CHAPTER 10

Liabilities

FEATURE STORY

Financing His Dreams

What would you do if you had a great idea for a new product but couldn’t come up with the cash to get the business off the ground? Small businesses often cannot attract investors. Nor can they obtain traditional debt financing through bank loans or bond issuances. Instead, they often resort to unusual, and costly, forms of non-traditional financing.

Such was the case for Wilbert Murdock. Murdock grew up in a low-income housing project but always had high goals. His entrepreneurial spirit led him into some business ventures that failed, such as a device to keep people from falling asleep while driving. Another idea was computerized golf clubs that analyze a golfer’s swing and provide immediate feedback. Murdock saw great potential in the idea. Many golfers are willing to shell out considerable sums of money for devices that might improve their game. But Murdock had no cash to develop his product, and banks and other lenders had shied away. Rather than give up, Murdock resorted to credit cards—in a big way. He quickly owed $25,000 to credit card companies.

While funding a business with credit cards might sound unusual, it isn’t. A recent study by the London-based Institute of Directors found that more than half of companies seeking bank financing had been turned down. About 20% of the 1,000 companies studied relied, at least in part, on credit card financing.

Murdock’s credit card debt forced him to sacrifice nearly everything in order to keep his business afloat. His car stopped running, he barely had enough money to buy food, and he lived and worked out of a dimly lit apartment in his mother’s basement. Through it all he tried to maintain a positive spirit, joking that, if he becomes successful, he might some day get to appear in an American Express (USA) commercial.

Sources: Rodney Ho, “Banking on Plastic: To Finance a Dream, Many Entrepreneurs Binge on Credit Cards,” Wall Street Journal (March 9, 1998), p. A1; Brian Groom, “Banks Fail to Help Half of Companies, Say IoD,” Financial Times Online (FT.com) (February 16, 2010). ![]()

PREVIEW OF CHAPTER 10

Inventor-entrepreneur Wilbert Murdock, as you can tell from the Feature Story, had to use multiple credit cards to finance his business ventures. Murdock’s credit card debts would be classified as current liabilities because they are due every month. Yet, by making minimal payments and paying high interest each month, Murdock used this credit source long-term. Some credit card balances remain outstanding for years as they accumulate interest.

Earlier, we defined liabilities as creditors’ claims on total assets and as existing debts and obligations. These claims, debts, and obligations must be settled or paid at some time in the future by the transfer of assets or services. The future date on which they are due or payable (maturity date) is a significant feature of liabilities. This “future date” feature gives rise to two basic classifications of liabilities: (1) current liabilities and (2) non-current liabilities. Our discussion in this chapter is divided into these two classifications.

The content and organization of Chapter 10 are as follows.

Current Liabilities

Learning Objective 1

Explain a current liability, and identify the major types of current liabilities.

What Is a Current Liability?

You have learned that liabilities are defined as “creditors’ claims on total assets” and as “existing debts and obligations.” Companies must settle or pay these claims, debts, and obligations at some time in the future by transferring assets or services. The future date on which they are due or payable (the maturity date) is a significant feature of liabilities.

As explained in Chapter 4, a current liability is a debt that a company expects to pay within one year or the operating cycle, whichever is longer. is a debt that a company expects to pay within one year or the operating cycle, whichever is longer. Debts that do not meet this criterion are non-current liabilities.

Financial statement users want to know whether a company’s obligations are current or non-current. A company that has more current liabilities than current assets often lacks liquidity, or short-term debt-paying ability. In addition, users want to know the types of liabilities a company has. If a company declares bankruptcy, a specific, predetermined order of payment to creditors exists. Thus, the amount and type of liabilities are of critical importance.

The different types of current liabilities include notes payable, accounts payable, unearned revenues, and accrued liabilities such as taxes, salaries and wages, and interest payable. In the sections that follow, we discuss common types of current liabilities.

Notes Payable

Learning Objective 2

Describe the accounting for notes payable.

Companies record obligations in the form of written notes as notes payable. Notes payable are often used instead of accounts payable because they give the lender formal proof of the obligation in case legal remedies are needed to collect the debt. Companies frequently issue notes payable to meet short-term financing needs. Notes payable usually require the borrower to pay interest.

Notes are issued for varying periods of time. Those due for payment within one year of the statement of financial position date are usually classified as current liabilities.

To illustrate the accounting for notes payable, assume that Hong Kong National Bank agrees to lend HK$100,000 on September 1, 2017, if C. W. Co. signs a HK$100,000, 12%, four-month note maturing on January 1. When a company issues an interest-bearing note, the amount of assets it receives upon issuance of the note generally equals the note’s face value. C. W. Co. therefore will receive HK$100,000 cash and will make the following journal entry.

Interest accrues over the life of the note, and the company must periodically record that accrual. If C. W. Co. prepares financial statements annually, it makes an adjusting entry at December 31 to recognize interest expense and interest payable of . Illustration 10-1 shows the formula for computing interest and its application to C. W. Co.’s note.

Illustration 10-1 Formula for computing interest

C. W. Co. makes an adjusting entry as follows.

In the December 31 financial statements, the current liabilities section of the statement of financial position will show notes payable HK$100,000 and interest payable HK$4,000. In addition, the company will report interest expense of HK$4,000 under “Other income and expense” in the income statement. If C. W. Co. prepared financial statements monthly, the adjusting entry at the end of each month would have been .

At maturity (January 1, 2018), C. W. Co. must pay the face value of the note (HK$100,000) plus HK$4,000 interest . It records payment of the note and accrued interest as follows.

Sales Taxes Payable

Learning Objective 3

Explain the accounting for other current liabilities.

Many of the products we purchase at retail stores are subject to sales taxes.1 Many governments also are now collecting sales taxes on purchases made on the Internet as well. Sales taxes are expressed as a percentage of the sales price. The selling company collects the tax from the customer when the sale occurs. Periodically (usually monthly), the retailer remits the collections to the government’s department of revenue.

Under most government sales tax laws, the selling company must enter separately on the cash register the amount of the sale and the amount of the sales tax collected. The company then uses the cash register readings to credit Sales Revenue and Sales Taxes Payable. For example, if the March 25 cash register reading for Cooley Grocery shows sales of NT$10,000 and sales taxes of NT$600 (sales tax rate of 6%), the journal entry is as follows.

