CHAPTER 3

Adjusting the Accounts

FEATURE STORY

What Was Your Profit?

The accuracy of the financial reporting system depends on answers to a few fundamental questions: At what point has revenue been recognized? When have expenses really been incurred?

Unfortunately, all too often companies overstate their revenues. For example, during the dot-com boom, most dot-coms earned a large percentage of their revenue from selling advertising space on their websites. To boost reported revenue, some dot-coms began swapping website ad space. Company A would put an ad for its website on company B’s website, and company B would put an ad for its website on company A’s website. No money changed hands, but each company recorded revenue (for the value of the space that it gave the other company on its site). This practice did little to boost net income, and it resulted in no additional cash flow—but it did boost reported revenue. Regulators eventually put an end to this misleading practice.

Another type of transgression results from companies recording revenues or expenses in the wrong year. In fact, shifting revenues and expenses is one of the most common abuses of financial accounting. For example, here is a sample of British companies that have recently disclosed issues regarding revenue recognition: the Nigerian unit of candy company Cadbury (GBR); vehicle and accident management company Helphire (GBR), which appeared to overstate the amount it was due in reimbursement from insurance companies; and Alterian (GBR), a software firm that specializes in social media, email, and web content management and analytics.

Perhaps one of the most unusual cases of reporting expenses in the wrong period was revealed by Olympus Corporation (JPN). The company admitted that it had covered up investment losses for more than a decade. It then tried to eliminate the losses from the books through a fraudulent process of overstating the price of some acquired assets and then writing down those assets in subsequent adjusting entries.

Unfortunately, revelations such as these have become all too common in the corporate world. It is no wonder that a survey of affluent investors reported that 85% of respondents believed that there should be tighter regulation of financial disclosures; 66% said they did not trust the management of publicly traded companies.

Why do so many companies violate basic financial reporting rules and sound ethics? Many speculate that executives are under increasing pressure to meet higher and higher earnings expectations. If actual results aren’t as good as hoped for, some give in to temptation and “adjust” their numbers to meet market expectations.

PREVIEW OF CHAPTER 3

In Chapter 1, you learned a neat little formula: . In Chapter 2, you learned some rules for recording revenue and expense transactions. Guess what? Things are not really that nice and neat. In fact, it is often difficult for companies to determine in what time period they should report some revenues and expenses. In other words, in measuring net income, timing is everything.

The content and organization of Chapter 3 are as follows.

The Navigator

The Navigator

Timing Issues

Learning Objective 1

Explain the time period assumption.

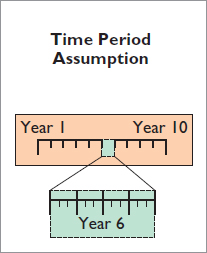

If we could wait to prepare financial statements until a company ended its operations, no adjustments would be needed. At that point, we could easily determine its final statement of financial position and the amount of lifetime income it earned.

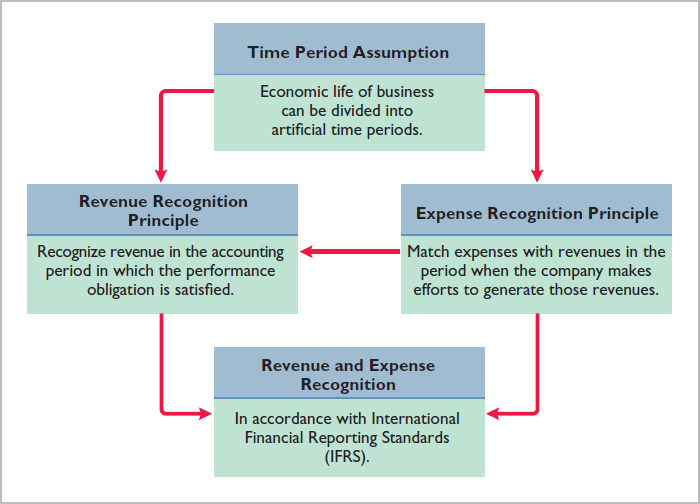

However, most companies need immediate feedback about how well they are doing. For example, management usually wants monthly financial statements, and taxing agencies require all businesses to file annual tax returns. Therefore, accountants divide the economic life of a business into artificial time periods. This convenient assumption is referred to as the time period assumption.

Many business transactions affect more than one of these arbitrary time periods. For example, the airplanes purchased by Cathay Pacific (HKG) five years ago are still in use today. We must determine the relevance of each business transaction to specific accounting periods. (How much of the cost of an airplane contributed to operations this year?)

Fiscal and Calendar Years

Both small and large companies prepare financial statements periodically in order to assess their financial condition and results of operations. Accounting time periods are generally a month, a quarter, or a year. Monthly and quarterly time periods are called interim periods. Most large companies must prepare both quarterly and annual financial statements.

An accounting time period that is one year in length is a fiscal year. A fiscal year usually begins with the first day of a month and ends 12 months later on the last day of a month. Many businesses use the calendar year (January 1 to December 31) as their accounting period. Some do not, such as Vodafone Group’s (GBR) fiscal year which ends March 31. Further, sometimes a company’s year-end will vary from year to year. For example, JJB Sports’ (GBR) fiscal year ends on the Sunday that falls closest before January 31, resulting in accounting periods of either 52 or 53 weeks.

• Alternative Terminology

The time period assumption is also called the periodicity assumption.

Accrual- versus Cash-Basis Accounting

Learning Objective 2

Explain the accrual basis of accounting.

What you will learn in this chapter is accrual-basis accounting. Under the accrual basis, companies record transactions that change a company’s financial statements in the periods in which the events occur. For example, using the accrual basis to determine net income means companies recognize revenues when they perform the services (rather than when they receive cash). It also means recognizing expenses when incurred (rather than when paid).

An alternative to the accrual basis is the cash basis. Under cash-basis accounting, companies record revenue when they receive cash. They record an expense when they pay out cash. The cash basis seems appealing due to its simplicity, but it often produces misleading financial statements. It fails to record revenue for a company that has performed services but for which the company has not received the cash. As a result, the cash basis does not match expenses with revenues.

Accrual-basis accounting is therefore in accordance with International Financial Reporting Standards (IFRS). Individuals and some small companies, however, do use cash-basis accounting. The cash basis is justified for small businesses because they often have few receivables and payables. Medium and large companies use accrual-basis accounting.

Recognizing Revenues and Expenses

It can be difficult to determine when to report revenues and expenses. The revenue recognition principle and the expense recognition principle help in this task.

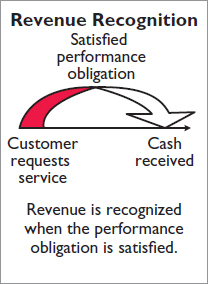

REVENUE RECOGNITION PRINCIPLE

When a company agrees to perform a service or sell a product to a customer, it has a performance obligation. When the company meets this performance obligation, it recognizes revenue. The revenue recognition principle therefore requires that companies recognize revenue in the accounting period in which the performance obligation is satisfied. To illustrate, assume that Soon’s Dry Cleaning cleans clothing on June 30, but customers do not claim and pay for their clothes until the first week of July. Soon’s should record revenue in June when it performed the service (satisfied the performance obligation) rather than in July when it received the cash. At June 30, Soon’s would report a receivable on its statement of financial position and revenue in its income statement for the service performed.

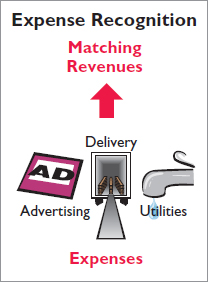

EXPENSE RECOGNITION PRINCIPLE

Accountants follow a simple rule in recognizing expenses: “Let the expenses follow the revenues.” Thus, expense recognition is tied to revenue recognition. In the dry cleaning example, this means that Soon’s should report the salary expense incurred in performing the June 30 cleaning service in the same period in which it recognizes the service revenue. The critical issue in expense recognition is when the expense makes its contribution to revenue. This may or may not be the same period in which the expense is paid. If Soon’s does not pay the salary incurred on June 30 until July, it would report salaries payable on its June 30 statement of financial position.

This practice of expense recognition is referred to as the expense recognition principle (often referred to as the matching principle). It dictates that efforts (expenses) be matched with results (revenues). Illustration 3-1 summarizes the revenue and expense recognition principles.

Illustration 3-1 IFRS relationships in revenue and expense recognition

• HELPFUL HINT

Recognize means to record or to report.

The Basics of Adjusting Entries

Learning Objective 3

Explain the reasons for adjusting entries.

In order for revenues to be recorded in the period in which services are performed, and for expenses to be recognized in the period in which they are incurred, companies make adjusting entries. Adjusting entries ensure that the revenue recognition and expense recognition principles are followed.

Adjusting entries are necessary because the trial balance—the first pulling together of the transaction data—may not contain up-to-date and complete data. This is true for several reasons:

- Some events are not recorded daily because it is not efficient to do so. Examples are the use of supplies and the earning of wages by employees.

- Some costs are not recorded during the accounting period because these costs expire with the passage of time rather than as a result of recurring daily transactions. Examples are charges related to the use of buildings and equipment, rent, and insurance.

- Some items may be unrecorded. An example is a utility service bill that will not be received until the next accounting period.

Adjusting entries are required every time a company prepares financial statements. The company analyzes each account in the trial balance to determine whether it is complete and up-to-date for financial statement purposes. Every adjusting entry will include one income statement account and one statement of financial position account.

Types of Adjusting Entries

Learning Objective 4

Identify the major types of adjusting entries.

Adjusting entries are classified as either deferrals or accruals. As Illustration 3-2 shows, each of these classes has two subcategories.

Illustration 3-2 Categories of adjusting entries

Subsequent sections give examples of each type of adjustment. Each example is based on the October 31 trial balance of Yazici Advertising A.Ş. from Chapter 2, reproduced in Illustration 3-3.

Illustration 3-3 Trial balance

| YAZICI ADVERTISING A.Ş. Trial Balance October 31, 2017 |

||

| Debit | Credit | |

| Cash | ||

| Supplies | 2,500 |

|

| Prepaid Insurance | 600 |

|

| Equipment | 5,000 |

|

| Notes Payable | ||

| Accounts Payable | 2,500 |

|

| Unearned Service Revenue | 1,200 |

|

| Share Capital—Ordinary | 10,000 |

|

| Retained Earnings | –0– |

|

| Dividends | 500 |

|

| Service Revenue | 10,000 |

|

| Salaries and Wages Expense | 4,000 |

|

| Rent Expense | 900 |

|

We assume that Yazici uses an accounting period of one month. Thus, monthly adjusting entries are made. The entries are dated October 31.

Adjusting Entries for Deferrals

Learning Objective 5

Prepare adjusting entries for deferrals.

To defer means to postpone or delay. Deferrals are expenses or revenues that are recognized at a date later than the point when cash was originally exchanged. Companies make adjusting entries for deferrals to record the portion of the deferred item that was incurred as an expense or recognized as revenue during the current accounting period. The two types of deferrals are prepaid expenses and unearned revenues.

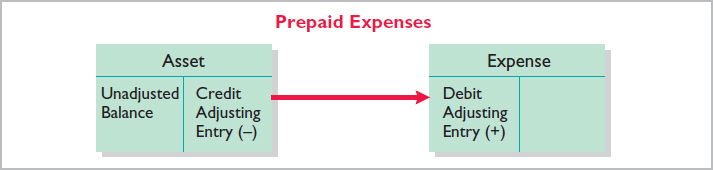

PREPAID EXPENSES

When companies record payments of expenses that will benefit more than one accounting period, they record an asset called prepaid expenses or prepayments. When expenses are prepaid, an asset account is increased (debited) to show the service or benefit that the company will receive in the future. Examples of common prepayments are insurance, supplies, advertising, and rent. In addition, companies make prepayments when they purchase buildings and equipment.

