Chapter 12

ACCOUNTING FOR PARTNERSHIPS

CHAPTER LEARNING OBJECTIVES

After studying this chapter, you should be able to:

1. Identify the characteristics of the partnership form of business organization.

2. Explain the accounting entries for the formation of a partnership.

3. Identify the bases for dividing net income or net loss.

4. Describe the form and content of partnership financial statements.

5. Explain the effects of the entries to record the liquidation of a partnership.

*6. Explain the effects of the entries when a new partner is admitted.

*7. Describe the effects of the entries when a partner withdraws from the firm.

Note: All asterisked (*) items relate to material contained in the Appendix to the chapter.

![]()

PREVIEW OF CHAPTER 12

In this chapter, we will discuss reasons why the partnership form of organization is often selected and explain the major issues in accounting for partnerships. The content and organization of this chapter are as follows:

![]()

Partnership Form of Organization

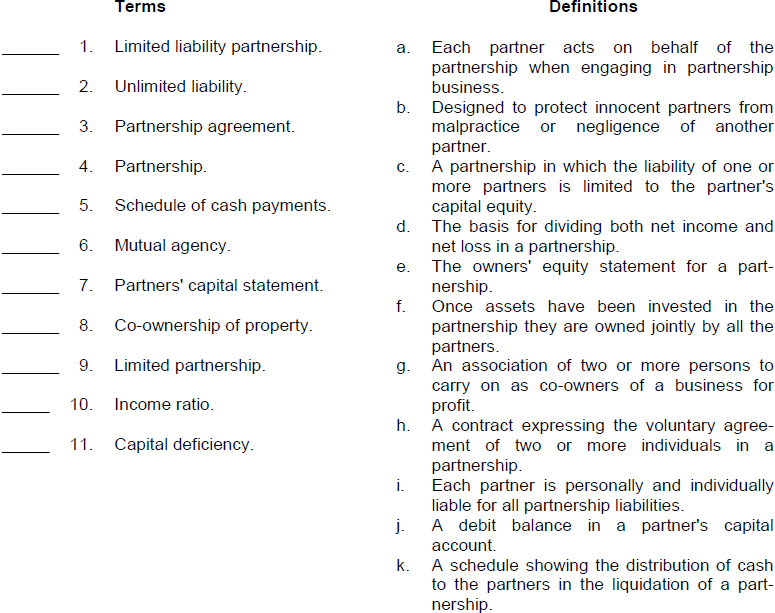

- (L.O. 1) A partnership is an association of two or more persons to carry on as co-owners of a business for a profit.

Characteristics of Partnerships

2. The principal characteristics of the partnership form of business organization are (a) association of individuals, (b) mutual agency, (c) limited life, (d) unlimited liability, and (e) co-ownership of property.

3. The association of individuals in a partnership may be based on as simple an act as a handshake; however, it is preferable to state the agreement in writing.

a. A partnership is a legal entity for certain purposes.

b. A partnership is an accounting entity for financial reporting purposes.

c. Net income of a partnership is not taxed as a separate entity.

4. Mutual agency means that each partner acts on behalf of the partnership when engaging in partnership business, and the act of any partner is binding on all other partners. This is true even when partners act beyond the scope of their authority, so long as the act appears to be appropriate for the partnership.

5. Partnerships have a limited life. Partnership dissolution occurs whenever a partner withdraws or a new partner is admitted.

6. Each partner has unlimited liability.

a. Each partner is personally and individually liable for all partnership liabilities.

b. Creditors' claims attach first to partnership assets and then to the personal resources of any partner, irrespective of that partner's capital equity in the company.

7. Partnership assets are co-owned by the partners. Once assets have been invested in the partnership they are owned jointly by all the partners.

Advantages and Disadvantages

8. Organizations with partnership characteristics include limited partnerships, limited liability partnerships, limited liability companies, and S corporations.

9. The major advantages of a partnership are:

a. Combining skills and resources of two or more individuals.

b. Ease of formation.

c. Freedom from governmental regulations and restrictions.

d. Ease of decision making.

10. The major disadvantages of a partnership are

a. mutual agency.

b. limited life.

c. unlimited liability.

