Chapter 24

HYBRID SECURITIES

It's a kind of magic

Before we begin the study of these different products, we caution the reader to bear in mind the following points:

- Some types of securities offer a lower interest rate in exchange for other advantages to the holder, and therefore give the impression of lowering the cost of financing to the company. It is an error to think this way. In markets in equilibrium, all sources of financing have the same cost if one adjusts for the risk borne by the investor.

- To know whether a source of financing is cheap or dear, one must look past the apparent cost to the overall valuation of the financing. Only if securities have been issued at prices higher than market value can one say that the cost of financing is indeed lower.

- With the exception of products that exactly match a particular market demand, sophisticated hybrid securities are costly to issue and sell. As such, they are a signal to investors that the company, or its majority shareholder, is having trouble attracting investors, perhaps because it is experiencing other difficulties.

- By emphasising the fundamental asymmetry of information between issuer and investor, agency theory and signalling theory are both very useful for explaining the appeal of products of this kind.

- Lastly, it must not be forgotten that corporate finance is not immune to fashion. Investors have a great appetite for novelty, especially if it gives them the feeling of doing high finance!

Section 24.1 WARRANTS

1/ DEFINITION

A warrant is a security that allows the holder to subscribe to another newly issued security (share, bond or even another warrant) during a given period, in a proportion and at a price fixed in advance.

Subscription warrants may be attached to an issue of shares or bonds, in which case the issue is said to be one of “shares cum warrants” or “bonds cum warrants” or “convertible bonds cum warrants”. Attached warrants to buy shares may be called an “equity sweetener” or “equity kicker”. Warrants can also be issued and distributed to existing shareholders at no charge. Once securities with attached warrants have been issued, the whole is split into its two component parts: the shares or bonds become traditional securities and the warrants take on a life of their own. The warrants are traded separately after issue.

As an illustration, Marlin issued free equity subscription. A warrant allowed the holder to subscribe to one Marlin share at NZ$1.28 on 20 May 2022. In June 2021 the Marlin warrants were trading at NZ$0.24, whereas Marlin shares were trading at NZ$1.45.

As liquidity in the stock and bond markets has increased, financial institutions have taken the opportunity to issue warrants on existing securities independently of the company that issued the underlying shares. These securities are also called covered warrants because the issuing institution covers itself by buying the underlying securities on the market.

Warrants ordinarily involve a transaction between one investor and another and therefore play no direct role in financing a business. There being no limits to the imagination, some players have not hesitated in creating warrants on baskets of existing securities (such as indices). Thus, a warrant on a basket of different shares gives one the right to acquire, during a given period of time, a lot consisting of those shares, in proportions and at an overall price fixed in advance.

2/ VALUE

Conceptually, a warrant is similar to a call option sold by a company on shares in issue or to be issued. The exercise price of this option is the price at which the holder of the warrant can acquire the underlying security; the expiry date of the option is the same as the expiry date of the warrant.

A warrant, however, has a few particular characteristics that must be taken into account in its valuation:

- It normally has a long life (typically two to three years but sometimes much more, six years for Prologue), which increases its time value and makes it more difficult to accept the assumption of constancy in interest rates and volatility used in the Black–Scholes model.

- The underlying asset is more likely to pay a periodic return during the time the warrant is held:

- For an equity warrant, the payment of dividends on the underlying share lowers the value of that share and thereby reduces the value of the warrant. More generally, any transaction that changes the value of the share affects the value of the warrant.

- For a debt warrant, the price of the underlying bond varies over time and, as we saw in Chapter 20, the closer a bond comes to maturity, the more its market price tends towards its redemption price. Its volatility gradually declines, making the Black–Scholes model, which assumes constant volatility, inapplicable as stated.

- Lastly, in the case of subscription warrants, the dilution associated with exercise of the warrants entails a gradual change in the value of the underlying security. When investors exercise warrants, the number of outstanding shares increases and the issuing firm receives the strike price as a cash inflow. When investors exercise call options, no change in outstanding shares occurs as call options are options on shares that already exist and not on new shares to be issued; hence, the firm receives no cash.

