Case 3 ‘Take Customer Cash to Survive?’ Compliance and Chaos at MF Global

The trades are safe. Europe will pay its debts. – Jon Corzine “Imagine you had your life savings in your bank account, your bank committed fraud, and as a result you could not touch your money” – former MF Global customer

THE ROOF WAS STARTING TO CAVE IN. It felt like that to Edith O’Brien, Assistant Treasurer of MF Global International (MFGI). It was October 28, 2011. MFGI and its holding company had just been downgraded to “junk status” by all three rating agencies, Moody’s, S&P and Fitch. The downgrades and other adverse events had set off a liquidity crisis. MFGI was being hit by a cascade of margin calls on positions it had taken in risky European Sovereign Debt. J.P. Morgan, MFGI’s “clearing bank,” had just advised it was cancelling all intraday credit lines. MF Global UK (MF UK) had overdrawn several of these lines, prompting the move.1 Now, a new crisis was at hand. O’Brien looked at a set of wire instructions sitting on her desk. The first wire would transfer $200M from segregated customer accounts at MFGI to MF UK. The second would fund an MF UK account at J.P. Morgan, remedying the Morgan bank overdrafts. These wires had been composed in response to a message received by MFGI CEO Jon Corzine that the J.P. Morgan overdraft situation was “HOLDING UP VITAL BUSINESS IN THE U.S. AS A RESULT.” Corzine had then contacted O’Brien’s office and asked them to resolve the Morgan overdraft problem urgently.2

Segregated accounts are a distinctive feature of the broker/dealer business. MFGI, acting as a broker/dealer, received cash from clients in anticipation of trades they would later make. Thus, segregated account cash is cash that belongs to customers. MFGI is legally constrained from using client cash for its own purposes, and as a manifestation of such limits, is required at the end of each day to assure that “seg account” cash matched the cash clients had left un-invested. Within MFGI, this was known as verifying the “Seg Account Balance.”

Edith O’Brien had good reason to be worried about sending the new wires. Compliance reports for the previous two days indicated that MFGI had used client funds to meet its own pressing liquidity needs. Internally, confusion reigned. The Financial Regulatory Group was convinced MFGI had overdrawn the client accounts. Treasury believed an accounting error was responsible for this result and that client accounts were properly funded. No one was certain of the actual situation. MFGI routinely used client funds during intraday trading/operations with the intention of “squaring up” at day’s end. However, the firm lacked the systems to monitor client positions throughout the day. This meant that as of mid-day October 28, O’Brien was flying blind as to the actual situation. All she knew was that CEO Jon Corzine was pressing for a resolution of London’s overdraft situation. O’Brien saw only one way to resolve that issue quickly—send the two wires sitting on her desk.

Should she send out the wires? Not sending them could propel the firm into a death spiral, as counterparties ceased doing business and refused to roll over repo financings. Sending the wires involved personal risk for O’Brien. If MFGI was using client funds to pay the firm’s debts, it would be engaging in illegal, fraudulent activity—and O’Brien’s name would be all over the paper trail.

Edith O’Brien decided to review the previous weeks’ hectic activity before deciding a course of action.

Client Protections and Segregated Accounts

Broker/Dealers (B/Ds) are prime players in U.S. capital markets. Typically, these firms arrange buy or sell transactions for clients. They also assist the orderly functioning of the capital markets by holding inventories and making markets in securities. As such, broker/dealers have long played a major role in setting and adjusting security prices.

Many clients operate through one or a limited number of broker/dealers. Clients use these firms to execute transactions and to hold purchased securities on their behalf. To facilitate trading, clients leave cash balances in their broker accounts. This practice creates a controls challenge for the broker/dealer. In theory, client cash and securities should not be commingled with the firm’s assets. In practice, broker/dealers frequently use client cash and securities. Clients sometimes allow brokers to borrow securities for “shorting” transactions, i.e., the firm sells a borrowed security in the expectation of buying it back and replacing it in the client’s account at a later date. Brokers also routinely borrow clients’ cash for intraday transactions. Broker/dealers typically have control systems to report how much money must be restored to client “segregated accounts” at day’s end.

