CHAPTER 11

Corporations: Organization, Share Transactions, Dividends, and Retained Earnings

FEATURE STORY

To the Victor Go the Spoils

You never know where a humble start might take you. One of the most recognized brands in the world began in 1924 when Adolf “Adi” Dassler became committed to the idea of providing high-quality, sport-specific shoes to athletes. He and his brother stitched together canvas and whatever else he could find in post-World War I Germany to create his shoes. They were so dedicated to their company that they sometimes ran their equipment with electricity generated by riding an exercise bicycle.

Just like today, success in the early years of the Dassler Brothers Shoe Company hinged on affiliations with famous athletes. So it was very fortunate for the brothers that in the 1936 Olympics, their shoes were worn by the famous African-American runner Jesse Owens. After World War II, as a result of a family quarrel, Adi’s brother left and formed his own shoe company, Puma (DEU). Adi renamed his company using a combination of his nickname “Adi” and the first part of his last name, Dassler, to create the now famous name adidas (DEU). In the 1990s, adidas became a publicly traded company for the first time when its shares began to trade on both German and French exchanges.

By becoming a public company, adidas increased its ability to raise funds. It would need these funds in order to compete in the increasingly competitive world of sports apparel. Within two years of going public, adidas AG acquired the Salomon Group (FRA). This acquisition brought in the brands Salomon, TaylorMade, Mavic, and Bonfire. Less than 10 years later, adidas acquired Reebok (GBR). The combination of Reebok and adidas created a company with a global footprint large enough to compete with Nike (USA).

The shoe market is fickle, with new styles becoming popular almost daily and vast international markets still lying untapped. Whether one of these two giants does eventually take control of the pedi-planet remains to be seen. Meanwhile, the shareholders of each company sit anxiously in the stands as this Olympic-size drama unfolds.

PREVIEW OF CHAPTER 1

Corporations like adidas (DEU) have substantial resources at their disposal. In fact, the corporation is the dominant form of business organization in the world in terms of sales, earnings, and number of employees. In this chapter, we will explain the essential features of a corporation and the accounting for a corporation’s share capital transactions.

The content and organization of Chapter 11 are as follows.

The Navigator

The Navigator

The Corporate Form of Organization

Learning Objective 1

Identify the major characteristics of a corporation.

Many years ago, a noted scholar defined a corporation as “an artificial being, invisible, intangible, and existing only in contemplation of law.” This definition is the foundation for the prevailing legal interpretation in many countries that a corporation is an entity separate and distinct from its owners.

A corporation is created by law, and its continued existence depends upon the statutes of the jurisdiction in which it is incorporated. As a legal entity, a corporation has most of the rights and privileges of a person. The major exceptions relate to privileges that only a living person can exercise, such as the right to vote or to hold public office. A corporation is subject to the same duties and responsibilities as a person. For example, it must abide by the laws, and it must pay taxes.

Two common ways to classify corporations are by purpose and by ownership. A corporation may be organized for the purpose of making a profit, or it may be not-for-profit. For-profit corporations include such well-known companies as Compass Group (GBR), Hyundai Motors (KOR), LUKOIL (RUS), and Google (USA). Not-for-profit corporations are organized for charitable, medical, or educational purposes. Examples are the Salvation Army (USA), the International Committee of the Red Cross (CHE), and the Bill & Melinda Gates Foundation (USA).

Classification by ownership differentiates publicly held and privately held corporations. A publicly held corporation may have thousands of shareholders. Its shares are regularly traded on a national securities exchange such as the São Paùlo Stock Exchange (BRA). Examples are Toyota (JPN), Siemens (DEU), Sinopec (CHN), and General Electric (USA).

In contrast, a privately held corporation usually has only a few shareholders, and does not offer its shares for sale to the general public. Privately held companies are generally much smaller than publicly held companies, although some notable exceptions exist. Cargill Inc. (USA), a private corporation that trades in grain and other commodities, is one of the largest companies in the world.

• Alternative Terminology

Privately held corporations are also referred to as closely held corporations.

Characteristics of a Corporation

A number of characteristics distinguish corporations from proprietorships and partnerships. We explain the most important of these characteristics below.

SEPARATE LEGAL EXISTENCE

In most countries, an entity is separate and distinct from its owners. The corporation acts under its own name rather than in the name of its shareholders. Volvo (SWE) may buy, own, and sell property. It may borrow money, and it may enter into legally binding contracts in its own name. It may also sue or be sued, and it pays its own taxes.

In a partnership, the acts of the owners (partners) bind the partnership. In contrast, the acts of its owners (shareholders) do not bind the corporation unless such owners are agents of the corporation. For example, if you owned shares of Volvo, you would not have the right to purchase inventory for the company unless you were designated as an agent of the corporation.

LIMITED LIABILITY OF SHAREHOLDERS

Since a corporation is a separate legal entity, in most countries creditors have recourse only to corporate assets to satisfy their claims. The liability of shareholders is normally limited to their investment in the corporation. Creditors have no legal claim on the personal assets of the owners unless fraud has occurred. Even in the event of bankruptcy, shareholders’ losses are generally limited to their capital investment in the corporation.

TRANSFERABLE OWNERSHIP RIGHTS

Ordinary shares give ownership in a corporation. These shares are transferable units. Shareholders may dispose of part or all of their interest in a corporation simply by selling their shares. The transfer of an ownership interest in a partnership requires the consent of each owner. In contrast, the transfer of shares is entirely at the discretion of the shareholder. It does not require the approval of either the corporation or other shareholders.

The transfer of ownership rights between shareholders normally has no effect on the daily operating activities of the corporation. Nor does it affect the corporation’s assets, liabilities, and total equity. The transfer of these ownership rights is a transaction between individual owners. The company does not participate in the transfer of these ownership rights after the original sale of the ordinary shares.

ABILITY TO ACQUIRE CAPITAL

It is relatively easy for a corporation to obtain capital through the issuance of shares. Investors buy shares in a corporation to earn money over time as the share price grows. Investors also like to invest in shares because they have limited liability and shares are readily transferable. Also, individuals can become shareholders by investing relatively small amounts of money. In sum, the ability of a successful corporation to obtain capital is virtually unlimited.

CONTINUOUS LIFE

The life of a corporation is stated in its charter. The life may be perpetual, or it may be limited to a specific number of years. If it is limited, the company can extend the life through renewal of the charter. Since a corporation is a separate legal entity, its continuance as a going concern is not affected by the withdrawal, death, or incapacity of a shareholder, employee, or officer. As a result, a successful company can have a continuous and perpetual life.

CORPORATION MANAGEMENT

Shareholders legally own the corporation. However, they manage the corporation indirectly through a board of directors they elect. The board, in turn, formulates the operating policies for the company. The board also selects officers, such as a president and one or more vice presidents, to execute policy and to perform daily management functions.

Illustration 11-1 (page 540) presents a typical organization chart showing the delegation of responsibility. The chief executive officer (CEO) has overall responsibility for managing the business. As the organization chart shows, the CEO delegates responsibility to other officers. The chief accounting officer is the controller. The controller’s responsibilities include (1) maintaining the accounting records, (2) maintaining an adequate system of internal control, and (3) preparing financial statements, tax returns, and internal reports. The treasurer has custody of the corporation’s funds and is responsible for maintaining the company’s cash position.

The organizational structure of a corporation enables a company to hire professional managers to run the business. On the other hand, the separation of ownership and management often reduces an owner’s ability to actively manage the company.

GOVERNMENT REGULATIONS

A corporation is subject to governmental regulations. Laws prescribe the requirements for issuing shares, the distributions of earnings permitted to shareholders, and the effects of retiring shares. Securities laws govern the sale of shares to the general public. Also, most publicly held corporations are required to make extensive disclosure of their financial affairs to securities regulators through quarterly and annual reports. In addition, when a corporation lists its shares on organized securities exchanges, it must comply with the reporting requirements of these exchanges. Government regulations are designed to protect the owners of the corporation.

