OVERVIEW

Owners' equity of a corporation is called shareholders' equity because a corporation's owners hold shares as evidence of their ownership claims. Shareholders' equity typically consists of two major categories of corporate capital: contributed capital (share capital and contributed surplus) and earned capital (retained earnings and, under IFRS, accumulated other comprehensive income).

“Earnings” refers to net income for a period, whereas “retained earnings” refers to accumulated earnings retained for use in the business since inception of the corporation. Specifically, retained earnings is the total of all amounts reported as net income, less the total of all amounts reported as net loss and dividends declared, plus or minus the effects of any prior period adjustments (error corrections) through retained earnings, adjustments due to financial reorganization, and treasury share transactions, since inception of the corporation. A dividend distribution may represent a distribution of income (return on capital) or a return of invested capital. A corporation may distribute dividends to its owners in the form of cash, non-cash assets, or additional shares. A dividend paid in the form of additional shares of the corporation results in capitalization of retained earnings or reclassification of earned capital to contributed capital (reclassification of retained earnings to share capital).

This chapter also discusses accounting for transactions related to share capital, including issuance, reacquisition, retirement, and cancellation of shares.

Understanding the Nature and Purpose of Equity

Resources (assets) of a company are financed either by the company's internal operations or by debt or equity. Debt holders and shareholders each have different rights and claims on the company. Debt holders usually have more rights. For example, debt holders have preferential treatment with respect to return on their investment (interest) after a specified period of time, or on liquidation of the company.

All forms of debt and equity financing fit somewhere on a spectrum ranging from lower risk of loss with no risks and rewards of ownership (secured debt), to highest risk of loss with risks and rewards of ownership (common shares). Common shares are considered residual in nature because common shareholders get whatever is left after other claims on the company have been settled. (They are not guaranteed annual dividends or any return of capital if the corporation is dissolved.) However, common shareholders have voting rights (along with the ability to control management through these rights), and tend to profit most if the company is successful. Therefore, common shareholders have the highest risk of loss (of return on capital as well as return of capital), along with risks and rewards of ownership (voting rights and participation in the company's earnings/losses and appreciation/depreciation).

Preferred shares fit somewhere in between debt and equity, and have characteristics of both. Shares that have a fixed term or are retractable at the option of the preferred shareholder are considered more debt-like. Preferred shares that are convertible to common shares or are participating (in profit distributions that are higher than the prescribed rate of the preferred share) are considered more equity-like.

Shareholders' equity typically consists of two major categories of capital: contributed capital (share capital and contributed surplus), and earned capital (retained earnings and, under IFRS, accumulated other comprehensive income). Contributed capital consists of amounts invested by shareholders and amounts contributed to the company as a result of certain shareholder transactions. Earned capital is the cumulative amount earned by the company itself through net income and, under IFRS, other comprehensive income.

Understanding the Nature of Issuance and Reacquisition of Equity

Issuance of shares

In a share issuance, the net amount that is received by the corporation (the net amount that is received, after payment of direct incremental costs and fees, such as underwriting costs, and accounting and legal fees) is credited to the appropriate share capital account. Thus, the book value of share capital includes the amounts invested by shareholders, net of the direct incremental costs and fees of issuing the related share capital.

When shares are sold on a subscription basis, the full price of the shares is not received immediately, and may result in defaulted subscription accounts. Resolution of defaulted subscription accounts is determined by the subscription contract, corporate policy, and any applicable law of the jurisdiction of the corporation.

Reacquisition of shares

A corporation may buy back (reacquire or repurchase) some or all of its own outstanding shares. When this happens, it is likely that the repurchase price paid by the corporation will be different from the amount that was received by the corporation when the shares were originally issued. ASPE provides specific guidance for this scenario, and for accounting for the reacquisition of shares. Under IFRS, no explicit guidance is given for accounting for the reacquisition of shares, although the accounting may end up the same as it would under ASPE, using basic principles.

Understanding the Nature of Distributions of Equity

Contributed capital versus earned capital

Contributed capital consists of share capital and contributed surplus, whereas earned capital consists of retained earnings and, under IFRS, accumulated other comprehensive income. Retained earnings is an earned surplus (of cumulative net income earned by the company but not yet distributed to shareholders). On the other hand, contributed surplus is not an earned surplus, because it is the result of certain shareholder transactions, such as par value share issues. As such, contributed surplus is not connected with the company's operations or earnings process.

Both retained earnings and contributed surplus are forms of surplus in the company. However, one is earned and the other is contributed. The distinction between retained earnings and contributed surplus may not always be clear, and may require professional judgement.

Dividends

Dividends are charged against retained earnings, and effectively represent distribution of the company's profits to its shareholders.

There are legal restrictions on dividend amounts. In general, a dividend should not be declared or paid if there are reasonable grounds for believing that the corporation is (or would be after payment of the dividend) unable to pay its liabilities as they become due, or if the realizable value of the corporation's assets would, as a result of the dividend, be less than its total liabilities and stated or legal capital for all classes of shares. Often there are other major reasons for restricting the dividend amount, including debt covenants and alternative uses for cash, such as financing of company growth or expansion.

Legal restrictions on dividend amounts need not be separately disclosed because it is presumed that legal restrictions are public knowledge. However, other restrictions on dividend amounts should be disclosed since this information is relevant to financial statement users.

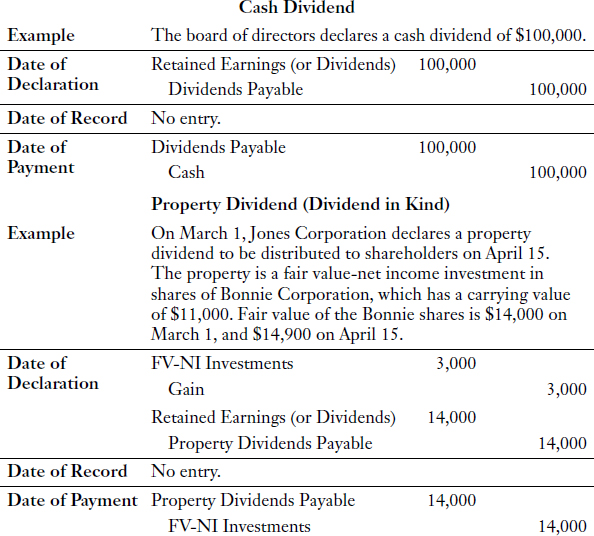

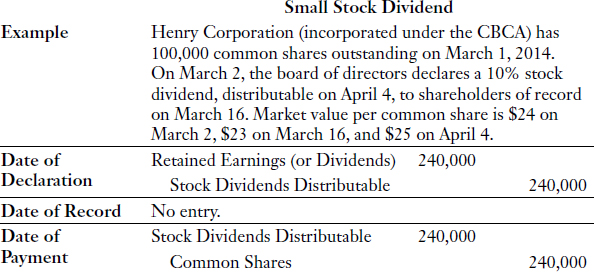

Usually dividends are paid in cash; however, sometimes they are paid in the form of property or stock. A dividend paid in the form of property is called a dividend in kind and is generally valued at the fair value of the property given up, unless the transaction is considered a spinoff, restructuring, or liquidation, in which case the dividend is valued at the carrying value of the property given up. A dividend paid in the form of shares is called a stock dividend and is generally valued at the market value of the shares given up. A stock dividend usually results in capitalization of earnings (reclassification of retained earnings to share capital).

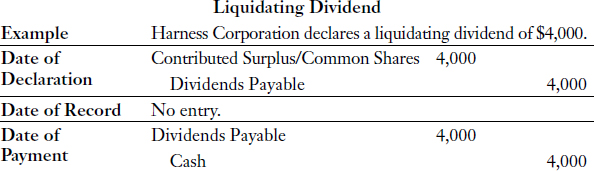

Liquidating dividends represent a return of contributed capital or return of capital to shareholders, and thus are usually charged against contributed surplus, rather than retained earnings.