These practices present no problem so long as the broker/dealer is solvent. However, if a broker/dealer bets its own capital and sustains losses, it may be challenged to restore the client account balances. Such events can ultimately result in clients losing cash or suffering losses that did not result from their own trading. Past history showed how this could happen. Broker/dealer activity expanded dramatically during the 1960s as mutual funds gained popularity. Then a recession hit in 1969–70, and numerous B/Ds consolidated or went through bankruptcy. Clients lost cash and securities or endured significant waits until their account balances were restored via the bankruptcy process.3

These events triggered demands for reform. Congress responded with the Securities Investor Protection Act (SIPA). This law upgraded the financial responsibility required of broker/dealers. SIPA empowered the Securities and Exchange Commission (SEC) to demand information from broker/dealers regarding their protection of customer accounts. The SEC could also impose penalties for fraud or withholding information. Finally, SIPA established the Securities Investor Protection Corporation (SIPC). This non-profit entity collects insurance premiums from member B/Ds and then affords clients a faster and more complete restoration in the event that their broker/dealer should fail.4

Shortly after the SIPC was formed, exchange trading of futures and options accelerated. Formerly sedate markets for agricultural and mineral commodities became homes of intensive speculation. Derivative securities, i.e., securities whose value referenced the price of an underlying commodity, achieved enormous trading volumes on the Chicago Board Options Exchange (CBOE) and the New York Mercantile Exchange (NYMEX). This growth led Congress to pass the Commodities Exchange Act in 1974. That Act set up the Commodity Futures Trading Commission (CFTC) and empowered it to regulate the clearing of trades on the nation’s commodity exchanges.5

Because of their familiarity with futures and options contracts, commodity exchanges later expanded into financial derivatives. Thus, contracts involving interest rates and currencies came to be traded alongside wheat and oil futures. The exchanges determined which firms were allowed to join as members and provided members with the assurance that the exchange would stand behind their trade settlements. This meant that if an individual firm failed to settle an open transaction, it would be resolved by the exchange.

Modeled in part on the Securities and Exchange Commission, the CFTC was empowered to oversee all U.S. commodity exchanges, assure the integrity of clearing processes, and prevent market manipulation. With the expansion of futures and options trading during the 1980–90s, the CFTC found itself monitoring vast positions in U.S. and foreign government securities, currency and interest rate swaps, and an expanded set of commodities that now included oil and natural gas.

The net result of this history is that broker/dealers like MFGI are highly regulated. If publicly traded, they answer to both their stock exchange and the SEC. As commodity B/Ds they are supervised by their commodity exchange and the CFTC. Within this web, there is no doubt that B/Ds are supposed to segregate client funds and not violate this segregation to solve a liquidity crunch. This principle is so clear that it has been seldom tested. Yet, numerous situations have not been addressed in detailed regulations. There are, for example, no rules prohibiting the use of client funds on an “intraday” basis. There also are no rules specifying the types of systems and controls B/Ds must create to ensure that customer funds remain protected. Instead, exchanges and regulators rely on a “market discipline” —B/Ds know that violating client cash segregation is tantamount to signaling the market that it is insolvent.

MF Global Courts an Illiquidity Crisis

MFGI’s core business was to make markets for clients in exchange-traded products. It also borrowed and lent securities from/to clients, realizing an interest margin in the process. Normally, MFGI did not trade for its “own account.” As products and trading volumes grew on the exchanges, MFGI earned reasonable returns. However, starting around 2005 MFGI struggled to differentiate itself from other B/Ds. Recognizing this, MFGI’s parent, the Man Group, spun off the firm via an IPO in 2007.6

Matters took a turn for the worse in 2008. On February 28, the firm announced a bad debt provision of $141 million due to unauthorized trading losses. An MFGI trader in wheat futures exceeded his limits and racked up over $200 million in losses. MFGI stock plummeted on the news. The CFTC and several exchanges issued statements that MFGI was in full regulatory compliance. However, the CFTC subsequently fined the firm $10 million. The incident left an impression that MFGI had financial control weaknesses.7

From there MFGI’s business deteriorated. Several rating agencies warned that MFGI’s investment grade credit rating could be in jeopardy. A high quality credit rating is essential to a large trading house. B/Ds must convey soundness to clients in order to attract their deposits. Counterparties also favor doing business with firms they can trust to execute transactions. Firms with weak credit must often post bigger cash collateral positions. B/D firms who lose their investment grade credit rating typically are acquired or otherwise go out of business.