Illustration 11-1 Corporation organization chart

ADDITIONAL TAXES

In most countries, owners of proprietorships and partnerships report their share of earnings on their personal income tax returns. The individual owner then pays taxes on this amount. Corporations, on the other hand, must pay government taxes as a separate legal entity. These taxes can be substantial.

In addition, shareholders must pay taxes on cash dividends (pro rata distributions of net income). Thus, many argue that the government taxes corporate income twice (double taxation)—once at the corporate level, and again at the individual level.

In summary, Illustration 11-2 shows the advantages and disadvantages of a corporation compared to a proprietorship and a partnership.

Illustration 11-2 Advantages and disadvantages of a corporation

| Advantages | Disadvantages |

| Separate legal existence | Corporation management—separation of ownership and management |

| Limited liability of shareholders | |

| Transferable ownership rights | Government regulations |

| Ability to acquire capital | Additional taxes |

| Continuous life | |

| Corporation management—professional managers |

Forming a Corporation

The steps for forming a corporation vary somewhat across countries. The initial step in forming a corporation is to file an application with the appropriate governmental agency in the jurisdiction in which incorporation is desired. The application describes the name and purpose of the corporation, the types and number of shares that are authorized to be issued, the names of the individuals that formed the company, and the number of shares that these individuals agreed to purchase. Regardless of the number of jurisdictions in which a corporation has operating divisions, it is typically incorporated in only one state or country.

It is to the company’s advantage to incorporate in a state or country whose laws are favorable to the corporate form of business organization. For example, Gulf Oil (USA) changed its state of incorporation to Delaware to thwart possible unfriendly takeovers. There, certain defensive tactics against takeovers can be approved by the board of directors alone, without a vote by shareholders.

• Alternative Terminology

The charter is often referred to as the articles of incorporation.

After the government approves the application, it grants a charter. The charter may be an approved copy of the application form, or it may be a separate document containing the same basic data. Upon receipt of its charter, the corporation establishes by-laws. The by-laws establish the internal rules and procedures for conducting the affairs of the corporation. Corporations engaged in commerce outside their state or country must also obtain a license from each of those governments in which they do business. The license subjects the corporation’s operating activities to the general corporation laws of that state or country.

Costs incurred in the formation of a corporation are called organization costs. These costs include legal and government fees, and promotional expenditures involved in the organization of the business. Corporations expense organization costs as incurred. Determining the amount and timing of future benefits is so difficult that it is standard procedure to take a conservative approach of expensing these costs immediately.

Ownership Rights of Shareholders

When chartered, the corporation may begin selling ownership rights in the form of shares. When a corporation has only one class of shares, it is ordinary shares. Each ordinary share gives the shareholder the ownership rights pictured in Illustration 11-3 (page 542). The articles of incorporation or the by-laws state the ownership rights of a share.

Proof of share ownership is evidenced by a form known as a share certificate. As Illustration 11-4 shows (page 542), the face of the certificate shows the name of the corporation, the shareholder’s name, the class and special features of the share, the number of shares owned, and the signatures of authorized corporate officials. Prenumbered certificates facilitate accountability. They may be issued for any quantity of shares.

Share Issue Considerations

In considering the issuance of shares, a corporation must resolve a number of basic questions: How many shares should it authorize for sale? How should it issue the shares? At what price should it issue the shares? What value should the corporation assign to the shares? These questions are addressed in the following sections.

Illustration 11-3 Ownership rights of shareholders

Illustration 11-4 A share certifi cate

AUTHORIZED SHARES

The charter indicates the amount of shares that a corporation is authorized to sell. The total amount of authorized shares at the time of incorporation normally anticipates both initial and subsequent capital needs. As a result, the number of shares authorized generally exceeds the number initially sold. If it sells all authorized shares, a corporation must obtain consent of the jurisdiction to amend its charter before it can issue additional shares.

The authorization of ordinary shares does not result in a formal accounting entry. The reason is that the event has no immediate effect on either corporate assets or equity. However, the number of authorized shares is often reported in the equity section. It is then simple to determine the number of unissued shares that the corporation can issue without amending the charter: subtract the total shares issued from the total authorized. For example, if Quanta Computer (TWN) was authorized to sell 100,000 ordinary shares and issued 80,000 shares, 20,000 shares would remain unissued.

ISSUANCE OF SHARES

A corporation can issue ordinary shares directly to investors. Alternatively, it can issue the shares indirectly through an investment banking firm that specializes in bringing securities to the attention of prospective investors. Direct issue is typical in closely held companies. Indirect issue is customary for a publicly held corporation.

In an indirect issue, the investment banking firm may agree to underwrite the entire share issue. In this arrangement, the investment banker buys the shares from the corporation at a stipulated price and resells them to investors. The corporation thus avoids any risk of being unable to sell the shares. Also, it obtains immediate use of the cash received from the underwriter. The investment banking firm, in turn, assumes the risk of reselling the shares, in return for an underwriting fee. For example, Google (USA) (the world’s number-one Internet search engine) used underwriters when it issued a highly successful initial public offering, raising $1.67 billion. The underwriters charged a 3% underwriting fee (approximately $50 million) on Google’s share offering.

How does a corporation set the price for a new issue of shares? Among the factors to be considered are (1) the company’s anticipated future earnings, (2) its expected dividend rate per share, (3) its current financial position, (4) the current state of the economy, and (5) the current state of the securities market. The calculation can be complex and is properly the subject of a finance course.

MARKET PRICE OF SHARES

The shares of publicly held companies are traded on organized exchanges. The interaction between buyers and sellers determines the prices per share. In general, the prices set by the marketplace tend to follow the trend of a company’s earnings and dividends. But, factors beyond a company’s control, such as an oil embargo, changes in interest rates, or the outcome of a presidential election, may cause day-to-day fluctuations in market prices.

The trading of ordinary shares on securities exchanges involves the transfer of already issued shares from an existing shareholder to another investor. These transactions have no impact on a corporation’s equity.

PAR AND NO-PAR VALUE SHARES

Par value shares (sometimes nominal) are ordinary shares to which the charter has assigned a value per share. Years ago, par value determined the legal capital per share that a company must retain in the business for the protection of corporate creditors; that amount was not available for withdrawal by shareholders. Thus, in the past, most governments required the corporation to sell its shares at par or above.

However, par value was often immaterial relative to the value of the company’s shares—even at the time of issue. Thus, its usefulness as a protective device to creditors was questionable. For example, Loews Corporation’s (USA) par value is $0.01 per share, yet a new issue in 2014 would have sold at a market price in the $44 per share range. Thus, par has no relationship with market price. In the vast majority of cases, it is an immaterial amount. As a consequence, today many governments do not require a par value. Instead, they use other means to protect creditors.

No-par value shares are ordinary shares to which the charter has not assigned a value. No-par value shares are fairly common today. For example, Nike (USA) and Anheuser-Busch InBev (BEL) both have no-par shares. In many countries, the board of directors assigns a stated value to no-par shares.

Corporate Capital

Equity is identified by various names: stockholders’ equity, shareholders’ equity, or corporate capital. The equity section of a corporation’s statement of financial position consists of two parts: (1) share capital and (2) retained earnings (earned capital).

The distinction between share capital and retained earnings is important from both a legal and a financial point of view. Legally, corporations can make distributions of earnings (declare dividends) out of retained earnings in most countries. However, they often cannot declare dividends out of share capital. Management, shareholders, and others often look to retained earnings for the continued existence and growth of the corporation.

SHARE CAPITAL

Share capital is the total amount of cash and other assets paid in to the corporation by shareholders in exchange for shares. As noted earlier, when a corporation has only one class of shares, they are ordinary shares.