When the company remits the taxes to the taxing agency, it debits Sales Taxes Payable and credits Cash. The company does not report sales taxes as an expense. It simply forwards to the government the amount paid by the customers. Thus, Cooley Grocery serves only as a collection agent for the taxing authority.

Sometimes companies do not enter sales taxes separately in the cash register. To determine the amount of sales in such cases, divide total receipts by 100% plus the sales tax percentage. For example, assume that Cooley Grocery enters total receipts of NT$10,600. The receipts from the sales are equal to the sales price (100%) plus the tax percentage (6% of sales), or 1.06 times the sales total. We can compute the sales amount as follows.

Thus, we can find the sales tax amount of NT$600 by either (1) subtracting sales from total receipts or (2) multiplying sales by the sales tax rate .

• HELPFUL HINT

For point-of-sale systems, the company receives sales information through the computer network.

Unearned Revenues

An airline company, such as Qantas Airways (AUS), often receives cash when it sells tickets for future flights. A magazine publisher, such as Finance Asia (HKG), receives customers’ payments when they order magazines. Season tickets for concerts, sporting events, and theater programs are also paid for in advance. How do companies account for unearned revenues that are received before goods are delivered or services are performed?

- When a company receives the advance payment, it debits Cash and credits a current liability account identifying the source of the unearned revenue.

- When the company recognizes revenue, it debits an unearned revenue account and credits a revenue account.

To illustrate, assume that the Busan IPark (KOR) sells 10,000 season football tickets at ![]() 50,000 each for its five-game home schedule. The club makes the following entry for the sale of season tickets (in thousands of

50,000 each for its five-game home schedule. The club makes the following entry for the sale of season tickets (in thousands of ![]() ).

).

As each game is completed, Busan IPark records the recognition of revenue with the following entry (in thousands of ![]() ).

).

The account Unearned Ticket Revenue represents unearned revenue, and Busan IPark reports it as a current liability. As the club recognizes revenue, it reclassifies the amount from unearned revenue to Ticket Revenue. Unearned revenue is substantial for some companies. In the airline industry, for example, tickets sold for future flights represent almost 50% of total current liabilities. At United Airlines (USA), unearned ticket revenue is its largest current liability, recently amounting to over $1 billion.

Illustration 10-2 shows specific unearned revenue and revenue accounts used in selected types of businesses.

Illustration 10-2 Unearned revenue and revenue accounts

Current Maturities of Long-Term Debt

Companies often have a portion of long-term debt that comes due in the current year. That amount is considered a current liability. As an example, assume that Wendy Construction issues a five-year, interest-bearing €25,000 note on January 1, 2017. This note specifies that each January 1, starting January 1, 2018, Wendy should pay €5,000 of the note. When the company prepares financial statements on December 31, 2017, it should report €5,000 as a current liability and €20,000 as a non-current liability. (The €5,000 amount is the portion of the note that is due to be paid within the next 12 months.) Companies often identify current maturities of long-term debt on the statement of financial position as long-term debt due within one year.

It is not necessary to prepare an adjusting entry to recognize the current maturity of long-term debt. At the statement of financial position date, all obligations due within one year are classified as current, and all other obligations as non-current.

GLOSSARY REVIEW

- Bond certificate

- A legal document that indicates the name of the issuer, the face value of the bonds, the contractual interest rate, and the maturity date of the bonds. (p. 488).

- Bond indenture

- A legal document that sets forth the terms of the bond issue. (p. 488).

- Bonds

- A form of interest-bearing notes payable. (p. 487).

- Callable bonds

- Bonds that are subject to redemption at a stated currency amount prior to maturity at the option of the issuer. (p. 488).

- Contractual interest rate

- Rate used to determine the amount of cash interest the borrower pays and the investor receives. (p. 488).

- Convertible bonds

- Bonds that permit bondholders to convert them into ordinary shares at the bondholders’ option. (p. 488).

- Current liabilities

- Obligations that a company expects to pay within one year or the operating cycle, whichever is longer. (p. 482).

- Current ratio

- A measure of a company’s liquidity; computed as current assets divided by current liabilities. (p. 486).

- Debenture bonds

- Bonds issued against the general credit of the borrower. Also called unsecured bonds. (p. 488).

- Debt to assets ratio

- A solvency measure that indicates the percentage of total assets provided by creditors; computed as total liabilities divided by total assets. (p. 500).

- Discount (on a bond)

- The difference between the face value of a bond and its selling price, when the bond is sold for less than its face value. (p. 492).

- * Effective-interest method of amortization

- A method of amortizing bond discount or bond premium that results in periodic interest expense equal to a constant percentage of the carrying value of the bonds. (p. 502).

- Face value

- Amount of principal the issuer must pay at the maturity date of the bond. (p. 488).

- Market interest rate

- The rate investors demand for loaning funds to the corporation. (p. 490).

- Maturity date

- The date on which the final payment on the bond is due from the bond issuer to the investor. (p. 488).

- Mortgage bond

- A bond secured by real estate. (p. 488).

- Mortgage notes payable

- A long-term note secured by a mortgage that pledges title to specific assets as security for a loan. (p. 497).

- Non-current liabilities

- Obligations expected to be paid more than one year in the future. (p. 486).

- Notes payable

- Obligations in the form of written notes. (p. 482).

- Premium (on a bond)

- The difference between the selling price and the face value of a bond, when the bond is sold for more than its face value. (p. 493).

- Secured bonds

- Bonds that have specific assets of the issuer pledged as collateral. (p. 488).

- Sinking fund bonds

- Bonds secured by specific assets set aside to redeem them. (p. 488).

- * Straight-line method of amortization

- A method of amortizing bond discount or bond premium that results in allocating the same amount to interest expense in each interest period. (p. 505).

- Times interest earned

- A solvency measure that indicates a company’s ability to meet interest payments; computed by dividing the sum of net income, interest expense, and income tax expense by interest expense. (p. 500).

- Time value of money

- The relationship between time and money. A dollar received today is worth more than a dollar promised at some time in the future. (p. 490).

- Unsecured bonds

- Bonds issued against the general credit of the borrower. Also called debenture bonds. (p. 488).

- Working capital

- A measure of a company’s liquidity; computed as current assets minus current liabilities. (p. 486).

