4  Completing the Accounting Cycle

Completing the Accounting Cycle

Feature Story Everyone Likes to Win

![]()

When Ted Castle was a hockey coach at the University of Vermont, his players were self-motivated by their desire to win. Hockey was a game you usually either won or lost. But at Rhino Foods, Inc., a bakery-foods company he founded in Burlington, Vermont, he discovered that manufacturing-line workers were not so self-motivated. Ted thought, what if he turned the food-making business into a game, with rules, strategies, and trophies?

In a game, knowing the score is all-important. Ted felt that only if the employees know the score—know exactly how the business is doing daily, weekly, monthly—could he turn food-making into a game. But Rhino is a closely held, family-owned business, and its financial statements and profits were confidential. Ted wondered, should he open Rhino's books to the employees?

A consultant put Ted's concerns in perspective when he said, “Imagine you're playing touch football. You play for an hour or two, and the whole time I'm sitting there with a book, keeping score. All of a sudden I blow the whistle, and I say, ‘OK, that's it. Everybody go home.’ I close my book and walk away. How would you feel?” Ted opened his books and revealed the financial statements to his employees.

The next step was to teach employees the rules and strategies of how to “win” at making food. The first lesson: “Your opponent at Rhino is expenses. You must cut and control expenses.” Ted and his staff distilled those lessons into daily scorecards—production reports and income statements—that keep Rhino's employees up-to-date on the game. At noon each day, Ted posts the previous day's results at the entrance to the production room. Everyone checks whether they made or lost money on what they produced the day before. And it's not just an academic exercise: There's a bonus check for each employee at the end of every four-week “game” that meets profitability guidelines.

Rhino has flourished since the first game. Employment has increased from 20 to 130 people, while both revenues and profits have grown dramatically.

![]()

Scan Learning Objectives

Scan Learning Objectives- Read Feature Story

- Read Preview

- Read text and answer DO IT! p. 171

p. 176 p. 185 p. 187

- Work Comprehensive DO IT! p. 188

- Review Summary of Learning Objectives

- Answer Self-Test Questions

- Complete Assignments

- Go to WileyPLUS for practice and tutorials

Read A Look at IFRS p. 215

Read A Look at IFRS p. 215

Learning Objectives ![]()

After studying this chapter, you should be able to:

[1] Prepare a worksheet.

[2] Explain the process of closing the books.

[3] Describe the content and purpose of a post-closing trial balance.

[4] State the required steps in the accounting cycle.

[5] Explain the approaches to preparing correcting entries.

[6] Identify the sections of a classified balance sheet.

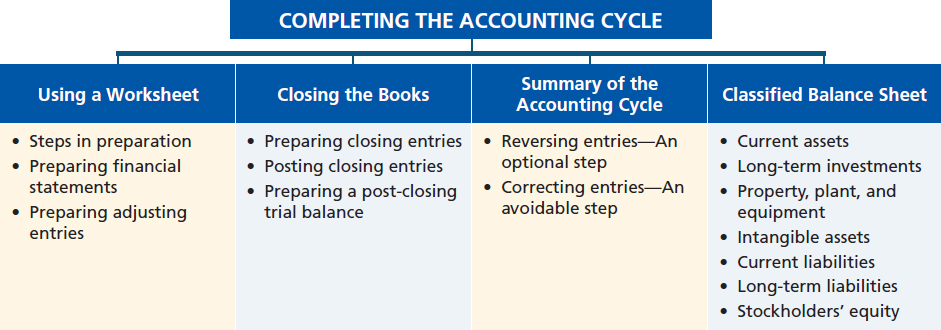

Preview of Chapter 4

![]()

At Rhino Foods, Inc., financial statements help employees understand what is happening in the business. In Chapter 3, we prepared financial statements directly from the adjusted trial balance. However, with so many details involved in the end-of-period accounting procedures, it is easy to make errors. One way to minimize errors in the records and to simplify the end-of-period procedures is to use a worksheet.

In this chapter, we will explain the role of the worksheet in accounting. We also will study the remaining steps in the accounting cycle, especially the closing process, again using Pioneer Advertising Agency Inc. as an example. Then we will consider correcting entries and classified balance sheets. The content and organization of Chapter 4 are as follows.

![]() 1

1

Prepare a worksheet.

Using a Worksheet

A worksheet is a multiple-column form used in the adjustment process and in preparing financial statements. As its name suggests, the worksheet is a working tool. It is not a permanent accounting record. It is neither a journal nor a part of the general ledger. The worksheet is merely a device used in preparing adjusting entries and the financial statements. Companies generally computerize worksheets using an electronic spreadsheet program such as Excel.

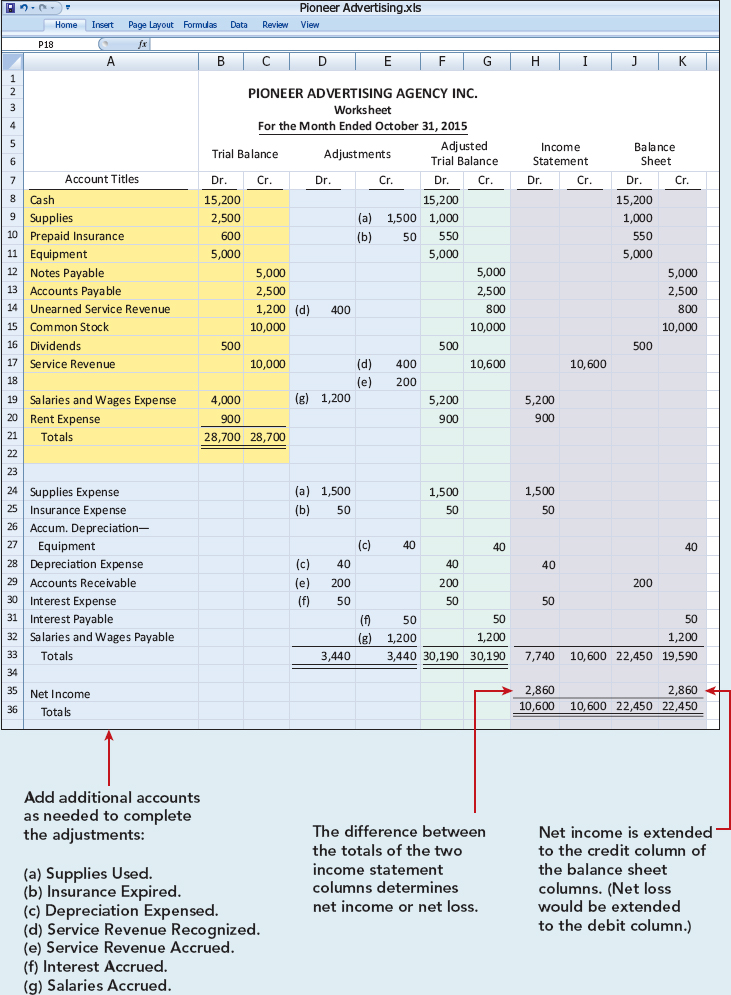

Illustration 4-1 shows the basic form of a worksheet and the five steps for preparing it. Each step is performed in sequence. The use of a worksheet is optional. When a company chooses to use one, it prepares financial statements directly from the worksheet. It enters the adjustments in the worksheet columns and then journalizes and posts the adjustments after it has prepared the financial statements. Thus, worksheets make it possible to provide the financial statements to management and other interested parties at an earlier date.

Illustration 4-1

Form and procedure for a worksheet

Steps in Preparing a Worksheet

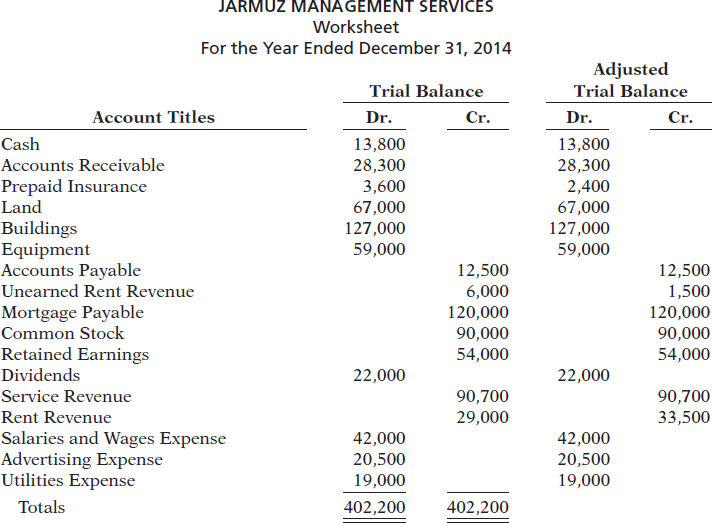

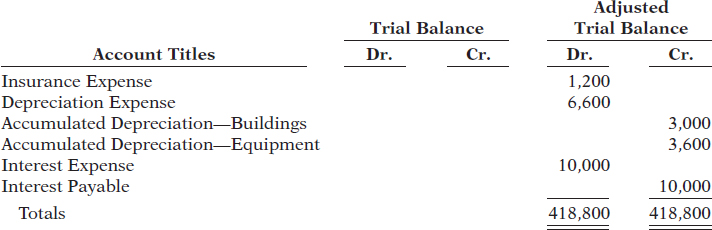

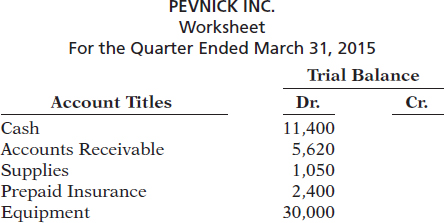

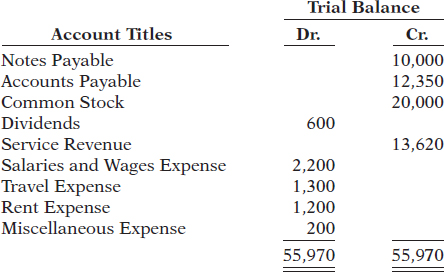

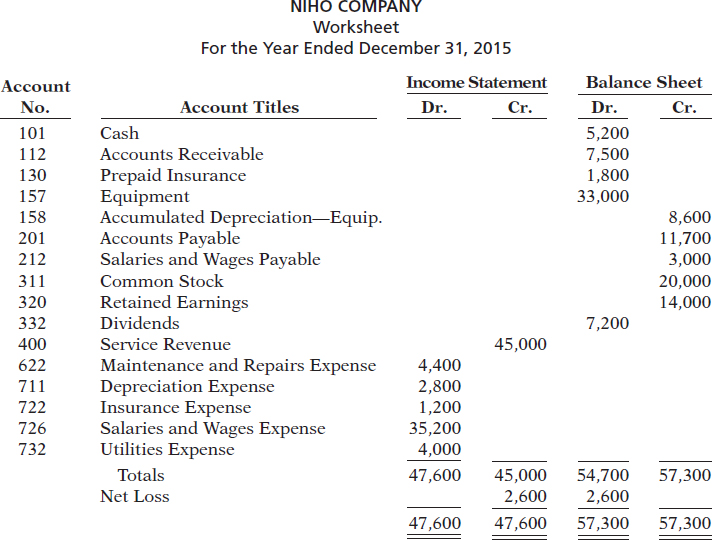

We will use the October 31 trial balance and adjustment data of Pioneer Advertising Agency Inc. from Chapter 3 to illustrate how to prepare a worksheet. We describe each step of the process and demonstrate these steps in Illustration 4-2 (page 168).

