5.8 CASE STUDY: HEDGING A FORECAST SALE AND SUBSEQUENT RECEIVABLE WITH A PARTICIPATING FORWARD

In this case, as in the previous cases, the cash flow stemming from a highly expected forecast sale and its ensuing receivable denominated in a foreign currency are hedged from a hedge accounting perspective. In this case, however, a participating forward is chosen to hedge the FX risk. The participating forward is one of the most basic and conservative hedges available. As its name implies, this hedge provides guaranteed protection, while allowing the entity some degree of “participation” in favourable movements of the EUR–USD exchange rate.

Suppose that on 1 October 20X4, ABC Corporation, a company whose functional currency was the EUR, was expecting to sell finished goods to a US client. The sale was expected to occur on 31 March 20X5, and the sale receivable was expected to be settled on 30 June 20X5. Sale proceeds were expected to be USD 100 million, to be received in USD.

ABC had the view that the USD could appreciate against the EUR in the following months and wanted to benefit were its view right. At the same time, ABC wanted full protection in case its view was wrong. As a consequence, on 1 October 20X4, ABC entered into a participating forward with the following terms:

| FX participating forward terms | |

| Start date | 1 October 20X4 |

| Counterparties | ABC and XYZ Bank |

| Maturity | 30 June 20X5 |

| ABC sells | USD 100 million |

| ABC buys | EUR 100 million/forward rate |

| Forward rate | 1.2760, if final spot ≥ 1.2760 1.2760 – (1.2760 – Final spot)/2, otherwise |

| Final spot | The EUR–USD spot rate at maturity |

| Premium | Zero |

| Settlement | Physical delivery |

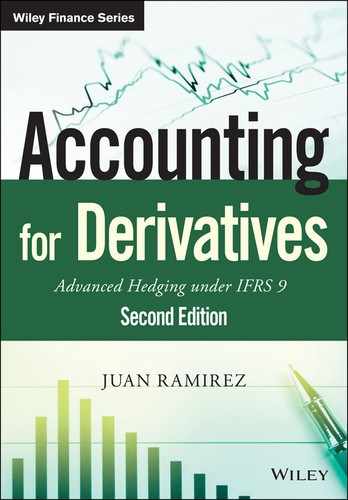

At maturity, ABC had the obligation to exchange USD 100 million for EUR at the forward rate. The forward rate was a function of the spot at maturity. The maximum forward rate was 1.2760. ABC participated in half of the USD appreciation below 1.2760. Figure 5.13 illustrates the resulting forward rate as a function of the EUR–USD spot rate at maturity. Figure 5.14 shows the EUR amount that ABC would receive in exchange for the USD 100 million, as a function of the EUR–USD spot rate at maturity.

Figure 5.13 Participating forward resulting forward rate.

Figure 5.14 Participating forward resulting EUR amount.

5.8.1 Participating Forward Hedge Accounting Issues

One of the fundamental issues that ABC faced regarding the participating forward was how to formalise the instrument in order to minimise volatility in profit or loss (i.e., to maximise its eligibility for hedge accounting). ABC considered the following choices:

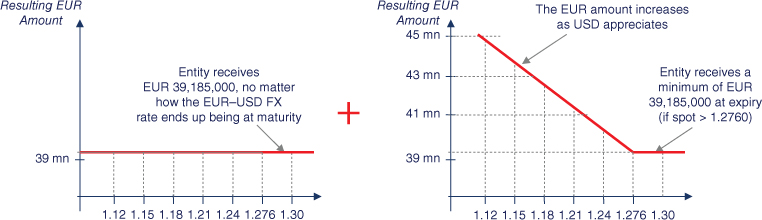

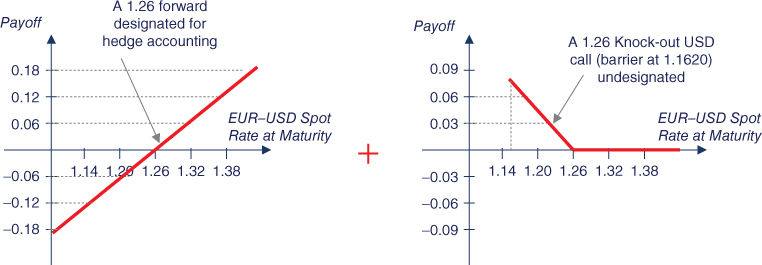

- Alternative 1. To divide the participating forward into the following two contracts (see Figure 5.15): (i) an FX forward at 1.2760 and a nominal of USD 50 million, and (ii) a purchase of a USD put with strike 1.2760 and a nominal of USD 50 million. Each contract would require a separate confirmation. This alternative should not encounter opposition from an external auditor as both the forward and the option are clearly eligible for designation as hedging instruments in a hedging relationship.

- Alternative 2. To designate the participating forward in its entirety as the hedging instrument. Whilst this alternative may bring some ineffectiveness, it is much simpler from an operational standpoint.

- Alternative 3. To divide the participating forward into the following two contracts: (i) a purchased USD put with strike 1.2760 and nominal 100 million, and (ii) a written USD call with strike 1.2760 and nominal 50 million. This alternative was discarded as it was likely to show a greater volatility in profit or loss than alternative 1 due to the recognition in profit or loss of the changes in the fair value of the written USD call.

Figure 5.15 Participating forward – resulting EUR amount.

In the following subsections I will cover the application of hedge accounting for alternatives 1 and 2.

5.8.2 Alternative 1: Participating Forward Split into a Forward and an Option

In this section the application of hedge accounting is covered step-by-step on a strategy in which our previous participating forward was split into two contracts (see Figure 5.15): (i) an FX forward contract at 1.2760 and a nominal of USD 50 million, and (ii) a purchase of a USD put contract with strike 1.2760 and a nominal of USD 50 million. Each contract required a separate confirmation to be considered as separate hedging instruments.

The terms of the two instruments were as follows:

| Hedge 1: FX forward terms | |

| Start date | 1 October 20X4 |

| Counterparties | ABC and XYZ Bank |

| Maturity | 30 June 20X5 |

| ABC sells | USD 50 million |

| ABC sells | EUR 39,185,000 |

| Forward rate | 1.2760 |

| Premium | ABC receives EUR 799,000 on the start date |

| Settlement | Physical delivery |

| Hedge 2: USD put/EUR call terms | |

| Start date | 1 October 20X4 |

| Option type | USD put/EUR call |

| Counterparties | ABC and XYZ Bank |

| Option buyer | ABC |

| Expiry | 30 June 20X5 |

| ABC buys | USD 50,000,000 |

| ABC sells | EUR 39,185,000 |

| Strike Rate | 1.2760 |

| Premium | ABC pays EUR 799,000 on the start date |

| Settlement | Physical delivery |

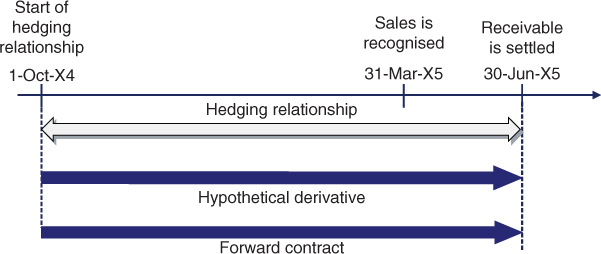

In our case, there would be two hedging relationships. Each would end on 30 June 20X5, when the two contracts matured (see Figure 5.16). On 31 March 20X5, the hedged cash flow (i.e., the sale) would be recognised in ABC's profit or loss and, simultaneously, any amounts previously recorded in equity would be reclassified to profit or loss. Also on 31 March 20X5, a receivable denominated in USD would be recognised in ABC's statement of financial position.

Figure 5.16 Hedge timeframe.

During the period from 31 March 20X5 until 30 June 20X5, in theory it would not be necessary to have a hedging relationship in place because there would already be an offset between FX gains and losses on the revaluation of the USD accounts receivable and revaluation gains and losses on the forward and the option. During that period ABC could implement two approaches:

- To continue the hedging relationship. Regarding the option, changes in the actual option time value, to the extent that they related to the hedged item, would be recorded in OCI and simultaneously reclassified to profit or loss.

- To discontinue the hedging relationship by changing the hedge's risk management objective on 31 March 20X5. As mentioned in our previous case, whilst this is a simpler approach, an auditor may find it contrary to the prohibition under IFRS 9 of voluntary discontinuation of a hedging relationship.

Hedging Relationship 1 – Documentation

At the inception of the first hedging relationship, ABC documented the relationship as follows:

| Hedging relationship 1 – documentation | |

| Risk management objective and strategy for undertaking the hedge | The objective of the hedge is to protect the EUR value of the cash flow stemming from a USD 50 million highly expected sale of finished goods and its ensuing receivable against unfavourable movements in the EUR–USD exchange rate. This hedging objective is consistent with the entity's overall FX risk management strategy of reducing the variability of its profit or loss statement caused by purchases and sales denominated in foreign currency. The designated risk being hedged is the risk of changes in the EUR fair value of the highly expected sale |

| Type of hedge | Cash flow hedge |

| Hedged item | The cash flow stemming from a USD 50 million sale of finished goods expected to be shipped on 31 March 20X5 and its payment expected to be received on 30 June 20X5. This sale is highly probable as similar transactions have occurred in the past with the potential buyer, for sales of similar size, and the negotiations with the buyer are at an advanced stage |

| Hedging instrument | The forward contract with reference number 014565. The main terms of the forward are a USD 50 million notional, a 1.2760 forward rate, a 30 June 20X5 maturity and a physical settlement provision. The counterparty to the forward is XYZ Bank and the credit risk associated with this counterparty is considered to be very low |

| Hedge effectiveness assessment | See below |

Hedge effectiveness will be assessed by comparing changes in the fair value of the hedging instrument in its entirety (i.e., both the forward and the spot elements are included in the hedging relationship) to changes in the fair value of a hypothetical derivative. The terms of the hypothetical derivative – a EUR–USD forward contract for maturity 30 June 20X5 with nil fair value at the start of the hedging relationship – reflected the terms of the hedged item. The terms of the hypothetical derivative are as follows:

| Hypothetical derivative 1 – terms | |

| Start date | 1 October 20X4 |

| Counterparties | ABC and credit risk-free counterparty |

| Maturity | 30 June 20X5 |

| ABC sells | USD 50 million |

| ABC buys | EUR 39,936,000 |

| Forward Rate | 1.2520 (*) |

(*) The forward rate of the hypothetical derivative (1.2520) was different from the forward rate of the hedging instrument (1.2760) – this was due to (i) their different initial fair values and (ii) the absence of CVA in the hypothetical derivative (the counterparty to the hypothetical derivative is assumed to be credit risk-free).

