6.11 CASE STUDY: NET INVESTMENT HEDGE WITH A FLOATING-TO-FLOATING CROSS-CURRENCY SWAP

The aim of this case study is to illustrate the hedge of a net investment in a foreign operation with a floating-to-floating CCS. ABC, a group with presentation currency the EUR, decided to enter into this type of CCS because the USD interest rate curve was markedly steep. When curves are very steep, short-term rates are notably lower than long-term rates, and entities paying a floating rate experience substantial savings relative to paying the fixed rate during the initial interest periods.

Suppose that ABC's objective was to hedge USD 500 million of its investment in its US subsidiary SubCo over the next 3 years. The terms of the CCS were as follows:

| Cross-currency swap terms | |

| Start date | 1 January 20X0 |

| Counterparties | ABC and XYZ Bank |

| Maturity | 31 December 20X2 |

| EUR notional | EUR 400 million |

| USD notional | USD 500 million |

| Implied FX rate | 1.2500 |

| ABC pays | USD 12-month Libor + 10 bps annually, actual/360 basis, on the USD nominal |

| ABC receives | 12-month Euribor annually, actual/360 basis, on the EUR nominal |

| Final exchange | On maturity date, there would be a EUR cash settlement amount based on the EUR–USD fixing prevailing on such date (i.e., there would be no notionals exchange) Settlement amount = 400 mn – 500 mn/EUR–USD fixing If the settlement amount were positive, ABC would receive the settlement amount If the settlement amount were negative, ABC would pay the absolute value of the settlement amount |

It is important to note that the CCS did not have the usual exchange of principals at maturity. Instead the CCS had a “cash settlement” provision. The reason for this was that since ABC was not planning to sell the US subsidiary on the CCS maturity date, ABC was not interested on that date in selling USD 500 million and buying EUR 400 million. Instead ABC would receive (or pay) compensation equivalent to the depreciation (or appreciation) of its investment in the US subsidiary.

ABC designated the CCS as the hedging instrument in a net investment hedge.

6.11.1 Hedging Relationship Documentation

At its inception, ABC documented the hedging relationship as follows:

| Hedging relationship documentation | |

| Risk management objective and strategy for undertaking the hedge | The objective of the hedge is to protect, in the group's consolidated financial statements, the value of the USD 500 million investment in the US subsidiary SubCo against unfavourable movements in the EUR–USD exchange rate. This hedging objective is consistent with ABC's overall FX risk management strategy of reducing the variability of its shareholders' equity as stated in the group's hedging policy using FX forwards, FX options and foreign currency debt. The risk being hedged is the risk of changes in the EUR–USD exchange rate that will result in changes in the value of the group's net investment in SubCo when translated into EUR. The risk is hedged from 1 January 20X0 to 31 December 20X2 |

| Type of hedge | Net investment hedge |

| Hedged item | The first USD 500 million of the net assets of SubCo |

| Hedging instrument | The pay USD floating and receive EUR floating cross-currency swap with reference number 016795. The notionals are USD 500 million and EUR 400 million, the entity pays annually 12-month Euribor on the EUR leg and receives annually USD 12-month Libor on the USD leg, and the term is 3 years. The counterparty to the CCS is XYZ Bank and the credit risk associated with this counterparty is considered to be very low |

| Hedge effectiveness assessment | See below |

6.11.2 Hedge Effectiveness Assessment

Hedge effectiveness will be assessed by comparing the change in fair value of the hedging instrument to the foreign currency gains and losses on the net investment that are attributable to the hedged risk (i.e., changes in spot exchange rates).

Hedge effectiveness will be assessed prospectively at hedging relationship inception and on an ongoing basis at least upon each reporting date and upon occurrence of a significant change in the circumstances affecting the hedge effectiveness requirements.

The hedging relationship will qualify for hedge accounting only if all the following criteria are met:

- The hedging relationship consists only of eligible hedge items and hedging instruments. The hedge item is eligible as it is a foreign operation that exposes the group to currency retranslation risk and it is reliably measurable. The hedging instrument is eligible as it is a derivative instrument other than a written option.

- At hedge inception there is a formal designation and documentation of the hedging relationship and the entity's risk management objective and strategy for undertaking the hedge.

- The hedging relationship is considered effective.

The hedging relationship will be considered effective if the following three requirements are met:

- There is an economic relationship between the hedged item and the hedging instrument.

- The effect of credit risk does not dominate the fair value changes in the hedging relationship.

- The weightings of the hedged item and the hedging instrument (i.e., hedge ratio) are designated based on the quantities of hedged item and hedging instrument that the entity actually uses to meet the risk management objective, unless doing so would deliberately create ineffectiveness.

Whether there is an economic relationship between the hedged item and the hedging instrument will be assessed on a qualitative basis by comparing the critical terms of the hedging instrument and the hedged item. The critical terms considered will be the notional amount, the term and the underlying.

The effective and ineffective amounts of the change in fair value of the hedging instrument will be computed by comparing the cumulative change in fair value of the hedging instrument with that of the hedged item. The effective amount will be recognised in the “translation differences” reserve in OCI. Any part of the cumulative change in fair value of the hedging instrument that does not offset a corresponding cumulative change in the fair value of the hedged item will be treated as ineffectiveness and recorded in profit or loss.

6.11.3 Hedge Effectiveness Assessment Performed at Hedge Inception

An effectiveness assessment was performed at inception and at each reporting date. The assessment also included the relationship hedge ratio and an identification of the sources of potential ineffectiveness.

The hedge qualified for hedge accounting as it met the three effectiveness requirements:

- The critical terms (such as the nominal amount, maturity and underlying) of the hedging instrument and the hedged item matched. Although the CCS had interest payments/receipts not present in the net investment, the change in fair value of the CCS was expected to be largely offset by the change in the translation amount of the net investment due to (i) the floating profile of both legs of the CCS and (ii) the concurrence of the dates on which the CCS's intermediate payments/receipts were made and the reporting dates. As a result it was concluded that the hedging instrument and the hedged item had values that would generally move in opposite directions, and hence that an economic relationship existed between the hedged item and the hedging instrument.

- Because the credit rating of counterparty to the hedging instrument was relatively strong (rated A+ by Standard & Poor's) the effect of credit risk did not dominate the value changes resulting from that economic relationship.

- The hedge ratio designated (1:1) was the one actually used for risk management and it did not attempt to avoid recognising ineffectiveness. Therefore, it was determined that a hedge ratio of 1:1 was appropriate.

There were three main sources of potential ineffectiveness: firstly, a significant credit deterioration of the counterparty to the hedging instrument (XYZ Bank); secondly, a reduction of the net assets of the hedged foreign operation below the hedging instrument notional; and finally, a substantial increase in the CCS basis.

6.11.4 Other Relevant Information

The net investment translation into EUR was calculated using the EUR–USD spot rate at each relevant date as follows:

| Date | Spot EUR–USD | Net investment (USD) | Net investment (EUR) (*) | Period retranslation difference (EUR) |

| 1-Jan-X0 | 1.2500 | 500,000,000 | 400,000,000 | — |

| 31-Dec-X0 | 1.2700 | 500,000,000 | 393,701,000 | <6,299,000> |

| 31-Dec-X1 | 1.3100 | 500,000,000 | 381,679,000 | <12,022,000> |

| 31-Dec-X2 | 1.2900 | 500,000,000 | 387,597,000 | 5,918,000 |

(*) Net investment in EUR = 500 million/Spot rate

The fair values of the CCS, including credit valuation adjustments and excluding accrued interest, at each reporting date were as follows:

| Date | CCS fair value (EUR) | Period fair value change |

| 31-Dec-X0 | 6,335,000 | 6,335,000 |

| 31-Dec-X1 | 18,502,000 | 12,167,000 |

| 31-Dec-X2 | 12,403,000 | <6,099,000> |

The effective and ineffective parts of the change in fair value of the CCS were the following (see Section 5.5.6 for an explanation of the calculations):

| 31-Dec-X0 | 31-Dec-X1 | 31-Dec-X2 | |

| Cumulative change in fair value of hedging instrument | 6,335,000 | 18,502,000 | 12,403,000 |

| Cumulative change in translation value of hedged item (opposite sign) | 6,299,000 | 18,321,000 | 12,403,000 |

| Lower amount | 6,299,000 | 18,321,000 | 12,403,000 |

| Previous cumulative effective amount | Nil | 6,299,000 | 18,321,000 |

| Available amount | 6,299,000 | 12,022,000 | <5,918,000> |

| Period change in fair value of hedging instrument | 6,335,000 | 12,167,000 | <6,099,000> |

| Effective part | 6,299,000 | 12,022,000 | <5,918,00> |

| Ineffective part | 36,000 | 145,000 | <181,000> |

The interest flows/expenses related to the USD leg of the CCS were as follows:

| Date | Spot EUR–USD | Annual average EUR–USD | USD Libor rate | Interest payments (USD) | Interest expense (EUR) | Interest payment (EUR) |

| 31-Dec-X0 | 1.2700 | 1.2650 | 5.20% | 26,868,000 (1) | 21,240,000 (1) | 21,156,000 (1) |

| 31-Dec-X1 | 1.3100 | 1.2840 | 5.50% | 28,389,000 | 22,110,000 | 21,671,000 |

| 31-Dec-X2 | 1.2900 | 1.3020 | 5.70% | 29,403,000 | 22,583,000 | 22,793,000 |

Notes:

(1) Interest payment (USD) = USD 500 million × (5.20%+0.10%) × 365/360

(2) Interest expense (EUR) = Interest payment (USD)/Annual average FX rate = 26,868,000/1.2650

(3) Interest payment (EUR) = Interest payment (USD)/Spot FX rate = 26,868,000/1.2700

The interest flows/expenses related to the EUR leg of the CCS were as follows:

| Date | EUR Euribor Rate | Interest received/ income (EUR) |

| 31-Dec-X0 | 4.00% | 16,222,000 (*) |

| 31-Dec-X1 | 4.20% | 17,033,000 |

| 31-Dec-X2 | 4.40% | 17,844,000 |

(*) Interest received = EUR 400 million × 4.00% × 365/360

6.11.5 Accounting Entries

Assuming that ABC closed its books annually at year's end, the accounting entries related to the hedge were as follows.