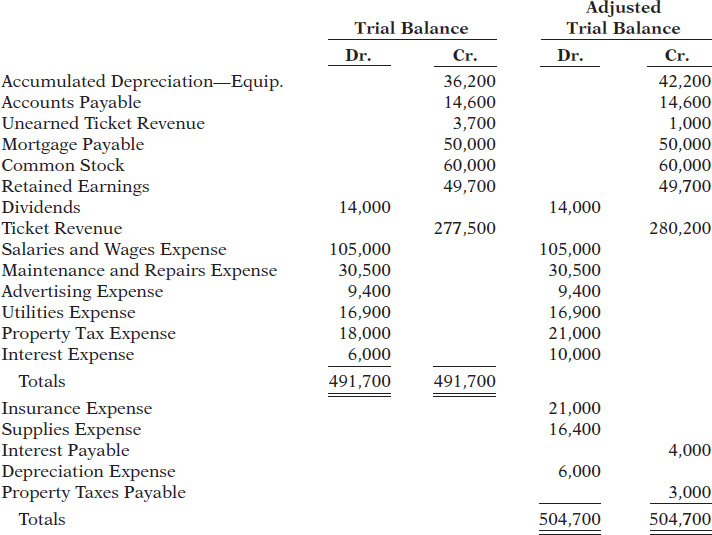

STEP 1. PREPARE A TRIAL BALANCE ON THE WORKSHEET

Enter all ledger accounts with balances in the account titles column. Enter debit and credit amounts from the ledger in the trial balance columns. Illustration 4-2 shows the worksheet trial balance for Pioneer Advertising Agency Inc. This trial balance is the same one that appears in Illustration 2-32 (page 76) and Illustration 3-3 (page 107).

STEP 2. ENTER THE ADJUSTMENTS IN THE ADJUSTMENTS COLUMNS

When using a worksheet, enter all adjustments in the adjustments columns. In entering the adjustments, use applicable trial balance accounts. If additional accounts are needed, insert them on the lines immediately below the trial balance totals. A different letter identifies the debit and credit for each adjusting entry. The term used to describe this process is keying. Companies do not journalize the adjustments until after they complete the worksheet and prepare the financial statements.

The adjustments for Pioneer Advertising Agency Inc. are the same as the adjustments in Illustration 3-23 (page 121). They are keyed in the adjustments columns of the worksheet as follows.

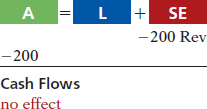

- (a) Pioneer debits an additional account, Supplies Expense, $1,500 for the cost of supplies used, and credits Supplies $1,500.

- (b) Pioneer debits an additional account, Insurance Expense, $50 for the insurance that has expired, and credits Prepaid Insurance $50.

- (c) The company needs two additional depreciation accounts. It debits Depreciation Expense $40 for the month's depreciation, and credits Accumulated Depreciation—Equipment $40.

- (d) Pioneer debits Unearned Service Revenue $400 for services performed, and credits Service Revenue $400.

- (e) Pioneer debits an additional account, Accounts Receivable, $200 for services performed but not billed, and credits Service Revenue $200.

- (f) The company needs two additional accounts relating to interest. It debits Interest Expense $50 for accrued interest, and credits Interest Payable $50.

- (g) Pioneer debits Salaries and Wages Expense $1,200 for accrued salaries, and credits an additional account, Salaries and Wages Payable, $1,200.

After Pioneer has entered all the adjustments, the adjustments columns are totaled to prove their equality. (See the yellow-shaded area in Illustration 4-2.)

STEP 3. ENTER ADJUSTED BALANCES IN THE ADJUSTED TRIAL BALANCE COLUMNS

Pioneer determines the adjusted balance of an account by combining the amounts entered in the first four columns of the worksheet for each account. For example, the Prepaid Insurance account in the trial balance columns has a $600 debit balance and a $50 credit in the adjustments columns. The result is a $550 debit balance recorded in the adjusted trial balance columns. For each account, the amount in the adjusted trial balance columns is the balance that will appear in the ledger after journalizing and posting the adjusting entries. The balances in these columns are the same as those in the adjusted trial balance in Illustration 3-25 (page 123).

After Pioneer has entered all account balances in the adjusted trial balance columns, the columns are totaled to prove their equality. (See the blue-shaded area in Illustration 4-2.) If the column totals do not agree, the financial statement columns will not balance and the financial statements will be incorrect.

STEP 4. EXTEND ADJUSTED TRIAL BALANCE AMOUNTS TO APPROPRIATE FINANCIAL STATEMENT COLUMNS

The fourth step is to extend adjusted trial balance amounts to the income statement and balance sheet columns of the worksheet. Pioneer enters balance sheet accounts in the appropriate balance sheet debit and credit columns. For instance, it enters Cash in the balance sheet debit column, and Notes Payable in the balance sheet credit column. Pioneer extends Accumulated Depreciation—Equipment to the balance sheet credit column. The reason is that accumulated depreciation is a contra asset account with a credit balance.

Helpful Hint

Every adjusted trial balance amount must be extended to one of the four statement columns.

Pioneer extends the balances in Common Stock and Retained Earnings, if any, to the balance sheet credit column. In addition, it extends the balance in Dividends to the balance sheet debit column because it is a stockholders' equity account with a debit balance.

The company enters the expense and revenue accounts such as Salaries and Wages Expense and Service Revenue in the appropriate income statement columns. (See the green-shaded area in Illustration 4-2.)

STEP 5. TOTAL THE STATEMENT COLUMNS, COMPUTE THE NET INCOME (OR NET LOSS), AND COMPLETE THE WORKSHEET

The company now must total each of the financial statement columns. The net income or net loss for the period is the difference between the totals of the two income statement columns. If total credits exceed total debits, the result is net income. In such a case, as shown in Illustration 4-2, the company inserts the words “Net Income” in the account titles space. It then enters the amount in the income statement debit column and the balance sheet credit column. The debit amount balances the income statement columns; the credit amount balances the balance sheet columns. In addition, the credit in the balance sheet column indicates the increase in stockholders' equity resulting from net income.

What if total debits exceed total credits in the income statement columns? In that case, the company has a net loss. It enters the amount of the net loss in the income statement credit column and the balance sheet debit column.

After entering the net income or net loss, the company determines new column totals. The totals shown in the debit and credit income statement columns will match. So will the totals shown in the debit and credit balance sheet columns. If either the income statement columns or the balance sheet columns are not equal after the net income or net loss has been entered, there is an error in the worksheet. (See the grey-shaded area in Illustration 4-2.)

Preparing Financial Statements from a Worksheet

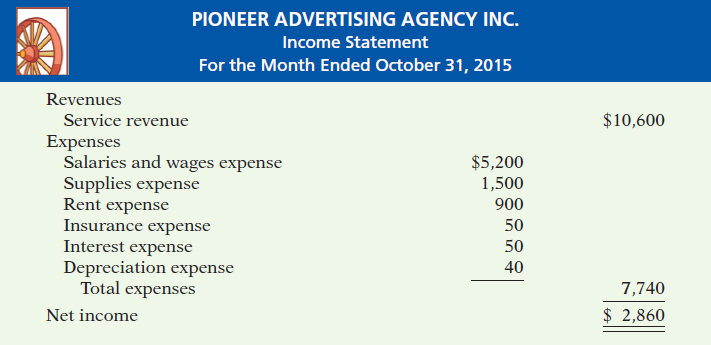

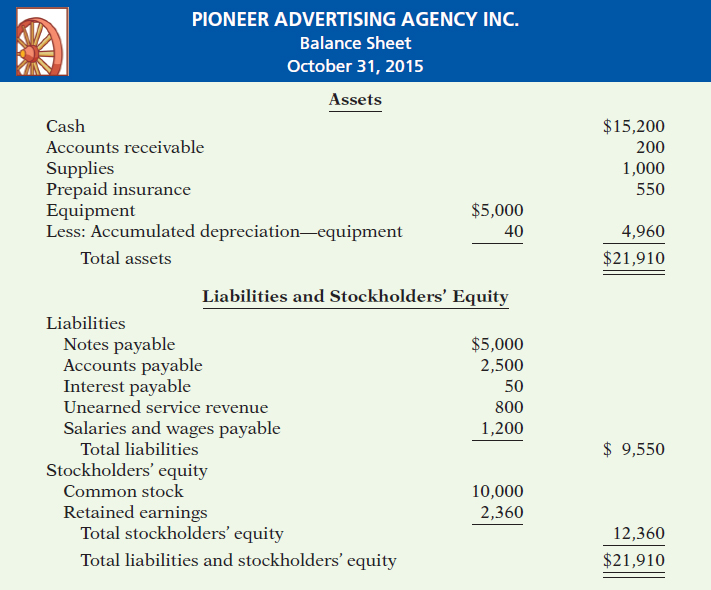

After a company has completed a worksheet, it has at hand all the data required for preparation of financial statements. The income statement is prepared from the income statement columns. The balance sheet and retained earnings statement are prepared from the balance sheet columns. Illustration 4-3 (page 170) shows the financial statements prepared from Pioneer's worksheet. At this point, the company has not journalized or posted adjusting entries. Therefore, ledger balances for some accounts are not the same as the financial statement amounts.

Illustration 4-3

Financial statements from a worksheet

The amount shown for common stock on the worksheet does not change from the beginning to the end of the period unless the company issues additional stock during the period. Because there was no balance in Pioneer's retained earnings, the account is not listed on the worksheet. Only after dividends and net income (or loss) are posted to retained earnings does this account have a balance at the end of the first year of the business.

Using a worksheet, companies can prepare financial statements before they journalize and post adjusting entries. However, the completed worksheet is not a substitute for formal financial statements. The format of the data in the financial statement columns of the worksheet is not the same as the format of the financial statements. A worksheet is essentially a working tool of the accountant; companies do not distribute it to management and other parties.

