Appendix A

Ball Corporation: Example Report

Ball Corporation Sustainability Report

This illustration of the use of the Global Reporting Initiative (GRI) Reporting Guidelines has been summarized from Ball Corporation’s original report.1 Ball Corporation published their first report covering the year 2007 on June 30, 2008. Ceres and the Association of Chartered Certified Accountants (ACCA) awarded Ball Corporation as a cowinner of Best First Time Reporter Award as part of the 2009 Ceres-ACCA North American Sustainability Awards. Ball Corporation represents the first packaging and first aerospace company to receive this honor.2 The award is for Ball Corporation’s comprehensive approach to sustainability and commitment to stakeholder engagement in addition to its strategy for manufacturing sustainable packaging and for promoting recycling.

- The most senior official (e.g., CEO, chair, or equivalent senior position) of the organization provides a statement about the relevance of sustainability to the organization and its strategy.

- The report should describe the organization’s key impacts, risks, and opportunities.

Organizational Profile

This section contains some fundamental detailed facts about the company. The name of the organization and its primary brands, products, and services should be listed in addition to how it provides the products and services. If outsourcing plays a role, the extent is disclosed. The operating structure—main divisions, operating companies, subsidiaries, and joint ventures—are listed. The location of the company’s headquarters and the number and names of countries where major operations occur are listed. Ownership and legal form (corporation, partnership, or sole proprietorship) are given. The markets served (geographic, sectors, and customers) along with the size of the company in terms of number of employees, net sales, total capitalization by type (debt, equity), quantity of products, and total assets are presented. The names and ownership percentages of largest stockholders are listed. For countries that consist of 5% or more of total revenues, sales or revenues and costs by region or country are presented. Employee numbers by region are given. If significant changes in size, structure, ownership, location, or facilities (openings, expansions, closings), they are reported. Changes in the capital structure need to be presented. Any awards during the reporting period are listed in this section.

- The name of the organization is listed.

- The report should describe the operational structure of the organization. This involves listing main divisions, operating companies, subsidiaries, and joint ventures.

- The location of the organization’s headquarters must be listed.

- The section lists the number and names of countries where the organization operates. It should include the countries that have specific relevance to sustainability.

- The organization must disclose the nature of ownership and its legal form.

- The report should disclose the markets served. This includes geographic location, sectors served, and types of customers. Table A-1 contains Ball Corporation’s information.

- The scale of the reporting organization should be listed. Scale refers to the number of employees, net sales or revenues, and the volume of products or services provided. Table A-2 illustrates Ball Corporation’s scale of operations.

- If any material changes occurred during the reporting period, this needs to be disclosed. Examples of changes are size, structure, ownership, location, operations, and facilities (openings, closings, and expansions). Table A-3 shows the major changes that Ball Corporation experienced during its report period.

- The organization should disclose its awards received in the reporting period.

Report Parameters

- The reporting period is presented.

- The date of previous report is listed.

- The reporting cycle specifies how often reports are published.

- Information is provided so that stakeholders may contact company personnel to address questions over the report or contents

- The process for determining the report’s content should be disclosed. This encompasses how the organization determines materiality, gives priority to topics within the report, and identifies stakeholders that are likely to use the report. This section needs to include a rationale of the organization’s application of the GRI’s Guidance on Defining Report Content and the associated principles. This declaration communicates the specific elements that have been applied to prepare the report. There are three levels to meet the needs of organizations’ stage of reporting—beginning, midlevel, and advanced. The corresponding levels are C, B, and A, where C is beginning and A is advance. To designate that a report has received external assurance, C+, B+, or A+ can be used.

- The organization must discuss the boundary of the report such as subsidiaries, countries, divisions, leased facilities, joint ventures, and suppliers.

- If there are limitations on the scope of the report, these must be listed. If the full extent of significant economic, environmental, and social effects cannot be addressed, the organization’s approach and timeframe for coverage need to be stated.

- The organization should disclose the basis for reporting on joint ventures, subsidiaries, leased facilities, outsourced operations, and other entities that can materially affect comparisons from period to period and between organizations.

- The organization must disclose data measurement techniques and the basis of its calculations. This should include assumptions and methods that support estimates related to the indicators and other information in the report. Any deviations or choices to not implement GRI Indicator Protocols must be explained.

- The organization must explain how any restatement of information from prior reports affects the presentation in the report. Reasons such as mergers, acquisitions, nature of business, and measurement methods are to be included.

