation are certain to have profound effects on its economy and business. Western Europe, Japan, China, and the United States, for example, are all trying to come to terms with the aging of their populations. Their governments have to figure out how to take care of all these older people, and companies are trying to figure out how to sell them their products or services. (Flip to Chapter 6 for more info on customer demographics and Chapter 7 for a rundown on generational customer groupings.)

Social changes

A society is made up of the combined values, customs, and traditions that its people hold in common. Social behavior changes over time, of course, but people tend to give up their traditions slowly and grudgingly (boy, don’t we know this in the United States today). Most American schools still give their children the summer off, for example, even though most children no longer need to work on the farm during those months.

Some still cling to a belief that women should remain as stay-at-home moms and leave the workaday world as a male-only domain. Honestly. But look at enrollments in college-degree programs for attorneys and physicians; women outnumber men today. Look at trending numbers in business schools; women are on a rapid rise. Can science and technology fields be far behind? If you said yes, that’s probably a losing wager.

But what happens to customs and traditions as the population changes — as people move from place to place, as families start to look different, and as newly sworn-in citizens bring along their own customs and traditions? Think of all the opportunities for ethnic restaurants (Vietnamese, Middle Eastern, and Ethiopian, for example) as new waves of immigrants move into different regions of the country. Any change in broad social behavior, no matter how slowly it occurs, can have a dramatic effect on your company and on industries across the economy.

Lifestyle changes

Changes in the way people live their lives affect how they work, what they buy, how they play, and where they live. Decades ago, for example, the health-and-fitness craze caught on in the United States. Today, the industry includes the makers of sports shoes, sportswear, exercise equipment, tennis rackets, mountain bikes, kayaks, yogurt, diet drinks, bottled water, and many other products. Diets also changed as awareness of healthy eating habits began to sink in; fish and white meat became preferred sources of protein, replacing traditional red meat entrees. Due to dramatic improvements in healthcare, most Americans can count on a longer lifespan than previous generations. One result is that growing numbers of seniors have given a kick start to pastimes like gardening.

Other major lifestyle changes that affect industries include

- Growing gender identification equality in every area

- Work-from-home (WFH) or hybrid jobs that have reduced in-office hours

- At-home shopping, education, and entertainment as the web expanded

- Alternative family units and their definition

- Older folks continuing to work past traditional retirement age

- Younger folks seeking better work-life balance

Technological trends

Technology breeds change, and change breeds technology. In the past 150 years, America has gone from buggies to citizen travel on space shuttles and from the Pony Express to the Internet. A hundred years from now, likely only 50 and possibly less, people may look back at our era and marvel at how primitive our technologies were. Today we are truly in another great Industrial Revolution that is touching almost every corner of the business world.

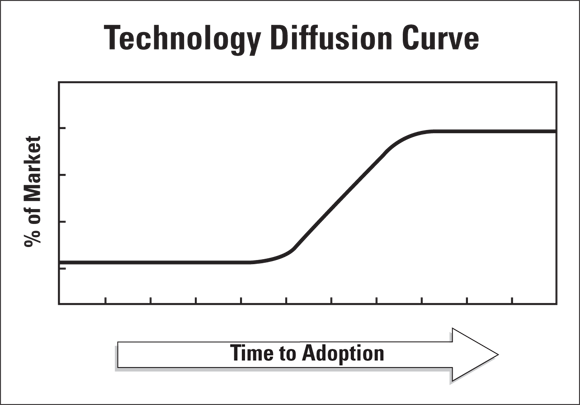

Every new technology doesn’t change the world overnight. Most don’t change the world at all, in fact. You could produce a television show on the world’s funniest inventions that pop up each week (though it would likely be better to stream for smartphone viewing). For the most part, the technologies that succeed have been evolving for quite some time. No matter how fast a new technology takes over from the old, it usually follows a diffusion curve, which traces how a new technology catches on in an industry (see Figure 13-2).

© John Wiley & Sons, Inc.

FIGURE 13-2: The technology diffusion curve points out that when a new technology takes off, it usually catches on rapidly.