Preparing Adjusting Entries from a Worksheet

A worksheet is not a journal, and it cannot be used as a basis for posting to ledger accounts. To adjust the accounts, the company must journalize the adjustments and post them to the ledger. The adjusting entries are prepared from the adjustments columns of the worksheet. The reference letters in the adjustments columns and the explanations of the adjustments at the bottom of the worksheet help identify the adjusting entries. The journalizing and posting of adjusting entries follow the preparation of financial statements when a worksheet is used. The adjusting entries on October 31 for Pioneer Advertising Agency Inc. are the same as those shown in Illustration 3-23 (page 121).

Helpful Hint

Note that writing the explanation of the adjustment at the bottom of the worksheet is not required.

> DO IT!

Worksheet

Susan Elbe is preparing a worksheet. Explain to Susan how she should extend the following adjusted trial balance accounts to the financial statement columns of the worksheet.

| Cash | Dividends |

| Accumulated Depreciation—Equipment | Service Revenue |

| Accounts Payable | Salaries and Wages Expense |

Action Plan

![]() Balance sheet: Extend assets to debit column. Extend liabilities to credit column. Extend contra assets to credit column. Extend Dividends account to debit column.

Balance sheet: Extend assets to debit column. Extend liabilities to credit column. Extend contra assets to credit column. Extend Dividends account to debit column.

![]() Income statement: Extend expenses to debit column. Extend revenues to credit column.

Income statement: Extend expenses to debit column. Extend revenues to credit column.

Solution

Income statement debit column—Salaries and Wages Expense

Income statement credit column—Service Revenue

Balance sheet debit column—Cash; Dividends

Balance sheet credit column—Accumulated Depreciation—Equipment; Accounts Payable

Related exercise material: BE4-1, BE4-2, BE4-3, E4-1, E4-2, E4-5, E4-6, and DO IT! 4-1.

![]()

![]() 2

2

Explain the process of closing the books.

Closing the Books

At the end of the accounting period, the company makes the accounts ready for the next period. This is called closing the books. In closing the books, the company distinguishes between temporary and permanent accounts.

Temporary accounts relate only to a given accounting period. They include all income statement accounts and the Dividends account. The company closes all temporary accounts at the end of the period.

In contrast, permanent accounts relate to one or more future accounting periods. They consist of all balance sheet accounts, including stockholders' equity accounts. Permanent accounts are not closed from period to period. Instead, the company carries forward the balances of permanent accounts into the next accounting period. Illustration 4-4 identifies the accounts in each category.

Illustration 4-4

Temporary versus permanent accounts

Alternative Terminology

Temporary accounts are sometimes called nominal accounts, and permanent accounts are sometimes called real accounts.

Preparing Closing Entries

At the end of the accounting period, the company transfers temporary account balances to the permanent stockholders' equity account, Retained Earnings, by means of closing entries.

Closing entries formally recognize in the ledger the transfer of net income (or net loss) and Dividends to Retained Earnings. The retained earnings statement shows the results of these entries. Closing entries also produce a zero balance in each temporary account. The temporary accounts are then ready to accumulate data in the next accounting period separate from the data of prior periods. Permanent accounts are not closed.

Journalizing and posting closing entries is a required step in the accounting cycle. (See Illustration 4-11 on page 179.) The company performs this step after it has prepared financial statements. In contrast to the steps in the cycle that you have already studied, companies generally journalize and post closing entries only at the end of the annual accounting period. Thus, all temporary accounts will contain data for the entire year.

In preparing closing entries, companies could close each income statement account directly to Retained Earnings. However, to do so would result in excessive detail in the permanent Retained Earnings account. Instead, companies close the revenue and expense accounts to another temporary account, Income Summary, and they transfer the resulting net income or net loss from this account to Retained Earnings.

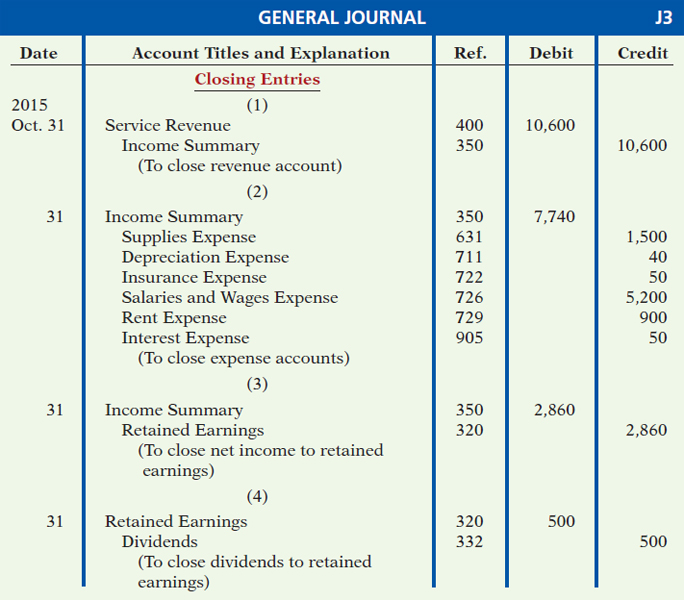

Companies record closing entries in the general journal. A center caption, Closing Entries, inserted in the journal between the last adjusting entry and the first closing entry, identifies these entries. Then the company posts the closing entries to the ledger accounts.

Companies generally prepare closing entries directly from the adjusted balances in the ledger. They could prepare separate closing entries for each nominal account, but the following four entries accomplish the desired result more efficiently:

- Debit each revenue account for its balance, and credit Income Summary for total revenues.

- Debit Income Summary for total expenses, and credit each expense account for its balance.

- Debit Income Summary and credit Retained Earnings for the amount of net income.

- Debit Retained Earnings for the balance in the Dividends account, and credit Dividends for the same amount.

Helpful Hint

The Dividends account is closed directly to Retained Earnings and not to Income Summary because dividends are not an expense.

Illustration 4-5 presents a diagram of the closing process. In it, the boxed numbers refer to the four entries required in the closing process.

Illustration 4-5

Diagram of closing process—corporation

If there were a net loss (because expenses exceeded revenues), entry 3 in Illustration 4-5 would be reversed: there would be a credit to Income Summary and a debit to Retained Earnings.

CLOSING ENTRIES ILLUSTRATED

In practice, companies generally prepare closing entries only at the end of the annual accounting period. However, to illustrate the journalizing and posting of closing entries, we will assume that Pioneer Advertising Agency Inc. closes its books monthly. Illustration 4-6 (page 174) shows the closing entries at October 31. (The numbers in parentheses before each entry correspond to the four entries diagrammed in Illustration 4-5.)

Illustration 4-6

Closing entries journalized

Note that the amounts for Income Summary in entries (1) and (2) are the totals of the income statement credit and debit columns, respectively, in the worksheet.

A couple of cautions in preparing closing entries: (1) Avoid unintentionally doubling the revenue and expense balances rather than zeroing them. (2) Do not close Dividends through the Income Summary account. Dividends are not an expense, and they are not a factor in determining net income.

Posting Closing Entries

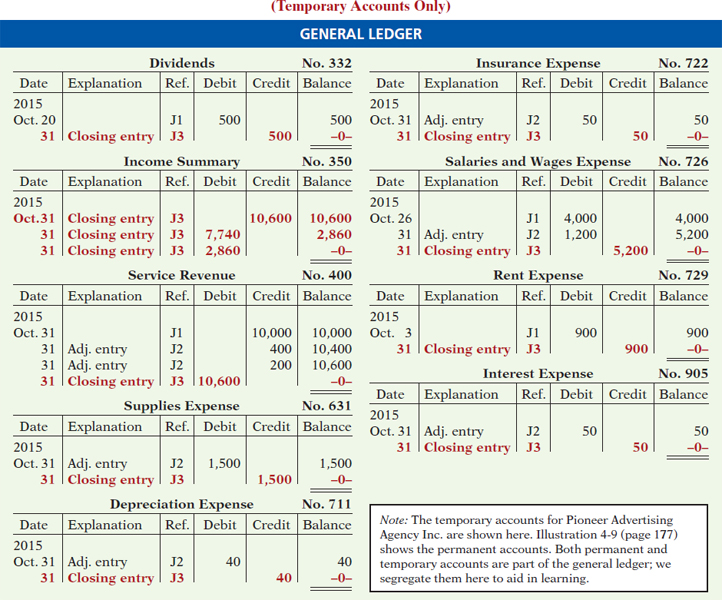

Illustration 4-7 shows the posting of the closing entries and the underlining (ruling) of the accounts. Note that all temporary accounts have zero balances after posting the closing entries. In addition, you should realize that the balance in Retained Earnings represents the accumulated undistributed earnings of the corporation at the end of the accounting period. This balance is shown on the balance sheet and is the ending amount reported on the retained earnings statement, as shown in Illustration 4-3 on page 170. Pioneer uses the Income Summary account only in closing. It does not journalize and post entries to this account during the year.

Helpful Hint

The balance in Income Summary before it is closed must equal the net income or net loss for the period.

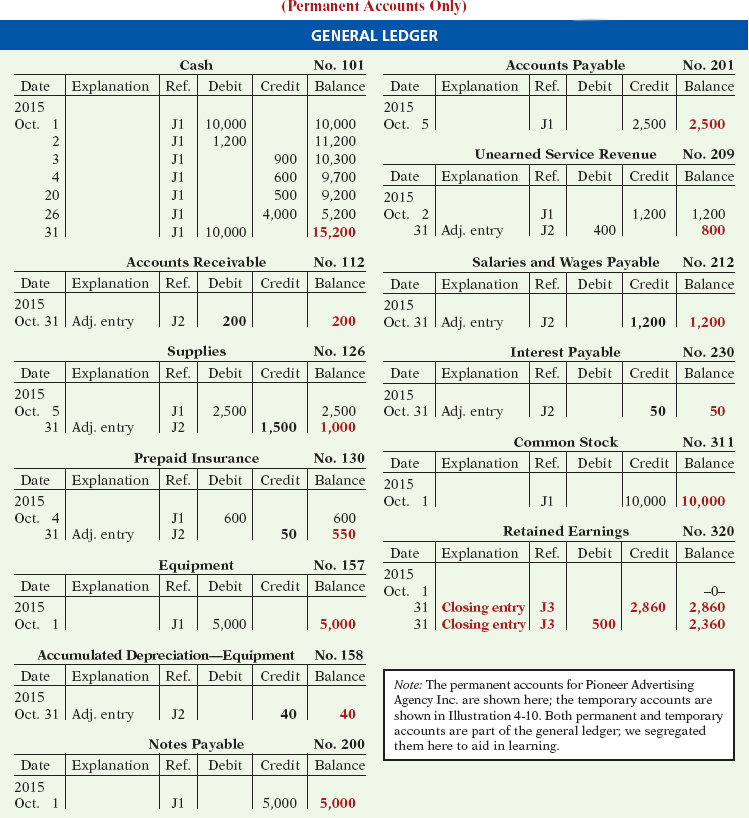

As part of the closing process, Pioneer totals, balances, and double-underlines its temporary accounts—revenues, expenses, and Dividends, as shown in T-account form in Illustration 4-7. It does not close its permanent accounts—assets, liabilities, and stockholders' equity (Common Stock and Retained Earnings). Instead, Pioneer draws a single underline beneath the current-period entries for the permanent accounts. The account balance is then entered below the single underline and is carried forward to the next period. (For example, see Retained Earnings.)