Changes in the fair value of the hedging instrument will be recognised as follows:

- The effective part of the gain or loss on the hedging instrument will be recognised in the cash flow hedge reserve of OCI. The accumulated amount in equity will be reclassified to profit or loss in the same period during which the hedged expected future cash flow affects profit or loss, initially adjusting the sale amount when the sale is recognised and thereafter adjusting the revaluation of the receivable.

- The ineffective part of the gain or loss on the hedging instrument will be recognised immediately in profit or loss.

Hedge effectiveness will be assessed prospectively at hedging relationship inception, on an ongoing basis at least upon each reporting date and upon occurrence of a significant change in the circumstances affecting the hedge effectiveness requirements.

Hedge effectiveness will be assessed, and effective/ineffective amounts will be calculated, on a forward-forward basis. In other words, the forward element of both the hedging instrument and the hypothetical derivative will be included in the hedging relationship.

The hedging relationship will qualify for hedge accounting only if all the following criteria are met:

- The hedging relationship consists only of eligible hedge items and hedging instruments. The hedge item is eligible as it is a highly expected forecast transaction that exposes the entity to fair value risk, affects profit or loss and is reliably measurable. The hedging instrument is eligible as it is a derivative and it does not result in a net written option.

- At hedge inception there is a formal designation and documentation of the hedging relationship and the entity's risk management objective and strategy for undertaking the hedge.

- The hedging relationship is considered effective.

The hedging relationship will be considered effective if the following three requirements are met:

- There is an economic relationship between the hedged item and the hedging instrument.

- The effect of credit risk does not dominate the value changes that result from that economic relationship.

- The hedge ratio of the hedging relationship is the same as that resulting from the quantity of hedged item that the entity actually hedges and the quantity of the hedging instrument that the entity actually uses to hedge that quantity of hedged item. The hedge ratio should not be intentionally weighted to create ineffectiveness.

Whether there is an economic relationship between the hedged item and the hedging instrument will be assessed on a qualitative basis. The assessment will be complemented by a quantitative assessment using the scenario analysis method for one scenario in which the EUR–USD FX rate at the end of the hedging relationship (30 June 20X5) will be calculated by shifting the EUR–USD spot rate prevailing on the assessment date by +10%, and the change in fair value of both the hypothetical derivative and the hedging instrument compared.

Hedging Relationship 2 – Documentation

Additionally, at the inception of the second hedging relationship, ABC documented the relationship as follows:

| Hedging relationship 2 – documentation | |

| Risk management objective and strategy for undertaking the hedge | The objective of the hedge is to protect the EUR value of the cash flow stemming from a USD 50 million highly expected sale of finished goods and its ensuing receivable against unfavourable movements in the EUR–USD exchange rate above 1.2760. This hedging objective is consistent with the entity's overall FX risk management strategy of reducing the variability of its profit or loss statement caused by purchases and sales denominated in foreign currency. The designated risk being hedged is the risk of changes in the EUR fair value of the highly expected sale |

| Type of hedge | Cash flow hedge |

| Hedged item | The cash flow stemming from a USD 50 million sale of finished goods expected to be shipped on 31 March 20X5 and its payment expected to be received on 30 June 20X5. This sale is highly probable as similar transactions have occurred in the past with the potential buyer, for sales of similar size, and the negotiations with the buyer are at an advanced stage |

| Hedging instrument | The intrinsic value of the purchased USD put/EUR call contract with reference number 014566. The main terms of the contract are a USD 50 million notional, a 1.2760 strike rate, a 30 June 20X5 maturity and a physical settlement provision. The counterparty to the option is XYZ Bank and the credit risk associated with this counterparty is considered to be very low |

| Hedge effectiveness assessment | See below |

Hedge effectiveness will be assessed, and effective/ineffective amounts will be calculated, by comparing changes in the fair value of the hedging instrument to changes in the fair value of a hypothetical derivative. The terms of the hypothetical derivative – a USD put/EUR call contract for maturity 30 June 20X5 with strike price 1.2760 reflected the terms of the hedged item. The terms of the hypothetical derivative are as follows:

| Hypothetical derivative 2 – terms | |

| Start date | 1 October 20X4 |

| Instrument | USD put/EUR call FX option |

| Counterparties | ABC and credit risk-free counterparty |

| Option buyer | ABC |

| Expiry | 30 June 20X5 |

| ABC buys | USD 50,000,000 |

| ABC sells | EUR 39,185,000 |

| Strike rate | 1.2760 |

| Initial aligned time value (premium) | EUR 820,000 |

| Settlement | Physical delivery |

Changes in the fair value of the hedging instrument (i.e., the option's intrinsic value) will be recognised as follows:

- The effective part of the gain or loss on the hedging instrument will be recognised in the cash flow hedge reserve of OCI. The accumulated amount in equity will be reclassified to profit or loss in the same period during which the hedged expected future cash flow affects profit or loss, initially adjusting the sales amount when the sale is recognised and thereafter adjusting the revaluation of the receivable.

- The ineffective part of the gain or loss on the hedging instrument will be recognised immediately in profit or loss.

The change in time value of the option will be excluded from the hedging relationship, and compared to the change in “aligned time” value. The aligned time value will be the time value of an option that has critical terms identical to those of the hedged item. Because, at the start of the hedging relationship, the aligned time value (EUR 820,000) exceeds the actual time value (EUR 799,000), the lower of their accumulated changes in fair value will be recognised temporarily in the time value reserve of OCI and reclassified to profit or loss when the hedged item impacts profit or loss. Any remainder will be recognised immediately in profit or loss.

Hedge effectiveness will be assessed prospectively at inception of the hedging relationship, on an ongoing basis at least upon each reporting date and upon occurrence of a significant change in the circumstances affecting the hedge effectiveness requirements.

The hedging relationship will qualify for hedge accounting only if all the following criteria are met:

- The hedging relationship consists only of eligible hedge items and hedging instruments. The hedge item is eligible as it is a highly expected forecast transaction that exposes the entity to fair value risk, affects profit or loss and is reliably measurable. The hedging instrument is eligible as it is a bought financial option.

- At hedge inception there is a formal designation and documentation of the hedging relationship and the entity's risk management objective and strategy for undertaking the hedge.

- The hedging relationship is considered effective.

The hedging relationship will be considered effective if the following three requirements are met:

- There is an economic relationship between the hedged item and the hedging instrument.

- The effect of credit risk does not dominate the value changes that result from that economic relationship.

- The hedge ratio of the hedging relationship is the same as that resulting from the quantity of hedged item that the entity actually hedges and the quantity of the hedging instrument that the entity actually uses to hedge that quantity of hedged item. The hedge ratio should not be intentionally weighted to create ineffectiveness.

Whether there is an economic relationship between the hedged item and the hedging instrument will be assessed on a qualitative basis. The assessment will be complemented by a quantitative assessment using the scenario analysis method for one scenario in which the EUR–USD FX rate at the end of the hedging relationship (30 June 20X5) will be established by shifting the EUR–USD spot rate prevailing on the assessment date by +10%, and the change in fair value (i.e., in time value) of both the hypothetical derivative and the hedging instrument compared.

Hedging Relationship 1 – Hedge Effectiveness Assessment Performed at Hedge Inception

The hedging relationship was considered effective as the following three requirements were met:

- There was an economic relationship between the hedged item and the hedging instrument. Based on the qualitative assessment performed and supported by a quantitative analysis, ABC concluded that the change in fair value of the hedged item was expected to be substantially offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

- The effect of credit risk did not dominate the value changes resulting from that economic relationship as the credit ratings of both the entity and XYZ Bank were considered sufficiently strong.

- The hedge ratio of the hedging relationship was the same as that resulting from the quantity of hedged item that the entity actually hedged and the quantity of the hedging instrument that the entity actually used to hedge that quantity of hedged item. The hedge ratio was not intentionally weighted to create ineffectiveness.

Due to the fact that the main terms (USD notional, underlying and expiry date) of the hedging instrument and those of the expected cash flow closely matched (with the exception of the forward rate) and the low credit risk exposure to the counterparty of the forward contract, it was concluded that the hedging instrument and the hedged item had values that would generally move in opposite directions. This conclusion was supported by a quantitative assessment. This assessment consisted of one scenario analysis performed as follows. A EUR–USD spot rate at the end of the hedging relationship (1.3585) was assumed by shifting the EUR–USD spot rate prevailing on the assessment date (1.2350) by +10%. As shown in the table below, the change in fair value of the hedged item is expected to be substantially offset by the change in fair value of the hedging instrument, corroborating that both elements have values that will generally move in opposite directions.

| Scenario analysis assessment | ||

| Hedging instrument | Hypothetical derivative | |

| Nominal USD | 50,000,000 | 50,000,000 |

| Forward rate | 1.2760 | 1.2520 |

| Nominal EUR | 39,185,000 | 39,936,000 |

| Nominal USD | 50,000,000 | 50,000,000 |

| Final spot rate | 1.3585 (1) | 1.3585 |

| Value in EUR | 36,805,000 (2) | 36,805,000 |

| Final fair value EUR | 2,380,000 (3) | 3,131,000 |

| Initial fair value EUR | <799,000> | Nil |

| Fair value change | 3,179,000 (4) | 3,131,000 |

| Degree of offset | 101.5% (5) | |

Notes:

(1) Assumed spot rate on hedging relationship end date

(2) 50,000,000/1.3585

(3) 39,185,000 – 36,805,000

(4) 2,380,000 – (<799,000>)

(5) 3,179,000/3,131,000

The hedge ratio was established at 1:1, resulting from the USD 50 million of hedged item that the entity actually hedged and the USD 50 million of the hedging instrument that the entity actually used to hedge that quantity of hedged item.

