Government Policy on Delivering Biofuels for the Aviation Sector

D. Thrän1,2,3 and J. Ponitka2, 1Department Bioenergy, Helmholtz Center for Environmental Research – UFZ, Leipzig, Germany, 2Deutsches Biomasseforschungszentrum gGmbH – DBFZ, Leipzig, Germany, 3University of Leizpig, IIRM, Leipzig, Germany

Abstract

Air transport is a developing business sector, with rapidly increasing rates in transport loads and fuel demand. Aircraft emissions are impacting greenhouse gas (GHG) emissions and hence inducing climate change. Decarbonization in the aviation sector is being addressed by international airline organizations (eg, IATA), and in different policies as well. Biojet fuels can contribute to this goal substantially in the short- and medium-term because they can be applied as drop-in fuels without major changes in infrastructure or aircraft engines. Technical standards for certain biojet fuels have successfully been established during the last several years. On the other hand, biojet fuel implementation needs policy adoption and instruments – that is, by considering the GHG emission reduction of renewable fuels in taxation, Emissions Trading System or quotas, or blending mandates. Additionally, sustainability of biojet fuels along the whole value chain needs to be reflected and assured by appropriate certification standards and schemes. During the last few years, experience from the application of biofuels has been gained; biojet fuel certification can be built upon this. The restricted land availability and the related environmental effects demand a coherent monitoring system for the market implementation of biojet fuels. This is in conjunction with long-term support for research and development on sustainable feedstock provisions, efficient conversion technologies, and integration of biojet fuels in overall concepts of an efficient and mainly renewable energy supply in the future. Due to the internationality of the sector, a coherent international biojet fuel policy is strongly recommended to realize the intended GHG emission reduction in the aviation sector.

Keywords

Climate effects from aviation; availability and costs of biojet fuels; instruments for biojet fuel implementation; technical standards for biojet fuels; sustainability standards for biojet fuels, biojet fuel policy in Europe; biojet fuel policy in Brazil; biojet fuel policy in the United States; biojet fuel targets

13.1 Biofuels in the Aviation Sector – Current Status and Expectations

This section highlights the current state-of-the-art of biofuel utilization within the aviation sector, as well as expectations for the use of biojet fuels in the future – that is, development of the aviation sector, greenhouse gas (GHG) effects from aviation, feedstock availability for biojet fuels, cost of biojet fuels, scenarios for market implementation, and supply conditions for biojet fuels.

13.1.1 Development of the Aviation Sector

Air transport is a developing business sector with rapidly increasing rates in transport loads and fuel demand (Fig. 13.1). For example: (1) air passenger transport increased from 2.072 billion in 2006 to 3.213 billion passengers in 2014 [1]; (2) the related revenue passenger kilometres (RPK) performed grew about 6% per year on average between 2001 and 2013, reaching 5.8 trillion RPK, international and domestic services combined [2]; (3) world scheduled air freight traffic expressed in freight tonne-kilometres performed grew by 0.4% in 2013, and is expected to increase by about 4% per year in 2014, 2015, and 2016, respectively [2]; and (4) kerosene demand increased steadily to 6.3 mb/day in 2013, which is equivalent to about 10 EJ/a (see Fig. 13.1).

A strong increase in air transport is also expected for the future – that is, Airbus and Boeing project passenger transport growth of about 5% per year from 2010 to 2030 [5]. Air traffic is expected to increase from 3.8% to 5.1% [3] per year, which will lead to over 18 billion RPK in 2040 compared to around 5 billion RPK in 2010 (Fig. 13.1). The related increase in kerosene demand is expected with ‘only’ 1.5% per year between 2012 and 2035 [6] because of several improvements in the specific fuel demand. Due to the long life of aircraft products, particularly engines (typically 30–40 years), the speed at which these improvements are incorporated into the total fleet is a slow process. Besides the fuel efficiency of aircraft, another major area that offers considerable potential for significantly reducing fuel demand is the optimization of air traffic management [7].

13.1.2 Greenhouse Effects From Aviation

Aircraft emissions, in conjunction with other anthropogenic sources, are impacting GHGs and hence inducing climate change, though the extent of such impacts are difficult to predict and are heavily debated. Atmospheric changes from aircraft result from three types of processes: (1) direct emission of radioactive substances (eg, CO2 or water vapour); (2) emission of chemical species that produce or destroy radioactive substances (eg, NOx, which modifies O3 concentration); and (3) emission of substances that trigger the generation of aerosol particles or lead to changes in natural clouds (eg, contrails). The largest areas of scientific uncertainty in aircraft-induced climate effects lie with persistent contrails, with tropospheric ozone increases and consequent changes in methane, with potential particle impacts on ‘natural’ clouds, and with water vapour and ozone perturbations in the lower stratosphere (especially for supersonic transport) [8].

Aviation contributed about 2% of anthropogenic CO2 emissions in the year 2000, which is equivalent to 10% of the direct emissions of the transport sector [9]. In the absence of additional measures, an increase in emissions of 3–4% per year is projected. There is also considerable concern regarding aviation’s total climate impact on the global climate, which has been estimated by the Intergovernmental Panel on Climate Change (IPCC) as being two to four times higher than the effect of carbon dioxide emissions alone due to release of nitrogen oxides, water vapour, and sulphate and soot particles (excluding cirrus cloud effects) [10]. Lee et al. [11] estimated radiative forcing from aviation in the year 2005 to be 3.5% (range 1.3–10%, 90% likelihood range) of current anthropogenic forcing, or, including cirrus cloud enhancement, 4.9% of current forcing (range 2–14%, 90% likelihood range).

