Chapter 11

CURRENT LIABILITIES AND PAYROLL ACCOUNTING

CHAPTER LEARNING OBJECTIVES

After studying this chapter, you should be able to:

1. Explain a current liability and identify the major types of current liabilities.

2. Describe the accounting for notes payable.

3. Explain the accounting for other current liabilities.

4. Explain financial statement presentation and analysis of current liabilities.

5. Describe the accounting and disclosure requirements for contingent liabilities.

6. Compute and record the payroll for a pay period.

7. Describe and record employer payroll taxes.

8. Discuss the objectives of internal control for payroll.

*9. Identify additional fringe benefits associated with employee compensation.

*10. Compare the accounting for payroll under GAAP and IFRS.

![]()

*Note: All asterisked (*) items relate to material contained in the Appendix to the chapter.

PREVIEW OF CHAPTER 11

All enterprises have liabilities for payroll. In addition, they also have many other types of liabilities. Examples are the purchase of supplies on account, the borrowing of money on a bank loan, and the obligation to pay interest. Liabilities are classified as current or long-term on the balance sheet. We will explain current liabilities in this chapter and long-term liabilities in Chapter 15. The content and organization of this chapter are as follows:

CHAPTER REVIEW

- (L.O. 1) A current liability is a debt that that a company expects to pay within one year or the operating cycle whichever is longer. Current liabilities include notes payable, accounts payable, unearned revenues, and accrued liabilities.

Notes Payable

2. (L.O. 2) Notes payable are obligations in the form of written notes that usually require the borrower to pay interest. Notes due for payment within one year of the balance sheet date are usually classified as current liabilities.

3. When an interest-bearing note is issued, the assets received generally equal the face value of the note:

a. During the term of the note, it is necessary to accrue interest expense.

b. At maturity, Notes Payable is debited for the face value of the note and Interest Payable is debited for accrued interest.

Sales Taxes Payable

4. (L.O. 3) A sales tax is expressed as a stated percentage of the sales price on goods sold to customers by a retailer. The entry by the selling company to record sales taxes is as follows:

When sales taxes are not rung up separately on the cash register, total receipts are divided by 100% plus the sales tax percentage to determine the sales.

Unearned Revenues

5. Unearned Revenues (advances from customers) are recorded by a debit to Cash and a credit to a current liability account identifying the source of the unearned revenue. When the revenue is earned, the unearned revenue account is debited and an earned revenue account is credited.

Current Maturities of Long-Term Debt

6. Another item classified as a current liability is current maturities of long-term debt. Current maturities of long-term debt are often identified on the balance sheet as long-term debt due within one year.

Financial Statement Presentation and Analysis

7. (L.O. 4) Current liabilities is the first category under liabilities on the balance sheet.

a. Each of the principal types of current liabilities is listed separately.

b. Current liabilities are usually in order of magnitude with the largest obligations being listed first. However, many companies, as a matter of custom, show notes payable and accounts payable first regardless of amount.

8. The excess of current assets over current liabilities is working capital. The current ratio is current assets divided by current liabilities.

Contingent Liabilities

9. (L.O. 5) A contingent liability is a potential liability that may become an actual liability in the future. The accounting guidelines require that:

a. If the contingency is probable and the amount can be reasonably estimated, the liability should be recorded in the accounts.

b. If the contingency is only reasonably possible, then it need be disclosed only in the notes accompanying the financial statements.

c. If the contingency is remote, it need not be recorded or disclosed.

10. Product warranties are a good example of a contingent liability. They are recorded by estimating the cost of honoring product warranty contracts and expensing the amount in the period in which the sale occurs. Warranty expense is reported under selling expenses in the income statement, and estimated warranty liability is classified as a current liability on the balance sheet.

Payroll Accounting

11. The term payroll pertains to all salaries and wages paid to employees. Payments made to professional individuals who are independent contractors are called fees. Government regulations relating to the payment and reporting of payroll taxes apply only to employees.