The diffusion curve demonstrates that it always takes a certain amount of time for any new technology to take off. When (and if) it does hit hyperspace and catch on, the technology usually sweeps through an industry quickly, because companies don’t want to fall behind. But speed of diffusion is also changing — due to technology itself. It took more than 50 years for landline telephones to penetrate 80 percent of U.S. households, but less than 15 years for cellphones. The reason is because new information is not only being created in volumes unheard of in the past, but also because it’s communicated worldwide at laser-like speed (and laser-like is not an exaggeration). This is serendipity in action: The speed of transmission of new data quickens the pace of new data creation. This alone should offer insight to the value of a firm like Google.

As Figure 13-2 shows, the technology reaches its plateau when most of the incumbents in an industry adopt the new technology. The only groups left are the laggards — a topic we take up in Chapter 15, where we introduce you to the Product Life Cycle concept (no, this is not a product made by Peloton). But don’t blink when an industry gets to that stage, because the search for the Next Big Thing has already begun.

Knowing that not everyone wants the latest and greatest

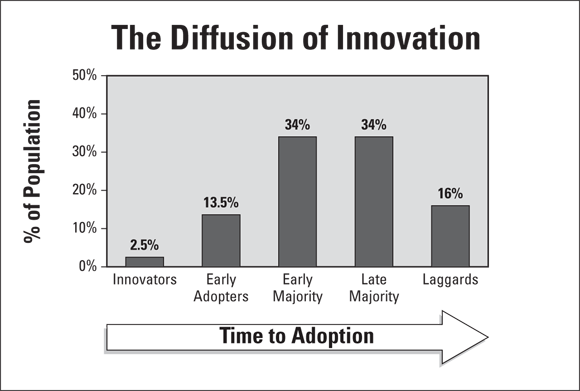

When technology leads to the emergence of product and service innovations, there isn’t a stampede for them by everyone. In fact, some customers are downright put off by the changes. Different strokes for different folks and all that. Behavioral scientists have come up with five basic personality types that react to the new in decidedly different ways, as we describe in Table 13-1.

TABLE 13-1 Customer Personality Types

Type | Description |

|---|---|

Innovators | Risk-takers of the world Young and well educated Comfortable with new ideas and technologies Mobile and networked Informed by outside sources |

Early adopters | Opinion leaders in their communities Careful evaluators Open to well-reasoned arguments Respected by their peers |

Early majority | Risk avoiders whenever possible Deliberate in their actions Unlikely to try new products until those products catch on |

Late majority | Skeptics Extremely cautious Disappointed by other products Reluctant to try new products Respond only to pressure from friends |

Laggards | Hold out until the bitter end Wait until products are old-fashioned Still hesitate! |

Why are customer personality types so important when you think about how to market that bright shiny new thing they came up with in the R&D lab? Because individual personality has a great deal to do with how eager people are to try out new products and services. Although some people are adventurous and willing to try anything new, others are quite the opposite. As shown in Figure 13-3, the percentage of people who represent each personality type is just an estimate, of course. But you get a rough idea of the relative size of each personality group.

© John Wiley & Sons, Inc.

FIGURE 13-3: Product adoption occurs at different times for different personality types.

We might not be willing to bet on it, but there’s a good chance you’re one of the Indiana Jones innovator types, or you wouldn’t be reading this book. For some firms, this has presented a problem. Why? Because these personality types tend to project their admiration for the new onto the entire population out there: “Hey, wow, look at this! I love it, it works! Let’s green-light it now.” And they did — and it sold, and this led to an expansion of production and in increase in expenditures. But then … the wall. Suddenly sales slowed or altogether died, and shelves full of those neat little new do-hickeys sat lonely and forlorn, as the bills came due while the cash register went silent.

The problem was that those shoppers who fit the innovator or early adopter type (see Table 13-1) were a relatively small segment of the overall market. The big segments — two-thirds to three-quarters of all customers — didn’t really “buy” products; rather, they had to be “sold” on them. This meant the engineers and scientists had to rely on the marketing team to conjure up creative ways to convince the skeptics that this really was something superior. Unfortunately, many of the R&D folks didn’t even have a marketing department up and in place; they were so convinced of the innate value of their innovation. They had to learn how to jump the wall (or “cross the chasm,” as it was explained in a classic study of Silicon Valley technology adoption stories). Many never could make the leap, and died.

The important thing to remember about the diffusion of innovation is that if you bring a brand-new kind of business or service to the marketplace, the innovators and early adopters are going to be easier to capture than the majority of consumers out there. The longer your kind of product or service has been around on the market, the more effort you must spend focusing on your customers and understanding their wants, needs, and motives. (For more on how to do this, go to Chapter 7.)