PRACTICE MULTIPLE-CHOICE QUESTIONS

- The time period for classifying a liability as current is one year or the operating cycle, whichever is:

- longer.

- shorter.

- probable.

- possible.

- To be classified as a current liability, a debt must be expected to be paid within:

- one year.

- the operating cycle.

- 2 years.

- (a) or (b), whichever is longer.

- Maggie Sharrer SA borrows R$88,500 on September 1, 2017, from Sandwich Bank by signing an R$88,500, 12%, one-year note. What is the accrued interest at December 31, 2017?

- R$2,655.

- R$4,425.

- R$3,540.

- R$10,620.

- Becky Sherrick SE has total proceeds from sales of €4,515. If the proceeds include sales taxes of 5%, the amount to be credited to Sales Revenue is:

- €4,000.

- €4,300.

- €4,289.25.

- No correct answer given.

- Sensible Insurance collected a premium of £18,000 for a 1-year insurance policy on April 1. What amount should Sensible report as a current liability for Unearned Service Revenue at December 31?

- £0.

- £4,500.

- £13,500.

- £18,000.

- The term used for bonds that are unsecured is:

- callable bonds.

- indenture bonds.

- debenture bonds.

- convertible bonds.

- Karson Ltd. issues 10-year bonds with a maturity value of £200,000. If the bonds are issued at a premium, this indicates that:

- the contractual interest rate exceeds the market interest rate.

- the market interest rate exceeds the contractual interest rate.

- the contractual interest rate and the market interest rate are the same.

- no relationship exists between the two rates.

- Gester Ltd. redeems its HK$1,000,000 face value bonds at 105 on January 1, following the payment of annual interest. The carrying value of the bonds at the redemption date is HK$1,037,450. The entry to record the redemption will include a:

- credit of HK$37,450 to Loss on Bond Redemption.

- debit of HK$1,037,450 to Bonds Payable.

- credit of HK$12,550 to Gain on Bond Redemption.

- debit of HK$50,000 to Bonds Payable.

- Andrews Ltd. issues a €497,000, 10%, 3-year mortgage note on January 1. The note will be paid in three annual installments of €200,000, each payable at the end of the year. What is the amount of interest expense that should be recognized by Andrews in the second year?

- €16,567.

- €49,700.

- €34,670.

- €346,700.

- Howard Ltd. issued a 20-year mortgage note payable on January 1, 2017. At December 31, 2017, the unpaid principal balance will be reported as:

- a current liability.

- a non-current liability.

- part current and part non-current liability.

- interest payable.

- For 2017, Kim Ltd. reported net income of

300,000. Interest expense was 40,000 and income taxes were 100,000. The times interest earned was:

300,000. Interest expense was 40,000 and income taxes were 100,000. The times interest earned was:

- 3 times.

- 4.4 times.

- 7.5 times.

- 11 times.

- * On January 1, Besalius plc issued £1,000,000, 9% bonds for £938,554. The market rate of interest for these bonds is 10%. Interest is payable annually on December 31. Besalius uses the effective-interest method of amortizing bond discount. At the end of the first year, Besalius should report unamortized bond discount of:

- £54,900.

- £57,591.

- £51,610.

- £51,000.

- *On January 1, Dias SA issued R$1,000,000, 10%, 5-year bonds with interest payable annually on December 31. The bonds sold for R$1,072,096. The market rate of interest for these bonds was 12%. On the first interest date, using the effective-interest method, the debit entry to Interest Expense is for:

- R$120,000.

- R$125,581.

- R$128,652.

- R$140,000.

- *On January 1, 2017, Hurley Ltd. issued NT$5,000,000, 5-year, 12% bonds at 96 with interest payable annually on December 31. The entry on December 31, 2018, to record payment of bond interest and the amortization of bond discount using the straight-line method will include a:

- debit to Interest Expense NT$300,000.

- debit to Interest Expense NT$600,000.

- credit to Bonds Payable NT$40,000.

- credit to Bonds Payable NT$20,000.

- *For the bonds issued in Question 14 above, what is the carrying value of the bonds at the end of the third interest period?

- NT$4,920,000.

- NT$4,880,000.

- NT$4,860,000.

- NT$4,640,000.

Solutions

PRACTICE EXERCISES

Prepare entries for interest-bearing notes..

- On June 1, JetSet plc borrows £150,000 from First Bank on a 6-month, £150,000, 8% note.

Instructions

- Prepare the entry on June 1.

- Prepare the adjusting entry on June 30.

- Prepare the entry at maturity (December 1), assuming monthly adjusting entries have been made through November 30.

- What was the total financing cost (interest expense)?

Solution

Prepare entries for bonds issued at face value..

- Global Airlines Ltd. issued NT$900,000 of 8%, 10-year bonds on January 1, 2017, at face value. Interest is payable annually on January 1.

Instructions

Prepare the journal entries to record the following events.

- The issuance of the bonds.

- The accrual of interest on December 31.

- The payment of interest on January 1, 2018.

- The redemption of bonds at maturity, assuming interest for the last interest period has been paid and recorded.

Solution

Prepare entries to record mortgage note and installment payments.

- Trawler SA borrowed €500,000 on December 31, 2017, by issuing a €500,000, 7% mortgage note payable. The terms call for annual installment payments of €80,000 on December 31.

Instructions

- Prepare the journal entries to record the mortgage loan and the first two installment payments.

- Indicate the amount of mortgage note payable to be reported as a current liability and as a non-current liability at December 31, 2018.

Solution

PRACTICE PROBLEM

Prepare entries to record issuance of bonds and longterm notes, interest accrued, and bond redemption..

Lee Software Ltd. has successfully developed a new spreadsheet program. To produce and market the program, the company needs additional financing. On January 1, 2017, Lee borrowed money as follows.

- Lee issued NT$1 million, 10%, 10-year bonds at face value. Interest is payable annually on January 1.

- Lee also issued a NT$400,000, 6%, 15-year mortgage payable. The terms provide for annual installment payments of NT$41,185 on December 31.

Instructions

- For the 10-year, 10% bonds:

- Journalize the issuance of the bonds on January 1, 2017.

- Prepare the journal entries for interest expense in 2017.

- Prepare the entry for the redemption of the bonds at 101 on January 1, 2020, after paying the interest due on this date.

- For the mortgage payable:

- Prepare the entry for the issuance of the note on January 1, 2017.