During 2009, the MFGI Board became increasingly concerned with the firm’s weak performance (Attachment 1). In response they sought to attract a top-tier CEO to turn the firm around. This resulted in the March 2010 hiring of Jon Corzine as CEO.8 Corzine was a famous Wall Street figure. He had been Goldman Sach’s CEO from 1994–99, after which he became first a U.S. Senator and then Governor of New Jersey. Ousted as Governor in 2008, Corzine was looking for a new challenge. Turning around MFGI looked attractive. Hiring Corzine seemed like a coup for MFGI. Corzine’s turnaround plan was not limited to improving MFGI’s existing business. Corzine made his reputation at Goldman Sachs by driving that firm deep into proprietary trading. He planned a similar strategy at MFGI. At Goldman, however, Corzine benefited from a giant balance sheet and a strong credit rating. MFGI offered much more limited resources. In fact, the rating agencies were stepping up their demands for near-term profit improvement; a failure to deliver higher profits likely would lead to MFGI being downgraded. The firm’s credit rating was only BBB, close to the lowest investment grade. Suffering a downgrade could render MFGI a takeover target or even lead to insolvency.

Corzine pondered how to combine his plans for proprietary trading with the near-term imperative of profit improvement. Scanning the horizon, he spotted an opportunity in European Sovereign Debt. His gambit involved the accounting associated with a transaction known as “Repo-to-Maturity.”

Repo-to-Maturity is a well-known transaction on Wall Street. Like other “repurchase agreements,” it involves selling a security to another firm against a commitment to repurchase the same security on a future date. Such “Repos” essentially amount to short-term loans. The firm selling the security receives cash upfront, and pays interest in the form of a higher purchase price when it buys back the underlying asset. The security being passed back and forth provides collateral. If the selling firm is unable to repurchase as agreed, the purchasing firm keeps the underlying security.

Repo-to-Maturity differs from a standard repo in one respect. The underlying security is sold for a period that takes it to that security’s maturity date. This means that the purchasing firm can look to be repaid by the security’s actual debtor rather than by the firm selling the security.

This difference results in other unique “Repo-to-Maturity” characteristics. First, the purchasing firm gains certain rights. It can, for example, require the selling firm to repurchase the security a few days before its maturity. This gives the purchasing firm protection against a default by the underlying debtor. Second, Repo-to-Maturity also qualifies for a different accounting treatment. Whereas standard repos are accounted for as loans, Repo-to-Maturity is treated as an asset sale. This means that if the sale price is higher than the security’s carrying cost on the books, the selling firm books a gain to income.

Corzine spotted this Repo-to-Maturity feature and thought he saw an answer to MFG’s problems. Corzine reasoned that MFGI could purchase large amounts of European Sovereign Debt at significant discounts to par value. In 2010, government bonds for countries such as Italy, Spain, Ireland and Portugal were seen to carry significant default risk; consequently, they were selling well below par. Corzine saw that MFGI could buy these bonds at prices like 75–80% of par and then Repo them to Maturity. The sale price negotiated for the Repo would be much closer to par in anticipation of the fact that the bonds would move to par as they approached the time for governments to pay them off. Other security firms would be willing to pay these higher prices because they also would have the option to put them back to MFGI if default was imminent. In the meantime, MFGI could book big gains on the original Repo-to-Maturity sales. Those gains would boost MFGI’s profits, stave off a debt rating downgrade, and buy Corzine time to implement the rest of his proprietary trading strategy.

