11  Corporations: Organization, Stock Transactions, Dividends, and Retained Earnings

Corporations: Organization, Stock Transactions, Dividends, and Retained Earnings

Feature Story What's Cooking?

![]()

What major U.S. corporation got its start 41 years ago with a waffle iron? Hint: It doesn't sell food. Another hint: Swoosh. Another hint: “Just do it.” That's right, Nike. In 1971, Nike co-founder Bill Bowerman put a piece of rubber into a kitchen waffle iron, and the trademark waffle sole was born. It seems fair to say that at Nike, “They don't make 'em like they used to.”

Nike was co-founded by Bowerman and Phil Knight, a member of Bowerman's University of Oregon track team. Each began in the shoe business independently during the early 1960s. Bowerman got his start by making hand-crafted running shoes for his University of Oregon track team. Knight, after completing graduate school, started a small business importing low-cost, high-quality shoes from Japan. In 1964, the two joined forces, each contributing $500, and formed Blue Ribbon Sports, a partnership that marketed Japanese shoes. It wasn't until 1971 that the company began manufacturing its own line of shoes. With the new shoes came a new corporate name–Nike–the Greek goddess of victory. It is hard to imagine that the company that now boasts a stable full of world-class athletes as promoters at one time had part-time employees selling shoes out of car trunks at track meets. Nike has achieved its success through relentless innovation combined with unbridled promotion.

By 1980, Nike was sufficiently established and issued its first stock to the public. That same year, it created a stock ownership program for its employees, allowing them to share in the company's success. Since then, Nike has enjoyed phenomenal growth, with 2012 sales reaching $24.1 billion and total dividends paid of $619 million.

Nike is not alone in its quest for the top of the sport shoe world. Reebok used to be Nike's arch rival (get it? “arch”), but then Reebok was acquired by the German company adidas. Now adidas pushes Nike every step of the way.

![]()

Scan Learning Objectives

Scan Learning Objectives- Read Feature Story

- Read Preview

- Read text and answer DO IT! p. 551

p. 553 p. 556 p. 560 p. 565 p. 569 p. 572 p. 575

- Work Comprehensive DO IT! p. 575

- Review Summary of Learning Objectives

- Answer Self-Test Questions

- Complete Assignments

- Go to WileyPLUS for practice and tutorials

Read A Look at IFRS p. 600

Read A Look at IFRS p. 600

Learning Objectives ![]()

After studying this chapter, you should be able to:

[1] Identify the major characteristics of a corporation.

[2] Record the issuance of common stock.

[3] Explain the accounting for treasury stock.

[4] Differentiate preferred stock from common stock.

[5] Prepare the entries for cash dividends and stock dividends.

[6] Identify the items reported in a retained earnings statement.

[7] Prepare and analyze a comprehensive stockholders' equity section.

The shoe market is fickle, with new styles becoming popular almost daily and vast international markets still lying untapped. Whether one of these two giants does eventually take control of the pedi-planet remains to be seen. Meanwhile, the shareholders sit anxiously in the stands as this Olympic-size drama unfolds.

Preview of Chapter 11

![]()

Corporations like Nike and adidas have substantial resources at their disposal. In fact, the corporation is the dominant form of business organization in the United States in terms of sales, earnings, and number of employees. All of the 500 largest companies in the United States are corporations. In this chapter, we will explain the essential features of a corporation and the accounting for a corporation's capital stock transactions.

The content and organization of Chapter 11 are as follows.

![]() 1

1

Identify the major characteristics of a corporation.

The Corporate Form of Organization

In 1819, Chief Justice John Marshall defined a corporation as “an artificial being, invisible, intangible, and existing only in contemplation of law.” This definition is the foundation for the prevailing legal interpretation that a corporation is an entity separate and distinct from its owners.

A corporation is created by law, and its continued existence depends upon the statutes of the state in which it is incorporated. As a legal entity, a corporation has most of the rights and privileges of a person. The major exceptions relate to privileges that only a living person can exercise, such as the right to vote or to hold public office. A corporation is subject to the same duties and responsibilities as a person. For example, it must abide by the laws, and it must pay taxes.

Two common ways to classify corporations are by purpose and by ownership. A corporation may be organized for the purpose of making a profit, or it may be not-for-profit. For-profit corporations include such well-known companies as McDonald's, Nike, PepsiCo, and Google. Not-for-profit corporations are organized for charitable, medical, or educational purposes. Examples are the Salvation Army and the American Cancer Society.

Classification by ownership differentiates publicly held and privately held corporations. A publicly held corporation may have thousands of stockholders. Its stock is regularly traded on a national securities exchange such as the New York Stock Exchange. Examples are IBM, Caterpillar, and General Electric.

Alternative Terminology

Privately held corporations are also referred to as closely held corporations.

In contrast, a privately held corporation usually has only a few stockholders, and does not offer its stock for sale to the general public. Privately held companies are generally much smaller than publicly held companies, although some notable exceptions exist. Cargill Inc., a private corporation that trades in grain and other commodities, is one of the largest companies in the United States.

Characteristics of a Corporation

In 1964, when Nike's founders Phil Knight and Bill Bowerman were just getting started in the running shoe business, they formed their original organization as a partnership. In 1968, they reorganized the company as a corporation. A number of characteristics distinguish corporations from proprietorships and partnerships. We explain the most important of these characteristics below.

SEPARATE LEGAL EXISTENCE

As an entity separate and distinct from its owners, the corporation acts under its own name rather than in the name of its stockholders. Nike may buy, own, and sell property. It may borrow money, and may enter into legally binding contracts in its own name. It may also sue or be sued, and it pays its own taxes.

In a partnership, the acts of the owners (partners) bind the partnership. In contrast, the acts of its owners (stockholders) do not bind the corporation unless such owners are agents of the corporation. For example, if you owned shares of Nike stock, you would not have the right to purchase inventory for the company unless you were designated as an agent of the corporation.

LIMITED LIABILITY OF STOCKHOLDERS

Since a corporation is a separate legal entity, creditors have recourse only to corporate assets to satisfy their claims. The liability of stockholders is normally limited to their investment in the corporation. Creditors have no legal claim on the personal assets of the owners unless fraud has occurred. Even in the event of bankruptcy, stockholders' losses are generally limited to their capital investment in the corporation.

TRANSFERABLE OWNERSHIP RIGHTS

Shares of capital stock give ownership in a corporation. These shares are transferable units. Stockholders may dispose of part or all of their interest in a corporation simply by selling their stock. The transfer of an ownership interest in a partnership requires the consent of each owner. In contrast, the transfer of stock is entirely at the discretion of the stockholder. It does not require the approval of either the corporation or other stockholders.

The transfer of ownership rights between stockholders normally has no effect on the daily operating activities of the corporation. Nor does it affect the corporation's assets, liabilities, and total ownership equity. The transfer of these ownership rights is a transaction between individual owners. The company does not participate in the transfer of these ownership rights after the original sale of the capital stock.

ABILITY TO ACQUIRE CAPITAL

It is relatively easy for a corporation to obtain capital through the issuance of stock. Buying stock in a corporation is often attractive to an investor because a stockholder has limited liability and shares of stock are readily transferable. Also, numerous individuals can become stockholders by investing relatively small amounts of money.

CONTINUOUS LIFE

The life of a corporation is stated in its charter. The life may be perpetual, or it may be limited to a specific number of years. If it is limited, the company can extend the life through renewal of the charter. Since a corporation is a separate legal entity, its continuance as a going concern is not affected by the withdrawal, death, or incapacity of a stockholder, employee, or officer. As a result, a successful company can have a continuous and perpetual life.

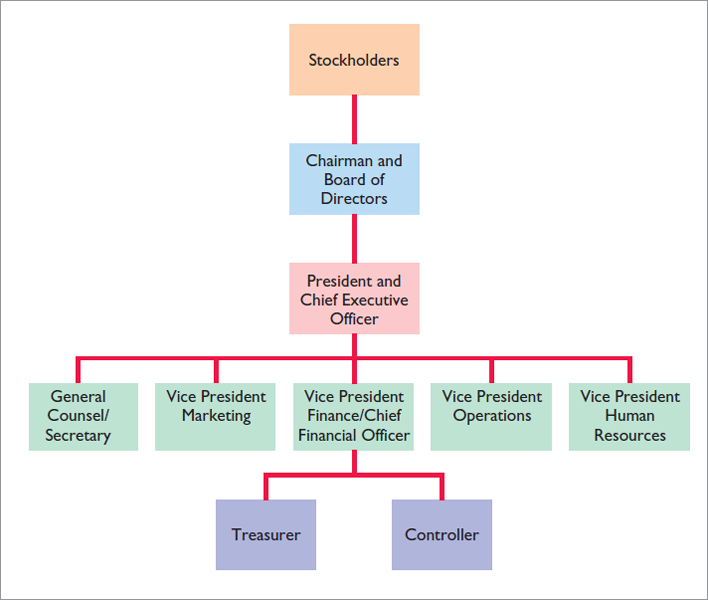

CORPORATION MANAGEMENT

Stockholders legally own the corporation. However, they manage the corporation indirectly through a board of directors they elect. Philip Knight is the chairman of the board for Nike. The board, in turn, formulates the operating policies for the company. The board also selects officers, such as a president and one or more vice presidents, to execute policy and to perform daily management functions. As a result of the Sarbanes-Oxley Act, the board is now required to monitor management's actions more closely. Many feel that the failures of Enron, WorldCom, and more recently MF Global could have been avoided by more diligent boards.