The public and political pressure on the sector to decrease its GHG emissions is increasing, particularly in Europe. The International Air Transport Association (IATA) has therefore already agreed on global targets for GHG emissions, as follow [3,12–14]:

• Improve fuel efficiency by 1.5% annually to 2020;

• Cap net emissions from 2020 onward through carbon-neutral growth;

To support these targets, in 2050 technologies and procedures need to be available that allow a 75% reduction in CO2 emissions per passenger kilometre [15].

Several studies have investigated the development of aviation-related global CO2 emissions, but found that the suggested CO2 reduction needs to incorporate additional efforts to change the currently expected trends [5]. Along with this increase, and despite improvements in efficiency, consumption of jet fuels, and also absolute emissions, will steadily increase [16]. This was also pointed out by the International Civil Aviation Organization (ICAO) in 2013 (see Fig. 13.2). Biojet fuels are seen as one approach to close the CO2 gap.

This is not only discussed by the aviation sector, but also pointed out in different energy scenarios with ambitious GHG reduction targets (eg, Refs [17–19,70]). Policy makers argue that due to persistent reliance on fossil fuels, it is often posited that transport, especially aviation relying entirely on kerosene, is more difficult to decarbonize than other sectors [20]. So climate policy is an important driver for the implementation of biojet fuels.

13.1.3 Feedstock Availability for Biojet Fuels

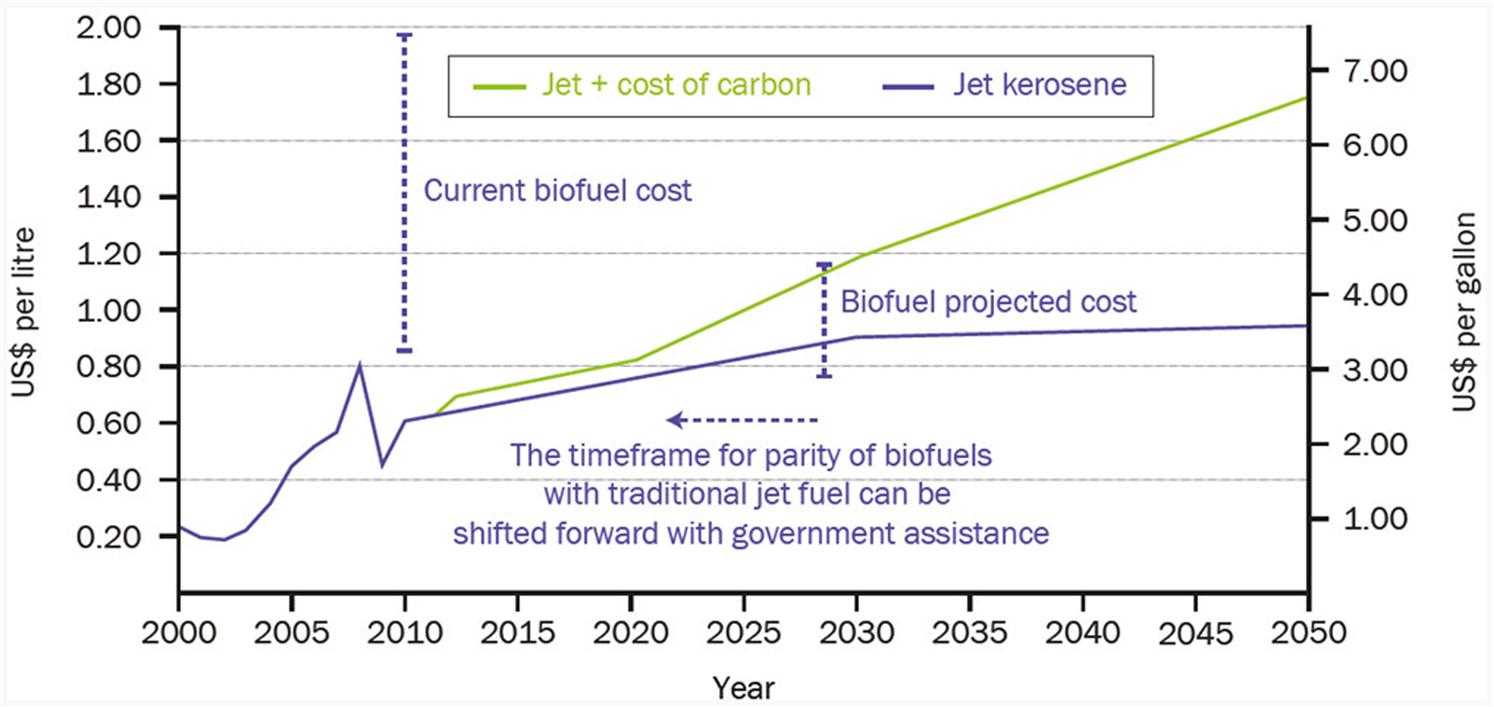

Going for a biojet fuel application, a reasonable question is, what is the overall biomass feedstock availability in the medium- and long-term? It proves difficult to provide any reliable forecast, but different scenarios suggest an overall aviation fuel demand of 16 to 25 exajoules (EJ) in 2050, which is equivalent to a biomass demand of about 33 to 45 EJ/a [5,21] if all the aviation fuel was be provided via biojet fuels (see Fig. 13.3).

This amount is in the range of about 65–80% of the overall biomass use of 55 EJ/a [23] for bioenergy today. The future biomass potential is estimated to be in the range of 100–300 EJ/a in 2050 [22]. So in a very first, theoretical approach, the biomass resource potential is seen as potentially sufficient to meet future kerosene demands if other bioenergy applications (heat, power, transport fuels) are not extended significantly in the future. Those theoretical numbers do not give any information about specific feedstock availabilities for different conversion routes.