Corzine saw many ways this strategy could work. If sovereign debt conditions improved, the deals would liquidate in an orderly fashion. Even if conditions only stabilized and MFGI got the bonds “put back,” bond prices might still be higher than the firm’s original purchase price. Only if European sovereigns deteriorated further would Corzine’s strategy yield losses. This could produce a dangerous scenario where scores of Repo bonds could come back to MFGI and be worth lower prices than the firm now paid to repurchase. Corzine, however, considered this outcome unlikely; he felt that the Euro zone could not afford to let governments default and would ultimately back their sovereign debt. He decided MFGI would take the plunge. Attachment 2 diagrams these Repo-to-Maturity transactions and their associated accounting.9

Corzine ‘Bets the House’ on Euro Sovereign Debt

When Corzine joined MF Global, the firm owned only $400 million in sovereign bonds issued by the combined countries of Italy, Spain, Portugal and Ireland (ISPI). MFGI had a $1 billion limit on total exposure from such countries, which amount moved to $2 billion in September of that year. MFGI’s Chief Risk Officer (CRO) believed this level of exposure could put the firm at risk for up to $200 million in cash margin calls. The CRO was sufficiently concerned by this risk that he reviewed the new limit with MFGI’s Board even though he had authority to approve it himself.10

There were multiple reasons for the CRO to be concerned. For one thing, MFGI had limited amounts of reserve borrowing capacity; these consisted of an emergency unsecured bank revolver of $1.2 billion and a $300 M secured bank facility. That seems like a lot of funding until one realizes that firms like MFGI have balance sheets in the tens of billions of dollars and are subject to sudden funds redemption calls. Another liquidity threat involves B/D’s heavy reliance on repo financing. Such financing requires constant “rollovers.” If lenders become uneasy about MFGI’s credit, the firm’s requests to roll over repo funding can be refused. Should redemption calls and cancelled repos concentrate at a moment in time, the firm can face an unappetizing choice: liquidate securities at fire-sale prices or draw down all available bank lines. New cash margin calls on remaining repos could then compound the squeeze. MFGI’s CRO knew well that its secured reserve bank lines would not be enough to withstand a liquidity crisis of this sort.

A weak “back office,” compounded MFGI’s vulnerability. Audits conducted after the 2008 trading losses identified many control weaknesses. The most significant involved information systems. Under heavy volume the firm’s systems had difficulty tracking and clearing trades. Manual interventions were then required to clear failed trades. MFGI accounting system also had difficulties reporting data after a heavy volume of trades. Multiple audits called for the firm to make substantial investments in system upgrades.11

Jon Corzine’s priorities lay elsewhere. His immediate goal was to stave off a credit downgrade by improving reported profits. To that end, Corzine repeatedly sought Board approval to increase the firm’s ISPI sovereign exposure. This began in September 2010 when Corzine obtained an increase to $4.5 billion. This amount was quickly exhausted. Less than two months later, Corzine pushed for a limit of $4.75 billion. The CRO pointed out that this level of exposure could cause MFGI to face over $500 million of margin calls in a bad market scenario. His warning caused the Board to pause before granting Corzine’s request.

Corzine responded by forcing out the CRO, replacing him with a close associate, David Stockman. Following this change, Corzine was able to secure new European Sovereign debt limits of $5 billion and ultimately $8.5 billion. This last limit increase was granted in June 2011. Attachment 3 shows how this exposure limit was distributed by country.12

To Corzine these increases were required because MFGI’s core business continued to struggle. Core profitability was not good, and exposing this was likely to trigger a ratings downgrade. However, Repos-to-Maturity (RtMs) produce only one-time gains when first booked. A growing volume of such repos was thus required to patch up MFGI’s profits as one reporting period gave way to another. Unfortunately, growing MFGI’s RtMs book also compounded its liquidity risks. By June 2011, new CRO Stockman was reporting that margin calls could exhaust the firm’s unsecured emergency credit line. The board agreed to Corzine’s last request only when hearing that MFGI had a reserve of “easy to sell” securities it could turn to if a crisis developed.

The Euro Sovereign Debt Crisis Hits

Throughout late 2010 and 1H 2011, Corzine minimized the risks of his strategy when requesting new limits from the MFGI Board. Part of Corzine’s assurances was based on diversification. MFGI was purchasing bonds from multiple countries and for different maturities (initially 6–12 months, later extended to 21 months). A second risk mitigant was the European Financial Stability Facility (EFSF). Corzine took comfort from this Euro 440 billion fund financed by the stronger Euro Zone members. In the eyes of Corzine and others, the EFSF committed the Euro Zone to prevent a debt default by any sovereign governments other than Greece, which was especially troubled.