Prepaid expenses are costs that expire either with the passage of time (e.g., rent and insurance) or through use (e.g., supplies). The expiration of these costs does not require daily entries, which would be impractical and unnecessary. Accordingly, companies postpone the recognition of such cost expirations until they prepare financial statements. At each statement date, they make adjusting entries to record the expenses applicable to the current accounting period and to show the remaining amounts in the asset accounts.

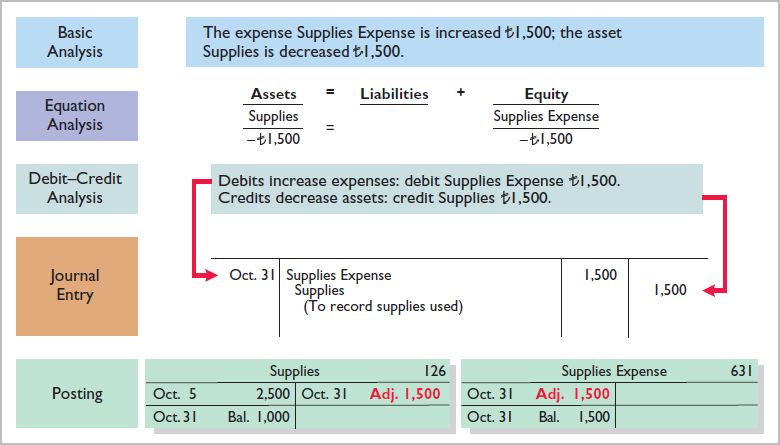

Prior to adjustment, assets are overstated and expenses are understated. Therefore, as shown in Illustration 3-4, an adjusting entry for prepaid expenses results in an increase (a debit) to an expense account and a decrease (a credit) to an asset account.

Illustration 3-4 Adjusting entries for prepaid expenses

Let’s look in more detail at some specific types of prepaid expenses, beginning with supplies.

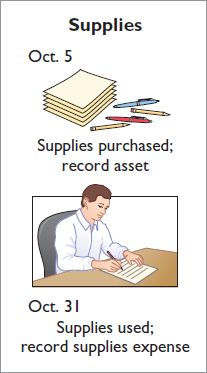

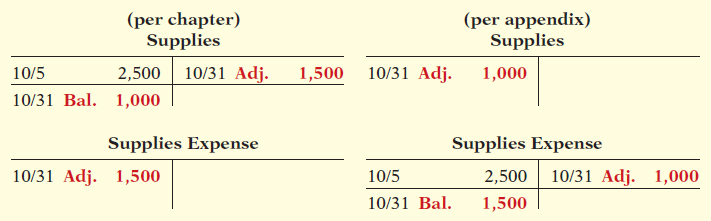

SUPPLIES The purchase of supplies, such as paper and envelopes, results in an increase (a debit) to an asset account. During the accounting period, the company uses supplies. Rather than record supplies expense as the supplies are used, companies recognize supplies expense at the end of the accounting period. At the end of the accounting period, the company counts the remaining supplies. The difference between the unadjusted balance in the Supplies (asset) account and the actual cost of supplies on hand represents the supplies used (an expense) for that period.

Recall from Chapter 2 that Yazici Advertising purchased supplies costing ![]() 2,500 on October 5. Yazici recorded the purchase by increasing (debiting) the asset Supplies. This account shows a balance of

2,500 on October 5. Yazici recorded the purchase by increasing (debiting) the asset Supplies. This account shows a balance of ![]() 2,500 in the October 31 trial balance. An inventory count at the close of business on October 31 reveals that

2,500 in the October 31 trial balance. An inventory count at the close of business on October 31 reveals that ![]() 1,000 of supplies are still on hand. Thus, the cost of supplies used is

1,000 of supplies are still on hand. Thus, the cost of supplies used is ![]() 1,500 (

1,500 (![]() 2,500 −

2,500 − ![]() 1,000). This use of supplies decreases an asset, Supplies. It also decreases equity by increasing an expense account, Supplies Expense. This is shown in Illustration 3-5.

1,000). This use of supplies decreases an asset, Supplies. It also decreases equity by increasing an expense account, Supplies Expense. This is shown in Illustration 3-5.

Illustration 3-5 Adjustment for supplies

After adjustment, the asset account Supplies shows a balance of ![]() 1,000, which is equal to the cost of supplies on hand at the statement date. In addition, Supplies Expense shows a balance of

1,000, which is equal to the cost of supplies on hand at the statement date. In addition, Supplies Expense shows a balance of ![]() 1,500, which equals the cost of supplies used in October. If Yazici does not make the adjusting entry, October expenses are understated and net income is overstated by

1,500, which equals the cost of supplies used in October. If Yazici does not make the adjusting entry, October expenses are understated and net income is overstated by ![]() 1,500. Moreover, both assets and equity will be overstated by

1,500. Moreover, both assets and equity will be overstated by ![]() 1,500 on the October 31 statement of financial position.

1,500 on the October 31 statement of financial position.

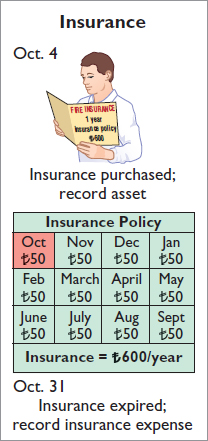

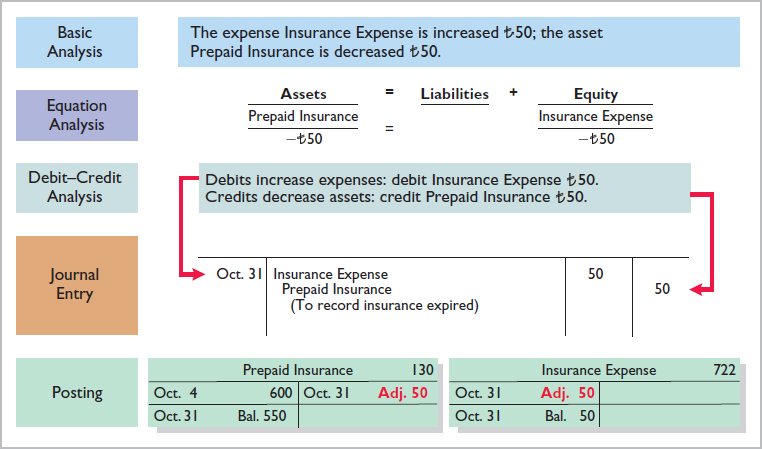

INSURANCE Companies purchase insurance to protect themselves from losses due to fire, theft, and unforeseen events. Insurance must be paid in advance, often for more than one year. The cost of insurance (premiums) paid in advance is recorded as an increase (debit) in the asset account Prepaid Insurance. At the financial statement date, companies increase (debit) Insurance Expense and decrease (credit) Prepaid Insurance for the cost of insurance that has expired during the period.

On October 4, Yazici Advertising paid ![]() 600 for a one-year fire insurance policy. Coverage began on October 1. Yazici recorded the payment by increasing (debiting) Prepaid Insurance. This account shows a balance of

600 for a one-year fire insurance policy. Coverage began on October 1. Yazici recorded the payment by increasing (debiting) Prepaid Insurance. This account shows a balance of ![]() 600 in the October 31 trial balance. Insurance of

600 in the October 31 trial balance. Insurance of ![]() 50 (

50 (![]() 600 ÷ 12) expires each month. The expiration of prepaid insurance decreases an asset, Prepaid Insurance. It also decreases equity by increasing an expense account, Insurance Expense.

600 ÷ 12) expires each month. The expiration of prepaid insurance decreases an asset, Prepaid Insurance. It also decreases equity by increasing an expense account, Insurance Expense.

As shown in Illustration 3-6 (page 108), the asset Prepaid Insurance shows a balance of 550, which represents the unexpired cost for the remaining 11 months of coverage. At the same time, the balance in Insurance Expense equals the insurance cost that expired in October. If Yazici does not make this adjustment, October expenses are understated by ![]() 50 and net income is overstated by

50 and net income is overstated by ![]() 50. Moreover, both assets and equity will be overstated by 50 on the October 31 statement of financial position.

50. Moreover, both assets and equity will be overstated by 50 on the October 31 statement of financial position.

Illustration 3-6 Adjustment for insurance

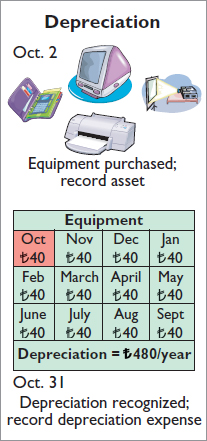

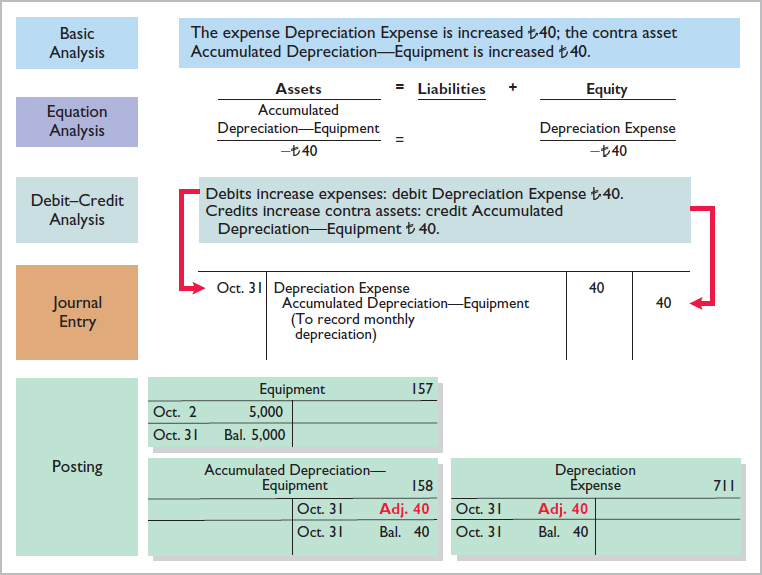

DEPRECIATION A company typically owns a variety of assets that have long lives, such as buildings, equipment, and motor vehicles. The period of service is referred to as the useful life of the asset. Because a building is expected to be of service for many years, it is recorded as an asset, rather than an expense, on the date it is acquired. As explained in Chapter 1, companies record such assets at cost, as required by the historical cost principle. To follow the expense recognition principle, companies allocate a portion of this cost as an expense during each period of the asset’s useful life. Depreciation is the process of allocating the cost of an asset to expense over its useful life.

Need for Adjustment. The acquisition of long-lived assets is essentially a long-term prepayment for the use of an asset. An adjusting entry for depreciation is needed to recognize the cost that has been used (an expense) during the period and to report the unused cost (an asset) at the end of the period. One very important point to understand: Depreciation is an allocation concept, not a valuation concept. That is, depreciation allocates an asset’s cost to the periods in which it is used. Depreciation does not attempt to report the actual change in the value of the asset.

For Yazici Advertising, assume that depreciation on the equipment is ![]() 480 a year, or

480 a year, or ![]() 40 per month. As shown in Illustration 3-7 on the next page, rather than decrease (credit) the asset account directly, Yazici instead credits Accumulated Depreciation—Equipment. Accumulated Depreciation is called a contra asset account. Such an account is offset against an asset account on the statement of financial position. Thus, the Accumulated Depreciation—Equipment account offsets the asset account Equipment. This account keeps track of the total amount of depreciation expense taken over the life of the asset. To keep the accounting equation in balance, Yazici decreases equity by increasing an expense account, Depreciation Expense.