Illustration 11-1 (page 546) presents a typical organization chart showing the delegation of responsibility. The chief executive officer (CEO) has overall responsibility for managing the business. As the organization chart shows, the CEO delegates responsibility to other officers. The chief accounting officer is the controller. The controller's responsibilities include (1) maintaining the accounting records, (2) maintaining an adequate system of internal control, and (3) preparing financial statements, tax returns, and internal reports. The treasurer has custody of the corporation's funds and is responsible for maintaining the company's cash position.

Ethics Note ![]()

Managers who are not owners are often compensated based on the performance of the firm. They thus may be tempted to exaggerate firm performance by inflating income figures.

The organizational structure of a corporation enables a company to hire professional managers to run the business. On the other hand, the separation of ownership and management often reduces an owner's ability to actively manage the company.

Illustration 11-1

Corporation organization chart

GOVERNMENT REGULATIONS

A corporation is subject to numerous state and federal regulations. For example, state laws usually prescribe the requirements for issuing stock, the distributions of earnings permitted to stockholders, and the acceptable methods for buying back and retiring stock. Federal securities laws govern the sale of capital stock to the general public. Also, most publicly held corporations are required to make extensive disclosure of their financial affairs to the Securities and Exchange Commission (SEC) through quarterly and annual reports. In addition, when a corporation lists its stock on organized securities exchanges, it must comply with the reporting requirements of these exchanges. Government regulations are designed to protect the owners of the corporation.

ADDITIONAL TAXES

Owners of proprietorships and partnerships report their share of earnings on their personal income tax returns. The individual owner then pays taxes on this amount. Corporations, on the other hand, must pay federal and state income taxes as a separate legal entity. These taxes can be substantial. They can amount to as much as 40% of taxable income.

In addition, stockholders must pay taxes on cash dividends (pro rata distributions of net income). Thus, many argue that the government taxes corporate income twice (double taxation)—once at the corporate level and again at the individual level.

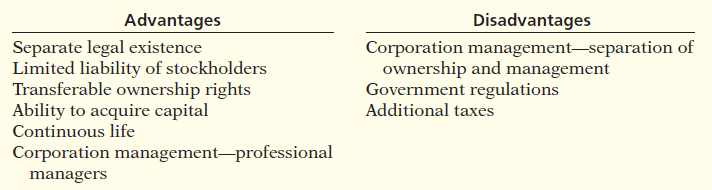

In summary, Illustration 11-2 shows the advantages and disadvantages of a corporation compared to a proprietorship and a partnership.

Forming a Corporation

A corporation is formed by grant of a state charter. The charter is a document that describes the name and purpose of the corporation, the types and number of shares of stock that are authorized to be issued, the names of the individuals that formed the company, and the number of shares that these individuals agreed to purchase. Regardless of the number of states in which a corporation has operating divisions, it is incorporated in only one state.

Illustration 11-2

Advantages and disadvantages of a corporation

Alternative Terminology

The charter is often referred to as the articles of incorporation.

It is to the company's advantage to incorporate in a state whose laws are favorable to the corporate form of business organization. For example, although General Motors has its headquarters in Michigan, it is incorporated in New Jersey. In fact, more and more corporations have been incorporating in states with rules that favor existing management. For example, Gulf Oil changed its state of incorporation to Delaware to thwart possible unfriendly takeovers. There, certain defensive tactics against takeovers can be approved by the board of directors alone, without a vote by shareholders.

Upon receipt of its charter from the state of incorporation, the corporation establishes by-laws. The by-laws establish the internal rules and procedures for conducting the affairs of the corporation. Corporations engaged in interstate commerce must also obtain a license from each state in which they do business. The license subjects the corporation's operating activities to the general corporation laws of the state.

Costs incurred in the formation of a corporation are called organization costs. These costs include legal and state fees, and promotional expenditures involved in the organization of the business. Corporations expense organization costs as incurred. Determining the amount and timing of future benefits is so difficult that it is standard procedure to take a conservative approach of expensing these costs immediately.

ACCOUNTING ACROSS THE ORGANIZATION

A Thousand Millionaires!

Traveling to space or embarking on an expedition to excavate lost Mayan ruins are normally the stuff of adventure novels. But for employees of Facebook, these and other lavish dreams moved closer to reality when the world's No. 1 online social network went public through an initial public offering (IPO) that may have created at least a thousand millionaires. The IPO was the largest in Internet history, valuing Facebook at over $104 billion.

With all these riches to be had, why did Mark Zuckerberg, the founder of Facebook, delay taking his company public? Consider that the main motivation for issuing shares to the public is to raise money so you can grow your business. However, unlike a manufacturer or even an online retailer, Facebook doesn't need major physical resources, it doesn't have inventory, and it doesn't really need much money for marketing. So in the past, the company hasn't had much need for additional cash beyond what it was already generating on its own. Finally, as head of a closely held, nonpublic company, Zuckerberg was subject to far fewer regulations than a public company.

Source: “Status Update: I'm Rich! Facebook Flotation to Create 1,000 Millionaires Among Company's Rank and File,” Daily Mail Reporter (February 1, 2012).

Why did Mark Zuckerberg, the CEO and founder of Facebook, delay taking his company's shares public through an initial public offering (IPO)? (See page 600.)

Why did Mark Zuckerberg, the CEO and founder of Facebook, delay taking his company's shares public through an initial public offering (IPO)? (See page 600.)

Stockholder Rights

When chartered, the corporation may begin selling shares of stock. When a corporation has only one class of stock, it is common stock. Each share of common stock gives the stockholder the ownership rights pictured in Illustration 11-3. The articles of incorporation or the by-laws state the ownership rights of a share of stock.

Illustration 11-3

Ownership rights of stockholders

Proof of stock ownership is evidenced by a form known as a stock certificate. As Illustration 11-4 shows, the face of the certificate shows the name of the corporation, the stockholder's name, the class and special features of the stock, the number of shares owned, and the signatures of authorized corporate officials. Prenumbered certificates facilitate accountability. They may be issued for any quantity of shares.

Stock Issue Considerations

Although Nike incorporated in 1968, it did not sell stock to the public until 1980. At that time, Nike evidently decided it would benefit from the infusion of cash that a public sale would bring. When a corporation decides to issue stock, it must resolve a number of basic questions: How many shares should it authorize for sale? How should it issue the stock? What value should the corporation assign to the stock? We address these questions in the following sections.

Illustration 11-4

A stock certificate

AUTHORIZED STOCK

The charter indicates the amount of stock that a corporation is authorized to sell. The total amount of authorized stock at the time of incorporation normally anticipates both initial and subsequent capital needs. As a result, the number of shares authorized generally exceeds the number initially sold. If it sells all authorized stock, a corporation must obtain consent of the state to amend its charter before it can issue additional shares.

The authorization of capital stock does not result in a formal accounting entry. The reason is that the event has no immediate effect on either corporate assets or stockholders' equity. However, the number of authorized shares is often reported in the stockholders' equity section. It is then simple to determine the number of unissued shares that the corporation can issue without amending the charter: subtract the total shares issued from the total authorized. For example, if Advanced Micro was authorized to sell 100,000 shares of common stock and issued 80,000 shares, 20,000 shares would remain unissued.

ISSUANCE OF STOCK

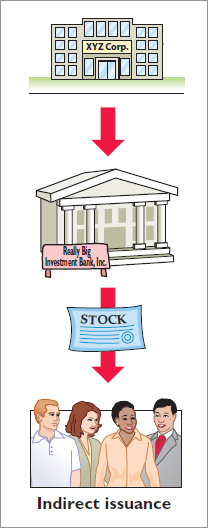

A corporation can issue common stock directly to investors. Alternatively, it can issue the stock indirectly through an investment banking firm that specializes in bringing securities to the attention of prospective investors. Direct issue is typical in closely held companies. Indirect issue is customary for a publicly held corporation.

In an indirect issue, the investment banking firm may agree to underwrite the entire stock issue. In this arrangement, the investment banker buys the stock from the corporation at a stipulated price and resells the shares to investors. The corporation thus avoids any risk of being unable to sell the shares. Also, it obtains immediate use of the cash received from the underwriter. The investment banking firm, in turn, assumes the risk of reselling the shares, in return for an underwriting fee.2 For example, Google (the world's number-one Internet search engine) used underwriters when it issued a highly successful initial public offering, raising $1.67 billion. The underwriters charged a 3% underwriting fee (approximately $50 million) on Google's stock offering.

How does a corporation set the price for a new issue of stock? Among the factors to be considered are (1) the company's anticipated future earnings, (2) its expected dividend rate per share, (3) its current financial position, (4) the current state of the economy, and (5) the current state of the securities market. The calculation can be complex and is properly the subject of a finance course.

MARKET PRICE OF STOCK

The stock of publicly held companies is traded on organized exchanges. The interaction between buyers and sellers determines the prices per share. In general, the prices set by the marketplace tend to follow the trend of a company's earnings and dividends. But, factors beyond a company's control, such as an oil embargo, changes in interest rates, and the outcome of a presidential election, may cause day-to-day fluctuations in market prices.