- To record the CCS trade on 1 January 20X0

No entries in the financial statements were required as the fair value of the CCS was zero.

- To record the closing of the accounting period on 31 December 20X0

The net investment lost EUR 6,299,000 in value over the period when translated into EUR. In practice all the net assets of SubCo would have been translated. In our case, the retranslation of just USD 500 million of net assets are assumed and summarised in a “net investment in subsidiary” figurative account for illustrative purposes.

- The CCS fair value change, excluding accrued interest, was a gain of EUR 6,335,000. The effective part (EUR 6,299,000) was recognised in the translation differences account. The ineffective part (EUR 36,000) was recognised in profit or loss.

- Under the USD leg of the CCS, ABC paid the equivalent of EUR 21,156,000 and recognised a EUR 21,240,000 interest expense. The EUR 84,000 difference between these amounts was recognised in profit or loss. Under the EUR leg of the CCS, ABC received EUR 16,222,000, recognised as interest income.

- To record the closing of the accounting period on 31 December 20X1

- To record the closing of the accounting period on 31 December 20X2

- Additionally on 31 December 20X2, a settlement amount was received under the CCS related to the notionals. The EUR–USD spot rate on that date was 1.2900. ABC received EUR 12,403,000 (= EUR 400 mn – USD 500 mn/1.2900):

6.11.6 Final Remarks

In our case the hedge performed very well, as the decline in value of the net investment due to the depreciation of the USD relative to the EUR was completely offset by the change in fair value of the CCS. Several comments are worth noting:

- The pay floating/receive floating CCS is an effective way to implement long-term hedges of net investments in foreign operations.

- ABC's profit or loss statement was temporarily exposed to the ineffective part of the hedge (i.e., to the excess of the CCS fair value change relative to the net investment retranslation gain/loss). Ineffectiveness was due to changes in the CCS basis and to credit valuation adjustments. In our case, ABC's profit or loss was not exposed to changes in the fair value of the CCS due to movements in the USD and EUR interest rate curves because both legs were linked to floating interest rates and the absence of accrued interest. In reality, slight ineffectiveness may arise when the ends of the CCS interest periods do not coincide with the reporting dates.

- In our case, the sum of all the ineffective parts during the life of the CCS was zero. In other words, the translation differences account showed no deficit because the changes in the net investment translation were perfectly offset by the fair value changes in the CCS.

- IFRS 9 allows an entity to choose whether to exclude the basis component of a CCS from a hedging relationship and to recognise changes in this component in equity to the extent that they relate to hedged item.

- At CCS maturity, ABC received EUR 12,403,000 in cash. In this case, the outcome was very favourable to ABC, but it could have been the other way around. In other words, a hedge of a large investment in a foreign operation through a CCS may have strong implications in an entity's cash resources.

- The amount in the translation differences account will be reclassified from equity to profit or loss on disposal or liquidation of SubCo.

6.12 CASE STUDY: NET INVESTMENT HEDGE WITH A FIXED-TO-FIXED CROSS-CURRENCY SWAP

The aim of this case study is to illustrate the hedge of a net investment in a foreign operation with a fixed-to-fixed CCS. Assume that ABC's objective was to hedge USD 500 million of its investment in its US subsidiary SubCo over the next 3 years. The group's presentation currency was the EUR. SubCo's functional currency was the USD. The terms of the CCS were as follows:

| Cross-currency swap terms | |

| Start date | 1 January 20X0 |

| Counterparties | ABC and XYZ Bank |

| Maturity | 31 December 20X2 |

| EUR notional | EUR 400 million |

| USD notional | USD 500 million |

| Implied FX rate | 1.2500 |

| ABC pays | 6.10% annually, 30/360 basis, on the USD nominal |

| ABC receives | 5% annually, 30/360 basis, on the EUR nominal |

| Final exchange | On maturity date, a EUR cash settlement amount (the “settlement amount”) will be calculated based on the EUR–USD fixing (the “fixing”) prevailing on such date (i.e., there would be no notional exchange). Settlement amount = EUR 400 mn – 500 mn/Fixing If settlement amount is positive, ABC receives the settlement amount. If the settlement amount is negative, ABC pays the absolute value of the settlement amount. |

As explained in the previous case, the CCS had a “cash settlement” provision to avoid exchanging principals at maturity. ABC designated the CCS as the hedging instrument in a net investment hedge.

An important element of the hedge is the definition of the amount of net assets being hedged. There are two alternative views within the accounting community on defining this amount, when hedged with fixed-to-fixed CCSs:

- the foreign currency notional of the CCS (in our case, USD 500 million);

- the sum of the undiscounted cash flows on the foreign currency leg of the CCS (in our case, USD 591.5 million (= 500 mn + 3 × 6.10% × 500 mn)).

In this case, I used the former alternative.

6.12.1 Hedging Relationship Documentation

ABC designated the CCS as the hedging instrument in a net investment hedge. At its inception, ABC documented the hedging relationship as follows:

| Hedging relationship documentation | |

| Risk management objective and strategy for undertaking the hedge | The objective of the hedge is to protect, in the group's consolidated financial statements, the value of the USD 500 million investment in the US subsidiary SubCo against unfavourable movements in the EUR–USD exchange rate. This hedging objective is consistent with ABC's overall FX risk management strategy of reducing the variability of its shareholders' equity as stated in the group's hedging policy using FX forwards, FX options and foreign currency debt. The risk being hedged is the risk of changes in the EUR–USD exchange rate that will result in changes in the value of the group's net investment in SubCo when translated into EUR. The risk is hedged from 1 January 20X0 to 31 December 20X2 |

| Type of hedge | Net investment hedge |

| Hedged item | The first USD 500 million of the net assets of SubCo |

| Hedging instrument | The pay USD fixed and receive EUR fixed cross-currency swap with reference number 016796. The notionals are USD 500 million and EUR 400 million, the interest payments are USD 6.10% and EUR 5.00%, and the term is 3 years. The counterparty to the CCS is XYZ Bank and the credit risk associated with this counterparty is considered to be very low |

| Hedge effectiveness assessment | See below |

6.12.2 Hedge Effectiveness Assessment

Hedge effectiveness will be assessed by comparing changes in the fair value of the hedging instrument to changes in the fair value of a hypothetical derivative. In this hedging relationship, the terms of the hypothetical derivative mirror those of the hedging instrument except, due to the absence of CVA risk, the EUR leg fixed rate which is 4.99%.

Hedge effectiveness will be assessed prospectively at hedging relationship inception and on an ongoing basis at least upon each reporting date and upon occurrence of a significant change in the circumstances affecting the hedge effectiveness requirements.

The hedging relationship will qualify for hedge accounting only if all the following criteria are met:

- The hedging relationship consists only of eligible hedge items and hedging instruments. The hedge item is eligible as it is a foreign operation that exposes the group to currency retranslation risk and it is reliably measurable. The hedging instrument is eligible as it is a derivative instrument other than a written option.

- At hedge inception there is a formal designation and documentation of the hedging relationship and the entity's risk management objective and strategy for undertaking the hedge.

- The hedging relationship is considered effective.

The hedging relationship will be considered effective if the following three requirements are met:

- There is an economic relationship between the hedged item and the hedging instrument.

- The effect of credit risk does not dominate the fair value changes in the hedging relationship.

- The weightings of the hedged item and the hedging instrument (i.e., hedge ratio) are designated based on the quantities of hedged item and hedging instrument that the entity actually uses to meet the risk management objective, unless doing so would deliberately create ineffectiveness.

Whether there is an economic relationship between the hedged item and the hedging instrument will be assessed on a qualitative basis by comparing the critical terms of the hedging instrument and the hypothetical derivative. The critical terms considered will be the notional amounts, the interest periods and the fixed rates. The assessment will be complemented by a quantitative assessment using the scenario analysis method for one scenario in which a EUR–USD exchange rate will be simulated by shifting the spot price prevailing on the assessment date by +10%, and the change in fair value of the hedging instrument with that of the hypothetical derivative compared.

The effective and ineffective amounts of the change in fair value of the hedging instrument will be computed by comparing the cumulative change in fair value of the hedging instrument with that of the hypothetical derivative. The effective amount will be recognised in the “translation differences” reserve in OCI. Any part of the cumulative change in fair value of the hedging instrument that does not offset a corresponding cumulative change in the fair value of the hypothetical derivative will be treated as ineffectiveness and recorded in profit or loss.

6.12.3 Hedge Effectiveness Assessment Performed at Hedge Inception

An effectiveness assessment was performed at inception and at each reporting date. The assessment also included the relationship hedge ratio and an identification of the sources of potential ineffectiveness.