RETAINED EARNINGS

Retained earnings is net income that a corporation retains for future use. Net income is recorded in Retained Earnings by a closing entry that debits Income Summary and credits Retained Earnings. For example, assuming that net income for Delta Robotics in its first year of operations is HK$1,300,000, the closing entry is:

| Income Summary | 1,300,000 | |

| Retained Earnings | 1,300,000 | |

| (To close Income Summary and transfer net income to Retained Earnings) |

If Delta Robotics has a balance of HK$8,000,000 in Share Capital—Ordinary at the end of its first year, its equity section is as follows.

Illustration 11-5 Equity section

Illustration 11-6 compares the equity accounts reported on a statement of financial position for a proprietorship and a corporation.

Illustration 11-6 Comparison of equity accounts

Accounting for Share Transactions

Learning Objective 2

Record the issuance of ordinary shares.

Accounting for Ordinary Share Issues

Let’s now look at how to account for issues of ordinary shares. The primary objective in accounting for the issuance of ordinary shares is to identify the specific sources of capital.

ISSUING PAR VALUE ORDINARY SHARES FOR CASH

As discussed earlier, par value does not indicate a share’s market price. Therefore, the cash proceeds from issuing par value shares may be equal to, greater than, or less than par value. When the company records issuance of ordinary shares for cash, it credits the par value of the shares to Share Capital—Ordinary. It records in a separate account the portion of the proceeds that is above or below par value.

To illustrate, assume that Hydro-Slide SA issues 1,000 shares of €1 par value ordinary shares at par for cash. The entry to record this transaction is:

| Cash | 1,000 | |

| Share Capital—Ordinary | 1,000 | |

| (To record issuance of 1,000 €1 par ordinary shares at par) |

Now assume that Hydro-Slide issues an additional 1,000 shares of the €1 par value ordinary shares for cash at €5 per share. The amount received above the par value, in this case , is credited to Share Premium—Ordinary. The entry is:

| Cash | 5,000 | |

| Share Capital—Ordinary | 1,000 | |

| Share Premium—Ordinary | 4,000 | |

| (To record issuance of 1,000 €1 par ordinary shares) |

The total capital from these two transactions is €6,000, and the legal capital is €2,000. Assuming Hydro-Slide has retained earnings of €27,000, Illustration 11-7 (page 548) shows the company’s equity section.

Illustration 11-7 Share premium

When a corporation issues shares for less than par value, it debits the account Share Premium—Ordinary if a credit balance exists in this account. If a credit balance does not exist, then the corporation debits to Retained Earnings the amount less than par. This situation occurs only rarely. Most jurisdictions do not permit the sale of ordinary shares below par value because shareholders may be held personally liable for the difference between the price paid upon original sale and par value.

ISSUING NO-PAR ORDINARY SHARES FOR CASH

When no-par ordinary shares have a stated value, the entries are similar to those illustrated for par value shares. The corporation credits the stated value to Share Capital—Ordinary. Also, when the selling price of no-par shares exceeds stated value, the corporation credits the excess to Share Premium—Ordinary.

For example, assume that instead of €1 par value shares, Hydro-Slide SA has €5 stated value no-par shares and the company issues 5,000 shares at €8 per share for cash. The entry is:

| Cash | 40,000 | |

| Share Capital—Ordinary | 25,000 | |

| Share Premium—Ordinary | 15,000 | |

| (To record issuance of 5,000 €5 stated value no-par shares) |

Hydro-Slide reports Share Premium—Ordinary below Share Capital—Ordinary in the equity section.

What happens when no-par shares do not have a stated value? In that case, the corporation credits the entire proceeds to Share Capital—Ordinary. Thus, if Hydro-Slide does not assign a stated value to its no-par shares, it records the issuance of the 5,000 shares at €8 per share for cash as follows.

| Cash | 40,000 | |

| Share Capital—Ordinary | 40,000 | |

| (To record issuance of 5,000 no-par shares) |

ISSUING ORDINARY SHARES FOR SERVICES OR NON-CASH ASSETS

Corporations also may issue shares for services (compensation to attorneys or consultants) or for non-cash assets (land, buildings, and equipment). In such cases, what cost should be recognized in the exchange transaction? To comply with the historical cost principle, in a non-cash transaction cost is the cash equivalent price. Thus, cost is either the fair value of the consideration given up or the fair value of the consideration received, whichever is more clearly determinable.

To illustrate, assume that attorneys have helped Jordan Company incorporate. They have billed the company €5,000 for their services. They agree to accept 4,000 shares of €1 par value ordinary shares in payment of their bill. At the time of the exchange, there is no established market price for the shares. In this case, the fair value of the consideration received, €5,000, is more clearly evident. Accordingly, Jordan makes the following entry.

| Organization Expense | 5,000 | |

| Share Capital—Ordinary | 4,000 | |

| Share Premium—Ordinary | 1,000 | |

| (To record issuance of 4,000 €1 par value shares to attorneys) |

As explained on page 541, organization costs are expensed as incurred.

In contrast, assume that Athletic Research AG is an existing publicly held corporation. Its €5 par value shares are actively traded at €8 per share. The company issues 10,000 shares to acquire land recently advertised for sale at €90,000. The most clearly evident value in this non-cash transaction is the market price of the consideration given, €80,000. The company records the transaction as follows.

| Land | 80,000 | |

| Share Capital—Ordinary | 50,000 | |

| Share Premium—Ordinary | 30,000 | |

| (To record issuance of 10,000 €5 par value shares for land) |

As illustrated in these examples, the par value of the shares is never a factor in determining the cost of the assets received. This is also true of the stated value of no-par shares.

Accounting for Treasury Shares

Learning Objective 3

Explain the accounting for treasury shares.

Treasury shares are a corporation’s own shares that it has issued and subsequently reacquired from shareholders but not retired. A corporation may acquire treasury shares for various reasons:

- To reissue the shares to officers and employees under bonus and share compensation plans.

- To signal to the securities market that management believes the shares are underpriced, in the hope of enhancing its market price.

- To have additional shares available for use in the acquisition of other companies.

- To reduce the number of shares outstanding and thereby increase earnings per share.

Another infrequent reason for purchasing shares is that management may want to eliminate hostile shareholders by buying them out.

• HELPFUL HINT

Treasury shares do not have dividend rights or voting rights.

Many corporations have treasury shares. In fact, over 50% of IFRS companies have treasury shares. As examples, adidas (DEU) and Lenovo (CHN) report purchasing treasury shares in recent years.

PURCHASE OF TREASURY SHARES

Companies generally account for treasury shares by the cost method. This method uses the cost of the shares purchased to value the treasury shares. Under the cost method, the company debits Treasury Shares for the price paid to reacquire the shares. When the company disposes of the shares, it credits to Treasury Shares the same amount it paid to reacquire the shares.

To illustrate, assume that on January 1, 2017, the equity section of Mead, Ltd. has 100,000 HK$50 par value ordinary shares outstanding (all issued at par value) and Retained Earnings of HK$2,000,000. The equity section before purchase of treasury shares is as follows.

Illustration 11-8 Equity section with no treasury shares

On February 1, 2017, Mead acquires 4,000 of its shares at HK$80 per share. The entry is:

| Feb. 1 | Treasury Shares | 320,000 | |

| Cash | 320,000 | ||

| (To record purchase of 4,000 treasury shares at HK$80 per share) |

Mead debits Treasury Shares for the cost of the shares purchased. Is the original Share Capital—Ordinary account affected? No, because the number of issued shares does not change. In the equity section of the statement of financial position, Mead deducts treasury shares after retained earnings to determine total equity. Treasury Shares is a contra equity account. Thus, the acquisition of treasury shares reduces equity.

The equity section of Mead after purchase of treasury shares is as follows.

Illustration 11-9 Equity section with treasury shares

Mead discloses in the statement of financial position both the number of shares issued (100,000) and the number in the treasury (4,000). The difference is the number of shares outstanding (96,000). The term outstanding shares means the number of issued shares that are being held by shareholders.