Gross Earnings

12. (L.O. 6) Gross earnings is the total compensation earned by an employee. It consists of: wages or salaries, plus any bonuses and commissions.

a. Total wages are determined by applying the hourly rate of pay to the hours worked.

b. Most companies are required to pay a minimum of one and one-half times the regular hourly rate for overtime work.

Payroll Deductions

13. Mandatory payroll deductions consist of FICA taxes and income taxes.

a. These deductions do not result in payroll tax expense to the employer.

b. FICA taxes are designed to provide workers with supplemental retirement, employment disability, and medical benefits.

c. FICA taxes are also known as social security taxes.

14. Income taxes are required to be withheld from employees each pay period and the amount is determined by three variables: (a) the employees' gross earnings: (b) the number of allowances claimed by the employee; and (c) the length of the pay period.

15. Voluntary deductions pertain to withholdings for charitable, retirement, and other purposes. All voluntary deductions from gross earnings should be authorized in writing by the employee.

16. Net pay is determined by subtracting payroll deductions from gross earnings.

17. The employee earnings record provides a cumulative record of each employee's gross earnings, deductions, and net pay during the year. This record is used by the employer in:

a. Determining when an employee has earned the maximum earnings subject to FICA taxes.

b. Filing state and federal payroll tax returns.

c. Providing each employee with a statement of gross earnings and tax withholdings for the year.

18. Many companies use a payroll register to accumulate the gross earnings, deductions, and net pay by employee for each period. In some cases, this record is a journal or book of original entry.

19. The typical journal entry to record a payroll is as follows:

20. When the payroll is paid, Salaries and Wages Payable is debited and Cash is credited. Each payroll check is usually accompanied by a detachable statement of earnings document that shows the employee's gross earnings, payroll deductions, and net pay.

Employer Payroll Taxes

21. (L.O. 7) There are three taxes imposed on employers by government agencies that result in payroll tax expense.

a. FICA Taxes. The employer must match each employee's FICA contribution.

b. Federal Unemployment Taxes. The employer is required to pay a tax on the first $7,000 of gross wages paid to each employee during a calendar year.

c. State Unemployment Taxes. All states have unemployment compensation programs that require the employer to pay a tax on the first $7,000 of gross wages paid to each employee during a calendar year. This offsets the federal amount.

22. The typical entry for recording payroll tax expense is as follows:

23. Preparation of payroll tax returns is the responsibility of the payroll department; payment of the taxes is made by the treasurer's department.

24. The employer is required to provide each employee with a Wage and Tax Statement (Form W-2) by January 31 following the end of a calendar year. This statement shows gross earnings, FICA taxes withheld, and income taxes withheld for the year.

25. (L.O. 8) The objectives of internal accounting control concerning payroll are (a) to safeguard company assets from unauthorized payments of payrolls, and (b) to ensure the accuracy and reliability of the accounting records pertaining to payrolls.

26. The payroll activities consist of four functions (a) hiring employees, (b) timekeeping, (c) preparing the payroll, and (d) paying the payroll. These four functions should be assigned to different departments or individuals.

Additional Fringe Benefits

*27. (L.O. 9) When the compensation for paid absences (paid vacations, sick pay benefits, and paid holidays) is probable and the amount can be reasonably estimated, a liability should be accrued. The entry to record the liability will include a debit to vacation benefits expense and a credit to vacation benefits payable. When the amount cannot be reasonably estimated, the potential liability should be disclosed.

*28. (L.O. 9) Post-retirement benefits are benefits that employers provide to retired employees for (a) pensions, and (b) healthcare and life insurance.

*29. (L.O. 9) A pension plan is an agreement whereby an employer provides benefits (payments) to employees after they retire. The most popular type of pension plan is the 401(k) plan. When a company makes a contribution to the 401(k) plan on behalf of the employee, it debits pension expense and credits cash for the amount contributed.

*30. (L.O. 9) A defined-contribution plan defines the contribution an employer will make but not the benefit that the employee will receive at retirement. A 401(k) plan is an example of a defined-contribution plan. In a defined-benefit plan, the employer agrees to pay a defined amount to retirees, based on employees meeting certain eligibility standards.