During 2011 MFGI’s risk management team increasingly worried about this perspective. CRO Stockman repeatedly brought up his concerns. One was that the EFSF was not big enough to handle multiple sovereign defaults. The facility was based on the idea that its existence would keep the capital markets open to all ISPI countries; yet, if it failed to do so for one country, the markets for others would collapse; a contagion might ensue and multiple defaults were then likely.

A second concern was the volatility of sovereign bond prices and their implications for MFGI’s earnings. MFGI carried an inventory of sovereign bonds in anticipation of new RtM transactions. Even without a default, there was a risk that some ISPI bonds would deteriorate in quality, resulting in lower prices. Should this happen, MFGI would be forced to “Mark” its held securities “to Market,” i.e., lower the values at which it carried such bonds on its books. These haircuts count as losses to be reported in the firm’s next earnings release. They also allow repo counterparties to demand additional cash collateral. Throughout spring 2011, CRO Stockman warned that such a scenario could put acute pressure on MFGI’s liquidity lines. Lastly, repeated haircuts posed another conundrum. By damaging reported earnings, they threatened to bring about the ratings downgrade they were intended to forestall.

In the view of Stockman and others, this last threat was having the perverse effect of forcing Corzine to increase the firm’s sovereign RtM bets. Only by purchasing more ISPI sovereigns could MFGI generate enough new income gains to offset the haircuts on its prior transactions.

Unfortunately for MFGI, Stockman’s fears were realized during spring and summer of 2011. The capital markets began to fear that multiple ISPI defaults might occur. Debt spreads widened out. For example, Italian bond yields began to trade 2–3% higher than their German counterparts Spanish and Portuguese spreads widened even more. When interest spreads widen, bond prices fall. Such is what happened to MFGI’s existing ISPI portfolio.

It was in response to these developments that CEO Corzine made his request for an increase in Sovereign RtM limit to $8.5 billion.13

Markets Begin to Close in on MFGI

Sovereign debt markets continued to put further pressure on MFGI’s portfolio as spring turned to summer. CRO Stockman also grew concerned that the firm was not respecting the risk limits set by the Board. In July, he spoke to Corzine about violations of these limits, e.g., 20% over for Italy, 31% for Spain and 12% overall. In August, Stockman informed the Board that the firm’s daily cash requirement for margin calls was approaching $500 million. In response to these and other warnings, the Board suspended purchases of sovereign securities. The Board also asked for a “Break-the-Glass” analysis of how the firm would handle a liquidity crisis. One senior MFGI executive, who ran the Operations Department, captured the sentiment at that time:

“I [do not] have any real confidence at this point that we know our liquidity in each of days 1–7 in event of a stress event. This is troubling as we need to provide an answer to [the Board] and Corzine and I need to know so that we can assess if there are steps we need to take over [the] next several weeks.”14

This belated move to contain risk did not alleviate pressures on MFGI. FINRA is the U.S. regulator supervising broker/dealers. It noticed MFGI’s sovereign positions and its lack of reserves, and began to press MFGI to make a new capital allocation in anticipation of possible losses. MFGI argued that European sovereign debts are comparable to U.S. Treasury securities, which do not require capital reserves. FINRA was not impressed. MFGI began to prepare for a capital charge in the range of $50–100 million. Then the news got much worse. In late August, FINRA imposed a capital reserve of $255 million. FINRA also restricted MFGI’s underwriting activities and placed the firm under “special surveillance.”15

The news rocked MFGI’s world. Immediate filings were required disclosing this development to the CFTC, SEC and investors. Many read MFGI’s announcement for what it was—a disclosure that the firm’s sovereign debt bet was huge and not going well. In response the N.Y. Federal Reserve Bank and the U.K.’s FSA both requested additional information. Press reports grew increasingly skeptical about the MFGI situation. Then on October 24 Moody’s downgraded MFGI to Baa3, the lowest investment grade, and placed the firm on watch for a further downgrade to “junk.” Moody’s commented:

“MF Global’s increased exposure to European sovereign debt in peripheral countries and its need to inject capital into its [B/D] subsidiary to rectify a regulatory capital shortfall highlights the [Company’s] increased risk appetite and raises questions about the [Company’s] risk governance.”16

The stage was set for final days that would expose MFGI’s multiple weaknesses and place Jon Corzine and Edith O’Brien in a difficult predicament.