Another hedge assessment was performed on 31 December 20X4 (reporting date). This assessment was very similar to the one performed at inception and has been omitted to avoid unnecessary repetition. Additionally, the hedge ratio was assumed to be 1:1 on that assessment date.

Hedging Relationship 2 – Hedge Effectiveness Assessment Performed at Hedge Inception

The hedging relationship was considered effective as the following three requirements were met:

- There was an economic relationship between the hedged item and the hedging instrument. Based on the qualitative assessment performed and supported by a quantitative analysis, ABC concluded that the change in fair value of the hedged item was expected to be substantially offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

- The effect of credit risk did not dominate the value changes resulting from that economic relationship as the credit ratings of both the entity and XYZ Bank were considered sufficiently strong.

- The hedge ratio of the hedging relationship was the same as that resulting from the quantity of hedged item that the entity actually hedged and the quantity of the hedging instrument that the entity actually used to hedge that quantity of hedged item. The hedge ratio was not intentionally weighted to create ineffectiveness.

Due to the fact that the terms (notionals, underlying, strike price and expiry date) of the hedging instrument and those of the expected cash flow closely matched and the low credit risk exposure to the counterparty to the option contract, it was concluded that the hedging instrument and the hedged item had values that would generally move in opposite directions. This conclusion was supported by a quantitative assessment. This assessment consisted of one scenario analysis performed as follows. A EUR–USD spot rate at the end of the hedging relationship (1.3585) was simulated by shifting the EUR–USD spot rate prevailing on the assessment date (1.2350) by +10%. The fair value of the hedging instrument was calculated taking only the option intrinsic value. As shown in the table below, the change in fair value of the hedged item was expected to largely be offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

| Scenario analysis assessment | ||

| Hedging instrument | Hypothetical derivative | |

| Initial spot rate | 1.2350 | 1.2350 |

| Strike rate | 1.2760 | 1.2760 |

| Initial intrinsic value in EUR | Nil | Nil |

| Nominal USD | 50,000,000 | 50,000,000 |

| Spot rate | 1.3585 (1) | 1.3585 |

| Final intrinsic value in EUR | 2,380,000 (2) | 2,380,000 |

| Change in intrinsic value | 2,380,000 (3) | 2,380,000 |

| Degree of offset | 100% (4) | |

Notes:

(1) Assumed spot rate on 30 June 20X5 (hedging relationship end date)

(2) 2,380,000 = max[ 50,000,000/1.2760 – 50,000,000/1.3585, 0]

(3) 2,380,000 = 2,380,000 – Nil

(4) 100% = 2,380,000/2,380,000 = Change in fair value of hedging instrument/Change in fair value of hypothetical derivative. Remember that both fair values were only composed of intrinsic value.

The hedge ratio was established at 1:1, resulting from the USD 50 million of hedged item that the entity actually hedges and the USD 50 million of the hedging instrument that the entity actually uses to hedge that quantity of hedged item.

Another hedge assessment was performed on 31 December 20X4 (reporting date). This assessment was very similar to the one performed at inception and has been omitted to avoid unnecessary repetition. Additionally, the hedge ratio was assumed to be 1:1 on that assessment date.

Hedging Relationship 1 – Fair Valuations of Derivative Contracts and Hypothetical Derivative at the Relevant Dates

The actual spot and forward exchange rates prevailing at the relevant dates were as follows:

| Date | Spot rate at indicated date | Forward rate for 30-Jun-20X5 (*) | Discount factor for 30-Jun-20X5 |

| 1-Oct-20X4 | 1.2350 | 1.2520 | 0.9804 |

| 31-Dec-20X4 | 1.2700 | 1.2800 | 0.9839 |

| 31-Mar-20X5 | 1.2950 | 1.3000 | 0.9901 |

| 30-Jun-20X5 | 1.3200 | 1.3200 | 1.0000 |

(*) Credit risk-free forward rate

The fair value calculation of hedging instrument 1 at each relevant date was as follows:

| 1-Oct-20X4 | 31-Dec-20X4 | 31-Mar-20X5 | 30-Jun-20X5 | |

| Nominal EUR | 39,185,000 | 39,185,000 | 39,185,000 | 39,185,000 |

| Nominal USD | 50,000,000 | 50,000,000 | 50,000,000 | 50,000,000 |

| Forward rate for 30-Jun-20X5 (1) | /1.2520 | /1.2800 | /1.3000 | /1.3200 |

| Value in EUR | 39,936,000 | 39,063,000 | 38,462,000 (2) | 37,879,000 |

| Difference | <751,000> | 122,000 | 723,000 (3) | 1,306,000 |

| Discount factor | × 0.9804 | × 0.9839 | × 0.9901 | × 1.0000 |

| Credit risk-free fair value | <736,000> | 120,000 | 716,000 (4) | 1,306,000 |

| CVA | <63,000> | <1,000> | <2,000> | -0- |

| Fair value | <799,000> | 119,000 | 714,000 (5) | 1,306,000 |

| Fair value change (cumulative) | — | 918,000 | 1,513,000 (6) | 2,105,000 |

| Fair value change (period) | — | 918,000 | 595,000 (7) | 592,000 |

Notes:

(1) Credit risk-free forward rate

(2) 38,462,000 = 50,000,000/1.3000

(3) 723,000 = 39,185,000 – 38,462,000

(4) 716,000 = 723,000 × 0.9901

(5) 714,000 = 716,000 – 2,000

(6) 1,513,000 = 714,000 – <799,000>

(7) 595,000 = 714,000 – 119,000

The fair value calculation of hypothetical derivative 1 at each relevant date was as follows:

| 1-Oct-20X4 | 31-Dec-20X4 | 31-Mar-20X5 | 30-Jun-20X5 | |

| Nominal EUR | 39,936,000 | 39,936,000 | 39,936,000 | 39,936,000 |

| Nominal USD | 50,000,000 | 50,000,000 | 50,000,000 | 50,000,000 |

| Forward rate for 30-Jun-20X5 | /1.2520 | /1.2800 | /1.3000 | /1.3200 |

| Value in EUR | 39,936,000 | 39,063,000 | 38,462,000 | 37,879,000 |

| Difference | -0- | 873,000 | 1,474,000 | 2,057,000 |

| Discount factor | × 0.9804 | × 0.9839 | × 0.9901 | × 1.0000 |

| Fair value | -0- | 859,000 | 1,459,000 | 2,057,000 |

| Fair value change (Cumulative) | — | 859,000 | 1,459,000 | 2,057,000 |

The calculation of the effective and ineffective amounts of the change in fair value of the hedging instrument 1 was as follows:

| 31-Dec-20X4 | 31-Mar-20X5 | 30-Jun-20X5 | |

| Cumulative change in fair value of hedging instrument | 918,000 | 1,513,000 | 2,105,000 |

| Cumulative change in fair value of hypothetical derivative | 859,000 | 1,459,000 | 2,057,000 |

| Lower amount | 859,000 | 1,459,000 (1) | 2,057,000 |

| Previous cumulative effective amount | Nil | 859,000 (2) | 1,454,000 |

| Available amount | 859,000 | 600,000 (3) | 603,000 |

| Period change in fair value of hedging instrument | 918,000 | 595,000 (4) | 592,000 |

| Effective part | 859,000 | 595,000 (5) | 592,000 |

| Ineffective part | 59,000 | Nil (6) | Nil |

Notes:

(1) Lower of 1,513,000 and 1,459,000

(2) Nil +859,000, the sum of all prior effective amounts

(3) 1,459,000 – 859,000

(4) Change in the fair value of the hedging instrument since the last fair valuation

(5) Lower of 600,000 (available amount) and 595,000 (period change in fair value of hedging instrument)

(6) 595,000 (period change in fair value of hedging instrument) – 595,000 (effective part)

Hedging Relationship 2 – Fair Valuations of Hedged Item and Hypothetical Derivative at the Relevant Dates

Using the spot rates and discount factors from hedging relationship 1, the fair value of the option was calculated using the Black–Scholes model, and incorporating CVA/DVA. The intrinsic value was calculated using the spot rates. The time value of the option was calculated as follows:

The following table details the calculation of the changes in the option's intrinsic and time values from the option's total value. It is worth noting that although the option had no time value at the beginning and end of its life, its time value change showed a significant volatility.