Some maintain that companies should report treasury shares as an asset because they can be sold for cash. But under this reasoning, companies would also show unissued shares as an asset, which is clearly incorrect. Rather than being an asset, treasury shares reduce shareholder claims on corporate assets. This effect is correctly shown by reporting treasury shares as a deduction from equity.

DISPOSAL OF TREASURY SHARES

Treasury shares are usually sold or retired. The accounting for their sale differs when treasury shares are sold above cost than when they are sold below cost.

• HELPFUL HINT

Treasury share transactions are classified as equity transactions. As in the case when shares are issued, the income statement is not involved.

SALE OF TREASURY SHARES ABOVE COST If the selling price of the treasury shares is equal to their cost, the company records the sale of the shares by a debit to Cash and a credit to Treasury Shares. When the selling price of the shares is greater than their cost, the company credits the difference to Share Premium—Treasury.

To illustrate, assume that on July 1, Mead, Ltd. sells for HK$100 per share 1,000 of the 4,000 treasury shares previously acquired at HK$80 per share. The entry is as follows.

| July 1 | Cash | 100,000 | |

| Treasury Shares | 80,000 | ||

| Share Premium—Treasury | 20,000 | ||

| (To record sale of 1,000 treasury shares above cost) |

Mead does not record a HK$20,000 gain on sale of treasury shares because (1) gains on sales occur when assets are sold, and treasury shares are not an asset, and (2) a corporation does not realize a gain or suffer a loss from share transactions with its own shareholders. Thus, companies should not include in net income any capital arising from the sale of treasury shares. Instead, they report Share Premium—Treasury separately on the statement of financial position, as a part of equity.

SALE OF TREASURY SHARES BELOW COST When a company sells treasury shares below their cost, it usually debits to Share Premium—Treasury the excess of cost over selling price. Thus, if Mead sells an additional 800 treasury shares on October 1 at HK$70 per share, it makes the following entry.

| Oct. 1 | Cash | 56,000 | |

| Share Premium—Treasury | 8,000 | ||

| Treasury Shares | 64,000 | ||

| (To record sale of 800 treasury shares below cost) |

Observe the following from the two sales entries. (1) Mead credits Treasury Shares at cost in each entry. (2) Mead uses Share Premium—Treasury for the difference between cost and the resale price of the shares. (3) The original Share Capital—Ordinary account is not affected. The sale of treasury shares increases both total assets and total equity.

After posting the foregoing entries, the treasury share accounts will show the following balances on October 1.

Illustration 11-10 Treasury share accounts

When a company fully depletes the credit balance in Share Premium—Treasury, it debits to Retained Earnings any additional excess of cost over selling price. To illustrate, assume that Mead sells its remaining 2,200 shares at HK$70 per share on December 1. The excess of cost over selling price is . In this case, Mead debits HK$12,000 of the excess to Share Premium—Treasury. It debits the remainder to Retained Earnings. The entry is:

| Dec. 1 | Cash | 154,000 | |

| Share Premium—Treasury | 12,000 | ||

| Retained Earnings | 10,000 | ||

| Treasury Shares | 176,000 | ||

| (To record sale of 2,200 treasury shares at HK$70 per share) |

Accounting for Preference Shares

Learning Objective 4

Differentiate preference shares from ordinary shares.

To appeal to more investors, a corporation may issue an additional class of shares, called preference shares. Preference shares have contractual provisions that give them some preference or priority over ordinary shares. Typically, preference shareholders have a priority as to (1) distributions of earnings (dividends) and (2) assets in the event of liquidation. However, they sometimes do not have voting rights.

Like ordinary shares, corporations may issue preference shares for cash or for non-cash assets. The entries for these transactions are similar to the entries for ordinary shares. When a corporation has more than one class of shares, each capital account title should identify the shares to which it relates. A company might have the following accounts: Share Capital—Preference, Share Capital—Ordinary, Share Premium—Preference, and Share Premium—Ordinary. For example, if Florence SpA issues 10,000 shares of €10 par value preference shares for €12 cash per share, the entry to record the issuance is:

| Cash | 120,000 | |

| Share Capital—Preference | 100,000 | |

| Share Premium—Preference | 20,000 | |

| (To record issuance of 10,000 €10 par value preference shares) |

Preference shares may have either a par value or no-par value. In the equity section of the statement of financial position, companies list preference shares first because of their dividend and liquidation preferences over ordinary shares.

We discuss various features associated with the issuance of preference shares on the following pages.

DIVIDEND PREFERENCES

Preference shareholders have the right to receive dividends before ordinary shareholders. For example, if the dividend rate on preference shares is €5 per share, ordinary shareholders will not receive any dividends in the current year until preference shareholders have received €5 per share. The first claim to dividends does not, however, guarantee the payment of dividends. Dividends depend on many factors, such as adequate retained earnings and availability of cash. If a company does not pay dividends to preference shareholders, it cannot pay dividends to ordinary shareholders.

For preference shares, companies state the per share dividend amount as a percentage of the par value or as a specified amount. For example, Earthlink (USA) specifies a 3% dividend on its $100 par value preference shares. Rostelecom (RUS) specifies preference dividends as the higher of 10% of net income or the dividend paid to ordinary shareholders.

CUMULATIVE DIVIDEND Preference shares often contain a cumulative dividend feature. This feature stipulates that preference shareholders must be paid both current-year dividends and any unpaid prior-year dividends before ordinary shareholders are paid dividends. When preference shares are cumulative, preference dividends not declared in a given period are called dividends in arrears.

To illustrate, assume that Scientific Leasing has 5,000 shares of 7%, €100 par value, cumulative preference shares outstanding. Each €100 share pays a €7 dividend . The annual dividend is . If dividends are two years in arrears, preference shareholders are entitled to receive the dividends shown in Illustration 11-11.

Illustration 11-11 Computation of total dividends to preference shares

The company cannot pay dividends to ordinary shareholders until it pays the entire preference dividend. In other words, companies cannot pay dividends to ordinary shareholders while any preference dividends are in arrears.

Dividends in arrears are not considered a liability. No payment obligation exists until the board of directors formally declares that the company will pay a dividend. However, companies should disclose in the notes to the financial statements the amount of dividends in arrears. Doing so enables investors to assess the potential impact of this commitment on the corporation’s financial position.

The investment community does not look favorably on companies that are unable to meet their dividend obligations. As a financial officer noted in discussing one company’s failure to pay its cumulative preference dividend for a period of time, “Not meeting your obligations on something like that is a major black mark on your record.”

LIQUIDATION PREFERENCE

Most preference shares also have a preference on corporate assets if the corporation fails. This feature provides security for the preference shareholder. The preference to assets may be for the par value of the shares or for a specified liquidating value. The liquidation preference establishes the respective claims of creditors and preference shareholders in litigation involving bankruptcy lawsuits.

Dividends

Learning Objective 5

Prepare the entries for cash dividends and share dividends.

A dividend is generally a corporation’s distribution of cash or shares to its shareholders on a pro rata (proportional to ownership) basis. Pro rata means that if you own 10% of the ordinary shares, you will receive 10% of the dividend. Dividends can take four forms: cash, property, scrip (a promissory note to pay cash), or shares. Cash dividends predominate in practice although companies also declare share dividends with some frequency. These two forms of dividends are therefore the focus of discussion in this chapter.

Investors are very interested in a company’s dividend practices. In the financial press, dividends are generally reported quarterly on a per share basis. (Sometimes they are reported on an annual basis.) For example, in a recent year, BASF’s (DEU) dividend rate was €1.95 a share, The Hershey Company’s (USA) was $1.19, and Marks and Spencer plc’s (GBR) was 22.5p.

Cash Dividends

A cash dividend is a pro rata distribution of cash to shareholders. For a corporation to pay a cash dividend, it must have the following.