13.1.4 Cost of Biojet Fuels

There is a wide range of potential costs for biojet fuels, from as low as 21 EUR/GJ up to 90 EUR/GJ (Table 13.1), usually greatly exceeding current kerosene prices. Feedstock costs not only vary substantially by region [24], but are usually an important component of total provision cost. As feedstock for the biojet fuel technologies is the major cost factor, the future costs of biojet fuels will be highly dependent on feedstock cost development.

Table 13.1

Costs of Biojet Fuels (Exemplarily)

| Today | Range (Approximate) | Projections | |

| BTL (Fischer–Tropsch fuel) | Approximately 29 €/GJ [5] (but no commercial plant) | 35–65€/GJ [25–27] | 18–23€/GJ (based on Ref. [5]) |

| HEFA (vegetable oil) | 26–29 €/GJ [28] | 21–50€/GJ [5,25–27] | 20–26€/GJ (based on Ref. [5]) |

| Bio-GTL | – | 55–90€/GJ [25,26] | |

| Kerosene (Jet A-1) | 10.8 €/GJa | 8–20 €/GJb (10/2005–10/2015) (based on [29]) | 2050: 19.4€/GJ (based on 2% annual increase, following IEA WEO projections [6]) |

Note: Due to changes in price and currency exchange rates, the price gap between fossil kerosene and biojet fuel provision costs may vary.

a30 Oct. 2015: 1.543 US$ per gallon aviation jet fuel [approximately 460€/t or 10.8 €/GJ] [67,68].

b1.26–3.89 $/gallon, exchange rates: http://www.finanzen.net/devisen/dollarkurs/historisch.

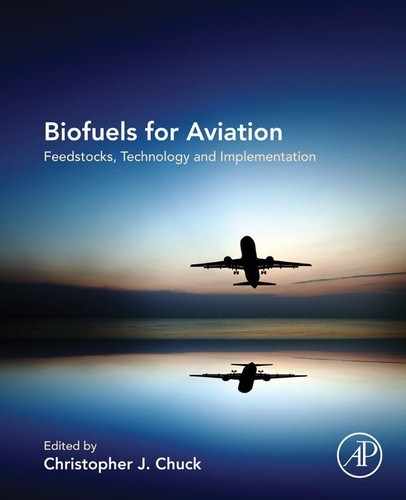

As kerosene is one of the major cost factors in an airline’s total operating costs, the fossil fuel price and price development are also relevant for the market development of biojet fuels. In the past several years, the price of jet kerosene has fluctuated between less than $1 and up to $4 per gallon, with a recent declining trend.

Due to the recent decrease in oil prices, kerosene price projections (eg, Fig. 13.4), and the possible parity of renewable kerosene with fossil kerosene, proves difficult. In the longer term, price parity could be achieved with additional measures (eg, carbon price).

The production costs of renewable kerosene will, for the foreseeable future, be considerably higher than the corresponding fossil kerosene costs [30].

Another promising renewable, nonbio-based option in the future could be jet fuels based on power (PTL, Power-to-Liquid), for which the first demonstration projects (eg, Sunfire or SOLAR-Jet) have already reported the feasibility of various concepts [31–32]. Nevertheless, for those renewable biojet fuels, even higher costs are reported, such as PTL (via Fischer–Tropsch (F-T) or methanol) with a cost range of 25–150€/GJ [25,26]. Consequently, policy action is needed in the short term to induce a sufficient demand.

13.1.5 Supply Conditions for Aviation Fuels

The main aviation fuels (Aviation Turbine Fuel) are Jet A-1 (standard commercial aviation fuel outside the United States) and Jet A (in the United States). Other jet fuels (eg, Jet B, JP-8) for military uses or cold climates do exist. Aviation fuels are based on kerosene fractions as a complex mixture of hydrocarbons that varies depending on crude source and manufacturing process, typically derived from crude oil [33]. The requirements are specified in the fuel standards DEF STAN 91-91 [33] and American Society for Testing Materials (ASTM) D16551. The standard ASTM D7566 specifies Aviation Turbine Fuel Containing Synthesized Hydrocarbons, and is relevant for renewable jet fuels. Important specifications of the main fuel JET A-1 are the following:

From a variety of feedstocks and their pretreatment, extraction, or separation steps, the main conversion (physico-chemical, thermo-chemical, bio-chemical) and subsequent processing or upgrading provide the final product (examples in Table 13.2). Three of these renewable fuels (hydroprocessed esters and fatty acids (HEFA), F-T, synthesised iso-paraffins (SIP)) are already ASTM (ASTM D7566) certified, which allows a blending of up to 50% (SIP up to 10%) with conventional commercial and military jet fuels. In different projects (burnFAIR; High Biofuel Blends in Aviation (HBBA)), the test of blended jet fuels showed no negative effects on noise emissions, no effects or positive effects on CO2 and NOx, and positive effects on soot and particle emissions [34]. The commercial availability of the fuels is still limited, and to date, there has been little routine production of alternative jet fuel. Commercial flights thus far have been operated with specially produced batches of fuel [35].