11. Under limited partnerships, the liability of a limited partner is limited to the partners' capital equity. However, there must always be at least one partner with unlimited liability, often referred to as the general partner.

Limited Liability Partnership

12. Professionals such as lawyers, doctors, and accountants can be protected from malpractice or negligence claims of other partners by forming a limited liability partnership.

Limited Liability Companies

13. A new hybrid form of business organization with certain features like a corporation and others like a limited partnership is a limited liability company.

The Partnership Agreement

14. The written contract often referred to as the partnership agreement, contains such basic information as the name and principal location of the firm, the purpose of the business, and the date of inception.

Forming a Partnership

15. (L.O. 2) In the formation of a partnership, each partner's initial investment in a partnership should be recorded at the fair value of the assets at the date of their transfer to the partnership.

Dividing Net Income or Net Loss

16. (L.O. 3) Partnership net income or net loss is shared equally unless the partnership contract specifically indicates otherwise.

a. A partner's share of net income or net loss is recognized in the accounts through closing entries.

b. Closing entries for a partnership are identical to the entries made for a proprietorship, except for the use of multiple capital and drawing accounts.

17. The various income ratios that may be used include:

a. A fixed ratio, expressed as a proportion (6:4), a percentage (70% and 30%), or a fraction (2/3 and 1/3).

b. A ratio based either on capital balances at the beginning of the year or on average capital balances during the year.

c. Salaries to partners and the remainder on a fixed ratio.

d. Interest on partners' capitals and the remainder on a fixed ratio.

e. Salaries to partners, interest on partners' capitals, and the remainder on a fixed ratio.

The objective is to reach agreement on a basis that will equitably reflect the differences among partners in terms of their capital investment and service to the partnership.

18. Provisions for salaries and interest must be applied before the remainder of net income or net loss is allocated on the specified fixed ratio. Detailed information concerning the division of net income or net loss should be shown at the bottom of the income statement.

Partnership Financial Statements

19. (L.O. 4) The financial statements of a partnership are similar to a proprietorship. The differences are generally related to the fact that a number of owners are involved in a partnership. The income statement for a partnership is identical to the income statement for a proprietorship except for the division of net income.

20. The owners' equity statement for a partnership is called the partners' capital statement. It explains the changes in each partners' equity during an accounting period. Changes in capital may result from additional capital investment, drawings, and net income or net loss.

Liquidation of a Partnership

21. (L.O. 5) The liquidation of a partnership terminates the business. In a liquidation, it is necessary to:

a. Sell noncash assets for cash and recognize a gain or loss on realization. The journal entry to record this will include a debit to cash for the amount received from the sale, debits to any contra-asset accounts, a debit for the loss on realization/or a credit for the gain on realization and credits to all asset accounts.

b. Allocate gain/loss on realization to the partners based on their income ratios. The journal entry to record this will include a debit to the gain on realization and credits to each partner's capital account or debits to each partner's capital account and a credit to the loss on realization.

c. Pay partnership liabilities in cash. The journal entry to record this will include debits to all liability accounts and a credit to cash.

d. Distribute remaining cash to partners on the basis of their remaining capital balances. The journal entry to record this will include debits to each partner's capital account and a credit to cash.

Each of the steps must be performed in sequence.

22. The liquidation of a partnership may result in no capital deficiency (all partners have credit balances in their capital accounts) or in a capital deficiency (at least one partner's capital account has a debit balance.)

23. A schedule of cash payments may be used to determine the distribution of cash to each partner.

24. When there is a capital deficiency, the partners with the deficiency may pay the amount owed and the deficiency is eliminated.

25. If a partner with a capital deficiency is unable to pay the amount owed to the partnership, the partners with credit balances must absorb the loss as follows:

a. The cash distributed to each partner is the difference between the partner's present capital balance and the loss that the partner may have to absorb if the capital deficiency is not paid.

b. The allocation of the deficiency is made on the income ratios that exist between the partners with credit balances. The allocation is journalized and posted.