Illustration 4-7

Posting of closing entries

ACCOUNTING ACROSS THE ORGANIZATION

Cisco Performs the Virtual Close

Technology has dramatically shortened the closing process. Recent surveys have reported that the average company now takes only six to seven days to close, rather than 20 days. But a few companies do much better. Cisco Systems can perform a “virtual close”—closing within 24 hours on any day in the quarter. The same is true at Lockheed Martin Corp., which improved its closing time by 85% in just the last few years. Not very long ago, it took 14 to 16 days. Managers at these companies emphasize that this increased speed has not reduced the accuracy and completeness of the data.

This is not just showing off. Knowing exactly where you are financially all of the time allows the company to respond faster than competitors. It also means that the hundreds of people who used to spend 10 to 20 days a quarter tracking transactions can now be more usefully employed on things such as mining data for business intelligence to find new business opportunities.

Source: “Reporting Practices: Few Do It All,” Financial Executive (November 2003), p. 11.

Who else benefits from a shorter closing process? (See page 215.)

Who else benefits from a shorter closing process? (See page 215.)

Closing Entries

The worksheet for Hancock Company shows the following in the financial statement columns:

Dividends $15,000

Common stock $42,000

Net income $18,000

Prepare the closing entries at December 31 that affect stockholders' equity.

Action Plan

![]() Close Income Summary to Retained Earnings.

Close Income Summary to Retained Earnings.

![]() Close Dividends to Retained Earnings.

Close Dividends to Retained Earnings.

Solution

Related exercise material: BE4-4, BE4-5, BE4-6, E4-4, E4-7, E4-8, E4-11, and DO IT! 4-2.

![]()

![]() 3

3

Describe the content and purpose of a post-closing trial balance.

Preparing a Post-Closing Trial Balance

After Pioneer has journalized and posted all closing entries, it prepares another trial balance, called a post-closing trial balance, from the ledger. The post-closing trial balance lists permanent accounts and their balances after the journalizing and posting of closing entries. The purpose of the post-closing trial balance is to prove the equality of the permanent account balances carried forward into the next accounting period. Since all temporary accounts will have zero balances, the post-closing trial balance will contain only permanent—balance sheet—accounts.

Illustration 4-8 shows the post-closing trial balance for Pioneer Advertising Agency Inc.

Illustration 4-8

Post-closing trial balance

Pioneer prepares the post-closing trial balance from the permanent accounts in the ledger. Illustration 4-9 shows the permanent accounts in Pioneer's general ledger.

Illustration 4-9

General ledger, permanent accounts

A post-closing trial balance provides evidence that the company has properly journalized and posted the closing entries. It also shows that the accounting equation is in balance at the end of the accounting period. However, like the trial balance, it does not prove that Pioneer has recorded all transactions or that the ledger is correct. For example, the post-closing trial balance still will balance even if a transaction is not journalized and posted or if a transaction is journalized and posted twice.

The remaining accounts in the general ledger are temporary accounts, shown in Illustration 4-10. After Pioneer correctly posts the closing entries, each temporary account has a zero balance. These accounts are double-underlined to finalize the closing process.

Illustration 4-10

General ledger, temporary accounts

![]() 4

4

State the required steps in the accounting cycle.

Summary of the Accounting Cycle

Illustration 4-11 summarizes the steps in the accounting cycle. You can see that the cycle begins with the analysis of business transactions and ends with the preparation of a post-closing trial balance.

Illustration 4-11

Steps in the accounting cycle

Steps 1–3 may occur daily during the accounting period. Companies perform Steps 4–7 on a periodic basis, such as monthly, quarterly, or annually. Steps 8 and 9—closing entries and a post-closing trial balance—usually take place only at the end of a company's annual accounting period.

There are also two optional steps in the accounting cycle. As you have seen, companies may use a worksheet in preparing adjusting entries and financial statements. In addition, they may use reversing entries, as explained below.

Reversing Entries—An Optional Step

Some accountants prefer to reverse certain adjusting entries by making a reversing entry at the beginning of the next accounting period. A reversing entry is the exact opposite of the adjusting entry made in the previous period. Use of reversing entries is an optional bookkeeping procedure; it is not a required step in the accounting cycle. Accordingly, we have chosen to cover this topic in Appendix 4A at the end of this chapter.

![]() 5

5

Explain the approaches to preparing correcting entries.

Correcting Entries—An Avoidable Step

Unfortunately, errors may occur in the recording process. Companies should correct errors, as soon as they discover them, by journalizing and posting correcting entries. If the accounting records are free of errors, no correcting entries are needed.

You should recognize several differences between correcting entries and adjusting entries. First, adjusting entries are an integral part of the accounting cycle. Correcting entries, on the other hand, are unnecessary if the records are error-free. Second, companies journalize and post adjustments only at the end of an accounting period. In contrast, companies make correcting entries whenever they discover an error. Finally, adjusting entries always affect at least one balance sheet account and one income statement account. In contrast, correcting entries may involve any combination of accounts in need of correction. Correcting entries must be posted before closing entries.

![]() Ethics Note

Ethics Note

When companies find errors in previously released income statements, they restate those numbers. Perhaps because of the increased scrutiny caused by Sarbanes-Oxley, in a recent year companies filed a record 1,195 restatements.

To determine the correcting entry, it is useful to compare the incorrect entry with the correct entry. Doing so helps identify the accounts and amounts that should—and should not—be corrected. After comparison, the accountant makes an entry to correct the accounts. The following two cases for Mercato Co. illustrate this approach.

CASE 1

On May 10, Mercato Co. journalized and posted a $50 cash collection on account from a customer as a debit to Cash $50 and a credit to Service Revenue $50. The company discovered the error on May 20, when the customer paid the remaining balance in full.

Illustration 4-12

Comparison of entries

Comparison of the incorrect entry with the correct entry reveals that the debit to Cash $50 is correct. However, the $50 credit to Service Revenue should have been credited to Accounts Receivable. As a result, both Service Revenue and Accounts Receivable are overstated in the ledger. Mercato makes the following correcting entry.

Illustration 4-13

Correcting entry

CASE 2

On May 18, Mercato purchased on account equipment costing $450. The transaction was journalized and posted as a debit to Equipment $45 and a credit to Accounts Payable $45. The error was discovered on June 3, when Mercato received the monthly statement for May from the creditor.

Illustration 4-14

Comparison of entries

Comparison of the two entries shows that two accounts are incorrect. Equipment is understated $405, and Accounts Payable is understated $405. Mercato makes the following correcting entry.

Illustration 4-15

Correcting entry

Instead of preparing a correcting entry, it is possible to reverse the incorrect entry and then prepare the correct entry. This approach will result in more entries and postings than a correcting entry, but it will accomplish the desired result.

ACCOUNTING ACROSS THE ORGANIZATION

Yale Express Loses Some Transportation Bills

Yale Express, a short-haul trucking firm, turned over much of its cargo to local truckers to complete deliveries. Yale collected the entire delivery charge. When billed by the local trucker, Yale sent payment for the final phase to the local trucker. Yale used a cutoff period of 20 days into the next accounting period in making its adjusting entries for accrued liabilities. That is, it waited 20 days to receive the local truckers' bills to determine the amount of the unpaid but incurred delivery charges as of the balance sheet date.

On the other hand, Republic Carloading, a nationwide, long-distance freight forwarder, frequently did not receive transportation bills from truckers to whom it passed on cargo until months after the year-end. In making its year-end adjusting entries, Republic waited for months in order to include all of these outstanding transportation bills.

When Yale Express merged with Republic Carloading, Yale's vice president employed the 20-day cutoff procedure for both firms. As a result, millions of dollars of Republic's accrued transportation bills went unrecorded. When the company detected the error and made correcting entries, these and other errors changed a reported profit of $1.14 million into a loss of $1.88 million!

What might Yale Express's vice president have done to produce more accurate financial statements without waiting months for Republic's outstanding transportation bills? (See page 215.)

![]() 6

6

Identify the sections of a classified balance sheet.

The Classified Balance Sheet

The balance sheet presents a snapshot of a company's financial position at a point in time. To improve users' understanding of a company's financial position, companies often use a classified balance sheet. A classified balance sheet groups together similar assets and similar liabilities, using a number of standard classifications and sections. This is useful because items within a group have similar economic characteristics. A classified balance sheet generally contains the standard classifications listed in Illustration 4-16.

Illustration 4-16

Standard balance sheet classifications

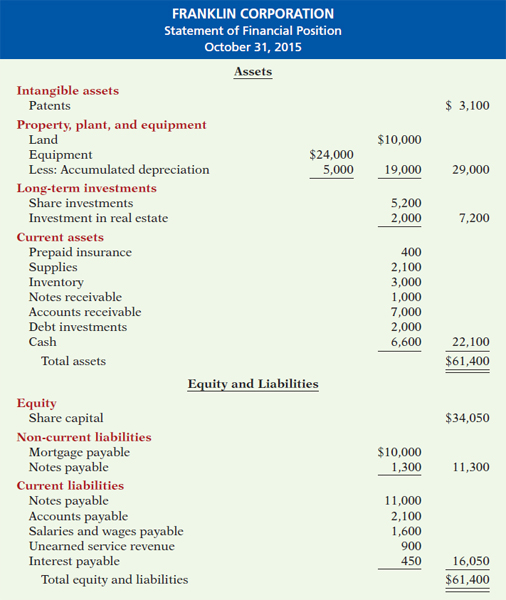

These groupings help financial statement readers determine such things as (1) whether the company has enough assets to pay its debts as they come due, and (2) the claims of short- and long-term creditors on the company's total assets. Many of these groupings can be seen in the balance sheet of Franklin Corporation shown in Illustration 4-17 below. In the sections that follow, we explain each of these groupings.

Illustration 4-17

Classified balance sheet

Helpful Hint

Recall that the basic accounting equation is Assets = Liabilities + Stockholders' Equity.

Current Assets

Current assets are assets that a company expects to convert to cash or use up within one year or its operating cycle, whichever is longer. In Illustration 4-17, Franklin Corporation had current assets of $22,100. For most businesses, the cutoff for classification as current assets is one year from the balance sheet date. For example, accounts receivable are current assets because the company will collect them and convert them to cash within one year. Supplies is a current asset because the company expects to use them up in operations within one year.