Table 13.2

Conversion Pathways for Biojet Fuels

| Pathway | Feedstock/Technology | ASTM Certification |

| HEFA | Hydro-processed esters and fatty acids (vegetable oils); future: algae oils | X |

| F-T | Fischer–Tropsch kerosene (BTL) from lignocellulosics | X |

| DSCH/SIP | Direct sugar to hydrocarbon/Synthesized Iso-Paraffinic fuel (sugar to farnesene from, eg, sugar cane) | X |

| Bio-GTL | Biogas to liquid via biomethane and a wide range of biomass feedstock | – |

| ATJ | Alcohol to jet | – |

| HDCJ | Hydrotreated depolymerized cellulosic jet | – |

| PTL | Power-to-Liquid; electrolysis and subsequent synthesis either via F-T or methanol | – |

Data from U. Lambrecht, F. Müller-Langer, Themenbereich 3 “Alternative Energieträger im Verkehr und ihre Infrastruktur”. Presentation Hold: Mobilitäts-und Kraftstoffstrategie (MKS) Jahreskonferenz 2015. On 09-06-2015 in Berlin, 2015; F. Müller-Langer, K. Zech, K. Naumann, Alternative Fuels for Aviation – Status quo and Perspectives of Different Options. Presentation Hold: CORE JetFuel Workshop | Sustainable Alternative Aviation Fuels – Innovative Conversion Technologies and Deployment. On 01-06-2015 in Vienna, 2015; [36] AIREG (Ed.), Klimafreundlicher Fliegen: Zehn Prozent Alternative Flugkraftstoffe bis 2025. Aireg – Aviation Initiative for Renewable Energy in Germany e.V., 2012; [37] AIREG e.V., http://www.aireg.de/en/production.html. Biofuel Production, Aviation Initiative for Renewable Energy in Germany e.V. Retrieved from: <http://www.aireg.de/en/production.html>, 2015 (26.11.15); [38] L.A.B. Cortez, G.M. Souza, C.H.de B. Cruz, R. Maciel, An Assessment of Brazilian Government Initiatives and Policies for the promotion of biofuels through research, commercialization, and private investment support, in: S.S. da Silva, A.K. Chandel (Eds.), Biofuels in Brazil, Springer International Publishing, pp. 31–60. ISBN 978-3-319-05019-5, 2014.

The supply chain of Jet A-1 and biojet fuels includes extraction, conversion, and distribution [39]. The aim of the aviation industry is that the drop-in characteristics of biojet fuels will allow the fuels to be fully integrated into the conventional jet fuel storage and distribution systems, and therefore be used by all aircraft refuelling from those systems with no barriers [40]. As biojet fuels meet the technical standards (Jet A-1, ASTM), no modifications within the current distribution system are necessary. The certified biojet fuel (and conventional Jet A-1 from different sources) can be blended at any point (preferably at the refinery) of the supply chain with Jet A-1.

In most cases the biojet fuel will be delivered to and blended at a small number of international consumer points. International agreements are therefore a precondition to delivering the biojet fuels to the big international airports and selling them to international airlines. As the future sees increasing quantities of biofuels available at the main aviation hubs, logistics remain a challenge, and so does transport from the producer to the airport or the location of fuel blending. About 50% of current cargo and passenger transport are organized in less than 50 airports worldwide (see Fig. 13.5). Adjusted frame condition is also demanded for international trade for the majority of the biojet fuels [5].

13.2 Policies Influencing the Market Introduction of Biojet Fuels

This section describes the current situation in government policies for delivering biojet fuels, including the target definition and the different instruments in general, and the more detailed description regarding government policies in different countries/regions in particular.

13.2.1 Agreements on Targets for Biojet Fuel Implementation

Renewable energy policy in general, and biojet fuel implementation interests in particular, follow different overall targets in different nations and regions. Those include climate policies, policies on energy security, agriculture policies, and economic policies. So it is not surprising that there is no globally agreed-upon target regarding the amount or share of biojet fuels.

There are some national targets and usage goals to encourage the production of biojet fuels: in the United States, ‘1 billion gallons of alternative jet fuels annually by 2018’ [41]; in Indonesia, 2% aviation biofuels by 2018; in Norway, 10% biojet fuel by 2020; and in Mexico (2011), 1% by 2015 and 45% by 2020 [42].

Different goals were formulated within the European Union (EU) regarding biojet fuels. According to the Biofuel FlightPath Initiative [43], the targeting of two million tonnes annual production of fuel derived from renewable sources by 2020 would facilitate the deployment of sustainably produced advanced biofuels for the EU aviation sector [43]. One white paper [9] formulated the goal of 40% low-carbon sustainable fuels in aviation by 2050.

Stakeholders also propose national goals, such as the use of 10% biojet fuels in 2025 in Germany [36]. Several airlines have announced that they have already concluded long-term (up to 10 years) off-take agreements with biofuel suppliers within the range of 10,000 to 100,000 tonnes per year from different feedstocks (waste, forest residues, HEFA) [12].

The International Energy Agency (IEA) has come up with expectations for the deployment of biofuels and biojet fuels as well (Fig. 13.6). The IEA sees advanced aviation fuels as a middle-term solution, with the demand expected to increase significantly [44]. It must be mentioned that there are many other projections of future supply of biojet fuels, and the expected share of renewables in the aviation sector differs wildly from 10% of the overall fuel demand up to 100% [5].

13.2.2 Instruments for Biojet Fuel Implementation

A wide variety of policy instruments and measures is available to achieve the desired goal of limiting emissions of GHG and hence influence the market introduction of biojet fuels. This includes, for example, raising communication or awareness, research and development support (innovation), guidelines, governance and coordination, voluntary agreements, market-based instruments, private and nonprivate financing schemes, tradable permits, taxes and charges, subsidies and incentives, and new regulations and standards (see Refs [9,10,45]). The main stimulus for current biofuels is blending mandates. Their outlook is highly sensitive to possible changes in government subsidies [6].

The market implementation for renewable energies is supported by a wide range of instruments. In general, they can be classified into five major groups, which are described in Table 13.3. Those systems are prototypes, while in practice the instruments are often combined.