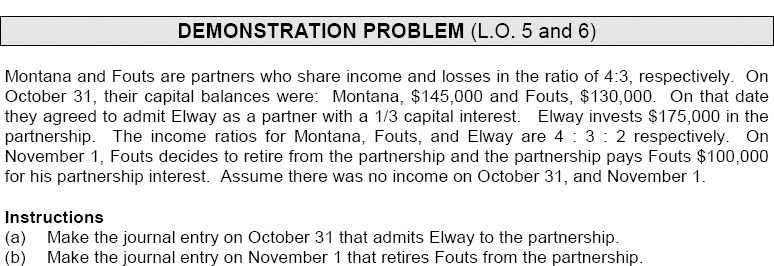

*26. (L.O. 6) A new partner may be admitted either by (1) purchasing the interest of one or more existing partners, or (2) investing assets in the partnership. The former affects only partners' capital accounts whereas the latter increases both net assets and total capital of the partnership.

*27. When a new partner is admitted by purchase of an interest,

a. The transaction is a personal one between one or more existing partners and the new partner.

b. Any money or other consideration exchanged is the property of the participants and not the property of the partnership.

c. Each partner's capital account is debited for the ownership claims that have been relinquished, and the new partner's capital account is credited with the capital equity purchased.

d. Total assets, total liabilities, and total capital remain unchanged.

*28. When a new partner is admitted by the investment of assets, both the total net assets and the total capital of the partnership increase. This is done by debiting Cash and crediting the new partner's capital account. When the capital credit does not equal the investment of assets in the partnership, the difference is considered a bonus either to the existing partners or the new partner.

*29. A bonus to old partners results when the new partner's capital credit on the date of admittance is less than the new partner's investment in the firm. The procedure for determining the new partner's capital credit and the bonus to the old partners is as follows:

a. Determine the total capital of the new partnership by adding the new partner's investment to the total capital of the old partnership.

b. Determine the new partner's capital credit by multiplying the total capital of the new partnership by the new partner's ownership interest.

c. Determine the amount of bonus by subtracting the new partner's capital credit from the new partner's investment.

d. Allocate the bonus to the old partners on the basis of their income ratios.

*30. A bonus to a new partner results when the new partner's capital credit is greater than the partner's investment of assets in the firm. The bonus results in a decrease in the capital balances of the old partners based on their income ratios before admission of the new partner.

Withdrawal of a Partner

*31. (L.O. 7) As in the case of the admission of a partner, the withdrawal of a partner legally dissolves the partnership. The withdrawal of a partner may be accomplished by (a) payment from partners' personal assets or (b) payment from partnership assets. The former affects only the partners' capital accounts, whereas the latter decreases total net assets and total capital of the partnership.

*32. The withdrawal of a partner when payment is made from partners' personal assets is the direct opposite of admitting a new partner who purchases a partner's interest.

a. Payment from partners' personal assets is a personal transaction between the partners.

b. Partnership assets are not involved and total capital does not change.

c. The effect on the partnership is limited to a realignment of the partners' capital balances.

*33. Using partnership assets to pay for a withdrawing partner's interest is the reverse of admitting a partner through the investment of assets in the partnership.

a. Payment from partnership assets is a transaction that involves the partnership.

b. Both partnership net assets and total capitals are decreased.

c. Asset reevaluations should not be recorded.

*34. When the partnership assets paid are in excess of the withdrawing partner's capital interest, a bonus to the retiring partner results. The bonus is deducted from the remaining partners' capital balances on the basis of their income ratios at the time of the withdrawal.

*35. When the partnership assets paid are less than the withdrawing partner's capital interest, a bonus to the remaining partners results. The bonus is allocated to the capital accounts of the remaining partners on the basis of their income ratios.

Death of a Partner

*36. The death of a partner dissolves the partnership, but provision generally is made for the surviving partners to continue operations. When a partner dies it is necessary to determine the partner's equity at the date of death.

![]()

![]()

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

![]()

MULTIPLE CHOICE

Circle the letter that best answers each of the following statements.

- (L.O. 1) Which of the following would not be considered a characteristic of a partnership?

- Mutual agency.

- Unlimited life.

- Unlimited liability.

- Co-ownership of property.

- (L.O. 1) Which of the following would not be considered an advantage of forming a partnership?

- Skills and resources can be combined.

- A partnership is easily formed.

- A partnership has unlimited liability.