To get round these difficulties, traders use models derived from the binomial and Black–Scholes models, taking into account the fact that the exercise of warrants can create more shares and thus affect the stock price.

3/ THEORETICAL ANALYSIS

Agency theory offers an almost “psychological” approach to these securities. They are seen as a preferred means of resolving conflicts between shareholders, lenders and managers.

Take a bond with attached equity warrant as an example. A hybrid security of this kind may seem unnatural since it combines a low-risk asset (bond) with a high-risk asset (share).

However, there is something in it for each of the parties.

The company's managers benefit from the flexibility that warrants provide, since the company can set bounds on the date of the capital increase (by setting the subscription period of the warrant) and the amount of funds that will be raised (by setting the exercise price and the number of warrants per bond at appropriate levels). The amount of funds raised in the form of bonds can be completely different from the amount potentially raised later in the form of shares. Furthermore, the company may be able to use the funds from both sources for several years, since the warrants may be exercised before the bonds are paid off.

A company that wants to accomplish the capital increase part of the issue quickly will set an exercise price barely above, or even below, the current price of the share. If it chooses, it can also move up the beginning of the subscription period. If it prefers to bring in a greater amount of funds, it will increase the number of warrants per bond (which must then have a lower yield to maturity if equilibrium is to be maintained) and potentially raise the exercise price of the warrants.

Because it entails selling an option, though, the opportunity cost of a warrant can be substantial. Take the case of a company that has sold for €10 the right to buy one share at €100. Suppose that at the time this warrant becomes exercisable the shares are trading at €210. A straight capital increase without a rights issue at a very slight discount to the share price would bring in, say, €205 per share, whereas exercise of the warrants will bring in €110 per share all told. The opportunity cost is €95 per share.

Stock market history has shown that exercise of warrants can never be taken for granted. After the steep decline in stock markets in 2007/2009, firms that issued warrants before this period have a very low probability of being able to raise equity thanks to these warrants.

The holders of bonds with attached equity warrants, if they keep both securities, are both creditors and potential shareholders. As creditors, they benefit from a small but relatively certain yield; as potential shareholders, they have hopes of realising a capital gain.

In a context of rising interest rates and falling share prices, however, holders of bonds cum warrants suffer the downside risks of both debt and equity securities, instead of combining their advantages.

On the other hand, the holders of the bonds may be different from the holders of the warrants. The bonds may end up with investors preferring a fixed-rate security, while the warrants go to investors seeking a more volatile security.

In appearance only, existing shareholders retain their proportionate equity stake in the company. The warrant mechanism makes for gradual dilution over time. An issue of bonds with equity warrants allows existing shareholders to maintain their control over the company with a smaller outlay of funds, since they can buy the warrants and resell the bonds. If they do this, the securities they end up holding will be much riskier overall because the bonds will no longer be there to cushion fluctuations in the value of the warrants.

The dilution problem is postponed. When the warrants are exercised, they may have risen in value to such an extent that existing shareholders can pay for virtually all of their proportionate share of the capital increase by selling their warrants in order to finance their share subscription.

4/ PRACTICAL USES

Warrants are increasingly widely used in corporate finance:

- By a company in difficulty that wants to raise fresh capital. Before going ahead with a capital increase, the company decides to make a bonus distribution of warrants to existing shareholders. In practice, the shareholders are giving themselves these warrants. They can then speculate more readily on the company's turnaround. This was the case for CGG in 2018.

- When creditors are cancelling debts due to them, shareholders may give them equity warrants in return. The value of these warrants is virtually nil at the start, but if the company regains its footing, the warrants will rise in value and make up for some or all of the loss on the cancelled debts. A deal of this kind is the way to reconcile the normally divergent interests of creditors and shareholders. In modern finance, this technique replaces the “return to better fortune” clause in loan agreements.

- In a tender offer for shares of company A in exchange for shares of company B, shareholders of A may be offered not only shares of B but also warrants for shares of B.

- In a leveraged buyout (LBO, see Chapter 47), warrants may be used to offer an additional reward to holders of mezzanine debt or even to management (another instance of an “equity kicker”).