Retained earnings. The legality of a cash dividend depends on the laws of the state or country in which the company is incorporated. Payment of cash dividends from retained earnings is legal in all jurisdictions. In general, cash dividend distributions from only the balance in share capital—ordinary (legal capital) are illegal.

A dividend declared out of share capital or share premium is termed a liquidating dividend. Such a dividend reduces or “liquidates” the amount originally paid in by shareholders.

Adequate cash. The legality of a dividend and the ability to pay a dividend are two different things. For example, adidas (DEU), with retained earnings of over €5.0 billion, could legally declare a dividend of at least €5.0 billion. But adidas’ cash balance is only €1.6 billion.

Before declaring a cash dividend, a company’s board of directors must carefully consider both current and future demands on the company’s cash resources. In some cases, current liabilities may make a cash dividend inappropriate. In other cases, a major plant expansion program may warrant only a relatively small dividend.

- A declaration of dividends. A company does not pay dividends unless its board of directors decides to do so, at which point the board “declares” the dividend. The board of directors has full authority to determine the amount of income to distribute in the form of a dividend and the amount to retain in the business. Dividends do not accrue like interest on a note payable, and they are not a liability until declared.

The amount and timing of a dividend are important issues for management to consider. The payment of a large cash dividend could lead to liquidity problems for the company. On the other hand, a small dividend or a missed dividend may cause unhappiness among shareholders. Many shareholders expect to receive a reasonable cash payment from the company on a periodic basis. Many companies declare and pay cash dividends quarterly. On the other hand, a number of high-growth companies pay no dividends, preferring to conserve cash to finance future capital expenditures.

ENTRIES FOR CASH DIVIDENDS

Three dates are important in connection with dividends: (1) the declaration date, (2) the record date, and (3) the payment date. Normally, there are two to four weeks between each date. Companies make accounting entries on the declaration date and the payment date.

On the declaration date, the board of directors formally declares (authorizes) the cash dividend and announces it to shareholders. Declaration of a cash dividend commits the corporation to a legal obligation. The obligation is binding and cannot be rescinded. The company makes an entry to recognize the increase in Cash Dividends and the increase in the liability Dividends Payable.

To illustrate, assume that on December 1, 2017, the directors of Media General declare a €0.50 per share cash dividend on 100,000 €10 par value ordinary shares. The dividend is . The entry to record the declaration is:

| Declaration Date | |||

| Dec. 1 | Cash Dividends | 50,000 | |

| Dividends Payable | 50,000 | ||

| (To record declaration of cash dividend) | |||

Media General debits the account Cash Dividends. Cash dividends decrease retained earnings. We use the specific title Cash Dividends to differentiate it from other types of dividends, such as share dividends. Dividends Payable is a current liability. It will normally be paid within the next several months.

Whichever account is used for the dividend declaration, the effect is the same: Retained Earnings decreases, and a current liability increases. For homework problems, you should use the Cash Dividends account for recording dividend declarations.

• HELPFUL HINT

The purpose of the record date is to identify the persons or entities that will receive the dividend, not to determine the amount of the dividend liability.

At the record date, the company determines ownership of the outstanding shares for dividend purposes. The shareholders’ records maintained by the corporation supply this information. In the interval between the declaration date and the record date, the corporation updates its share ownership records. For Media General, the record date is December 22. No entry is required on this date because the corporation’s liability recognized on the declaration date is unchanged.

| Record Date | |||

| Dec. 22 | No entry | ||

On the payment date, the company makes cash dividend payments to the shareholders of record (as of December 22) and records the payment of the dividend. If January 20 is the payment date for Media General, the entry on that date is as follows.

| Payment Date | |||

| Jan. 20 | Dividends Payable | 50,000 | |

| Cash | 50,000 | ||

| (To record payment of cash dividend) | |||

Note that payment of the dividend reduces both current assets and current liabilities. It has no effect on equity. The cumulative effect of the declaration and payment of a cash dividend is to decrease both equity and total assets. Illustration 11-2 summarizes the three important dates associated with dividends for Media General.

Illustration 11-12 Key dividend dates

When using a Cash Dividends account, Media General should transfer the balance of that account to Retained Earnings at the end of the year by a closing entry. The entry for Media General at closing is as follows.

| Retained Earnings | 50,000 | |

| Cash Dividends | 50,000 | |

| (To close Cash Dividends to Retained Earnings) |

ALLOCATING CASH DIVIDENDS BETWEEN PREFERENCE AND ORDINARY SHARES

As indicated, preference shares have priority over ordinary shares in regard to dividends. Holders of cumulative preference shares must be paid any unpaid prior-year dividends and their current year’s dividend before ordinary shareholders receive dividends.

To illustrate, assume that at December 31, 2017, IBR SE has 1,000 shares of 8%, €100 par value cumulative preference shares. It also has 50,000 €10 par value ordinary shares outstanding. The dividend per share for preference shares is . The required annual dividend for preference shares is therefore . At December 31, 2017, the directors declare a €6,000 cash dividend. In this case, the entire dividend amount goes to preference shareholders because of their dividend preference. The entry to record the declaration of the dividend is:

| Dec. 31 | Cash Dividends | 6,000 | |

| Dividends Payable | 6,000 | ||

| (To record €6 per share cash dividend to preference shareholders) |

Because of the cumulative feature, dividends of per share are in arrears on preference shares for 2017. IBR must pay these dividends to preference shareholders before it can pay any future dividends to ordinary shareholders. IBR should disclose dividends in arrears in the financial statements.

At December 31, 2018, IBR declares a €50,000 cash dividend. The allocation of the dividend to the two classes of shares is as follows.

Illustration 11-13 Allocating dividends to preference and ordinary shares

The entry to record the declaration of the dividend is as follows.

| Dec. 31 | Cash Dividends | 50,000 | |

| Dividends Payable | 50,000 | ||

| (To record declaration of cash dividends of €10,000 to preference shares and €40,000 to ordinary shares) |

If IBR’s preference shares are not cumulative, preference shareholders receive only €8,000 in dividends in 2018. Ordinary shareholders receive €42,000.

Share Dividends

A share dividend is a pro rata distribution to shareholders of the corporation’s own shares. Whereas a company pays cash in a cash dividend, a company issues shares in a share dividend. A share dividend results in a decrease in retained earnings and an increase in share capital and share premium. Unlike a cash dividend, a share dividend does not decrease total equity or total assets.

To illustrate, assume that you have a 2% ownership interest in Cetus Ltd.; you own 20 of its 1,000 ordinary shares. If Cetus declares a 10% share dividend, it would issue 100 shares . You would receive two shares . Would your ownership interest change? No, it would remain at 2% . You now own more shares, but your ownership interest has not changed. Illustration 11-14 shows the effect of a share dividend for shareholders.

Illustration 11-14 Effect of share dividend for shareholders

Cetus has disbursed no cash and has assumed no liabilities. What, then, are the purposes and benefits of a share dividend? Corporations issue share dividends generally for one or more of the following reasons.

- To satisfy shareholders’ dividend expectations without spending cash.

- To increase the marketability of the corporation’s shares. When the number of shares outstanding increases, the market price per share decreases. Decreasing the market price of the shares makes it easier for smaller investors to purchase the shares.

- To emphasize that a portion of equity has been permanently reinvested in the business (and is unavailable for cash dividends).

When the dividend is declared, the board of directors determines the size of the share dividend and the value assigned to each dividend.

IFRS is silent regarding the accounting for share dividends. One approach used in some countries is that if the company issues a small share dividend (less than 20–25% of the corporation’s issued shares), the value assigned to the dividend is the fair value (market price) per share. This treatment is based on the assumption that a small share dividend will have little effect on the market price of the shares previously outstanding. Thus, many shareholders consider small share dividends to be distributions of earnings equal to the fair value of the shares distributed. If a company issues a large share dividend (greater than 20–25%), the value assigned to the dividend is the par or stated value. Small share dividends predominate in practice. Thus, we will illustrate only entries for small share dividends.