Stock dividends versus stock splits

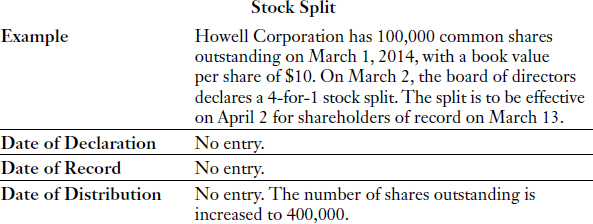

A stock dividend is a dividend paid in the form of shares, and does not affect total assets, liabilities, or total shareholders' equity. A stock dividend usually results in the reclassification of retained earnings to share capital and a lower book value per common share, due to the increased number of shares outstanding. A stock split also does not affect total assets, liabilities, or shareholders' equity, and results in a lower book value per common share (again, due to the increased number of shares outstanding). However, no journal entry is required for a stock split; it does not result in reclassification of retained earnings to share capital. A stock split is usually initiated in order to decrease the market price per share and to make the shares more accessible to a wide variety of investors. In general, a 2:1 stock split means that for each outstanding share before the split, there will be two outstanding shares after the split. Therefore, after the split, each (new) share will trade at approximately half of the previous price of one outstanding share.

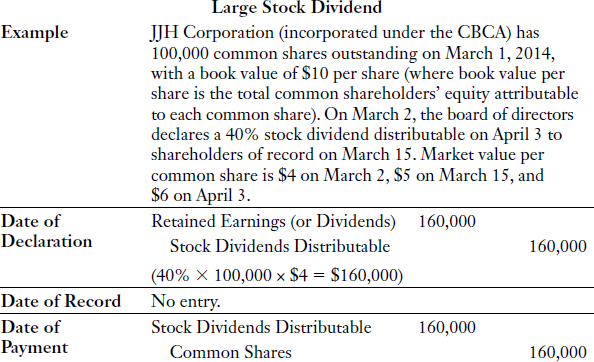

When a large stock dividend is issued, in economic substance, the transaction may more closely resemble a stock split. For companies incorporated under the Canada Business Corporations Act (CBCA), stock dividends (whether small or large) are generally recorded as dividends and measured at market value of the shares given up. For companies incorporated under other legal jurisdictions, stock dividends that result in issuance of more than 20% to 25% of the number of shares previously outstanding may be accounted for as stock splits. Professional judgement should be exercised in accounting for large stock dividends.

Becoming Proficient in Related Calculations

There are a few complex calculations in this chapter. The par value method of accounting for shares is common in the United States; however, in Canada, most companies do not issue par value shares. (Under the CBCA and most provincial acts, par value shares are not permitted.) Under ASPE, the journal entries for reacquisition of shares and subsequent sale or cancellation may be tricky, and are the focus of a number of the multiple-choice questions and exercises that follow. Under IFRS, no explicit guidance is given regarding accounting for reacquisition of shares.

Understanding Financial Reorganizations

A financial reorganization occurs when a financially troubled company restructures its debt and equity through an agreement between existing creditors and shareholders. Often, existing creditors exchange their non-equity interests for equity in the company. In general, equity and non-equity interests are substantially realigned to place less of a financial burden on the company, in order to allow the company to proceed with its plans for recovery and growth.

Under ASPE, if a financial reorganization involves a change in ownership or voting control (often it is the creditors who gain control), and new costs are reasonably determinable, the company should undergo a comprehensive revaluation of assets and liabilities. Comprehensive revaluation involves three steps: (1) bringing the deficit (negative retained earnings balance) to zero (by reclassifying it against accounts in shareholders' equity), (2) recording the changes in debt and equity, and (3) comprehensively revaluing assets and liabilities (and recording the revaluation adjustment against shareholders' equity). This gives the company a fresh start and allows retained earnings to start from zero.

Under IFRS, comprehensive revaluation is not discussed, and no specific guidance is given for accounting for financial reorganizations. However, note that IFRS does allow revaluation of property, plant, and equipment and intangibles (under the revaluation model), financial instruments (under the fair value option), and investment properties (under the fair value model).

TIPS ON CHAPTER TOPICS

- Shareholders' equity is often referred to as capital. In accounting for shareholders' equity, the emphasis is on the source of capital, which is classified into two categories: contributed capital and earned capital.

- Contributed capital consists of share capital and contributed surplus. Earned capital consists of retained earnings and, under IFRS, accumulated other comprehensive income (AOCI). (The concept of other comprehensive income does not apply under ASPE.) Earned capital is cumulative income that remains undistributed or is invested in the company. Contributed capital arises from amounts invested in the company by shareholders or contributed to the company as a result of certain shareholder transactions.

- Share capital accounts include Common Shares, Preferred Shares, Common Shares Subscribed, and Preferred Shares Subscribed.

- Contributed surplus can be affected by a variety of transactions, including par value share issue and/or retirement, treasury share transactions, liquidating dividends, share subscriptions forfeited, and donated assets by a shareholder.

- When a company sells or issues shares directly to new owners, the issuance is recorded on the company's books with an increase in assets and an increase in shareholders' equity. If a shareholder later sells his or her shares to another investor (in a secondary market or stock market), the company does not record a journal entry. The company only records the name of the new shareholder in its shareholder records. The assets, liabilities, and shareholders' equity of the company are not affected by secondary purchase (or sale) of shares by investors in the stock market.

- When a corporation issues more than one class of share capital, separate contributed surplus general ledger accounts should be maintained for each class of share capital. The balances of all contributed surplus accounts are usually summed and reported as a single amount on the statement of financial position under the caption Contributed Surplus.

- If shares from more than one class of share capital are issued in exchange for a lump-sum payment, the payment must be allocated between each class of share capital using either the relative fair value method or the residual value method. These methods are also applied in accounting for lump-sum purchases of property, plant, and equipment, and lump-sum revenue received for bundled sales.

- Direct costs of share issuance (including underwriting costs and accounting and legal fees) are debited to share capital because they represent a reduction of contributed capital (not operating expenses).

- Under IFRS, if shares are issued in a nonmonetary exchange, the fair value of the asset acquired should be used to measure the acquisition cost of the asset. (It is presumed that fair value of the asset acquired can be determined except in rare cases.) If the asset's fair value cannot be determined reliably, then the fair value and cost of the asset acquired are determined using the fair value of the shares given in exchange. Under ASPE, the acquisition cost of the asset may be measured by either the fair value of the asset acquired or fair value of the shares given up, whichever is more reliably determinable.

- Under ASPE, specific guidance is given for accounting for a reacquisition of shares. If the reacquisition cost is greater than the original issue amount, the reacquisition cost is allocated in this order. (1) First, it is allocated to share capital, in an amount equal to the par, stated, or assigned value of the shares. (2) Second, for any excess after the first allocation, it is allocated to contributed surplus, to the extent that contributed surplus was created by a net excess of proceeds over cost on a cancellation or resale of shares of the same class. (3) Third, for any excess after the second allocation, cost is allocated to contributed surplus in an amount equal to the pro rata share of the portion of contributed surplus that arose from transactions, other than those above, in the same class of shares. (4) Last, for any excess after the third allocation, cost is allocated to retained earnings. If the reacquisition cost is less than the original issue amount, the reacquisition cost is allocated (1) first, to share capital, in an amount equal to the par, stated, or assigned value of the shares; and (2) second, for the difference after the first allocation, to contributed surplus. Note that par value shares are not permitted under the CBCA; therefore, for most shares in Canada, the assigned value is equal to the average per share amount in the respective share capital account at the transaction date.

- Neither par value nor treasury shares are allowed under the CBCA. (Under the act, shares issued by corporations must be without par value, and reacquired shares are generally cancelled.) However, for companies incorporated in jurisdictions that allow par value and treasury shares, par value is a fixed per share amount printed on each share certificate. Par value usually has no direct relationship with the share's issuance price or fair value (the value at which it can be bought or sold) at any date subsequent to the issuance date. A treasury share is a corporation's own share that has been reacquired after having been issued and fully paid for, has not been cancelled, and is being held in the treasury for reissue.

- Treasury shares are not common in Canada; however, repurchase and cancellation of shares is common in Canada. Treasury shares are more common in the United States where reacquired shares are often not retired.

- The retained earnings account balance has no relationship with the amount of cash held by the company; retained earnings is simply a calculation of cumulative net income earned by the company not yet distributed to shareholders. Calculation of net income is affected by accounting accruals and other non-cash items, and cash is also generated and used in a variety of investing and financing transactions. It is possible for a company to have a large balance in its cash account with a small balance in its retained earnings account, or a small balance in its cash account with a large balance in its retained earnings account.

- There are three dates associated with declaration of any dividend: (1) declaration date, (2) date of record, and (3) date of payment (or distribution). A journal entry is required on the date of declaration and on the date of payment.