- Prepare a payment schedule for the first four installment payments.

- Indicate the current and non-current amounts for the mortgage payable at December 31, 2017.

Solution

WileyPLUS

Brief Exercises, DO IT! Review, Exercises, and Problems, and many additional resources are available for practice in WileyPLUS.

NOTE: Asterisked Questions, Exercises, and Problems relate to material in the appendix to the chapter.

QUESTIONS

Brenda Gable believes a current liability is a debt that can be expected to be paid in one year. Is Brenda correct? Explain.

Delhi Ltd. obtains Rs300,000 in cash by signing a 9%, 6-month, Rs300,000 note payable to First Bank on July 1. Delhi’s fiscal year ends on September 30. What information should be reported for the note payable in the annual financial statements?

- Your roommate says, “Sales taxes are reported as an expense in the income statement.” Do you agree? Explain.

- Planet Hollywood has cash proceeds from sales of £7,400. This amount includes £400 of sales taxes. Give the entry to record the proceeds.

Rotterdam University sold 10,000 season football tickets at €90 each for its five-game home schedule. What entries should be made (a) when the tickets were sold, and (b) after each game?

What is liquidity? What are two measures of liquidity?

(a) What are non-current liabilities? Give three examples. (b) What is a bond?

(a) As a source of long-term financing, what are the major advantages of bonds over ordinary shares? (b) What are the major disadvantages in using bonds for long-term financing?

Contrast the following types of bonds: (a) secured and unsecured, and (b) convertible and callable.

The following terms are important in issuing bonds: (a) face value, (b) contractual interest rate, (c) bond indenture, and (d) bond certificate. Explain each of these terms.

Describe the two major obligations incurred by a company when bonds are issued.

Assume that Bedazzled Ltd. sold bonds with a face value of €100,000 for €104,000. Was the market interest rate equal to, less than, or greater than the bonds’ contractual interest rate? Explain.

If a 6%, 10-year, R$800,000 bond is issued at face value and interest is paid annually, what is the amount of the interest payment at the end of the first period?

If the Bonds Payable account has a balance of HK$8,400,000 and the amount of the unamortized bond discount is HK$600,000, what is the face value of the bonds?

Which accounts are debited and which are credited if a bond issue originally sold at a premium is redeemed before maturity at 97 immediately following the payment of interest?

Roy Toth, a friend of yours, has recently purchased a home for €125,000, paying €25,000 down and the remainder financed by a 6.5%, 20-year mortgage, payable at €745.57 per month. At the end of the first month, Roy receives a statement from the bank indicating that only €203.90 of principal was paid during the month. At this rate, he calculates that it will take over 40 years to pay off the mortgage. Is he right? Discuss.

*In general, what are the requirements for the financial statement presentation of non-current liabilities?

*Ginny Bellis is discussing the advantages of the effective-interest method of bond amortization with her accounting staff. What do you think Ginny is saying?

*Redbone AG issues CHF500,000 of 8%, 5-year bonds on January 1, 2014, at 104. If Redbone uses the effective-interest method in amortizing the premium, will the annual interest expense increase or decrease over the life of the bonds? Explain.

*Explain the straight-line method of amortizing discount and premium on bonds payable.

*Fleming Ltd. issues £400,000 of 7%, 5-year bonds on January 1, 2017, at 105. Assuming that the straightline method is used to amortize the premium, what is the total amount of interest expense for 2017?

*Identify two taxes commonly withheld by the employer from an employee’s gross pay.

BRIEF EXERCISES

Identify whether obligations are current liabilities.

BE10-1 Cardinal SpA has the following obligations at December 31: (a) a note payable for €100,000 due in 2 years, (b) a 10-year mortgage payable of €300,000 payable in ten €30,000 annual payments, (c) interest payable of €12,000 on the mortgage, and (d) accounts payable of €60,000. For each obligation, indicate whether it should be classified as a current liability. (Assume an operating cycle of less than one year.)

Prepare entries for an interestbearing note payable.

BE10-2 Becky Ltd. borrows £60,000 on July 1 from the bank by signing a £60,000, 10%, one-year note payable.

- Prepare the journal entry to record the proceeds of the note.

- Prepare the journal entry to record accrued interest at December 31, assuming adjusting entries are made only at the end of the year.

Compute and record sales taxes payable.

BE10-3 Goodwin Auto Supply does not segregate sales and sales taxes at the time of sale. The register total for March 16 is £12,826. All sales are subject to a 6% sales tax. Compute sales taxes payable, and make the entry to record sales taxes payable and sales revenue.

Prepare entries for unearned revenues.

BE10-4 Hamburg University sells 4,000 season basketball tickets at €180 each for its 10-game home schedule. Give the entry to record (a) the sale of the season tickets and (b) the revenue recognized for playing the first home game.

Compare bond versus share financing.

BE10-5 Shaffer Ltd. is considering two alternatives to finance its construction of a new €2 million plant.

- Issuance of 200,000 ordinary shares at the market price of €10 per share.

- Issuance of €2 million, 6% bonds at face value.

Complete the following table, and indicate which alternative is preferable.

Prepare entries for bonds issued at face value.

BE10-6 Meera Ltd. issued 4,000, 8%, 5-year, £1,000 bonds dated January 1, 2017, at 100. Interest is paid each January 1.

- Prepare the journal entry to record the sale of these bonds on January 1, 2017.

- Prepare the adjusting journal entry on December 31, 2017, to record interest expense.

- Prepare the journal entry on January 1, 2018, to record interest paid.

Prepare entries for bonds sold at a discount and a premium.

BE10-7 Nasreen Company issues €2 million, 10-year, 8% bonds at 97, with interest payable each January 1.

- Prepare the journal entry to record the sale of these bonds on January 1, 2017.

- Assuming instead that the above bonds sold for 104, prepare the journal entry to record the sale of these bonds on January 1, 2017.

Prepare entries for bonds issued.

BE10-8 Frankum SpA has issued three different bonds during 2017. Interest is payable annually on each of these bonds.

- On January 1, 2017, 1,000, 8%, 5-year, €1,000 bonds dated January 1, 2017, were issued at face value.

- On July 1, €900,000, 9%, 5-year bonds dated July 1, 2017, were issued at 102.

