To calculate the ATR, perform the following steps:

- The ATR is based on the low and high price of

Ndays, usually the last 20 days.N = 5 h = h[-N:] l = l[-N:]

- We also need to know the close price of the previous day:

previousclose = c[-N -1: -1]

For each day, we calculate the following:

The daily range—the difference between the high and low price:

h – lThe difference between the high and previous close:

h – previouscloseThe difference between the previous close and the low price:

previousclose – l - The

max()function returns the maximum of an array. Based on those three values, we calculate the so-called true range, which is the maximum of these values. We are now interested in the element-wise maxima across arrays—meaning the maxima of the first elements in the arrays, the second elements in the arrays, and so on. Use the NumPymaximum()function instead of themax()function for this purpose:truerange = np.maximum(h - l, h - previousclose, previousclose - l)

- Create an

atrarray of sizeNand initialize its values to0:atr = np.zeros(N)

- The first value of the array is just the average of the

truerangearray:atr[0] = np.mean(truerange)

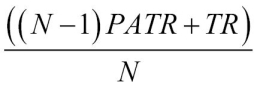

Calculate the other values with the following formula:

Here, PATR is the previous day's ATR; TR is the true range:

for i in range(1, N): atr[i] = (N - 1) * atr[i - 1] + truerange[i] atr[i] /= N

We formed three arrays, one for each of the three ranges—daily range, the gap between the high of today and the close of yesterday, and the gap between the close of yesterday and the low of today. This tells us how much the stock price moved and, therefore, how volatile it is. The algorithm requires us to find the maximum value for each day. The max() function that we used before can give us the maximum value within an array, but that is not what we want here. We need the maximum value across arrays, so we want the maximum value of the first elements in the three arrays, the second elements, and so on. In preceding Time for action section, we saw that the maximum() function can do this. After this, we computed a moving average of the true range values (see atr.py):

from __future__ import print_function

import numpy as np

h, l, c = np.loadtxt('data.csv', delimiter=',', usecols=(4, 5, 6), unpack=True)

N = 5

h = h[-N:]

l = l[-N:]

print("len(h)", len(h), "len(l)", len(l))

print("Close", c)

previousclose = c[-N -1: -1]

print("len(previousclose)", len(previousclose))

print("Previous close", previousclose)

truerange = np.maximum(h - l, h - previousclose, previousclose - l)

print("True range", truerange)

atr = np.zeros(N)

atr[0] = np.mean(truerange)

for i in range(1, N):

atr[i] = (N - 1) * atr[i - 1] + truerange[i]

atr[i] /= N

print("ATR", atr)In the following sections, we will learn better ways to calculate moving averages.