- Declaration of a cash dividend reduces working capital, but payment of a previously declared cash dividend has no effect on working capital. Unless otherwise indicated, a balance in dividends payable represents an obligation to be settled by cash.

- In recording the declaration of any dividend (except for a liquidating dividend), a temporary account called Dividends may be used, instead of debiting retained earnings directly. In the closing process at the end of the period, the balance of Dividends is closed to retained earnings.

- A dividend is usually considered a distribution of income, not a reduction of income (expense), unless the underlying security that generated the dividend is classified as debt (see Chapter 17).

- A preferred share's dividend preference is usually expressed either as a percentage of par or stated value, or in terms of dollars per share.

- Dividends in arrears are dividends on cumulative preferred shares that were not paid in previous year(s). Until the board of directors formally declares that dividends in arrears are to be paid, they are not reported as a liability. However, dividends in arrears should be disclosed in the notes to the financial statements.

- A dividend in kind or property dividend (a dividend payable with assets of the corporation other than cash) is an example of a non-reciprocal transfer of nonmonetary assets. A dividend in kind is generally measured at the fair value of the assets given up unless the transaction is considered to represent a spinoff or other form of restructuring or liquidation, in which case the dividend should be recorded at the carrying value of the assets or liabilities transferred.

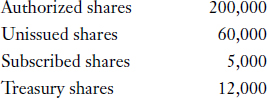

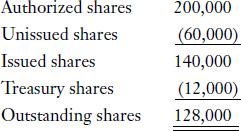

PURPOSE: This exercise will highlight the relationships among authorized, issued, outstanding, and subscribed shares.

The following data are available regarding common shares of Daffy Corporation at December 31, 2014:

Instructions

Calculate the number of outstanding shares. Assume treasury shares are allowed in Daffy's legal jurisdiction.

Solution to Exercise 15-1

EXPLANATION: Write down the formula for the number of outstanding shares:

![]()

Determine the data required to calculate the number of outstanding shares according to the above formula. Authorized shares are either issued or unissued, and subscribed shares should be included in the number of unissued shares (because they are not issued until they are fully paid); therefore, the number of issued shares can be calculated from the facts given. Issued shares are either treasury shares or outstanding shares. Subtracting the number of treasury shares from the number of issued shares results in the number of outstanding shares.

Transactions That May Affect Contributed Surplus

Contributed surplus may be affected by a variety of transactions or events as noted below:

- Par value share issue and/or retirement

- Treasury share transactions including the resale and retirement of shares

- Liquidating dividends

- Financial reorganizations

- Stock options and warrants

- Issue of convertible debt

- Share subscriptions forfeited

- Donation of assets or capital by a shareholder

- Redemption or conversion of shares

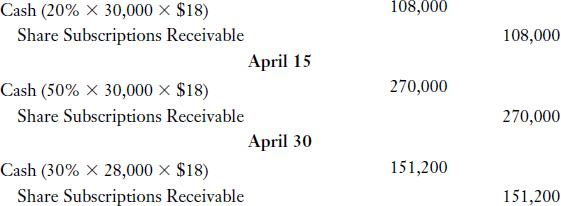

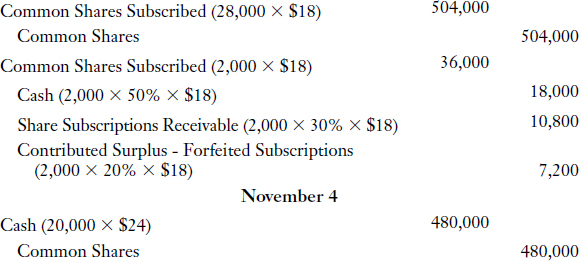

PURPOSE: This exercise will illustrate journal entries related to issuance of share capital.

Bimini Bay Corporation prepares financial statements under ASPE. On February 1, 2014, Bimini received authorization to issue 400,000 no par value common shares. The following transactions occurred during 2014:

Instructions

Prepare the journal entries to record the transactions listed above.

Solution to Exercise 15-2

In accounting for share subscriptions, share capital increases (by crediting Common Shares Subscribed) on the date the subscriptions (contracts) are received, not when the related cash is received. However, if Share Subscriptions Receivable is classified as a contra shareholders' equity account (as it often is), total shareholders' equity is unaffected by the entry to record the receipt of subscriptions. Total shareholders' equity would increase only when cash is received, which would reduce Share Subscriptions Receivable, the contra shareholders' equity account.

EXPLANATION:

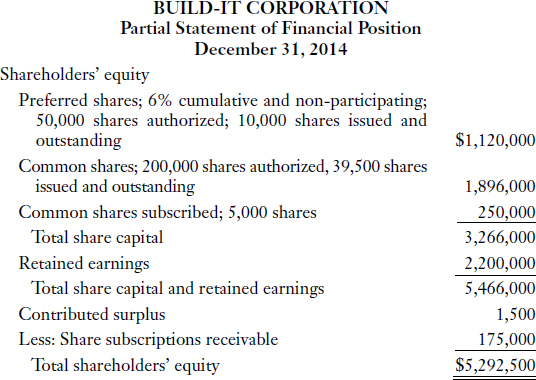

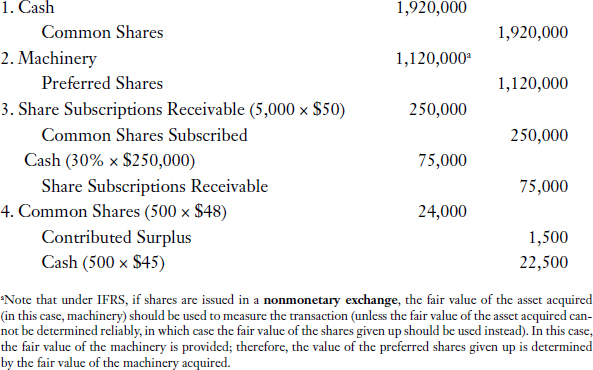

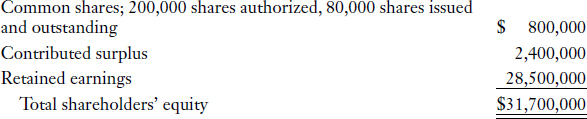

PURPOSE: This exercise will illustrate how the components of shareholders' equity are reported on the statement of financial position.

Build-It Corporation prepares financial statements under IFRS. Build-It's charter authorizes 200,000 common shares and 50,000 6% cumulative and non-participating preferred shares.

The corporation had the following share transactions between the date of incorporation and December 31, 2014:

- Issued 40,000 common shares for $1,920,000.

- Issued 10,000 preferred shares in exchange for machinery valued at $1,120,000.

- Received subscriptions for 5,000 common shares and collected 30% of the subscription price of $50 per share.

- Reacquired and cancelled 500 common shares at $45 per share.

At December 31, 2014, Build-It's retained earnings balance was $2.2 million.

Instructions

Prepare the shareholders' equity section of the statement of financial position in good form.

Solution to Exercise 15-3

APPROACH: Reconstruct journal entries to record the transactions. Use the resulting account balances to prepare the shareholders' equity section of the statement of financial position at December 31, 2014.

EXPLANATION:

PURPOSE: This exercise will examine major classifications within the shareholders' equity section of the statement of financial position.

Shareholders' equity is an important element on a corporation's statement of financial position.

Instructions

Identify and discuss the general categories of shareholders' equity for a corporation. List specific sources of equity included in each general category.

Solution to Exercise 15-4

The general categories of shareholders' equity (or corporate capital) are as follows:

- Contributed capital (share capital plus contributed surplus)

- Earned capital (retained earnings plus, under IFRS, accumulated other comprehensive income)

Contributed capital usually consists of amounts paid-in for all classes of shares. Contributed capital also includes contributed surplus, which may be affected by a variety of transactions or events, including:

- Par value share issue and/or retirement

- Treasury share transactions including the resale and retirement of shares

- Liquidating dividends

- Financial reorganizations

- Stock options and warrants

- Issue of convertible debt

- Share subscriptions forfeited

- Donations of assets or capital by a shareholder

- Redemption or conversion of shares

Earned capital is cumulative undistributed income that remains invested in the company. Earned capital includes retained earnings, which represents accumulated net earnings of a corporation in excess of net losses and dividends. A corporation may have appropriations (or restrictions) on retained earnings, which would make a portion of the retained earnings balance unavailable as a basis for dividends. Appropriations on retained earnings may arise as a result of restrictions per bond indentures or other formal agreements, or they may be initiated at the discretion of the board of directors.