- The organization must state major changes that have occurred from prior reporting periods. The changes of interest here are in the scope, boundary, or measurement methods applied in the report.

- A table is needed to specify where the standard disclosures are in the report. This is to include page numbers or Web links for strategy and analysis; organizational profile; report parameters; and governance, commitments, and engagement.

- The organization should state its policy and current practice for external assurance for the report. The scope and basis of external assurance should be explained if it is not in the assurance report. The nature of the relationship between the reporting organization and the assuring company should be detailed.

Governance, Commitments, and Engagement

- The organization should disclose the governance structure of the organization including high-level committees that are involved in two specific tasks: setting strategy or organizational oversight. The mandate and composition of such committees are to be described. This includes a statement concerning direct responsibility for economic, social, and environmental performance.

- The organization must indicate if the chair of the top governance board is an executive officer and the reasons why.

- Assuming that the organization has a single board structure, the report should list the number of members of the highest governance body that are both independent and nonexecutive members. The terms independent and nonexecutive need to be defined.

- The report should list the mechanisms that the organization has for shareholders and employees to communicate to the highest governance body. This includes describing shareholder resolutions or other methods that allows minority shareholders to communicate with the highest governance body. In addition, the report should describe ways that the organization can inform and consult workers about how they can be represented at the highest governance body. The mechanisms should allow for the identification of issues related to economic, environmental, and social performance.

- The report must provide information about how compensation for members of the highest governance body, senior managers, and executives (including departure arrangements) is linked to the organization’s performance (including social and environmental performance).

- The report should specify the processes that are instituted for the highest governance body to avoid conflicts of interest.

- The organization should describe the process to determine the qualifications and expertise of the members of the highest governance body that lead the organization’s strategy on economic, environmental, and social topics.

- The organization should present their internally developed statements of mission or values; codes of conduct; and principles relevant to economic, environmental, and social performance and the status of their implementation. An explanation of how they are applied across the organization and to what degree they apply to internationally agreed standards.

- The report should disclose the procedures that the highest governance body has for monitoring the organization’s identification and management of economic, environmental, and social performance. This includes monitoring the identification of relevant risks and opportunities and compliance with internationally agreed standards, codes of conduct, and principles. This section should include how frequently the governance body evaluates sustainability performance.

- The report should list the processes to evaluate the highest governance body’s economic, environmental, and social performance.

- The report should explain if and how the precautionary approach (Article 15 of the Rio Principles) is used. This could be answered by the organization’s approach to risk management in operational planning or new product development and introduction. The precautionary approach states, “In order to protect the environment, the precautionary approach shall be widely applied by States according to their capabilities. Where there are threats of serious or irreversible damage, lack of full scientific certainty shall not be used as a reason for postponing cost-effective measures to prevent environmental degradation.”3

- The report should present externally developed economic; environmental; and social charters, principles, or other initiatives that organization subscribes or endorses. Date of adoption, location of application, and stakeholder involvement should be included. The degree of obligation (voluntary vs. obligatory) to comply with these initiatives should be reported.

- The report should list the company’s association memberships and both national and international advocacy organizations where it is part of the governance body, engages in committee work, donates material funds beyond membership fees, or considers membership as a strategic benefit.

- Stakeholders that are engaged by the organization should be presented. Stakeholder groups include communities, civil society, customers, shareholders (and providers of capita), suppliers, and employees (other workers and their trade unions).

- The report should include the organization’s basis for identifying and selecting the stakeholders to engage. The organization’s process used to define its stakeholder groups, and the selection process should also be described.

- The report should discuss approaches to stakeholder engagement, including frequency of engagement by type and by stakeholder group. Examples of engagement methods include surveys, focus groups, community panels, corporate advisory panels, written communication, management and union structures, and others. Disclosure in this area should also indicate if the engagement was part of the report preparation process.

- The report should discuss key topics and concerns that have that been raised through stakeholder engagement. An explanation of how the organization has responded to those key topics and concerns should be included.

Management Approach and Performance

Performance indicators are organized by economic, environmental, and social categories. Social indicators are broken down into subcategories of labor, human rights, society, and product responsibility. Each category includes a disclosure on management approach and a set of core and additional performance indicators. Core indicators have been developed through GRI’s multistakeholder processes. The core indicators identify generally applicable indicators and are assumed to be material for most organizations. Core indicators should be reported unless they are not material on the basis of the GRI Reporting Principles. Additional indicators are emerging practice or topics that may be material for some organizations but not for others.