The hedge qualified for hedge accounting as it met the three effectiveness requirements:

- Because the critical terms (such as notional amounts, interest periods and fixed rates) of the hedging instrument and the hypothetical derivative matched (or almost matched) it was concluded that the hedging instrument and the hedged item had values that would generally move in opposite directions, and hence that an economic relationship existed between the hedged item and the hedging instrument. This conclusion was supported by the qualitative analysis documented below.

- Because the credit rating of counterparty to the hedging instrument was relatively strong (rated A+ by Standard & Poor's) the effect of credit risk did not dominate the value changes that result from that economic relationship.

- The hedge ratio designated (1:1) was the one actually used for risk management and it did not attempt to avoid recognising ineffectiveness. Therefore, it was determined that a hedge ratio of 1:1 was appropriate.

A test EUR–USD spot rate (1.3750) was simulated by shifting the EUR–USD spot rate prevailing on the assessment date (1.2500) by +10%. As shown in the table below, the change in fair value of the hedged item was expected to be largely offset by the change in fair value of the hedging instrument, corroborating that both elements had values that would generally move in opposite directions.

The fair value of the hypothetical derivative at inception of the hedging relationship, prior to the shift in the EUR–USD spot rate, was calculated as follows:

| Hypothetical derivative fair valuation on 1-Jan-20X0 | ||||

| 31-Dec-20X0 | 31-Dec-20X1 | 31-Dec-20X2 | Total | |

| USD leg: | ||||

| USD cash flow | <30,500,000> | <30,500,000> | <530,500,000> | |

| USD discount factor | 0.9477 | 0.8930 | 0.8367 | |

| PV USD cash flow | <28,905,000> | <27,237,000> | <443,859,000> | |

| EUR–USD spot rate | 1.2500 | 1.2500 | 1.2500 | |

| EUR translated amount | <23,124,000> | <21,790,000> | <355,086,000> | <400,000,000> |

| EUR leg: | ||||

| EUR cash flow | 19,960,000 | 19,960,000 | 419,960,000 | |

| EUR discount factor | 0.9578 | 0.9121 | 0.8636 | |

| PV EUR cash flow | 19,118,000 | 18,206,000 | 362,676,000 | 400,000,000 |

| Total fair value | Nil | |||

The fair value of the hypothetical derivative at inception of the hedging relationship, after the shift in the EUR–USD spot rate, was calculated as follows:

| Hypothetical derivative fair valuation on 1-Jan-20X0 | ||||

| 31-Dec-20X0 | 31-Dec-20X1 | 31-Dec-20X2 | Total | |

| USD leg: | ||||

| USD cash flow | <30,500,000> | <30,500,000> | <530,500,000> | |

| USD discount factor | 0.9477 | 0.8930 | 0.8367 | |

| PV USD cash flow | <28,905,000> | <27,237,000> | <443,859,000> | |

| EUR–USD spot rate | 1.3750 | 1.3750 | 1.3750 | |

| EUR translated amount | <21,022,000> | <19,809,000> | <322,807,000> | <363,638,000> |

| EUR leg: | ||||

| EUR cash flow | 19,960,000 | 19,960,000 | 419,960,000 | |

| EUR discount factor | 0.9578 | 0.9121 | 0.8636 | |

| PV EUR cash flow | 19,118,000 | 18,206,000 | 362,676,000 | 400,000,000 |

| Total fair value | 36,362,000 | |||

The change in fair value of the hedging instrument was calculated in a similar way, resulting in a EUR 36,347,000 gain. The difference between the fair value changes of the two instruments was mainly due to changes in CVA in the hedging instrument.

| Scenario analysis assessment | ||

| Hedging instrument | Hypothetical derivative | |

| Initial fair value | Nil | Nil |

| Final fair value | 36,347,000 | 36,362,000 |

| Fair value change | 36,347,000 | 36,362,000 |

| Degree of offset | 100.0% | |

The hedge ratio is established at 1:1.

There were three main sources of potential ineffectiveness: firstly, a significant credit deterioration of the counterparty to the hedging instrument (XYZ Bank); secondly, a reduction of the net assets of the hedged foreign operation below the hedging instrument notional; and finally, a substantial increase in the basis element of the CCS.

6.12.4 Other Relevant Information

The net investment translation into EUR was calculated using the EUR–USD spot rate at each relevant date as follows:

| Date | Spot EUR–USD | Net investment (USD) | Net investment (EUR) (*) | Period retranslation difference (EUR) |

| 1-Jan-20X0 | 1.2500 | 500,000,000 | 400,000,000 | — |

| 31-Dec-20X0 | 1.2700 | 500,000,000 | 393,701,000 | <6,299,000> |

| 31-Dec-20X1 | 1.3100 | 500,000,000 | 381,679,000 | <12,022,000> |

| 31-Dec-20X2 | 1.2900 | 500,000,000 | 387,597,000 | 5,918,000 |

(*) Net investment in EUR = 500 million/Spot rate

The fair values of the CCS and the hypothetical derivative, excluding accrued interest, at each reporting date are shown in the following table. Differences between both fair values arose primarily due to the CVA performed on the CCS.

| Date | CCS Fair Value ( EUR) | CCS Fair Value Change ( EUR) | Hypothetical Deriv. Fair Value ( EUR) | Hypothetical Der. Fair Value Change (EUR) | Effective Part of CCS Fair Value Change |

| 31-Dec-20X0 | 7,559,000 | 7,559,000 | 7,594,000 | 7,594,000 | 7,559,000 |

| 31-Dec-20X1 | 21,985,000 | 14,426,000 | 21,996,000 | 14,402,000 | 14,426,000 |

| 31-Dec-20X2 | 12,403,000 | <9,582,000 > | 12,403,000 | <9,593,000> | <9,582,000 > |

The ineffective part of the change in fair value of the CCS was the excess of its cumulative change in fair value over that of the hypothetical derivative. In our case, no ineffectiveness was recognised. The effective and ineffective parts of the change in fair value of the CCS were the following (see Section 5.5.6 for an explanation of the calculations):

| 31-Dec-20X0 | 31-Dec-20X1 | 31-Dec-20X2 | |

| Cumulative change in fair value of hedging instrument | 7,559,000 | 21,985,000 | 12,403,000 |

| Cumulative change in fair value of hypothetical derivative | 7,594,000 | 21,996,000 | 12,403,000 |

| Lower amount | 7,559,000 | 21,985,000 | 12,403,000 |

| Previous cumulative effective amount | Nil | 7,559,000 | 21,985,000 |

| Available amount | 7,559,000 | 14,426,000 | <9,582,000> |

| Period change in fair value of hedging instrument | 7,559,000 | 14,426,000 | <9,582,000> |

| Effective part | 7,559,000 | 14,426,000 | <9,582,000> |

| Ineffective part | Nil | Nil | Nil |

The interest flows/expenses related to the USD leg of the CCS were as follows:

| Date | Spot EUR–USD | Annual average EUR–USD | USD fixed rate | Interest payment (USD) | Interest expense (EUR) | Interest payment (EUR) |

| 31-Dec-20X0 | 1.2700 | 1.2650 | 6.10% | 30,500,000 (1) | 24,111,000 (1) | 24,016,000 (1) |

| 31-Dec-20X1 | 1.3100 | 1.2840 | 6.10% | 30,500,000 | 23,754,000 | 23,282,000 |

| 31-Dec-20X2 | 1.2900 | 1.3020 | 6.10% | 30,500,000 | 23,425,000 | 23,643,000 |

Notes:

(1) Interest payment (USD) = USD 500 million × 6.10%

(2) Interest expense (EUR) = Interest payment (USD)/Annual average FX rate = 30,500,000/1.2650

(3) Interest payment (EUR) = Interest payment (USD)/Spot FX rate = 30,500,000/1.2700

The interest flows/expenses related to the EUR leg of the CCS were as follows:

| Date | EUR fixed rate | Interest received/ income (EUR) |

| 31-Dec-20X0 | 5.00% | 20,000,000 (*) |

| 31-Dec-20X1 | 5.00% | 20,000,000 |

| 31-Dec-20X2 | 5.00% | 20,000,000 |

(*) Interest received/income = EUR 400 million × 5.00%

6.12.5 Accounting Entries

Assuming that ABC closed its books annually at year's end, the accounting entries related to the hedge were as follows.

- To record the CCS trade on 1 January 20X0

No entries in the financial statements were required as the fair value of the CCS was zero.

- To record the closing of the accounting period on 31 December 20X0

The net investment lost EUR 6,299,000 in value over the period when translated into EUR. In practice all the net assets of SubCo would have been translated. In our case, the retranslation of just USD 500 million of net assets is assumed and summarised in a “net investment in subsidiary” figurative account for illustrative purposes.

- The CCS fair value change, excluding accrued interest, was a gain of EUR 7,559,000. All this gain was effective and recognised in the translation differences account. There was no ineffective part, and therefore, no amount was recognised in profit or loss.

- Under the USD leg of the CCS, ABC paid the equivalent of EUR 24,016,000 and recognised a EUR 21,111,000 interest expense. The EUR 95,000 difference between these amounts was recognised in profit or loss. Under the EUR leg of the CCS, ABC received EUR 20,000,000, recognised as interest income.