- On September 1, €400,000, 7%, 5-year bonds dated September 1, 2017, were issued at 98.

Prepare the journal entry to record each bond transaction at the date of issuance.

Prepare entry for redemption of bonds.

BE10-9 The statement of financial position for Miley Consulting reports the following

Miley decides to redeem these bonds at 101 (face value of bonds £1,000,000) after paying annual interest. Prepare the journal entry to record the redemption on July 1, 2017.

Prepare entries for long-term notes payable.

BE10-10 Hanschu plc issues an £800,000, 10%, 10-year mortgage note on December 31, 2017, to obtain financing for a new building. The terms provide for annual installment payments of £130,196. Prepare the entry to record the mortgage loan on December 31, 2017, and the first installment payment on December 31, 2018.

Prepare statement presentation of non-current liabilities.

BE10-11 Presented below are non-current liability items for Suarez AG at December 31, 2017. Prepare the non-current liabilities section of the statement of financial position for Suarez.

Analyze solvency.

BE10-12 Suppose the 2017 adidas financial statements contain the following selected data (in millions)

Compute the following values and provide a brief interpretation of each.

- Working capital.

- Current ratio.

- Debt to assets ratio.

- Times interest earned.

Use effective-interest method of bond amortization.

*BE10-13 Presented below is the partial bond discount amortization schedule for Gomez SA. Gomez uses the effective-interest method of amortization.

- Prepare the journal entry to record the payment of interest and the discount amortization at the end of period 1.

Explain why interest expense is greater than interest paid.

Explain why interest expense is greater than interest paid.- Explain why interest expense will increase each period.

Prepare entries for bonds issued at a discount.

*BE10-14 Zhu Ltd. issues HK$5 million, 10-year, 9% bonds at 96, with interest payable annually on January 1. The straight-line method is used to amortize bond discount.

- Prepare the journal entry to record the sale of these bonds on January 1, 2017.

- Prepare the adjusting journal entry to record interest expense and bond discount amortization on December 31, 2017.

Prepare entries for bonds issued at a premium.

*BE10-15 Golden plc issues £4 million, 5-year, 10% bonds at 102, with interest payable annually January 1. The straight-line method is used to amortize bond premium.

- Prepare the journal entry to record the sale of these bonds on January 1, 2017.

- Prepare the adjusting journal entry to record interest expense and bond premium amortization on December 31, 2017.

Prepare entry to record payroll.

*BE10-16 Lexington AG’s weekly payroll of €24,000 included Social Security taxes withheld of €1,920, income taxes withheld of €2,990, and insurance premiums withheld of €250. Prepare the journal entry to record Lexington’s payroll.

Prepare entries to record profit-sharing bonus.

*BE10-17 Mayaguez Ltd. provides its officers with bonuses based on net income. For 2017, the bonuses total £350,000 and are paid on February 15, 2018. Prepare Mayaguez’s December 31, 2017, adjusting entry and the February 15, 2018, entry.

EXERCISES

Prepare entries for interest-bearing notes.

E10-1 Padillio SpA had the following transactions involving notes payable.

| July 1, 2017 | Borrows €60,000 from Fourth National Bank by signing a 9-month, 8% note. |

| Nov. 1, 2017 | Borrows €42,000 from Livingston Bank by signing a 3-month, 7% note. |

| Dec. 31, 2017 | Prepares adjusting entries. |

| Feb. 1, 2018 | Pays principal and interest to Livingston Bank. |

| Apr. 1, 2018 | Pays principal and interest to Fourth National Bank. |

Instructions

Prepare journal entries for each of the transactions.

Prepare entries for interest-bearing notes.

E10-2 On June 1, Yoon Ltd. borrows €70,000 from First Bank on a 6-month, €70,000, 9% note.

Instructions

- Prepare the entry on June 1.

- Prepare the adjusting entry on June 30.

- Prepare the entry at maturity (December 1), assuming monthly adjusting entries have been made through November 30.

- What was the total financing cost (interest expense)?

Journalize sales and related taxes.

E10-3 In performing accounting services for small businesses, you encounter the following situations pertaining to cash sales.

- Kemer A.Ş. enters sales and sales taxes separately on its cash register. On April 10, the register totals are sales

30,000 and sales taxes 1,800.

30,000 and sales taxes 1,800. - Bodrum A.Ş. does not segregate sales and sales taxes. Its register total for April 15 is 20,330, which includes a 7% sales tax.

Instructions

Prepare the entry to record the sales transactions and related taxes for each client.

Journalize unearned subscription revenue.

E10-4 Nevin Ltd. publishes a monthly sports magazine, Fishing Preview. Subscriptions to the magazine cost £18 per year. During November 2017, Nevin sells 12,000 subscriptions beginning with the December issue. Nevin prepares financial statements quarterly and recognizes subscription revenue at the end of the quarter. The company uses the accounts Unearned Subscription Revenue and Subscription Revenue.

Instructions

- Prepare the entry in November for the receipt of the subscriptions.

- Prepare the adjusting entry at December 31, 2017, to record sales revenue recognized in December 2017.

- Prepare the adjusting entry at March 31, 2018, to record sales revenue recognized in the first quarter of 2018.

Calculate current ratio and working capital before and after paying accounts payable.

E10-5 The following financial data were reported by 3M Company (USA) for 2012 and 2013 (dollars in millions).

Instructions

- Calculate the current ratio and working capital for 3M for 2012 and 2013.

- Suppose that at the end of 2013, 3M management used $200 million cash to pay off $200 million of accounts payable. How would its current ratio and working capital have changed?

Evaluate statements about bonds.

E10-6 Liane Hansen has prepared the following list of statements about bonds.

- Bonds are a form of interest-bearing notes payable.

- When seeking long-term financing, an advantage of issuing bonds over issuing ordinary shares is that shareholder control is not affected.

- When seeking long-term financing, an advantage of issuing ordinary shares over issuing bonds is that tax savings result.

- Secured bonds have specific assets of the issuer pledged as collateral for the bonds.

- Secured bonds are also known as debenture bonds.

- A conversion feature may be added to bonds to make them more attractive to bond buyers.

- The rate used to determine the amount of cash interest the borrower pays is called the stated rate.

- Bond prices are usually quoted as a percentage of the face value of the bond.

- The present value of a bond is the value at which it should sell in the marketplace.