The trading of capital stock on securities exchanges involves the transfer of already issued shares from an existing stockholder to another investor. These transactions have no impact on a corporation's stockholders' equity.

INVESTOR INSIGHT

How to Read Stock Quotes

Organized exchanges trade the stock of publicly held companies at dollar prices per share established by the interaction between buyers and sellers. For each listed security, the financial press reports the high and low prices of the stock during the year, the total volume of stock traded on a given day, the high and low prices for the day, and the closing market price, with the net change for the day. Nike is listed on the New York Stock Exchange. Here is a listing for Nike:

These numbers indicate the following. The high and low market prices for the last 52 weeks have been $78.55 and $48.76. The trading volume for the day was 5,375,651 shares. The high, low, and closing prices for that date were $72.44, $69.78, and $70.61, respectively. The net change for the day was a decrease of $1.69 per share.

For stocks traded on organized exchanges, how are the dollar prices per share established? What factors might influence the price of shares in the marketplace? (See page 600.)

PAR AND NO-PAR VALUE STOCKS

Par value stock is capital stock to which the charter has assigned a value per share. Years ago, par value determined the legal capital per share that a company must retain in the business for the protection of corporate creditors. That amount was not available for withdrawal by stockholders. Thus, in the past, most states required the corporation to sell its shares at par or above.

However, par value was often immaterial relative to the value of the company's stock—even at the time of issue. Thus, its usefulness as a protective device to creditors was questionable. For example, Loews Corporation's par value is $0.01 per share, yet a new issue in 2013 would have sold at a market price in the $46 per share range. Thus, par has no relationship with market price. In the vast majority of cases, it is an immaterial amount. As a consequence, today many states do not require a par value. Instead, they use other means to protect creditors.

No-par value stock is capital stock to which the charter has not assigned a value. No-par value stock is fairly common today. For example, Nike and Procter & Gamble both have no-par stock. In many states, the board of directors assigns a stated value to no-par shares.

> DO IT!

Corporate Organization

Indicate whether each of the following statements is true or false. If false, indicate how to correct the statement.

- _____ 1. Similar to partners in a partnership, stockholders of a corporation have unlimited liability.

- _____ 2. It is relatively easy for a corporation to obtain capital through the issuance of stock.

- _____ 3. The separation of ownership and management is an advantage of the corporate form of business.

- _____ 4. The journal entry to record the authorization of capital stock includes a credit to the appropriate capital stock account.

- _____ 5. All states require a par value per share for capital stock.

Action Plan

![]() Review the characteristics of a corporation and understand which are advantages and which are disadvantages.

Review the characteristics of a corporation and understand which are advantages and which are disadvantages.

![]() Understand that corporations raise capital through the issuance of stock, which can be par or no-par.

Understand that corporations raise capital through the issuance of stock, which can be par or no-par.

Solution

- False. The liability of stockholders is normally limited to their investment in the corporation.

- True.

- False. The separation of ownership and management is a disadvantage of the corporate form of business.

- False. The authorization of capital stock does not result in a formal accounting entry.

- False. Many states do not require a par value.

Related exercise material: BE11-1, E11-1, E11-2, and DO IT! 11-1.

![]()

Corporate Capital

Owners' equity is identified by various names: stockholders' equity, shareholders' equity, or corporate capital. The stockholders' equity section of a corporation's balance sheet consists of two parts: (1) paid-in (contributed) capital and (2) retained earnings (earned capital).

The distinction between paid-in capital and retained earnings is important from both a legal and a financial point of view. Legally, corporations can make distributions of earnings (declare dividends) out of retained earnings in all states. However, in many states they cannot declare dividends out of paid-in capital. Management, stockholders, and others often look to retained earnings for the continued existence and growth of the corporation.

PAID-IN CAPITAL

Paid-in capital is the total amount of cash and other assets paid in to the corporation by stockholders in exchange for capital stock. As noted earlier, when a corporation has only one class of stock, it is common stock.

RETAINED EARNINGS

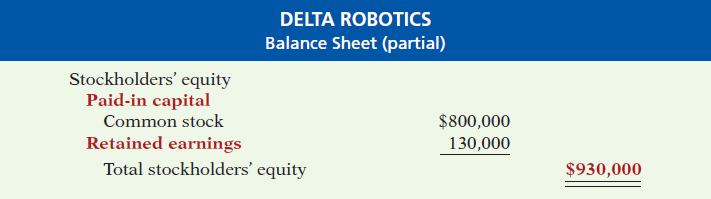

Retained earnings is net income that a corporation retains for future use. Net income is recorded in Retained Earnings by a closing entry that debits Income Summary and credits Retained Earnings. For example, assuming that net income for Delta Robotics in its first year of operations is $130,000, the closing entry is:

If Delta Robotics has a balance of $800,000 in common stock at the end of its first year, its stockholders' equity section is as follows.

Illustration 11-5

Stockholders' equity section

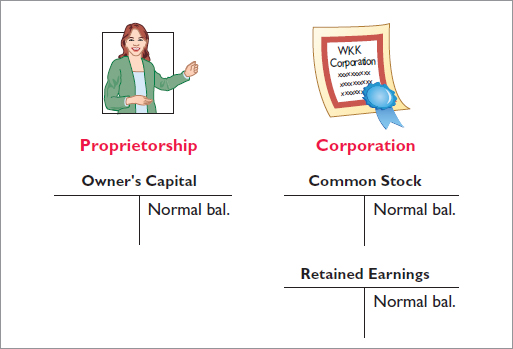

Illustration 11-6 compares the owners' equity (stockholders' equity) accounts reported on a balance sheet for a proprietorship and a corporation.

Illustration 11-6

Comparison of owners' equity accounts

PEOPLE, PLANET, AND PROFIT INSIGHT ![]()

The Impact of Corporate Social Responsibility

A recent survey conducted by Institutional Shareholder Services, a proxy advisory firm, shows that 83% of investors now believe environmental and social factors can significantly impact shareholder value over the long term. This belief is clearly visible in the rising level of support for shareholder proposals requesting action related to social and environmental issues.

The following table shows that the number of corporate social responsibility (CSR)-related shareholder proposals rose from 150 in 2000 to 191 in 2010. Moreover, those proposals received average voting support of 18.4% of votes cast versus just 7.5% a decade earlier.

Trends in Shareholder Proposals on Corporate Responsibility

Source: Investor Responsibility Research Center, Ernst & Young, Seven Questions CEOs and Boards Should Ask About: “Triple Bottom Line” Reporting.

Why are CSR-related shareholder proposals increasing? (See page 600.)

> DO IT!

Corporate Capital

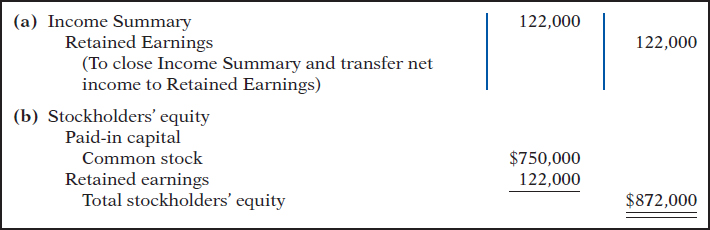

At the end of its first year of operation, Doral Corporation has $750,000 of common stock and net income of $122,000. Prepare (a) the closing entry for net income and (b) the stockholders' equity section at year-end.

Action Plan

![]() Record net income in Retained Earnings by a closing entry in which Income Summary is debited and Retained Earnings is credited.

Record net income in Retained Earnings by a closing entry in which Income Summary is debited and Retained Earnings is credited.

![]() In the stockholders' equity section, show (1) paid-in capital and (2) retained earnings.

In the stockholders' equity section, show (1) paid-in capital and (2) retained earnings.

Solution

Related exercise material: DO IT! 11-2.

![]()

Accounting for Stock Transactions

![]() 2

2

Record the issuance of common stock.

Accounting for Common Stock

Let's now look at how to account for issues of common stock. The primary objectives in accounting for the issuance of common stock are (1) to identify the specific sources of paid-in capital, and (2) to maintain the distinction between paid-in capital and retained earnings. The issuance of common stock affects only paid-in capital accounts.

ISSUING PAR VALUE COMMON STOCK FOR CASH

As discussed earlier, par value does not indicate a stock's market price. Therefore, the cash proceeds from issuing par value stock may be equal to, greater than, or less than par value. When the company records issuance of common stock for cash, it credits the par value of the shares to Common Stock. It also records in a separate paid-in capital account the portion of the proceeds that is above or below par value.

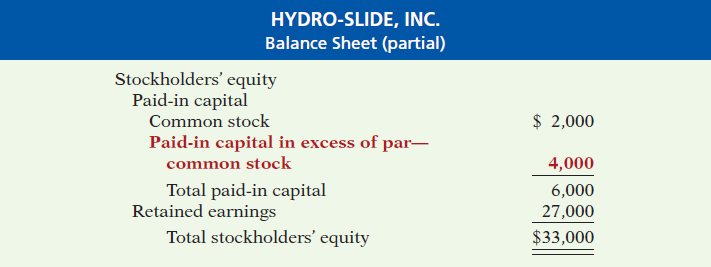

To illustrate, assume that Hydro-Slide, Inc. issues 1,000 shares of $1 par value common stock at par for cash. The entry to record this transaction is:

Now assume that Hydro-Slide issues an additional 1,000 shares of the $1 par value common stock for cash at $5 per share. The amount received above the par value, in this case $4 ($5 − $1), is credited to Paid-in Capital in Excess of Par—Common Stock. The entry is:

The total paid-in capital from these two transactions is $6,000, and the legal capital is $2,000. Assuming Hydro-Slide, Inc. has retained earnings of $27,000, Illustration 11-7 shows the company's stockholders' equity section.