- To record the closing of the accounting period on 31 December 20X1

- To record the closing of the accounting period on 31 December 20X2

- Additionally on 31 December 20X2, a settlement amount was received under the CCS representing a net amount related to the final exchange of notionals. The EUR–USD spot rate on this date was 1.2900. ABC received EUR 12,403,000 (= EUR 400 mn – USD 500 mn/1.2900):

6.13 CASE STUDY: HEDGING INTRAGROUP FOREIGN DIVIDENDS

Generally foreign subsidiaries distribute dividends to their shareholders. Because dividends are usually paid in the foreign subsidiary's functional currency, both the parent company and the group may be exposed to FX risk. In this section, I discuss the accounting impact of dividends at foreign subsidiary, parent and group levels, as well as the potential distortions that hedges may create. It is worth noting that hedging only dividends (i.e., without taking into account the earnings translation and net investment risk exposures) may end up creating undesirable effects in the consolidated financial statements.

6.13.1 Effects of Intercompany Foreign Dividends on Individual and Consolidated Statements

Suppose that ABC, a group whose presentation currency is the EUR, has a 100% owned US foreign subsidiary. The foreign subsidiary declared, and later paid, a dividend of USD 100 million to ABC. The exchange rates at the relevant dates were as follows:

| Date | Spot EUR–USD | USD dividend | Dividend EUR value |

| Previous reporting date: 31-Dec-20X0 | 1.2000 | ||

| Declaration date: 1-Jan-20X1 | 1.2300 | 100 mn | 81.3 mn |

| Reporting date: 31-Mar-20X1 | 1.2500 | 100 mn | 80.0 mn |

| Dividend payment date: 30-Jun-20X1 | 1.2850 | 100 mn | 77.8 mn |

In order to analyse the FX exposure caused by the dividend, let us review the accounting of intragroup dividends from the subsidiary, parent and group perspectives.

Impact on the Subsidiary's Financial Statements

On declaration date (1 January 20X1), the subsidiary recorded a USD 100 million declared dividend as follows:

On the first reporting date, 31 March 20X1, no accounting entries were required. On dividend payment date, 30 June 20X1, the subsidiary recorded the payment as follows:

As shown in the previous accounting entries, the subsidiary was not exposed to any FX risk because all the flows were denominated in its functional currency (USD).

Impact on the Parent's Stand-alone Financial Statements

The required accounting entries on the parent financial statements were as follows:

- Accounting entries on 1 January 20X1

Under the cost method, the parent recorded the foreign subsidiary's declared USD dividend as “dividend income” and as “dividend receivable”. The exchange rate used to convert the USD amount into EUR was the exchange rate prevailing on the dividend declaration date (1.2300). As a result, on 1 January 20X1 the parent entity recorded a EUR 81,300,000 (= USD 100 mn/1.2300) dividend.

- Accounting entries on 31 March 20X1

In the parent's stand-alone financial statements, the dividend receivable constituted a monetary item denominated in a foreign currency (USD), and therefore it was revalued at each balance sheet date. Any changes in the exchange rate from the last revaluation resulted in an FX gain or loss that was recognised in profit or loss. Since 1 January 20X1, the USD 100 million dividend receivable lost EUR 1.3 million (=80,000,000 – 81,300,000) in value.

- Accounting entries on 30 June 20X1

On this date the USD dividend was received by the parent entity. The parent first had to revalue the dividend receivable, recognising a EUR 2,100,000 loss (=77,800,000 – 80,000,000):

- The receipt of the USD 100 million from the subsidiary was recorded as follows:

It can be seen that the parent entity was exposed to FX risk in its stand-alone statements. This exposure was caused by the revaluation of the USD-denominated monetary item resulting from the subsidiary's declared USD dividend.

Impact on the Group's Consolidated Financial Statements

ABC carried out the consolidation process at each reporting date.

- Consolidation adjustments on 31 March 20X1

On this date, in the subsidiary's financial statements there was a USD dividend payable and in the parent's financial statements there was a USD dividend receivable. Upon consolidation, intragroup receivables and payables were eliminated and all its effects unwound.

- On this date also, ABC had to calculate the translation differences adjustment related to its net investment in the US subsidiary. I had only looked at the dividend portion of the net investment to isolate the dividend effect from the rest. As the dividend was still unpaid, the USD 100 million was still part of the net investment. The spot rate prevailing at the previous reporting date (31 December 20X0) was 1.2000. The spot rate prevailing at the current reporting date (31 March 20X1) was 1.2500. Accordingly, the change in the net investment was a EUR 3,333,000 (= 100 mn/1.25 – 100 mn/1.20) loss. The loss was recorded in the translation differences account of equity:

- Consolidation adjustments on 30 June 20X1

On this date and prior to the recognition of the dividend payment/receipt, the revaluation of the USD 100 million net investment showed a EUR 2,179,000 (= 100 mn/1.285 – 100 mn/1.25) loss that was recorded in the translation differences account of equity:

- Also on this date, the dividend was paid to the parent. As a result, the USD 100 million was now part of the parent's monetary assets and no longer part of the net investment in the subsidiary. Upon consolidation, the revaluation of the parent monetary assets performed at the stand-alone parent level also remained at the consolidated level. The net investment exposure decreased as well, and thus the translation differences adjustment was computed on a smaller net assets base.

Summary of Impacts on the Financial Statements

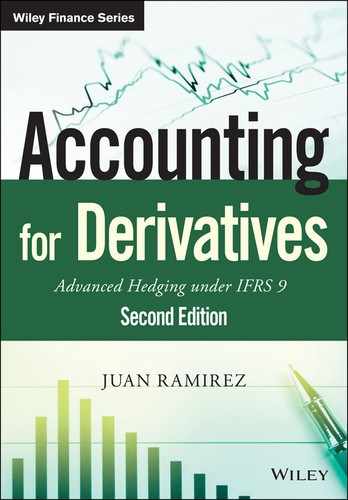

On dividend declaration date, 1 January 20X1, the accounting effects were the following (see Figure 6.17):

- In the subsidiary's financial statements, a dividend payable and a corresponding reduction in retained earnings were recognised.

- In the parent's financial statements, the declared dividend was valued at the then prevailing EUR–USD exchange rate and recognised as dividend income and dividend receivable. The recognition in profit or loss had a tax impact.

-

In the consolidated financial statements, there was still no effect as no consolidation

process took place.

Figure 6.17 Dividend declaration (1-Jan-20X1) – effect on stand-alone financial statements.

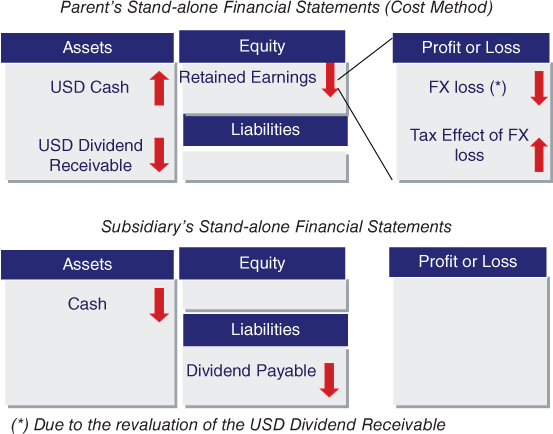

On the first reporting date, 31 March 20X1, the accounting effects were the following:

- In the subsidiary's financial statements, there was no effect (see Figure 6.18).

- In the parent's financial statements, the declared dividend was revalued at the then prevailing EUR–USD exchange rate and recognised as FX gains or losses (a loss in our case) in profit or loss. The recognition in profit or loss had a tax impact. Figure 6.18 highlights these effects.

- In the consolidated financial statements, the declared dividend still remained part of the net investment, as it was still unpaid. Therefore, the FX gains and losses due to the net investment revaluation were recorded in the translation differences account in equity (see Figure 6.19). In our case, as the USD depreciated against the EUR, a translation loss was recorded.

Figure 6.18 Reporting date (31-Mar-20X1) – effect on stand-alone financial statements.

Figure 6.19 Reporting date (31-Mar-20X1) – effect on consolidated financial statements.

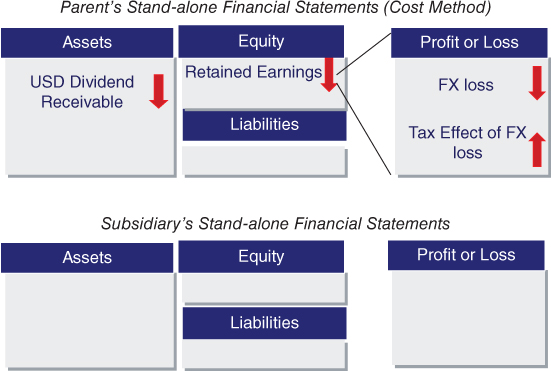

On 30 June 20X1, the USD 100 million dividend was paid. This USD cash was transferred from the subsidiary's USD cash account to the parent's USD cash account. The accounting effects on the three different reported financial statements were the following:

- In the subsidiary's financial statements, the balance of the USD cash account showed a USD 100 million reduction and the dividend payable was cancelled (see Figure 6.20).

- In the parent's financial statements, there were several effects (see Figure 6.20). Firstly, there was an FX loss due to the revaluation of the dividend receivable. This loss was recognised in profit or loss, which also had a tax impact. Secondly, the balance of the USD cash account increased by USD 100 million and the dividend receivable was cancelled.