- As a management-incentivisation tool, warrants can be used as an alternative to stock options or performance shares. The key difference lies in the fact that warrants have to be acquired by management (whereas stock options or performance shares are distributed free of charge).

5/ REDEEMABLE WARRANTS

Redeemable warrants are warrants that can be redeemed by the issuer. The company can redeem, at nominal price, the warrants in case the share price exceeds a certain threshold. In practice this means that the company can force the exercise of the warrants after a certain time if conversion conditions are met, as the redeemable warrant holder will prefer exercising rather than being redeemed at nominal price.

This is equivalent to a “soft call” clause in a convertible bond contract (see below).

This product is usually tied to a bond and issued by mid-sized companies to refinance bank loans. Some groups issued bonds cum redeemable warrants subscribed by banks that kept the bonds and sold the warrants to the management, thus partially replicating the management packages of LBOs.

Section 24.2 CONVERTIBLE BONDS

1/ DEFINITION

A convertible bond is like a traditional bond except that it also gives the holder the right to exchange it for one or more shares of the issuing company during a conversion period set in advance.

Source: Data from Dealogic

As an example, in April 2021 the medtech Predilife issued a convertible bond with the following characteristics:

The conversion period is specified in the bond indenture or issue contract. It may begin on the issue date or later. It may run to the maturity date, or a decision may be forced if the company calls the bonds before maturity, in which case investors must choose between converting them into shares or seeing them being redeemed in cash.

The bond may be convertible into one or more shares (612.5 shares for each bond in our example). This ratio, called the conversion ratio,1 is set at the time of issue. The conversion ratio is adjusted for any equity issues or large buy-backs above market price, mergers, asset distributions or distributions of bonus shares in order to preserve the rights of holders of the convertibles as if they were shareholders at the time of issue.

The conversion premium is the amount by which the conversion price exceeds the current market price of the share. A conversion premium is typical. In our Predilife example, the conversion premium is 38%.2 Since Predilife offered no redemption premium, its shares must rise 38% by the maturity date of the bonds for investors to be willing to convert their bonds into shares rather than redeem them for cash. The calculation is slightly different when a redemption premium is involved.

Some convertible bonds are issued with a call provision that allows the issuer to buy them back at a predetermined price. Holders must then choose between redeeming for cash or converting into shares. The indenture may provide for a minimum period of time during which the call provision may not be exercised (“hard non-call” period, usually at least one year) and/or set a condition for exercising the call provision, such that the share price exceeds the conversion price by more than a percentage, most of the time 30%, for more than 10 days (“soft call” provision). The Predilife convertible bond does not have a soft call provision.

In some cases, the issuer may, upon conversion at the holder's request, provide either newly issued shares or existing shares held in portfolio – for example, following a share buy-back, as is the case for the Predilife bond issuance. In other cases, the issuer has the right to provide the counter value in cash of the shares that were to be given for repayment. This makes it possible to limit the dilution of current shareholders.

As with other debt instruments, convertible bonds can be green if the proceeds are used for energy transition investments (Neoen, EDF), or sustainable (Schneider), if the return paid to investors is increased in case certain ESG objectives are not met (energy consumption, CO2 emissions, increasing gender diversity, etc.).

Convertible bonds must not be confused with the similar-sounding exchangeable bonds, which are pure debt securities from the point of view of investors. We are going to study them in Section 24.4.

2/ VALUE

The value of a convertible bond during its life is the sum of two components:

Convertible bond = bond value + call option

- The value of the straight bond alone is called the bond value of the convertible bond. It is calculated by discounting the future cash flows on the bond at the market interest rate, assuming no conversion. The bond value thus represents a minimum value: the convertible will never be worth less than this floor value, even if the share price falls significantly. It also cushions the impact of a falling share price on the price of the convertible. Bear in mind, though, that investment value is not a fixed number but one that varies as a function of changes in interest rates.