40 per month. As shown in Illustration 3-7 on the next page, rather than decrease (credit) the asset account directly, Yazici instead credits Accumulated Depreciation—Equipment. Accumulated Depreciation is called a contra asset account. Such an account is offset against an asset account on the statement of financial position. Thus, the Accumulated Depreciation—Equipment account offsets the asset account Equipment. This account keeps track of the total amount of depreciation expense taken over the life of the asset. To keep the accounting equation in balance, Yazici decreases equity by increasing an expense account, Depreciation Expense.

Illustration 3-7 Adjustment for depreciation

The balance in the Accumulated Depreciation—Equipment account will increase ![]() 40 each month, and the balance in Equipment remains

40 each month, and the balance in Equipment remains ![]() 5,000.

5,000.

Statement Presentation. As indicated, Accumulated Depreciation—Equipment is a contra asset account. It is offset against Equipment on the statement of financial position. The normal balance of a contra asset account is a credit. A theoretical alternative to using a contra asset account would be to decrease (credit) the asset account by the amount of depreciation each period. But using the contra account is preferable for a simple reason: It discloses both the original cost of the equipment and the total cost that has been expensed to date. Thus, in the statement of financial position, Yazici deducts Accumulated Depreciation—Equipment from the related asset account, as shown in Illustration 3-8.

• HELPFUL HINT

All contra accounts have increases, decreases, and normal balances opposite to the account to which they relate.

Illustration 3-8 Statement of financial position presentation of accumulated depreciation

| Equipment | |

| Less: Accumulated depreciation—equipment | 40 |

• Alternative Terminology Book value is also referred to as carrying value.

Book value is the difference between the cost of any depreciable asset and its related accumulated depreciation. In Illustration 3-8, the book value of the equipment at the statement of financial position date is ![]() 4,960. The book value and the fair value of the asset are generally two different values. As noted earlier, the purpose of depreciation is not valuation but a means of cost allocation.

4,960. The book value and the fair value of the asset are generally two different values. As noted earlier, the purpose of depreciation is not valuation but a means of cost allocation.

Depreciation expense identifies the portion of an asset’s cost that expired during the period (in this case, in October). Without this adjusting entry, assets, equity, and net income are overstated by ![]() 40 and depreciation expense is understated by

40 and depreciation expense is understated by ![]() 40.

40.

Illustration 3-9 summarizes the accounting for prepaid expenses.

Illustration 3-9 Accounting for prepaid expenses

| ACCOUNTING FOR PREPAID EXPENSES | |||

| Examples | Reason for Adjustment | Accounts Before Adjustment | Adjusting Entry |

| Insurance, supplies, advertising, rent, depreciation | Prepaid expenses recorded in asset accounts have been used. | Assets overstated. Expenses understated. | Dr. Expenses Cr. Assets or Contra Assets |

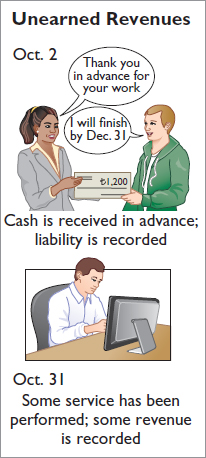

UNEARNED REVENUES

When companies receive cash before services are performed, they record a liability by increasing (crediting) a liability account called unearned revenue. In other words, a company now has a performance obligation (liability) to perform a service for one of its customers. Items like rent, magazine subscriptions, and customer deposits for future service may result in unearned revenues. Airlines such as Ryanair (IRL), Qatar Airways (QAT), and Singapore Airlines (SGP), for instance, treat receipts from the sale of tickets as unearned revenue until the flight service is provided.

Unearned revenues are the opposite of prepaid expenses. Indeed, unearned revenue on the books of one company is likely to be a prepaid expense on the books of the company that has made the advance payment. For example, if identical accounting periods are assumed, a landlord will have unearned rent revenue when a tenant has prepaid rent.

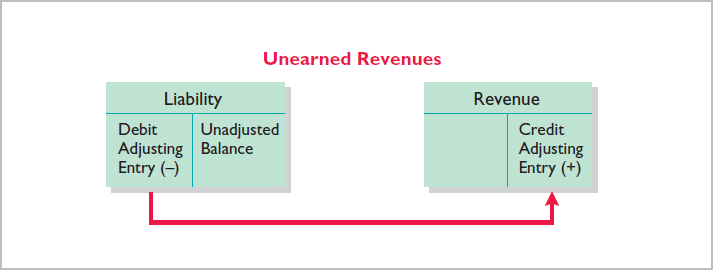

When a company receives payment for services to be performed in a future accounting period, it increases (credits) an unearned revenue (a liability) account to recognize the liability that exists. The company subsequently recognizes revenues when it performs the service. During the accounting period, it is not practical to make daily entries as the company performs services. Instead, the company delays recognition of revenue until the adjustment process. Then, the company makes an adjusting entry to record the revenue for services performed during the period and to show the liability that remains at the end of the accounting period. Typically, prior to adjustment, liabilities are overstated and revenues are understated. Therefore, as shown in Illustration 3-10, the adjusting entry for unearned revenues results in a decrease (a debit) to a liability account and an increase (a credit) to a revenue account.

Illustration 3-10 Adjusting entries for unearned revenues

• Alternative Terminology

Unearned revenue is sometimes referred to as deferred revenue.

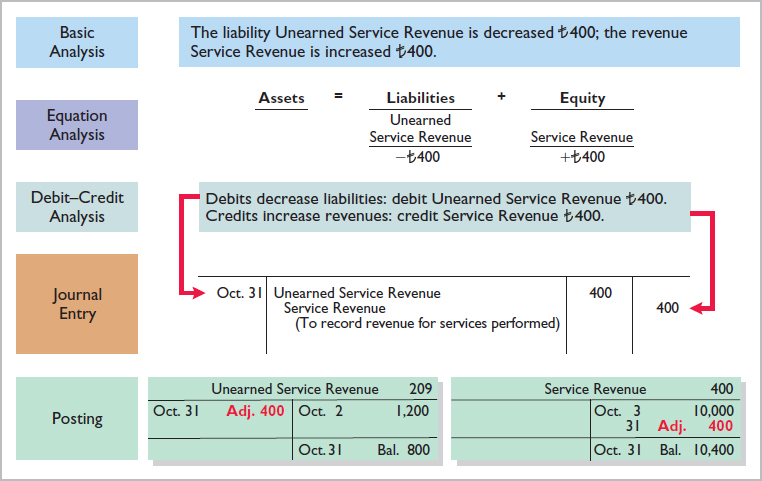

Yazici Advertising received ![]() 1,200 on October 2 from R. Knox for advertising services expected to be completed by December 31. Yazici credited the payment to Unearned Service Revenue. This liability account shows a balance of

1,200 on October 2 from R. Knox for advertising services expected to be completed by December 31. Yazici credited the payment to Unearned Service Revenue. This liability account shows a balance of ![]() 1,200 in the October 31 trial balance. From an evaluation of the services Yazici performed for Knox during October, the company determines that it should recognize

1,200 in the October 31 trial balance. From an evaluation of the services Yazici performed for Knox during October, the company determines that it should recognize ![]() 400 of revenue in October. The liability (Unearned Service Revenue) is therefore decreased, and equity (Service Revenue) is increased.

400 of revenue in October. The liability (Unearned Service Revenue) is therefore decreased, and equity (Service Revenue) is increased.

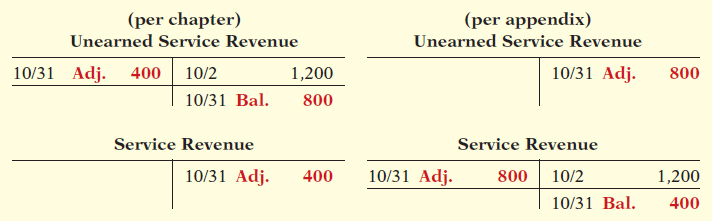

As shown in Illustration 3-11, the liability Unearned Service Revenue now shows a balance of ![]() 800. That amount represents the remaining advertising services expected to be performed in the future. At the same time, Service Revenue shows total revenue recognized in October of

800. That amount represents the remaining advertising services expected to be performed in the future. At the same time, Service Revenue shows total revenue recognized in October of ![]() 10,400. Without this adjustment, revenues and net income are understated by

10,400. Without this adjustment, revenues and net income are understated by ![]() 400. Moreover, liabilities are overstated and equity is understated by

400. Moreover, liabilities are overstated and equity is understated by ![]() 400 on the October 31 statement of financial position.

400 on the October 31 statement of financial position.

Illustration 3-11 Service revenue accounts after adjustment

Illustration 3-12 summarizes the accounting for unearned revenues.

Illustration 3-12 Accounting for unearned revenues

| ACCOUNTING FOR UNEARNED REVENUES | |||

| Examples | Reason for Adjustment | Accounts Before Adjustment | Adjusting Entry |

| Rent, magazine subscriptions, customer deposits for future service | Unearned revenues recorded in liability accounts are now recognized as revenue for services performed. | Liabilities overstated. Revenues understated. | Dr. Liabilities Cr. Revenues |

Adjusting Entries for Accruals

Learning Objective 6

Prepare adjusting entries for accruals.

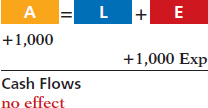

The second category of adjusting entries is accruals. Prior to an accrual adjustment, the revenue account (and the related asset account) or the expense account (and the related liability account) are understated. Thus, the adjusting entry for accruals will increase both a statement of financial position and an income statement account.

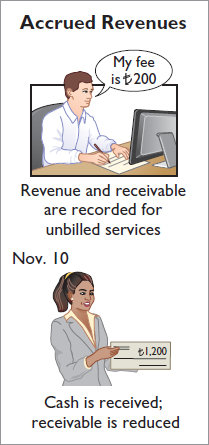

ACCRUED REVENUES

Revenues for services performed but not yet recorded at the statement date are accrued revenues. Accrued revenues may accumulate (accrue) with the passing of time, as in the case of interest revenue. These are unrecorded because the earning of interest does not involve daily transactions. Companies do not record interest revenue on a daily basis because it is often impractical to do so. Accrued revenues also may result from services that have been performed but not yet billed or collected, as in the case of commissions and fees. These may be unrecorded because only a portion of the total service has been performed and the clients will not be billed until the service has been completed.

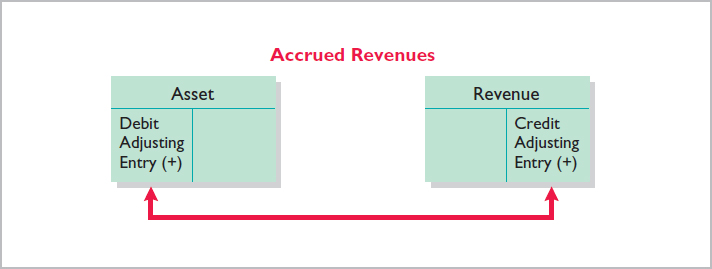

An adjusting entry records the receivable that exists at the statement of financial position date and the revenue for the services performed during the period. Prior to adjustment, both assets and revenues are understated. As shown in Illustration 3-13, an adjusting entry for accrued revenues results in an increase (a debit) to an asset account and an increase (a credit) to a revenue account.

Illustration 3-13 Adjusting entries for accrued revenues

• HELPFUL HINT

For accruals, there may have been no prior entry, and the accounts requiring adjustment may both have zero balances prior to adjustment.