- In the consolidated financial statements, at first sight, the dividend payment seemed to have no effect on a consolidated basis as the two USD cash accounts are grouped together. However, there was an important effect: the FX gains or losses from the revaluation of the USD 100 million were recognised differently, as explained next.

Figure 6.20 Divided payment date (30-Jun-20X1) – effect on stand-alone financial statements.

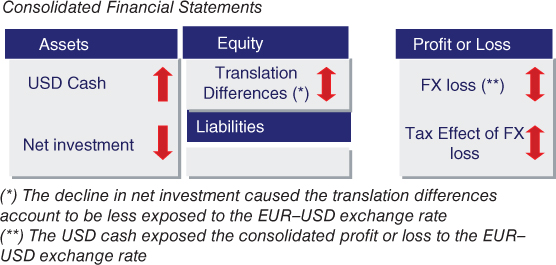

Before the dividend was paid, the USD 100 million cash was part of the net investment in the US subsidiary. Thus, foreign exchange gains or losses on the USD 100 million cash remeasurement in EUR were recorded in the translation differences account in equity.

After the dividend was paid, the USD 100 million cash was part of the monetary items of a group entity (i.e., the parent) that had the same functional currency as the group. Thus, foreign exchange gains or losses arising from the USD 100 million cash remeasurement impacted consolidated profit or loss.

Consequently, the effect of the dividend payment on a consolidated basis was a reduction in the net investment in the US subsidiary and an increase in the monetary items of the parent company (see Figure 6.21).

Figure 6.21 Divided payment date (30-Jun-20X1) – effect on consolidated financial statements.

The FX risk would have been eliminated from 30 June 20X1 had the parent exchanged the USD 100 million for EUR in the FX spot market on that date.

6.13.2 Hedging Intercompany Foreign Dividends with an FX Forward

Many companies seek to hedge forecast foreign currency dividends distributed by their foreign subsidiaries. Next, the implications of hedging foreign intragroup dividends are discussed in detail.

Suppose that on 1 January 20X1 ABC (the parent company) hedged the declared dividend through an FX forward with the following terms:

| FX forward terms | |

| Trade date | 1 January 20X1 |

| Nominal | USD 100,000,000 |

| Maturity | 30 June 20X1 |

| Forward Rate | 1.2320 |

| Settlement | Cash settlement |

Suppose further that the fair value of the FX forward at each relevant date was as follows:

| Date | Forward to 30-Jun-20X1 | Forward fair value |

| Declaration date: 1-Jan-20X1 | 1.2320 | -0- |

| Reporting date: 31-Mar-20X1 | 1.2510 | 1,222,000 |

| Dividend payment date: 30-Jun-20X1 | 1.2850 | 3,348,000 |

Subsidiary's Accounting Entries Relating to the FX Forward

No entries were required as the subsidiary was not a party to the FX forward.

Parent's Stand-alone Accounting Entries Relating to the FX Forward

The required accounting entries on the parent financial statements relating to the FX forward were as follows.

- Entries on 1 January 20X1

No entries were required as the fair value of the forward was zero at its inception.

- Entries on 31 March 20X1 (reporting date)

The change in fair value of the FX forward was a EUR 1,222,000 (=1,222,000 – 0) gain.

- Entries on 30 June 20X1 (reporting and FX forward maturity dates)

On this date the FX forward matured. The change in fair value of the forward was a EUR 2,126,000 (=3,348,000 – 1,222,000) gain.

- Through the forward, ABC delivered the dividend proceeds (USD 100 million, having a market value of EUR 77,821,000) and received EUR 81,169,000:

Consolidated Accounting Entries Relating to the FX Forward

Whilst the USD 100 million dividend represented a forecast intragroup transaction, on a consolidated basis ABC was not be able to apply cash flow hedge accounting because the foreign risk did not affect consolidated profit or loss. As a result, the FX forward was undesignated. Therefore, no entries were required as no adjustments were necessary to the parent accounting entries.

Summary of Impacts of the Hedge on the Financial Statements

On 31 March 20X1, the effects on the financial statements of the entities involved were the following:

- In the subsidiary's financial statements, there was no effect as the subsidiary was not a party to the FX forward.

- In the parent's profit or loss statement, the EUR 1,222,000 gain on the hedge largely offset the EUR 1,300,000 loss on the revaluation of the dividend receivable (see Figure 6.22). Therefore, the hedge performed well at the parent level.

- In the consolidated statements, the EUR 1,222,000 gain on the hedge showed up in profit or loss. This FX gain had no offsetting FX losses in profit or loss. The only FX loss showed up in the translation differences account, and as a result, the hedge largely eliminated the FX exposure (relating to the USD 100 million portion of the net investment in the subsidiary) of the consolidated equity. Therefore, while the FX forward offset the changes in the translation of USD 100 million of net assets, it exposed the consolidated profit or loss to movements in the EUR–USD exchange rate, as shown in Figure 6.23.

Figure 6.22 Reporting date (31-Mar-20X1) – effect on parent's stand-alone financial statements.

Figure 6.23 Reporting date (31-Mar-20X1) – effect on consolidated financial statements.

On 30 June 20X1, the effects on the financial statements of the entities involved were the following:

- In the subsidiary's financial statements, there was no effect as the subsidiary was not a party to the FX forward.

- In the parent's profit or loss statement, the effect was similar to that on 31 March 20X1. The EUR 2,126,000 gain on the hedge largely offset the EUR 2,100,000 loss on the revaluation of the dividend receivable. Therefore, the hedge performed well at the parent level.

- In the consolidated statements, the effect was similar to that on 31 March 20X0. The FX forward showed a EUR 2,126,000 gain that was recognised in the consolidated profit or loss statement, while there was a EUR 2,179,000 gain in the translation differences account. Therefore, the consolidated profit or loss was exposed to movements in the EUR–USD exchange rate.

In summary, the hedge worked well at the individual financial statements, but created distortions in the consolidated profit or loss.

What ABC Could Have Done Better

The distortion created by the hedge at the consolidated level could have been avoided if ABC had considered the FX forward as undesignated at the parent-only level. As a consequence, the changes in the FX forward fair value would have been recognised in profit or loss. ABC had already adopted this solution at the parent level. As discussed earlier, the hedge performed very well because the loss on the revaluation of the dividend receivable was almost completely offset by the gain in the FX forward (see Figure 6.22).

Alternatively, at the consolidated level, ABC could have designated the FX forward as the hedging instrument in a net investment hedge. The hedged item would have been USD 100 million of the net investment in the US subsidiary. As a consequence, the effective part of the change in the FX forward fair value would have been recognised in the translation differences account of equity. This way, there would have been a natural offset in the translation differences account between the effective part of the changes of the FX forward and the revaluation changes of the net investment. Section 6.8 includes a detailed explanation of the accounting mechanics of a net investment hedge with an FX forward.

Under this alternative, the parent's stand-alone accounting entries relating to the FX forward would have been identical to those covered previously. However, the consolidated accounting entries would have been different, as shown next.

Optimised Solution: Consolidated Accounting Entries Related to the FX Forward

The accounting entries at the parent and consolidated levels resulting from the FX forward were as follows.

- Entries on 1 January 20X1

None required.

- Entries on 31 March 20X1 (reporting date)

The EUR 1,222,000 gain recognised at the parent level was reversed. At the consolidated level, the FX forward was designated as hedging instrument in a net investment hedge. Assuming that the hedge was completely effective, the changes in the fair value of the FX forward were recognised in the translation differences account.

- Entries on 30 June 20X1

The EUR 2,126,000 gain on the forward was recorded similarly to the 31 March 20X0 adjustment.

Now the hedge performed very well at both the parent-only and consolidated levels, as shown in Figure 6.24.

Figure 6.24 Optimised solution – Effect on parent and consolidated financial statements.

6.14 CASE STUDY: HEDGING FOREIGN SUBSIDIARY EARNINGS

This case study illustrates a problem presently faced by many multinationals: the hedge of foreign earnings translation risk. Upon consolidation, most multinationals translate foreign subsidiaries' profit or loss at the average exchange rate for the accounting period. As a consequence, corporations are exposed to movements in that average exchange rate. The hedging problem arises because IFRS 9 at present does not allow the direct hedging of foreign earnings translation.

Suppose that ABC, a group whose presentation currency is the EUR, had a US subsidiary with a USD functional currency and that the subsidiary was expected to earn USD 400 million evenly during 20X0. Suppose further that ABC reported quarterly on a consolidated basis and that in order to hedge the quarterly translation exposure arising from the US subsidiary, ABC entered into the following four FX average rate forwards (AVRFs):

| AVRF 1 | AVRF 2 | AVRF 3 | AVRF 4 | |

| Trade date | 1-Jan-20X0 | 1-Jan-20X0 | 1-Jan-20X0 | 1-Jan-20X0 |

| Nominal | USD 100 mn | USD 100 mn | USD 100 mn | USD 100 mn |

| Maturity | 31-Mar-20X0 | 30-Jun-20X0 | 30-Sep-20X0 | 31-Dec-20X0 |

| Forward rate | 1.2500 | 1.2500 | 1.2500 | 1.2500 |

| Final rate | The arithmetic average of the daily closing EUR–USD spot from 1-Jan-20X0 until 31-Mar-20X0 | The arithmetic average of the daily closing EUR–USD spot from 1-Apr-20X0 until 30-Jun-20X0 | The arithmetic average of the daily closing EUR–USD spot from 1-Jul-20X0 until 30-Sep-20X0 | The arithmetic average of the daily closing EUR–USD spot from 1-Oct-20X0 until 31-Dec-20X0 |

| Initial premium | EUR 475,000 | EUR 150,000 | <EUR 160,000> | <EUR 465,000> |

| Settlement | Cash settlement | Cash settlement | Cash settlement | Cash settlement |

The payoff at maturity of each AVRF guaranteed an arithmetic average daily EUR–USD exchange rate during the quarter of 1.2500. For example, the EUR payoff of the first AVRF at maturity was:

where “Average” was the arithmetic average of the daily closing EUR–USD spot from 1-Jan-20X0 until 31-Mar-20X0.