- A partnership is relatively free from governmental regulations and restrictions.

- (L.O. 1) The Unitas, Sayers, and Blanda partnership is terminated when the claims of company creditors exceed partnership assets by $50,000 The capital balances for Unitas, Sayers, and Blanda are $35,000, $5,000, and $0, respectively. The original claims of the creditors were negotiated by Sayers and Blanda. Which partner(s) is(are) personally and individually liable for all partnership liabilities?

- Unitas.

- Sayers.

- Sayers and Blanda.

- Unitas, Sayers, and Blanda.

- (L.O. 2) J. Nicklaus and S. Snead combine their individual sole proprietorships to start the Nicklaus-Snead partnership. J. Nicklaus and S. Snead invest in the partnership as follows:

The entries to record the investment will include a credit to:

- Nicklaus, Capital of $13,500.

- Snead, Capital of $5,700.

- Nicklaus, Capital of $14,000.

- Snead, Capital of $7,700.

- (L.O. 3) The partnership agreement of Payton and Namath provides for salary allowances of $45,000 to Payton and $35,000 to Namath, with the remaining income or loss to be divided equally. During the year, Payton and Namath each withdraw cash equal to 80% of their salary allowances. If partnership net income is $100,000, Payton's equity in the partnership would:

- increase more than Namath's.

- decrease more than Namath's.

- increase the same as Namath's.

- decrease the same as Namath's.

The following information pertains to items 6 and 7.

The partnership agreement of Owens, Gehrig, and Nagurski provides for the following income ratio: (a) Owens, the managing partner, receives a salary allowance of $18,000, (b) each partner receives 15% interest on average capital investment, and (c) remaining net income or loss is divided equally. The average capital investments for the year were: Owens $100,000, Gehrig $200,000, and Nagurski $300,000.

6. (L.O. 3) If partnership net income is $120,000, the amount distributed to Gehrig should be:

a. $30,000.

b. $31,000.

c. $34,000.

d. $40,000.

7. (L.O. 3) If partnership net income is $90,000, the amount distributed to Owens should be:

a. $15,000.

b. $27,000.

c. $30,000.

d. $33,000.

8. (L.O. 5) In the liquidation of a partnership, the gains and losses from assets sold are:

a. divided equally among the partners.

b. divided among the partners in the stated income ratio.

c. divided among the partners in proportion to their capital equity interests.

d. ignored.

9. (L.O. 5) In liquidation, balances prior to the distribution of cash to the partners are: Cash $240,000; Marciano, Capital $112,000; Tunney, Capital $104,000, and Jeffries, Capital $24,000. The income ratio is 6 : 2 : 2, respectively. How much cash should be distributed to Marciano?

a. $100,000.

b. $109,000.

c. $112,000.

d. $120,000.

10. (L.O. 5) Assume the same facts in question 9 above, except that there is only $204,000 in cash and Jeffries has a capital deficiency of $12,000. How much cash should be distributed to Tunney if Jeffries does not pay his deficiency?

a. $98,000.

b. $101,000.

c. $95,000.

d. $104,000.

11. (L.O. 5) An entry is not required in the liquidation of a partnership to record the:

a. payment of cash to creditors.

b. distribution of cash to the partners.

c. sale of noncash assets.

d. allocation of a capital deficiency to partners with credit balances when the deficient partner is expected to pay the deficiency.

*12. (L.O. 6) H. Aaron joins the partnership of Kubek and Musial by paying $30,000 in cash. If the net assets of the partnership are still the same amount after Aaron has been admitted as a partner, then Aaron:

a. must have been admitted by investment of assets.

b. must have been admitted by purchase of a partner's interest.

c. must have received a bonus upon being admitted.

d. could have been admitted by an investment of assets or by a purchase of a partner's interest.

*13. (L.O. 6) D. Butkus purchases a 25% interest for $10,000 when the Marchetti, Nomellini, Jones partnership has total capital of $90,000. Prior to the admission of Butkus, each partner has a capital balance of $30,000. Each partner relinquishes an equal amount of his capital balance to Butkus. The amount to be relinquished by Jones is:

a. $5,000.

b. $6,333.

c. $7,500.

d. $12,500.