Because other comprehensive income is not discussed under ASPE, accumulated other comprehensive income (AOCI) is a concept that applies only under IFRS. Therefore, for companies under IFRS, earned capital includes retained earnings as well as AOCI. AOCI is the cumulative change in equity due to revenues, expenses, gains, and losses that are excluded from the calculation of net income (and therefore bypass the income statement). Examples include unrealized gains on property revaluation, unrealized gains and losses on FV-OCI investments, and unrealized exchange differences on translation of foreign operations.

- A liquidating dividend is a distribution to shareholders from invested capital. Thus, a liquidating dividend results in a reduction of contributed capital and does not affect retained earnings. The shareholders' investment in the corporation is reduced, but not necessarily eliminated, by this type of dividend. If a dividend is only partially liquidating (it is partially a return of capital and partially a return on capital), both contributed capital and retained earnings are reduced.

- Although a stock dividend usually results in a reduction of retained earnings, contributed capital would increase by the same amount, resulting in no change in total shareholders' equity. The CBCA requires that any newly issued shares be measured at market value (including those issued as stock dividends).

- Capitalization of retained earnings refers to the transfer of retained earnings to contributed capital. Stock dividends result in capitalization of retained earnings (they are recorded with a debit to retained earnings and a credit to a contributed capital account), and they result in the retention of earned capital rather than the distribution of earned capital in the form of cash dividends.

- Stock Dividends Distributable is a share capital account and is therefore reported as an element of contributed capital. This account only has a balance during the short period between the date of stock dividend declaration and the date of stock dividend distribution.

- All changes in all shareholders' equity accounts for the period should be disclosed. Under IFRS, such changes (including changes in retained earnings, AOCI, and share capital) are required to be disclosed in a statement of changes in shareholders' equity. A popular format for presentation of the statement of changes in shareholders' equity is illustrated in the Solution to Exercise 15-8. Under ASPE, a statement of retained earnings is required, and any changes in share capital should be disclosed in the notes to the financial statements.

- If the return on common shareholders' equity is higher than the return on assets, the entity is (favourably) using borrowed money from bondholders and/or obtaining capital from preferred shareholders, and earning a return on those funds that is higher than the cost of using those funds. This is called trading on the equity at a gain or favourably trading on the equity. However, if cost of debt and/or cost of preferred dividends exceeds return on total assets, the entity is said to be trading on the equity at a loss or unfavourably trading on the equity, and the return on common shareholders' equity will be lower than return on assets.

Journal Entries for Recording Dividends and Stock Splits

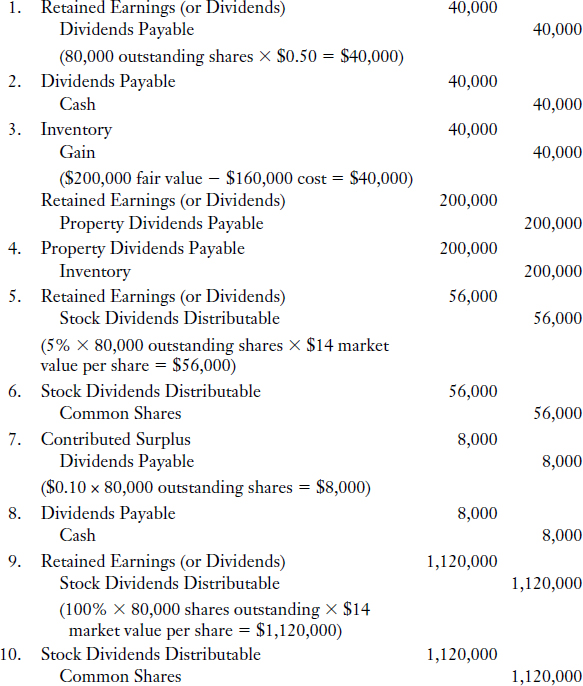

Any change in fair value of the property between the date of declaration and date of payment is ignored.

Under ASPE and IFRS, there is no clear guidance on how to account for stock dividends; however, since Henry was incorporated under the CBCA, stock dividends should be treated as dividends and measured at the fair value of the shares given up.

Because JJH was incorporated under the CBCA, its stock dividends should be treated as dividends and measured at the market value of the shares given up. However, if the company was incorporated under another jurisdiction, given the significance of the stock dividend, it should be considered whether the economic substance of the transaction more resembles a stock split. Sometimes, a stock dividend of more than 20% to 25% of the number of shares previously outstanding is accounted for as a stock split. There is no specific guidance under ASPE or IFRS on this issue; in Canada, this is a matter of professional judgement. See Exercise 15-5 for more detail on this topic.

The carrying value of Common Shares increases by $160,000, but the book value per share drops to $7.14 ($1,000,000 / 140,000 shares).

The carrying value of Common Shares does not change, but the book value per share drops to $2.50 ($1,000,000 ÷ 400,000 shares).

PURPOSE: This exercise will compare a large stock dividend with a small stock dividend.

Both stock splits and stock dividends change the number of shares outstanding.

Instructions

(a) Explain what is meant by a stock split carried out in the form of a dividend.

(b) From an accounting viewpoint, explain how a stock split carried out in the form of a dividend differs from an ordinary stock dividend.

(c) Explain how a stock dividend that has been declared but not yet issued should be classified on a statement of financial position.

Solution to Exercise 15-5

(a) A stock split carried out in the form of a dividend is a distribution of corporate shares to present shareholders, in proportion to each shareholder's current shareholdings, which is expected to cause a material decrease in market value per share. Usually a distribution in excess of 20% to 25% of the number of shares previously outstanding would cause a material decrease in market value per share, and may have the same effect on the market price of the share as a stock split.

(b) Because a distribution in excess of 20% to 25% of the number of shares previously outstanding would cause a material decrease in market value per share, it must be determined whether a large stock dividend is more like a stock split or a stock dividend. Under the CBCA, any newly issued shares must be measured at market value (including those issued as stock dividends). However, in jurisdictions where legal requirements for stated share capital values are not a constraint, a large stock dividend (such as a 40%, 50%, or 100% stock dividend) may be considered a stock split carried out in the form of a dividend, and may be treated for accounting purposes as a stock split. Accounting for a stock dividend as an ordinary stock dividend would require a debit to retained earnings and a credit to common shares for either the market value or par or stated value of the shares given up (and therefore capitalization of retained earnings). Accounting for a stock dividend as a stock split would not require any journal entries or capitalization of retained earnings. However, accounting for a stock dividend either as an ordinary stock dividend or as a stock split would decrease the book value per share in proportion to the increase in the number of shares outstanding.

(c) A declared but unissued stock dividend should be classified as part of contributed capital rather than as a liability. A stock dividend affects only shareholders' equity accounts (retained earnings decreases and contributed capital increases). Thus, there is no debt obligation, and no transfer of corporate assets when a stock dividend is distributed. Furthermore, at any time prior to issuance, a corporation's board of directors can revoke a stock dividend declared.

PURPOSE: This exercise will allow you to practise recording various types of dividends.

Scot Corporation, incorporated under the CBCA, had the following shareholders' equity items at December 31, 2013:

Instructions

Record journal entries for each of the following transactions in 2014. Assume each transaction is independent of the others, unless otherwise indicated. Dividends are declared only on outstanding shares.

- Declared a cash dividend of $0.50 per share.

- Paid the dividend declared in item (1) above.

- Declared a property dividend. Inventory with a cost of $160,000 and a fair value of $200,000 is to be distributed.

- Distributed the property for the dividend declared in item (3) above.

- Declared a 5% stock dividend when the market value was $14 per share.

- Distributed shares for the stock dividend described in item (5) above.

- Declared a liquidating dividend of $0.10 per share.

- Distributed the dividend described in item (7) above.

- Declared a 100% stock dividend when the market value was $14 per share.

- Distributed the dividend declared in item (9) above.

- Declared a 2:1 stock split.

Solution to Exercise 15-6

11. No journal entry required; memorandum-type entry noted for increase in number of shares issued and outstanding. Number of shares issued and outstanding is doubled (from 80,000 to 160,000), reducing carrying value per common share to one half of what it was previously (from $10 per share to $5 per share).