*31. (L.O. 9) Companies estimate and expense post-retirement costs during the working years of the employee. The company rarely sets up funds to meet the cost of the future benefits.

A Look at IFRS

*32. (L.O. 10) IFRS and GAAP have similar definitions of liabilities.

*33. Under GAAP, some contingent liabilities are recorded in the financial statements, others are disclosed, and in some cases no disclosure is required. Unlike GAAP, IFRS reserves the use of the term contingent liability to refer only to possible obligations that are not recognized in the financial statements but may be disclosed if certain criteria are met.

*34. For those items that GAAP would treat as recordable contingent liabilities, IFRS instead uses the term “provisions”. Provisions are defined as liabilities of uncertain timing or amount.

*35. IFRS and GAAP separate plans into defined benefit and defined contribution. The accounting for defined contribution plans is similar. For defined benefit plans, there are still some technical differences in the reporting between GAAP and IFRS, but they plan on eliminating the differences in the future.

![]()

![]()

REVIEW QUESTIONS AND EXERCISES

Indicate whether each of the following is true (T) or false (F) in the space provided.

![]()

MULTIPLE CHOICE

Circle the letter that best answers each of the following statements.

- (L.O. 1) Which of the following statements concerning current liabilities is incorrect?

- Current liabilities include unearned revenues.

- A company that has more current liabilities than current assets is usually the subject of some concern.

- Current liabilities include prepaid expenses.

- A current liability is a debt that a company expects to pay within one year or the operating cycle, whichever is longer.

Items 2 and 3 pertain to the following information:

On October 1, 2014, Frederick Douglass Company issued a $28,000, 10%, nine-month interest-bearing note.

2. (L.O. 2) If the Frederick Douglass Company is preparing financial statements at December 31, 2014, the adjusting entry for accrued interest will include:

a. credit to Notes Payable of $700.

b. debit to Interest Expense of $700.

c. credit to Interest Payable of $1,400.

d. debit to Interest Expense of $1,050.

3. (L.O. 2) Assuming interest was accrued on June 30, 2015, the entry to record the payment of the note on July 1, 2015, will include a:

a. debit to Interest Expense of $700.

b. credit to Cash of $28,000.

c. debit to Interest Payable of $2,100.

d. debit to Notes Payable of $30,100.

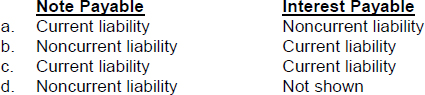

4. (L.O. 2 and 3) On August 1, 2014, a company borrowed cash and signed a one-year interest-bearing note on which both the face value and interest are payable on August 1, 2013. How will the note payable and the related interest be classified in the December 31, 2012, balance sheet?

5. (L.O. 3) The Pam Travis Company has total proceeds (before segregation of sales taxes) from sales of $2,100. If the sales tax is 5%, the amount to be credited to the account Sales Revenue is:

a. $2,100.

b. $1,995.

c. $1,900.

d. $2,000.

6. (L.O. 3) Assume that Carlson Theaters sells 5,000 movie tickets at $5 each for use by customers in the future. The entry for the sale of the advance tickets should include a

a. debit to unearned ticket revenue.

b. credit to cash.

c. credit to accounts payable.

d. credit to unearned ticket revenue.

7. (L.O. 3) Any balance in an unearned revenue account should be reported as

a. a current asset.

b. a current liability.

c. a revenue.

d. an expense.

8. (L.O. 4) Working capital is equal to:

a. current assets − current liabilities

b. current liabilities − current assets

c. long-term assets − current assets

d. current liabilities − long-term liabilities

9. (L.O. 4) The current ratio is:

a. long-term assets ÷ current assets

b. current liabilities ÷ current assets

c. current assets ÷ long-term assets

d. current assets ÷ current liabilities

10. (L.O. 4) Seth company has current assets of $40,000, current liabilities of $60,000, longterm assets of $80,000 and long-term liabilities of $50,000. Seth company's working capital and its current ratio are:

a. $40,000 and .66:1

b. −$20,000 and 2:1

c. $20,000 and .66:1

d. −20,000 and .66:1

11. (L.O. 5) How should a contingency that is reasonably possible and for which the amount can be reasonably estimated be handled?