Illustration 11-7

Stockholders' equity—paid-in capital in excess of par

Alternative Terminology

Paid-in Capital in Excess of Par is also called Premium on Stock.

When a corporation issues stock for less than par value, it debits the account Paid-in Capital in Excess of Par—Common Stock if a credit balance exists in this account. If a credit balance does not exist, then the corporation debits to Retained Earnings the amount less than par. This situation occurs only rarely. Most states do not permit the sale of common stock below par value because stockholders may be held personally liable for the difference between the price paid upon original sale and par value.

ISSUING NO-PAR COMMON STOCK FOR CASH

When no-par common stock has a stated value, the entries are similar to those illustrated for par value stock. The corporation credits the stated value to Common Stock. Also, when the selling price of no-par stock exceeds stated value, the corporation credits the excess to Paid-in Capital in Excess of Stated Value—Common Stock.

For example, assume that instead of $1 par value stock, Hydro-Slide, Inc. has $5 stated value no-par stock and the company issues 5,000 shares at $8 per share for cash. The entry is:

Hydro-Slide, Inc. reports Paid-in Capital in Excess of Stated Value—Common Stock as part of paid-in capital in the stockholders' equity section.

What happens when no-par stock does not have a stated value? In that case, the corporation credits the entire proceeds to Common Stock. Thus, if Hydro-Slide does not assign a stated value to its no-par stock, it records the issuance of the 5,000 shares at $8 per share for cash as follows.

ISSUING COMMON STOCK FOR SERVICES OR NONCASH ASSETS

Corporations also may issue stock for services (compensation to attorneys or consultants) or for noncash assets (land, buildings, and equipment). In such cases, what cost should be recognized in the exchange transaction? To comply with the historical cost principle, in a noncash transaction cost is the cash equivalent price. Thus, cost is either the fair value of the consideration given up or the fair value of the consideration received, whichever is more clearly determinable.

To illustrate, assume that attorneys have helped Jordan Company incorporate. They have billed the company $5,000 for their services. They agree to accept 4,000 shares of $1 par value common stock in payment of their bill. At the time of the exchange, there is no established market price for the stock. In this case, the fair value of the consideration received, $5,000, is more clearly evident. Accordingly, Jordan Company makes the following entry.

As explained on page 547, organization costs are expensed as incurred.

In contrast, assume that Athletic Research Inc. is an existing publicly held corporation. Its $5 par value stock is actively traded at $8 per share. The company issues 10,000 shares of stock to acquire land recently advertised for sale at $90,000. The most clearly evident value in this noncash transaction is the market price of the consideration given, $80,000. The company records the transaction as follows.

As illustrated in these examples, the par value of the stock is never a factor in determining the cost of the assets received. This is also true of the stated value of no-par stock.

ANATOMY OF A FRAUD

The president, chief operating officer, and chief financial officer of SafeNet, a software encryption company, were each awarded employee stock options by the company's board of directors as part of their compensation package. Stock options enable an employee to buy a company's stock sometime in the future at the price that existed when the stock option was awarded. For example, suppose that you received stock options today, when the stock price of your company was $30. Three years later, if the stock price rose to $100, you could “exercise” your options and buy the stock for $30 per share, thereby making $70 per share. After being awarded their stock options, the three employees changed the award dates in the company's records to dates in the past, when the company's stock was trading at historical lows. For instance, using the previous example, they would choose a past date when the stock was selling for $10 per share, rather than the $30 price on the actual award date. This would increase the profit from exercising the options to $90 per share.

Total take: $1.7 million

THE MISSING CONTROL

Independent internal verification. The company's board of directors should have ensured that the awards were properly administered. For example, the date on the minutes from the board meeting could be compared to the dates that were recorded for the awards. In addition, the dates should again be confirmed upon exercise.

> DO IT!

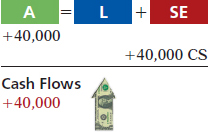

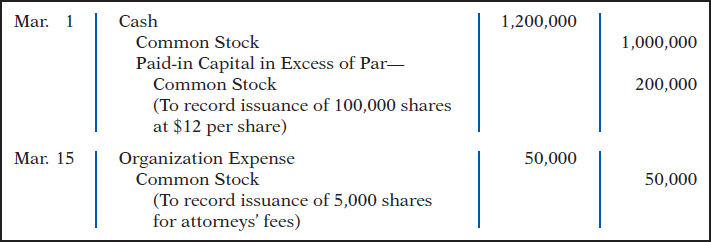

Issuance of Stock

Cayman Corporation begins operations on March 1 by issuing 100,000 shares of $10 par value common stock for cash at $12 per share. On March 15, it issues 5,000 shares of common stock to attorneys in settlement of their bill of $50,000 for organization costs. Journalize the issuance of the shares, assuming the stock is not publicly traded.

Action Plan

![]() In issuing shares for cash, credit Common Stock for par value per share.

In issuing shares for cash, credit Common Stock for par value per share.

![]() Credit any additional proceeds in excess of par to a separate paid-in capital account.

Credit any additional proceeds in excess of par to a separate paid-in capital account.

![]() When stock is issued for services, use the cash equivalent price.

When stock is issued for services, use the cash equivalent price.

![]() For the cash equivalent price, use either the fair value of what is given up or the fair value of what is received, whichever is more clearly determinable.

For the cash equivalent price, use either the fair value of what is given up or the fair value of what is received, whichever is more clearly determinable.

Solution

Related exercise material: BE11-2, BE11-3, BE11-4, E11-3, E11-4, E11-8, and DO IT! 11-3.

![]()

![]() 3

3

Explain the accounting for treasury stock.

Accounting for Treasury Stock

Treasury stock is a corporation's own stock that it has issued and subsequently reacquired from shareholders but not retired. A corporation may acquire treasury stock for various reasons:

- To reissue the shares to officers and employees under bonus and stock compensation plans.

- To increase trading of the company's stock in the securities market. Companies expect that buying their own stock will signal that management believes the stock is underpriced, which they hope will enhance its market price.

- To have additional shares available for use in the acquisition of other companies.

- To reduce the number of shares outstanding and thereby increase earnings per share.

Helpful Hint

Treasury shares do not have dividend rights or voting rights.

Another infrequent reason for purchasing shares is that management may want to eliminate hostile shareholders by buying them out.

Many corporations have treasury stock. For example, approximately 68% of U.S. companies have treasury stock.3 In a recent year, Nike purchased more than 6 million treasury shares.

PURCHASE OF TREASURY STOCK

Companies generally account for treasury stock by the cost method. This method uses the cost of the shares purchased to value the treasury stock. Under the cost method, the company debits Treasury Stock for the price paid to reacquire the shares. When the company disposes of the shares, it credits to Treasury Stock the same amount it paid to reacquire the shares.

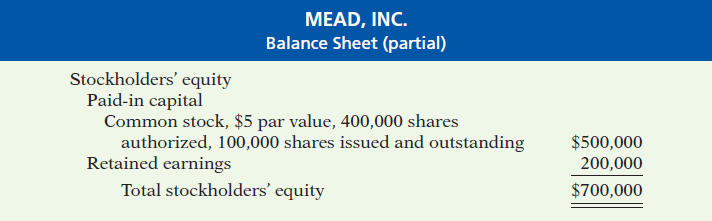

To illustrate, assume that on January 1, 2015, the stockholders' equity section of Mead, Inc. has 400,000 shares authorized and 100,000 shares of $5 par value common stock outstanding (all issued at par value) and Retained Earnings of $200,000. The stockholders' equity section before purchase of treasury stock is as follows.

Illustration 11-8

Stockholders' equity with no treasury stock

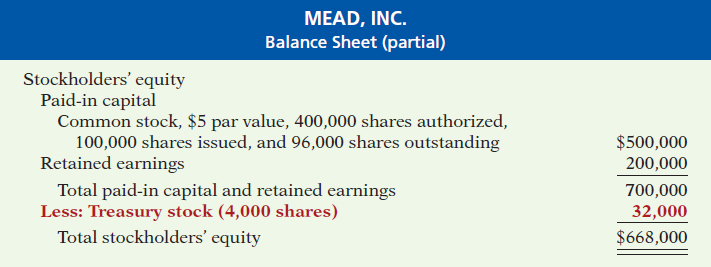

On February 1, 2015, Mead acquires 4,000 shares of its stock at $8 per share. The entry is:

Mead debits Treasury Stock for the cost of the shares purchased ($32,000). Is the original paid-in capital account, Common Stock, affected? No, because the number of issued shares does not change.

In the stockholders' equity section of the balance sheet, Mead deducts treasury stock from total paid-in capital and retained earnings. Treasury Stock is a contra stockholders' equity account. Thus, the acquisition of treasury stock reduces stockholders' equity. The stockholders' equity section of Mead, Inc. after purchase of treasury stock is as follows.