Instructions

Identify each statement as true or false. If false, indicate how to correct the statement.

Compare two alternatives of financing—issuance of ordinary shares vs. issuance of bonds.

E10-7 Global Car Rental is considering two alternatives for the financing of a purchase of a fleet of cars. These two alternatives are:

- Issue 60,000 ordinary shares at ¥40 per share. (Cash dividends have not been paid nor is the payment of any contemplated.)

- Issue 7%, 10-year bonds at face value for ¥2,400,000.

It is estimated that the company will earn ¥800,000 before interest and taxes as a result of this purchase. The company has an estimated tax rate of 30% and has 90,000 ordinary shares outstanding prior to the new financing.

Instructions

Determine the effect on net income and earnings per share for these two methods of financing.

Prepare entries for issuance of bonds, and payment and accrual of bond interest.

E10-8 On January 1, 2017, Klosterman Ltd. issued £500,000, 10%, 10-year bonds at face value. Interest is payable annually on January 1.

Instructions

Prepare journal entries to record the following.

- The issuance of the bonds.

- The accrual of interest on December 31, 2017.

- The payment of interest on January 1, 2018.

Prepare entries for bonds issued at face value.

E10-9 On January 1, 2017, Forrester SA issued R$400,000, 8%, 5-year bonds at face value. Interest is payable annually on January 1.

Instructions

Prepare journal entries to record the following.

- The issuance of the bonds.

- The accrual of interest on December 31, 2017.

- The payment of interest on January 1, 2018.

Prepare entries to record issuance of bonds at discount and premium.

E10-10 Pueblo Company issued €500,000 of 5-year, 8% bonds at 97 on January 1, 2017. The bonds pay interest annually.

Instructions

-

- Prepare the journal entry to record the issuance of the bonds.

- Compute the total cost of borrowing for these bonds.

- Repeat the requirements from part (a), assuming the bonds were issued at 105.

Prepare entries for bond interest and redemption.

E10-11 The following section is taken from Ohlman Ltd.’s. statement of financial position at December 31, 2016.

Bond interest is payable annually on January 1. The bonds are callable on any interest date.

Instructions

- Journalize the payment of the bond interest on January 1, 2017.

- Assume that on January 1, 2017, after paying interest, Ohlman calls bonds having a face value of HK$6,000,000. The call price is 103. Record the redemption of the bonds.

- Prepare the entry to record the accrual of interest on December 31, 2017.

Prepare entries for redemption of bonds.

E10-12 Presented below are two independent situations.

- Longbine plc redeemed £130,000 face value, 12% bonds on June 30, 2017, at 102. The carrying value of the bonds at the redemption date was £117,500. The bonds pay annual interest, and the interest payment due on June 30, 2017, has been made and recorded.

- Tastove Ltd. redeemed £150,000 face value, 12.5% bonds on June 30, 2017, at 98. The carrying value of the bonds at the redemption date was £151,000. The bonds pay annual interest, and the interest payment due on June 30, 2017, has been made and recorded.

Instructions

Prepare the appropriate journal entry for the redemption of the bonds in each situation.

Prepare entries to record mortgage note and payments.

E10-13 Jernigan Co. receives €240,000 when it issues a €240,000, 6%, mortgage note payable to finance the construction of a building at December 31, 2017. The terms provide for annual installment payments of €33,264 on December 31.

Instructions

Prepare the journal entries to record the mortgage loan and the first two payments.

Prepare non-current liabilities section.

E10-14 The adjusted trial balance for Zhang Ltd. at the end of the current year contained the following accounts.

| Interest Payable | HK$ 9,000 |

| Lease Liability | 59,500 |

| Bonds Payable, due 2022 | 204,000 |

Instructions

Prepare the non-current liabilities section of the statement of financial position.

Calculate liquidity and solvency ratios; discuss impact of unrecorded obligations on liquidity and solvency.

E10-15 Suppose Lin Ltd.’s 2017 financial statements contain the following selected data (in millions).

| Current assets | NT$ 3,416.3 | Interest expense | NT$ 473.2 |

| Total assets | 30,224.9 | Income taxes | 1,936.0 |

| Current liabilities | 2,988.7 | Net income | 4,551.0 |

| Total liabilities | 16,191.0 |

Instructions

- Compute the following values and provide a brief interpretation of each.

- Working capital.

- Current ratio.

- Debt to assets ratio.

- Times interest earned.

- Suppose the notes to Lin’s financial statements show that subsequent to 2017, the company will have future minimum lease payments under operating leases of NT$10,717.5 million. If these assets had been purchased with debt, assets and liabilities would rise by approximately NT$8,800 million. Recompute the debt to assets ratio after adjusting for this. Discuss your result.

Prepare entries for issuance of bonds, payment of interest, and amortization of discount using effective-interest method.

*E10-16 Lorance SpA issued €400,000, 7%, 20-year bonds on January 1, 2017, for €360,727. This price resulted in an effective-interest rate of 8% on the bonds. Interest is payable annually on January 1. Lorance uses the effective-interest method to amortize bond premium or discount.

Instructions

Prepare the journal entries to record the following. (Round to the nearest euro.)

- The issuance of the bonds.

- The accrual of interest and the discount amortization on December 31, 2017.

- The payment of interest on January 1, 2018.

Prepare entries of issuance of bonds, payment of interest, and amortization of discount using effective-interest method.

*E10-17 LRNA Ltd. issued £380,000, 7%, 10-year bonds on January 1, 2017, for £407,968. This price resulted in an effective-interest rate of 6% on the bonds. Interest is payable annually on January 1. LRNA uses the effective-interest method to amortize bond premium or discount.

Instructions

Prepare the journal entries to record the following. (Round to the nearest pound.)

- The issuance of the bonds.

- The accrual of interest and the premium amortization on December 31, 2017.

- The payment of interest on January 1, 2018.

Prepare entries to record issuance of bonds, payment of interest, amortization of premium, and redemption at maturity.

*E10-18 Adcock A/S issued €600,000, 9%, 20-year bonds on January 1, 2017, at 103. Interest is payable annually on January 1. Adcock uses straight-line amortization for bond premium or discount.

Instructions

Prepare the journal entries to record the following.

- The issuance of the bonds.

- The accrual of interest and the premium amortization on December 31, 2017.

- The payment of interest on January 1, 2018.