Tracking tech trends

What do these examples say about trends in technology? Although each industry is different, a few generalizations come to mind:

- Older technologies often have time to adjust to innovations.

- Older technologies can be improved even after they mature.

- New technologies usually begin by focusing on specialized customers and markets.

- New technologies can create new customers, expanding the marketplace.

- Old and new technologies often live together for many years.

You may struggle to predict the coming of a new technology and what’s going to happen when it arrives. To prepare yourself for possible changes in technology and the potential effects on your industry, review the major technologies that consumers currently use. For each technology, do the following things:

- Find out which research laboratories specialize in the technology and what technical journals and publications, print and digital, cover and report on it. Make sure that you check out academic, private, and government institutions.

- Attend major conventions and scientific meetings on the technology and subscribe to any relevant news sources.

- Monitor online blogs and company press releases on the technology and keep track of patents that innovators file in the field.

- Compare your company’s capability to adapt to and apply technology to that of your key competitors.

- On a regular basis, re-examine the likelihood of a fundamental technological breakthrough and check the status of small, step-by-step process improvements in technology.

Although technologies within your industry may be unpredictable, you should track them over time and take them into account as you create your business plan. The technology advances in unfamiliar areas, however, have the potential to bite you while you sleep. When Xerox introduced its first copier in 1959, it basically stopped mimeograph machine makers cold. When Hewlett-Packard came out with its first handheld calculator in 1970, slide-rule manufacturers took a fast slide into oblivion. Kodak may have missed the digitization of photography, but the Sonys and Canons and Minoltas and others who produced those substitutes failed to recognize the incorporation of optics technology into smartphones. These pocket-sized devices spelled their doom. Today that Swiss-knife do-it-all tool has powerful camera capabilities, both still and video. Why carry a heavy camera about when your phone does just as well — and allows for immediate transmission via texting to either friends or your social media platform? No-brainer.

So you want to keep your eye on technology trends beyond your immediate industry. That way, you become better prepared for unexpected changes.

Anticipating Change

You probably have a hard time keeping track of what goes on around you; never mind trying to anticipate what’s going to happen in the future. The point isn’t to predict the future, however; you can’t. Instead, your goal should be to understand what may happen to prepare yourself better than your competition.

To do that, you need to estimate which of the many trends — economic, governmental, cultural, and technological — will become the megatrend that produces tomorrow’s innovation and makes tomorrow’s entrepreneurs rich. What trend will have an influence on your industry, your strategies, and the competition?

Start by turning to the professionals and hearing what they have to say. Scan the various sources, online and otherwise, that follow these trends. After time passes, you can judge which of them are most useful. In the business world, there’s no shortage of news sources that can keep you up-to-date on what’s going on, either in general or in your specific little corner. For the big picture stuff, the traditional go-tos remain The New York Times and the Wall Street Journal, the U.S. editions of The Financial Times and the Economist, Bloomberg BusinessWeek, Forbes, Foreign Affairs, and Public Policy, among others. All of these media have both print and digital versions available. When it gets down to industry specifics, you may want to visit Chapters 5 and 8 for lists of sources.

And don’t forget that some organizations specialize in keeping their clients up-to-date about a given field of interest, including the Aspen Institute, Deloitte, McKinsey, and PwC among many others. They’re not free, but they have full-time experts who constantly stay on top of current events and bring a wealth of knowledge of the past as well in order to see what the future might hold.

Sometimes trends are too unpredictable or too numerous to track, so you can’t project a single view of the future that seems to make any sense. Scenario planning allows you to imagine several complete versions of the future and consider how each version can affect your company’s fortunes. Military strategists use war scenarios all the time. So do experts in public health when they try to anticipate and prepare for the spread of a global epidemic (or at least they used to). Scenarios can help your business imagine a variety of future prospects, too.

Start with a trend — the inflation rate, for example — and think about how you can create two or three alternative scenarios for the future, based on different levels of inflation. (For more information on inflation, refer to the earlier section “Economic trends.”) Try to include a fairly complete description of what your business environment may look like in each case.

Don’t hesitate to introduce another important trend into your scenario. Maybe your company’s future is also tied to federal regulations that the government may announce sometime in the next five years; you can put together another set of scenarios that involve those regulations. But now you have three possibilities for regulation and three possible levels of inflation to juggle. Obviously, this situation can get out of hand rather quickly.