ENTRIES FOR SHARE DIVIDENDS

To illustrate the accounting for small share dividends, assume that Danshui Ltd. has a balance of NT$3,000,000 in retained earnings. It declares a 10% share dividend on its 50,000 shares of NT$100 par value ordinary shares. The current fair value of its shares is NT$150 per share. The number of shares to be issued is . Therefore, the total amount to be debited to Share Dividends is . The entry to record the declaration of the share dividend is as follows.

| Share Dividends | 750,000 | |

| Ordinary Share Dividends Distributable | 500,000 | |

| Share Premium—Ordinary | 250,000 | |

| (To record declaration of 10% share dividend) |

Danshui debits Share Dividends for the fair value of the shares issued . (Similar to Cash Dividends, Share Dividends decrease retained earnings.) Danshui also credits Ordinary Share Dividends Distributable for the par value of the dividend shares and credits Share Premium—Ordinary for the excess over par .

Ordinary Share Dividends Distributable is an equity account. It is not a liability because assets will not be used to pay the dividend. If the company prepares a statement of financial position before it issues the dividend shares, it reports the distributable account as shown in Illustration 11-15.

Illustration 11-15 Statement presentation of ordinary share dividends distributable

When Danshui issues the dividend shares, it debits Ordinary Share Dividends Distributable and credits Share Capital—Ordinary, as follows.

| Ordinary Share Dividends Distributable | 500,000 | |

| Share Capital—Ordinary | 500,000 | |

| (To record issuance of 5,000 shares in a share dividend) |

EFFECTS OF SHARE DIVIDENDS

How do share dividends affect equity? They change the composition of equity because they transfer a portion of retained earnings to share capital and share premium. However, total equity remains the same. Share dividends also have no effect on the par or stated value per share, but the number of shares outstanding increases. Illustration 11-16 shows these effects for Danshui Ltd.

Illustration 11-16 Share dividend effects

In this example, the total of share capital—ordinary and share premium—ordinary increases by and retained earnings decreases by the same amount. Note also that total equity remains unchanged at NT$8,000,000. The number of shares increases by .

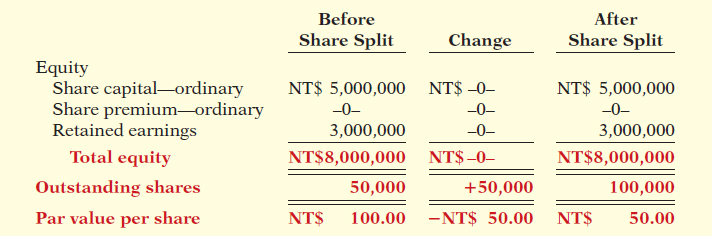

Share Splits

A share split, like a share dividend, involves issuance of additional shares to shareholders according to their percentage ownership. However, a share split results in a reduction in the par or stated value per share. The purpose of a share split is to increase the marketability of the shares by lowering the market price per share. This, in turn, makes it easier for the corporation to issue additional shares.

The effect of a split on market price is generally inversely proportional to the size of the split. For example, after a 2-for-1 share split, the market price of Nike’s (USA) shares fell from $111 to approximately $55. The lower market price stimulated market activity, and within one year the shares were trading above $100 again.

In a share split, the company increases the number of shares in the same proportion that par or stated value per share decreases. For example, in a 2-for-1 split, the company exchanges one $10 par value share for two $5 par value shares. A share split does not have any effect on share capital, share premium, retained earnings, or total equity. However, the number of shares outstanding increases, and par value per share decreases. Illustration 11-17 shows these effects for Danshui Ltd., assuming that it splits its 50,000 ordinary shares on a 2-for-1 basis.

Illustration 11-17 Share split effects

A share split does not affect the balances in any equity accounts. Therefore, a company does not need to journalize a share split.

• HELPFUL HINT

A share split changes the par value per share but does not affect any balances in equity.

Illustration 11-18 summarizes the differences between share dividends and share splits.

Illustration 11-18 Differences between the effects of share dividends and share splits

Retained Earnings

Learning Objective 6

Identify the items reported in a retained earnings statement.

Recall that retained earnings is net income that a company retains in the business. The balance in retained earnings is part of the shareholders’ claim on the total assets of the corporation. It does not, though, represent a claim on any specific asset. Nor can the amount of retained earnings be associated with the balance of any asset account. For example, a NT$10,000,000 balance in retained earnings does not mean that there should be NT$10,000,000 in cash. The reason is that the company may have used the cash resulting from the excess of revenues over expenses to purchase buildings, equipment, and other assets.

To demonstrate that retained earnings and cash may be quite different, Illustration 11-19 shows recent amounts of retained earnings and cash in selected companies.

Illustration 11-19 Retained earnings and cash balances

Remember that when a company has net income, it closes net income to retained earnings. The closing entry is a debit to Income Summary and a credit to Retained Earnings.

• HELPFUL HINT

Remember that Retained Earnings is an equity account, whose normal balance is a credit.

When a company has a net loss (expenses exceed revenues), it also closes this amount to retained earnings. The closing entry in this case is a debit to Retained Earnings and a credit to Income Summary. To illustrate, assume that Rendle Corporation has a net loss of $400,000 in 2017. The closing entry to record this loss is as follows.

| Retained Earnings | 400,000 | |

| Income Summary | 400,000 | |

| (To close net loss to Retained Earnings) |

This closing entry is done even if it results in a debit balance in Retained Earnings. Companies do not debit net losses to share capital or share premium. If cumulative losses exceed cumulative income over a company’s life, a debit balance in Retained Earnings results. A debit balance in Retained Earnings is identified as a deficit. A company reports a deficit as a deduction in the equity section, as shown below.

Illustration 11-20 Equity with deficit

The balance in retained earnings is generally available for dividend declarations. In some cases, however, there may be retained earnings restrictions. These make a portion of the retained earnings balance currently unavailable for dividends. Restrictions result from one or more of the following causes.

- Legal restrictions. Many governments require a corporation to restrict retained earnings for the cost of treasury shares purchased. The restriction keeps intact the corporation’s legal capital that is being temporarily held as treasury shares. When the company sells the treasury shares, the restriction is lifted.

- Contractual restrictions. Long-term debt contracts may restrict retained earnings as a condition for the loan. The restriction limits the use of corporate assets for payment of dividends. Thus, it increases the likelihood that the corporation will be able to meet required loan payments.

- Voluntary restrictions. The board of directors may voluntarily create retained earnings restrictions for specific purposes. For example, the board may authorize a restriction for future plant expansion. By reducing the amount of retained earnings available for dividends, the company makes more cash available for the planned expansion.

Companies generally disclose retained earnings restrictions in the notes to the financial statements. For example, as shown in Illustration 11-21, Tektronix Inc. (USA), a manufacturer of electronic measurement devices, had total retained earnings of $774 million, but the unrestricted portion was only $223.8 million.

Illustration 11-21 Disclosure of restriction

Prior Period Adjustments

Suppose that a company has closed its books and issued financial statements. The company then discovers that it made a material error in reporting net income of a prior year. How should the company record this situation in the accounts and report it in the financial statements?

The correction of an error in previously issued financial statements is known as a prior period adjustment. The company makes the correction directly to Retained Earnings because the effect of the error is now in this account. The net income for the prior period has been recorded in retained earnings through the journalizing and posting of closing entries.

To illustrate, assume that General Microwave AG discovers in 2017 that it understated depreciation expense on equipment in 2016 by £300,000 due to computational errors. These errors overstated both net income for 2016 and the current balance in retained earnings. The entry for the prior period adjustment, ignoring all tax effects, is as follows.

| Retained Earnings | 300,000 | |

| Accumulated Depreciation—Equipment | 300,000 | |

| (To adjust for understatement of depreciation in a prior period) |

A debit to an income statement account in 2017 is incorrect because the error pertains to a prior year.