The next thing that ABC had to decide was how to account for each AVRF. ABC had two alternatives:

- To treat each AVRF as undesignated, and therefore to recognise in profit or loss any changes in fair value of the AVRF. The potential increase in profit or loss volatility precluded ABC from adopting this alternative.

- To designate, in the consolidated statements, each AVRF as the hedging instrument in a hedge accounting relationship. The problem was that IFRS 9 did not allow the direct hedging of foreign earnings translation. One way to overcome this problem was to designate the AVRF as the hedging instrument in a cash flow hedge, as shown next.

The hedged item would be a highly expected forecast USD-denominated sales sufficient to equal the foreign subsidiary's forecast profit (USD 100 million) for each quarterly accounting period. ABC looked at all the entities within the group that had at least USD 100 million external sales denominated in USD. ABC found four entities that met such a requirement (see Figure 6.25).

- The parent entity. Because the functional currency of the parent entity was the EUR, the sales would be directly impacting consolidated profit or loss, constituting a transaction risk. As a result, assuming that all other requirements for the application of hedge accounting were met, those highly expected forecast sales could be designated as the hedged item.

- Subsidiary A. Because the functional currency of this subsidiary was the EUR, its sales would be directly impacting consolidated profit or loss on consolidation, constituting a transaction risk. As a result, assuming that all other requirements for the application of hedge accounting were met, those highly expected forecast sales could be designated as the hedged item.

- Subsidiary B. Because the functional currency of this subsidiary was the USD, its USD-denominated sales would not expose this entity to FX risk. Although on consolidation those USD sales would be indirectly impacting consolidated profit or loss, as part of the translation of Subsidiary B's profit or loss, they could not be designated as a hedged item because their risk was a translation risk rather than a transaction risk.

- Subsidiary C. The functional currency of this subsidiary was the JPY. Although its highly forecast USD sales exposed, when occurring, Subsidiary C's profit or loss statement to FX risk, the incorporation of this risk into consolidated profit or loss would be as a translation risk rather than as a transaction risk. Consequently, those sales could not be designated as a hedged item.

Figure 6.25 Hedge item preliminary candidates.

ABC nominated four hedging relationships. In each hedging relationship, ABC designated the first USD 100 million of the parent entity's highly forecast USD-denominated sales as the hedged item in a cash flow hedge. The AVRF related to the quarterly period being hedged was designated as the hedging instrument. As a consequence, changes in the effective part of the AVRF fair value were initially recognised in equity, and reclassified to profit or loss once the hedged cash flow affected profit or loss.

6.14.1 Hedging Relationship Documentation

The four hedging relationships, one for each quarter, were documented in a similar way. ABC documented the first quarter hedging relationship as follows:

| Hedging relationship documentation | |

| Risk management objective and strategy for undertaking the hedge | The objective of the hedge is to protect the EUR value of the cash flow stemming from a USD 100 million highly expected forecast sales of finished goods against unfavourable movements in the EUR–USD exchange rate. This hedging objective is consistent with ABC's overall FX risk management strategy of reducing the variability of its profit or loss statement with FX forwards and options |

| Type of hedge | Cash flow hedge |

| Hedged item | The cash flows stemming from the first USD 100 million highly forecast sales of finished goods originated by the parent entity, expected to take place during the period from 1 January 20X0 to 30 March 20X0. The sales are highly expected to occur as the parent entity has a consistent history of generating sales denominated in USD well in excess of USD 100 million |

| Hedging instrument | The FX average rate forward contract with reference number 017812, notionals of USD 100 million and EUR 80 million, maturity 31-Mar-20X0, and FX rate 1.2500. The counterparty to the AVRF is XYZ Bank and the credit risk associated with this counterparty is considered to be very low |

| Hedge effectiveness assessment | See below |

6.14.2 Hedge Effectiveness Assessment

Hedge effectiveness will be assessed by comparing, on a spot-spot basis, changes in the fair value of the hedging instrument to changes in the fair value of the highly expected cash flows.

Hedge effectiveness will be assessed prospectively at hedging relationship inception and on an ongoing basis at least upon each reporting date and upon occurrence of a significant change in the circumstances affecting the hedge effectiveness requirements.

The hedging relationship will qualify for hedge accounting only if all the following criteria are met:

- The hedging relationship consists only of eligible hedge items and hedging instruments. The hedge item is eligible as it is a highly expected cash flow that exposes the entity to FX risk and it is reliably measurable. The hedging instrument is eligible as it is a derivative instrument other than a written option.

- At hedge inception there is a formal designation and documentation of the hedging relationship and the entity's risk management objective and strategy for undertaking the hedge.

- The hedging relationship is considered effective.

The hedging relationship will be considered effective if the following three requirements are met:

- There is an economic relationship between the hedged item and the hedging instrument.

- The effect of credit risk does not dominate the fair value changes in the hedging relationship.

- The weightings of the hedged item and the hedging instrument (i.e., hedge ratio) are designated based on the quantities of hedged item and hedging instrument that the entity actually uses to meet the risk management objective, unless doing so would deliberately create ineffectiveness.

Whether there is an economic relationship between the hedged item and the hedging instrument will be assessed on a quantitative basis using a scenario analysis, comparing the cumulative change since hedge inception in the fair value of the expected cash flow arising from the forecast sale with the cumulative change since hedge inception in the fair value of the hedging instrument. The scenario to be analysed would be a 10% adverse move in the EUR–USD exchange rate.

The effective and ineffective amounts of the change in fair value of the hedging instrument will be computed by comparing the cumulative change in fair value of the hedging instrument with that of the hedged item. The effective amount will be recognised in the “cash flow hedge” reserve in equity. Any part of the cumulative change in fair value of the hedging instrument that does not offset a corresponding cumulative change in the fair value of the hedged item will be treated as ineffectiveness and recorded in profit or loss.

6.14.3 Hedge Effectiveness Assessment Performed at Hedge Inception

An effectiveness assessment was performed at inception and at each reporting date. The assessment also included the relationship hedge ratio and an identification of the sources of potential ineffectiveness. The conclusion that an economic relationship existed between the hedged item and the hedging instrument was justified by analysing one scenario in which the EUR–USD FX rate suffered a 10% unfavourable move during the quarter, as follows. The EUR–USD spot rate was 1.2392 at hedge inception (1 January 20X0). The hedged highly probable forecast sales for the first quarter were USD 100 million, split into three monthly forecast amounts of USD 33,333,000 for the months ending 31 January 20X0, 28 February 20X0 and 31 March 20X0. A 10% unfavourable move in the exchange rate implied a 1.3631 (=1.2392 × 1.10) EUR–USD spot rate on 31 March 20X0. Assuming a gradual move in the FX spot rate during the quarter, it implied a 1.2805 spot rate (= 1.2391 + 1/3 × (1.3631 – 1.2392)) on 31 January 20X0 and a 1.3218 spot rate (= 1.2391 + 2/3 × (1.3631 – 1.2392)) on 28 February 20X0.

The expected cash flows hedged under the first hedging relationship were USD 33,333,000 at the end of each month within the quarter. The overall change in fair value of these cash flows was a EUR 4,993,000 loss as evidenced in the following table:

| Date | Spot rate | Fair valued cash flow 1 | Fair valued cash flow 2 | Fair valued cash flow 3 | Total fair value change |

| 1-Jan-20X0 | 1.2392 | 26,899,000 (1) | 26,899,000 | 26,899,000 | |

| 31-Jan-20X0 | 1.2805 | 26,031,000 (1) | |||

| 28-Feb-20X0 | 1.3218 | 25,218,000 | |||

| 31-Mar-20X0 | 1.3631 | 24,455,000 | |||

| Change | <868,000> (1) | <1,681,000> | <2,444,000> | <4,993,000> |

Notes:

(1) 33,333,000/1.2392 = 26,899,000

(2) 33,333,000/1.2805 = 26,031,000

(3) 26,031,000 – 26,899,000

The change in fair value of the hedging instrument was calculated as follows:

- Fair value at inception: <475,000> (i.e., ABC received EUR 475,000 at the inception of AVRF 1).

- Fair value at maturity: 4,346,000 (= 100 mn/1.25 – 100 mn/1.3218), where 1.3218 was the quarterly average rate (= (1.2805 + 1.3218 + 1.3631)/3)).

- Hence, the change in fair value of the hedging instrument was a EUR 4,821,000 (= 4,346,000 + 475,000) gain.

The hedge qualified for hedge accounting as it met the three effectiveness requirements:

- Because in the scenario analysed the change in fair value of the hedged item (a loss of EUR 4,993,000) and the change in fair value of the hedging instrument (a gain of EUR 4,891,000) moved in opposite directions, it was concluded that the hedging instrument and the hedged item had values that would generally move in opposite directions, and hence that an economic relationship existed between the hedged item and the hedging instrument.