Table 13.3

Typical Support Schemes for Renewable Energies

| Instrument | Principle | Cost Burden for… |

| GENERAL INSTRUMENTS FOR CLIMATE POLICY | ||

| European ETS | For the emission of GHG, certificates need to be posessed/bought. | Supplier/end user |

| Taxation | For products with higher GHG-related emissions, higher tax rates have to be paid. | Supplier/end user |

| DEDICATED INSTRUMENTS FOR RENEWABLE ENERGY IMPLEMENTATION | ||

| Feed-in tariffs | Producer gets a guaranteed price for the provided renewable energy. | End user |

| Investment support programs | Producer gets investment support for certain parts of the conversion plant and/or infrastructure. | Government |

| Taxation | For renewable products, lower tax rates have to be paid (tax credit, tax exemption). | Government |

| Quotas/blending mandates | Suppliers have to provide a certain share of renewables in their product portfolio. | Supplier/end user |

Data from IEA, World Energy Outlook 2013, International Energy Agency. Paris, ISBN 978-92-64-20130-9, 2013; [46] D. Thrän, M. Edel, T. Seidenberger, S. Gesemann, M. Rohde, Identifizierung strategischer Hemmnisse und Entwicklung von Lösungsansätzen zur Reduzierung der Nutzungskonkurrenzen beim weiteren Ausbau der energetischen Biomassenutzung. 1. Zwischenbericht für das deutsche Minisiterium für Umwelt, Naturschutz und Reaktorsicherheit, Deutsches Biomasseforschungszentrum, Leipzig, 2009.

Within the scope of the market implementation of alternative aviation fuels, the main policies discussed or implemented are the following:

• Taxation (eg, VAT or ticket tax, carbon tax, tax exemptions/credits, kerosene tax);

• Emission charges (emissions cap-and-trade system; Emissions Trading System (ETS)).

Worldwide quotas are often proposed, as EU-wide, national, or regional measures may lead to certain market distortions, competitive disadvantages, and adverse effects, such as the shift of passengers or airlines to unaffected airport hubs.

In addition, research and commercialization funding and investment (promotion actions) are considered to be a required action to support a range of potentially successful biofuel technologies, from which a winner, or winners, may emerge [14]. This, for example, includes the planning and construction of biojet fuel refineries to achieve economies of scale and to gain experience.

13.2.3 European Union

The EU is currently responsible for 35% of global aviation emissions [47]. With acknowledgement for the Kyoto Protocol’s project mechanisms in 2004, the EU established a scheme for GHG emission allowance trading within the Community (Directive 2004/101/EC). The EU ETS remains the world’s largest scheme, covering all 28 member states of the EU, plus Norway, Iceland, and Liechtenstein [6].

To attempt to mitigate emissions in the aviation sector, although a Europe-wide emissions charge ‘has proved difficult’ [48], the emissions from international aviation were included as a binding policy from the 1 Jan. 2012 into the carbon market in the EU ETS [48]. Emissions from all flights arriving and departing from airports in the EU were to be incorporated into the scheme, covering around a third of global aviation emissions. The aviation sector cap has been defined as 210 MtCO2e per year for 2013–2020 (and not decreasing). Also in 2012, 85% of the allowances were allocated for free based on benchmarks [49]. For the time period 2012–2020, 15% of allowances are to be auctioned and 82% allocated for free based on benchmarks. The remaining 3% constitutes a special reserve for new entrants and fast-growing airlines [49]. In response to a backlash from the aviation sector, in Apr. 2013 the EU temporarily suspended enforcement of the EU ETS requirements for flights operating from or to non-European countries, while continuing to apply the legislation to flights within and between countries in the European Economic Area, regardless of the carriers’ origin [49,50]. The EU institutions will decide on how to further regulate aviation emissions within the EU ETS after 2016 based on progress within the ICAO on developing a global market-based mechanism to address international aviation emissions from 2020 [49].

The EU Directive 2009/30/EC sets targets for fuel suppliers to gradually reduce life cycle GHG emissions by up to 10% per unit of energy from fuel and energy supplied by 2020. This reduction should be obtainable through the use of biofuels and alternative fuels. It is recognized that production of biofuels in certain developing countries might not meet minimum environmental or social requirements, and these countries are encouraged to develop agreements and voluntary international or national schemes that cover key environmental and social considerations in order to promote the production of biofuels worldwide in a sustainable manner.

In order to ensure the sustainability of alternative fuels, a range of legal policies were implemented in Europe, in particular, the EU Renewable Energy Directive (EU RED) 2009/28/EC [51] for the promotion of the use of energy from renewable sources, including sustainability criteria for biofuels and bioliquids. The RED sets a 10% target for the use of renewable energy in transport by 2020, and is currently realizing a new public consultation related to the ‘preparation of a new Renewable Energy Directive for the period after 2020’. For aviation biofuels to be counted, this requires implementation at the member state level. At present this has only been implemented by the Netherlands [52].

Alongside the RED, the EU Fuel Quality Directive 2009/30/EC (FQD) sets a 6% target of GHG emission reduction from all energy used in transport for 2020 as compared to 2010. The FQD target does not apply to aviation fuel, but is expected to be a driver for increased road biofuels, alongside the RED [52]. The RED and the FQD have harmonized requirements regarding biofuel sustainability [40]. National implementation of the EU RED is necessary and leads to differences between the policies in the EU member states, especially with regard to priorities in market implementation of renewables in different energy sectors.

Further progress of the EU RED with respect to aviation will depend on the commission’s report (scheduled for 2021), which reviews the application of this directive. That report shall in particular address ‘technological developments in energy from renewable sources, including the development of the use of biofuels in commercial aviation’ [51] on the best cost-benefit basis. Also, the results of the COP21 negotiations in Paris might influence the further development of European policies on biofuel delivery.