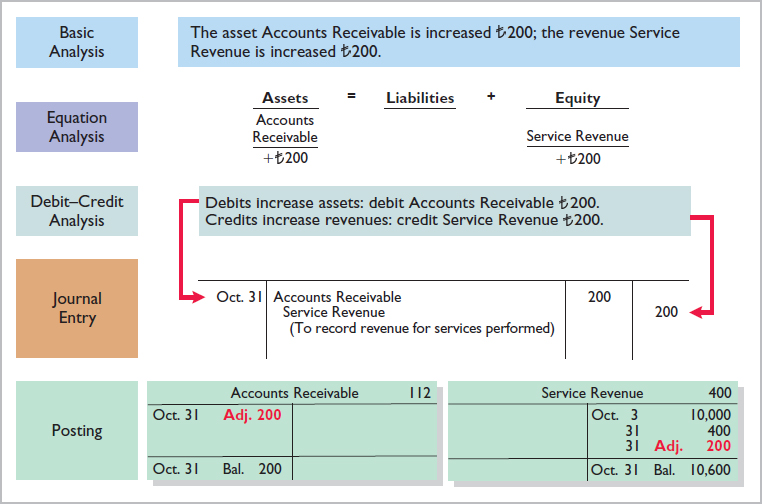

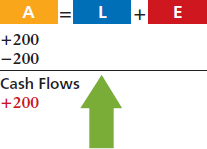

In October, Yazici Advertising performed services worth ![]() 200 that were not billed to clients on or before October 31. Because these services are not billed, they are not recorded. The accrual of unrecorded service revenue increases an asset account, Accounts Receivable. It also increases equity by increasing a revenue account, Service Revenue, as shown in Illustration 3-14.

200 that were not billed to clients on or before October 31. Because these services are not billed, they are not recorded. The accrual of unrecorded service revenue increases an asset account, Accounts Receivable. It also increases equity by increasing a revenue account, Service Revenue, as shown in Illustration 3-14.

Illustration 3-14 Adjustment for accrued revenue

The asset Accounts Receivable shows that clients owe Yazici ![]() 200 at the statement of financial position date. The balance of

200 at the statement of financial position date. The balance of ![]() 10,600 in Service Revenue represents the total revenue for services performed by Yazici during the month (

10,600 in Service Revenue represents the total revenue for services performed by Yazici during the month (![]() 10,000 +

10,000 + ![]() 400 +

400 + ![]() 200). Without the adjusting entry, assets and equity on the statement of financial position and revenues and net income on the income statement are understated.

200). Without the adjusting entry, assets and equity on the statement of financial position and revenues and net income on the income statement are understated.

On November 10, Yazici receives cash of ![]() 200 for the services performed in October and makes the following entry.

200 for the services performed in October and makes the following entry.

The company records the collection of the receivables by a debit (increase) to Cash and a credit (decrease) to Accounts Receivable.

Illustration 3-15 summarizes the accounting for accrued revenues.

Illustration 3-15 Accounting for accrued revenues

| ACCOUNTING FOR ACCRUED REVENUES | |||

| Examples | Reason for Adjustment | Accounts Before Adjustment | Adjusting Entry |

| Interest, rent, services performed but not collected | Services performed but not yet recorded. | Assets understated. Revenues understated. | Dr. Assets Cr. Revenues |

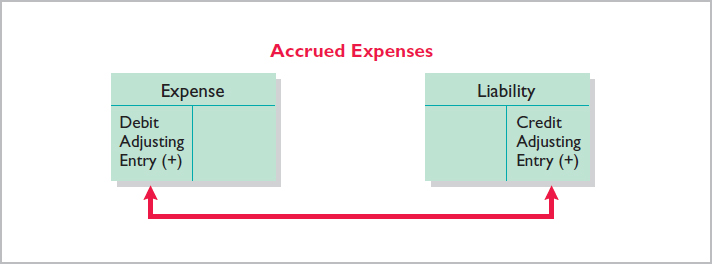

ACCRUED EXPENSES

Expenses incurred but not yet paid or recorded at the statement date are called accrued expenses. Interest, taxes, and salaries are common examples of accrued expenses.

Companies make adjustments for accrued expenses to record the obligations that exist at the statement of financial position date and to recognize the expenses that apply to the current accounting period. Prior to adjustment, both liabilities and expenses are understated. Therefore, as Illustration 3-16 shows, an adjusting entry for accrued expenses results in an increase (a debit) to an expense account and an increase (a credit) to a liability account.

Illustration 3-16 Adjusting entries for accrued expenses

Let’s look in more detail at some specific types of accrued expenses, beginning with accrued interest.

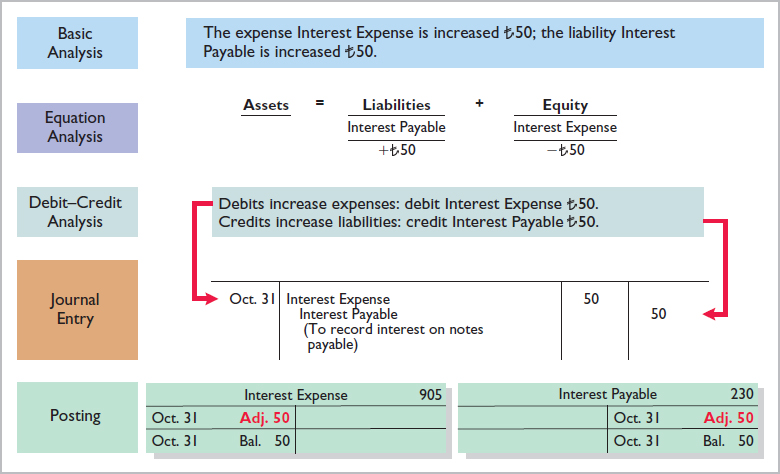

ACCRUED INTEREST Yazici Advertising signed a three-month note payable in the amount of ![]() 5,000 on October 1. The note requires Yazici to pay interest at an annual rate of 12%.

5,000 on October 1. The note requires Yazici to pay interest at an annual rate of 12%.

The amount of the interest recorded is determined by three factors: (1) the face value of the note; (2) the interest rate, which is always expressed as an annual rate; and (3) the length of time the note is outstanding. For Yazici, the total interest due on the ![]() 5,000 note at its maturity date three months in the future is

5,000 note at its maturity date three months in the future is ![]() 150 (

150 (![]() 5,000 × 12% × ), or

5,000 × 12% × ), or ![]() 50 for one month. Illustration 3-17 shows the formula for computing interest and its application to Yazici for the month of October.

50 for one month. Illustration 3-17 shows the formula for computing interest and its application to Yazici for the month of October.

Illustration 3-17 Formula for computing interest

• HELPFUL HINT

In computing interest, we express the time period as a fraction of a year.

As Illustration 3-18 (page 116) shows, the accrual of interest at October 31 increases a liability account, Interest Payable. It also decreases equity by increasing an expense account, Interest Expense.

Illustration 3-18 Adjustment for accrued interest

Interest Expense shows the interest charges for the month of October. Interest Payable shows the amount of interest the company owes at the statement date. Yazici will not pay the interest until the note comes due at the end of three months. Companies use the Interest Payable account, instead of crediting Notes Payable, to disclose the two different types of obligations—interest and principal—in the accounts and statements. Without this adjusting entry, liabilities and interest expense are understated, and net income and equity are overstated.

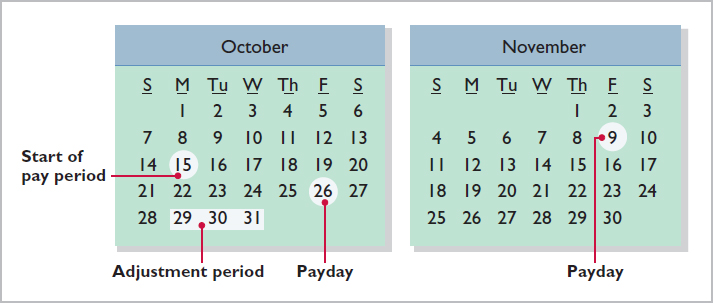

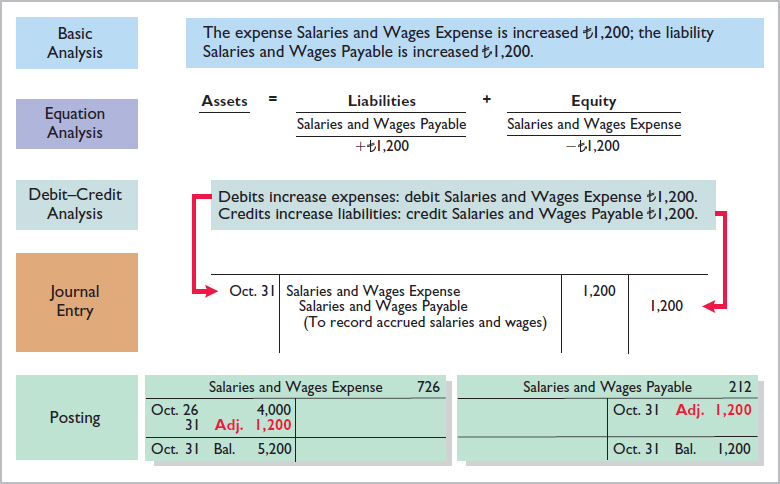

ACCRUED SALARIES AND WAGES Companies pay for some types of expenses, such as employee salaries and wages, after the services have been performed. Yazici paid salaries and wages on October 26 for its employees’ first two weeks of work. The next payment of salaries will not occur until November 9. As Illustration 3-19 shows, three working days remain in October (October 29–31).

Illustration 3-19 Calendar showing Yazici’s pay periods

At October 31, the salaries and wages for these three days represent an accrued expense and a related liability to Yazici. The employees receive total salaries and wages of ![]() 2,000 for a five-day work week, or

2,000 for a five-day work week, or ![]() 400 per day. Thus, accrued salaries and wages at October 31 are

400 per day. Thus, accrued salaries and wages at October 31 are ![]() 1,200 (

1,200 (![]() 400 × 3). This accrual increases a liability, Salaries and Wages Payable. It also decreases equity by increasing an expense account, Salaries and Wages Expense, as shown in Illustration 3-20.

400 × 3). This accrual increases a liability, Salaries and Wages Payable. It also decreases equity by increasing an expense account, Salaries and Wages Expense, as shown in Illustration 3-20.

Illustration 3-20 Adjustment for accrued salaries and wages

After this adjustment, the balance in Salaries and Wages Expense of ![]() 5,200 (13 days ×

5,200 (13 days × ![]() 400) is the actual salary and wages expense for October. The balance in Salaries and Wages Payable of

400) is the actual salary and wages expense for October. The balance in Salaries and Wages Payable of ![]() 1,200 is the amount of the liability for salaries and wages Yazici owes as of October 31. Without the

1,200 is the amount of the liability for salaries and wages Yazici owes as of October 31. Without the ![]() 1,200 adjustment for salaries and wages, Yazici’s expenses are understated

1,200 adjustment for salaries and wages, Yazici’s expenses are understated ![]() 1,200 and its liabilities are understated

1,200 and its liabilities are understated ![]() 1,200.

1,200.

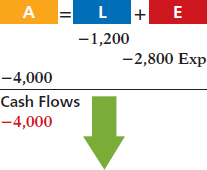

Yazici pays salaries and wages every two weeks. Consequently, the next payday is November 9, when the company will again pay total salaries and wages of ![]() 4,000. The payment consists of

4,000. The payment consists of ![]() 1,200 of salaries and wages payable at October 31 plus

1,200 of salaries and wages payable at October 31 plus ![]() 2,800 of salaries and wages expense for November (7 working days, as shown in the November calendar ×

2,800 of salaries and wages expense for November (7 working days, as shown in the November calendar × ![]() 400). Therefore, Yazici makes the following entry on November 9.