Illustration 11-9

Stockholders' equity with treasury stock

Mead discloses in the balance sheet both the number of shares issued (100,000) and the number in the treasury (4,000). The difference is the number of shares of stock outstanding (96,000). The term outstanding stock means the number of shares of issued stock that are being held by stockholders.

![]() Ethics Note

Ethics Note

The purchase of treasury stock reduces the cushion (cash available) for creditors and preferred stockholders. A restriction for the cost of treasury stock purchased is often required. The restriction is usually applied to retained earnings.

Some maintain that companies should report treasury stock as an asset because it can be sold for cash. But under this reasoning, companies would also show unissued stock as an asset, which is clearly incorrect. Rather than being an asset, treasury stock reduces stockholder claims on corporate assets. This effect is correctly shown by reporting treasury stock as a deduction from total paid-in capital and retained earnings.

ACCOUNTING ACROSS THE ORGANIZATION

Why Did Reebok Buy Its Own Stock?

In a bold (and some would say risky) move, Reebok at one time bought back nearly a third of its shares. This repurchase of shares dramatically reduced Reebok's available cash. In fact, the company borrowed significant funds to accomplish the repurchase. In a press release, management stated that it was repurchasing the shares because it believed its stock was severely underpriced. The repurchase of so many shares was meant to signal management's belief in good future earnings.

Skeptics, however, suggested that Reebok's management was repurchasing shares to make it less likely that another company would acquire Reebok (in which case Reebok's top managers would likely lose their jobs). By depleting its cash, Reebok became a less attractive acquisition target. Acquiring companies like to purchase companies with large cash balances so they can pay off debt used in the acquisition.

What signal might a large stock repurchase send to investors regarding management's belief about the company's growth opportunities? (See page 600.)

DISPOSAL OF TREASURY STOCK

Treasury stock is usually sold or retired. The accounting for its sale differs when treasury stock is sold above cost than when it is sold below cost.

SALE OF TREASURY STOCK ABOVE COST If the selling price of the treasury shares is equal to their cost, the company records the sale of the shares by a debit to Cash and a credit to Treasury Stock. When the selling price of the shares is greater than their cost, the company credits the difference to Paid-in Capital from Treasury Stock.

Helpful Hint

Treasury stock transactions are classified as capital stock transactions. As in the case when stock is issued, the income statement is not involved.

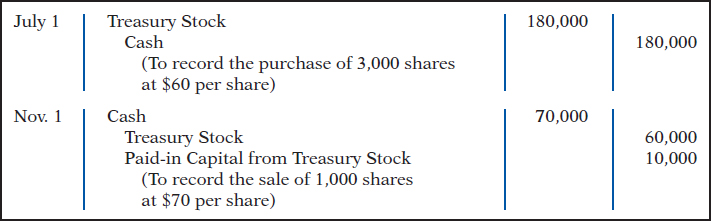

To illustrate, assume that on July 1, Mead, Inc. sells for $10 per share the 1,000 shares of its treasury stock previously acquired at $8 per share. The entry is as follows.

Mead does not record a $2,000 gain on sale of treasury stock because (1) gains on sales occur when assets are sold, and treasury stock is not an asset, and (2) a corporation does not realize a gain or suffer a loss from stock transactions with its own stockholders. Thus, companies should not include in net income any paid-in capital arising from the sale of treasury stock. Instead, they report Paid-in Capital from Treasury Stock separately on the balance sheet, as a part of paid-in capital.

SALE OF TREASURY STOCK BELOW COST When a company sells treasury stock below its cost, it usually debits to Paid-in Capital from Treasury Stock the excess of cost over selling price. Thus, if Mead, Inc. sells an additional 800 shares of treasury stock on October 1 at $7 per share, it makes the following entry.

Observe the following from the two sales entries. (1) Mead credits Treasury Stock at cost in each entry. (2) Mead uses Paid-in Capital from Treasury Stock for the difference between cost and the resale price of the shares. (3) The original paid-in capital account, Common Stock, is not affected. The sale of treasury stock increases both total assets and total stockholders' equity.

After posting the foregoing entries, the treasury stock accounts will show the following balances on October 1.

Illustration 11-10

Treasury stock accounts

When a company fully depletes the credit balance in Paid-in Capital from Treasury Stock, it debits to Retained Earnings any additional excess of cost over selling price. To illustrate, assume that Mead, Inc. sells its remaining 2,200 shares at $7 per share on December 1. The excess of cost over selling price is $2,200 [2,200 × ($8 − $7)]. In this case, Mead debits $1,200 of the excess to Paid-in Capital from Treasury Stock. It debits the remainder to Retained Earnings. The entry is:

> DO IT!

Treasury Stock

Santa Anita Inc. purchases 3,000 shares of its $50 par value common stock for $180,000 cash on July 1. It will hold the shares in the treasury until resold. On November 1, the corporation sells 1,000 shares of treasury stock for cash at $70 per share. Journalize the treasury stock transactions.

Action Plan

![]() Record the purchase of treasury stock at cost.

Record the purchase of treasury stock at cost.

![]() When treasury stock is sold above its cost, credit the excess of the selling price over cost to Paid-in Capital from Treasury Stock.

When treasury stock is sold above its cost, credit the excess of the selling price over cost to Paid-in Capital from Treasury Stock.

![]() When treasury stock is sold below its cost, debit the excess of cost over selling price to Paid-in Capital from Treasury Stock.

When treasury stock is sold below its cost, debit the excess of cost over selling price to Paid-in Capital from Treasury Stock.

Solution

Related exercise material: BE11-5, E11-5, E11-7, E11-9, and DO IT! 11-4.

![]()

![]() 4

4

Differentiate preferred stock from common stock.

Accounting for Preferred Stock

To appeal to a larger segment of potential investors, a corporation may issue an additional class of stock, called preferred stock. Preferred stock has contractual provisions that give it some preference or priority over common stock. Typically, preferred stockholders have a priority as to (1) distributions of earnings (dividends) and (2) assets in the event of liquidation. However, they generally do not have voting rights.

Like common stock, corporations may issue preferred stock for cash or for non-cash assets. The entries for these transactions are similar to the entries for common stock. When a corporation has more than one class of stock, each paid-in capital account title should identify the stock to which it relates. A company might have the following accounts: Preferred Stock, Common Stock, Paid-in Capital in Excess of Par—Preferred Stock, and Paid-in Capital in Excess of Par—Common Stock.

For example, if Stine Corporation issues 10,000 shares of $10 par value preferred stock for $12 cash per share, the entry to record the issuance is:

Preferred stock may have either a par value or no-par value. In the stockholders' equity section of the balance sheet, companies list preferred stock first because of its dividend and liquidation preferences over common stock.

DIVIDEND PREFERENCES

As indicated above, preferred stockholders have the right to receive dividends before common stockholders. For example, if the dividend rate on preferred stock is $5 per share, common shareholders will not receive any dividends in the current year until preferred stockholders have received $5 per share. The first claim to dividends does not, however, guarantee the payment of dividends. Dividends depend on many factors, such as adequate retained earnings and availability of cash. If a company does not pay dividends to preferred stockholders, it cannot of course pay dividends to common stockholders.

For preferred stock, companies state the per share dividend amount as a percentage of the par value or as a specified amount. For example, Earthlink specifies a 3% dividend on its $100 par value preferred. PepsiCo pays $4.56 per share on its no-par value stock.

CUMULATIVE DIVIDEND Preferred stock often contains a cumulative dividend feature. This right means that preferred stockholders must be paid both current-year dividends and any unpaid prior-year dividends before common stockholders receive dividends. When preferred stock is cumulative, preferred dividends not declared in a given period are called dividends in arrears.

To illustrate, assume that Scientific Leasing has 5,000 shares of 7%, $100 par value, cumulative preferred stock outstanding. Each $100 share pays a $7 dividend (.07 × $100). The annual dividend is $35,000 (5,000 × $7 per share). If dividends are two years in arrears, preferred stockholders are entitled to receive the following dividends in the current year.

Illustration 11-11

Computation of total dividends to preferred stock

The company cannot pay dividends to common stockholders until it pays the entire preferred dividend. In other words, companies cannot pay dividends to common stockholders while any preferred dividends are in arrears.

Are dividends in arrears considered a liability? No—no payment obligation exists until the board of directors declares a dividend. However, companies should disclose in the notes to the financial statements the amount of dividends in arrears. Doing so enables investors to assess the potential impact of this commitment on the corporation's financial position.

The investment community does not look favorably on companies that are unable to meet their dividend obligations. As a financial officer noted in discussing one company's failure to pay its cumulative preferred dividend for a period of time, “Not meeting your obligations on something like that is a major black mark on your record.” The accounting entries for preferred stock dividends are explained later in this chapter.

LIQUIDATION PREFERENCE

Most preferred stocks also have a preference on corporate assets if the corporation fails. This feature provides security for the preferred stockholder. The preference to assets may be for the par value of the shares or for a specified liquidating value. For example, Commonwealth Edison's preferred stock entitles its holders to receive $31.80 per share, plus accrued and unpaid dividends, in the event of liquidation. The liquidation preference establishes the respective claims of creditors and preferred stockholders in litigation involving bankruptcy lawsuits.

![]() 5

5

Prepare the entries for cash dividends and stock dividends.