- The option value. To the bond value is added the value of the conversion option. The higher the share value exceeds the redemption price of the convertible bond, the higher the value of the conversion option, and the lower the share value falls below the redemption price of the convertible bond, the lower the value of the conversion option.

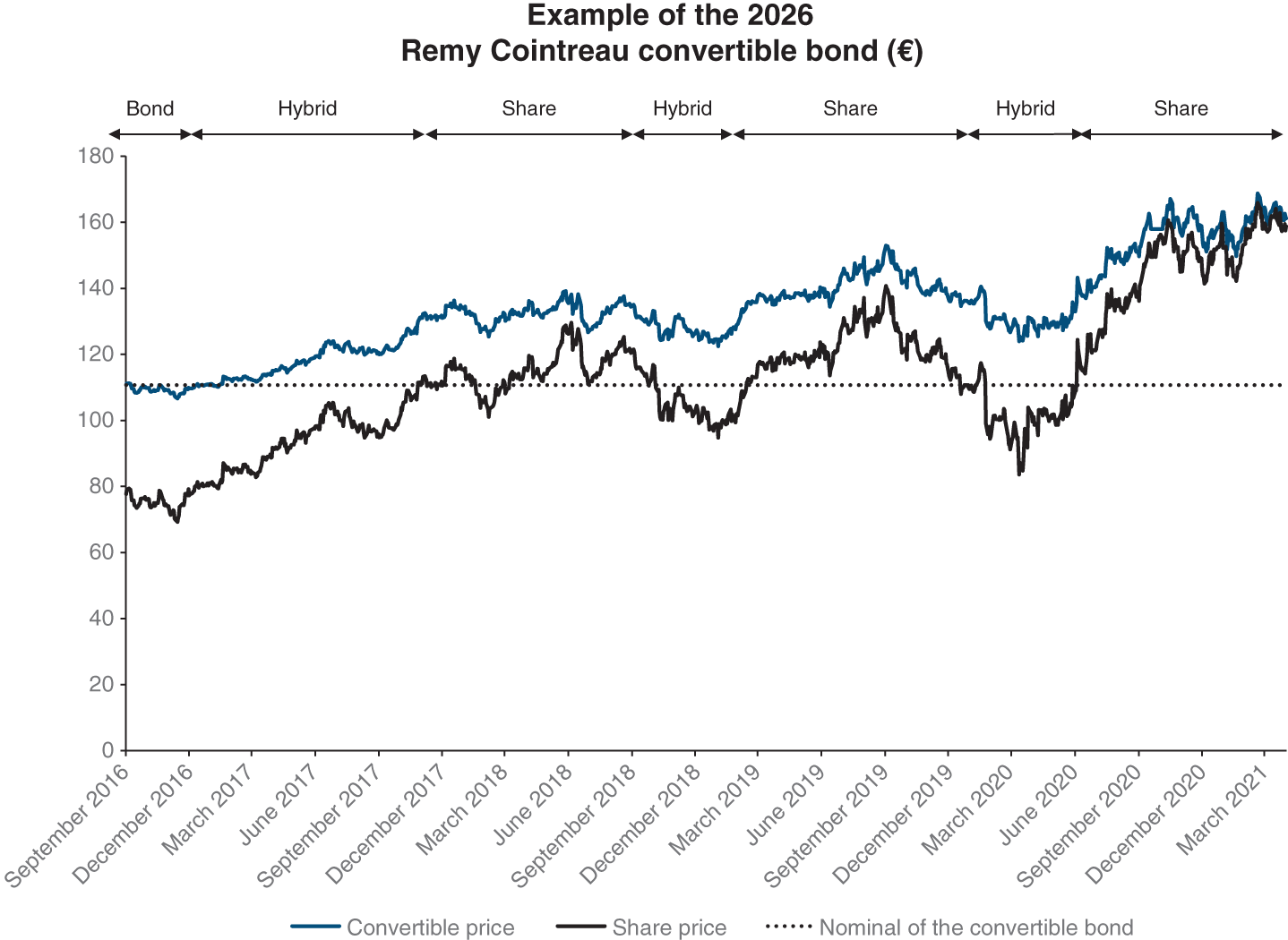

Whenever the share price is well above the redemption value of the convertible bond – as in the “share” zone of the following chart for Rémy Cointreau in summer 2020 – the convertible bond behaves more and more like the share because the probability that it will be converted into shares is very high.