Experienced scenario jugglers are quick to point out the wisdom of working with no more than three or four scenarios at a time. Rather than add trend after trend into a growing set of scenarios, limit yourself to three complete scenarios based on different views of your industry in the future:

- A scenario based on an optimistic view

- A scenario based on a pessimistic view

- A scenario based on the most likely view

You may decide that low inflation, minimum regulation, and a technology breakthrough create an optimistic scenario, and high inflation, heavy regulation, and no technology breakthroughs create the pessimistic view. The most likely view falls somewhere in between. You should include the most likely view in the “Business Environment” section of your business plan (see Chapter 1).

You may want to create a business plan for the future by looking backward and doing what you’ve always done in the past. That method is easy and comfortable — and dangerous. Scenario planning isn’t meant to predict the future; its real value lies in offering you new options and a wider range of possibilities to think about. Different business scenarios stimulate your imagination and bring to life compelling glimpses of your company’s future.

You may want to create a business plan for the future by looking backward and doing what you’ve always done in the past. That method is easy and comfortable — and dangerous. Scenario planning isn’t meant to predict the future; its real value lies in offering you new options and a wider range of possibilities to think about. Different business scenarios stimulate your imagination and bring to life compelling glimpses of your company’s future.

Preparing for a Changing Future

Changes take place around you all the time. Some changes have a big effect on your company; you scarcely notice others. Some changes are obvious and predictable; others come out of nowhere. The critical questions you face are

- Which changes may actually take place?

- What do the changes mean for your industry?

- What impact do the changes have on your company?

- What opportunities and threats are created by change? (See Chapter 5 for more details.)

The impact that a trend or an event has on your business tells you how hopeful or worried you should be if your predictions do come true. A trend may be the best thing to happen to one industry and a complete disaster for another. An event may create a major opportunity for your company or have no noticeable effect at all.

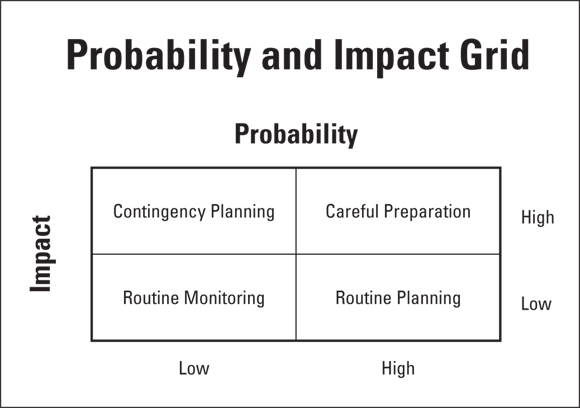

Review the business trends and scenarios you developed in the previous section, and place the significant events or possible outcomes you foresee in one of the four probability/impact categories shown in Figure 13-4. Each category requires a different level of planning and investment on your part:

- High-probability, high-impact events demand careful preparation.

- High-probability, low-impact events call for routine planning.

- Low-probability, high-impact events require contingency planning.

- Low-probability, low-impact events suggest routine monitoring.

© John Wiley & Sons, Inc.

FIGURE 13-4: The Probability and Impact Grid divides events into categories based on how likely they are to occur and what effect they may have.

If you need help figuring out which trends and scenarios belong in which categories, you always can call in the experts — but you’d better be prepared to open your wallet (and that’s not a guess). But first, see what you can do on your own. Assemble a group of your colleagues and maybe one or two of your best customers for a brainstorming session on the future of your company. You may be surprised by the insights that come out of your get-together when you start the ball rolling. Here’s what you do:

- Give the group members a fixed amount of time to review the trends and scenarios that you come up with and to throw in any new ones of their own.

- Have someone make a list as the group generates ideas.

- Put the complete list of trends and scenarios in front of the group.

- Rank trends and scenarios, based on their potential to affect your company’s future.

- Rank these trends and scenarios again, this time based on the probability that they will actually occur.

- Divide the trends and scenarios into the four probability/impact categories (refer to Figure 13-4).

The Probability and Impact Grid tells you where to concentrate your investment in time and company resources. Placing the trends and scenarios that you generate into probability/impact categories gives you a place to begin. Don’t go chasing after every trend. You should prepare for change, allocate time, budget resources, and plan for possible events based on a practical combination of probabilities and potential impact on your business. We bet your business plans will be much better off if you take a chance on this simple exercise.