Dividends

A dividend is a corporation's distribution of cash or stock to its stockholders on a pro rata (proportional to ownership) basis. Pro rata means that if you own 10% of the common shares, you will receive 10% of the dividend. Dividends can take four forms: cash, property, scrip (a promissory note to pay cash), or stock. Cash dividends predominate in practice. Also, companies declare stock dividends with some frequency. These two forms of dividends are the focus of discussion in this chapter.

Investors are very interested in a company's dividend practices. In the financial press, dividends are generally reported quarterly as a dollar amount per share. (Sometimes they are reported on an annual basis.) For example, Nike's quarterly dividend rate in the fourth quarter of 2012 was 21 cents per share. The dividend rate for the fourth quarter of 2012 for GE was 19 cents, and for ConAgra Foods it was 25 cents.

Cash Dividends

A cash dividend is a pro rata distribution of cash to stockholders. Cash dividends are not paid on treasury shares. For a corporation to pay a cash dividend, it must have the following.

- Retained earnings. The legality of a cash dividend depends on the laws of the state in which the company is incorporated. Payment of cash dividends from retained earnings is legal in all states. In general, cash dividend distributions from only the balance in common stock (legal capital) are illegal.

A dividend declared out of paid-in capital is termed a liquidating dividend. Such a dividend reduces or “liquidates” the amount originally paid in by stockholders. Statutes vary considerably with respect to cash dividends based on paid-in capital in excess of par or stated value. Many states permit such dividends.

- Adequate cash. The legality of a dividend and the ability to pay a dividend are two different things. For example, Nike, with retained earnings of over $5.8 billion, could legally declare a dividend of at least $5.8 billion. But Nike's cash balance is only $1.9 billion.

Before declaring a cash dividend, a company's board of directors must carefully consider both current and future demands on the company's cash resources. In some cases, current liabilities may make a cash dividend inappropriate. In other cases, a major plant expansion program may warrant only a relatively small dividend.

- Declared dividends. A company does not pay dividends unless its board of directors decides to do so, at which point the board “declares” the dividend. The board of directors has full authority to determine the amount of income to distribute in the form of a dividend and the amount to retain in the business. Dividends do not accrue like interest on a note payable, and they are not a liability until declared.

The amount and timing of a dividend are important issues for management to consider. The payment of a large cash dividend could lead to liquidity problems for the company. On the other hand, a small dividend or a missed dividend may cause unhappiness among stockholders. Many stockholders expect to receive a reasonable cash payment from the company on a periodic basis. Many companies declare and pay cash dividends quarterly. On the other hand, a number of high-growth companies pay no dividends, preferring to conserve cash to finance future capital expenditures.

ENTRIES FOR CASH DIVIDENDS

Three dates are important in connection with dividends: (1) the declaration date, (2) the record date, and (3) the payment date. Normally, there are two to four weeks between each date. Companies make accounting entries on the declaration date and the payment date.

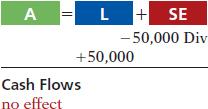

On the declaration date, the board of directors formally declares (authorizes) the cash dividend and announces it to stockholders. The declaration of a cash dividend commits the corporation to a legal obligation. The company must make an entry to recognize the increase in Cash Dividends and the increase in the liability Dividends Payable.

To illustrate, assume that on December 1, 2015, the directors of Media General declare a 50 cents per share cash dividend on 100,000 shares of $10 par value common stock. The dividend is $50,000 (100,000 × $0.50). The entry to record the declaration is:

Media General debits the account Cash Dividends. Cash dividends decrease retained earnings. We use the specific title Cash Dividends to differentiate it from other types of dividends, such as stock dividends. Dividends Payable is a current liability. It will normally be paid within the next several months. When using a Cash Dividends account, the company transfers the balance of that account to Retained Earnings at the end of the year by a closing entry. For homework problems, you should use the Cash Dividends account for recording dividend declarations.

At the record date, the company determines ownership of the outstanding shares for dividend purposes. The stockholders' records maintained by the corporation supply this information. In the interval between the declaration date and the record date, the corporation updates its stock ownership records. For Media General, the record date is December 22. No entry is required on this date because the corporation's liability recognized on the declaration date is unchanged.

Helpful Hint

The purpose of the record date is to identify the persons or entities that will receive the dividend, not to determine the amount of the dividend liability.

![]()

On the payment date, the company makes cash dividend payments to the stockholders of record (as of December 22) and records the payment of the dividend. If January 20 is the payment date for Media General, the entry on that date is:

Note that payment of the dividend reduces both current assets and current liabilities. It has no effect on stockholders' equity. The cumulative effect of the declaration and payment of a cash dividend is to decrease both stockholders' equity and total assets. Illustration 11-12 (page 564) summarizes the three important dates associated with dividends for Media General.

Illustration 11-12

Key dividend dates

ALLOCATING CASH DIVIDENDS BETWEEN PREFERRED AND COMMON STOCK

As explained earlier in the chapter, preferred stock has priority over common stock in regard to dividends. Holders of cumulative preferred stock must be paid any unpaid prior-year dividends and their current year's dividend before common stockholders receive dividends.

To illustrate, assume that at December 31, 2015, IBR Inc. has 1,000 shares of 8%, $100 par value cumulative preferred stock. It also has 50,000 shares of $10 par value common stock outstanding. The dividend per share for preferred stock is $8 ($100 par value × 8%). The required annual dividend for preferred stock is therefore $8,000 (1,000 shares × $8). At December 31, 2015, the directors declare a $6,000 cash dividend. In this case, the entire dividend amount goes to preferred stockholders because of their dividend preference. The entry to record the declaration of the dividend is:

Because of the cumulative feature, dividends of $2 ($8 − $6) per share are in arrears on preferred stock for 2015. IBR must pay these dividends to preferred stockholders before it can pay any future dividends to common stockholders. IBR should disclose dividends in arrears in the financial statements.

At December 31, 2016, IBR declares a $50,000 cash dividend. The allocation of the dividend to the two classes of stock is as follows.

Illustration 11-13

Allocating dividends to preferred and common stock

The entry to record the declaration of the dividend is:

If IBR's preferred stock is not cumulative, preferred stockholders receive only $8,000 in dividends in 2016. Common stockholders receive $42,000.

> DO IT!

Dividends on Preferred and Common Stock

MasterMind Corporation has 2,000 shares of 6%, $100 par value preferred stock outstanding at December 31, 2015. At December 31, 2015, the company declared a $60,000 cash dividend. Determine the dividend paid to preferred stockholders and common stockholders under each of the following scenarios.

- The preferred stock is noncumulative, and the company has not missed any dividends in previous years.

- The preferred stock is noncumulative, and the company did not pay a dividend in each of the two previous years.

- The preferred stock is cumulative, and the company did not pay a dividend in each of the two previous years.

Action Plan

![]() Determine dividends on preferred shares by multiplying the dividend rate times the par value of the stock times the number of preferred shares.

Determine dividends on preferred shares by multiplying the dividend rate times the par value of the stock times the number of preferred shares.

![]() Understand the cumulative feature. If preferred stock is cumulative, then any missed dividends (dividends in arrears) and the current year's dividend must be paid to preferred stockholders before dividends are paid to common stockholders.

Understand the cumulative feature. If preferred stock is cumulative, then any missed dividends (dividends in arrears) and the current year's dividend must be paid to preferred stockholders before dividends are paid to common stockholders.

Solution

- The company has not missed past dividends and the preferred stock is noncumulative. Thus, the preferred stockholders are paid only this year's dividend. The dividend paid to preferred stockholders would be $12,000 (2,000 × .06 × $100). The dividend paid to common stockholders would be $48,000 ($60,000 − $12,000).

- The preferred stock is noncumulative. Thus, past unpaid dividends do not have to be paid. The dividend paid to preferred stockholders would be $12,000 (2,000 × .06 × $100). The dividend paid to common stockholders would be $48,000 ($60,000 − $12,000).

- The preferred stock is cumulative. Thus, dividends that have been missed (dividends in arrears) must be paid. The dividend paid to preferred stockholders would be $36,000 (3 × 2,000 × .06 × $100). The dividend paid to common stockholders would be $24,000 ($60,000 − $36,000).

Related exercise material: BE11-7, E11-6, E11-13, and DO IT! 11-5.

![]()

Stock Dividends

A stock dividend is a pro rata (proportional to ownership) distribution of the corporation's own stock to stockholders. Whereas a company pays cash in a cash dividend, a company issues shares of stock in a stock dividend. A stock dividend results in a decrease in retained earnings and an increase in paid-in capital. Unlike a cash dividend, a stock dividend does not decrease total stockholders' equity or total assets.

To illustrate, assume that you have a 2% ownership interest in Cetus Inc. That is, you own 20 of its 1,000 shares of common stock. If Cetus declares a 10% stock dividend, it would issue 100 shares (1,000 × 10%) of stock. You would receive two shares (2% × 100). Would your ownership interest change? No, it would remain at 2% (22 ÷ 1,100). You now own more shares of stock, but your ownership interest has not changed.

Cetus has disbursed no cash and has assumed no liabilities. What, then, are the purposes and benefits of a stock dividend? Corporations issue stock dividends generally for one or more of the following reasons.

- To satisfy stockholders' dividend expectations without spending cash.

- To increase the marketability of the corporation's stock. When the number of shares outstanding increases, the market price per share decreases. Decreasing the market price of the stock makes it easier for smaller investors to purchase the shares.

- To emphasize that a company has permanently reinvested in the business a portion of stockholders' equity, which therefore is unavailable for cash dividends.