In the “bond” zone, the convertible bond behaves essentially like a bond because, given the level and trend of the share price, the probability of conversion is low. The price of the convertible bond is close to its investment value. This was the case for the Rémy Cointreau convertible bond in the months following its issue in the autumn of 2016.

In the “hybrid” zone, the value of the convertible reflects the simultaneous influence of both the level of interest rates and the price of the underlying security, as for the Rémy Cointreau convertible bond in spring 2020.

There can also be a high-risk zone for the convertible bond if the share price has fallen sharply. Heavy doubts appear as to the company's ability to repay its debts. The price of the convertible bond adjusts downwards accordingly, until it offers a yield to maturity consistent with the risk of default by the issuer.

Source: Data from Bloomberg

At issue, the bond value most often represents 85–95% of the value of the convertible bond and the call option 5–15%. The lower the conversion premium, the closer the convertible bond will be to a share since conversion into shares will be very likely. The coupon of the convertible bond may therefore be low. Conversely, the higher the conversion premium, the closer the convertible bond will be to a bond requiring a higher yield. By balancing these characteristics of the convertible bond, the CFO will be able to tailor the convertible bond to the cash flow profile of the company and the dilution appetite of its shareholders.

3/ SYNTHETIC BONDS

In the mid-2010s, peculiar convertible bond issues were implemented with the following principle: the firm issues convertible bonds to investors and acquires call options at the same time (from one or several banks) that mirror the options imbedded in the convertible bonds. The convertible bonds and options have the specificity of offering only a cash settlement (the counter value in cash of the shares being paid in case the option is exercised). For the firm, the bundling of the issuance of a convertible bond and the acquisition of a call replicates the cash flows of a plain vanilla bond exactly. For the company, it is the same as issuing a plain vanilla bond.

This product can be attractive when market appetite for convertible bonds is high. There may then be a true arbitrage opportunity that allows the firm to sell the call option to investors at a higher price than the price it paid the banks. In this case, the yield of the instrument, called an Equity Neutral Convertible Bond (ENCB), will come out as lower than that of a traditional bond. This combination can also be used for firms that do not have access to the bond market.

Companies that have issued synthetic bonds include LVMH, National Grid, Total, Iberdrola, Michelin, and HDFC, amongst others.

4/ THEORETICAL ANALYSIS

Unlike a bond with attached equity warrants, a convertible bond is an indivisible product. The straight bond cannot be sold separately from the call option.

For the investor, the convertible bond is often presented as a miracle product, with downside protection by virtue of its debt component and upside potential by virtue of its equity component.

In much the same fashion, the convertible bond is pitched to issuers as the panacea of corporate finance. Initially, it enables the company to issue debt at an interest rate lower than the normal market rate; at a later point, it may enable the company to issue fresh equity at a price higher than the current share price.

No! There are no miracles in finance. At best, one can find mirages, and this is one. If the company is able to issue bonds at an interest rate below its normal cost of debt, it is because it has agreed to issue shares in the future at a price below the share value at that time – necessarily below, or conversion would not take place. Current shareholders will therefore be diluted on poor terms for them. In addition, the argument of a lower rate is true only in terms of cash, as under IFRS the current interest rate at which the company could issue an ordinary bond must be applied when recording associated interest expenses in the P&L, even if it actually pays a lower interest rate on its convertible bonds.

Similarly, if investors are getting a call option on the share, it is because in return they accept a lower rate of return on the bond than the issuer-specific risk would justify.

The apparent cost of the convertible bond is low only because its true cost is partly hidden. The company is selling investors call options, which they pay for by accepting a lower interest rate on the bonds than the company could normally obtain given its risk.

The cost of a convertible bond may be calculated in intuitive fashion as a weighted average of the cost of equity and the cost of debt. The weighting corresponds to the probability that the convertible will actually be converted. This probability is not hard to estimate if one assumes that returns on the share are normally distributed (then the expected yearly increase in share price is equal to the cost of equity less the dividend yield).