400). Therefore, Yazici makes the following entry on November 9.

This entry eliminates the liability for Salaries and Wages Payable that Yazici recorded in the October 31 adjusting entry, and it records the proper amount of Salaries and Wages Expense for the period between November 1 and November 9.

Illustration 3-21 summarizes the accounting for accrued expenses.

Illustration 3-21 Accounting for accrued expenses

| ACCOUNTING FOR ACCRUED EXPENSES | |||

| Examples | Reason for Adjustment | Accounts Before Adjustment | Adjusting Entry |

| Interest, rent, salaries | Expenses have been incurred but not yet paid in cash or recorded. | Expenses understated. Liabilities understated. | Dr. Expenses Cr. Liabilities |

Summary of Basic Relationships

Illustration 3-22 summarizes the four basic types of adjusting entries. Take some time to study and analyze the adjusting entries. Be sure to note that each adjusting entry affects one statement of financial position account and one income statement account.

Illustration 3-22 Summary of adjusting entries

| Type of Adjustment | Accounts Before Adjustment | Adjusting Entry |

| Prepaid expenses | Assets overstated. Expenses understated. |

Dr. Expenses Cr. Assets or Contra Assets |

| Unearned revenues | Liabilities overstated. Revenues understated. |

Dr. Liabilities Cr. Revenues |

| Accrued revenues | Assets understated. Revenues understated. |

Dr. Assets Cr. Revenues |

| Accrued expenses | Expenses understated. Liabilities understated. |

Dr. Expenses Cr. Liabilities |

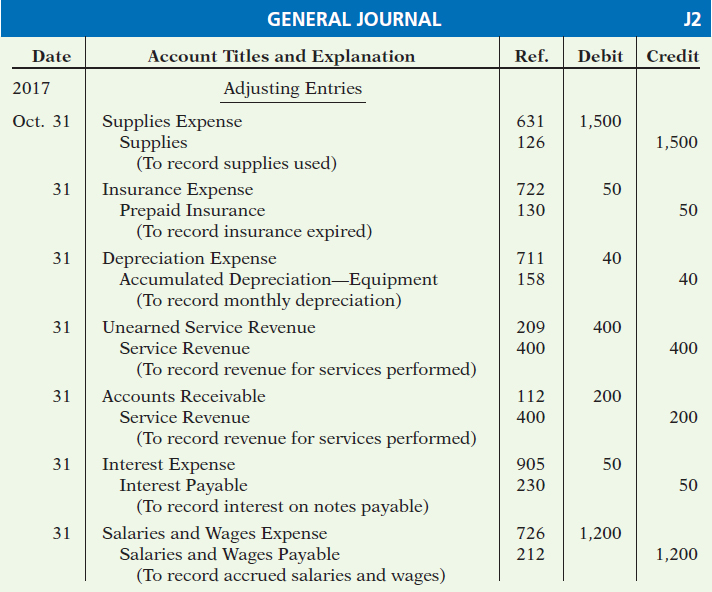

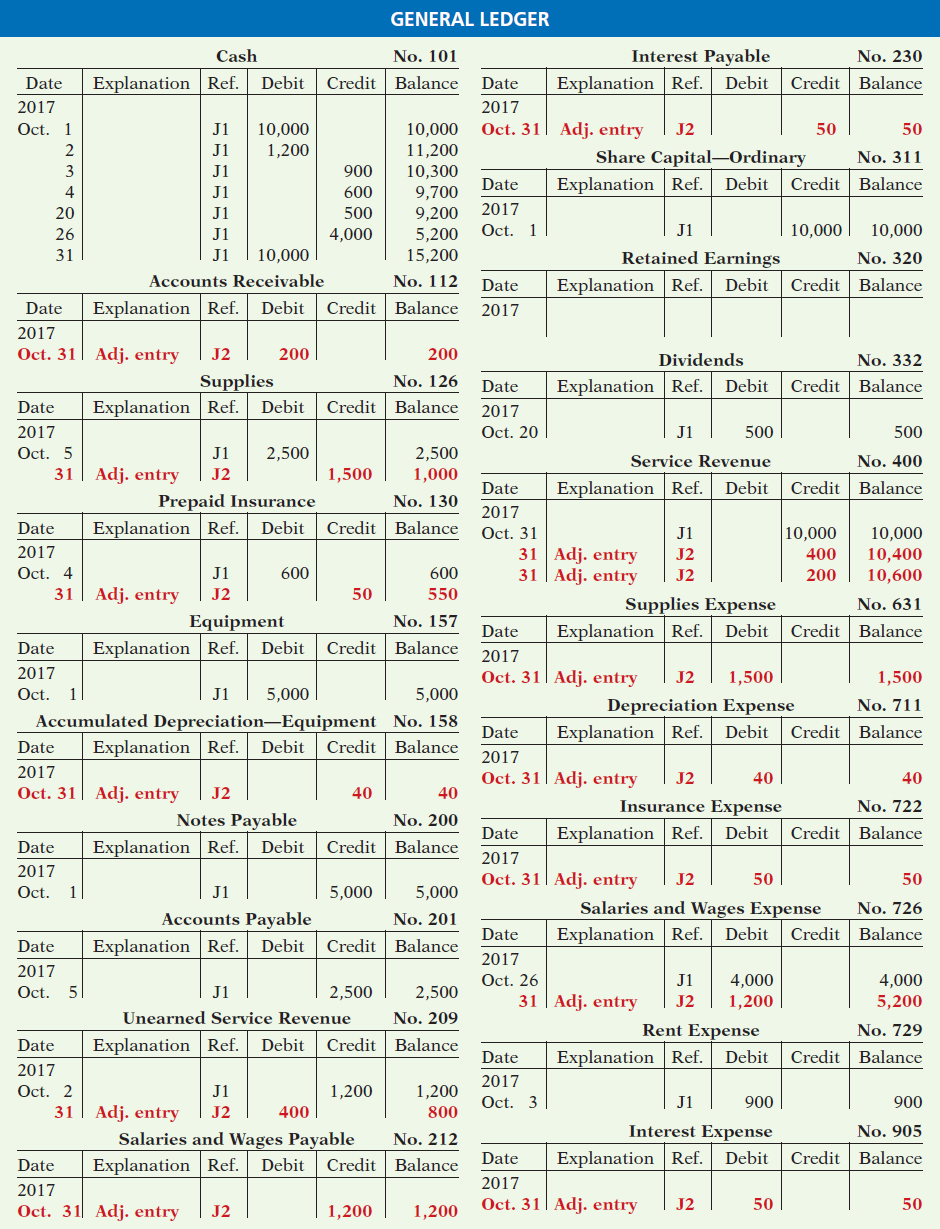

Illustrations 3-23 (below) and 3-24 (on page 120) show the journalizing and posting of adjusting entries for Yazici Advertising A.Ş. on October 31. The ledger identifies all adjustments by the reference J2 because they have been recorded on page 2 of the general journal. The company may insert a center caption “Adjusting Entries” between the last transaction entry and the first adjusting entry in the journal. When you review the general ledger in Illustration 3-24, note that the entries highlighted in red are the adjustments.

Illustration 3-23 General journal showing adjusting entries

• HELPFUL HINT

- Adjusting entries should not involve debits or credits to cash.

- Evaluate whether the adjustment makes sense. For example, an adjustment to recognize supplies used should increase supplies expense.

- Double-check all computations.

- Each adjusting entry affects one statement of financial position account and one income statement account.

Illustration 3-24 General ledger after adjustment

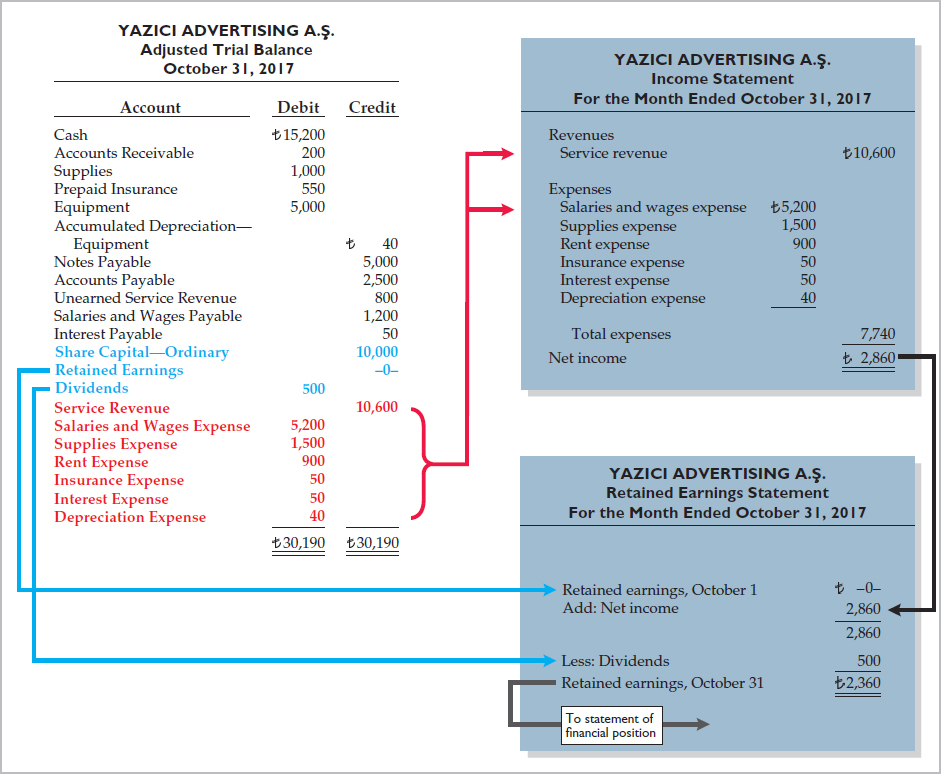

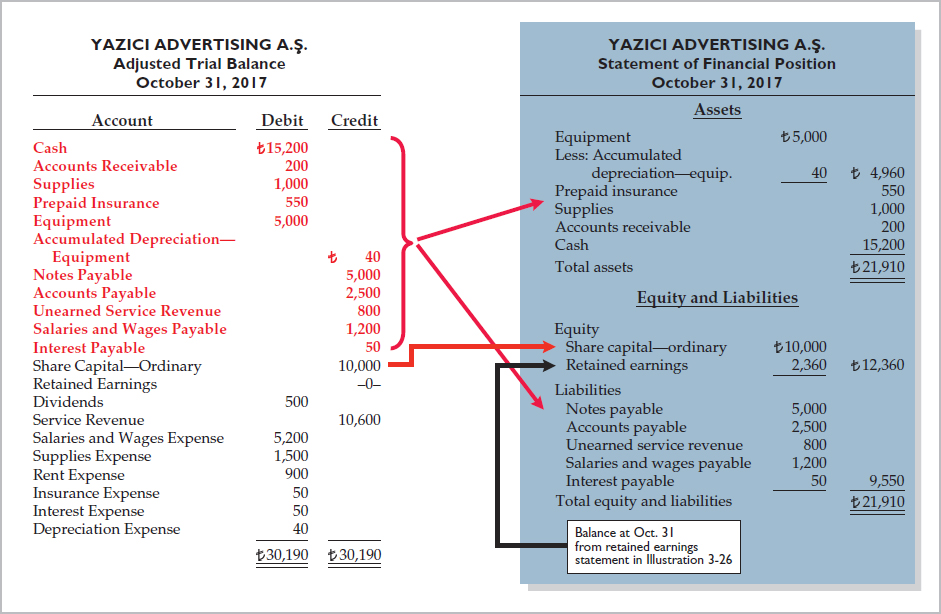

The Adjusted Trial Balance and Financial Statements

Learning Objective 7

Describe the nature and purpose of an adjusted trial balance.