Some companies use a period longer than one year to classify assets and liabilities as current because they have an operating cycle longer than one year. The operating cycle of a company is the average time that it takes to purchase inventory, sell it on account, and then collect cash from customers. For most businesses, this cycle takes less than a year, so they use a one-year cutoff. But, for some businesses, such as vineyards or airplane manufacturers, this period may be longer than a year. Except where noted, we will assume that companies use one year to determine whether an asset or liability is current or long-term.

Common types of current assets are (1) cash, (2) investments (such as short-term U.S. government securities), (3) receivables (notes receivable, accounts receivable, and interest receivable), (4) inventories, and (5) prepaid expenses (supplies and insurance). On the balance sheet, companies usually list these items in the order in which they expect to convert them into cash.

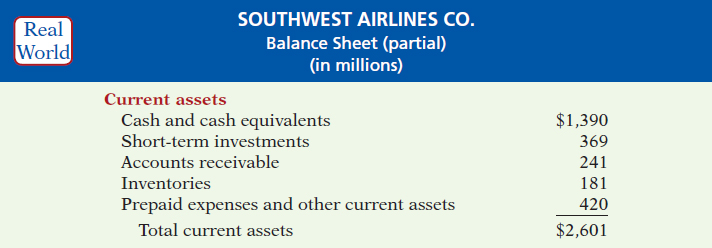

Illustration 4-18 presents the current assets of Southwest Airlines Co.

Illustration 4-18

Current assets section

As explained later in the chapter, a company's current assets are important in assessing its short-term debt-paying ability.

Long-Term Investments

Long-term investments are generally (1) investments in stocks and bonds of other companies that are normally held for many years, (2) long-term assets such as land or buildings that a company is not currently using in its operating activities, and (3) long-term notes receivable. In Illustration 4-17, Franklin Corporation reported total long-term investments of $7,200 on its balance sheet.

Alternative Terminology

Long-term investments are often referred to simply as investments.

Yahoo! Inc. reported long-term investments in its balance sheet as shown in Illustration 4-19.

Illustration 4-19

Long-term investments section

Property, plant, and equipment is sometimes called fixed assets or plant assets.

Property, Plant, and Equipment

Property, plant, and equipment are assets with relatively long useful lives that a company is currently using in operating the business. This category includes land, buildings, machinery and equipment, delivery equipment, and furniture. In Illustration 4-17, Franklin Corporation reported property, plant, and equipment of $29,000.

![]() International Note

International Note

Recently, China adopted International Financial Reporting Standards (IFRS). This was done in an effort to reduce fraud and increase investor confidence in financial reports. Under these standards, many items, such as property, plant, and equipment, may be reported at current fair values rather than historical cost.

Depreciation is the practice of allocating the cost of assets to a number of years. Companies do this by systematically assigning a portion of an asset's cost as an expense each year (rather than expensing the full purchase price in the year of purchase). The assets that the company depreciates are reported on the balance sheet at cost less accumulated depreciation. The accumulated depreciation account shows the total amount of depreciation that the company has expensed thus far in the asset's life. In Illustration 4-17, Franklin Corporation reported accumulated depreciation of $5,000.

Illustration 4-20 presents the property, plant, and equipment of Cooper Tire & Rubber Company.

Illustration 4-20

Property, plant, and equipment section

Intangible Assets

Many companies have long-lived assets that do not have physical substance yet often are very valuable. We call these assets intangible assets. One significant intangible asset is goodwill. Others include patents, copyrights, and trademarks or trade names that give the company exclusive right of use for a specified period of time. In Illustration 4-17, Franklin Corporation reported intangible assets of $3,100.

Helpful Hint

Sometimes intangible assets are reported under a broader heading called “Other assets.”

Illustration 4-21 shows the intangible assets of media giant Time Warner, Inc.

Illustration 4-21

Intangible assets section

PEOPLE, PLANET, AND PROFIT INSIGHT ![]()

Regaining Goodwill

After falling to unforeseen lows amidst scandals, recalls, and economic crises, the American public's positive perception of the reputation of corporate America is on the rise. Overall corporate reputation is experiencing rehabilitation as the American public gives high marks overall to corporate America, specific industries, and the largest number of individual companies in a dozen years. This is according to the findings of the 2011 Harris Interactive RQ Study, which measures the reputations of the 60 most visible companies in the United States.

The survey focuses on six reputational dimensions that influence reputation and consumer behavior. Four of these dimensions, along with the five corporations that ranked highest within each, are as follows.

- Social Responsibility: (1) Whole Foods Market, (2) Johnson & Johnson, (3) Google, (4) The Walt Disney Company, (5) Procter & Gamble Co.

- Emotional Appeal: (1) Johnson & Johnson, (2) Amazon.com, (3) UPS, (4) General Mills, (5) Kraft Foods

- Financial Performance: (1) Google, (2) Berkshire Hathaway, (3) Apple, (4) Intel, (5) The Walt Disney Company

- Products and Services: (1) Intel Corporation, (2) 3M Company, (3) Johnson & Johnson, (4) Google, (5) Procter & Gamble Co.

Source: www.harrisinteractive.com.

Name two industries today which are probably rated low on the reputational characteristics of “being trusted” and “having high ethical standards.” (See page 215.)

> DO IT!

Assets Section of Classified Balance Sheet

Baxter Hoffman recently received the following information related to Hoffman Company's December 31, 2015, balance sheet.

Prepare the assets section of Hoffman Company's classified balance sheet.

Action Plan

![]() Present current assets first. Current assets are cash and other resources that the company expects to convert to cash or use up within one year.

Present current assets first. Current assets are cash and other resources that the company expects to convert to cash or use up within one year.

![]() Present current assets in the order in which the company expects to convert them into cash.

Present current assets in the order in which the company expects to convert them into cash.

![]() Subtract accumulated depreciation—equipment from equipment to determine the book value of equipment.

Subtract accumulated depreciation—equipment from equipment to determine the book value of equipment.

Solution

Related exercise material: BE4-10 and DO IT! 4-3.

![]()

![]() Ethics Note

Ethics Note

A company that has more current assets than current liabilities can increase the ratio of current assets to current liabilities by using cash to pay off some current liabilities. This gives the appearance of being more liquid. Do you think this move is ethical?

Current Liabilities

In the liabilities and stockholders' equity section of the balance sheet, the first grouping is current liabilities. Current liabilities are obligations that the company is to pay within the coming year or its operating cycle, whichever is longer. Common examples are accounts payable, salaries and wages payable, notes payable, interest payable, and income taxes payable. Also included as current liabilities are current maturities of long-term obligations—payments to be made within the next year on long-term obligations. In Illustration 4-17, Franklin Corporation reported five different types of current liabilities, for a total of $16,050.

Illustration 4-22 shows the current liabilities section adapted from the balance sheet of Marcus Corporation.

Illustration 4-22

Current liabilities section

Users of financial statements look closely at the relationship between current assets and current liabilities. This relationship is important in evaluating a company's liquidity—its ability to pay obligations expected to be due within the next year. When current assets exceed current liabilities, the likelihood for paying the liabilities is favorable. When the reverse is true, short-term creditors may not be paid, and the company may ultimately be forced into bankruptcy.

ACCOUNTING ACROSS THE ORGANIZATION

Can a Company Be Too Liquid?

There actually is a point where a company can be too liquid—that is, it can have too much working capital (current assets less current liabilities). While it is important to be liquid enough to be able to pay short-term bills as they come due, a company does not want to tie up its cash in extra inventory or receivables that are not earning the company money.

By one estimate from the REL Consultancy Group, the thousand largest U.S. companies have on their books cumulative excess working capital of $764 billion. Based on this figure, companies could have reduced debt by 36% or increased net income by 9%. Given that managers throughout a company are interested in improving profitability, it is clear that they should have an eye toward managing working capital. They need to aim for a “Goldilocks solution”—not too much, not too little, but just right.

Source: K. Richardson, “Companies Fall Behind in Cash Management,” Wall Street Journal (June 19, 2007).

What can various company managers do to ensure that working capital is managed efficiently to maximize net income? (See page 215.)

Long-Term Liabilities

Long-term liabilities are obligations that a company expects to pay after one year. Liabilities in this category include bonds payable, mortgages payable, long-term notes payable, lease liabilities, and pension liabilities. Many companies report long-term debt maturing after one year as a single amount in the balance sheet and show the details of the debt in notes that accompany the financial statements. Others list the various types of long-term liabilities. In Illustration 4-17, Franklin Corporation reported long-term liabilities of $11,300.

Illustration 4-23 shows the long-term liabilities that The Procter & Gamble Company reported in its balance sheet.

Illustration 4-23

Long-term liabilities section

Stockholders' (Owners') Equity

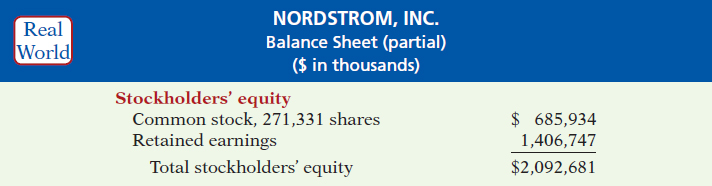

The content of the owners' equity section varies with the form of business organization. In a proprietorship, there is one capital account. In a partnership, there is a capital account for each partner. Corporations divide owners' equity into two accounts—Common Stock (sometimes referred to as Capital Stock) and Retained Earnings. Corporations record stockholders' investments in the company by debiting an asset account and crediting the Common Stock account. They record in the Retained Earnings account income retained for use in the business. Corporations combine the Common Stock and Retained Earnings accounts and report them on the balance sheet as stockholders' equity. (We'll learn more about these corporation accounts in later chapters.) Nordstrom, Inc. recently reported its stockholders' equity section as follows.

Alternative Terminology

Common stock is sometimes called capital stock.

Illustration 4-24

Stockholders' equity section

> DO IT!

Balance Sheet Classifications

The following accounts were taken from the financial statements of Callahan Company.

| ________ Salaries and wages payable | ________ Stock investments (long-term) |

| ________ Service revenue | ________ Equipment |

| ________ Interest payable | ________ Accumulated depreciation—equipment |

| ________ Goodwill | |

| ________ Debt investments (short-term) | ________ Depreciation expense |

| ________ Mortgage payable (due in 3 years) | ________ Common stock |

| ________ Unearned service revenue |

Match each of the accounts to its proper balance sheet classification, shown below. If the item would not appear on a balance sheet, use “NA.”

| Current assets (CA) | Current liabilities (CL) |

| Long-term investments (LTI) | Long-term liabilities (LTL) |

| Property, plant, and equipment (PPE) | Stockholders' equity (SE) |

| Intangible assets (IA) |

Action Plan

![]() Analyze whether each financial statement item is an asset, liability, or stockholders' equity.