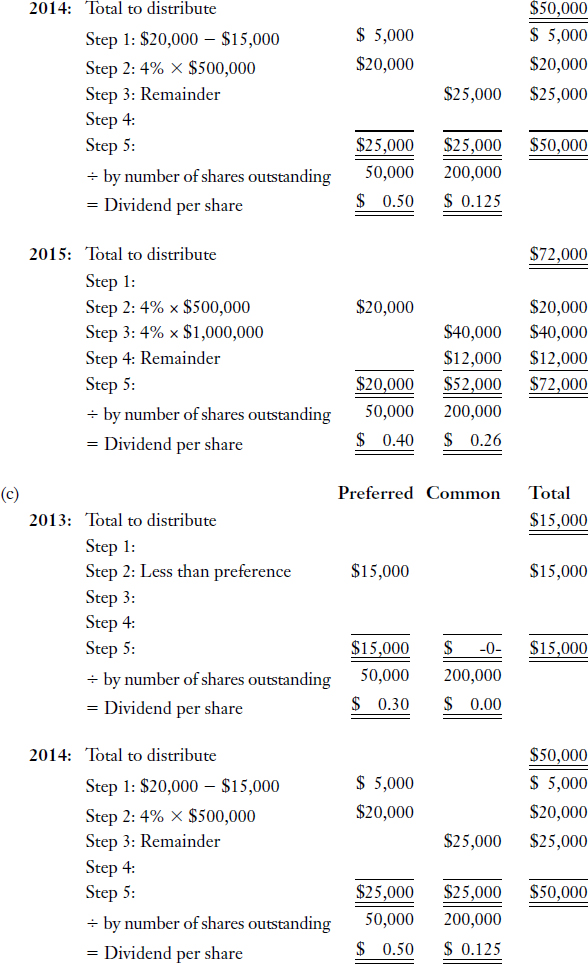

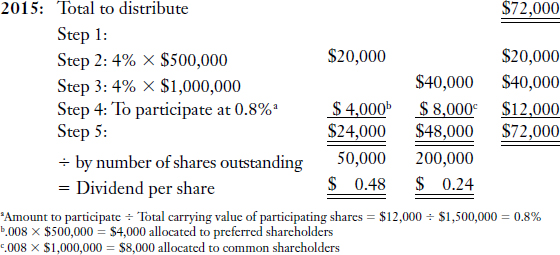

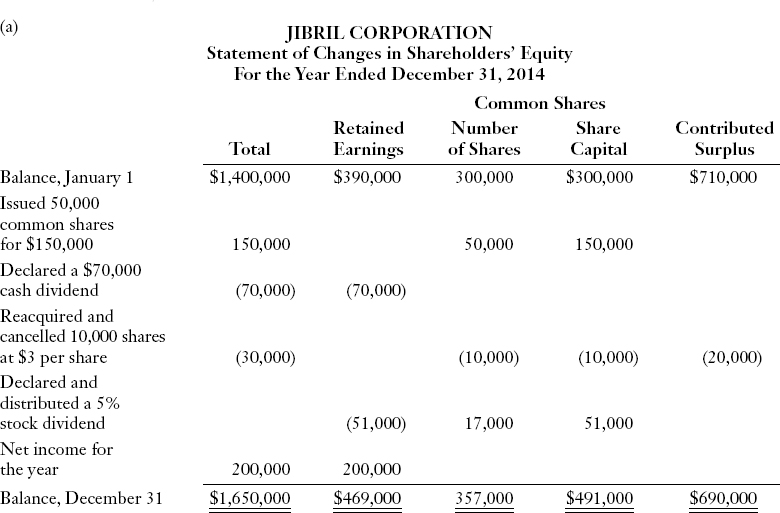

Steps in Allocating Dividends to Preferred and Common Shareholders

Step 1: Assign cumulative dividends in arrears, if any, to preferred shareholders.

If there are any cumulative dividends in arrears, allocate dividends to preferred shareholders first, in the amount of arrearage. Then, calculate the amount of dividends remaining to be allocated. (If the amount of dividends is not enough to cover the arrearage, no further steps in allocating dividends are performed, all dividends declared are allocated to preferred shareholders, and remaining arrearage is calculated and disclosed.)

Step 2: Assign current-period preference to preferred shareholders.

Calculate the amount of preferred shareholders' current-year preference, and allocate that amount to preferred shareholders. Then, calculate the amount of dividends remaining to be allocated. (If the amount of dividends is not enough to cover preferred shareholders' current-year preference, no further steps in allocating dividends are performed, and all dividends are allocated to preferred shareholders.)

Step 3: Assign common shareholders an equal percentage dividend.

Calculate the amount of dividends required to give common shareholders a “like” percentage dividend as was given to preferred shareholders (for current-year preference only), and allocate that amount to common shareholders. If the remaining amount of dividends is sufficient to cover this “like” percentage dividend, the remaining amount of dividends (after the “like” percentage dividend allocation to common shares) is the amount that both preferred and common shareholders will “participate” in. (If the amount of dividends is not enough to give common shareholders a “like” percentage dividend, whatever is remaining after preferred shareholders get their allocations as calculated in steps 1 and 2 is allocated to common shareholders.)

Step 4: Assign participation amounts to preferred and common shares.

If the preferred shares are non-participating, the remaining dividends are assigned to common shareholders. If the preferred shares are participating, the remaining dividends are allocated between preferred and common shareholders by prorating them based on their relative carrying amounts.

Step 5: Total amounts allocated and calculate per share amounts.

Assigned dividend amounts calculated from the steps above are added together, on a per class basis. The total amount of dividends assigned to preferred shareholders and to common shareholders is often expressed on a per share basis. To calculate dividend per share, the total dividend per class is divided by the number of shares outstanding in the class.

“Arrearage” refers to the amount of cumulative preferred dividends in arrears.

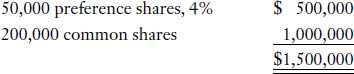

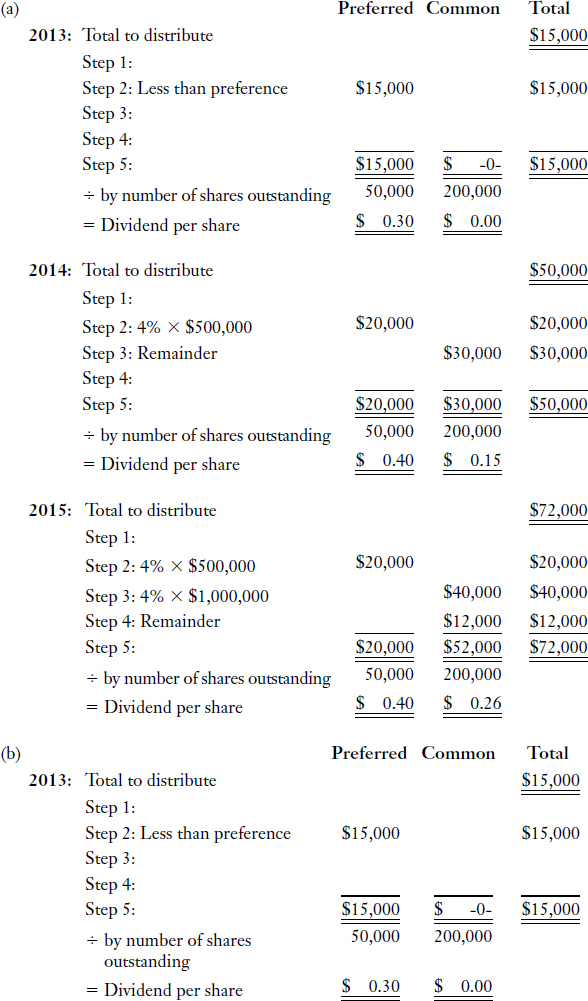

PURPOSE: This exercise will illustrate the allocation of dividends when a corporation has both preferred and common shares outstanding.

Daly Corporation has the following shares outstanding, without any changes, for years 2013, 2014, and 2015.

Dividends are declared as follows:

Instructions

Calculate the amount of dividends (total and per share) to be allocated to preferred shareholders and to common shareholders for each of the three years under each of the independent assumptions below:

(a) The preferred shares are non-cumulative and non-participating.

(b) The preferred shares are cumulative and non-participating.

(c) The preferred shares are cumulative and fully participating.

Solution to Exercise 15-7

APPROACH: Calculate the preferred shares' current-year preference ($500,000 × 4% = $20,000) and the amount that would be required to give common shareholders a “like” percentage dividend ($1,000,000 × 4% = $40,000). Then refer to the steps listed in Illustration 15-3 to solve.