To set the context for performance, the disclosure(s) on management approach should provide a brief overview of the organization’s management approach to each dimension. The disclosure section should address all the aspects associated with each category. Within the overall structure of the standard disclosures, strategy and profile are intended to provide a concise overview of the risks and opportunities facing the organization as a whole. The disclosure(s) on management approach presents details of the organization’s approach to managing the risks and opportunities of sustainability.

The GRI provides guidance on data compilation. Providing the current period and at least two prior ones is indicated to show trends. If future targets are available, these should be presented for the short and medium terms. GRI Protocols for the indicators should be used for interpreting and compiling report information. Absolute data along with ratios or normalized data should be presented. Aggregation of information should be determined by the organization. For metrics, generally accepted international metrics such as kilograms or liters along with standard conversion formulas should be used.

Economic Dimension Issues

The economic dimension presents the impacts on the economic conditions of an organization’s stakeholders and on local, national, and global entities (e.g., governments, associations, etc.). Although financial information is reported in the financial statements, this presentation’s focus is on the organization’s contribution to the sustainability of a bigger economic system.

Disclosure on Management Approach to Economic Issues

This disclosure is to provide a concise statement on management’s approach to economic performance, market presence, and indirect economic impacts. The organization’s goals and performance should be discussed along with the policies to specify the organization’s commitment to economic issues. Additional information is reported that explains major successes and failures, risks and opportunities, changes in systems and structures during the report period, and material strategies relevant to policies and performance.

Economic Performance Indicators

Economic Performance

- The organization should report direct economic value generated and distributed. Included in these categories are revenues, operating costs, employee compensation, donations and other community investments, retained earnings, and payments to capital providers and governments (core indicator). Tables A-7 and A-8 provide these values for 2005 through 2007.

- The report should provide the financial implications and other risks and opportunities due to climate change that the organization can identify (core indicator).

Ball Corporation reports their risks and opportunities with financial implications as follows.

- The report should disclose the organization’s defined benefit plan obligations (core indicator).

- The report should list material financial assistance received from government (core indicator).

Table A-9 shows government assistance by source.

Market Presence

- Standard entry-level wages can be compared to local minimum wage at material locations of the organization’s operation (additional indicator).

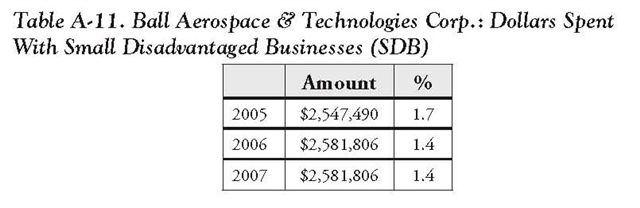

- The organization should disclose the policy, practices, and proportion of spending on locally based suppliers at material locations of operation (core indicator).

- The report should state the procedures for hiring local candidates and the percent of the senior management that are hired from the local community at material locations (core indicator).

Indirect Economic Impacts

- The organization should indicate the development and impact of infrastructure investments and services that are provided mostly for the public benefit through commercial, in kind, or pro bono engagement (core indicator).

- The report can provide information about significant indirect economic impacts, including the extent of impacts (additional indicator).

Environmental Dimension

The environmental dimension is the organization’s impacts on living and nonliving natural systems (ecosystems, land, air, and water). Environmental indicators report the organization’s use of inputs such as material, energy, and water. Its outputs that affect the environment are emissions, effluents, and waste. In addition, the indicators report performance related to biodiversity, environmental compliance, environmental expenditures, and the impacts of products and services.

Disclosure on Management Approach to Environmental Issues

The report should include a statement about the management’s approach regarding the organization’s use of materials, energy, water, biodiversity, emissions, effluents and waste, products and services, compliance, transport, and overall impact.

Environmental Performance Indicators

Materials

- The organization should disclose the materials that it uses by weight or volume (core indicator).

Table A-13 shows Ball Corporation’s material usage by type.

Energy

- The report should present the percentage of materials used that is recycled input materials (core indicator).

- The report should list direct energy consumption by primary energy source. Direct energy comes from energy created from sources like coal and natural gas that are brought into an organization’s operational boundaries and used there (core indicator).

Table A-14 displays Ball Corporation’s direct energy use.

- The report should list the organization’s indirect energy use by source. Indirect energy is generated outside of an organization’s operational boundaries to provide energy for the organization’s needs. The purchases of electric heat or steam are two examples (core indicator).