Analyze whether each financial statement item is an asset, liability, or stockholders' equity.

![]() Determine if asset and liability items are short-term or long-term.

Determine if asset and liability items are short-term or long-term.

Solution

Related exercise material: BE4-11, E4-9, E4-14, E4-15, E4-16, E4-17, and DO IT! 4-4.

![]()

> Comprehensive DO IT!

At the end of its first month of operations, Watson Answering Service Inc. has the following unadjusted trial balance.

Action Plan

![]() In completing the worksheet, be sure to (a) key the adjustments; (b) start at the top of the adjusted trial balance columns and extend adjusted balances to the correct statement columns; and (c) enter net income (or net loss) in the proper columns.

In completing the worksheet, be sure to (a) key the adjustments; (b) start at the top of the adjusted trial balance columns and extend adjusted balances to the correct statement columns; and (c) enter net income (or net loss) in the proper columns.

![]() In preparing a classified balance sheet, know the contents of each of the sections.

In preparing a classified balance sheet, know the contents of each of the sections.

![]() In journalizing closing entries, remember that there are only four entries and that Dividends are closed to Retained Earnings.

In journalizing closing entries, remember that there are only four entries and that Dividends are closed to Retained Earnings.

- Insurance expires at the rate of $200 per month.

- $1,000 of supplies are on hand at August 31.

- Monthly depreciation on the equipment is $900.

- Interest of $500 on the notes payable has accrued during August.

Instructions

(a) Prepare a worksheet.

(b) Prepare a classified balance sheet assuming $35,000 of the notes payable are long-term.

(c) Journalize the closing entries.

Solution to Comprehensive DO IT!

![]()

SUMMARY OF LEARNING OBJECTIVES

1 Prepare a worksheet. The steps in preparing a worksheet are as follows. (a) Prepare a trial balance on the worksheet. (b) Enter the adjustments in the adjustments columns. (c) Enter adjusted balances in the adjusted trial balance columns. (d) Extend adjusted trial balance amounts to appropriate financial statement columns. (e) Total the statement columns, compute net income (or net loss), and complete the worksheet.

2 Explain the process of closing the books. Closing the books occurs at the end of an accounting period. The process is to journalize and post closing entries and then underline and balance all accounts. In closing the books, companies make separate entries to close revenues and expenses to Income Summary, Income Summary to Retained Earnings, and Dividends to Retained Earnings. Only temporary accounts are closed.

3 Describe the content and purpose of a post-closing trial balance. A post-closing trial balance contains the balances in permanent accounts that are carried forward to the next accounting period. The purpose of this trial balance is to prove the equality of these balances.

4 State the required steps in the accounting cycle. The required steps in the accounting cycle are (1) analyze business transactions, (2) journalize the transactions, (3) post to ledger accounts, (4) prepare a trial balance, (5) journalize and post adjusting entries, (6) prepare an adjusted trial balance, (7) prepare financial statements, (8) journalize and post closing entries, and (9) prepare a post-closing trial balance.

5 Explain the approaches to preparing correcting entries. One way to determine the correcting entry is to compare the incorrect entry with the correct entry. After comparison, the company makes a correcting entry to correct the accounts. An alternative to a correcting entry is to reverse the incorrect entry and then prepare the correct entry.

6 Identify the sections of a classified balance sheet. A classified balance sheet categorizes assets as current assets; long-term investments; property, plant, and equipment; and intangibles. Liabilities are classified as either current or long-term. There is also a stockholders' (owners') equity section, which varies with the form of business organization.

GLOSSARY

Classified balance sheet A balance sheet that contains standard classifications or sections. (p. 181).

Closing entries Entries made at the end of an accounting period to transfer the balances of temporary accounts to a permanent stockholders' equity account, Retained Earnings. (p. 172).

Correcting entries Entries to correct errors made in recording transactions. (p. 180).

Current assets Assets that a company expects to convert to cash or use up within one year. (p. 182).

Current liabilities Obligations that a company expects to pay within the coming year or its operating cycle, whichever is longer. (p. 186).

Income Summary A temporary account used in closing revenue and expense accounts. (p. 172).

Intangible assets Noncurrent assets that do not have physical substance. (p. 184).

Liquidity The ability of a company to pay obligations expected to be due within the next year. (p. 186).

Long-term investments Generally, (1) investments in stocks and bonds of other companies that companies normally hold for many years, and (2) long-term assets, such as land and buildings, not currently being used in operations. (p. 183).

Long-term liabilities Obligations that a company expects to pay after one year. (p. 187).

Operating cycle The average time that it takes to purchase inventory, sell it on account, and then collect cash from customers. (p. 183).

Permanent (real) accounts Accounts that relate to one or more future accounting periods. Consist of all balance sheet accounts. Balances are carried forward to the next accounting period. (p. 172).

Post-closing trial balance A list of permanent accounts and their balances after a company has journalized and posted closing entries. (p. 176).

Property, plant, and equipment Assets with relatively long useful lives and currently being used in operations. (p. 184).

Reversing entry An entry, made at the beginning of the next accounting period, that is the exact opposite of the adjusting entry made in the previous period. (p. 179).

Stockholders' equity The ownership claim of shareholders on total assets. It is to a corporation what owner's equity is to a proprietorship. (p. 187).

Temporary (nominal) accounts Accounts that relate only to a given accounting period. Consist of all income statement accounts and the Dividends account. All temporary accounts are closed at the end of the accounting period. (p. 171).

Worksheet A multiple-column form that may be used in making adjusting entries and in preparing financial statements. (p. 166).

![]() 7

7

Prepare reversing entries.

APPENDIX 4A Reversing Entries

After preparing the financial statements and closing the books, it is often helpful to reverse some of the adjusting entries before recording the regular transactions of the next period. Such entries are reversing entries. Companies make a reversing entry at the beginning of the next accounting period. Each reversing entry is the exact opposite of the adjusting entry made in the previous period. The recording of reversing entries is an optional step in the accounting cycle.

The purpose of reversing entries is to simplify the recording of a subsequent transaction related to an adjusting entry. For example, in Chapter 3 (page 119), the payment of salaries after an adjusting entry resulted in two debits: one to Salaries and Wages Payable and the other to Salaries and Wages Expense. With reversing entries, the company can debit the entire subsequent payment to Salaries and Wages Expense. The use of reversing entries does not change the amounts reported in the financial statements. What it does is simplify the recording of subsequent transactions.

Reversing Entries Example

Companies most often use reversing entries to reverse two types of adjusting entries: accrued revenues and accrued expenses. To illustrate the optional use of reversing entries for accrued expenses, we will use the salaries expense transactions for Pioneer Advertising Agency Inc. as illustrated in Chapters 2, 3, and 4. The transaction and adjustment data are as follows.

- October 26 (initial salary entry): Pioneer pays $4,000 of salaries and wages earned between October 15 and October 26.

- October 31 (adjusting entry): Salaries and wages earned between October 29 and October 31 are $1,200. The company will pay these in the November 9 payroll.

- November 9 (subsequent salary entry): Salaries and wages paid are $4,000. Of this amount, $1,200 applied to accrued salaries and wages payable and $2,800 was earned between November 1 and November 9.

Illustration 4A-1 shows the entries with and without reversing entries.

The first three entries are the same whether or not Pioneer uses reversing entries. The last two entries are different. The November 1 reversing entry eliminates the $1,200 balance in Salaries and Wages Payable created by the October 31 adjusting entry. The reversing entry also creates a $1,200 credit balance in the Salaries and Wages Expense account. As you know, it is unusual for an expense account to have a credit balance. The balance is correct in this instance, though, because it anticipates that the entire amount of the first salaries and wages payment in the new accounting period will be debited to Salaries and Wages Expense. This debit will eliminate the credit balance. The resulting debit balance in the expense account will equal the salaries and wages expense incurred in the new accounting period ($2,800 in this example).

If Pioneer makes reversing entries, it can debit all cash payments of expenses to the expense account. This means that on November 9 (and every payday) Pioneer can debit Salaries and Wages Expense for the amount paid, without regard to any accrued salaries and wages payable. Being able to make the same entry each time simplifies the recording process. The company can record subsequent transactions as if the related adjusting entry had never been made.

Illustration 4A-1

Comparative entries—not reversing vs. reversing

Illustration 4A-2 shows the posting of the entries with reversing entries.

Illustration 4A-2

Postings with reversing entries

A company can also use reversing entries for accrued revenue adjusting entries. For Pioneer Advertising Agency Inc., the adjusting entry was Accounts Receivable (Dr.) $200 and Service Revenue (Cr.) $200. Thus, the reversing entry on November 1 is:

When Pioneer collects the accrued service revenue, it debits Cash and credits Service Revenue.

SUMMARY OF LEARNING OBJECTIVE FOR APPENDIX 4A

7 Prepare reversing entries. Reversing entries are the opposite of the adjusting entries made in the preceding period. Some companies choose to make reversing entries at the beginning of a new accounting period to simplify the recording of later transactions related to the adjusting entries. In most cases, only accrued adjusting entries are reversed.

![]() Self-Test, Brief Exercises, Exercises, Problem Set A, and many more components are available for practice in WileyPLUS.

Self-Test, Brief Exercises, Exercises, Problem Set A, and many more components are available for practice in WileyPLUS.

SELF-TEST QUESTIONS

Answers are on page 215.

| (LO 1)1. | Which of the following statements is incorrect concerning the worksheet?

(a) The worksheet is essentially a working tool of the accountant. (b) The worksheet is distributed to management and other interested parties. (c) The worksheet cannot be used as a basis for posting to ledger accounts. (d) Financial statements can be prepared directly from the worksheet before journalizing and posting the adjusting entries. |

| (LO 1) 2. | In a worksheet, net income is entered in the following columns:

(a) income statement (Dr) and balance sheet (Dr). (b) income statement (Cr) and balance sheet (Dr). (c) income statement (Dr) and balance sheet (Cr). (d) income statement (Cr) and balance sheet (Cr). |

| (LO 1) 3. | In the unadjusted trial balance of its worksheet for the year ended December 31, 2015, Knox Company reported Equipment of $120,000. The year-end adjusting entries require an adjustment of $15,000 for depreciation expense for the equipment. After adjustment, the following adjusted amount should be reported:

(a) a debit of $105,000 for Equipment in the balance sheet column. (b) a credit of $15,000 for Depreciation Expense—Equipment in the income statement column. (c) a debit of $120,000 for Equipment in the balance sheet column. (d) a debit of $15,000 for Accumulated Depreciation—Equipment in the balance sheet column. |

| (LO 2) 4. | An account that will have a zero balance after closing entries have been journalized and posted is:

(a) Service Revenue. (b) Supplies. (c) Prepaid Insurance. (d) Accumulated Depreciation—Equipment. |

| (LO 2) 5. | When a net loss has occurred, Income Summary is:

(a) debited and Retained Earnings is credited. (b) credited and Retained Earnings is debited. (c) debited and Dividends are credited. (d) credited and Dividends are is debited. |

| (LO 2) 6. | The closing process involves separate entries to close (1) expenses, (2) dividends, (3) revenues, and (4) income summary. The correct sequencing of the entries is:

(a) (4), (3), (2), (1) (b) (1), (2), (3), (4) (c) (3), (1), (4), (2) (d) (3), (2), (1), (4) |

| (LO 3) 7. | Which types of accounts will appear in the post-closing trial balance?