Notice that in performing step 3, the amount of remaining dividends ($25,000) is not sufficient to give common shareholders a “like” percentage dividend (4% × $1,000,000 > $25,000), so the entire amount ($25,000) is allocated to common shareholders.

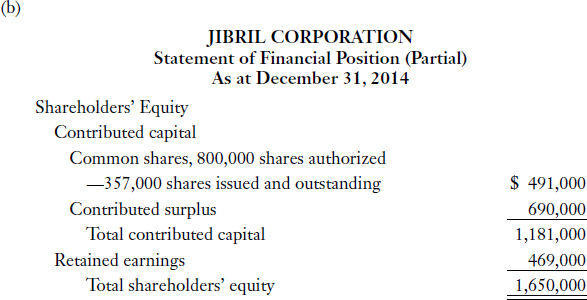

PURPOSE: This exercise will illustrate the preparation of a statement of changes in shareholders' equity and the related shareholders' equity section of the statement of financial position.

On January 1, 2014, Jibril Corporation had the following shareholders' equity balances:

During 2014, the following occurred in sequence:

- Issued 50,000 common shares for $150,000.

- Declared a $70,000 cash dividend.

- Reacquired and cancelled 10,000 shares at $3 per share.

- Declared and distributed a 5% stock dividend when the market value was $3 per share.

- Earned net income for the year of $200,000.

Of the contributed surplus of $710,000 as at January 1, 2014, $70,000 arose from net excess of proceeds over cost on a previous cancellation of common shares.

Instructions

(a) Prepare a statement of changes in shareholders' equity for the year ended December 31, 2014.

(b) Prepare the shareholders' equity section of the statement of financial position as at December 31, 2014.

Solution to Exercise 15-8

Notice how the columns on this statement foot (add down) and crossfoot (add across).

EXPLANATION: Under IFRS, changes in all shareholders' equity accounts for the period are required to be disclosed in a statement of changes in shareholders' equity. Under ASPE, a statement of retained earnings is required, and any changes in share capital are usually disclosed in the notes to the financial statements. A statement of changes in shareholders' equity contains all of the information that a statement of retained earnings would contain plus information regarding changes in the other components of shareholders' equity.

The journal entry for the reacquisition and cancellation of shares:

Calculations for the stock dividend are as follows:

340,000 shares outstanding × 5% = 17,000 dividend shares.

17,000 shares × $3 market value per share = $51,000 decrease in Retained

Earnings and increase in Common Shares.

Ratios for Analysis of Shareholders' Equity

The following four ratios use shareholders' equity amounts to evaluate a company's profitability and long-term solvency.

1. Rate of return on common shareholders' equity. This widely used ratio measures profitability from the common shareholders' viewpoint. This ratio shows how many dollars of net income were earned for each dollar invested by the owners, and is calculated as follows:

When rate of return on common shareholders' equity is greater than rate of return on total assets, the company is said to be “trading on the equity at a gain” or “favourably trading on the equity.” Trading on the equity is the practice of using borrowed money at fixed interest rates, or proceeds from the issuance of preferred shares with constant dividend rates, to purchase assets in hopes of earning a rate of return on those assets that exceeds the rate of interest on the bonds and/or rate of constant dividends on the preferred shares. If this can be done, the capital obtained from bondholders and/or preferred shareholders will earn enough to pay interest on the bonds and/or dividends on the preferred shares, and still leave a margin for the common shareholders. When this occurs, trading on the equity is profitable.

2. Payout ratio. Payout ratio is the ratio of cash dividends to net income, and is calculated for common shareholders as follows:

![]()

Some investors prefer investing in shares that have a payout ratio sufficiently high to provide a good yield or rate of return on the shares. Other investors prefer investing in shares that have higher potential for share appreciation (increase in market value).

Another closely watched ratio is dividend yield, which is cash dividend per share divided by market price. This ratio gives investors some idea of the rate of return that will be received in the form of cash dividends.

3. Price earnings (P/E) ratio. Analysts often highlight this ratio when discussing the investment potential of a given company. It is calculated by dividing market price per share by earnings per share:

![]()

- The P/E ratio is often referred to as a “multiple.”

- When one company's P/E ratio is significantly different than another company's P/E ratio, the difference may be due to several factors, for example: relative business risk, stability of earnings, earnings trend, and market perception of growth potential and quality of earnings.

4. Book value per share. Book value or equity value per share is a much-used basis for evaluating the net worth of a corporation. Book value per share is the amount each share would receive if the company were liquidated, based on the amounts reported on the statement of financial position. However, this ratio loses much of its relevance if the valuations on the statement of financial position do not approximate fair value. Assuming no preferred shares are outstanding, the ratio is calculated as follows:

![]()

To calculate book value per common share when there are also preferred shares outstanding, apply the following steps:

Step 1:

Allocate retained earnings between preferred shareholders and common shareholders, considering preferred dividends in arrears (if any), current-year preference dividends, and effect of participation (if the preferred shares are participating).

Step 2:

Calculate total shareholders' equity allocated between preferred shareholders and common shareholders, equal to contributed capital plus allocated retained earnings (from step 1), for each class.

Step 3:

Calculate book value per common share by dividing total shareholders' equity allocated to common shareholders (from step 2) by number of common shares outstanding.

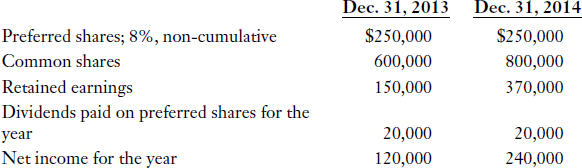

PURPOSE: This exercise will give you an example of how to calculate the rate of return on common shareholders' equity.

Instructions

Calculate the rate of return on common shareholders' equity (rounded to the nearest percentage) for 2014.

Solution to Exercise 15-9

EXPLANATION: Return on common shareholders' equity is a widely used ratio that measures profitability from the common shareholders' viewpoint. This ratio shows how many dollars of net income were earned for each dollar invested by the owners. It is calculated by dividing net income applicable to common shareholders (net income − preferred dividends) by average common shareholders' equity.

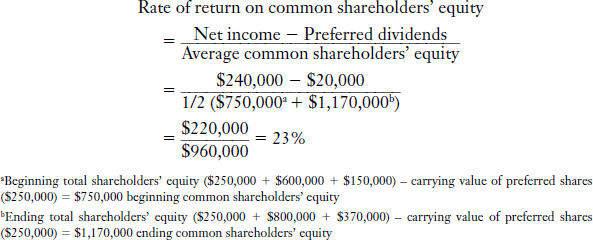

PURPOSE: This exercise will illustrate the procedures applied in accounting for a financial reorganization.

The following facts pertain to the Huang Corporation at December 31, 2014:

- Retained earnings has a negative balance of $30,000.

- Inventory cost exceeds fair value by $12,000.

- Plant assets' total carrying value exceeds total fair value by $28,000.

- There are 3,000 common shares with a carrying value of $300,000.

- There is no contributed surplus.

Future prospects for successful operations are good. In order to eliminate the deficit (negative retained earnings balance), a financial reorganization is successfully negotiated with a change in control of the company. Huang prepares financial statements in accordance with ASPE.

Instructions

(a) Record all of the journal entries related to this financial reorganization.

(b) Explain what must be disclosed after the financial reorganization.

Solution to Exercise 15-10

APPROACH: Apply the three steps listed below.

| Step 1: | Bring the deficit balance to zero. Begin by recording any asset writedowns or impairments that existed prior to the reorganization. Then reclassify the deficit to Share Capital, Contributed Surplus, or a separately identified account within Shareholders' Equity. |

| Step 2: | Record the changes in debt and equity (as negotiated). Often debt is exchanged for equity, causing a change in control. |

| Step 3: | Comprehensively revalue assets and liabilities. Assign appropriate going concern values to all assets and liabilities based on the negotiations. The total difference between carrying values prior to the reorganization and new values is called the “revaluation adjustment.” The revaluation adjustment and any costs incurred to carry out the financial reorganization are accounted for as capital transactions and are closed to Share Capital, Contributed Surplus, or a separately identified account within Shareholders' Equity. Note that the total of the new values of the identifiable assets and liabilities must not exceed the entity's fair value (if known). |

(a) Journal entries:

(b) After a financial reorganization, the following must be disclosed: the date of the reorganization, a description of the reorganization, and the amount of change in each major class of assets, liabilities, and shareholders' equity resulting from the reorganization. In the following fiscal period, in subsequent reports, the following must be disclosed: the date of the reorganization, the revaluation adjustment amount and the shareholders' equity account in which it was recorded, and the amount of the deficit that was reclassified and the account to which it was reclassified.