- The redemption of the bonds at maturity, assuming interest for the last interest period has been paid and recorded.

Prepare entries to record issuance of bonds, payment of interest, amortization of discount, and redemption at maturity.

*E10-19 Gridley Ltd. issued £800,000, 11%, 10-year bonds on December 31, 2016, for £730,000. Interest is payable annually on December 31. Gridley uses the straight-line method to amortize bond premium or discount.

Instructions

Prepare the journal entries to record the following.

- The issuance of the bonds.

- The payment of interest and the discount amortization on December 31, 2017.

- The redemption of the bonds at maturity, assuming interest for the last interest period has been paid and recorded.

Record payroll-related deductions.

*E10-20 Dan Noll’s gross earnings for the week were $1,780, his income tax withholding was $303, and his social security tax total was $136.

Instructions

- What was Noll’s net pay for the week?

- Journalize the entry for the recording of his pay in the general journal. (Note: Use Salaries and Wages Payable; not Cash.)

- Record the issuing of the check for Noll’s pay in the general journal.

PROBLEMS: SET A

Prepare current liability entries, adjusting entries, and current liabilities section.

P10-1A On January 1, 2017, the ledger of Shumway Ltd. contains the following liability accounts.

| Accounts Payable | £52,000 |

| Sales Taxes Payable | 5,800 |

| Unearned Service Revenue | 13,000 |

During January, the following selected transactions occurred.

| Jan. | 5 | Sold merchandise for cash totaling £22,470, which includes 7% sales taxes. |

| 12 | Performed services for customers who had made advance payments of £10,000. (Credit Service Revenue.) | |

| 14 | Paid revenue department for sales taxes collected in December 2016 (£5,800). | |

| 20 | Sold 700 units of a new product on credit at £52 per unit, plus 7% sales tax. | |

| 21 | Borrowed £14,000 from DeKalb Bank on a 3-month, 6%, £14,000 note. | |

| 25 | Sold merchandise for cash totaling £12,947, which includes 7% sales taxes. |

Instructions

- Journalize the January transactions.

- Journalize the adjusting entries at January 31 for the outstanding notes payable. (Hint: Use one-third of a month for the DeKalb Bank note.)

- Prepare the current liabilities section of the statement of financial position at January 31, 2017. Assume no change in accounts payable.

Journalize and post note transactions; show statement of financial position presentation.

P10-2A The following are selected transactions of Graves ASA. Graves prepares financial statements quarterly.

| Jan. | 2 | Purchased merchandise on account from Ally Company, €30,000, terms 2/10, n/30. (Graves uses the perpetual inventory system.) |

| Feb. | 1 | Issued a 6%, 2-month, €30,000 note to Ally in payment of account. |

| Mar. | 31 | Accrued interest for 2 months on Ally note. |

| Apr. | 1 | Paid face value and interest on Ally note. |

| July | 1 | Purchased equipment from Clark Equipment paying €8,000 in cash and signing a 7%, 3-month, €40,000 note. |

| Sept. | 30 | Accrued interest for 3 months on Clark note. |

| Oct. | 1 | Paid face value and interest on Clark note. |

| Dec. | 1 | Borrowed €15,000 from the Jonas Bank by issuing a 3-month, 6% note with a face value of €15,000. |

| Dec. | 31 | Recognized interest expense for 1 month on Jonas Bank note. |

Instructions

- Prepare journal entries for the listed transactions and events.

- Post to the accounts Notes Payable, Interest Payable, and Interest Expense.

- Show the statement of financial position presentation of notes and interest payable at December 31.

- What is total interest expense for the year?

Prepare entries to record issuance of bonds, interest accrual, and bond redemption.

P10-3A On May 1, 2017, Herron Industries AG issued CHF600,000, 9%, 5-year bonds at face value. The bonds were dated May 1, 2017, and pay interest annually on May 1. Financial statements are prepared annually on December 31.

Instructions

- Prepare the journal entry to record the issuance of the bonds.

- Prepare the adjusting entry to record the accrual of interest on December 31, 2017.

- Show the statement of financial position presentation on December 31, 2017.

- Prepare the journal entry to record payment of interest on May 1, 2018.

- Prepare the adjusting entry to record the accrual of interest on December 31, 2018.

- Assume that on January 1, 2019, Herron pays the accrued bond interest and calls the bonds at 102. Record the payment of interest and redemption of the bonds.

Prepare entries to record issuance of bonds, interest accrual, and bond redemption.

P10-4A Kershaw Electric Ltd. sold £6,000,000, 10%, 15-year bonds on January 1, 2017. The bonds were dated January 1, 2017, and paid interest on January 1. The bonds were sold at 98.

Instructions

- Prepare the journal entry to record the issuance of the bonds on January 1, 2017.

- At December 31, 2017, the amount of amortized bond discount is £8,000. Show the statement of financial position presentation of the bond liability at December 31, 2017.

- On January 1, 2019, when the carrying value of the bonds was £5,896,000, the company redeemed the bonds at 102. Record the redemption of the bonds assuming that interest for the period has already been paid.

Prepare installment payments schedule and journal entries for a mortgage note payable.

P10-5A Talkington Electronics issues a R$400,000, 8%, 10-year mortgage note on December 31, 2016. The proceeds from the note are to be used in financing a new research laboratory. The terms of the note provide for annual installment payments, exclusive of real estate taxes and insurance, of R$59,612. Payments are due on December 31.

Instructions

- Prepare an installment payments schedule for the first 4 years.

- Prepare the entries for (1) the loan and (2) the first installment payment.

- Show how the total mortgage liability should be reported on the statement of financial position at December 31, 2017.

Prepare journal entries to record issuance of bonds, payment of interest, and amortization of bond discount using effective-interest method.

*P10-6A On January 1, 2017, Lock Industries Ltd. issued £1,800,000 face value, 5%, 10-year bonds at £1,667,518. This price resulted in an effective-interest rate of 6% on the bonds. Lock uses the effective-interest method to amortize bond premium or discount. The bonds pay annual interest January 1.

Instructions

(Round all computations to the nearest pound.)

- Prepare the journal entry to record the issuance of the bonds on January 1, 2017.

- Prepare an amortization table through December 31, 2019 (3 interest periods) for this bond issue.

- Prepare the journal entry to record the accrual of interest and the amortization of the discount on December 31, 2017.