*14. (L.O. 6) S. Koufax invests $40,000 in cash in the DiMaggio and Mantle partnership for a one-third capital interest. If DiMaggio and Mantle each had $40,000 capital equity before the admission, what is Mantle's capital equity after the admission of Koufax?

a. $26,667.

b. $30,000.

c. $40,000.

d. $60,000.

*15. (L.O. 6) Jordon is admitted to a partnership with a 25% capital interest by a cash investment of $150,000. If total capital of the partnership is $650,000 before admitting Jordon, the bonus to Jordon is:

a. $50,000.

b. $25,000.

c. $75,000.

d. $100,000.

The following information pertains to items *16 and *17.

Ederle and Lenglen are partners who share income and losses in the ratio of 3 : 2, respectively. On August 31, their capital balances were: Ederle, $70,000 and Lenglen $60,000. On that date, they agree to admit Marble as a partner with a one-third capital interest.

*16. (L.O. 6) If Marble invests $50,000 in the partnership, what is Ederle's capital balance after Marble's admittance?

a. $60,000.

b. $63,333.

c. $64,000.

d. $70,000.

*17. (L.O. 6) If Marble invests $80,000 in the partnership, what is Lenglen's capital balance after Marble's admittance?

a. $70,000.

b. $64,000.

c. $63,000.

d. $60,000.

Items *18, *19, and *20 relate to the following information.

On November 30, capital balances are Holm $60,000, Berg $50,000 and Madison $50,000. The income ratios are 20%, 20% and 60% respectively. Holm decides to retire from the partnership.

*18. (L.O. 7) The partnership pays Holm $70,000 cash for her partnership interest. After Holm's retirement, what is the balance of Berg's capital account?

a. $47,500.

b. $48,000.

c. $50,000.

d. $65,000.

*19. (L.O. 7) The partnership pays Holm $50,000 cash for her partnership interest. After Holm's retirement, what is the balance of Madison's capital account?

a. $44,000.

b. $50,000.

c. $56,000.

d. $57,500.

*20. (L.O. 7) In order for Berg and Madison to have equal capital interests after the retirement of Holm, how much partnership cash would have to be paid to Holm for her partnership interest?

a. $0.

b. $53,333.

c. $60,000.

d. Any amount paid to Holm will cause Berg and Madison to still have the capital balances remain as they were before this transaction.

![]()

Match each term with its definition by writing the appropriate letter in the space provided.

![]()

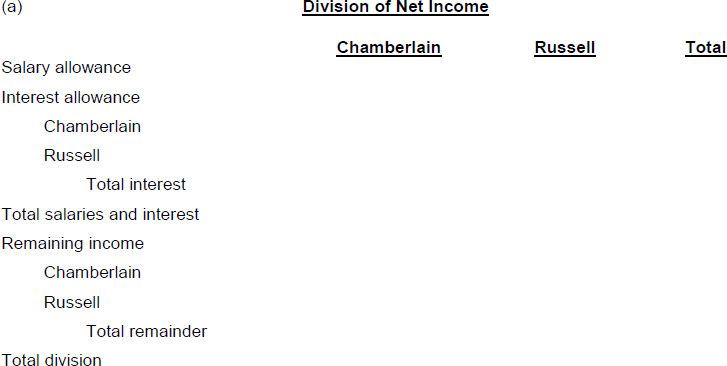

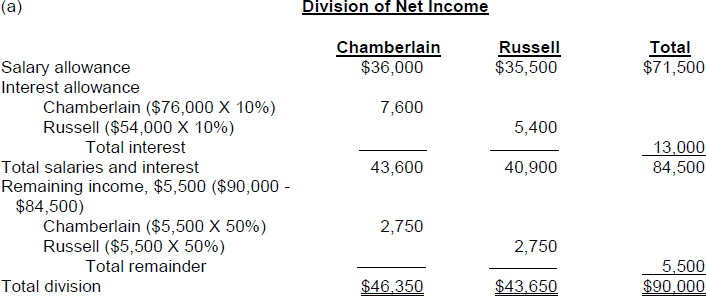

EX. 12-1 (L.O. 3) A partnership agreement between W. Chamberlain and B. Russell provides for (1) salary allowances of $36,000 to Chamberlain and $35,500 to Russell, (2) interest allowances of 10% on beginning capital balances, and (3) remaining income or loss is to be divided equally. The beginning capital balances are Chamberlain $76,000 and Russell $54,000, and net income is $90,000.