- Because the credit rating of counterparty to the hedging instrument was relatively strong (rated A+ by Standard & Poor's) the effect of credit risk did not dominate the value changes resulting from that economic relationship.

- The hedge ratio designated (1:1) was the one actually used for risk management and it did not attempt to avoid recognising ineffectiveness. Therefore, it was determined that a hedge ratio of 1:1 was appropriate.

There were three main sources of potential ineffectiveness: firstly, a significant credit deterioration of the counterparty to the hedging instrument (XYZ Bank); secondly, a reduction of the net assets of the hedged foreign operation below the hedging instrument notional; and finally, a substantial increase in the CCS basis. The credit risk of the counterparty of the hedging instrument would be continuously monitored.

Similar assessments were performed for the other three hedging relationships with similar results. The group concluded that all four hedging relationships met the requirements for the application of hedge accounting. The assessments performed at each reporting date yielded similar conclusions.

6.14.4 Other Relevant Information

The spot EUR–USD exchange rates and the fair value of the AVRFs on the relevant dates were as follows:

| Date | Spot rate | AVRF 1 fair value | AVRF 2 fair value | AVRF 3 fair value | AVRF 4 fair value |

| 1-Jan-20X0 | 1.2392 | <475,000> | <150,000> | 160,000 | 465,000 |

| 31-Jan-20X0 | 1.2400 | ||||

| 28-Feb-20X0 | 1.2600 | ||||

| 31-Mar-20X0 | 1.2800 | 635,000 | 2,057,000 | 2,333,000 | 2,602,000 |

| 30-Apr-20X0 | 1.3000 | ||||

| 31-May-20X0 | 1.2900 | ||||

| 30-Jun-20X0 | 1.2700 | 2,280,000 | 1,451,000 | 1,738,000 | |

| 31-Jul-20X0 | 1.2800 | ||||

| 31-Aug-20X0 | 1.2600 | ||||

| 30-Sep-20X0 | 1.2500 | 844,000 | 211,000 | ||

| 31-Oct-20X0 | 1.2700 | ||||

| 30-Nov-20X0 | 1.2900 | ||||

| 31-Dec-20X0 | 1.3100 | 2,481,000 |

6.14.5 Accounting Entries

The required journal entries were as follows.

- Entries on 1 January 20X0

The following entries were required as the fair value of the AVRFs at their inception were not zero.

- To record the closing of the accounting period on 31 March 20X0

The change in fair value of the AVRFs since the last valuation were as follows:

- AVRF 1, a gain of EUR 1,110,000 (=635,000+475,000);

- AVRF 2, a gain of EUR 2,207,000 (=2,057,000+150,000);

- AVRF 3, a gain of EUR 2,173,000 (=2,333,000-160,000);

- AVRF 4, a gain of EUR 2,137,000 (=2,602,000-465,000).

For simplicity, all hedges were assumed to have been fully effective (in practice, a small ineffective part would have arisen due to the FX forward points), and hence, all the changes in the fair value of the AVRFs were recorded in equity:

- USD 100 million sales of the parent entity, designated as the hedged item in the first hedging relationship, were recorded in the profit or loss statement of the parent and the group. As a consequence, the amounts related to AVRF 1 accumulated in equity (EUR 1,110,000) were reclassified to profit or loss:

- Finally, AVRF 1 matured and ABC received EUR 635,000 (=100 mn ×(1/1.25 – 1/Average)), where “Average” was the average of the spot rates at the end of each month during the first quarter (= (1.24+1.26+1.28)/3).

- To record the closing of the accounting period on 30 June 20X0

The change in fair value of the three remaining AVRFs since the last valuation was as follows:

- AVRF 2, a gain of EUR 223,000 (=2,280,000 – 2,057,000);

- AVRF 3, a loss of EUR 882,000 (=1,451,000 – 2,333,000);

- AVRF 4, a loss of EUR 864,000 (=1,738,000 – 2,602,000).

As the hedges were assumed to be fully effective, all these changes in fair value were recorded in equity:

- USD 100 million sales of the parent entity, designated as the hedged item in the second hedging relationship, were recorded in the profit or loss statement of the parent and the group. As a consequence, the amounts related to AVRF 2 accumulated in equity (EUR 2,430,000 = 2,207,000 + 223,000) were recycled to profit or loss:

- Finally, AVRF 2 matured and ABC received EUR 2,280,000 (=100 mn × (1/1.25 – 1/Average)), where “Average” was the average of the spot rates at the end of each month during the second quarter (= (1.30+1.29+1.27)/3).

- To record the closing of the accounting period on 30 September 20X0

The change in fair value of the two remaining AVRFs since the last valuation were as follows:

- AVRF 3, a loss of EUR 607,000 (=844,000 – 1,451,000);

- AVRF 4, a loss of EUR 1,527,000 (=211,000 – 1,738,000).

As the hedges were assumed to be fully effective, all these changes in fair value were recorded in equity:

- USD 100 million sales of the parent entity, designated as the hedged item in the third hedging relationship, were recorded in the profit or loss statement of the parent and the group. As a consequence, the amounts related to AVRF 3 accumulated in equity (EUR 684,000 = 2,173,000 – 882,000 – 607,000) were recycled to profit or loss:

- Finally, AVRF 3 matured and ABC received EUR 844,000 (=100 mn × (1/1.25 – 1/Average)), where “Average” was the average of the spot rates at the end of each month during the third quarter (= (1.28+1.26+1.25)/3).

- To record the closing of the accounting period on 31 December 20X0

The change in fair value of AVRF 4 since the last valuation was a gain of EUR 2,270,000 (=2,481,000 –211,000). As the hedge was assumed to be completely effective, this change in fair value was recorded in equity:

- USD 100 million sales of the parent entity, designated as the hedged item in the fourth hedging relationship, were recorded in the profit or loss statement of the parent and the group. As a consequence, the amounts related to AVRF 4 accumulated in equity (EUR 2,016,000) were reclassified to profit or loss.

- Finally, AVRF 4 matured and ABC received EUR 2,481,000 (=100 mn × (1/1.25 – 1/Average)), where “Average” was the average of the spot rates at the end of each month during the fourth quarter (= (1.27+1.29+1.31)/3).

6.14.6 Final Remarks

The hedge worked well as the objective of protecting the EUR translation value of USD 400 million of the US subsidiary's profit or loss at an exchange rate of 1.2500, or EUR 320 million, was achieved on a pre-tax basis, as shown in Figure 6.26.

Figure 6.26 US subsidiary's earnings hedge – effect on consolidated profit or loss.

However, specific issues may arise as a result of implementing a hedging strategy like the one just covered. Five in particular are worth noting:

- Firstly, ABC needed to arbitrarily identify within the group external highly expected USD-denominated forecast sales and designate them as hedged items in the four hedging relationships. If the group were to hedge those identified forecast sales as well, they would be part of an additional hedging relationship and, therefore, not available to their designation as hedged items in our four hedging relationships.

- Secondly, when deciding the USD nominal of the AVRFs, ABC needed to forecast its foreign subsidiary earnings and inefficiencies may arise from inaccurate forecasts.

- Thirdly, there could be undesired tax effects in profit or loss. In our case both the hedging instruments and the hedged items were booked in the parent entity, allowing it to consider the application of hedge accounting in the parent's stand-alone financial statements. However, were the hedged items located in an entity different from the parent, the four AVRFs would have been classified as undesignated, and as a result, the change in fair value of the AVRFs would have been recorded in profit or loss, increasing the volatility of the parent's profit or loss statement. If this entity was a tax-paying entity, losses on the AVRFs would be tax deductible, while gains on the AVRFs would be taxed. These tax effects may affect the parent entity's ability to distribute dividends. In reality, most corporations execute consolidation-related hedges in a treasury centre, reducing undesired tax effects on their group hedges.

- Fourthly, the hedge may distort EBITDA figures if the hedging instrument gains/losses were not recorded, adjusting the sales line. This did not apply in our case, as the AVRF results adjusted the USD sales figures.

- Finally, the average EUR–USD exchange rate used to translate the subsidiary's profit or loss may differ from the average rate used in the AVRFs. Often, a subsidiary's profit or loss is translated using the daily average rate during the accounting period ,while the group may decide to use monthly average rate in the AVRFs in order to reduce their administrative load. Average mismatches may create hedge ineffectiveness and result in undesired effects on profit or loss.

6.15 CASE STUDY: INTEGRAL HEDGING OF AN INVESTMENT IN A FOREIGN OPERATION

In my experience of advising multinationals on how to hedge their exposure to foreign subsidiaries, I have found an evolution (see Figure 6.27) in their hedging strategies over the years. Usually entities start hedging the exposure stemming from dividends received from their foreign subsidiaries. After a few years of hedging dividends, multinationals also address the exposure stemming from the translation of their subsidiaries' profit or loss statements. Finally, after gaining experience hedging earnings and dividends, multinationals also decide to hedge their net investment exposure.

Figure 6.27 Foreign subsidiaries hedging – common evolution pattern.

If an entity hedges these three risks separately – dividends, income statement and net investment – it could experience severe hedging inefficiencies as the three risks are interrelated. A special analysis is then needed when trying to hedge the combined risk. The key to the analysis is to understand how the net assets of a subsidiary change during an accounting year and which exchange rates affect their translation into the group's consolidated financial statements.