When the dividend is declared, the board of directors determines the size of the stock dividend and the value assigned to each dividend.

Generally, if the company issues a small stock dividend (less than 20–25% of the corporation's issued stock), the value assigned to the dividend is the fair value per share. This treatment is based on the assumption that a small stock dividend will have little effect on the market price of the shares previously outstanding. Thus, many stockholders consider small stock dividends to be distributions of earnings equal to the market price of the shares distributed. If a company issues a large stock dividend (greater than 20–25%), the price assigned to the dividend is the par or stated value. Small stock dividends predominate in practice. Thus, we will illustrate only entries for small stock dividends.

ENTRIES FOR STOCK DIVIDENDS

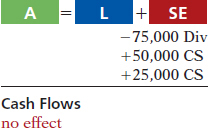

To illustrate the accounting for small stock dividends, assume that Medland Corporation has a balance of $300,000 in retained earnings. It declares a 10% stock dividend on its 50,000 shares of $10 par value common stock. The current market price of its stock is $15 per share. The number of shares to be issued is 5,000 (10% × 50,000). Therefore, the total amount to be debited to Stock Dividends is $75,000 (5,000 × $15). The entry to record the declaration of the stock dividend is as follows.

Medland debits Stock Dividends for the market price of the stock issued ($15 × 5,000). (Similar to Cash Dividends, Stock Dividends decrease retained earnings.) Medland also credits Common Stock Dividends Distributable for the par value of the dividend shares ($10 × 5,000) and credits Paid-in Capital in Excess of Par—Common Stock for the excess of the market price over par ($5 × 5,000).

Common Stock Dividends Distributable is a stockholders' equity account. It is not a liability because assets will not be used to pay the dividend. If the company prepares a balance sheet before it issues the dividend shares, it reports the distributable account under paid-in capital as shown in Illustration 11-14.

Illustration 11-14

Statement presentation of common stock dividends distributable

When Medland issues the dividend shares, it debits Common Stock Dividends Distributable and credits Common Stock, as follows.

EFFECTS OF STOCK DIVIDENDS

How do stock dividends affect stockholders' equity? They change the composition of stockholders' equity because they transfer to paid-in capital a portion of retained earnings. However, total stockholders' equity remains the same. Stock dividends also have no effect on the par or stated value per share. But, the number of shares outstanding increases. Illustration 11-15 shows these effects for Medland Corporation.

Illustration 11-15

Stock dividend effects

In this example, total paid-in capital increases by $75,000 (50,000 shares × 10% × $15) and retained earnings decreases by the same amount. Note also that total stockholders' equity remains unchanged at $800,000. The number of shares increases by 5,000 (50,000 × 10%).

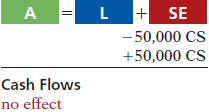

Stock Splits

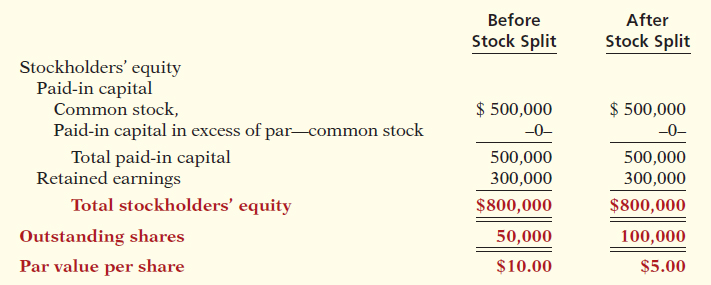

A stock split, like a stock dividend, involves issuance of additional shares to stockholders according to their percentage ownership. However, a stock split results in a reduction in the par or stated value per share. The purpose of a stock split is to increase the marketability of the stock by lowering its market price per share. This, in turn, makes it easier for the corporation to issue additional stock.

Helpful Hint

A stock split changes the par value per share but does not affect any balances in stockholders' equity.

The effect of a split on market price is generally inversely proportional to the size of the split. For example, after a 2-for-1 stock split, the market price of Nike's stock fell from $111 to approximately $55. The lower market price stimulated market activity. Within one year, the stock was trading above $100 again. Illustration 11-16 shows the effect of a 4-for-1 stock split for stockholders.

Illustration 11-16

Effect of stock split for stockholders

In a stock split, the number of shares increases in the same proportion that par or stated value per share decreases. For example, in a 2-for-1 split, one share of $10 par value stock is exchanged for two shares of $5 par value stock. A stock split does not have any effect on total paid-in capital, retained earnings, or total stockholders' equity. But, the number of shares outstanding increases, and par value per share decreases. Illustration 11-17 shows these effects for Medland Corporation, assuming that it splits its 50,000 shares of common stock on a 2-for-1 basis.

Illustration 11-17

Stock split effects

A stock split does not affect the balances in any stockholders' equity accounts. Therefore, it is not necessary to journalize a stock split.

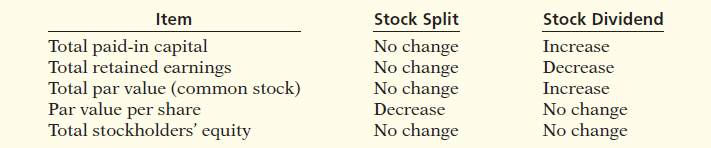

Illustration 11-18 summarizes the differences between stock splits and stock dividends.

Illustration 11-18

Differences between the effects of stock splits and stock dividends

INVESTOR INSIGHT

A No-Split Philosophy

Warren Buffett's company, Berkshire Hathaway, has two classes of shares. Until recently, the company had never split either class of stock. As a result, the class A stock had a market price of $97,000 and the class B sold for about $3,200 per share. Because the price per share is so high, the stock does not trade as frequently as the stock of other companies. Buffett has always opposed stock splits because he feels that a lower stock price attracts short-term investors. He appears to be correct. For example, while more than 6 million shares of IBM are exchanged on the average day, only about 1,000 class A shares of Berkshire are traded. Despite Buffett's aversion to splits, in order to accomplish a recent acquisition, Berkshire decided to split its class B shares 50 to 1.

Source: Scott Patterson, “Berkshire Nears Smaller Baby B's,” Wall Street Journal Online (January 19, 2010).

Why does Warren Buffett usually oppose stock splits? (See page 600.)

Stock Dividends and Stock Splits

Sing CD Company has had five years of record earnings. Due to this success, the market price of its 500,000 shares of $2 par value common stock has tripled from $15 per share to $45. During this period, paid-in capital remained the same at $2,000,000. Retained earnings increased from $1,500,000 to $10,000,000. President Joan Elbert is considering either a 10% stock dividend or a 2-for-1 stock split. She asks you to show the before-and-after effects of each option on retained earnings and total stockholders' equity.

Action Plan

![]() Calculate the stock dividend's effect on retained earnings by multiplying the number of new shares times the market price of the stock (or par value for a large stock dividend).

Calculate the stock dividend's effect on retained earnings by multiplying the number of new shares times the market price of the stock (or par value for a large stock dividend).

![]() Recall that a stock dividend increases the number of shares without affecting total stockholders' equity.

Recall that a stock dividend increases the number of shares without affecting total stockholders' equity.

![]() Recall that a stock split only increases the number of shares outstanding and decreases the par value per share.

Recall that a stock split only increases the number of shares outstanding and decreases the par value per share.

Solution

The stock dividend amount is $2,250,000 [(500,000 × 10%) × $45]. The new balance in retained earnings is $7,750,000 ($10,000,000 − $2,250,000). The retained earnings balance after the stock split is the same as it was before the split: $10,000,000. Total stockholders' equity does not change. The effects on the stockholders' equity accounts are as follows.

Related exercise material: BE11-8, BE11-9, E11-14, E11-15, and DO IT! 11-6.

![]()

![]() 6

6

Identify the items reported in a retained earnings statement.

Retained Earnings

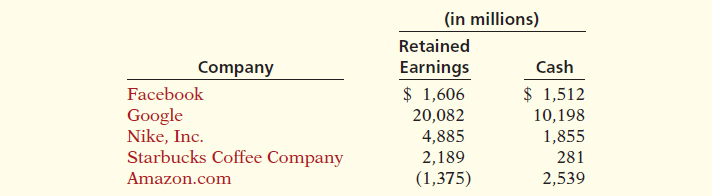

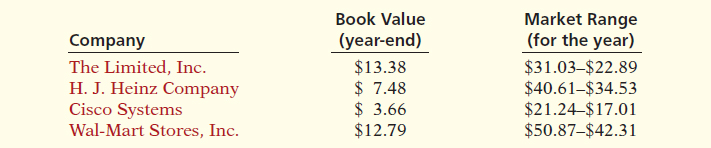

Recall that retained earnings is net income that a company retains in the business. The balance in retained earnings is part of the stockholders' claim on the total assets of the corporation. It does not, though, represent a claim on any specific asset. Nor can the amount of retained earnings be associated with the balance of any asset account. For example, a $100,000 balance in retained earnings does not mean that there should be $100,000 in cash. The reason is that the company may have used the cash resulting from the excess of revenues over expenses to purchase buildings, equipment, and other assets.

To demonstrate that retained earnings and cash may be quite different, Illustration 11-19 shows recent amounts of retained earnings and cash in selected companies.