Equilibrium market theory is not of much help in explaining why convertible bonds, which are no more than a combination of two existing products, should themselves exist. Agency theory and signalling theory – together with the “matching hypothesis” – are far more useful in understanding the usefulness of convertibles.

- According to agency theory, a convertible bond is a mode of resolving conflicts between shareholders and creditors. Managers of leveraged companies can be tempted to undertake risky investments that increase shareholder wealth at the creditors' expense. With this fear in mind, creditors refuse to finance the company except via convertible bonds. Creditors will then have some protection, since the convertible gives them the option of becoming shareholders if there are transfers of value working against them as creditors. A heavily indebted company may have to pass up highly profitable investment projects if it cannot obtain bank financing that would not put too great a strain on its cash flow at the start. With its low apparent interest cost, the convertible bond is an attractive alternative. A convertible bond also helps in resolving conflicts between shareholder-managers and outside shareholders. Shareholder-managers of a company with convertible bonds outstanding will hesitate to divert company resources to private use at the expense of other shareholders, since they know that would increase the probability of having to redeem the convertibles in cash. If the company is already carrying a sufficiently high debt load, redemption could put it in difficulty and threaten the managers' position, so they are deterred from taking such action.

- The matching hypothesis provides another contribution to the explanation of why convertible bonds exist. A young, fast-growing company or one with limited financial resources will avoid taking on too much debt, as its cash flow is likely to be highly variable and its cost of debt, given its short history, likewise high. In these cases, it makes sense to issue securities whose cash flows match those of the firm.

- A fast-growing company will have little inclination to issue more shares, either because it believes its shares are undervalued or because it fears sending out a negative signal (see Chapter 38). That leaves only convertible bonds. Investors, relieved that the signal associated with a capital increase has not been sent, will welcome an issue of convertibles (e.g. Voltalia). This is what the signalling theory assumes.

Taken together, these three explanations provide good reasons for issues of convertible bonds by smaller companies that are growing rapidly, are already heavily indebted or have assets that are quite risky. We could also add another explanation, which is commonly known as the “backdoor equity” hypothesis. Young, growing firms cannot usually issue debt because of the high financial distress costs. At the same time, they may be unwilling to issue equity if current stock prices are too low. Thus, convertible bonds could offer a good compromise solution. Convertible bonds cause expensive dilution, but it occurs when the firm can afford it!

The market for convertibles is also supplied by large groups (e.g. Safran, Schneider), which use it to raise funds from specialised investors that invest only in convertible bonds. For these large groups, convertibles offer a way of diversifying the investor base and raising money in large quantities more easily. Lastly, groups in financial difficulty will resort to issuing convertibles when the equity market is closed to them (Just Eat).

Section 24.3 PREFERENCE SHARES

The securities called preference shares (a term prevailing in the UK) or preferred shares (a term prevailing in the US) enjoy economic advantages over ordinary shares, typically in return for a total or partial absence of voting rights.

1/ DEFINITION

Preference shares are created on the occasion of a capital increase by the decision of the shareholders at an (extraordinary where applicable) general meeting.

The advantages conferred on preference shares may include:

- a claim to a higher proportion of earnings than is paid out on other shares;

- priority in dividend distributions, meaning the dividend on preference shares must be paid before any ordinary dividend is paid on other shares;

- a cumulative dividend, so that if earnings are insufficient to pay the preference dividend in full, then the amount not distributed becomes payable from future earnings;

- a firm cannot go into default if it misses paying some dividends;

- rating agencies and financial analysts consider preference shares a part of equity (thus improving the rating of the company).

At the same time, there are two important disadvantages in issuing preference shares.

- for the issuer – because it adds a layer of complexity; and

- for the investors – because they may have limited voting rights, although in private companies they may have multiple voting rights.