Ball Corporation’s indirect energy use is shown in Table A-15.

- The organization can describe the energy that it saved from conservation and efficiency efforts (additional indicator).

- The organization can report its initiatives that provide energy-efficient or renewable energy-based products and services. In addition, this would include reductions in energy requirements caused by these initiatives (additional indicator).

- The report can include the organization’s initiatives that are intended to reduce indirect energy consumption. The reductions achieved would be reported (additional indicator).

Water

- The organization should disclose total water that it withdraws by source (core indicator).

Table A-16 displays Ball Corporation’s water use by source.

- The organization can report if its water sources are significantly affected by withdrawal of water (additional indicator).

- The report can disclose the percentage and total volume of water recycled and reused (additional indicator).

Table A-17 shows Ball Corporation’s recycled and reused water.

Biodiversity

- The report should contain the location and size of land owned, leased, or managed in or adjacent to protected areas. In addition, the report should contain the same information for areas of high biodiversity value outside protected areas (core indicator).

- The organization should describe material impacts of activities, products, and services on biodiversity in protected areas. In addition, it should describe it impacts in areas of high biodiversity value outside protected areas (core indicator).

- The organization can list habitats protected or restored (additional indicator).

- The organization can provide its strategies, current actions, and future plans for managing affects on biodiversity (additional indicator).

- The organization can provide the number of IUCN (International Union for Conservation of Nature) Red List species and national conservation list species with habitats in areas affected by operations, by level of extinction risk (additional indicator).

Emissions, Effluents, and Waste

- The report should provide the organization’s total direct and indirect GHG emissions by weight (core indicator).

Ball Corporation’s total direct and indirect emissions are presented in Table A-18.

- The report should list other relevant indirect GHG emissions by weight (core indicator).

- The organization can indicate the initiatives that it engages in to reduce GHG emissions and the reductions it achieved (additional indicator).

- The report should present the emissions of ozone-depleting substances by weight (core indicator).

- The organization should report its NOx, SOx, and other significant air emissions by type and weight (core indicator).

Ball Corporation’s ozone depleting substances and amounts are listed in Table A-19.

- The organization should report its total water discharge by quality and destination (core indicator).

Ball Corporation reports that 90% of its total water withdrawal results in water discharge. The company measures on a regular basis the total amount of pollutants discharged from its facilities North America and Europe. Biological Oxygen Demand (BOD) is reported for 3 years. BOD, a measure of water quality, determines how quickly biological organisms use oxygen in a body of water. Pristine rivers have a BOD below 1 mg/l while efficiently treated sewage from a municipality is about 20 mg/l.

The measure of dry weight particles, total suspended solids (TSS), represents the weight of particles trapped by a filter with a specified pore size. It is a measure of the quantity of solids in the water. To treat certain solid pollutants such as aluminum (Al), manganese (Mn), fluorine (F), phosphorus (P), oils, or caustic water, aluminum can plants pretreat wastewater solids before discharging the water to a publicly owned treatment works (POTW). Table A-20 displays Ball Corporation’s water quality discharge.

- The organization should disclose total weight of waste by type and disposal method (core indicator).

Information about Ball Corporation’s waste is presented in Table A-21.

- The report should list the organization’s total number and volume of significant spills (core indicator).

Ball Corporation’s significant spills are presented in Table A-22.

- The organization can report the weight of transported, imported, exported, or treated waste deemed hazardous under the terms of the Basel Convention Annex I, II, III, and VIII. In addition, the percentage of transported waste shipped internationally can be presented (additional indicator).

- The organization can report identity, size, protected status, and biodiversity value of water bodies and related habitats significantly affected by the reporting organization’s discharges of water and runoff (additional indicator).

- The organization should report its initiatives that are in place to mitigate environmental impacts of products and services and the extent of impact mitigation (core indicator).

- The organization should report the percentage of products sold and their packaging materials that are reclaimed by category (core indicator).

- The report should disclose the monetary value of significant fines and total number of nonmonetary sanctions for noncompliance with environmental laws and regulations (core indicator).

Ball Corporation’s noncompliance events and sanctions are presented in Table A-23.

- The organization can report significant environmental impacts of transporting products and other goods and materials used for the organization’s operations. In addition, this includes the transporting of employees (additional indicator).

- The organization can report the total environmental protection expenditures and investments by type (additional indicator).