A financial reorganization is often called a fresh start.

ANALYSIS OF MULTIPLE-CHOICE QUESTIONS

Question

1. Which of the following rights does a preferred shareholder normally possess?

- right to vote

- right to receive a dividend before common shareholders

- pre-emptive right

- right to participate in management

EXPLANATION: A preferred shareholder usually has dividend preference and priority claim on assets (upon dissolution of the company) over common shareholders. In exchange for these special preferences and claims, a preferred shareholder normally has to sacrifice other rights, including the right to vote on operational and financial decisions, and the pre-emptive right. A common shareholder normally has the right to vote (and, along with other common shareholders, can exercise control over corporation management by electing the board of directors to make major decisions for them), and the pre-emptive right (the right to maintain the same percentage ownership when additional common shares are issued). (Solution = b.)

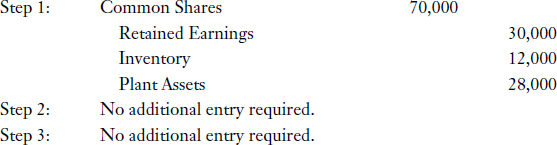

Question

2. The Wabasca Corporation has 10,000 common shares authorized. The following transactions took place during 2014, the first year of the corporation's existence:

- Sold 1,000 common shares for $18 per share.

- Issued 1,000 common shares in exchange for a patent valued at $20,000.

- Reported net income of $7,000.

At the end of Wabasca's first year, total contributed capital amounts to:

- $18,000.

- $20,000.

- $28,000.

- $38,000.

EXPLANATION: (1) Write down the components of contributed (paid-in) capital: (a) share capital, and (b) contributed surplus. (2) Reconstruct the journal entries for the transactions listed. (3) Calculate the balances of the relevant accounts. (4) Sum the relevant account balances.

Retained earnings is considered earned capital.

Question

3. Which of the following represents the total number of shares that a corporation may issue under the terms of its charter?

- authorized shares

- unissued shares

- outstanding shares

- treasury shares

EXPLANATION: Explain each of the terms listed as possible answers. Issued shares (shares the corporation has issued to date) plus unissued shares (shares that have not been issued yet but may be issued in future under the terms of the charter) equals total authorized (approved) shares. Outstanding shares are issued shares that are now in the hands of shareholders. Treasury shares are shares that have been reacquired after having been issued and fully paid, have not been cancelled, and are not outstanding at the present time. (Solution = a.)

Question

4. Under IFRS, if common shares are issued for non-cash assets, the common shares should be recorded at:

- fair value of the non-cash assets received.

- par value of the shares issued.

- legal value of the shares issued.

- book value of the non-cash assets on the seller's books.

EXPLANATION: Under IFRS, if shares are issued in a nonmonetary exchange, the fair value of the assets acquired should be used to measure the transaction; if the fair value of the assets acquired cannot be determined reliably, then the transaction should be measured at the fair value of the shares given up. Assuming equipment with a fair value of $70,000 is received in exchange for common shares, the journal entry to record the transaction would be as follows:

Under ASPE, shares issued in a nonmonetary exchange may be measured either by the fair value of the assets received or the fair value of the shares given up, whichever is more reliably determinable.

Question

5. The balance of Share Subscriptions Receivable should be classified as:

- a current asset.

- contra to the sum of share capital and retained earnings.

- contra to retained earnings.

- contra to common shares.

EXPLANATION: Under ASPE, whether the Share Subscriptions Receivable account should be presented as an asset or a contra to equity is a matter of judgement. Conceptually, it makes sense to present the balance of Share Subscriptions Receivable as a reduction of equity. (Solution = b.)

Question

6. Treasury shares are:

- shares held as an investment by the treasurer of the corporation.

- shares held as an investment of the corporation.

- shares that are issued but not outstanding.

- unissued shares.

EXPLANATION: Treasury shares are a corporation's own shares that were issued and fully paid for, and subsequently reacquired by the corporation but not retired (cancelled). Treasury shares refer to a company's own shares so they cannot be an investment of the corporation; acquisition of treasury shares represents a contraction of capital (shareholders' equity), not acquisition of an asset. Treasury shares are considered issued but not outstanding (as the corporation has reacquired them). (Solution = c.)

For companies incorporated under the CBCA, repurchased shares are usually cancelled, and if the company's articles limit the number of authorized shares, the cancelled shares revert to authorized but unissued status.

Question

7. Wheeler Company incorporated in 2014 and issued 10,000 common shares for $24 each. On April 15, 2014, 10,000 common shares were issued in exchange for a piece of land adjacent to property currently owned by Wheeler. An independent valuator determined that the land had an appraised value of $370,000. Wheeler's shares are actively traded and had a market price of $40 per share on April 15, 2014. Under IFRS, the total amount of contributed capital resulting from the above transactions would be:

- $640,000.

- $240,000.

- $400,000.

- $610,000.

EXPLANATION: Under IFRS, if shares are issued in a nonmonetary exchange, the fair value of the asset acquired should be used to measure the acquisition cost of the asset; if the asset's fair value cannot be determined reliably, then the fair value of the shares given up should be used instead. In this case, the common shares given up in the nonmonetary exchange should be measured at $370,000. The common shares given up in the nonmonetary exchange of $370,000 plus the initial common share issuance of $240,000 equals total contributed capital of $610,000. (Solution = d.)

Question

8. Preferred shares that can be returned to the corporation and exchanged for common shares at the option of the shareholder are referred to as:

- cumulative preferred shares.

- convertible preferred shares.

- participating preferred shares.

- callable preferred shares.

EXPLANATION: Holders of convertible preferred shares have an option to exchange their preferred shares for common shares at a predetermined ratio. Holders of cumulative preferred shares are entitled to receive dividends in arrears and the current-period dividend preference, before any dividends can be paid to common shareholders. Holders of participating preferred shares share (at the same rate as common shareholders) in any dividend distributions beyond the preferred shares' annual dividend preference. Callable preferred shares give the issuing corporation the option to call or redeem the outstanding preferred shares at specified future dates and at stipulated prices. (Solution = b.)

Question

9. Which of the following transactions will cause a net increase in total contributed surplus?

- sale of no par value common shares

- sale of no par value preferred shares

- sale of bonds at a price higher than face value

- share subscriptions forfeited, with partial payment collected

EXPLANATION: Recall what affects contributed surplus. Proceeds received from issuance of no par value common and preferred shares are included in their respective share capital accounts. Premium on bonds payable is accounted for in the liability section, not the shareholders' equity section. Contributed surplus increases if partially paid share subscriptions are forfeited. (Solution = d.)

Question

10. The date that determines who is considered a shareholder for purposes of dividend distribution is the:

- declaration date.

- record date.

- payment date.

- distribution date.

EXPLANATION: The date the board of directors formally declares (authorizes) a dividend and announces it to shareholders is called the declaration date. On the record date, ownership of outstanding shares is determined for dividend distribution purposes, according to records maintained by the corporation. On the payment date, dividend cheques are mailed to shareholders. (Solution = b.)

Question

11. Declaration and payment of cash dividends by a corporation will result in a(n):

- increase in Cash and an increase in Retained Earnings.

- increase in Cash and a decrease in Retained Earnings.

- decrease in Cash and an increase in Retained Earnings.

- decrease in Cash and a decrease in Retained Earnings.

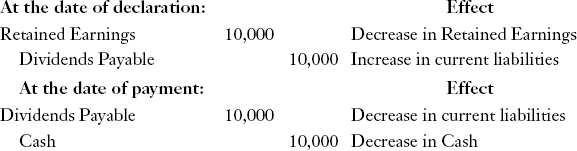

EXPLANATION: Prepare the journal entries required to record declaration and payment of a cash dividend. Analyze each debit and credit to determine how Cash and Retained Earnings are affected. Assuming cash dividends of $10,000 are declared, the entries and analysis are as follows:

The net effect of declaration and payment of a cash dividend is a decrease in retained earnings (and, thus, total shareholders' equity) and a decrease in Cash (and, thus, total assets). (Solution = d.)