Companies report prior period adjustments in the retained earnings statement. They add (or deduct, as the case may be) these adjustments from the beginning retained earnings balance. This results in an adjusted beginning balance. For example, assuming a beginning balance of £800,000 in retained earnings, General Microwave reports the prior period adjustment as follows.

Illustration 11-22 Statement presentation of prior period adjustments

Again, reporting the correction in the current year’s income statement would be incorrect because it applies to a prior year’s income statement.

Retained Earnings Statement

The retained earnings statement shows the changes in retained earnings during the year. The company prepares the statement from the Retained Earnings account. Illustration 11-23 shows (in T-account form) transactions that affect retained earnings.

Illustration 11-23 Debits and credits to retained earnings

As indicated, net income increases retained earnings, and a net loss decreases retained earnings. Prior period adjustments may either increase or decrease retained earnings. Both cash dividends and share dividends decrease retained earnings. The circumstances under which treasury share transactions decrease retained earnings are explained on page 552.

A complete retained earnings statement for Graber SA, based on assumed data, is as follows.

Illustration 11-24 Retained earnings statement

Statement Presentation and Analysis

Learning Objective 7

Prepare and analyze a comprehensive equity section.

The equity section of the statement of financial position reports share capital, share premium, and retained earnings.

- Share capital. This category consists of preference and ordinary shares. Preference shares are shown before ordinary shares because of their preferential rights. Par value, shares authorized, shares issued, and shares outstanding are reported for each class of shares.

- Share premium. This includes the excess of amounts paid over par or stated value and share premium from treasury shares.

Presentation

Illustration 11-25 presents the equity section of Graber SA’s statement of financial position. Note the following: (1) “Ordinary share dividends distributable” is shown under “Share capital—ordinary” and (2) A note (Note R) discloses a retained earnings restriction.

Illustration 11-25 Comprehensive equity section

The equity section of Graber SA in Illustration 11-25 includes most of the accounts discussed in this chapter. The disclosures pertaining to Graber’s ordinary shares indicate that the company issued 400,000 shares; 100,000 shares are unissued (500,000 authorized less 400,000 issued); and 390,000 shares are outstanding (400,000 issued less 10,000 shares in treasury).

Published annual reports often combine and report as a single amount the individual sources of share premium, as shown in Illustration 11-26. In addition, authorized shares are sometimes not reported. Finally, notice the line labeled “Reserves.”

Illustration 11-26 Equity section

Under IFRS, companies often use the term “Reserves” for forms of equity other than that contributed by shareholders. Reserves sometimes includes retained earnings. More commonly, this line item is used to report the equity impact of comprehensive income items, such as the Revaluation Surplus that resulted from the revaluation of property, plant, and equipment in Chapter 9.

Instead of presenting a detailed equity section in the statement of financial position and a retained earnings statement, many companies prepare a statement of changes in equity. This statement shows the changes (1) in each equity account and (2) in total that occurred during the year. An example of an equity statement is illustrated in an appendix to this chapter (see Illustration 11-26).

Analysis

Investors and analysts can measure profitability from the viewpoint of the investor in ordinary shares by the return on ordinary shareholders’ equity. This ratio, as shown below for Carrefour (FRA), indicates how many euros of net income the company earned for each euro invested by the ordinary shareholders. It is computed by dividing net income available to ordinary shareholders (which is net income minus preference dividends) by average ordinary shareholders’ equity.

Carrefour’s beginning-of-the-year and end-of-the-year ordinary shareholders’ equity were €8,047 and €8,597 million, respectively. Its net income was €1,263 million, and no preference shares were outstanding. The return on ordinary shareholders’ equity is computed as follows.

Illustration 11-27 Return on ordinary shareholders’ equity and computation

As shown above, if a company has preference shares, we deduct the amount of preference dividends from the company’s net income to compute income available to ordinary shareholders. Also, the par value of preference shares is deducted from total average shareholders’ equity to arrive at the amount of ordinary shareholders’ equity.

APPENDIX 11A Statement of Changes in Equity

Learning Objective *8

Describe the use and content of the statement of changes in equity.

When statements of financial position and income statements are presented by a corporation, changes in the separate accounts comprising equity should also be disclosed. Disclosure of such changes is necessary to make the financial statements sufficiently informative for users. The disclosures are made in an additional statement called the statement of changes in equity. The statement shows the changes in each equity account and in total equity during the year. As shown in Illustration 11-26, the statement is prepared in columnar form. It contains columns for each account and for total equity. The transactions are then identified and their effects are shown in the appropriate columns.

Illustration 11A-1 Statement of changes in equity

In practice, additional columns are usually provided to show the number of shares of issued shares and treasury shares. When a statement of changes in equity is presented, a retained earnings statement is not necessary because the retained earnings column explains the changes in this account.

APPENDIX 11B Book Value—Another per Share Amount

Book Value per Share

Learning Objective *9

Compute book value per share.

You have learned about a number of per share amounts in this chapter. Another per share amount of some importance is book value per share. It represents the equity an ordinary shareholder has in the net assets of the corporation from owning one share. Remember that the net assets (total assets minus total liabilities) of a corporation must be equal to total equity. Therefore, the formula for computing book value per share when a company has only one class of shares outstanding is as follows.

Illustration 11B-1 Book value per share formula

Thus, if Marlo Corporation has total ordinary shareholders’ equity of $1,500,000 (share capital—ordinary $1,000,000 and retained earnings $500,000) and 50,000 shares of ordinary shares outstanding, book value per share is .

When a company has both preference and ordinary shares, the computation of book value is more complex. Since preference shareholders have a prior claim on net assets over ordinary shareholders, their equity must be deducted from total equity. Then we can determine the equity that applies to the ordinary shares. The computation of book value per share involves the following steps.

- Compute the preference share equity. This equity is equal to the sum of the call price of preference shares plus any cumulative dividends in arrears. If the preference shares do not have a call price, the par value of the shares is used.

- Determine the ordinary shareholders’ equity. Subtract the preference share equity from total equity.

- Determine book value per share. Divide ordinary shareholders’ equity by ordinary shares.

EXAMPLE

We will use the equity section of Graber SA shown in Illustration 11-25. Graber’s preference shares are callable at €120 per share and are cumulative. Assume that dividends on Graber’s preference shares were in arrears for one year, . The computation of preference share equity (Step 1 in the preceding list) is shown below.

Illustration 11B-2 Computation of preference share equity—Step 1

The computation of book value (Steps 2 and 3) is as follows.

Illustration 11B-3 Computation of book value per share with preference shares—Steps 2 and 3

Note that we used the call price of €120 instead of the par value of €100. Note also that share premium—preference, €30,000, is not assigned to the preference share equity. Preference shareholders ordinarily do not have a right to amounts contributed in excess of par value. Therefore, such amounts are assigned to the ordinary shareholders’ equity in computing book value.

Book Value versus Market Price

Be sure you understand that book value per share may not equal market price per share. Book value generally is based on recorded costs. Market price reflects the subjective judgments of thousands of shareholders and prospective investors about a company’s potential for future earnings and dividends. Market price per share may exceed book value per share, but that fact does not necessarily mean that the shares are overpriced. The correlation between book value and the annual range of a company’s market price per share is often remote, as indicated by the following recent data for some U.S. companies.

Illustration 11B-4 Book value and market price compared

Book value per share is useful in determining the trend of a shareholder’s per share equity in a corporation. It is also significant in many contracts and in court cases where the rights of individual parties are based on cost information.

GLOSSARY REVIEW

- Authorized shares

- The amount of shares that a corporation is authorized to sell as indicated in its charter. (p. 543).

- *B ook value per share

- The equity an ordinary shareholder has in the net assets of the corporation from owning one share. (p. 569).

