Chapter 13

Hedge Accounting: A Double-Edged Sword

Hedge accounting is optional: it is a choice made by the management of an entity. Hedge accounting is a special accounting treatment available to ensure that the timing of profit or loss recognition on the hedging instrument matches that of the hedged item. When hedging, corporations face the decision between entering into hedge accounting compliant hedges and pure economic hedges (see Figure 13.1). At first glance, it seems a straightforward decision as the reduction in profit or loss volatility stemming from applying hedge accounting provides a powerful argument for adopting hedge accounting compliant hedges. However, in reality the decision whether or not to implement hedge accounting compliant hedges can be a difficult one: applying hedge accounting may be operationally complex and accounting compliant hedges are relatively limited (forwards/swaps and standard options).

Figure 13.1 Economic hedges versus hedge accounting compliant hedges.

The decision whether or not to adopt hedge accounting compliant hedges requires an in-depth analysis at both the entity level and the consolidated level as it may affect earnings, earnings per share, cash flows, gearing, interest cover, dividend cover, covenants, margins, bonuses and staff payment schemes. In my view it does not make sense to discard an attractive hedging strategy just because of the volatility it may add to profit or loss. Shareholders may punish executives for short-term volatility, but will certainly penalise underperforming companies. I believe that a well-designed disclosure to investors and analysts in which the merits and the drawbacks of a weak hedge accounting compliant strategy should be sufficient.

13.1 POSITIVE INFLUENCE ON THE PROFIT OR LOSS STATEMENT

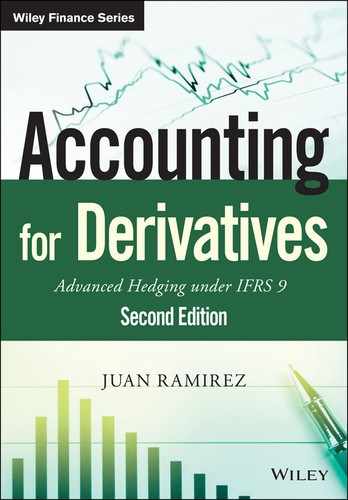

The application, or not, of hedge accounting treatment may have important effects on the profit or loss statement (see Figure 13.2), especially when hedging highly expected sales or purchases. Usually these hedges are implemented to mitigate commodity and/or FX risk.

Figure 13.2 Influence of hedges on profit or loss.

Suppose that an entity is considering hedging a highly expected foreign currency denominated sale of finished goods with a derivative. The expected sale will not be recorded in profit or loss until the sale finally takes place. The sale will be recorded in the EBITDA section of the profit or loss statement.

If the entity applies hedge accounting, the hedge will be treated as a cash flow hedge. The effective part of the change in fair value of the derivative will be recorded in OCI. When the hedged item (i.e., the highly expected sale) affects profit or loss, the accumulated amount in equity (i.e., in OCI) will be reclassified from OCI to profit or loss, on the same EBITDA line as the hedged item entry. This is relevant as EBITDA is a key indicator for financial analysts and investors. Thus, the application of hedge accounting in this example has two benefits: firstly, it ensures that the recognitions in profit or loss of the hedged item and the hedging instrument take place simultaneously; and secondly, that the recognitions are made on the same profit or loss line (e.g., sales).

If the entity does not apply hedge accounting, the change in fair value of the derivative for the period will be recognised in the “other financial gains and losses” item of profit or loss since the derivative's inception. Therefore, there will be a recognition mismatch between the hedged item and the hedging instrument in terms of not only timing but also profit or loss lines.

Thus, the use of hedge accounting may reduce not only profit or loss volatility, but also EBITDA volatility. The decision to use hedge accounting can be especially relevant to companies for which the price of raw materials is a very important component of their finished products sale price.

13.2 SUBSTANTIAL OPERATIONAL RESOURCES

Implementing hedge accounting is a big challenge as the requirements are far reaching. The administrative load needed to prepare disclosure and presentation requirements, to produce hedge documentation and to assess effectiveness can be substantial. A good deal of training is also needed for accounting and treasury personnel to achieve a sufficiently high level of competence. Additionally, strong information systems capabilities are needed to adequately process information flows and reporting. Also modelling tools are frequently needed to be able to correctly evaluate financial instruments and hedged items. Finally, supervision and appropriate policies and procedures are required to determine whether all hedge accounting requirements are properly met. Lack of appropriate controls can have a real and visible impact on the reported results of an organisation.