| 1-Oct-20X4 | 31-Dec-20X4 | 31-Mar-20X5 | 30-Jun-20X5 | |

| Option fair value | 799,000 | 941,000 | 1,017,000 (1) | 1,306,000 |

| Expected cash flow in USD | 50,000,000 | 50,000,000 | 50,000,000 | 50,000,000 |

| USD put strike | /1.2760 | /1.2760 | /1.2760 | /1.2760 |

| EUR amount at USD put strike | 39,185,000 | 39,185,000 | 39,185,000 (2) | 39,185,000 |

| Expected cash flow in USD | 50,000,000 | 50,000,000 | 50,000,000 | 50,000,000 |

| Spot rate | /1.2350 | /1.2700 | /1.2950 | /1.3200 |

| EUR amount at spot | 40,486,000 | 39,370,000 | 38,610,000 (3) | 37,879,000 |

| Undiscounted intrinsic value | -0- | -0- | 575,000 (4) | 1,306,000 |

| Discount factor | × 0.9804 | × 0.9839 | × 0.9901 | × 1.0000 |

| Intrinsic value (credit risk-free) | -0- | -0- | 569,000 (5) | 1,306,000 |

| CVA/DVA | -0- | -0- | <1,000> | -0- |

| Option intrinsic value | -0- | -0- | 568,000 (6) | 1,306,000 |

| Option total fair value | 799,000 | 941,000 | 1,017,000 | 1,306,000 |

| Option intrinsic value | -0- | -0- | 568,000 | 1,306,000 |

| Option time value | 799,000 | 941,000 | 449,000 | -0- |

| Period fair value change | — | 142,000 | 76,000 (7) | 289,000 |

| Period intrinsic value change | — | -0- | 568,000 (8) | 738,000 |

| Period time value change | — | 142,000 | <492,000> (9) | <449,000> |

Notes:

(1) Calculated using Black–Scholes model

(2) 39,185,000 = 50,000,000/1.2760

(3) 38,610,000 = 50,000,000/1.2950

(4) 575,000 = max(39,185,000 – 38,610,000; 0)

(5) 569,000 = 575,000 × 0.9901

(6) 568,000 = 569,000 + <1,000>

(7) 76,000 = 1,017,000 – 941,000

(8) 568,000 = 568,000 – Nil

(9) <492,000> = 449,000 – 941,000

The following table shows the change in fair value of the hypothetical derivative. Remember that hypothetical derivatives have no time value, so only the change in its intrinsic value was calculated (it is noted below that the time value – the “aligned time value” – also needs to be calculated).

| Hypothetical derivative (i.e., intrinsic values) | ||||

| 1-Oct-20X4 | 31-Dec-20X4 | 31-Mar-20X5 | 30-Jun-20X5 | |

| Expected cash flow in USD | 50,000,000 | 50,000,000 | 50,000,000 | 50,000,000 |

| USD put strike | /1.2760 | /1.2760 | /1.2760 | /1.2760 |

| EUR amount at USD put strike | 39,185,000 | 39,185,000 | 39,185,000 | 39,185,000 |

| Expected cash flow in USD | 50,000,000 | 50,000,000 | 50,000,000 | 50,000,000 |

| Spot rate | /1.2350 | /1.2700 | /1.2950 | /1.3200 |

| EUR amount at spot | 40,486,000 | 39,370,000 | 38,610,000 | 37,879,000 |

| Undisc. intrinsic value | -0- | -0- | 575,000 | 1,306,000 |

| Discount factor | × 0.9804 | × 0.9839 | × 0.9901 | × 1.0000 |

| Intrinsic value | -0- | -0- | 568,000 | 1,306,000 |

| Intrinsic value change (cumulative) | — | -0- | 575,000 | 1,306,000 |

The calculation of the effective and ineffective parts of the change in fair value of the hedging instrument (i.e., the change in intrinsic value of the option) was calculated as follows:

| 31-Dec-20X4 | 31-Mar-20X5 | 30-Jun-20X5 | |

| Cumulative change in fair value of hedging instrument | -0- | 568,000 | 1,306,000 |

| Cumulative change in fair value of hypothetical derivative | -0- | 575,000 | 1,306,000 |

| Lower amount | -0- | 568,000 (1) | 1,306,000 |

| Previous cumulative effective amount | -0- | -0- (2) | 568,000 |

| Available amount | -0- | 568,000 (3) | 738,000 |

| Period change in fair value of hedging instrument | -0- | 568,000 (4) | 738,000 |

| Effective part | -0- | 568,000 (5) | 738,000 |

| Ineffective part | -0- | -0- (6) | -0- |

Notes:

(1) 568,000 = Lower of 568,000 and 575,000

(2) Nil = Sum of all prior effective amounts

(3) 568,000 = 568,000 – Nil = (1) – (2)

(4) Change in the fair value of the hedging instrument since the last fair valuation

(5) Lower of 568,000 (available amount) and 568,000 (period change in fair value of hedging instrument) = Lower of (3) and (4)

(6) Nil = 568,000 (period change in fair value of hedging instrument) – 568,000 (effective part)

Under IFRS 9 the cumulative change in fair value of the time value component of an option from the date of designation of the hedging instrument, is accumulated in OCI to the extent that it relates to the hedged item.

The time value related to the hedged item is called the “aligned time value”. This time value represents the time value of an option that would have critical terms perfectly matching those of the hedged item. In our case, the aligned time value corresponds to the time value of an option that has main terms identical to those of the hypothetical derivative (i.e., notional, strike rate, expiry date and underlying). Therefore, ABC had to compute the value changes in the hypothetical derivative, as if this derivative had time value (the “aligned option”). To do that, ABC had to compute first the fair value of the aligned option using Black–Scholes, and then the time value as follows:

The following table shows the calculations of the cumulative change in the aligned time value. The intrinsic value was the hypothetical derivative's intrinsic value, taken from the previous table.

| Aligned time value | ||||

| 1-Oct-20X4 | 31-Dec-20X4 | 31-Mar-20X5 | 30-Jun-20X5 | |

| Total fair value | 820,000 | 951,000 | 1,029,000 | 1,306,000 |

| Total intrinsic value | -0- | -0- | 575,000 | 1,306,000 |

| Aligned time value | 820,000 | 951,000 | 454,000 | -0- |

| Cumulative change in aligned time value | — | 131,000 | <366,000> | <820,000> |

Because at the start of the hedging relationship the actual time value (EUR 799,000) was lower than the aligned time value (EUR 820,000), the part of the cumulative fair value change of the actual time value recognised in OCI was calculated as the lower of the following (in absolute terms):

- the cumulative fair value change of the actual time value; and

- the cumulative fair value change of the aligned time value.

Any excess of the cumulative change in the option's time value over that of the aligned time value was recognised in profit or loss.

The comparison of the aligned amounts and the option's time value amounts was calculated as follows (the mechanics are similar to the previous calculation of effective and ineffective amounts related to the hedging instrument):

| 31-Dec-20X4 | 31-Mar-20X5 | 30-Jun-X5 | |

| Cumulative actual time value change | 142,000 | <350,000> | <799,000> |

| Cumulative aligned time value change | 131,000 | <366,000> | <820,000> |

| Lower amount | 131,000 | <350,000> | <799,000> |

| Previous cumulative amount in OCI | -0- | 131,000 | <350,000> |

| Available amount | 131,000 | <481,000> | <449,000> |

| Period change in actual time value | 142,000 | <492,000> | <449,000> |

| Part in OCI | 131,000 | <481,000> | <449,000> |

| Part in profit or loss | 11,000 | <11,000> | -0- |

Accounting Entries

The required journal entries were as follows.

- To record the forward and the option trades on 1 October, 20X4

At their inception, the fair values of the FX forward and the FX option were EUR <799,000> and 799,000 respectively.

- To record the closing of the accounting period on 31 December 20X4

The change in fair value of the forward since the last valuation was a EUR 918,000 gain, of which EUR 859,000 was considered to be effective and recorded in the cash flow hedge reserve of OCI, while EUR 59,000 was deemed to be ineffective and recorded in profit or loss.

- The change in fair value of the option since the last valuation was a gain of EUR 142,000, all due to a change in the option's time value. Of this amount 131,000 corresponded to an “aligned” time value change (recognised in the time value reserve of OCI) and the EUR 11,000 remainder was recognised in profit or loss.

- To record the sale agreement on 31 March 20X5

The sale agreement was recorded at the spot rate prevailing on that date (1.2950). Therefore, the sale EUR proceeds were EUR 77,220,000 (=100 million/1.2950). Because the machinery sold was not yet paid, a receivable was recognised. Suppose that the machinery was valued at EUR 68 million in ABC's statement of financial position.

- The change in fair value of the forward since the last valuation was a gain of EUR 595,000, fully considered to be effective, and thus recorded in the cash flow hedge reserve of OCI. No ineffective amounts existed.

- The change in fair value of the option since the last valuation was a gain of EUR 76,000, split into a EUR 568,000 gain in the option's intrinsic value and a EUR 492,000 loss in the option's time value. All the change in the option's intrinsic value was considered to be effective and recorded in the cash flow hedge reserve of OCI. Regarding the change in time value, <481,000> corresponded to an “aligned” time value change (recognised in the time value reserve of OCI) and the EUR <11,000> remainder was recognised in profit or loss.

- The recognition of the sales transaction in profit or loss caused the release to profit or loss of the deferred hedge results accumulated in equity: EUR 1,454,000 from the cash flow hedge reserve and EUR <350,000> from the time value reserve. The hedging relationship ended on this date.

- To record the settlement of the receivable and the derivatives on 30 June 20X5

The receivable was revalued at the spot rate prevailing on this date, showing a loss of EUR 1,463,000 (=100 million/1.3200 – 100 million/1.2950):

- The change in the fair value of the forward since the last valuation was a gain of EUR 592,000, fully deemed to be effective.

- The change in fair value of the option since the last valuation was a gain of EUR 289,000, split into a EUR 738,000 gain in the option's intrinsic value and a EUR 449,000 loss in the option's time value. All the change in the option's intrinsic value was considered to be effective and recorded in the cash flow hedge reserve of OCI. Regarding the change in time value, <449,000> corresponded to an “aligned” time value change (recognised in the time value reserve of OCI) and no amounts were recognised in profit or loss.