After a company has journalized and posted all adjusting entries, it prepares another trial balance from the ledger accounts. This trial balance is called an adjusted trial balance. It shows the balances of all accounts, including those adjusted, at the end of the accounting period. The purpose of an adjusted trial balance is to prove the equality of the total debit balances and the total credit balances in the ledger after all adjustments. Because the accounts contain all data needed for financial statements, the adjusted trial balance is the primary basis for the preparation of financial statements.

Preparing the Adjusted Trial Balance

Illustration 3-25 presents the adjusted trial balance for Yazici Advertising prepared from the ledger accounts in Illustration 3-24. The amounts affected by the adjusting entries are highlighted in red. Compare these amounts to those in the unadjusted trial balance in Illustration 3-3 on page 105. In this comparison, you will see that there are more accounts in the adjusted trial balance as a result of the adjusting entries made at the end of the month.

Illustration 3-25 Adjusted trial balance

| YAZICI ADVERTISING A.Ş. Adjusted Trial Balance October 31, 2017 |

||

| Debit | Credit | |

| Cash | ||

| Accounts Receivable | 200 |

|

| Supplies | 1,000 |

|

| Prepaid Insurance | 550 |

|

| Equipment | 5,000 |

|

| Accumulated Depreciation—Equipment | ||

| Notes Payable | 5,000 |

|

| Accounts Payable | 2,500 |

|

| Interest Payable | 50 |

|

| Unearned Service Revenue | 800 |

|

| Salaries and Wages Payable | 1,200 |

|

| Share Capital—Ordinary | 10,000 |

|

| Retained Earnings | –0– |

|

| Dividends | 500 |

|

| Service Revenue | 10,600 |

|

| Salaries and Wages Expense | 5,200 |

|

| Supplies Expense | 1,500 |

|

| Rent Expense | 900 |

|

| Insurance Expense | 50 |

|

| Interest Expense | 50 |

|

| Depreciation Expense | 40 |

|

Preparing Financial Statements

Companies can prepare financial statements directly from the adjusted trial balance. Illustrations 3-26 and 3-27 present the interrelationships of data in the adjusted trial balance and the financial statements.

Illustration 3-26 Preparation of the income statement and retained earnings statement from the adjusted trial balance

Illustration 3-27 Preparation of the statement of financial position from the adjusted trial balance

As Illustration 3-26 shows, companies prepare the income statement from the revenue and expense accounts. Next, they use the Retained Earnings and Dividends accounts and the net income (or net loss) from the income statement to prepare the retained earnings statement. As Illustration 3-27 shows, companies then prepare the statement of financial position from the asset and liability accounts and the ending retained earnings balance as reported in the retained earnings statement.

APPENDIX 3A Alternative Treatment of Prepaid Expenses and Unearned Revenues

Learning Objective *8

Prepare adjusting entries for the alternative treatment of deferrals.

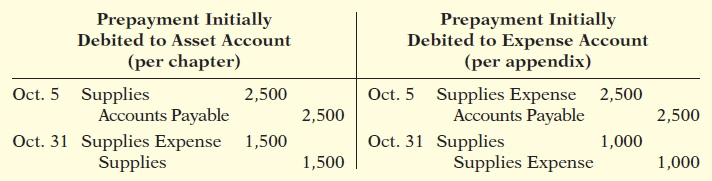

In discussing adjusting entries for prepaid expenses and unearned revenues, we illustrated transactions for which companies made the initial entries to statement of financial position accounts. In the case of prepaid expenses, the company debited the prepayment to an asset account. In the case of unearned revenues, the company credited a liability account to record the cash received.

Some companies use an alternative treatment: (1) When a company prepays an expense, it debits that amount to an expense account. (2) When it receives payment for future services, it credits the amount to a revenue account. In this appendix, we describe the circumstances that justify such entries and the different adjusting entries that may be required. This alternative treatment of prepaid expenses and unearned revenues has the same effect on the financial statements as the procedures described in the chapter.

Prepaid Expenses

Prepaid expenses become expired costs either through the passage of time (e.g., insurance) or through consumption (e.g., advertising supplies). If, at the time of purchase, the company expects to consume the supplies before the next financial statement date, it may choose to debit (increase) an expense account rather than an asset account. This alternative treatment is simply more convenient.

Assume that Yazici Advertising A.Ş. expects that it will use before the end of the month all of the supplies purchased on October 5. A debit of ![]() 2,500 to Supplies Expense (rather than to the asset account Supplies) on October 5 will eliminate the need for an adjusting entry on October 31. At October 31, the Supplies Expense account will show a balance of

2,500 to Supplies Expense (rather than to the asset account Supplies) on October 5 will eliminate the need for an adjusting entry on October 31. At October 31, the Supplies Expense account will show a balance of ![]() 2,500, which is the cost of supplies used between October 5 and October 31.

2,500, which is the cost of supplies used between October 5 and October 31.

But what if the company does not use all the supplies? For example, what if an inventory of ![]() 1,000 of advertising supplies remains on October 31? Obviously, the company would need to make an adjusting entry. Prior to adjustment, the expense account Supplies Expense is overstated

1,000 of advertising supplies remains on October 31? Obviously, the company would need to make an adjusting entry. Prior to adjustment, the expense account Supplies Expense is overstated ![]() 1,000, and the asset account Supplies is understated

1,000, and the asset account Supplies is understated ![]() 1,000. Thus, Yazici makes the following adjusting entry.

1,000. Thus, Yazici makes the following adjusting entry.

After the company posts the adjusting entry, the accounts show the following.

Illustration 3A-1 Prepaid expenses accounts after adjustment

After adjustment, the asset account Supplies shows a balance of ![]() 1,000, which is equal to the cost of supplies on hand at October 31. In addition, Supplies Expense shows a balance of

1,000, which is equal to the cost of supplies on hand at October 31. In addition, Supplies Expense shows a balance of ![]() 1,500. This is equal to the cost of supplies used between October 5 and October 31. Without the adjusting entry, expenses are overstated and net income is understated by

1,500. This is equal to the cost of supplies used between October 5 and October 31. Without the adjusting entry, expenses are overstated and net income is understated by ![]() 1,000 in the October income statement. Also, both assets and equity are understated by

1,000 in the October income statement. Also, both assets and equity are understated by ![]() 1,000 on the October 31 statement of financial position.

1,000 on the October 31 statement of financial position.

Illustration 3-29 compares the entries and accounts for advertising supplies in the two adjustment approaches.

Illustration 3A-2 Adjustment approaches—a comparison

After Yazici posts the entries, the accounts appear as follows.

Illustration 3A-3 Comparison of accounts

Note that the account balances under each alternative are the same at October 31: Supplies 1,000 and Supplies Expense ![]() 1,500.

1,500.

Unearned Revenues

Unearned revenues are recognized as revenue at the time services are performed. Similar to the case for prepaid expenses, companies may credit (increase) a revenue account when they receive cash for future services.

To illustrate, assume that Yazici Advertising received ![]() 1,200 for future services on October 2. Yazici expects to perform the services before October 31.1 In such a case, the company credits Service Revenue. If Yazici in fact performs the service before October 31, no adjustment is needed.

1,200 for future services on October 2. Yazici expects to perform the services before October 31.1 In such a case, the company credits Service Revenue. If Yazici in fact performs the service before October 31, no adjustment is needed.

• HELPFUL HINT

The required adjusted balances here are Service Revenue ![]() 400 and Unearned Service Revenue

400 and Unearned Service Revenue ![]() 800.

800.

However, if at the statement date Yazici has not performed ![]() 800 of the services, it would make an adjusting entry. Without the entry, the revenue account Service Revenue is overstated

800 of the services, it would make an adjusting entry. Without the entry, the revenue account Service Revenue is overstated ![]() 800, and the liability account Unearned Service Revenue is understated

800, and the liability account Unearned Service Revenue is understated ![]() 800. Thus, Yazici makes the following adjusting entry.

800. Thus, Yazici makes the following adjusting entry.

After Yazici posts the adjusting entry, the accounts show the following.

Illustration 3A-4 Unearned service revenue accounts after adjustment

The liability account Unearned Service Revenue shows a balance of ![]() 800. This equals the services that will be performed in the future. In addition, the balance in Service Revenue equals the services performed in October. Without the adjusting entry, both revenues and net income are overstated by

800. This equals the services that will be performed in the future. In addition, the balance in Service Revenue equals the services performed in October. Without the adjusting entry, both revenues and net income are overstated by ![]() 800 in the October income statement. Also, liabilities are understated by

800 in the October income statement. Also, liabilities are understated by ![]() 800, and equity is overstated by

800, and equity is overstated by ![]() 800 on the October 31 statement of financial position.

800 on the October 31 statement of financial position.

Illustration 3-32 compares the entries and accounts for initially recording unearned service revenue in (1) a liability account or (2) a revenue account.

Illustration 3A-5 Adjustment approaches—a comparison

After Yazici posts the entries, the accounts appear as follows.

Illustration 3A-6 Comparison of accounts

Note that the balances in the accounts are the same under the two alternatives: Unearned Service Revenue ![]() 800 and Service Revenue

800 and Service Revenue ![]() 400.

400.

Summary of Additional Adjustment Relationships

Illustration 3-34 provides a summary of basic relationships for deferrals.

Illustration 3A-7 Summary of basic relationships for deferrals

| Type of Adjustment | Reason for Adjustment | Accounts before Adjustment | Adjusting Entry | |

| Prepaid expenses | (a) | Prepaid expenses initially recorded in asset accounts have been used. | Assets overstated. Expenses understated. | Dr. Expenses Cr. Assets |

| (b) | Prepaid expenses initially recorded in expense accounts have not been used. | Assets understated. Expenses overstated. | Dr. Assets Cr. Expenses | |

| Unearned revenues | (a) | Unearned revenues initially recorded in liability accounts are now recognized as revenue. | Liabilities overstated. Revenues understated. | Dr. Liabilities Cr. Revenues |

| (b) | Unearned revenues initially recorded in revenue accounts are still unearned. | Liabilities understated. Revenues overstated. | Dr. Revenues Cr. Liabilities | |

Alternative adjusting entries do not apply to accrued revenues and accrued expenses because no entries occur before companies make these types of adjusting entries.

APPENDIX 3B Concepts in Action

Learning Objective *9

Discuss financial reporting concepts.

This appendix provides a summary of the financial reporting concepts used in this textbook. In addition, it provides other useful concepts that accountants use as a basis for recording and reporting financial information.