Instructions

(a) Prepare a schedule for the division of net income.

(b) Record the closing entry to transfer the net income to the partners' capital accounts.

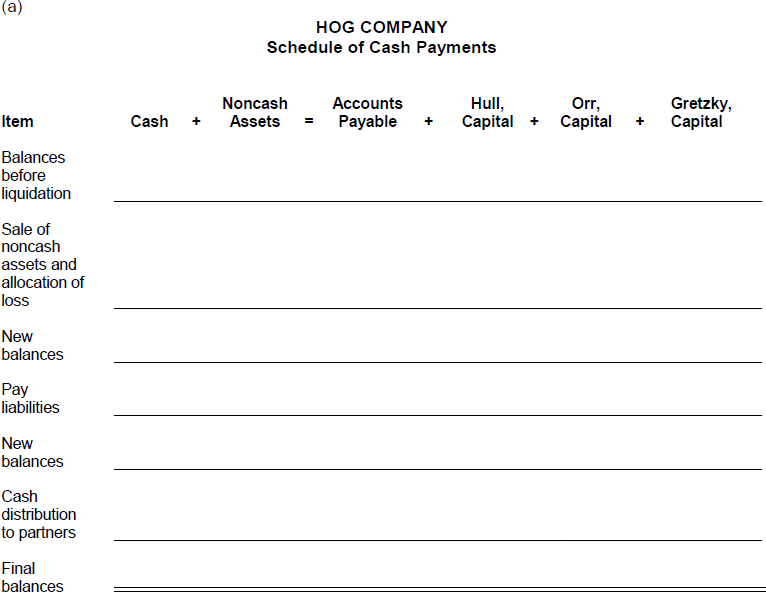

EX. 12-2 (L.O. 5) In the HOG Company, partners Hull, Orr, and Gretzky have income ratios of 3 : 2 : 1. At the time of liquidation the balance sheet shows: Cash $40,000; Noncash Assets $204,000; Accounts Payable $160,000; Hull, Capital $52,000; Orr, Capital $24,000; and Gretzky, Capital $8,000. The noncash assets are sold for $168,000 in cash.

Instructions

(a) Prepare a schedule of cash payments.

(b) Journalize the transactions assuming creditors are paid in full and available cash is distributed to the partners.

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

TRUE-FALSE

| 1. (F) | A partnership is a voluntary association of two or more individuals to carry on as co-owners of a business for profit. |

| 2. (F) | A partnership may be based on as simple an act as a handshake. |

| 3. (T) | |

| 4. (T) | |

| 5. (T) | |

| 6. (F) | Under a limited partnership, there must be at least one partner with unlimited liability, often referred to as the general partner. |

| 7. (T) | |

| 8. (T) | |

| 9. (F) | Mutual agency is thought of as a disadvantage because one partner can legally bind all of the other partners without the other partners' approval. |

| 10. (F) | An advantage of a partnership is that it is relatively free from government regulations and restrictions. |

| 11. (T) | |

| 12. (F) | Each partner's initial investment in a partnership should be recorded at the fair market value of the assets at the date of their transfer to the partnership. |

| 13. (T) | |

| 14. (F) | Partnership income or loss is shared equally unless the partnership contract specifically indicates the manner in which net income or net loss is to be divided. |

| 15. (T) | |

| 16. (F) | In liquidation, cash should be distributed to partners on the basis of their remaining capital balances. |

| *17. (F) | In an admission by investment of assets, the new partner is investing an asset of value to the partnership which will increase the net assets and total capital of the partnership. |

| *18. (T) | |

| *19. (T) | |

| *20. (F) | A bonus to the remaining partners will result when the cash paid to the retiring partner is less than the retiring partner's capital balance. |

MULTIPLE CHOICE

- b

- i

- h

- g

- k

- a

- e

- f

- c

- d

- j

EXERCISES

EX. 12-1

EX. 12-2

(a)