MFGI’s Final Week and a Decision on Segregated Accounts

The firm’s final week unfolded like a nightmare. On Tuesday, October 25, MFGI reported a quarterly loss of $191 million, a loss almost $100 million higher than the prior year’s comparable quarter. The response to this news and the debt downgrade was swift. Major clients began to withdraw funds. Margin calls skyrocketed. In the U.K. margin calls were made for 110% of the amounts technically required. MFGI was forced to draw down on its reserve liquidity line, which by now was more than 50% drawn.17

Pressures soon mounted on another front. MFGI’s back office, i.e., its systems and accounting processes, began to fail. Numerous trades failed to settle; other trades that were reported settled were in fact not cleared. Firm financial reports became detached from underlying reality. Literally hundreds of trades now needed to be handled manually.18

All of MFGI’s problems seemed to converge on Wednesday, October 26. The day began with S&P putting the firm on credit watch for a downgrade. Severe liquidity problems followed. Counterparties refused to roll over repurchase agreements, leaving MFGI’s broker/dealer scrambling to find funding from other sources. Some $400 million in cash was required to compensate for this loss of “repo financing.” New margin calls added to the crisis. MFGI responded by drawing a further $223 million from its credit facility. Then, at day’s end, MFGI transferred $615 million from the Commodity subsidiary to plug a gapping liquidity hole at MFGI’s B/D.19

This last transfer was dicey. Because MFGI could not monitor cash balances in segregated accounts, its Treasury Department could not tell whether segregated client cash had been used to fund the transfer. Its anxieties were evident in Edith O’Brien’s e-mail of that date to the Operations Department:

“I NEED TO KNOW HOW MUCH IS BEING RETURN[ED] — FROM WHERE TO WHERE” and“I NEED TO KNOW NOW — TO PRE-ADVISE FUNDING AND AVOID A SEG ISSUE.”[Emphasis in original]20

Operations failed to respond, but later that evening, O’Brien and her colleagues determined that in fact Segregated Customer Account balances had gone negative during the 26th.

October 27 brought even worse news. Both Moody’s and Fitch downgraded MFGI to “junk” status with a negative outlook. J.P. Morgan, the firm’s “clearing bank” sent personnel into MFGI to review each securities transaction. Before allowing trades to settle, the Morgan personnel would determine whether there were “good funds” in MFGI’s account. Morgan also cancelled all of MFGI’s intraday credit lines, effectively putting the B/D on “cash.” Struggling to stay afloat, MFGI took down the last $52 million of its unsecured revolving credit. Meanwhile, O’Brien and her Treasury colleagues determined that on the 26th, segregated customer accounts had gone negative by $167 million.21

As business closed on the 27th, confusion reigned inside MFGI. MF Global UK (MFG UK) advised that it had overdrawn accounts at J.P. Morgan to the tune of $175 M. Inside MFGI, differences arose as to whether segregated customer accounts were actually in deficit. Control reports showed a deficit; the accounting groups contended this was the result of misbookings and that the customer accounts were in surplus. Meanwhile, trades continued to be cleared manually; this meant the clearing process lagged well behind actual trading and left MFGI in the dark as to its financial position.

Knowing it faced an insolvency crisis, MFGI’s Board resolved to shrink the firm’s balance sheet. The specific plan involved selling $5 billion in securities on Friday. The sales would include a substantial portion of Sovereign securities.

When business resumed on Friday, Edith O’Brien quickly encountered the consequences of MFGI’s distress. Plans to shrink the balance sheet stalled in the face of MFGI’s overdrafts at J.P. Morgan. This prompted emails from London to Corzine asking for immediate help on the overdrafts which were: “HOLDING UP VITAL BUSINESS IN THE US AS A RESULT.” In response, Corzine phoned O’Brien in Chicago, asking that the overdrafts be immediately resolved.22

O’Brien prepared wire transfers to cover the overdrafts. The first would move $200 million from segregated customer accounts to MFGI B/D; the second transferred $175 million to MFG UK’s account at J.P. Morgan, London.