13.3 LIMITED ACCESS TO HEDGING ALTERNATIVES

Widespread adoption of hedge accounting compliant hedges may lead entities to undertake hedging instruments that are sub-optimal from an economic perspective. Usually hedging instruments that provide more potential room for economic benefit tend to show a lower degree of applicability of hedge accounting.

A good many hedging strategies are neither fully hedge accounting compliant nor completely non-compliant. As discussed in some of the case studies in Chapter 5, there are hedging instruments that can be split into a part that meets the requirements of hedge accounting and a part that does not meet these requirements. Figure 13.3 depicts the usual negative relationship between the potential economic upside (measured as the participation in potentially favourable market movements) and the degree of hedge accounting compliance in FX hedges of highly expected sales or purchases.

Figure 13.3 Economic upside versus degree of hedge accounting compliance.

13.4 RISK OF REASSESSMENT OF HIGHLY PROBABLE TRANSACTIONS

One potential problem with using hedge accounting occurs when the originally highly probable cash flow being hedged is suddenly no longer expected to take place. In a cash flow hedge of a highly expected cash flow, the change in fair value of the hedging instrument is recorded in equity until the underlying cash flow affects profit or loss. If the underlying cash flow is no longer expected to take place, the hedging instrument gain or loss deferred in equity has to be transferred to profit or loss immediately. This transfer can have a devastating effect on profit or loss if the deferred amount in equity represented a very large loss.

13.5 LOW COMPATIBILITY WITH PORTFOLIO HEDGING

Most large multinationals centralise their financial risk management in a treasury centre, which is responsible for risk and liquidity management, and funding for the whole group. Frequently, the treasury centre applies a portfolio approach to hedging. This means that it does not consider individual exposures, but combines different exposures together, and only enters into hedges with third parties when the residual risk in the portfolio may compromise the delivery of corporate objectives.

The overall risk is usually measured using the value at risk (VaR). The VaR approach attempts to measure the probability that the portfolio does not lose more than a specific amount within a specific time horizon. The hedging strategy then involves limiting the portfolio exposures so that the financial and other business targets are not endangered by financial risks. Figure 13.4 depicts the hedging process on a portfolio basis.

Figure 13.4 Portfolio hedging – decision process.

Unless macrohedging (i.e., portfolio hedge accounting) is applied, when a derivative is taken out to hedge a net group position the application of hedge accounting (microhedging) often requires assigning the hedging instrument to an individual transaction between an entity of the group and an outside party, an assignment that may sometimes not be feasible as shown in Section 5.17. As a consequence, an entity may end up not applying for hedge accounting for many of the hedging transactions with outside parties.

At the time of writing, the IFRS 9 macrohedging project was at a preliminary stage. If the macrohedging project ends up providing rigid application of portfolio hedging, there is likely to be a gap between risk management and hedge accounting, which may deter companies from applying hedge accounting for their dynamic or portfolio hedging strategies.

13.6 FINAL REMARKS

When a company is contemplating hedge accounting for a specific hedge, careful analysis is required of the costs and benefits of its application. This can be a complex decision because the main benefit – the added value that comes from reduced earnings volatility – is difficult to measure in practice.

Although most companies try to maximise the use of hedge accounting, it is important not to exclude attractive hedging strategies just because of an unfavourable accounting treatment. Let us not forget that risk management can be a competitive weapon: companies can gain advantage over competitors who fail to optimise risk management.

The following table summarises the pros and cons of applying hedge accounting to a specific hedge:

| Strengths | Weaknesses |

| Reduced volatility in earnings | Limited availability of hedging alternatives |

| Reduced volatility of EBITDA | Low compatibility with portfolio hedging techniques(*) |

| Improved cash flow forecasting | Systems and human resources to meet hedge documentation, effectiveness assessment and disclosure requirements |

| Reduced risk of breaching covenants | Potential volatility in reserves (if cash flow or net investment hedge) |

| Reduced risk of credit rating downgrades | Risk of accounting restatements |

(*) The IFRS 9 macrohedging project was not finalised at the time of writing