12. (L.O. 5) A contingency need not be recorded nor disclosed when:

a. it is probable the contingency will happen and the amount can be reasonably estimated.

b. it is probable the contingency will happen but the amount cannot be reasonably estimated.

c. it is reasonably possible the contingency will happen and the amount can be reasonably estimated.

d. the possibility of the contingency happening is remote.

13. (L.O. 5) A contingency for which the amount can be reasonably estimated should be disclosed when the outcome of the contingency is:

14. (L.O. 6) Jan Turner, earns $16 per hour for a 40 hour work week and $24 per hour for overtime work. If Turner works 44 hours, her gross earnings are:

a. $704.

b. $736.

c. $836.

d. $1,056.

15. (L.O. 6) Lewis Latimer, an employee of Spottswood Company, has gross earnings for the month of October of $4,000. FICA taxes are 7.65% of gross earnings, federal income taxes amount to $635 for the month, state income taxes are 2% of gross earnings, and Lewis authorizes voluntary deductions of $10 per month to the United Fund. What is the net pay for Lewis Latimer?

a. $2,961.40.

b. $2,969.00

c. $2,965.00

d. $2,967.70

16. (L.O. 6) The journal entry to record the payroll for Marcus Garvey Company for the week ending January 8, would probably include a:

a. credit to Salaries and Wages Expense.

b. debit to Salaries and Wages Payable.

c. debit to Federal IncomeTaxes Payable.

d. credit to FICA Taxes Payable.

17. (L.O. 6) A tax that is also known as social security taxes is:

a. state income taxes.

b. federal income taxes.

c. Federal Insurance Contribution Act taxes.

d. federal unemployment taxes.

18. (L.O. 7) The journal entry for Hansberry Corporation to record employer payroll taxes will include a:

a. debit to Salaries and Wages Expense.

b. debit to State Unemployment Expense.

c. debit to FICA Taxes Payable.

d. debit to Payroll Tax Expense.

19. (L.O. 7) The record that provides a cumulative summary of each employee's gross earnings, payroll deductions, and net pay during the year and is required to be maintained to comply with state and federal law is the:

a. payroll register.

b. employee earnings record.

c. statement of earnings.

d. Wage and Tax Statement.

*20. (L.O. 9) DuBois Company employees are entitled to one day's vacation for each month worked. If an employee earns an average of $150 per day in a given month, the entry to accrue vacation benefits expense for the year for one employee will be as follows:

![]()

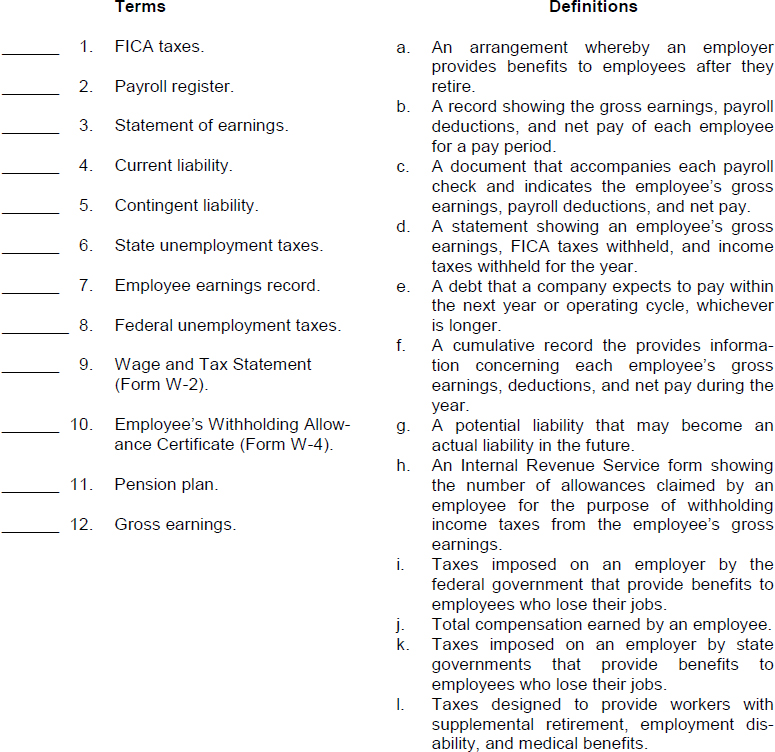

Match each term with its definition by writing the appropriate letter in the space provided.