(a) Permanent (real) accounts. (b) Temporary (nominal) accounts. (c) Accounts shown in the income statement columns of a worksheet. (d) None of the above. |

| (LO 4) 8. | All of the following are required steps in the accounting cycle except:

(a) journalizing and posting closing entries. (b) preparing financial statements. (c) journalizing the transactions. (d) preparing a worksheet. |

| (LO 4) 9. | The proper order of the following steps in the accounting cycle is:

(a) prepare unadjusted trial balance, journalize transactions, post to ledger accounts, journalize and post adjusting entries. (b) journalize transactions, prepare unadjusted trial balance, post to ledger accounts, journalize and post adjusting entries. (c) journalize transactions, post to ledger accounts, prepare unadjusted trial balance, journalize and post adjusting entries. (d) prepare unadjusted trial balance, journalize and post adjusting entries, journalize transactions, post to ledger accounts. |

| (LO 5) 10. | When Ramirez Company purchased supplies worth $500, it incorrectly recorded a credit to Supplies for $5,000 and a debit to Cash for $5,000. Before correcting this error:

(a) Cash is overstated and Supplies is overstated. (b) Cash is understated and Supplies is understated. (c) Cash is understated and Supplies is overstated. (d) Cash is overstated and Supplies is understated. |

| (LO 5) 11. | Cash of $100 received at the time the service was performed was journalized and posted as a debit to Cash $100 and a credit to Accounts Receivable $100. Assuming the incorrect entry is not reversed, the correcting entry is:

(a) debit Service Revenue $100 and credit Accounts Receivable $100. (b) debit Accounts Receivable $100 and credit Service Revenue $100. (c) debit Cash $100 and credit Service Revenue $100. (d) debit Accounts Receivable $100 and credit Cash $100. |

| (LO 6) 12. | The correct order of presentation in a classified balance sheet for the following current assets is:

(a) accounts receivable, cash, prepaid insurance, inventory. (b) cash, inventory, accounts receivable, prepaid insurance. (c) cash, accounts receivable, inventory, prepaid insurance. (d) inventory, cash, accounts receivable, prepaid insurance. |

| (LO 6) 13. | A company has purchased a tract of land. It expects to build a production plant on the land in approximately 5 years. During the 5 years before construction, the land will be idle. The land should be reported as:

(a) property, plant, and equipment. (b) land expense. (c) a long-term investment. (d) an intangible asset. |

| (LO 6) 14. | In a classified balance sheet, assets are usually classified using the following categories:

(a) current assets; long-term assets; property, plant, and equipment; and intangible assets. (b) current assets; long-term investments; property, plant, and equipment; and tangible assets. (c) current assets; long-term investments; tangible assets; and intangible assets. (d) current assets; long-term investments; property, plant, and equipment; and intangible assets. |

| (LO 6) 15. | Current assets are listed:

(a) by expected conversion to cash. (b) by importance. (c) by longevity. (d) alphabetically. |

| (LO 7) *16. | On December 31, Kevin Hartman Company correctly made an adjusting entry to recognize $2,000 of accrued salaries payable. On January 8 of the next year, total salaries of $3,400 were paid. Assuming the correct reversing entry was made on January 1, the entry on January 8 will result in a credit to Cash $3,400 and the following debit(s):

(a) Salaries and Wages Payable $1,400 and Salaries and Wages Expense $2,000. (b) Salaries and Wages Payable $2,000 and Salaries and Wages Expense $1,400. (c) Salaries and Wages Expense $3,400. (d) Salaries and Wages Payable $3,400. |

Go to the book's companion website, www.wiley.com/college/weygandt, for additional Self-Test Questions.

![]()

QUESTIONS

1. “A worksheet is a permanent accounting record and its use is required in the accounting cycle.” Do you agree? Explain.

2. Explain the purpose of the worksheet.

3. What is the relationship, if any, between the amount shown in the adjusted trial balance column for an account and that account's ledger balance?

4. If a company's revenues are $125,000 and its expenses are $113,000, in which financial statement columns of the worksheet will the net income of $12,000 appear? When expenses exceed revenues, in which columns will the difference appear?

5. Why is it necessary to prepare formal financial statements if all of the data are in the statement columns of the worksheet?

6. Identify the account(s) debited and credited in each of the four closing entries, assuming the company has net income for the year.

7. Describe the nature of the Income Summary account and identify the types of summary data that may be posted to this account.

8. What are the content and purpose of a post-closing trial balance?

9. Which of the following accounts would not appear in the post-closing trial balance? Interest Payable; Equipment; Depreciation Expense; Dividends; Unearned Service Revenue; Accumulated Depreciation—Equipment; and Service Revenue.

10. Distinguish between a reversing entry and an adjusting entry. Are reversing entries required?

11. Indicate, in the sequence in which they are made, the three required steps in the accounting cycle that involve journalizing.

12. Identify, in the sequence in which they are prepared, the three trial balances that are often used to report financial information about a company.

13. How do correcting entries differ from adjusting entries?

14. What standard classifications are used in preparing a classified balance sheet?

15. What is meant by the term “operating cycle?”

16. Define current assets. What basis is used for arranging individual items within the current assets section?

17. Distinguish between long-term investments and property, plant, and equipment.

18. (a) What is the term used to describe the owners' equity section of a corporation? (b) Identify the two owners' equity accounts in a corporation and indicate the purpose of each.

19. Using Apple's annual report, determine its current liabilities at September 25, 2010, and September 24, 2011. Were current liabilities higher or lower than current assets in these two years?

*20. Cigale Company prepares reversing entries. If the adjusting entry for interest payable is reversed, what type of an account balance, if any, will there be in Interest Payable and Interest Expense after the reversing entry is posted?

*21. At December 31, accrued salaries payable totaled $3,500. On January 10, total salaries of $8,000 are paid. (a) Assume that reversing entries are made at January 1. Give the January 10 entry, and indicate the Salaries and Wages Expense account balance after the entry is posted. (b) Repeat part (a) assuming reversing entries are not made.

BRIEF EXERCISES

| List the steps in preparing a worksheet.

(LO 1) |

BE4-1 The steps in using a worksheet are presented in random order below. List the steps in the proper order by placing numbers 1–5 in the blank spaces.

(a) ____Prepare a trial balance on the worksheet. (b) ____Enter adjusted balances. (c) ____Extend adjusted balances to appropriate statement columns. (d) ____Total the statement columns, compute net income (loss), and complete the worksheet. (e) ____Enter adjustment data. |

||||||||||||||||||||

| Prepare partial worksheet.

(LO 1) |

BE4-2 The ledger of Clayton Company includes the following unadjusted balances: Prepaid Insurance $3,000, Service Revenue $58,000, and Salaries and Wages Expense $25,000. Adjusting entries are required for (a) expired insurance $1,800; (b) services performed $1,100, but unbilled and uncollected; and (c) accrued salaries payable $800. Enter the unadjusted balances and adjustments into a worksheet and complete the worksheet for all accounts. ( Note: You will need to add the following accounts: Accounts Receivable, Salaries and Wages Payable, and Insurance Expense.) | ||||||||||||||||||||

| Identify worksheet columns for selected accounts.

(LO 1) |

BE4-3 The following selected accounts appear in the adjusted trial balance columns of the worksheet for Goulet Company: Accumulated Depreciation—Equipment; Depreciation Expense; Common Stock; Dividends; Service Revenue; Supplies; and Accounts Payable. Indicate the financial statement column (income statement Dr., balance sheet Cr., etc.) to which each balance should be extended. | ||||||||||||||||||||

| Prepare closing entries from ledger balances.

(LO 2) |

BE4-4 The ledger of Rios Company contains the following balances: Retained Earnings $30,000; Dividends $2,000; Service Revenue $50,000; Salaries and Wages Expense $27,000; and Supplies Expense $7,000. Prepare the closing entries at December 31. | ||||||||||||||||||||

| Post closing entries; underline and balance T-accounts.

(LO 2) |

BE4-5 Using the data in BE4-4, enter the balances in T-accounts, post the closing entries, and underline and balance the accounts. | ||||||||||||||||||||

| Journalize and post closing entries using the three-column form of account.

(LO 2) |

BE4-6 The income statement for Weeping Willow Golf Club for the month ending July 31 shows Service Revenue $16,400, Salaries and Wages Expense $8,200, Maintenance and Repairs Expense $2,500, and Net Income $5,700. Prepare the entries to close the revenue and expense accounts. Post the entries to the revenue and expense accounts, and complete the closing process for these accounts using the three-column form of account. | ||||||||||||||||||||

| Identify post-closing trial balance accounts.

(LO 3) |

BE4-7 Using the data in BE4-3, identify the accounts that would be included in a post-closing trial balance. | ||||||||||||||||||||

| List the required steps in the accounting cycle in sequence.

(LO 4) |

BE4-8 The steps in the accounting cycle are listed in random order below. List the steps in proper sequence, assuming no worksheet is prepared, by placing numbers 1-9 in the blank spaces.

(a) ______Prepare a trial balance. (b) ______Journalize the transactions. (c) ______Journalize and post closing entries. (d) ______Prepare financial statements. (e) ______Journalize and post adjusting entries. (f) ______Post to ledger accounts. (g) ______Prepare a post-closing trial balance. (h) ______Prepare an adjusted trial balance. (i) ______Analyze business transactions. | ||||||||||||||||||||

| Prepare correcting entries.

(LO 5) |

BE4-9 At Creighton Company, the following errors were discovered after the transactions had been journalized and posted. Prepare the correcting entries.

| ||||||||||||||||||||

| Prepare the current assets section of a balance sheet.

(LO 6) |

BE4-10 The balance sheet debit column of the worksheet for Hamidi Company includes the following accounts: Accounts Receivable $12,500; Prepaid Insurance $3,600; Cash $4,100; Supplies $5,200; and Debt Investments (short-term) $6,700. Prepare the current assets section of the balance sheet, listing the accounts in proper sequence. | ||||||||||||||||||||

| Classify accounts on balance sheet.