Social Performance Indicators

The social dimension of sustainability covers the impacts that an organization has on the social systems related to its operations. The GRI Social Performance Indicators involve aspects of labor practices, human rights, society, and product responsibility.

Labor Practices and Decent Work

Indicators under labor practices are based on internationally recognized universal standards. These include the United Nations Universal Declaration of Human Rights and Its Protocols: United Nations Convention: International Covenant on Civil and Political Rights; United Nations Convention: International Covenant on Economic, Social, and Cultural Rights; International Labor Organization (ILO) Declaration on Fundamental Principles and Rights at Work of 1998, and the Vienna Declaration and Programme of Action. In addition, two instruments that address the social responsibilities of business enterprises, the ILO Tripartite Declaration Concerning Multinational Enterprises and Social Policy and the Organisation for Economic Co-operation and Development (OECD) Guidelines for Multinational Enterprises, are used for these indicators.

Disclosure on Management Approach to Labor and Decent Work

The report should provide a concise description of the organization’s labor and management relations, occupational health and safety, training and education, and diversity and equal opportunity.

Labor Practices and Decent Work Performance Indicators

Employment

- The report should list the total number of employees by employment type, employment contract, and region (core indicator).

- The organization should disclose employee turnover by total number and rate. This disclosure should be broken down by age group, gender, and region (core indicator).

Ball Corporation’s employee turnover is presented in Tables A-25 through A-27.

- The organization can disclose the benefits given to full-time employees that are not given to temporary or part-time employees, by major operations (additional indicator).

Labor and Management Relations

- The report should list the percentage of employees covered by collective bargaining agreements (core indicator).

Ball Corporation’s collective bargaining agreements as a percentage of employees covered are presented in Table A-28.

- The organization should report the minimum notice period(s) for operational changes. This should indicate if it is required by collective agreements (core indicator).

Occupational Health and Safety

- The organization can report the percentage of total workforce represented in formal joint management–worker health and safety committees. These committees provide advice on occupational health and safety programs and assistance on monitoring (additional indicator).

- The report should include rates of injury, occupational diseases, lost days, and absenteeism, and number of work-related fatalities by region (core indicator).

Health and safety rates along with fatalities by region are presented in Table A-29.

- The organization should discuss its education, training, counseling, prevention, and risk-control programs in place to assist workforce members, their families, or community members regarding serious diseases (core indicator).

- The report can discuss the health and safety topics covered in formal agreements with trade unions (additional indicator).

Training and Education

- The organization should report by employee category the average hours of training per year per employee (core indicator).

- The organization can report programs that provide skills management and lifelong learning. These programs promote the continued employability of employees and assist end-of-career management (additional indicator).

- The report can include the percentage of employees receiving regular performance and career development reviews (additional indicator).

Diversity and Equal Opportunity

- The organization should report the composition of governance bodies. This includes categorizing employees according to gender, age group, minority group membership, and other indicators of diversity (core indicator).

The composition of Ball Corporation’s governance boards and employees by gender and minority status are presented in Table A-31.

- The report should present the ratio men’s basic salary to that of women by employee category (core indicator).

- Ball Corporation’s ratios of men’s to women’s basic salary are shown in Table A-32.

Human Rights

Human rights performance indicators represent the degree to which human rights are part of the organization’s investment and supplier and contractor selection practices. This includes employees and security forces training on human rights, training on nondiscrimination, freedom of association, child labor, indigenous rights, and forced and compulsory labor. Example of recognized human rights are the United Nations Universal Declaration of Human Rights and Its Protocols; United Nations Convention: International Covenant on Civil and Political Rights; United Nations Convention: International Covenant on Economic, Social, and Cultural Rights; ILO Declaration on Fundamental Principles and Rights at Work of 1998; and The Vienna Declaration and Programme of Action.

Disclosure on Management Approach to Human Rights

The management approach disclosure should provide a discussion of topics on investment and procurement practices, nondiscrimination, freedom of association and collective bargaining, abolition of child labor, prevention of forced and compulsory labor, complaints and grievances practices, security practices, and indigenous rights. The ILO Tripartite Declaration Concerning Multinational Enterprises and Social Policy and the Organisation for Economic Cooperation and Development Guidelines for Multinational Enterprises are the primary references.

Human Rights Performance Indicators

Investment and Procurement Practices

- The organization should report the percentage and total material investment agreements that include human rights clauses or that have undergone human rights screening (core indicator).

- The organization should report the percentage of material suppliers and contractors that have undergone screening on human rights and actions taken (core indicator).