Should she pull the trigger on these wires? If she did so and it turned out that the client accounts were overdrawn when the dust settled, O’Brien would be complicit in misappropriating client funds. This would become obvious from the documentation—it would be her signature authorizing the wire transfers. It was also likely that JPM would ask her to sign an Assurance Letter, i.e., a letter representing that the funds being transferred were in fact MFGI’s funds and not those of clients. Attachment 4 contains the draft of such a letter. O’Brien expected to be asked to sign this or something similar at close of business or over the weekend.

What other option was there? The firm’s solvency seemed to hang in the balance. On the other hand, O’Brien felt strongly that a decision of this magnitude should not be made at her level. Still, time was running out. Corzine might call back at any moment demanding to know whether the overdrafts were fixed. What would she say? What should be her next move?

Attachment 1

M. F. Global Inc.

Selected Financial Information

For Fiscal Years Ending March 31,

2008 and 2009

$ Millions

2008

2009

Revenue

$2,914.8

$6,019.8

EBITDA

$133.4

($91.51)

Net Income/(Loss)

(69.5)

(49.1)

Earnings per Share

($0.60)

($0.58)

Total Assets

49,254.87

38,835.63

Total Liabilities

47,995.01

37,387.87

Equity

1,249.02

1,223.55

Debt/Capital %

0.975

0.968

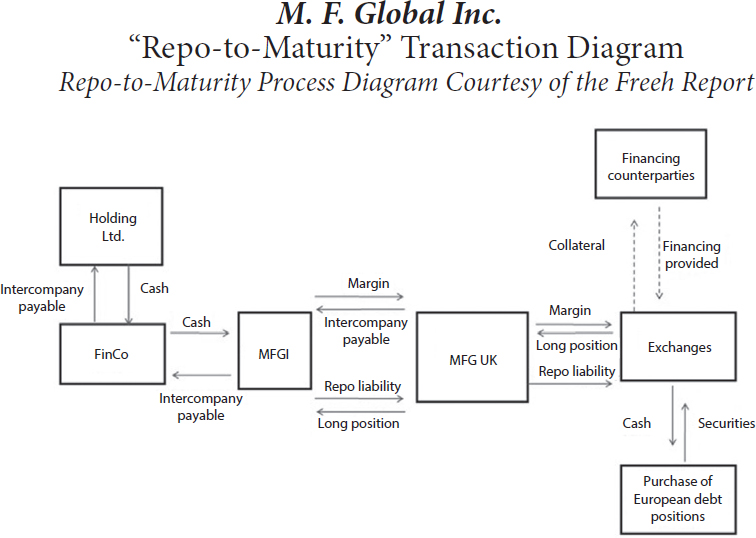

Attachment 2

M. F. Global Inc.

“Repo-to-Maturity” Transaction Diagram Repo-to-Maturity Process Diagram Courtesy of the Freeh Report

MFGUK buys $100 M ISPI Sovereign Bonds from “Street” @ 80% par for $80 M, creating a “long position” and sells the same security to MFGI at slight markup.

Transaction is booked as $81 M purchase on MFGI’s B/D accounts (Book 7) and then $80 M purchase on MFGI’s consolidated accounts, subject to Mark-to-Market Accounting treatment.

MFG UK negotiates “Repo-to-Maturity” with Third Party, selling the security at 99% of Par ($99 M). MFGI enters into internal Repo-to-Maturity with MFG UK on similar terms.

MFGI delivers the Sovereign Bonds to MFG UK who delivers them to the London Clearing House for delivery to the Third Party.

Cash transactions and margin posting are handled via funding out of MFG Holding, via Intercompany account transactions.

Accounting Results

MFGI records a sale for $99 M and a gain of $19 M versus the original purchase price.

Should MFG UK have to repurchase the Bonds at par from the Third Party right before maturity, MFGI would record this as a new purchase of bonds at par.

The risk to MFGI is that it would only have the bonds ‘put’ back to it right before their maturity if the Third Party feared a sovereign default, in which case the bonds would have market prices well below par.