13.2.4 United States

In the United States, several initiatives and broad national strategies of the federal government promote the development of a variety of alternative fuels – partly including alternative jet fuel – to help achieve national goals, such as securing energy independence, fostering economic development, and reducing GHG emissions. In addition, the renewable fuel program – established by law in 2005 to encourage greater use of renewable fuels – requires that US transportation fuels contain certain amounts of renewable fuels annually. Other federal agencies – that is, Department of Transportation’s (DOT) Federal Aviation Administration (FAA), US Department of Agriculture (USDA), Department of Energy (DOE), and Department of Defense (DOD) – directly support alternative jet fuels through targeted goals, initiatives, and interagency and industry coordination [41].

For example, the FAA set a goal for the US aviation industry to use 1 billion gallons of alternative jet fuels annually by 2018. The FAA and DOD support research to determine the technical feasibility of using new alternative jet fuels on aircraft and in the existing infrastructure. Also, the USDA, DOE, and DOD have coordinated their activities to support the future construction or retrofit of multiple domestic commercial- or precommercial-scale production facilities to produce alternative fuels, including alternative jet fuels. One example is the Farm to Fly initiative that has brought together the US aviation community, government stakeholders, the USDA, the DOE, the DOT, and the DOD, and has already been extended to Farm to Fly 2.0 [53,54]. Specifically, in May and Jun. 2013, four private fuel producers received awards totalling $20.5 million in federal funds, with private industry paying at least 50% of the cost [41].

The USDA recently announced a loan guarantee, provided through the Biorefinery Assistance Program, to help innovative companies turn waste into renewable jet fuel [55]. Congress established the Biorefinery Assistance Program within in the 2008 Farm Bill. It reauthorized and extended the program in the 2014 Farm Bill, and expanded the program to include bio-based renewable chemicals and bio-based product manufacturing through regulations to set forth upcoming application terms for additional loan guarantees under the program.

One of the more prominent forms of federal policy support is the Renewable Fuel Standard (RFS), where a minimum volume of biofuels is to be used in the national transportation fuel supply each year. Congress first established the RFS with the enactment of the Energy Policy Act of 2005. The Energy Independence and Security Act of 2007 greatly expanded the biofuel mandate volumes and extended the date through 2022. The expanded RFS (RFS2) required the annual use of 9 billion gallons of biofuels in 2008, rising to 36 billion gallons in 2022, with at least 16 billion gallons from cellulosic biofuels, and a cap of 15 billion gallons for corn-starch ethanol. The RFS is a market-based compliance system in which involved parties have to submit credits (Renewable Identification Numbers (RINs)) to cover their obligations. Nevertheless, jet fuel, among other things, is excluded from RFS2’s national transportation fuel supply. Renewable fuels used for these purposes may, however, count towards the RFS2 mandates [56].

Therefore, a combination of incentives according to the RFS, and incentives for agriculture, under the right conditions, may open the possibility for price-competitive biojet fuel being available [12].

13.2.5 Brazil

Brazil has long experience with biofuels in the transport sector. Currently, Brazil does not have a specific policy for alternative aviation fuels, however, initiatives exist on the state level. As a member of ICAO, Brazil supports its goal of carbon-neutral growth from 2020 [57].

In recent years, several initiatives have promoted alternative aviation fuels in Brazil. These include (among others) ABRABA, Sustainable Aviation Biofuels for Brazil, and the Brazilian Biojetfuel Platform [12,49,58]. In addition to these initiatives, in 2011 the US and Brazil signed a Memorandum of Understanding to cooperate on the development of renewable aviation biofuels [52]. Also, an action plan was formulated by industry and research stakeholders in 2013 [59].

Brazil’s first commercial biojet fuel flight (HEFA) was performed on 24 Oct. 2013. In 2014, the Brazilian airline GOL made its first flight on a 10% blend of ASTM-certified SIP jet fuel [60]. Over 200 flights were made in 2014 using alternative jet fuel in Brazil.

A global aviation fuel supplier and an industrial partner providing conversion technology currently collaborate to produce an alternative jet fuel blend containing 10% farnesane fermented from Brazilian sugar cane [57]. The farnesene molecule is already produced at an initial commercial scale in Brotas in Brazil; it can deliver 40 kt of fuel per year. The plant mainly uses sugar cane, but the process can be applied to other feedstocks, in particular, cellulosic sugars from woody biomass and agricultural or forest residues [35].

For policies concerning sustainability of Brazilian biojet fuels, only the decree on agroecological zoning for palm oil and sugar cane, as well as the decree on working conditions in the sugar cane industry, concern biofuel production. No laws have been implemented on GHG targets or chain of custody requirements [52].

The main policies and actions required for Brazil, formulated by [61], are as follows: ‘(1) Establish the “drop-in” sites as far as possible downstream in the distribution chain without compromising fuel quality and technical certification requirements of aviation; (2) Establish legal mechanisms to ensure that incentives for aviation biofuels are only available where demonstrated to fully implement national laws and regulations, especially environmental and social safeguards, natural forest and other habitat protections, land use zoning and worker protections; (3) Observe closely and anticipate regulatory actions by ICAO in such a way to take advantage of international regulations to promote a jet biofuel industry in Brazil; (4) Establish a governmental long-term program for integrated use of biofuels in all transportation modes in the country, to neutralize the cost difference of producing a “drop-in” fuel versus a product for biofuel-adapted engines as is the case for road transportation’ [61].

13.2.6 Other Countries

A number of other countries have announced initiatives to stimulate the development of biojet fuel, or have in place sustainability requirements. These include Australia (Australian Initiative for Sustainable Aviation Fuels, (AISAF)), New Zealand, China, and Korea (emission trading schemes) [12,49,58]. Indonesia has introduced a biojet fuel mandate of 2% commencing in 2016, rising to 5% by 2025 [12].

Besides funding of research and development, several initiatives and targets formulated by the industry have been examined. However, the inclusion of aviation and biojet fuels into ETS, and crediting for biofuel mandates, remain the only direct policy measures.