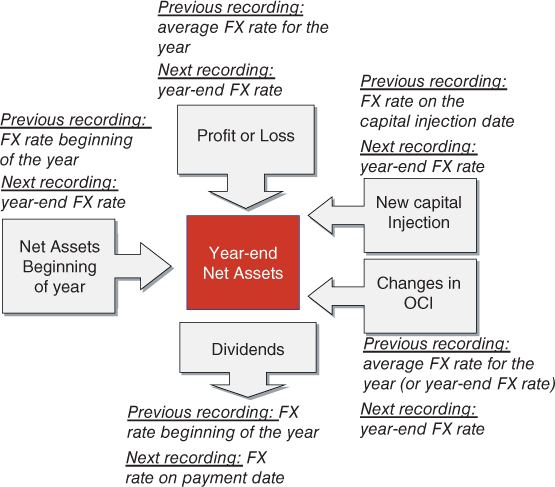

Assuming yearly reporting, a net investment in a foreign subsidiary can be split into five different components (see Figure 6.28):

- The net assets at the beginning of the year. The previous translation of this component was performed using the exchange rate prevailing at the closing of the previous year. As this component has to be revalued at the year-end exchange rate, the translation risk is caused by the change in the exchange rate from the end of the previous year to the end of the current year.

- The investment in new equity issued by the subsidiary during the year. Investing in new capital increases the net investment in the subsidiary. A capital injection is initially recorded at the FX rate prevailing at the moment of the capital increase. As this component has to be revalued at the year-end exchange rate, the translation risk is caused by the change in the exchange rate from the capital injection date to the end of the current year.

- The profit or loss generated by the subsidiary during the year. Positive earnings for the year increase the net investment in the subsidiary. Recall that a subsidiary's earnings are usually translated at the average exchange rate of the year. As this component has to be revalued at the year-end exchange rate, the translation risk is caused by the difference between the average exchange rate during the year and the exchange rate at the end of the current year.

- The dividends distributed by the subsidiary during the year. Dividends decrease a net investment. On the consolidated statements, dividends effectively leave the net investment when they are paid. Once paid, dividends do not affect net investment risk (they become part of the parent's monetary assets). Thus, a translation risk is caused by the change in the exchange rate from the closing of the previous year to the exchange rate prevailing on dividend payment date.

- The OCI generated by the subsidiary during the year. An increase in OCI for the year increases the net investment in the subsidiary. IAS 21 does not state the FX rate at which to translate changes in a subsidiary's OCI. The two most common alternatives are to translate them at the average exchange rate of the year or at the year-end exchange rate. In the former, the translation risk is caused by the difference between the average exchange rate during the year and the exchange rate at the end of the current year.

Figure 6.28 Foreign subsidiaries hedging – main components.

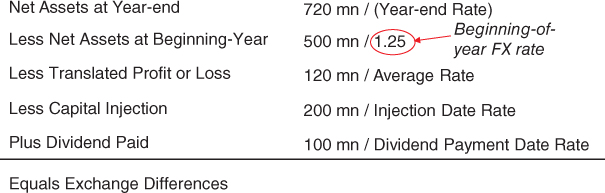

Let us consider a specific example. ABC, a group with the EUR as presentation currency, had a net investment in a US subsidiary whose functional currency was the USD. Suppose that at the beginning of 20X1 ABC was looking to fully hedge its net investment for the year ending 20X1. The expected changes to the net investment during the year 20X1 were as follows:

| Net investment in US subsidiary Expected changes during year 20X1 |

|

| Net assets (including goodwill and fair value adjustments) at the beginning of the year (31-Dec-20X0) | USD 500 million |

| Expected subsidiary's net earnings | USD 120 million (USD 10 million per month) |

| Expected dividends (expected to be paid on 31-May-20X1) | USD 100 million |

| Expected changes in the subsidiary's OCI | No changes expected |

| Expected new capital injection (expected to be executed on 30-Sep-20X1) | USD 200 million |

In order to get an idea of ABC's net investment exposure during 20X1, ABC produced the graph shown in Figure 6.29. During 20X1, the net investment was expected to increase by USD 10 million per month due to the subsidiary's net income. The net investment was expected to decline by USD 100 million due to subsidiary's expected dividend payment to the parent company on 31 May 20X1. Finally, the net investment was expected to increase by USD 200 million as a result of the parent's expected capital injection on 30 September 20X1.

Figure 6.29 Net investment profile – year 20X1.

One way to perfectly hedge the profile shown in Figure 6.29 was to execute on 1 January 20X1 a series of FX forwards aimed at hedging the five building blocks shown in Figure 6.28: hedging the year-end net assets, hedging the subsidiary's expected net earnings, hedging the expected new capital to be invested in the subsidiary, and hedging the expected dividends to be paid by the subsidiary (see also Figure 6.30). There was no need to hedge the net assets at the beginning of the year, as its rate was already known (1.25).

Figure 6.30 Exchange differences calculation – year 20X1.

Suppose that the market EUR–USD forward rates, as of 1 January 20X1, for the relevant dates were as follows:

| Date | Forward rate (as of 1-Jan-20X1) |

| 1 January 20X1 | 1.2500 |

| 31 May 20X1 | 1.2580 |

| 30 September 20X1 | 1.2650 |

| 31 December 20X1 | 1.2700 |

| Average during 20X1 | 1.2600 |

Hedge 1: Hedging Year-end Net Assets

The expected year-end net investment was USD 720 million, as shown in Figure 6.29. In order to hedge the year-end revaluation of the USD 720 million, ABC entered into a standard FX forward (“forward 1”) with a nominal of USD 720 million and maturity 31 December 20X1. The forward rate for 31 December 20X1 was 1.2700. The forward payoff at maturity compensated ABC for any appreciation of the year-end rate:

With this forward, ABC hedged the “net assets at year-end”, as shown in Figure 6.31 (first line of the table).

Figure 6.31 Exchange differences calculation, hedge 1, year 20X1.

Hedge 2: Hedging the Subsidiary's Expected Net Earnings

The subsidiary's expected profit or loss was USD 120 million. This amount was to become part of the net investment at the average rate for 20X1 and was to be revalued at year's end. The revaluation at year's end was already included in hedge 1. Therefore, ABC needed to hedge the translation of the subsidiary's expected profit or loss at the average rate for the year 20X1. This hedge covered the third line of Figure 6.32.

Figure 6.32 Exchange differences calculation, hedge 2, year 20X1.

As seen in the case study in Section 6.14, the appropriate hedging instrument was an average rate forward (forward 2).

The average rate forward had a USD 120 million nominal amount and a 31 December 20X1 maturity. The market expected the average rate to be 1.26. Its payoff at maturity was:

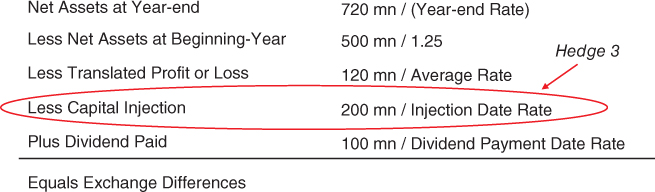

Hedge 3: Hedging the Expected New Capital Injection into the Subsidiary

ABC's parent entity expected to add USD 200 million capital to its US subsidiary. From a “net investment” perspective, ABC was exposed to the year-end appreciation of the EUR–USD rate relative to the rate prevailing on the capital investment date (30 September 20X1). The first part (the year-end revaluation) was already hedged through hedge 1. ABC needed then to hedge (“hedge 3”) the exposure to rate prevailing on the capital investment date, which was equivalent to hedge the fourth line of Figure 6.33.

Figure 6.33 Exchange differences calculation, hedge 3, year 20X1.

The appropriate instrument was an FX forward (“forward 3”) with a nominal of USD 200 million, maturity 30 September 20X1 and the following payoff at maturity:

Hedge 4: Hedging the Expected Dividends Paid by the Subsidiary

ABC's parent entity expected to receive USD 100 million dividends from its US subsidiary on 31 May 20X1. As a result, ABC's parent company was exposed to an appreciation of the EUR–USD FX rate prevailing on the dividend payment date (31 May 20X1).

The appropriate hedge was an FX forward (“forward 4”) with a nominal of USD 100 million and maturity 31 May 20X1. This hedge covered the exposure outlined in the fifth line of Figure 6.34. The payoff of forward 4 at maturity compensated ABC from any appreciation of the 31 May 20X1 exchange rate:

Figure 6.34 Exchange differences calculation, hedge 4, year 20X1.

Expected Translation Differences Adjustment for the Year 20X1

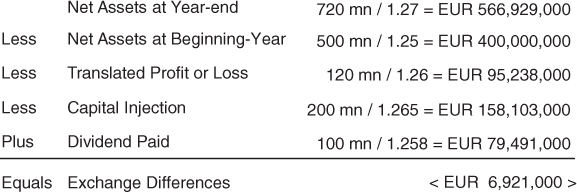

As a result of these four hedges, ABC expected to recognise a translation differences deficit of EUR 6,921,000, as shown in Figure 6.35.

Figure 6.35 Exchange differences calculation, integral hedge, year 20X1.

Hedge Performance Analysis

Let us assess whether the integral hedge worked well in practice. Suppose that the market EUR–USD FX rates during 20X1 were as follows:

| Date | Spot EUR–USD Rate |

| 1 January 20X1 | 1.2500 |

| 31 May 20X1 | 1.3000 |

| 30 September 20X1 | 1.2000 |