- Cash dividend

- A pro rata distribution of cash to shareholders. (p. 555).

- Charter

- A document that sets forth important terms and features regarding the creation of a corporation. (p. 541).

- Corporation

- A business organized as a legal entity separate and distinct from its owners under corporation law. (p. 538).

- Cumulative dividend

- A feature of preference shares entitling the shareholder to receive current and unpaid prior-year dividends before ordinary shareholders receive any dividends. (p. 554).

- Declaration date

- The date the board of directors formally declares the dividend and announces it to shareholders. (p. 556).

- Defi cit

- A debit balance in retained earnings. (p. 563).

- Dividend

- A corporation’s distribution of cash or shares to its shareholders on a pro rata (proportional) basis. (p. 555).

- Liquidating dividend

- A dividend declared out of share capital or share premium. (p. 555).

- No-par value shares

- Shares that have not been assigned a value in the corporate charter. (p. 544).

- Organization costs

- Costs incurred in the formation of a corporation. (p. 541).

- Outstanding shares

- Shares that have been issued and are being held by shareholders. (p. 551).

- Par value shares

- (sometimes nominal) Capital shares that have been assigned a value per share in the corporate charter. (p. 544).

- Payment date

- The date dividends are transferred to shareholders. (p. 556).

- Preference shares

- Shares that have some contractual preferences over ordinary shares. (p. 553).

- Prior period adjustment

- The correction of an error in previously issued fi nancial statements. (p. 564).

- Privately held corporation

- A corporation that has only a few shareholders and whose shares are not available for sale to the general public. (p. 538).

- Publicly held corporation

- A corporation that may have thousands of shareholders and whose shares are regularly traded on a national securities exchange. (p. 538).

- Record date

- The date when ownership of outstanding shares is determined for dividend purposes. (p. 556).

- Retained earnings

- Net income that a corporation retains for future use. (p. 545).

- Retained earnings restrictions

- Circumstances that make a portion of retained earnings currently unavailable for dividends. (p. 563).

- Retained earnings statement

- A fi nancial statement that shows the changes in retained earnings during the year. (p. 564).

- Return on ordinary shareholders’ equity

- A ratio that measures profi tability from the shareholders’ point of view. It is computed by dividing net income available to ordinary shareholders by average ordinary shareholders’ equity. (p. 567).

- Share capital

- Cash and other assets paid into the corporation by shareholders in exchange for shares. (p. 545).

- Share dividend

- A pro rata distribution of the corporation’s own shares to shareholders. (p. 558).

- Share split

- The issuance of additional shares to shareholders accompanied by a reduction in the par or stated value per share. (p. 560).

- Stated value

- The amount per share assigned by the board of directors to no-par shares that become legal capital per share. (p. 544).

- Statement of changes in equity

- A statement that shows the changes in each equity account and in total equity during the year. (p. 566).

- Treasury shares

- A corporation’s own shares that the corporation has issued and reacquired but not retired. (p. 550).

PRACTICE MULTIPLE-CHOICE QUESTIONS

- Which of the following is not a major advantage of the corporate form of organization?

Separate legal existence.

Continuous life.

Government regulations.

Transferable ownership rights.

A major disadvantage of a corporation is:

limited liability of shareholders.

additional taxes.

transferable ownership rights.

separate legal existence.

Which of the following statements is false?

Ownership of ordinary shares gives the owner a voting right.

The equity section begins with a share capital section.

The authorization of share capital does not result in a formal accounting entry.

Par value and market price of a company’s shares are always the same.

ABC Industries Ltd. issues 1,000 €10 par ordinary shares value at €12 per share. In recording the transaction, credits are made to:

Share Capital—Ordinary €10,000 and Share Premium—Ordinary €2,000.

Share Capital—Ordinary €12,000.

Share Capital—Ordinary €10,000 and Gain from Sale of Shares €2,000.

Share Capital—Ordinary €10,000 and Retained Earnings €2,000.

XYZ, Ltd. sells 100 of its £5 par value treasury shares at £13 per share. If the cost of acquiring the shares was £10 per share, the entry for the sale should include credits to:

Treasury Shares 1,000 and Share Premium—Treasury 300.

Treasury Shares 500 and Share Premium—Treasury 800.

Treasury Shares 1,000 and Retained Earnings 300.

Treasury Shares 500 and Gain from Sale of Treasury Shares 800.

In the statement of financial position, the cost of treasury shares is deducted in:

expenses.

revenues.

equity.

liabilities.

Preference shares may have priority over ordinary shares except in:

dividends.

assets in the event of liquidation.

cumulative dividend features.

voting.

M-Bot Enterprises has 10,000 8%, £100 par value, cumulative preference shares outstanding at December 31, 2017. No dividends were declared in 2015 or 2016. If M-Bot wants to pay £375,000 of dividends in 2017, ordinary shareholders will receive:

£0.

£295,000.

£215,000.

£135,000.

- Entries for cash dividends are required on the:

declaration date and the payment date.

record date and the payment date.

declaration date, record date, and payment date.

declaration date and the record date.

Which of the following statements about small share dividends is true?

A debit to Retained Earnings for the par value of the shares issued should be made.

A small share dividend decreases total equity.

Market price per share should be assigned to the dividend shares.

A small share dividend ordinarily will have an effect on par value per share.

All but one of the following is reported in a retained earnings statement. The exception is:

cash and share dividends.

net income and net loss.

sales revenue.

prior period adjustments.

A prior period adjustment is:

reported in the income statement as a non--typical item.

a correction of an error that is recorded directly to retained earnings.

reported directly in the equity section of the statement of financial position.

reported in the retained earnings statement as an adjustment of the ending balance of retained earnings.

In the equity section of the statement of financial position, share capital—ordinary:

is listed before share capital—preference.

is listed after retained earnings.

is listed after share capital—preference.

is reduced for treasury shares.

Adana A.Ş. reported net income of

186,000 during 2017, paid dividends of 26,000 on ordinary shares, and paid dividends of 60,000 on preference shares. It also has 10,000 shares of 6%, 100 par value, non-cumulative preference shares outstanding. Ordinary shareholders’ equity was 1,200,000 on January 1, 2017, and 1,600,000 on December 31, 2017. The company’s return on ordinary shareholders’ equity for 2017 is:

186,000 during 2017, paid dividends of 26,000 on ordinary shares, and paid dividends of 60,000 on preference shares. It also has 10,000 shares of 6%, 100 par value, non-cumulative preference shares outstanding. Ordinary shareholders’ equity was 1,200,000 on January 1, 2017, and 1,600,000 on December 31, 2017. The company’s return on ordinary shareholders’ equity for 2017 is:10.0%.

9.0%.

7.1%.

13.3%.

*When a statement of changes in equity is presented, it is not necessary to prepare a (an):

retained earnings statement.

statement of financial position.

income statement.

statement of cash flows.

The ledger of JFK, plc shows share capital—ordinary, treasury shares—ordinary, and no preference shares. For this company, the formula for computing book value per share is:

total equity divided by the number of ordinary shares issued.

share capital—ordinary divided by the number of ordinary shares issued.

total equity divided by the number of ordinary shares outstanding.

share capital—ordinary divided by the number of ordinary shares outstanding.

Solutions

PRACTICE EXERCISES

Journalize issuance of ordinary and preference shares and purchase of treasury shares.

- Maci plc had the following transactions during the current period.

| Mar. | 2 | Issued 5,000 shares of £5 par value ordinary shares to attorneys in payment of a bill for £35,000 for services performed in helping the company to incorporate. |

| June | 12 | Issued 60,000 shares of £5 par value ordinary shares for cash of £370,000. |

| July | 11 | Issued 1,000 shares of £100 par value preference shares for cash at £112 per share. |

| Nov. | 28 | Purchased 2,000 shares of treasury shares for £70,000. |

Instructions

Journalize the transactions.