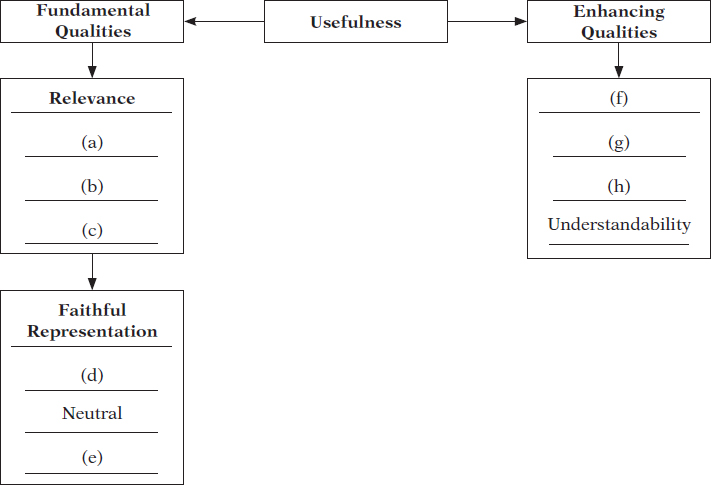

Qualities of Useful Information

Recently, the IASB and FASB completed the first phase of a joint project in which they developed a conceptual framework to serve as the basis for future accounting standards. The framework begins by stating that the primary objective of financial reporting is to provide financial information that is useful to investors and creditors for making decisions about providing capital. According to the IASB, useful information should possess two fundamental qualities, relevance and faithful representation, as shown in Illustration 3-35.

Illustration 3B-1 Fundamental qualities of useful information

|

Relevance Accounting information has relevance if it would make a difference in a business decision. Information is considered relevant if it provides information that has predictive value, that is, helps provide accurate expectations about the future, and has confirmatory value, that is, confirms or corrects prior expectations. Materiality is a company-specific aspect of relevance. An item is material when its size makes it likely to influence the decision of an investor or creditor. |

|

Faithful Representation Faithful representation means that information accurately depicts what really happened. To provide a faithful representation, information must be complete (nothing important has been omitted), neutral (is not biased toward one position or another), and free from error. |

ENHANCING QUALITIES

In addition to the two fundamental qualities, the IASB and FASB also describe a number of enhancing qualities of useful information. These include comparability, verifiability, timeliness, and understandability. In accounting, comparability results when different companies use the same accounting principles. Another type of comparability is consistency. Consistency means that a company uses the same accounting principles and methods from year to year. Information is verifiable if independent observers, using the same methods, obtain similar results. For accounting information to have relevance, it must be timely. That is, it must be available to decision-makers before it loses its capacity to influence decisions. For example, public companies like SAP (DEU) or Tencent Holdings (CHN) usually provide their annual reports to investors within 60 days of their year-end. Information has the quality of understandability if it is presented in a clear and concise fashion, so that reasonably informed users of that information can interpret it and comprehend its meaning.

Assumptions in Financial Reporting

To develop accounting standards, the IASB relies on some key assumptions, as shown in Illustration 3-36. These include assumptions about the monetary unit, economic entity, time period, and going concern.

Illustration 3B-2 Key assumptions in financial reporting

|

Monetary Unit Assumption The monetary unit assumption (discussed in Chapter 1) requires that only those things that can be expressed in money are included in the accounting records. This means that certain important information needed by investors, creditors, and managers, such as customer satisfaction, is not reported in the financial statements. |

|

Economic Entity Assumption The economic entity assumption (discussed in Chapter 1) states that the activities of the entity must be kept separate and distinct from the activities of the owner. In order to assess a company’s performance and financial position accurately, it is important not to blur company transactions with personal transactions (especially those of its managers) or transactions of other companies. |

|

Time Period (Periodicity) Assumption Notice that the income statement, retained earnings statement, and statement of cash flows all cover periods of one year, and the statement of financial position is prepared at the end of each year. The time period assumption (discussed in Chapter 3) states that the life of a business can be divided into artificial time periods and that useful reports covering those periods can be prepared for the business. |

|

Going Concern Assumption The going concern assumption (discussed in Chapter 9) states that the business will remain in operation for the foreseeable future. Of course, many businesses do fail, but in general it is reasonable to assume that the business will continue operating. |

Principles in Financial Reporting

MEASUREMENT PRINCIPLES

IFRS generally uses one of two measurement principles, the historical cost principle or the fair value principle. Selection of which principle to follow generally relates to trade-offs between relevance and faithful representation.

HISTORICAL COST PRINCIPLE The historical cost principle (or cost principle, discussed in Chapter 1) dictates that companies record assets at their cost. This is true not only at the time the asset is purchased but also over the time the asset is held. For example, if land that was purchased for €30,000 increases in value to €40,000, it continues to be reported at €30,000.

FAIR VALUE PRINCIPLE The fair value principle (discussed in Chapter 1) indicates that assets and liabilities should be reported at fair value (the price received to sell an asset or settle a liability). Fair value information may be more useful than historical cost for certain types of assets and liabilities. For example, certain investment securities are reported at fair value because market price information is often readily available for these types of assets. In choosing between cost and fair value, two qualities that make accounting information useful for decision-making are used—relevance and faithful representation. In determining which measurement principle to use, the factual nature of cost figures are weighed versus the relevance of fair value. In general, most assets follow the historical cost principle because fair values may not be representationally faithful. Only in situations where assets are actively traded, such as investment securities, is the fair value principle applied.

REVENUE RECOGNITION PRINCIPLE

The revenue recognition principle requires that companies recognize revenue in the accounting period in which the performance obligation is satisfied. As discussed earlier in the chapter, in a service company, revenue is recognized at the time the service is performed. In a merchandising company, the performance obligation is generally satisfied when the goods transfer from the seller to the buyer (discussed in Chapter 4). At this point, the sales transaction is complete and the sales price established.

EXPENSE RECOGNITION PRINCIPLE

The expense recognition principle (often referred to as the matching principle, discussed earlier in the chapter) dictates that efforts (expenses) be matched with results (revenues). Thus, expenses follow revenues.

FULL DISCLOSURE PRINCIPLE

The full disclosure principle (discussed in Chapter 11) requires that companies disclose all circumstances and events that would make a difference to financial statement users. If an important item cannot reasonably be reported directly in one of the four types of financial statements, then it should be discussed in notes that accompany the statements.

Cost Constraint

Providing information is costly. In deciding whether companies should be required to provide a certain type of information, accounting standard-setters consider the cost constraint. It weighs the cost that companies will incur to provide the information against the benefit that financial statement users will gain from having the information available.

GLOSSARY REVIEW

- Accrual-basis accounting

- Accounting basis in which companies record transactions that change a company’s financial statements in the periods in which the events occur. (p. 102).

- Accruals

- Adjusting entries for either accrued revenues or accrued expenses. (p. 105).

- Accrued expenses

- Expenses incurred but not yet paid in cash or recorded. (p. 114).

- Accrued revenues

- Revenues for services performed but not yet received in cash or recorded. (p. 113).

- Adjusted trial balance

- A list of accounts and their balances after the company has made all adjustments. (p. 121).

- Adjusting entries

- Entries made at the end of an accounting period to ensure that companies follow the revenue and expense recognition principles. (p. 104).

- Book value

- The difference between the cost of a depreciable asset and its related accumulated depreciation. (p. 109).

- Calendar year

- An accounting period that extends from January 1 to December 31. (p. 102).

- Cash-basis accounting

- Accounting basis in which companies record revenue when they receive cash and an expense when they pay out cash. (p. 102).

- *Comparability

- Ability to compare the accounting information of different companies because they use the same accounting principles. (p. 128).

- *Consistency

- Use of the same accounting principles and methods from year to year within a company. (p. 128).

- Contra asset account

- An account offset against an asset account on the statement of financial position. (p. 108).

- *Cost constraint

- Constraint of determining whether the cost that companies will incur to provide the information will outweigh the benefit that financial statement users will gain from having the information available. (p. 130).

- Deferrals

- Adjusting entries for either prepaid expenses or unearned revenues. (p. 105).

- Depreciation

- The allocation of the cost of an asset to expense over its useful life in a rational and systematic manner. (p. 108).

- *Economic entity assumption

- An assumption that every economic entity can be separately identified and accounted for. (p. 129).

- Expense recognition principle (matching principle)

- The principle that companies match efforts (expenses) with accomplishments (revenues). (pp. 103, 130).

- *Fair value principle

- Assets and liabilities should be reported at fair value (the price received to sell an asset or settle a liability). (p. 129).

- *Faithful representation

- Information that accurately depicts what really happened. (p. 128).

- Fiscal year

- An accounting period that is one year in length. (p. 102).

- *Full disclosure principle

- Accounting principle that dictates that companies disclose circumstances and events that make a difference to financial statement users. (p. 130).

- *Going concern assumption

- The assumption that the company will continue in operation for the foreseeable future. (p. 129).

- *Historical cost principle

- An accounting principle that states that companies should record assets at their cost. (p. 129).

- Interim periods

- Monthly or quarterly accounting time periods. (p. 102).

- *Materiality

- A company-specific aspect of relevance. An item is material when its size makes it likely to influence the decision of an investor or creditor. (p. 128).

- *Monetary unit assumption

- An assumption that requires that only those things that can be expressed in money are included in the accounting records. (p. 129).

- Prepaid expenses (prepayments)

- Expenses paid in cash before they are used or consumed. (p. 106).

- *Relevance

- The quality of information that indicates the information makes a difference in a decision. (p. 128).

- Revenue recognition principle

- The principle that companies recognize revenue in the accounting period in which the performance obligation is satisfied. (pp. 103, 130).

- *Timely

- Information that is available to decision-makers before it loses its capacity to influence decisions. (p. 128).

- Time period assumption

- An assumption that accountants can divide the economic life of a business into artificial time periods. (pp. 102, 129).

- *Understandability

- Information presented in a clear and concise fashion so that users can interpret it and comprehend its meaning. (p. 128).

- Unearned revenue

- A liability recorded for cash received before services are performed. (p. 110).

- Useful life

- The length of service of a long-lived asset. (p. 108).

- *Verifiable

- The quality of information that occurs when independent observers, using the same methods, obtain similar results. (p. 128).

PRACTICE MULTIPLE-CHOICE QUESTIONS

- The time period assumption states that:

- companies must wait until the calendar year is completed to prepare financial statements.

- companies use the fiscal year to report financial information.

- the economic life of a business can be divided into artificial time periods.

- companies record information in the time period in which the events occur.

- The revenue recognition principle states that:

- revenue should be recognized in the accounting period in which a performance obligation is satisfied.

- expenses should be matched with revenues.

- the economic life of a business can be divided into artificial time periods.

- the fiscal year should correspond with the calendar year.

- Which of the following statements about the accrual basis of accounting is false?

- Events that change a company’s financial statements are recorded in the periods in which the events occur.

- Revenue is recognized in the period in which services are performed.

- The accrual basis is in accordance with IFRS.

- Revenue is recorded only when cash is received, and expense is recorded only when cash is paid.

- The principle or assumption dictating that efforts (expenses) be matched with accomplishments (revenues) is the:

- expense recognition principle.

- cost assumption.

- time period assumption.

- revenue recognition principle.

- Adjusting entries are made to ensure that:

- expenses are recognized in the period in which they are incurred.

- revenues are recorded in the period in which services are performed.

- statement of financial position and income statement accounts have correct balances at the end of an accounting period.

- All the responses above are correct.

- Each of the following is a major type (or category) of adjusting entries except:

- prepaid expenses.

- accrued revenues.

- accrued expenses.

- recognized revenues.

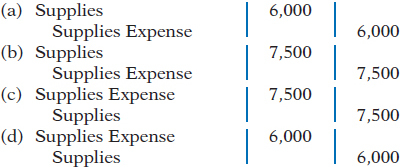

- The trial balance shows Supplies NT$13,500 and Supplies Expense NT$0. If NT$6,000 of supplies are on hand at the end of the period, the adjusting entry is:

- Adjustments for prepaid expenses:

- decrease assets and increase revenues.

- decrease expenses and increase assets.

- decrease assets and increase expenses.

- decrease revenues and increase assets.

- Accumulated Depreciation is:

- a contra asset account.