- The organization can report the total hours of employee training on policies and procedures concerning aspects of human rights that are relevant to operations. This includes the percentage of employees trained on these policies and procedures (additional indicator).

Nondiscrimination

- The organization should report the total number of incidents of discrimination and actions taken (core indicator).

Freedom of Association and Collective Bargaining

- The organization should report its operations where the right to practice freedom of association and collective bargaining may be at significant risk. In addition, the report should include what actions are taken to support these rights (core indicator).

Child Labor

- Organizations should report operations that have been identified as being at material risk for incidents of child labor. In addition, organizations should state the steps taken to eliminate child labor (core indicator).

Forced and Compulsory Labor

- Organizations should list the operations that are considered a significant risk for incidents of forced or compulsory labor. In addition, it should provide information about what the organization is doing to eliminate forced or compulsory labor (core indicator).

Security Practices

- The organization can list the percentage of security personnel trained in how the organization handles human rights that are pertinent to its operations (additional indicator).

Indigenous Rights

- The organization can list the total number of incidents of violations involving rights of indigenous people and results of the incidents (additional indicator).

Society

Society performance indicators are the impacts that organizations have on the communities affected by their operations. This involves disclosure of potential risks from interactions with other social institutions. The disclosure includes the management and mediation of these acknowledged risks. The risks include bribery and corruption, undue influence in public policy making, and monopoly practices.

Disclosure on Management Approach to Society

The management approach disclosure refers to the community, corruption, public policy, anticompetitive behavior, and compliance.

Society Performance Indicators

Community

- Nature, scope, and effectiveness of any programs and practices that assess and manage the impacts of operations on communities, including entering, operating, and exiting (core indicator).

Corruption

- The organization should report the percentage and total number of business units analyzed for risks related to corruption (core indicator).

- The report should include the percentage of employees trained in an organization’s anticorruption policies and procedures (core indicator).

- The organization should report the actions it has taken to respond to incidents of corruption (core indicator).

Public Policy

- The report should present the organization’s public policy positions and participation in public policy development and lobbying (core indicator).

- The organization can report the total value of financial and in-kind contributions to political parties, politicians, and related institutions by country (additional indicator).

Anticompetitive Behavior

- The organization can report the total number of legal actions for anticompetitive behavior, antitrust practices, and monopoly practices. In addition, the organization can report the resolution of these actions (additional indicator).

Compliance

- The report should disclose the monetary value of material fines and total number of nonmonetary sanctions for noncompliance with laws and regulations (core indicator).

Product Responsibility

Product responsibility performance indicators include aspects of a reporting organization’s products and services that directly affect customers. Health and safety, information and labeling, marketing, and privacy are the specific topics covered. Disclosure involves a discussion of an organization’s internal procedures and the degree to which these procedures are not complied with.

Disclosure on Management Approach to Product Responsibility

Management’s approach to product responsibility should include a discussion of customer health and safety, product and service labeling, marketing communications, customer privacy, and compliance.

Product Responsibility Performance Indicators

Customer Health and Safety

- The organization should report the health and safety impacts of products and services as they are assessed for improvement in the product life cycle stages. The report should include the percentage of material products and services categories that are covered by such procedures (core indicator).

- The organization can report the total number of incidents of noncompliance with regulations and voluntary codes concerning health and safety impacts of its products and services. This disclosure would include the impacts during the product’s life cycle and the type of outcomes (additional indicator).

Product and Service Labeling

- The organization should disclose the type of product and service information required by procedures. This should include the percentage of significant products and services subject to these information requirements (core indicator).

- The organization can report the total number of incidents of noncompliance with regulations and voluntary codes concerning product and service information and labeling, by type of outcomes (additional indicator).

- The organization can disclose its practices that are linked to customer satisfaction. This includes results of customer satisfaction surveys (additional indicator).

Marketing Communications

- The report should disclose programs for adherence to laws, standards, and voluntary codes related to marketing communications. This includes advertising, promotion, and sponsorship (core indicator).

- The organization can report the total number of incidents of noncompliance with regulations and voluntary codes concerning marketing communications, including advertising, promotion, and sponsorship by type of outcomes (additional indicator).

Customer Privacy

- The organization can report the total number of substantiated complaints regarding breaches of customer privacy and losses of customer data (additional indicator).

Compliance

- The organization should report the monetary value of material fines for noncompliance with laws and regulations concerning the provision and use of products and services (core indicator).