Question

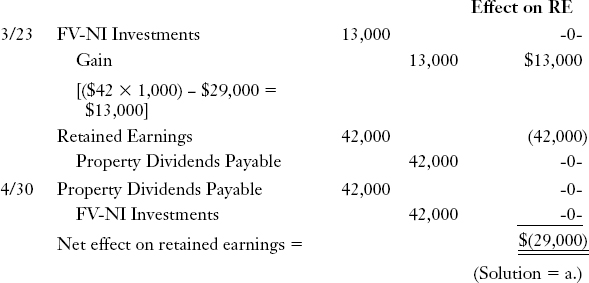

12. Barney's Corporation has a fair value-net income investment in DePaulo Corporation of 1,000 common shares at a carrying value of $29,000. These shares are used in a dividend in kind (property dividend) to shareholders of Barney's. The dividend in kind is declared on March 23 and distributed on April 30 to shareholders of record on April 15. Market value per share of DePaulo's stock is $42 on March 23, $44 on April 15, and $45 on April 30. The net effect of this dividend in kind is a reduction in retained earnings of:

- $29,000.

- $42,000.

- $44,000.

- $45,000.

EXPLANATION: Write down the journal entries involved in accounting for this dividend and summarize the results. The entries and their effects on retained earnings (RE) are as follows:

Although a property dividend is recorded at the fair value of the asset to be distributed, retained earnings decreases by the carrying value of the asset because the increase or decrease in the asset's fair value is also recorded (which goes through net income, and is closed to retained earnings).

Question

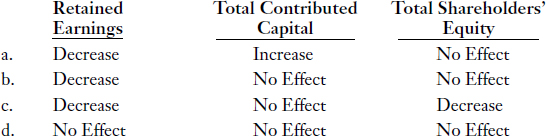

13. The net effect of the declaration and payment of a liquidating dividend is a decrease in:

- retained earnings and a decrease in total assets.

- total contributed capital and a decrease in total assets.

- total contributed capital and an increase in retained earnings.

- total shareholders' equity and an increase in liabilities.

EXPLANATION: A liquidating dividend represents return of contributed capital to shareholders, and is therefore based on contributed capital (rather than retained earnings). (Solution = b.)

Question

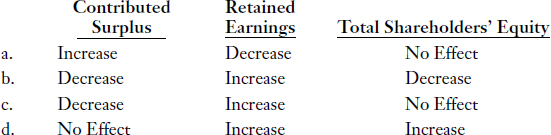

14. What effect does declaration and distribution of a 30% stock split carried out in the form of a dividend have on the following? (Assume that the company is incorporated under the CBCA.)

EXPLANATION: Write down the journal entries for declaration and distribution of a large stock dividend. Analyze each entry to determine how the above three amounts are affected.

Under the CBCA, the journal entry to record the declaration of a stock dividend will reduce Retained Earnings (or increase Dividends) and increase Stock Dividends Distributable (a component of share capital and, therefore, a component of total contributed capital). That entry will decrease Retained Earnings and increase total contributed capital by identical amounts, and thus have no effect on total shareholders' equity. The entry to record distribution will reduce Stock Dividends Distributable (contributed capital) and increase Common Shares. Therefore, the entry to record distribution will have no effect on any major total (or category) within shareholders' equity. (Solution = a.)

Question

15. A 300% stock dividend will have the same impact on the number of shares outstanding as a:

- 2-for-1 stock split.

- 3-for-1 stock split.

- 4-for-1 stock split.

- 5-for-1 stock split.

EXPLANATION: Set up an example with numbers. For instance, assume we begin with 10,000 shares outstanding. A 300% stock dividend would cause 30,000 new shares to be distributed, for a total of 40,000 total shares outstanding. A 2-for-1 stock split would cause 10,000 shares to be replaced with 20,000 shares. A 3-for-1 stock split would cause 10,000 shares to be replaced with 30,000 shares. A 4-for-1 stock split would cause 10,000 shares to be replaced with 40,000 shares. The example proves that a 300% stock dividend (a 300% increase in shares) has the same effect on the number of shares outstanding as a 4-for-1 stock split (each share is replaced with four shares). (Solution = c.)

Question

16. Trim Corporation declared a stock dividend of 10,000 shares when market value was $5 per share, and the number of shares outstanding was 200,000. If Trim Corporation was incorporated under the CBCA, how does the entry to record this transaction affect retained earnings?

- No effect

- $10,000 decrease

- $40,000 decrease

- $50,000 decrease

EXPLANATION: Under the CBCA, all stock dividends are recorded as dividends (debit to Retained Earnings and credit to Common Shares) and measured at the market value of the shares issued. A stock dividend of 10,000 shares multiplied by the $5 market price per share means retained earnings decreases by $50,000. (Solution = d.)

Question

17. A 4-for-1 stock split will cause a decrease in:

- total assets.

- total shareholders' equity.

- book value per share.

- retained earnings.

EXPLANATION: A stock split involves the issuance of additional shares to existing shareholders based on the number of shares currently outstanding. A stock split does not result in capitalization of retained earnings; however, book value per share decreases in proportion to the increase in the number of shares outstanding. Thus, in a 2-for-1 stock split, the number of shares is doubled and book value per share is cut in half. In a 4-for-1 stock split, there are four times as many shares outstanding after the split, and book value per share decreases to one quarter of book value per share before the split. Assets are not affected. (Solution = c.)

Question

18. The balance in Retained Earnings represents:

- cash set aside for specific purposes.

- earnings for the most recent accounting period.

- unrestricted cash on hand.

- total of all amounts reported as net income minus the total of all amounts reported as net loss and dividends declared since inception of the corporation.

EXPLANATION: Define retained earnings and select the answer that most closely matches the definition. Retained earnings is cumulative net income retained in a corporation. Net income (earnings for a period) increases retained earnings, and dividends (distributions of earnings to shareholders (owners)) decrease retained earnings. (Solution = d.)

Question

19. Assume common shares is the only class of shares outstanding in Min-Kyu Corporation. Total shareholders' equity divided by number of common shares outstanding is called:

- book value per share.

- par value per share.

- stated value per share.

- market value per share.

EXPLANATION: Briefly define each of the answer selections. Book value per share represents the equity a common shareholder has in the net assets of the corporation. When only one class of shares is outstanding, book value per share is determined by dividing total shareholders' equity by the number of shares outstanding. Par value is an arbitrary value that does not have much significance except in establishing legal capital and in determining the increase in the Common Shares account for each share issued. Stated value refers to an arbitrary value that may be placed on shares by the board of directors, and has about the same significance as par value. Market value refers to the price at which shares are currently being bought and sold in the open market. (Solution = a.)

Question

20. If a corporation has two classes of shares outstanding, rate of return on common shareholders' equity is calculated by dividing net income:

- minus preferred dividends by the number of common shares outstanding at the statement of financial position date.

- plus interest expense by the average amount of total assets.

- by the number of common shares outstanding at the statement of financial position date.

- minus preferred dividends by the average amount of common shareholders' equity during the period.

EXPLANATION: Rate of return on common shareholders' equity is calculated by dividing the amount of earnings available to common shareholders by the average amount of common shareholders' equity during the period. The amount of earnings available to common shareholders is net income for the period less the preferred dividend entitlement for the period. (Solution = d.)

Question

21. A corporation with a $4-million deficit undergoes a financial reorganization as at August 1, 2014. Certain assets will be written down by $800,000 to fair value. Liabilities will remain unchanged. Common shares have a carrying value of $6 million and contributed surplus of $5 million before the reorganization. How will the entries to record the financial reorganization on August 1, 2014, affect the following?

EXPLANATION: Write down the journal entry to record this reorganization. Analyze it to determine how the above three amounts will be affected.

The entry would be as follows:

Question

22. Which of the following items is not included in accumulated other comprehensive income (AOCI)?

- gains on property revaluation

- unrealized gains and losses on FV-NI investments

- unrealized gains and losses on FV-OCI investments

- exchange differences on translation of foreign operations

EXPLANATION: Recall the definition and components of accumulated other comprehensive income. Gains on property revaluation and exchange differences on translation of foreign operations are included in AOCI. Adjustments to mark FV-NI investments to fair value are included in net income, and therefore retained earnings. Unrealized gains and losses on FV-OCI investments are included in other comprehensive income, and therefore AOCI. (Solution = b.)

It is important to reconcile the components of AOCI because they may be transferred to net income when realized (depending on the accounting treatment of the item related to each component).