We should note here that the term “preferred securities” (often shortened to just “preferreds”) is much broader in scope and may encompass convertible bonds and subordinated debt securities as well as preference shares without voting rights. The reader is advised to look closely at the detailed characteristics of any security called a “preferred” and not to assume that it is necessarily a preference share.

Special features can be added to preference shares to make them more attractive to investors or less risky to issuers:

- adjustable-rate preference share: the dividend rate is pegged to an index rate, such as a Treasury bill or Treasury bond;

- participating preference share: the dividend is divided into a fixed and a variable component. The latter is generally set as a function of earnings;

- trust preference share: the dividend on these stocks is tax-deductible like interest expenses. Firms issuing this security get the tax shield of debt and keep leverage low (because preference shares are treated like equity by analysts and rating agencies).

2/ VALUE

It is complex to generalise the valuation formula of preference shares as the term covers products that can have very different features. Preference shares will normally be valued just like ordinary shares (taking into account the potential higher dividend stream). The value of the preference share will be equal to the value of the ordinary share to which you need to:

- add the value of the advantages granted;

- deduct a liquidity discount for public companies (as the preference share will generally have low liquidity). This discount is almost always observed in trading prices;

- potentially deduct the value of the voting right.

As each of these elements is difficult to assess, the value of the preference share will be quite uncertain.

3/ THEORETICAL ANALYSIS

(a) For the company

Preference shares can enable a company, which is in difficulty but has a good chance of recovering, to attract investors by granting them special advantages.

Banks are often issuers of preference shares because these securities are classified by central banks as part of the bank's own funds for the purpose of determining its net capital. This is so even though the preference share pays a constant annual dividend expressed as a percentage of par value, which gives it a strong resemblance to a debt security. Analysts are not fooled; for their purpose, preference shares are reclassified as debt.

Against these advantages, preference shares also present several drawbacks:

- They cost more than a traditional capital increase: the preference dividend is higher than the ordinary dividend, whereas the preference share itself is usually worth less than the ordinary share because of its lesser liquidity.

- Their issuance entails complications that are avoided with an ordinary capital increase, such as calling a special shareholders' meeting.

- Furthermore, understanding such issues can be quite difficult. Preference shares frequently trade at a steep discount to theoretical value because holders demand a big premium over market value before they will sell or exchange them.

(b) For current shareholders

For a majority shareholder, issuing preference shares makes sense only if those shares have no voting rights. When this is true, a capital increase can be accomplished without diluting their control of the company. A company with family shareholders may issue preference shares in order to attract outside financial investors without putting the family's power over the company in jeopardy. For the minority shareholder, this seems to us to be a second-best solution: the only way to strengthen shareholders' equity when the majority shareholder does not want to follow a capital increase or be diluted. It is just as if the company's cost of capital had been raised.

The flexibility offered by preference shares is undoubtedly of interest to unlisted companies. Indeed, they make it possible to organise corporate governance between the shareholders involved in management and the financial shareholders. We can therefore see them flourish in private equity (to finance start-up, development, transmission or the acquisition of a company), and in particular LBOs. Today, issuances of new preference shares have virtually disappeared from stock markets, which prefers a single line of listing per company with a large volume of transactions and equality of shareholders. Intesa Sanpaolo thus imposed the merger of its two types of shares in 2018.

Section 24.4 OTHER HYBRID SECURITIES

1/ HYBRID BONDS

Also called deeply subordinated bonds, or simply hybrids, they present the following features:

- Very long maturity (more than 50 years) or no duration (i.e. perpetual). Some hybrids include a hard non-call provision prohibiting the firm from redeeming the issue before a certain date. Generally the interest rate increases in time (step-up), which encourages the firm to redeem the bonds as the price becomes prohibitive (but there is no legal requirement to do so).

- Ranking: in case of liquidation, the securities must rank senior only to share capital.

- Conditional payment of interest: under certain conditions, such as non-payment of dividends to shareholders, payment of the coupon/dividend to investors must be left at the issuer's entire discretion. In certain cases, the non-payment must be compulsory if some debt ratios are not satisfied.

- No voting rights is attached.

- The issuer may commit to redeeming the issue only by issuing equity or a similar hybrid instrument.