Attachment 3

MFGI Euro Sovereign Debt RTM Exposure Limit Changes

June 2011

Tier or individual country limit

Increase

Tier 1 (Belgium, Italy, and Spain)

From $5.6 billion to $6.6 billion Belgium from $1 billion to $1.5 billion

Italy from $3.1 billion to $4 billion

Spain from $1.5 billion to $2 billion

Tier 2 (Ireland and Portugal)

From $1.7 billion to $1.9 billion Ireland from $400 million to $600 million

Portugal $1.3 billion limit unchanged

Source: Freeh Report

Attachment 4

Historical Recreation Draft

J.P. Morgan Chase Bank N.A., London Branch 25 Bank Street, Canary Wharf London, E14 5JP United Kingdom

October 28, 2011

Ms. Edith O’Brien, Assistant Treasurer

Treasury Department

M.F. Global Inc.

Chicago, U.S.A.

Dear Ms. O’Brien,

J.P. Morgan Chase Bank N.A., London Branch, along with other offices of the Bank (the Bank), operate as a clearing bank for trades conducted by your organization, M.F. Global Inc. and its various subsidiaries and branches (MFGI).

Recently, various instances of overdrafts in accounts have caused the bank to suspend intraday overdrafts normally made available to MFGI. The Bank has determined that until further notice, no MFGI trades requiring payments by your firm will be authorized unless it is determined that MFGI has “good funds” available in the account to be debited.

In that regard, we would like you, in your capacity as Assistant Treasurer, to assure and affirm that no funds made available to these clearing accounts will be drawn from the segregated client accounts at your firm. You may provide this assurance by signing and dating in the space provided below.

Very truly yours,

_____________________

J.P. Morgan Chase Bank N.A.

_____________________

Edith O’Brien, Assistant Treasurer

M.F. Global Inc.

Author’s Note

This case explores whether the dangers of Big Trading, exposed by the Financial Crisis, remain a danger in its aftermath. The MF Global case offers an opportunity to explore this through the actions of CEO Jon Corzine. Students should examine Corzine’s approach to several issues, i.e., his MFGI proprietary trading strategy, his attitude towards accounting for trades, and his handling of MFGI’s known financial control deficiencies. The case provides a vivid example of what happens when such issues crystallize under financial market stress.

It is important to note that this case’s events occured after the passage of Dodd-Frank. Students thus have an opportunity to observe how MFGI performed under the enhanced regulatory scrutiny which that law created. Regulators clearly are more in evidence here. Students should evaluate the extent to which their presence contributed to avoiding an MFGI default, to the avoidance of contagion and to an orderly process for handling MFGI’s problems.

At the other end of the spectrum, the case offers a chance to stand in the shoes of mid-level employee, Edith O’Brien. She has been put in a difficult situation by Corzine’s demands. She is not sure that the overdrafts can be remedied without violating segregated client cash. Information is confused and systems are not cooperating. If she sends the wires and it turns out that client accounts are underfunded, will O’Brien be the one taking the fall? If she doesn’t send them, will Corzine fire her? Is there any way for O’Brien to resist demands that she perform an illegal act and still survive in her job? Here students should consider what other players are present in this drama and whether their involvement creates options for O’Brien.

This case draws on news accounts of the MF Global scandal, and especially on the report of Lewis J. Freeh, the bankruptcy trustee. This report, filed April 4, 2014, provides a detailed account of MFGI’s story prior to Corzine’s arrival, how Corzine revamped the firm’s strategy, and the step-by-step buildup in the firm’s sovereign Euro debt exposure. It also explains the Repo-to-Maturity transaction, its accounting, and how Corzine saw this as a means of avoiding an MFGI debt downgrade.

Attachment 4 is a Historical Recreation, not a replica of actual correspondence between J.P. Morgan, London and MFGI. It does, however, reflect the substance of what the bank sought from MFGI in an Assurance Letter.

The MFGI story serves to remind us that the problems of excessive risk taking, weak controls and problematic accounting remain with us today. In this case they did not produce contagion or any material “knock-on” effects. Whether this means that systemic risk is greatly ameliorated is up for discussion.