13.3 Sustainability and Certification Issues

Sustainability certification is an additional relevant field for governmental policies. The current ongoing debate on adopted sustainability criteria for bioenergy in general, and biojet fuels specifically, with first hand experience with available certification schemes, is briefly described in the following section.

13.3.1 Sustainability Criteria for Biojet Fuels

Sustainable biojet fuel provision is one of the major prerequisites of bio-based jet fuels as land and biomass are limited resources. Much uncertainty has recently developed with regards to how biofuel policies in several key markets will evolve. The discussions are driven by sustainability issues, including concern that feedstock production for biofuels contributes to deforestation or uses land that could be used to grow food. This could impact production, trade, and use of biofuels [6,62]. Sustainability criteria and standards have to be met along the whole complex provision chain of biomass to energy, from cultivation and harvest/collection to conversion and use [69].

There is currently no dedicated indicator for biojet fuels, but a wide range of sustainability criteria and indicators for bioenergy is available, and could be applied to biojet fuels. The following are two approaches for the application of sustainability criteria in the bioenergy field: (1) The EU’s RED, and (2) The Global Bioenergy Partnership (GBEP).

When introducing the biofuels quota, the EU defined a set of sustainability indicators that needs to be fulfilled to get biofuels counted for the biofuels quota. So, biofuels and bioliquids produced in installations have to fulfill the following three indicators [51]:

• Conversion of natural habitats: Energy crops must not be produced on biodiversity-rich areas, carbon-rich areas, and peat lands;

• Sustainable agricultural production: Energy crop cultivation within the EU has to follow cross compliance requirements and maintain a good agricultural and environmental condition;

• GHG mitigation potential: The biofuels have to achieve GHG emission savings of at least 60% relative to fossil fuels, starting from 1 Jan. 2018.

Those indicators have to be verified by certification of the whole value chain. Different certification schemes have to be introduced to trace the value chains back to the biomass production and to provide the demanded information for each unit of biofuel (see next section). An issue that is often discussed in relation to biofuels in general is indirect land use change (ILUC). Within the EU in 2009 [51], a factor was proposed for indirect land use changes in the calculation of GHG emissions that uses concrete methodology to minimize those GHG emissions. Scientific work indicates that emissions from indirect land use change—emissions estimates are calculated through modelling, and remain sensitive to (and may vary according to) the modelling framework and assumptions made—can vary substantially between feedstocks, and can negate some or all of the GHG savings of individual biofuels relative to the fossil fuels they replace. The EU Commission was therefore of the ‘view that in the period after 2020 biofuels which do not lead to substantial GHG savings (when emissions from indirect land use change are included) and are produced from crops used for food and feed should not be subsidized’ [63]. In 2015, members of the European Parliament adopted an EU Council text that sets a new target regime to limit the amount of crop-generated biofuels used in the transport sector [64]. This includes, for example, a cap for first-generation biofuels, national targets for advanced biofuels, and reporting on ILUC.

Another approach was more holistic, taking not only environmental, but also economic and social factors, into consideration; it was developed under the GBEP in 2011 [65]. Those indicators refer more to national bodies and aim to monitor the development of different effects from bioenergy use over time. In the first round, GBEP proposed 24 indicators distributed over environmental, economic, and social principals (see Table 13.4). Those indicators are currently being tested in case studies.

Table 13.4

GBEP Indicators to Describe Sustainable Bioenergy Use

| Environmental | Social | Economic |

| Lifecycle GHG emissions (1) | Allocation and tenure of land for new bioenergy production (9) | Productivity (17) |

| Soil quality (2) | Price and supply of a national food basket (10) | Net energy balance (18) |

| Harvest levels of wood resources (3) | Change in income (11) | Gross added value (19) |

| Emissions of non-GHG air pollutants, including air toxics (4) | Jobs in the bioenergy sector (12) | Change in consumption of fossil fuels and traditional biomass (20) |

| Water use and efficiency (5) | Change in time spent by women and children for biomass collection (13) | Training and re-qualification of the workforce (21) |

| Water quality (6) | Bioenergy used to expand access to modern energy services (14) | Energy density (22) |

| Biological diversity in the landscape (7) | Change in mortality and burden disease attributed to indoor smoke (15) | Infrastructure and logistics for distribution of bioenergy (23) |

| Land use and land use change related to bioenergy feedstock production (8) | Incidence of occupational injury, illness, and fatalities (16) | Capacity and flexibility of use of bioenergy (24) |

Data from GBEP, The Global Bioenergy Partnership Sustainability Indicators for Bioenergy. Global Bioenergy Partnership (GBEP), Food and Agriculture Organization of the United Nations (FAO), Rome, 2011.

13.3.2 Certification Schemes and First Experiences from Practice

Besides a great variety of voluntary sustainability initiatives and standards (eg, ISO, CEN, and forest or biomass certification schemes), mandatory standards do apply on national/regional (eg, EU ETS, EU RED, US RFS, Brazil Agroecological zoning) and international levels (UN CBD convention). The implementation of the standards is ensured through third-party certification systems.

Three important voluntary standards and schemes are the following:

• Roundtable on Sustainable Biomaterials (RSB);

• International Sustainability and Carbon Certification (ISCC);

The ISCC and the RSB EU RED are the main voluntary certification schemes recognized under the European RED. The US RFS is a mandatory approach that also provides an effective incentive system based on tradable certificates (RINs) that are generated for each batch of biofuel [61].

Further voluntary schemes commonly used to certify agricultural, forestry, and waste feedstock are Biomass Biofuel Sustainability Voluntary Scheme (2BSvs), Bonsucro EU, and Roundtable on Sustainable Palm Oil (RSPO-RED) [52].