- Depending on the exact features, some issues may be classified as equity under IFRS as there is no commitment to redeem and as payment of interest may be suspended. Nevertheless, IASB is considering changing its stance on this subject.

Conceptually, these are nothing other than very long-term debt securities, whose extremely subordinated nature could lead to them being assimilated, from an accounting point of view, to equity, which in our view is wrong.

Rating agencies adopt a hybrid treatment by restating these issues in one part debt and one part equity (the equity content). So, for example, Moody's carries out a precise analysis of the terms and conditions of the issue (in accordance with a pre-established table) and classifies the issue in a basket (B, C or D) to which is attached an equity content (25%, 50% or 75%) for investment grade firms. Issues made by non-investment grade issuers are considered as 100% debt by Moody's.

Industrial groups use hybrid bonds either to diversify their investor base (Orange, Engie which issued a green hybrid) or to secure their rating and strengthen their capital structure (Arkema, Unibail-Rodamco-Westfield, Abertis).

2/ MANDATORY CONVERTIBLES

Unlike convertible bonds, for which there is always some risk of non-conversion, mandatory convertibles are necessarily transformed into equity capital (unless the issuing company goes bankrupt in the meantime) since the issuer redeems them by delivering shares; no cash changes hands at redemption.

The value of a bond redeemable in shares is the present value of the interest payments on it plus the present value of the shares received upon redemption. In pure theory, this is equal to the value of the share increased by the present value of the interest and decreased by the present value of the dividends that will be paid before redemption. The discount rate for the interest is the required rate of return on a risky debt security, while the discount rate for the dividends is the company's cost of equity.

Under IFRS, their issue value is broken down between the present value of interest shown as debt and the balance in shareholders' equity.

Mandatory convertibles are not a very attractive product on the financial markets (there is no suspense, unlike the convertible bond!), so it is not very common there. Rather, it is used in very specific arrangements for unlisted companies, often with tax or legal concerns. In 2020, ArcelorMittal issued a mandatory convertible for which the conversion parity was linked to the share price. This issue has allowed to differ the dilution of the Mittal family in the capital.

For tax purposes, bonds redeemable in shares are treated as bonds until they are redeemed, and subsequently as shares.

They have been issued by a number of companies, large and small, to raise capital, including Texas Instruments, General Motors, Citicorp, Lafarge, AXA and Sears.

3/ EXCHANGEABLE BONDS

An exchangeable bond is a bond issued by one company that is redeemable in the shares of a second company in which the first company holds an equity interest. Thus, while a convertible bond can be exchanged for specified amounts of common stock in the issuing firm, an exchangeable bond is an issue that can be exchanged for the common stock of a company other than the issuer of the bond.

At maturity, two cases are possible. If the price of the underlying shares has risen sufficiently, then holders will exchange their bonds for the shares; the liability associated with the bonds will disappear from the issuer's balance sheet, as well as the underlying shares. If the price has not risen enough, then holders will redeem their bonds for cash and the issuer will still have the underlying shares. In neither case will there be any contribution of equity capital. An exchangeable bond is therefore like a collateralised loan with a call option for the holder on securities held in the company's portfolio.

For the investor, a bond issued by company X that is exchangeable for shares of company Y is very close to a convertible bond issued by Y. The only thing separating these two financial instruments is the default risk of X versus that of Y.

By way of example, in February 2021 Bigben issued a bond exchangeable for shares in Nacon (for a total of 10.67% of Nacon). Bonds are exchangeable with shares with a premium of 16% for five years. This issue raised €87m for the group at an apparent interest rate of 1.70%. The quid pro quo is obviously twofold: for one thing, Bigben cannot be sure of having unloaded a part of its holding in Nacon; for another, if it does succeed in disposing of that stake, it will have let it go at a price below its market value. But on the face of it, Bigben has obtained long-term financing with a low interest rate.

For the investor, a bond issued by Bigben that is exchangeable for Nacon shares and a convertible bond issued by Nacon are very similar financial instruments; only the risk of default differentiates them (Bigben or Nacon).