- an expense account.

- an equity account.

- a liability account.

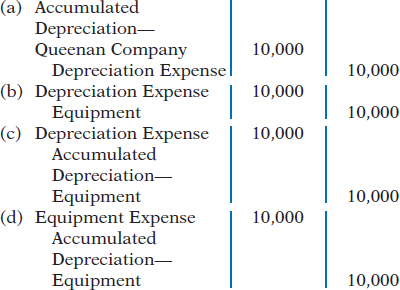

- Queenan Company computes depreciation on delivery equipment at HK$10,000 for the month of June. The adjusting entry to record this depreciation is as follows.

- Adjustments for unearned revenues:

- decrease liabilities and increase revenues.

- have an assets-and-revenues-account relationship.

- increase assets and increase revenues.

- decrease revenues and decrease assets.

- Adjustments for accrued revenues:

- have a liabilities-and-revenues-account relationship.

- have an assets-and-revenues-account relationship.

- decrease assets and revenues.

- decrease liabilities and increase revenues.

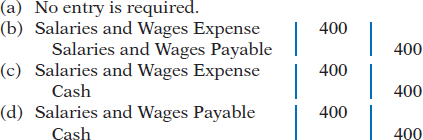

- Kathy Siska earned a salary of R$400 for the last week of September. She will be paid on October 1. The adjusting entry for Kathy’s employer at September 30 is:

- Which of the following statements is incorrect concerning the adjusted trial balance?

- An adjusted trial balance proves the equality of the total debit balances and the total credit balances in the ledger after all adjustments are made.

- The adjusted trial balance provides the primary basis for the preparation of financial statements.

- The adjusted trial balance lists the account balances segregated by assets and liabilities.

- The adjusted trial balance is prepared after the adjusting entries have been journalized and posted.

- The trial balance shows Supplies €0 and Supplies Expense €1,500. If €800 of supplies are on hand at the end of the period, the adjusting entry is:

- debit Supplies 800 and credit Supplies Expense 800.

- debit Supplies Expense 800 and credit Supplies 800.

- debit Supplies 700 and credit Supplies Expense 700.

- debit Supplies Expense 700 and credit Supplies 700.

- Neutrality is an ingredient of:

Faithful Representation Relevance (a) Yes Yes (b) No No (c) Yes No (d) No Yes

- Which item is a constraint in financial accounting?

- Comparability.

- Materiality.

- Cost.

- Consistency.

Solutions

PRACTICE EXERCISES

Prepare adjusting entries.

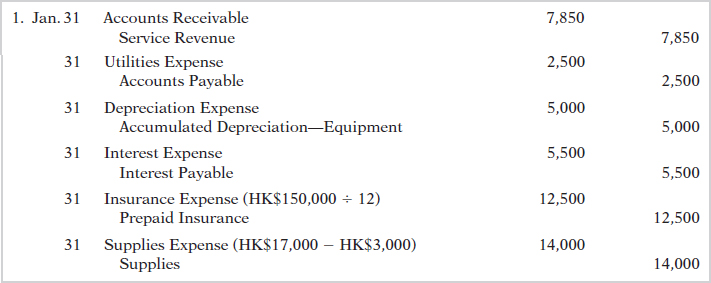

1. Chen’s Dental Practice opened on January 1, 2017. During the first month of operations, the following transactions occurred.

- Performed services for patients totaling HK$7,850, which has not yet been recorded.

- Utility expenses incurred but not paid prior to January 31 totaled HK$2,500.

- Purchased dental equipment on January 1 for HK$900,000, paying HK$250,000 in cash and signing a HK$650,000 3-year note payable. The equipment depreciates HK$5,000 per month. Interest is HK$5,500 per month.

- Purchased a 1-year malpractice insurance policy on January 1 for HK$150,000.

- Purchased HK$17,000 of dental supplies. On January 31, determined that HK$3,000 of supplies were on hand.

Instructions

Prepare the adjusting entries on January 31. Account titles are Accumulated Depreciation—Equipment, Depreciation Expense, Service Revenue, Accounts Receivable, Insurance Expense, Interest Expense, Interest Payable, Prepaid Insurance, Supplies, Supplies Expense, Utilities Expense, and Utilities Payable.

Solution

Prepare correct income statement.

2. The income statement of Zhou Ltd. for the month of July shows net income of NT$140,000 based on Service Revenue NT$550,000, Salaries and Wages Expense NT$230,000, Supplies Expense NT$120,000, and Utilities Expense NT$60,000. In reviewing the statement, you discover the following.

- Insurance expired during July of NT$45,000 was omitted.

- Supplies expense includes NT$30,000 of supplies that are still on hand at July 31.

- Depreciation on equipment of NT$18,000 was omitted.

- Accrued but unpaid salaries and wages at July 31 of NT$40,000 were not included.

- Services performed but unrecorded totaled NT$60,000.

Instructions

Prepare a correct income statement for July 2017.

Solution

PRACTICE PROBLEM

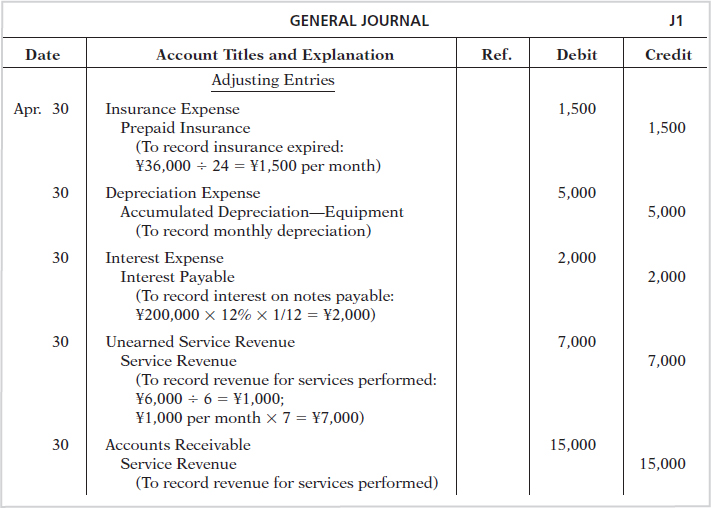

Prepare adjusting entries.

The Green Thumb Lawn Care Ltd. began on April 1. At April 30, the trial balance shows the following balances for selected accounts. (Amounts are in Chinese yuan.)

| Prepaid Insurance | ¥ 36,000 |

| Equipment | 280,000 |

| Notes Payable | 200,000 |

| Unearned Service Revenue | 42,000 |

| Service Revenue | 18,000 |

Analysis reveals the following additional data.

- Prepaid insurance is the cost of a 2-year insurance policy, effective April 1.

- Depreciation on the equipment is ¥5,000 per month.

- The note payable is dated April 1. It is a 6-month, 12% note.

- Seven customers paid for the company’s 6-month lawn service package of ¥6,000 beginning in April. The company performed services for these customers in April.

- Lawn services performed for other customers but not recorded at April 30 totaled ¥15,000.

Instructions

Prepare the adjusting entries for the month of April. Show computations.

Solution

WileyPLUS

Brief Exercises, DO IT! Review, Exercises, and Problems, and many additional resources are available for practice in WileyPLUS.

NOTE: Asterisked Questions, Exercises, and Problems relate to material in the appendices to the chapter.

QUESTIONS

-

How does the time period assumption affect an accountant’s analysis of business transactions?

Explain the terms fiscal year, calendar year, and interim periods.

Define two IFRS principles that relate to adjusting the accounts.

Gabe Corts, a lawyer, accepts a legal engagement in March, performs the work in April, and is paid in May. If Corts’ law firm prepares monthly financial statements, when should it recognize revenue from this engagement? Why?

Why do accrual-basis financial statements provide more useful information than cash-basis statements?

In completing the engagement in Question 3, Corts pays no costs in March, £2,200 in April, and £2,500 in May (incurred in April). How much expense should the firm deduct from revenues in the month when it recognizes the revenue? Why?

“Adjusting entries are required by the historical cost principle of accounting.” Do you agree? Explain.

Why may a trial balance not contain up-to-date and complete financial information?

Distinguish between the two categories of adjusting entries, and identify the types of adjustments applicable to each category.

What is the debit/credit effect of a prepaid expense adjusting entry?

“Depreciation is a valuation process that results in the reporting of the fair value of the asset.” Do you agree? Explain.

Explain the differences between depreciation expense and accumulated depreciation.

Jain Company purchased equipment for Rs18,000,000. By the current statement of financial position date, Rs7,000,000 had been depreciated. Indicate the statement of financial position presentation of the data.

What is the debit/credit effect of an unearned revenue adjusting entry?

A company fails to recognize revenue for services performed but not yet received in cash or recorded. Which of the following accounts are involved in the adjusting entry: (a) asset, (b) liability, (c) revenue, or (d) expense? For the accounts selected, indicate whether they would be debited or credited in the entry.

A company fails to recognize an expense incurred but not paid. Indicate which of the following accounts is debited and which is credited in the adjusting entry: (a) asset, (b) liability, (c) revenue, or (d) expense.

A company makes an accrued revenue adjusting entry for NT$27,000 and an accrued expense adjusting entry for NT$21,000. How much was net income understated prior to these entries? Explain.

On January 9, a company pays €6,000 for salaries and wages, of which €2,000 was reported as Salaries and Wages Payable on December 31. Give the entry to record the payment.

For each of the following items before adjustment, indicate the type of adjusting entry (prepaid expense, unearned revenue, accrued revenue, or accrued expense) that is needed to correct the misstatement. If an item could result in more than one type of adjusting entry, indicate each of the types.

Assets are understated.

Liabilities are overstated.

Liabilities are understated.

Expenses are understated.

Assets are overstated.

Revenue is understated.

One-half of the adjusting entry is given below. Indicate the account title for the other half of the entry.

Salaries and Wages Expense is debited.

Depreciation Expense is debited.

Interest Payable is credited.

Supplies is credited.

Accounts Receivable is debited.

Unearned Service Revenue is debited.

“An adjusting entry may affect more than one statement of financial position or income statement account.” Do you agree? Why or why not?

Why is it possible to prepare financial statements directly from an adjusted trial balance?

L. Thomas Company debits Supplies Expense for all purchases of supplies and credits Rent Revenue for all advanced rentals. For each type of adjustment, give the adjusting entry.

-

What is the primary objective of financial reporting?

Identify the characteristics of useful accounting information.

Dan Fineman, the president of King Company, is pleased. King substantially increased its net income in 2017 while keeping its unit inventory relatively the same. Howard Gross, chief accountant, cautions Dan, however. Gross says that since King changed its method of inventory valuation, there is a consistency problem and it is difficult to determine whether King is better off. Is Gross correct? Why or why not?

What is the distinction between comparability and consistency?

Describe the constraint inherent in the presentation of accounting information.

Laurie Belk is president of Better Books. She has no accounting background. Belk cannot understand why fair value is not used as the basis for all accounting measurement and reporting. Discuss.

What is the economic entity assumption? Give an example of its violation.

BRIEF EXERCISES

Indicate why adjusting entries are needed.

BE3-1 The ledger of Bacalao Company SLU includes the following accounts. Explain why each account may require adjustment.

- Prepaid Insurance.

- Depreciation Expense.

- Unearned Service Revenue.

- Interest Payable.

Identify the major types of adjusting entries.

BE3-2 Lucci Company SpA accumulates the following adjustment data at December 31. Indicate (a) the type of adjustment (prepaid expense, accrued revenue, and so on), and (b) the status of accounts before adjustment (overstated or understated).

- Supplies of €100 are on hand.

- Services performed but not recorded total €870.