![]()

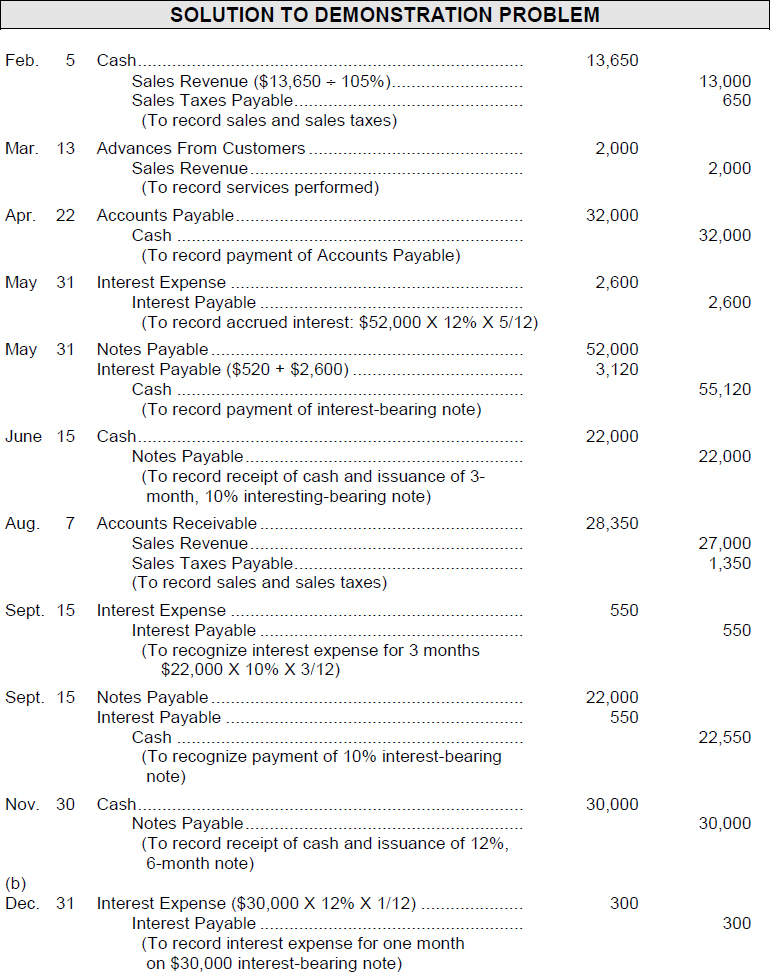

EX. 11-1 (L.O. 2 and 3) The following transactions took place during 2014 for Revel Pots and Pans Company:

| Aug. 1 | Borrowed $10,000 in cash from the Third National Bank by issuing a $10,000 eight-month, 12% interest-bearing note. |

| Dec. 1 | Borrowed $20,000 in cash from the Second Federal Savings & Loan by issuing a six-month, 10% interest-bearing note. |

| Dec. 24 | Determined from cash register readings that sales were $24,650 and sales taxes were $1,650. |

| Dec. 31 | Determined that it is probable and reasonably estimable that 400 units sold under warranty will be defective and that warranty repair costs will average $20 per unit. No warranty entries have been recorded during the year. |

Instructions

(a) Journalize the transactions above.

(b) Prepare the adjusting entries for the two notes at December 31, 2014.

(c) Record interest expense and payment of the two notes in 2015 at their maturity dates.