There are considerable differences between the standards in terms of the sustainability criteria. The applied methods for lifecycle analysis of GHG emissions are also not directly comparable to each other. Therefore, at the ICAO level (ie, 191 states), it will be challenging according to IATA [66] to ‘define a preferred set of sustainability criteria that have a chance to be accepted’ [35].

The certification itself is applicable. There is still a need to have international agreements or mutual recognition of different standards (EU RED and RFS2), and to develop a metastandard for aviation biofuels that was formulated by Refs [52,40].

When it comes to practical experiences, the RSB has already certified a biojet fuel supplier, and several aviation biofuel initiatives have recommended using RSB standards for their biofuel supplies. Also, feedstock supply for biojet fuel has already been RSB certified [61].

13.4 Conclusion and Outlook: What Is Necessary to Bring Biojet Fuels into the Markets

This chapter has assessed the main determining factors that shape the use of biofuels in commercial air transport. As stated, aviation is a global industry with global problems and challenges, and it demands global actions and solutions. Additionally, it is an industry for which an increase in fuel demand is expected. In answering those expectations, the IATA is committed to achieving carbon-neutral growth by 2020 and 50% reduction by 2050. To achieve those targets, biojet fuels are seen as one necessary element.

Some relevant preconditions of the market implementation of biojet fuels have been achieved during the last decade, especially the following:

• Demonstration of a wide range of biojet fuels that have been tested successfully;

• Definition of technical standards for drop-in biojet fuels, which are already fulfilled by three different biojet fuels (HEFA, F-T, and SIP);

• Establishment of sustainability assessment approaches and certification schemes for the biofuel sector, which can be implemented in the biojet fuel sector in principle;

• Multistakeholder groups around the world are already working together on initiatives for the deployment of biojet fuels. Some examples include CAAFI (US); Ubrabio (Brazil); Initiative Towards sustAinable Kerosene for Aviation, (mainly EU); aireg (Germany); Bioqueroseno (Spain); Bioport Holland (The Netherlands); Plan de Vuelo (Mexico); AISAF (Australia); NISA (Nordic countries); and BioFuelNet Canada [12].

On the other hand, there are many challenges to solve, and uncertainties to consider, before biojet fuels can be used in aviation on any significant scale, which can be summarized as follows:

• So far no mandatory international targets, international standards, or international certification schemes exist [40,52];

• Production costs remain the main stumbling block, and, even if they are expected to fall when more capacity is installed, additional governmental policy is necessary to make biojet fuels price-competitive by 2020–2030. Having the sustainability certification process being adapted to incorporate the use of biojet fuels is not expected to be an obstacle for its deployment in the medium term, though this will add additional costs;

• Mainly GHG savings, land conversion restrictions, and biodiversity and carbon stock protection are included in national legislation and voluntary schemes, whereas economic and social criteria and soil, air, and water protection are not (or only partially) included [35,52];

• Uncertainties on the achievable environmental effects of biojet fuel substitution are reported, concerning the no-carbon greenhouse effect of the air traffic and the GHG emissions of land use change caused by biojet fuel feedstock provision. Therefore, even in an advanced biojet fuel scenario, the aviation sector will continue to cause an increasing portion of greenhouse effects until 2050.

Government policies that bring biojet fuels to the market need to address different issues.

One key issue for delivering biofuels for the aviation sector is the development of an appropriate support mechanism. To achieve economies of scale and cost reduction for biojet fuel provision, a stable, long-term policy framework to build investor confidence and induce demand is necessary. This could be achieved, for example, by blending mandates, higher carbon taxes or penalties, taxation of fossil jet fuel, or by integration into international ETSs. In the past, the implementation of the EU ETS for biojet fuels did not succeed due to international competition issues. Those experiences clearly show that international agreements are a key factor. The best way might be to negotiate the frame condition for biojet fuel implementation within the international negotiation on GHG emission reduction.

Another key issue is the provision of sustainable biojet fuels. With the existing certification schemes in general, a sustainable production of biojet fuels under today’s definition of suitability can be certified. The next necessary step is to harmonize those schemes with regard to their applicability in the aviation sector. Additionally, it is necessary to also include the major concern of biomass availability. Therefore, biojet fuel policies need to be linked with other bioenergy application fields (biofuels for land transport, heat production from biomass, etc.) in order to make sure that restricted land is not promised to different applications in parallel. Such an overall bioenergy strategy is often missing on a country level, and also in the international debate. Additionally, GHG emission reduction from the use of biojet fuels is still discussed on a scientific basis and might change the picture in the future. Monitoring systems for bioenergy (with biojet fuels as part of them) need to be implemented internationally to make sure that the intended effects on GHG reduction occur, and leakage effects (such as direct and ILUC) are detected at early stages.

The third key issue is to provide long-term stable support for research and development in the different fields of biojet fuels, including: (1) improvements in costs and efficiency of biojet fuel production, logistics, and use; (2) further development of sustainability criteria and certification approaches; and (3) integration of biojet fuels in overall concepts of an efficient (and mainly based on) renewable energy supply in the future.

From an industry perspective, IATA [67] sees the role of government as especially important in helping to:

• Adopt globally recognized sustainability standards and work proactively to harmonize global standards;

• Allow biojet fuel to compete on an equal basis with land transport-based fuels through equivalent public incentives (ie, ‘level the playing field’);

• Encourage user-friendly biofuel accounting methods, and work to proactively harmonize global standards;

• Support biojet R&D and demonstration plants;

• Design effective policy to de-risk investments into biojet production plants;

• Engage in public-private partnerships for biojet fuel production and supply;

• Pursue a harmonized transport and energy policy;

• Commit to policy certainty, or at a minimum, policy timeframes that match investment timeframes.

Ref. [12].