Illustration 11-19

Retained earnings and cash balances

Remember that when a company has net income, it closes net income to retained earnings. The closing entry is a debit to Income Summary and a credit to Retained Earnings.

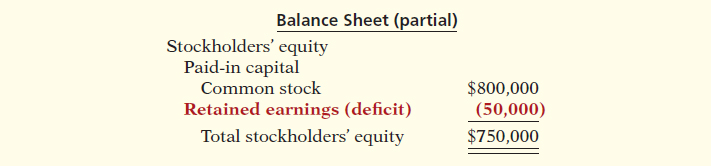

When a company has a net loss (expenses exceed revenues), it also closes this amount to retained earnings. The closing entry in this case is a debit to Retained Earnings and a credit to Income Summary. This is done even if it results in a debit balance in Retained Earnings. Companies do not debit net losses to paid-in capital accounts. To do so would destroy the distinction between paid-in and earned capital. If cumulative losses exceed cumulative income over a company's life, a debit balance in Retained Earnings results. A debit balance in Retained Earnings is identified as a deficit. A company reports a deficit as a deduction in the stockholders' equity section, as shown below.

Helpful Hint

Remember that Retained Earnings is a stockholders' equity account, whose normal balance is a credit.

Illustration 11-20

Stockholders' equity with deficit

Retained Earnings Restrictions

The balance in retained earnings is generally available for dividend declarations. Some companies state this fact. For example, Lockheed Martin Corporation states the following in the notes to its financial statements.

Illustration 11-21

Disclosure of unrestricted retained earnings

In some cases, there may be retained earnings restrictions. These make a portion of the retained earnings balance currently unavailable for dividends. Restrictions result from one or more of the following causes.

- Legal restrictions. Many states require a corporation to restrict retained earnings for the cost of treasury stock purchased. The restriction keeps intact the corporation's legal capital that is being temporarily held as treasury stock. When the company sells the treasury stock, the restriction is lifted.

- Contractual restrictions. Long-term debt contracts may restrict retained earnings as a condition for the loan. The restriction limits the use of corporate assets for payment of dividends. Thus, it increases the likelihood that the corporation will be able to meet required loan payments.

- Voluntary restrictions. The board of directors may voluntarily create retained earnings restrictions for specific purposes. For example, the board may authorize a restriction for future plant expansion. By reducing the amount of retained earnings available for dividends, the company makes more cash available for the planned expansion.

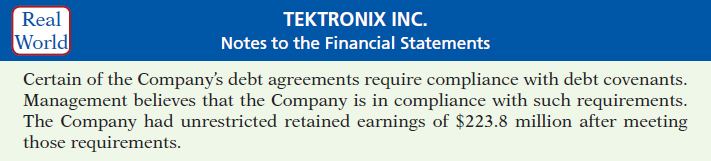

Companies generally disclose retained earnings restrictions in the notes to the financial statements. For example, as shown in Illustration 11-22, Tektronix Inc., a manufacturer of electronic measurement devices, had total retained earnings of $774 million, but the unrestricted portion was only $223.8 million.

Illustration 11-22

Disclosure of restriction

Prior Period Adjustments

Suppose that a corporation has closed its books and issued financial statements. The corporation then discovers that it made a material error in reporting net income of a prior year. How should the company record this situation in the accounts and report it in the financial statements?

The correction of an error in previously issued financial statements is known as a prior period adjustment. The company makes the correction directly to Retained Earnings because the effect of the error is now in this account. The net income for the prior period has been recorded in retained earnings through the journalizing and posting of closing entries.

To illustrate, assume that General Microwave discovers in 2015 that it understated depreciation expense on equipment in 2014 by $300,000 due to computational errors. These errors overstated both net income for 2014 and the current balance in retained earnings. The entry for the prior period adjustment, ignoring all tax effects, is as follows.

A debit to an income statement account in 2015 is incorrect because the error pertains to a prior year.

Companies report prior period adjustments in the retained earnings statement.4 They add (or deduct, as the case may be) these adjustments from the beginning retained earnings balance. This results in an adjusted beginning balance. For example, assuming a beginning balance of $800,000 in retained earnings, General Microwave reports the prior period adjustment as follows.

Illustration 11-23

Statement presentation of prior period adjustments

Again, reporting the correction in the current year's income statement would be incorrect because it applies to a prior year's income statement.

Retained Earnings Statement

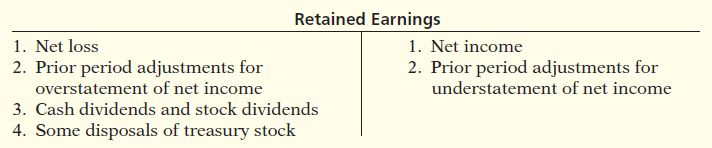

The retained earnings statement shows the changes in retained earnings during the year. The company prepares the statement from the Retained Earnings account. Illustration 11-24 shows (in T-account form) transactions that affect retained earnings.

Illustration 11-24

Debits and credits to retained earnings

As indicated, net income increases retained earnings, and a net loss decreases retained earnings. Prior period adjustments may either increase or decrease retained earnings. Both cash dividends and stock dividends decrease retained earnings. The circumstances under which treasury stock transactions decrease retained earnings are explained on page 559.

A complete retained earnings statement for Graber Inc., based on assumed data, is as follows.

Illustration 11-25

Retained earnings statement

> DO IT!

Retained Earnings Statement

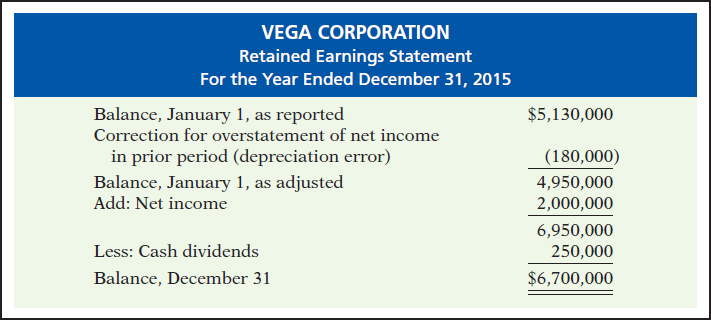

Vega Corporation has retained earnings of $5,130,000 on January 1, 2015. During the year, Vega earned $2,000,000 of net income. It declared and paid a $250,000 cash dividend. In 2015, Vega recorded an adjustment of $180,000 due to the understatement (from a mathematical error) of 2014 depreciation expense. Prepare a retained earnings statement for 2015.

Action Plan

![]() Recall that a retained earnings statement begins with retained earnings, as reported at the end of the previous year.

Recall that a retained earnings statement begins with retained earnings, as reported at the end of the previous year.

![]() Add or subtract any prior period adjustments to arrive at the adjusted beginning figure.

Add or subtract any prior period adjustments to arrive at the adjusted beginning figure.

![]() Add net income and subtract dividends declared to arrive at the ending balance in retained earnings.

Add net income and subtract dividends declared to arrive at the ending balance in retained earnings.

Solution

Related exercise material: BE11-10, BE11-11, BE11-12, E11-17, E11-18, and DO IT! 11-7.

![]()

![]() 7

7

Prepare and analyze a comprehensive stockholders' equity section.

Statement Presentation and Analysis

In the stockholders' equity section of the balance sheet, paid-in capital and retained earnings are reported. The specific sources of paid-in capital are identified. Within paid-in capital, two classifications are recognized:

- Capital stock. This category consists of preferred and common stock. Preferred stock is shown before common stock because of its preferential rights. Par value, shares authorized, shares issued, and shares outstanding are reported for each class of stock.

- Additional paid-in capital. This includes the excess of amounts paid over par or stated value and paid-in capital from treasury stock.

Presentation

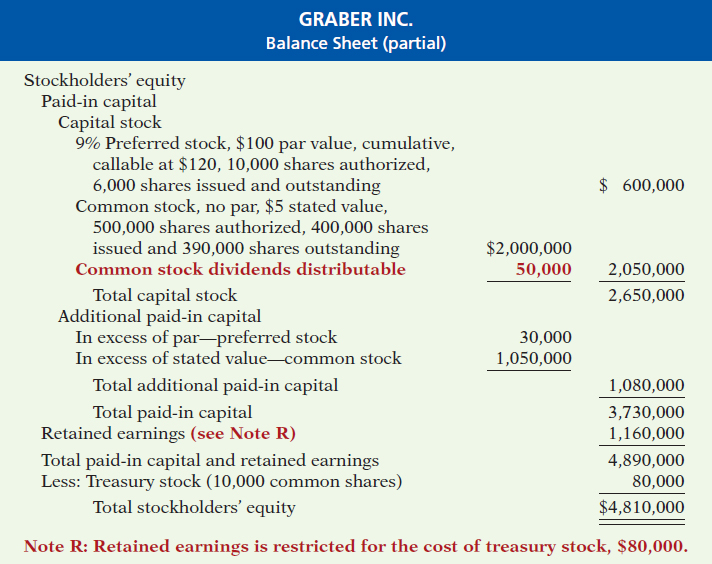

Illustration 11-26 presents the stockholders' equity section of Graber Inc.'s balance sheet. Note the following: (1) “Common stock dividends distributable” is shown under “Capital stock,” in “Paid-in capital.” (2) A note (Note R) discloses a retained earnings restriction.

Illustration 11-26

Comprehensive stockholders' equity section