- The recognition of the revaluation of the accounts receivable in profit or loss caused the release to profit or loss of the deferred hedge results accumulated in equity: EUR 1,330,000 (=592,000 + 738,000) from the cash flow hedge reserve and EUR <449,000> from the time value reserve. The hedging relationship ended on this date.

- On 30 June, 20X5 ABC received the USD 100 million from the client and eliminated the related account receivable. The USD 100 million receipt was valued at that date's exchange rate, EUR 75,758,000 (=100 mn/1.3200):

- Simultaneously, both the forward and the option expired being exercised. Through the forward and the option, ABC sold USD 50 million, worth EUR 37,879,000, and received EUR 39,185,000. The fair value of the forward and the option just prior to settlement was EUR 1,306,000 (= 50 million × (1/1.2760 – 1/1.3200)).

The following table gives a summary of the accounting entries, excluding the entries related to the cost of goods sold:

| Cash | Forward and option contracts | Accounts receivable | Cash flow hedge reserve | Time value reserve | Profit or loss | |

| 1-Oct-20X4 | ||||||

| Forward trade | 799,000 | <799,000> | ||||

| Option trade | <799,000> | 799,000 | ||||

| 31 Dec-20X4 | ||||||

| Forward revaluation | 918,000 | 859,000 | 59,000 | |||

| Option revaluation | 142,000 | 131,000 | 11,000 | |||

| 31-Mar-20X5 | ||||||

| Forward revaluation | 595,000 | 595,000 | ||||

| Option revaluation | 76,000 | 568,000 | <481,000> | <11,000> | ||

| Reserve reclassification | <2,022,000> | 350,000 | 1,672,000 | |||

| Sale shipment | 77,220,000 | 77,220,000 | ||||

| 30-Jun-20X5 | ||||||

| Forward revaluation | 592,000 | 592,000 | ||||

| Option revaluation | 289,000 | 738,000 | <449,000> | |||

| Reserve reclassification | <1,330,000> | 449,000 | 881,000 | |||

| Forward settlement | 1,306,000 | <1,306,000> | ||||

| Option settlement | 1,306,000 | <1,306,000> | ||||

| Receivable revaluation | <1,463,000> | <1,463,000> | ||||

| Receivable settlement | 75,758,000 | <75,758,000> | ||||

| TOTAL | 78,370,000 | -0- | -0- | -0- | -0- | 78,370,000 |

(1) Note: Total figures may not match the sum of their corresponding components due to rounding.

5.8.3 Alternative 2(a): Participating Forward in its Entirety

In this subsection I will cover an approach to apply hedge accounting when (i) a participating forward is involved and (ii) the entity does not want to split the instrument (see previous subsection) for hedge accounting purposes due to its operational complexity.

Under this approach the hedging instrument was the participating forward in its entirety. The hedged item was composed of two elements:

- The cash flow stemming from the first USD 50 million of the highly expected forecast sale. The risk management objective related to this first element was to mitigate its variability against movements in the EUR–USD FX rate.

- The cash flow stemming from the second USD 50 million of the highly expected forecast sale. The risk management objective related to this second element was to mitigate its variability against adverse movements in the EUR–USD FX rate above 1.2760.

Hedging Relationship Documentation

Consequently, the hedging relationship was documented as follows:

| Hedging relationship documentation | |

| Risk management objective and strategy for undertaking the hedge | The objective of the hedge is twofold: Firstly, to mitigate the variability in EUR of the first USD 50 million cash flow stemming from a USD 100 million highly expected sale of finished goods and its ensuing receivable against unfavourable movements in the EUR–USD exchange rate. Secondly, to protect the EUR value of the second USD 50 million cash flow stemming from the above mentioned USD 100 million highly expected sale of finished goods and its ensuing receivable against unfavourable movements in the EUR–USD exchange rate above 1.2760. This hedging objective is consistent with the entity's overall FX risk management strategy of reducing the variability of its profit or loss statement caused by purchases and sales denominated in foreign currency. The designated risk being hedged is the risk of changes in the EUR value of the hedged cash flows due to movements in the EUR–USD exchange rate |

| Type of hedge | Cash flow hedge |

| Hedged item | The cash flow stemming from a USD 100 million sale of finished goods expected to be shipped on 31 March 20X5 and its payment expected to be received on 30 June 20X5. This sale is highly probable as similar transactions have occurred in the past with the potential buyer, for sales of similar size, and the negotiations with the buyer are at an advanced stage. Due to the two risk management objectives, for hedge assessment purposes, the hedged item was split into two highly expected cash flows of USD 50 million each, referred to as “hedged item 1” and “hedged item 2” |

| Hedging instrument | The participating forward contract with reference number 014569. The main terms of the participating forward are a USD 100 million notional, a forward rate that is a function of the EUR–USD spot rate at maturity (1.2760 – (1.2760 – final spot)/2), a 30 June 20X5 maturity and a physical settlement provision. The counterparty to the forward is XYZ Bank and the credit risk associated with this counterparty is considered to be very low |

| Hedge effectiveness assessment | See below |

Hedge Effectiveness Assessment

Hedge effectiveness will be assessed by comparing changes in the fair value of the hedging instrument in its entirety to changes in the fair value of the hedged cash flows for the risks being hedged.

Changes in the fair value of the hedging instrument will be recognised as follows:

- The effective part of the gain or loss on the hedging instrument will be recognised in the cash flow hedge reserve of OCI. The accumulated amount in equity will be reclassified to profit or loss in the same period during which the hedged expected future cash flow affects profit or loss, initially adjusting the sales amount when the sale is recognised and thereafter adjusting the revaluation of the receivable.

- The ineffective part of the gain or loss on the hedging instrument will be recognised immediately in profit or loss.

Hedge effectiveness will be assessed prospectively at hedging relationship inception, on an ongoing basis at least upon each reporting date and upon occurrence of a significant change in the circumstances affecting the hedge effectiveness requirements.

The hedging relationship will qualify for hedge accounting only if all the following criteria are met:

- The hedging relationship consists only of eligible hedge items and hedging instruments. The hedge item is eligible as it is a highly expected forecast transaction that exposes the entity to fair value risk, affects profit or loss and is reliably measurable. The hedging instrument is eligible as it is a derivative that does not result in a net written option.

- At hedge inception there is a formal designation and documentation of the hedging relationship and the entity's risk management objective and strategy for undertaking the hedge.

- The hedging relationship is considered effective.

The hedging relationship will be considered effective if the following three requirements are met:

- There is an economic relationship between the hedged item and the hedging instrument.

- The effect of credit risk does not dominate the value changes that result from that economic relationship.

- The hedge ratio of the hedging relationship is the same as that resulting from the quantity of hedged item that the entity actually hedges and the quantity of the hedging instrument that the entity actually uses to hedge that quantity of hedged item. The hedge ratio should not be intentionally weighted to create ineffectiveness.

Whether there is an economic relationship between the hedged item and the hedging instrument will be assessed on a quantitative basis using the scenario analysis method for two scenarios in which the EUR–USD FX rate at the end of the hedging relationship (30 June 20X5) will be calculated by shifting the EUR–USD spot rate prevailing on the assessment date by ±10%, and the change in fair value of both the hedging instrument and the hedged item compared.

Hedge Effectiveness Assessment Performed at the Start of the Hedging Relationship

The hedging relationship was considered effective as the following three requirements were met:

- There was an economic relationship between the hedged item and the hedging instrument. Based on the quantitative assessment performed (see below), the entity concluded that the change in fair value of the hedged item was expected to be largely offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

- The effect of credit risk did not dominate the value changes resulting from that economic relationship as the credit ratings of both the entity and XYZ Bank were considered sufficiently strong.

- The hedge ratio of the hedging relationship was the same as that resulting from the quantity of hedged item that the entity actually hedged and the quantity of the hedging instrument that the entity actually used to hedge that quantity of hedged item. The hedge ratio was not intentionally weighted to create ineffectiveness.

A quantitative assessment was performed using the scenario analysis method in which the performance of the hedging instrument and the hedged item was assessed under two scenarios.

In a first scenario, a EUR–USD spot rate at the end of the hedging relationship (1.3585) was assumed by shifting the EUR–USD spot rate prevailing on the assessment date (1.2350) by +10%. As shown in the table below, the change in fair value of the hedged item was expected to be largely offset by the change in fair value of the hedging instrument, corroborating that both elements have values that will generally move in opposite directions. Of note is that the hedged item was valued using forward rates (i.e., on a forward basis).

| First scenario analysis assessment | ||||

| Hedging instrument | Hedged item (1st element) | Hedged item (2nd element) | Hedged item (Total) | |

| Nominal USD | 100,000,000 | 50,000,000 | 50,000,000 | |

| Initial rate | 1.2760 (1) | 1.2520 (2) | 1.2760 (3) | |

| Nominal EUR | 78,370,000 (4) | 39,936,000 (5) | 39,185,000 (6) | |

| Nominal USD | 100,000,000 | 50,000,000 | 50,000,000 | |

| Final rate | 1.3585 (7) | 1.3585 | 1.3585 | |

| Value in EUR | 73,611,000 (8) | 36,805,000 (9) | 36,805,000 (9) | |

| Final fair value EUR | 4,759,000 (10) | <3,131,000> (11) | <2,380,000> (12) | |

| Initial fair value EUR | Nil | Nil | Nil | |

| Fair value change | 4,759,000 (13) | <3,131,000> | <2,380,000> | <5,511,000> |

| Degree of offset | 86.4% (14) | |||

Notes:

(1) Instrument forward rate when final FX rate was 1.3585

(2) According to its risk management objective, the 1st hedged item was fully protected (i.e., from 1.2520, the expected rate on 30-Jun-X5 as of the start of the hedging relationship)

(3) According to its risk management objective, the 2nd hedged item was protected from 1.2760