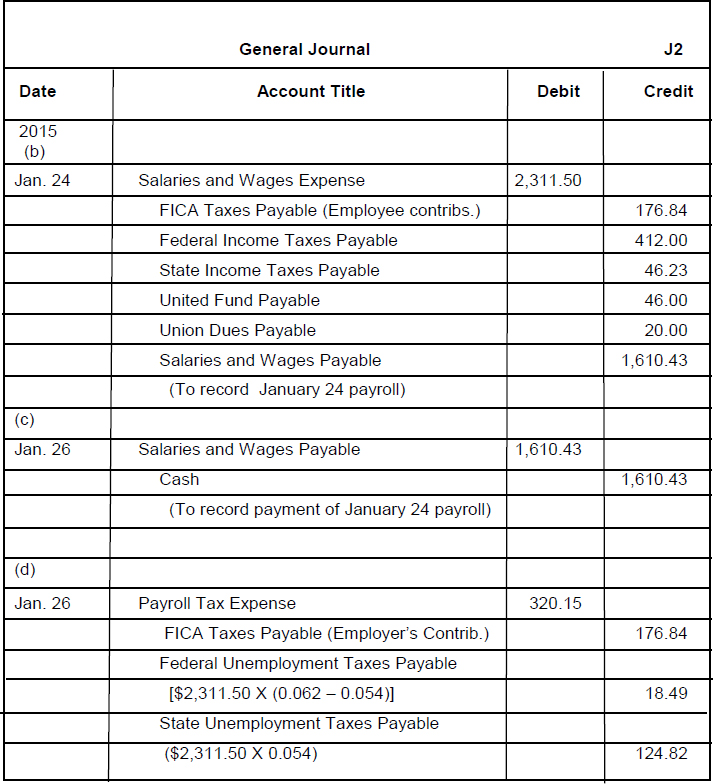

EX. 11-2 (L.O. 6) The following information pertains to the payroll of B.T. Washington Company for the week ended January 24, 2015. All hours over 40 are paid at one and one-half times the regular hourly rate.

Instructions

(a) Complete the schedule below. The state income tax rate is 2% of gross earnings and the FICA tax rate is 7.65% of gross earnings.

(b) Prepare the entry to record the payroll on January 24.

(c) Prepare the journal entry to record payment of the payroll on January 26.

(d) Record the employer's payroll taxes assuming state unemployment taxes are 5.4% and federal unemployment taxes are 0.8% (6.2% − 5.4%).

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

| 1. (F) | A current liability must meet both of the following criteria: (1) it is expected to be paid from existing current assets or through the creation of other current liabilities, and (2) it is expected to be paid within one year or the operating cycle, whichever is longer. |

| 2. (T) | |

| 3. (F) | Obligations in the form of written promissory notes are recorded as notes payable. |

| 4. (F) | Notes payable usually are issued to meet short-term financing needs. |

| 5. (T) | |

| 6. (F) | Unearned Revenues are classified as a current liability. |

| 7. (T) | |

| 8. (F) | Current liabilities are seldom listed in the order of maturity because of the varying maturity dates that may exist for a specific type of obligation such as notes payable. They are usually listed in order of magnitude. |

| 9. (T) | |

| 10. (F) | If a contingency is probable and it is reasonably estimable, the liability should be recorded in the accounts; a contingency that is possible and reasonably estimable should only be disclosed in the notes. |

| 11. (T) | |

| 12. (F) | The term payroll does not extend to payments made for personal service to the company by professionals, such as attorneys. These and other professional individuals are independent contractors, and payments to them are called fees rather than salaries and wages. |

| 13. (F) | FICA taxes are considered a mandatory deduction from employee earnings. |

| 14. (T) | |

| 15. (F) | The statement of earnings accompanies each payroll check and indicates the employee's gross earnings, payroll deductions, and net pay. The document that shows the data given in the true-false statement is the employee earnings record which is an internal document maintained by an employer to comply with state and federal laws. |

| 16. (T) | |

| 17. (T) | |

| 18. (T) | |

| 19. (T) | |

| 20. (T) |

MATCHING

- l

- b

- c

- e

- g

- k

- f

- i

- d

- h

- a

- j

EX. 11-1

EX. 11-2