(LO 6) |

BE4-11 The following are the major balance sheet classifications:

Match each of the following accounts to its proper balance sheet classification.

| ||||||||||||||||||||

| Prepare reversing entries.

(LO 7) |

*BE4-12 At October 31, Burgess Company made an accrued expense adjusting entry of $2,100 for salaries. Prepare the reversing entry on November 1, and indicate the balances in Salaries and Wages Payable and Salaries and Wages Expense after posting the reversing entry. |

> DO IT! Review

Prepare a worksheet.

(LO 1)

DO IT! 4-1 Bradley Decker is preparing a worksheet. Explain to Bradley how he should extend the following adjusted trial balance accounts to the financial statement columns of the worksheet.

| Service Revenue | Accounts Receivable |

| Notes Payable | Accumulated Depreciation |

| Common Stock | Utilities Expense |

Prepare closing entries.

(LO 2)

DO IT! 4-2 The worksheet for Tsai Company shows the following in the financial statement columns.

| Dividends | $22,000 |

| Common Stock | 70,000 |

| Net income | 41,000 |

Prepare the closing entries at December 31 that affect stockholders' equity.

Prepare assets section of the balance sheet.

(LO 6)

DO IT! 4-3 Ryan Newton recently received the following information related to Ryan Company's December 31, 2015, balance sheet.

Prepare the assets section of Ryan Company's classified balance sheet.

Match accounts to balance sheet classifications.

(LO 6)

DO IT! 4-4 The following accounts were taken from the financial statements of Lee Company.

| ______Interest revenue | ______Common stock |

| ______Utilities payable | ______Accumulated depreciation—equipment |

| ______Accounts payable | ______Equipment |

| ______Supplies | ______Salaries and wages expense |

| ______Bonds payable | ______Debt investments (long-term) |

| ______Goodwill | ______Unearned rent revenue |

Match each of the accounts to its proper balance sheet classification, as shown below. If the item would not appear on a balance sheet, use “NA.”

| Current assets (CA) | Current liabilities (CL) |

| Long-term investments (LTI) | Long-term liabilities (LTL) |

| Property, plant, and equipment (PPE) | Stockholders' equity (SE) |

| Intangible assets (IA) |

EXERCISES

| Complete the worksheet.

(LO 1) |

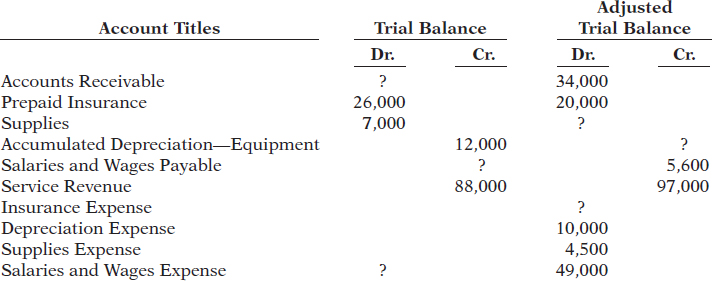

E4-1 The trial balance columns of the worksheet for Nanduri Company at June 30, 2015, are as follows.

Other data:

Instructions Enter the trial balance on a worksheet and complete the worksheet. |

||||||||||||||||||||||||

| Complete the worksheet.

(LO 1)

|

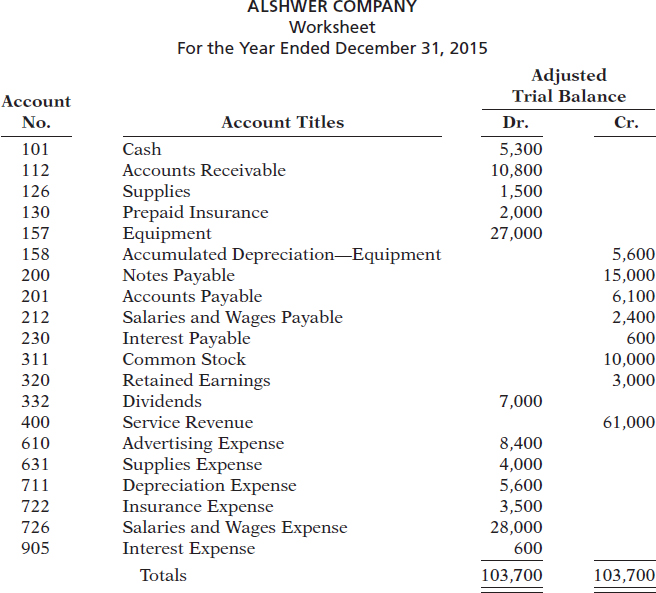

E4-2 The adjusted trial balance columns of the worksheet for DeSousa Company are as follows.

| ||||||||||||||||||||||||

| Prepare financial statements from worksheet.

(LO 1, 6)

|

E4-3 Worksheet data for DeSousa Company are presented in E4-2.

Instructions Prepare an income statement, a retained earnings statement, and a classified balance sheet. | ||||||||||||||||||||||||

| Journalize and post closing entries and prepare a post-closing trial balance.

(LO 2, 3) |

E4-4 Worksheet data for DeSousa Company are presented in E4-2.

Instructions (a) Journalize the closing entries at April 30. (b) Post the closing entries to Income Summary and Retained Earnings. (Use T-accounts.) (c) Prepare a post-closing trial balance at April 30. |

||||||||||||||||||||||||

| Prepare adjusting entries from a worksheet, and extend balances to worksheet columns.

(LO 1) |

E4-5 The adjustments columns of the worksheet for Misra Company are shown below.

Instructions (a) Prepare the adjusting entries. (b) Assuming the adjusted trial balance amount for each account is normal, indicate the financial statement column to which each balance should be extended. |

||||||||||||||||||||||||

| Derive adjusting entries from worksheet data.

(LO 1) |

E4-6 Selected worksheet data for Elsayed Company are presented below.

Instructions (a) Fill in the missing amounts. (b) Prepare the adjusting entries that were made. |

||||||||||||||||||||||||

| Prepare closing entries, and prepare a post-closing trial balance.

(LO 2, 3) |

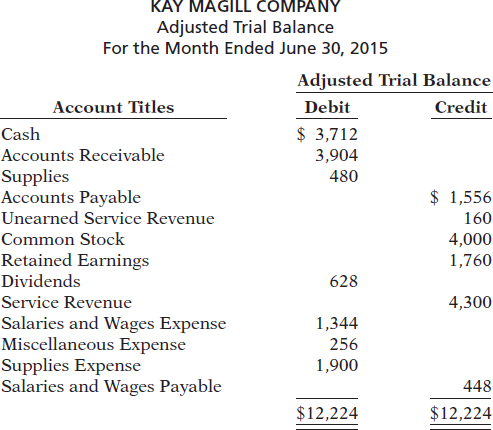

E4-7 Kay Magill Company had the following adjusted trial balance.

Instructions (a) Prepare closing entries at June 30, 2015. (b) Prepare a post-closing trial balance. |

||||||||||||||||||||||||

| Journalize and post closing entries, and prepare a post-closing trial balance.

(LO 2, 3) |

E4-8 Plevin Company ended its fiscal year on July 31, 2015. The company's adjusted trial balance as of the end of its fiscal year is shown below.

Instructions (a) Prepare the closing entries using page J15. (b) Post to the Retained Earnings and No. 350 Income Summary accounts. (Use the three-column form.) (c) Prepare a post-closing trial balance at July 31. | ||||||||||||||||||||||||

| Prepare financial statements.

(LO 6) |

E4-9 The adjusted trial balance for Plevin Company is presented in E4-8.

Instructions (a) Prepare an income statement and a retained earnings statement for the year. (b) Prepare a classified balance sheet at July 31. | ||||||||||||||||||||||||

| Answer questions related to the accounting cycle.

(LO 4) |

E4-10 Janis Engle has prepared the following list of statements about the accounting cycle.

Instructions Identify each statement as true or false. If false, indicate how to correct the statement. | ||||||||||||||||||||||||

| Prepare closing entries.

(LO 2) |

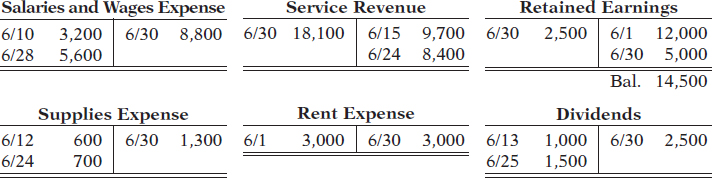

E4-11 Selected accounts for Heather's Salon are presented below. All June 30 postings are from closing entries.

Instructions (a) Prepare the closing entries that were made. (b) Post the closing entries to Income Summary. |

||||||||||||||||||||||||

| Prepare correcting entries.

(LO 5) |

E4-12 Andrew Clark Company discovered the following errors made in January 2015.

Instructions (a) Correct the errors by reversing the incorrect entry and preparing the correct entry. (b) Correct the errors without reversing the incorrect entry. | ||||||||||||||||||||||||

| Prepare correcting entries.

(LO 5) |

E4-13 Keenan Company has an inexperienced accountant. During the first 2 weeks on the job, the accountant made the following errors in journalizing transactions. All entries were posted as made.

Instructions Prepare the correcting entries. | ||||||||||||||||||||||||

| Prepare a classified balance sheet.

(LO 6) |

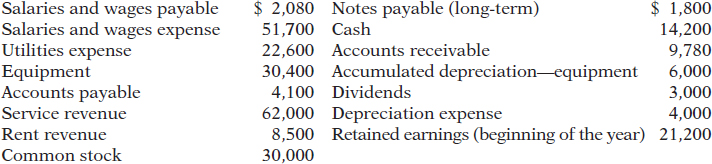

E4-14 The adjusted trial balance for Martell Bowling Alley at December 31, 2015, contains the following accounts.

Instructions (a) Prepare a classified balance sheet; assume that $22,000 of the note payable will be paid in 2016. (b) |

||||||||||||||||||||||||

| Classify accounts on balance sheet.

(LO 6) |

E4-15 The following are the major balance sheet classifications.

Instructions Classify each of the following accounts taken from Raman Company's balance sheet.

| ||||||||||||||||||||||||

| Prepare a classified balance sheet.

(LO 6) |

E4-16 The following items were taken from the financial statements of D. Gygi Company. (All amounts are in thousands.)

Instructions Prepare a classified balance sheet in good form as of December 31, 2015. | ||||||||||||||||||||||||

| Prepare financial statements.

(LO 6) |

E4-17 These financial statement items are for Norsted Company at year-end, July 31, 2015.

Instructions (a) Prepare an income statement and a retained earnings statement for the year. (b) Prepare a classified balance sheet at July 31. |

||||||||||||||||||||||||

| Use reversing entries.

(LO 7) |