(4) 100,000,000/1.2760

(5) 50,000,000/1.2520

(6) 50,000,000/1.2760

(7) Spot rate at the end of the hedging relationship

(8) 100,000,000/1.3585

(9) 50,000,000/1.3585

(10) 78,370,000 – 73,611,000

(11) 36,805,000 – 39,936,000

(12) 36,805,000 – 39,185,000

(13) 4,759,000 – Nil

(14) 4,759,000/(– <5,511,000>)

In a second scenario, a EUR–USD spot rate at the end of the hedging relationship (1.1115) was assumed by shifting the EUR–USD spot rate prevailing on the assessment date (1.2350) by –10%. As shown in the table below, the change in fair value of the hedged item was expected to be largely offset by the change in fair value of the hedging instrument, corroborating that both elements have values that will generally move in opposite directions.

| Second scenario analysis assessment | ||||

| Hedging instrument | Hedged item (1st element) | Hedged item (2nd element) | Hedged item (Total) | |

| Nominal USD | 100,000,000 | 50,000,000 | ||

| Initial rate | 1.1938 (1) | 1.2520 (2) | ||

| Nominal EUR | 83,766,000 (3) | 39,936,000 (4) | ||

| Nominal USD | 100,000,000 | 50,000,000 | ||

| Final rate | 1.1115 (5) | 1.1115 (5) | ||

| Value in EUR | 89,969,000 (6) | 44,984,000 (7) | ||

| Final fair value EUR | <6,202,000> (8) | 5,048,000 (9) | Nil (10) | |

| Initial fair value EUR | Nil | Nil | Nil | |

| Fair value change | <6,202,000> (11) | 5,048,000 | Nil | 5,048,000 |

| Degree of offset | 122.9% (12) | |||

Notes:

(1) Instrument forward rate when final FX rate was 1.1115

(2) According to its risk management objective, the 1st hedged item was fully protected (i.e., from 1.2520, the expected rate on 30-Jun-X5 as of the start of the hedging relationship)

(3) 100,000,000/1.1938

(4) 50,000,000/1.2520

(5) Spot rate at the end of the hedging relationship

(6) 100,000,000/1.1115

(7) 50,000,000/1.1115

(8) 83,766,000 – 89,969,000

(9) 44,984,000 – 39,936,000

(10) According to its risk management objective, the 2nd hedged item was protected from 1.2760. Because the spot rate (1.1115) was below the spot rate at which the protection kicked in, the 2nd hedged item was not taken into account for this scenario analysis

(11) <6,202,000> – Nil

(12) <6,202,000>/(–5,048,000)

Under the two scenarios, the degree of offset was notably high. Under the second scenario, the degree of offset exceeded 100% because the hedging instrument benefited on just half of the appreciation of the USD relative to the EUR below 1.2760, while the hedged item benefited fully from such appreciation. In any case, the entity concluded that the degree of offset under the two scenarios were large enough to conclude that an economic relationship existed between the hedging instrument and the hedged item.

The hedge ratio was established at 1:1, resulting from the USD 100 million of hedged item that the entity actually hedged and the USD 100 million of the hedging instrument that the entity actually used to hedge that quantity of hedged item.

Another hedge assessment was performed on 31 December 20X4 (reporting date). This assessment was very similar to the one performed at inception and has been omitted to avoid unnecessary repetition. Additionally, the hedge ratio was assumed to be 1:1 on that assessment date.

Fair Valuations on 31 December 20X4

The fair valuations of the hedging instrument were calculated in the previous subsection. The fair value of the participating forward (EUR 1,060,000) was the sum of the fair values of the forward (EUR 119,000) and option (EUR 941,000) embedded contracts.

The fair valuation of the hedged item on 31 December 20X4 was performed on a forward basis based on a forward rate for 30 June 20X5 of 1.2800 and a 0.9839 discount factor as follows:

| Hedged item 1 | Hedged item 2 | |

| Nominal EUR | 39,936,000 (1) | 39,185,000 (2) |

| Nominal USD | 50,000,000 | 50,000,000 |

| Rate for 30-Jun-20X5 | /1.2800 (3) | /1.2800 |

| Value in EUR | 39,063,000 (4) | 39,063,000 (4) |

| Difference | <873,000> (5) | <122,000> |

| Discount factor | × 0.9839 | × 0.9839 |

| Fair value | <859,000> (6) | <120,000> |

| Fair value change (Cumulative) | <859,000> (7) | <120,000> |

| Total fair value | <979,000> (8) |

Notes:

(1) 50,000,000/1.2520

(2) 50,000,000/1.2760

(3) Forward rate for 30 June 20X5 as of the valuation date

(4) 50,000,000/1.2800

(5) 39,063,000 – 39,936,000

(6) <873,000> × 0.9839

(7) <859,000> minus its initial fair value, which was nil

(8) <859,000> + <120,000>

The following table summarises the changes in values of both the hedging instrument and the hedged item:

| 31-Dec-20X4 | |

| Participating forward fair value | 1,060,000 |

| Participating forward previous fair value | -0- |

| Change in participating forward fair value (period) | 1,060,000 |

| Change in participating forward fair value (cumulative) | 1,060,000 |

| Hedged item fair value | <979,000> |

| Change in hedged item fair value (cumulative) | <979,000> |

Fair Valuations on 31 March 20X5

The fair valuations of the hedging instrument were calculated in the previous subsection. The fair value of the participating forward (EUR 1,731,000) was the sum of the fair values of the forward (EUR 714,000) and the option (EUR 1,017,000) embedded contracts.

The fair valuation of the hedged item on 31 March 20X5 was performed on a forward basis based on a forward rate for 30 June 20X5 of 1.3000 and a 0.9901 discount factor as follows:

| Hedged item 1 | Hedged item 2 | |

| Nominal EUR | 39,936,000 | 39,185,000 |

| Nominal USD | 50,000,000 | 50,000,000 |

| Rate for 30-Jun-20X5 | /1.3000 | /1.3000 |

| Value in EUR | 38,462,000 | 38,462,000 |

| Difference | <1,474,000> | <723,000> |

| Discount factor | × 0.9901 | × 0.9901 |

| Fair value | <1,459,000> | <716,000> |

| Total fair value | <2,175,000> |

The following table summarises the changes in values of both the hedging instrument and the hedged item:

| 31-March-20X5 | |

| Participating forward fair value | 1,731,000 |

| Participating forward previous fair value | 1,060,000 |

| Change in participating forward fair value (period) | 671,000 |

| Change in participating forward fair value (cumulative) | 1,731,000 |

| Hedged item fair value | <2,175,000> |

| Change in hedged item fair value (cumulative) | <2,175,000> |

Fair Valuations on 30 June 20X5

The fair valuations of the hedging instrument were calculated in the previous subsection. The fair value of the participating forward (EUR 2,612,000) was the sum of the fair values of the forward (EUR 1,306,000) and the option (EUR 1,306,000) embedded contracts.

The fair valuation of the hedged item on 30 June 20X5 was performed based on a spot rate of 1.3200 and a 1.0000 discount factor as follows:

| Hedged Item 1 | Hedged Item 2 | |

| Nominal EUR | 39,936,000 | 39,185,000 |

| Nominal USD | 50,000,000 | 50,000,000 |

| Rate for 30-Jun-20X5 | /1.3200 | /1.3200 |

| Value in EUR | 37,879,000 | 37,879,000 |

| Difference | <2,057,000> | <1,306,000> |

| Discount factor | × 1.0000 | × 1.0000 |

| Fair value | <2,057,000> | <1,306,000> |

| Total fair value | <3,363,000> |

The following table summarises the changes in values of both the hedging instrument and the hedged item:

| 30-Jun-20X5 | |

| Participating forward fair value | 2,612,000 |

| Participating forward previous fair value | 1,731,000 |

| Change in participating forward fair value (period) | 881,000 |

| Change in participating forward fair value (cumulative) | 2,612,000 |

| Hedged item fair value | <3,363,000> |

| Change in hedged item fair value (cumulative) | <3,363,000> |

Calculation of Effective and Ineffective Amounts

The calculation of the effective and ineffective parts of the period change in fair value of the participating forward was performed as follows:

| 31-Dec-20X4 | 31-Mar-20X5 | 30-Jun-20X5 | |

| Cumulative change in fair value of hedging instrument | 1,060,000 | 1,731,000 | 2,612,000 |

| Cumulative change in fair value of hedged item (opposite sign) | 979,000 | 2,175,000 | 3,363,000 |

| Lower amount | 979,000 | 1,731,000 | 2,612,000 |

| Previous cumulative effective amount | -0- | 979,000 | 1,650,000 |

| Available amount | 979,000 | 752,000 | 962,000 |

| Period change in fair value of hedging instrument | 1,060,000 | 671,000 | 881,000 |

| Effective part | 979,000 | 671,000 | 881,000 |

| Ineffective part | 81,000 | Nil | Nil |

Accounting Entries

The required journal entries were as follows.

- To record the forward and the option trades on 1 October, 20X4

At their inception, the fair value of the participating forward was zero. Consequently, no on-balance-sheet accounting entries were required.

- To record the closing of the accounting period on 31 December 20X4

The change in fair value of the participating forward since the last valuation was a EUR 1,060,000 gain, of which EUR 979,000 was deemed to be effective and recorded in the cash flow hedge reserve of equity, while EUR 81,000 was deemed to be ineffective and recorded in profit or loss.

- To record the sale agreement on 31 March 20X5

The sale agreement was recorded at the spot rate prevailing on that date (1.2950). Therefore, the sale EUR proceeds were EUR 77,220,000 (=100 million/1.2950). Because the machinery sold was not yet paid, a receivable was recognised. Suppose that the machinery was valued at EUR 68 million in ABC's statement of financial position.

- The change in fair value of the participating forward since the last valuation was a gain of EUR 671,000, fully considered to be effective and recorded in the cash flow hedge reserve of OCI.

- The recognition of the sales transaction in profit or loss caused the release to profit or loss of the EUR 1,650,000 deferred hedge results accumulated in the cash flow hedge reserve of equity.

- To record the settlement of the receivable and the derivatives on 30 June 20X5

The receivable was revalued at the spot rate prevailing on this date, showing a loss of EUR 1,463,000 (=100 million/1.3200 – 100 million/1.2950):

- The change in the fair value of the participating forward since the last valuation was a gain of EUR 881,000, fully deemed to be effective.

- The recognition of the revaluation of the accounts receivable in profit or loss caused the release to profit or loss of the EUR 881,000 deferred hedge results accumulated in the cash flow hedge reserve equity. The hedging relationship ended on this date.

- On 30 June, 20X5, ABC received the USD 100 million from the client and eliminated the related account receivable. The USD 100 million receipt was valued at that date's exchange rate, EUR 75,758,000 (=100 mn/1.3200):

- Simultaneously, the participating forward was settled: ABC sold USD 100 million, worth EUR 75,758,000, and received EUR 78,370,000. The fair value of the participating forward just prior to its settlement was EUR 2,612,000 (= 100 million × (1/1.2760 – 1/1.3200)).

The following table gives a summary of the accounting entries, excluding the entries related to the cost of goods sold:

| Cash | Participating forward | Accounts receivable | Cash flow Hedge reserve | Profit or loss | |

| 1-Oct-20X4 | |||||

| No entries | |||||

| 31 Dec-20X4 | |||||

| Partic. forward revaluation | 1,060,000 | 979,000 | 81,000 | ||

| 31-Mar-20X5 | |||||

| Partic. forward revaluation | 671,000 | 671,000 | |||

| Reserve reclassification | <1,650,000> | 1,650,000 | |||

| Sale shipment | 77,220,000 | 77,220,000 | |||

| 30-Jun-20X5 | |||||

| Partic. forward revaluation | 881,000 | 881,000 | |||

| Reserve reclassification | <881,000> | 881,000 | |||

| Partic. forward settlement | 2,612,000 | <2,612,000> | |||

| Receivable revaluation | <1,463,000> | <1,463,000> | |||

| Receivable settlement | 75,758,000 | <75,758,000> | |||

| TOTAL | 78,370,000 | -0- | -0- | -0- | 78,370,000 |

(1) Note: Total figures may not match the sum of their corresponding components due to rounding.

5.8.4 Alternative 2(b): Participating Forward in its Entirety – Readjusting the Hedge Ratio

Suppose that ABC decided to consider the whole participating forward as one instrument and, from an accounting perspective, tried to designate it as the hedging instrument in a hedging relationship. In this subsection I will cover an uncommon approach to the application of hedge accounting: the rebalancing approach. This approach rebalances the hedge ratio to changes in the circumstances surrounding a hedging relationship.

The rebalancing approach is an interesting alternative for the application of hedge accounting when exotic options are involved and either (i) it is not feasible a split of the derivative between a hedge accounting friendly part and an undesignated part or (ii) designating the derivative in its entirety results in economic assessments that are too dependent on the path followed by the underlying market variable. The rebalancing approach starts by estimating the quantity of hedged item that would be hedged with the quantity of derivative actually traded. Whilst this approach is notably less attractive than the two previous ones due to its complexity, I have included it is an interesting way to approach more structured hedges.

This approach is like starting to build a house from the roof down. It commences by calculating a preliminary hedge ratio at the inception of the hedging relationship, and subsequently adjusting it for changes in the EUR–USD FX rate. A hedge ratio provides the quantity of participating forward that on a “forward looking” basis provides the best hedge of the quantity of hedged item (i.e., the highly expected forecast sale denominated in USD).

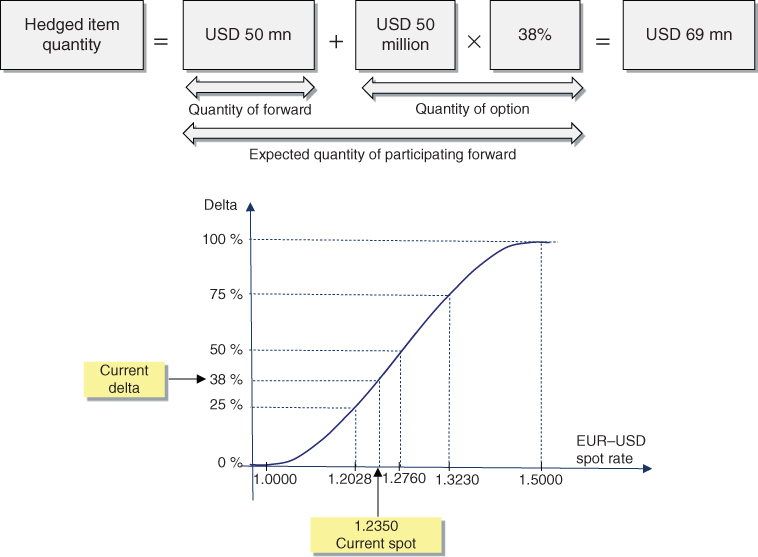

I describe two alternative methods to estimate the preliminary hedge ratio: (i) using the implied delta and (ii) using historical market rates. My suggestion is to use the first method as it is the best estimate of the market expectations for the hedge ratio.

Preliminary Hedge Ratio Estimation Using Implied Delta

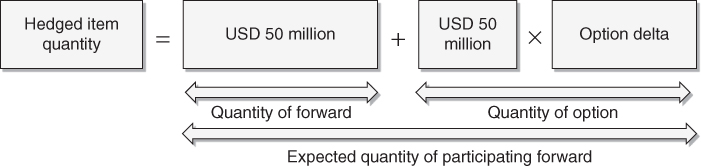

It was shown earlier that our participating forward could be split into two contracts (see Figure 5.15): (i) an FX forward at 1.2760 and a nominal of USD 50 million, and (ii) a purchase of a USD put with strike 1.2760 and USD 50 million nominal. The quantity of participating forward was the sum of the quantities of the forward and the option:

The quantity of forward to be used by ABC was USD 50 million as its probability of being exercised was 100% (i.e., there is no optionality in a forward as both parties will be obliged to exchange the notional amounts at maturity).

Whilst the quantity of forward was known, the quantity of option to be used by ABC depended on the EUR–USD spot rate at expiry. If the EUR–USD spot rate was above 1.2760, ABC would fully exercise the option, which may be interpreted as ABC using a USD 50 million quantity of the option. Alternatively, if the spot rate was at or below 1.2760 at expiry, ABC would not exercise the option, or in other words, ABC would not use any quantity of the option. Whilst ex ante ABC did not know whether the option would be exercised, the entity could estimate the option's probability of being exercised, which is approximated by the option's delta.

In order to calculate the appropriate hedge ratio, the quantity of hedged item should equal the quantity of participating forward. As noted above, the quantity of participating forward is unknown at the commencement of the hedging relationship and can be estimated according to the following expression:

As mentioned previously, the quantity of forward was USD 50 million as the probability of “exercising” the forward was 100%. The probability of exercising an option can be approximated by using its delta. Therefore, the quantity of hedged item can be estimated as:

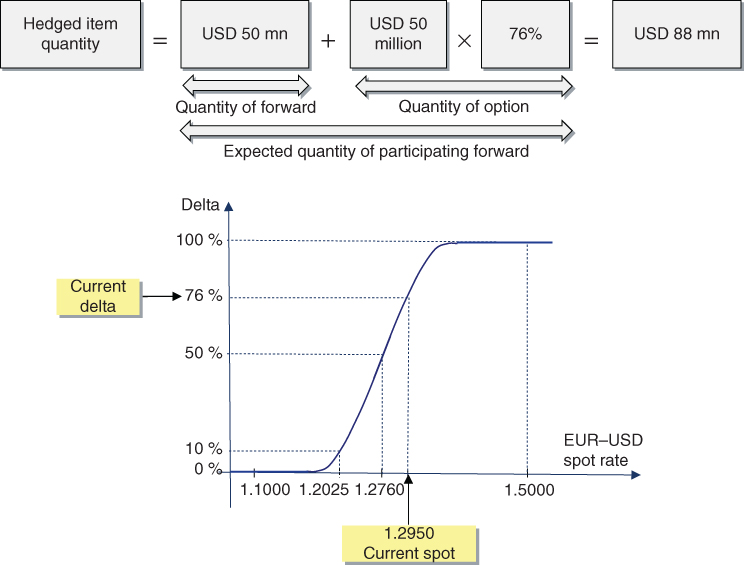

An option delta indicates the theoretical change in an option price with respect to changes in the price of the underlying price/rate. When the underlying price/rate changes by a small amount, the option price changes by the delta multiplied by that amount. The delta is commonly expressed as a percentage, measuring the change in an option price for a 1% change in the underlying price/rate.

The absolute value of the delta can be loosely interpreted as an approximate measure of the probability that an option will expire in-the-money (i.e., be exercised). If an option is very deep in-the-money, and therefore has a very high probability of being in-the-money at expiry, the absolute value of the delta will be close to 100%. If an option is very deep out-of-the-money, it has a low probability of being in-the-money at expiry, and therefore the absolute value of its delta will be close to zero. At-the-money options have a delta close to 50%, meaning roughly a 50% probability of being exercised at expiry. In our case, on 1 October 20X4 the delta of our option was 38%, using the Black–Scholes pricing model. The option delta as a function of the EUR–USD spot rate on that date had the profile depicted in Figure 5.17, showing that for example had the spot rate been 1.2028 the delta would have been 25%.

Figure 5.17 Option delta on 1 October 20X4.

As a result, the hedge ratio was established at 0.69:1, and USD 69 million of the hedged item was hedged using USD 100 million of the participating forward.

Preliminary Hedge Ratio Estimation Using Historical Data

A second method to estimate a preliminary hedge ratio is to simulate the historical performance of the hedging relationship using actual EUR–USD spot rate past behaviour and calculating the quantity of participating forward that the entity would have used. The following table details a hedge ratio estimation using monthly observations during the previous 2 years. For example, on 1 May 20X2 the EUR–USD spot rate was 1.3197, a 6-month hedging relationship would have finished on 31 October 20X2 and the spot rate on this date was 1.2489, while the participating forward rate would have been 1.3607, resulting in a USD 50 million quantity being used as the option element would not have been exercised.

According to the behaviour of the EUR–USD spot rate during the period from 1-May-X2 to 1-Apr-X4, the average quantity would have been USD 64,583,000, implying a 0.65:1 hedge ratio.

| Date | Spot start hedging relationship | Spot end hedging relationship | Participating forward rate | Quantity used |

| 1-May-X2 | 1.3197 | 1.2489 | 1.3607 | 50,000,000 |

| 1-Jun-X2 | 1.3175 | 1.2433 | 1.3585 | 50,000,000 |

| 1-Jul-X2 | 1.3016 | 1.2129 | 1.3426 | 50,000,000 |

| 1-Aug-X2 | 1.2783 | 1.2210 | 1.3193 | 50,000,000 |

| 1-Sep-X2 | 1.2501 | 1.1919 | 1.2911 | 50,000,000 |

| 1-Oct-X2 | 1.2869 | 1.1906 | 1.3279 | 50,000,000 |

| 1-Nov-X2 | 1.2489 | 1.2078 | 1.2899 | 50,000,000 |

| 1-Dec-X2 | 1.2433 | 1.1716 | 1.2843 | 50,000,000 |

| 1-Jan-X3 | 1.2129 | 1.1970 | 1.2539 | 50,000,000 |

| 1-Feb-X3 | 1.2210 | 1.2715 | 1.2620 | 100,000,000 |

| 1-Mar-X3 | 1.1919 | 1.2456 | 1.2329 | 100,000,000 |

| 1-Apr-X3 | 1.1906 | 1.2534 | 1.2316 | 100,000,000 |

| 1-May-X3 | 1.2078 | 1.1897 | 1.2488 | 50,000,000 |

| 1-Jun-X3 | 1.1716 | 1.1875 | 1.2126 | 50,000,000 |

| 1-Jul-X3 | 1.1970 | 1.1716 | 1.2380 | 50,000,000 |

| 1-Aug-X3 | 1.2522 | 1.1483 | 1.2932 | 50,000,000 |

| 1-Sep-X3 | 1.2126 | 1.1201 | 1.2536 | 50,000,000 |

| 1-Oct-X3 | 1.2104 | 1.1569 | 1.2514 | 50,000,000 |

| 1-Nov-X3 | 1.1897 | 1.1271 | 1.2307 | 50,000,000 |

| 1-Dec-X3 | 1.1875 | 1.2110 | 1.2285 | 50,000,000 |

| 1-Jan-X4 | 1.1716 | 1.2250 | 1.2126 | 100,000,000 |

| 1-Feb-X4 | 1.1483 | 1.2233 | 1.1893 | 100,000,000 |

| 1-Mar-X4 | 1.1201 | 1.1985 | 1.1611 | 100,000,000 |

| 1-Apr-X4 | 1.1569 | 1.2123 | 1.1979 | 100,000,000 |

| Average quantity used: | USD 64,583,000 |

In order to avoid unnecessary repetition, I will cover next only the elements of the hedge that are particularly specific to this case. I will be using a preliminary hedge ratio of 0.69:1

Hedged Item Description in the Hedging Relationship Documentation

The hedged item was defined in the hedge documentation as follows: “USD 69 million sale of finished goods expected to take place on 31 March 20X5. This sale is highly probable as similar transactions have occurred in the past with the potential buyer, for sales of similar size, and the negotiations with the buyer are at an advanced stage. The amount of hedged item will be adjusted in accordance with the hedge ratio.”

Hedging Instrument Description in the Hedging Relationship Documentation

The hedged item was defined in the hedge documentation as follows: “The participating forward contract with reference number 014565. The notional of the instrument is USD 100 million, its rate is 1.2760 and its maturity on 30 June 20X5. The counterparty to the instrument is XYZ Bank and the credit risk associated with this counterparty is considered to be very low.”

Hypothetical Derivative

The initial terms of the hypothetical derivative were as follows:

| Hypothetical derivative – terms | |

| Instrument | FX forward |

| Start date | 1 October 20X4 |

| Counterparties | ABC and credit risk-free counterparty |

| Maturity | 30 June 20X5 |

| ABC sells | USD 69 million |

| ABC buys | EUR 55,112,000 |

| Forward rate | 1.2520 |

| Initial fair value | Zero |

The notionals of the hypothetical derivative will be adjusted to reflect adjustments to the quantity of hedged item as a result of changes to the hedge ratio.

Fair Valuations at Inception and on 31 December 20X4

The fair valuations were calculated in the previous subsection. The fair value of the participating forward was the sum of the fair values of the embedded forward and option contracts.

| 1-Oct-20X4 | 31-Dec-20X4 | |

| Participating forward fair value | -0- | 1,060,000 |

| Change in participating forward fair value | — | 1,060,000 |

| Hypothetical derivative fair value | -0- | 1,185,000 (*) |

| Change in hypothetical derivative fair value | — | 1,185,000 |

(*) 859,000 × 69 mn/50 mn, where EUR 859,000 was the fair value of “hedged item 1” on 31-Dec-20X4 (which had a USD 50 mn notional) from Section 5.8.3 (Fair Valuations on 31 December 20X4).

The calculation of the effective and ineffective parts of the period change in fair value of the participating forward was performed as follows:

| 31-Dec-20X4 | |

| Cumulative change in fair value of hedging instrument | 1,060,000 |

| Cumulative change in fair value of hypothetical derivative | 1,185,000 |

| Lower amount | 1,060,000 |

| Previous cumulative effective amount | -0- |

| Available amount | 1,060,000 |

| Period change in fair value of hedging instrument | 1,060,000 |

| Effective part | 1,060,000 |

| Ineffective part | -0- |

Re-estimation of the Hedge Ratio on 31 December 20X4

The hedge ratio was re-estimated on 31 December 20X4 using the implied delta of the participating forward. Remember that the quantity of the hedged item was estimated using the following expression:

The embedded option's delta was 47% (see Figure 5.18), higher than at inception because the increase in the spot rate increased the option's probability of exercise. The estimate of the hedged item quantity was USD 74 million, calculated as follows:

Figure 5.18 Option delta on 31 December 20X4.

The terms of the hypothetical derivative were adjusted, as shown below:

| Hypothetical derivative – terms | |

| Instrument | FX forward |

| Start date | 1 October 20X4 |

| Counterparties | ABC and credit risk-free counterparty |

| Maturity | 30 June 20X5 |

| ABC sells | USD 74 million |

| ABC buys | EUR 59,105,000 |

| Forward rate | 1.2520 |

| Initial fair value | Zero |

Fair Valuations on 31 March 20X5

| 31-Dec-20X4 | 31-Mar-20X5 | |

| Participating forward fair value | 1,060,000 | 1,731,000 |

| Change in participating forward fair value (period) | 1,060,000 | 671,000 |

| Hypothetical derivative fair value | Not needed | 2,159,000 (*) |

| Change in hypoth. derivative fair value (cumulative since inception) | — | 2,159,000 |

(*) 1,459,000 × 74 mn /50 mn, where EUR 1,459,000 was the fair value of “hedged item 1” on 31-Mar-20X5 (which had a USD 50 mn notional) from Section 5.8.3 (Fair Valuations on 31 March 20X5).

The calculation of the effective and ineffective parts of the period change in fair value of the participating forward was performed as follows:

| 31-Mar-20X5 | |

| Cumulative change in fair value of hedging instrument | 1,731,000 |

| Cumulative change in fair value of hypothetical derivative | 2,159,000 |

| Lower amount | 1,731,000 |

| Previous cumulative effective amount | 1,060,000 |

| Available amount | 671,000 |

| Period change in fair value of hedging instrument | 671,000 |

| Effective part | 671,000 |

| Ineffective part | -0- |

Re-estimation of the Hedge Ratio on 30 March 20X5

The hedge ratio was re-estimated on 30 March 20X5 using the implied delta of the participating forward. Remember that the quantity of the hedged item was estimated using the following expression:

The embedded option's delta was 76% (see Figure 5.19), higher than at inception because the increase in the spot rate increased the option's probability of exercise. The estimate of the hedged item quantity was USD 88 million, calculated as follows:

Figure 5.19 Option delta on 31 March 20X5.

The terms of the hypothetical derivative were adjusted, as shown below:

| Hypothetical derivative – terms | |

| Instrument | FX forward |

| Start date | 1 October 20X4 |

| Counterparties | ABC and credit risk-free counterparty |

| Maturity | 30 June 20X5 |

| ABC sells | USD 88 million |

| ABC buys | EUR 70,288,000 |

| Forward rate | 1.2520 |

| Initial fair value | Zero |

Fair Valuations on 30 June 20X5

| 31-Mar-20X5 | 30-Jun-20X5 | |

| Participating forward fair value | 1,731,000 | 2,612,000 |

| Change in participating forward fair value (period) | — | 881,000 |

| Hypothetical derivative fair value | Not needed | 3,620,000 (*) |

| Change in hypoth. derivative fair value (cumulative since inception) | — | 3,620,000 |