- Prepare the journal entry to record the payment of interest on January 1, 2018.

- Prepare the journal entry to record the accrual of interest and the amortization of the discount on December 31, 2018.

Prepare journal entries to record issuance of bonds, payment of interest, and effective-interest amortization, and statement of financial position presentation.

*P10-7A On January 1, 2017, Jade SA issued €2,000,000 face value, 7%, 10-year bonds at €2,147,202. This price resulted in a 6% effective-interest rate on the bonds. Jade uses the effective-interest method to amortize bond premium or discount. The bonds pay annual interest on each January 1.

Instructions

- Prepare the journal entries to record the following transactions.

- The issuance of the bonds on January 1, 2017.

- Accrual of interest and amortization of the premium on December 31, 2017.

- The payment of interest on January 1, 2018.

- Accrual of interest and amortization of the premium on December 31, 2018.

- Show the proper non-current liabilities statement of financial position presentation for the bond liability at December 31, 2018.

- Provide the answers to the following questions in narrative form.

- What amount of interest expense is reported for 2018?

- Would the bond interest expense reported in 2018 be the same as, greater than, or less than the amount that would be reported if the straight-line method of amortization were used?

Prepare entries to record issuance of bonds, interest accrual, and straight-line amortization for 2 years.

*P10-8A Paris Electric sold €3,000,000, 10%, 10-year bonds on January 1, 2017. The bonds were dated January 1 and pay interest annually on January 1. Paris Electric uses the straight-line method to amortize bond premium or discount. The bonds were sold at 104.

Instructions

- Prepare the journal entry to record the issuance of the bonds on January 1, 2017.

- Prepare a bond premium amortization schedule for the first 4 interest periods.

- Prepare the journal entries for interest and the amortization of the premium in 2017 and 2018.

- Show the statement of financial position presentation of the bond liability at December 31, 2018.

Prepare entries to record -issuance of bonds, interest, and straight-line amortization of bond premium and discount.

*P10-9A Saberhagen Ltd. sold Rs3,500,000, 8%, 10-year bonds on January 1, 2017. The bonds were dated January 1, 2017, and pay interest annually on January 1. Saberhagen Company uses the straight-line method to amortize bond premium or discount.

Instructions

- Prepare all the necessary journal entries to record the issuance of the bonds and bond interest expense for 2017, assuming that the bonds sold at 104.

- Prepare journal entries as in part (a) assuming that the bonds sold at 98.

- Show the statement of financial position presentation for the bonds at December 31, 2017, for both the requirements in (a) and (b).

Prepare entries to record interest payments, straight-line premium amortization, and redemption of bonds.

*P10-10A The following is taken from the Colaw SA statement of financial position.

Interest is payable annually on January 1. The bonds are callable on any annual interest date. Colaw uses straight-line amortization for any bond premium or discount. From December 31, 2017, the bonds will be outstanding for an additional 10 years (120 months).

Instructions

- Journalize the payment of bond interest on January 1, 2018.

- Prepare the entry to amortize bond premium and to accrue the interest due on December 31, 2018.

- Assume that on January 1, 2019, after paying interest, Colaw calls bonds having a face value of €1,200,000. The call price is 101. Record the redemption of the bonds.

- Prepare the adjusting entry at December 31, 2019, to amortize bond premium and to accrue interest on the remaining bonds.

PROBLEMS: SET B

Prepare current liability entries, adjusting entries, and current liabilities section.

P10-1B On January 1, 2017, the ledger of Zaur Ltd. contains the following liability accounts.

| Accounts Payable | ¥42,500 |

| Sales Taxes Payable | 5,800 |

| Unearned Service Revenue | 15,000 |

During January, the following selected transactions occurred.

| Jan. | 1 | Borrowed ¥15,000 in cash from Platteville Bank on a 4-month, 6%, ¥15,000 note. |

| 5 | Sold merchandise for cash totaling ¥9,828, which includes 8% sales taxes. | |

| 12 | Performed services for customers who had made advance payments of ¥9,400. (Credit Service Revenue.) | |

| 14 | Paid government treasurer’s department for sales taxes collected in December 2016, ¥5,800. | |

| 20 | Sold 700 units of a new product on credit at ¥44 per unit, plus 8% sales tax. | |

| 25 | Sold merchandise for cash totaling ¥16,308, which includes 8% sales taxes. |

Instructions

- Journalize the January transactions.

- Journalize the adjusting entries at January 31 for the outstanding notes payable.

- Prepare the current liabilities section of the statement of financial position at January 31, 2017. Assume no change in accounts payable.

Prepare entries to record issuance of bonds, interest accrual, and bond redemption.

P10-2B On June 1, 2017, Weller SA issued €1,200,000, 8%, 5-year bonds at face value. The bonds were dated June 1, 2017, and pay interest annually on June 1. Financial statements are prepared annually on December 31.

Instructions

- Prepare the journal entry to record the issuance of the bonds.

- Prepare the adjusting entry to record the accrual of interest on December 31, 2017.

- Show the statement of financial position presentation on December 31, 2017.

- Prepare the journal entry to record payment of interest on June 1, 2018.

- Prepare the adjusting entry to record the accrual of interest on December 31, 2018.

- Assume that on January 1, 2019, Weller pays the accrued interest and calls the bonds at 102. Record the payment of interest and redemption of the bonds.

Prepare entries to record issuance of bonds, interest accrual, and bond redemption.

P10-3B Shonrock Co. sold R$800,000, 9%, 10-year bonds on January 1, 2017. The bonds were dated January 1, 2017, and paid interest on January 1. The bonds were sold at 105.

Instructions

- Prepare the journal entry to record the issuance of the bonds on January 1, 2017.

- At December 31, 2017, the amount of amortized bond premium is R$4,000. Show the statement of financial position presentation of the bond liability at December 31, 2017.

- On January 1, 2019, when the carrying value of the bonds was R$832,000, the company redeemed the bonds at 106. Record the redemption of the bonds, assuming that interest for the period has already been paid.

Prepare installment payments schedule and journal entries for a mortgage note payable.

P10-4B Crosetti’s Electronics issues an £800,000, 8%, 10-year mortgage note on December 31, 2016, to help finance a plant expansion program. The terms of the note provide for annual installment payments, exclusive of real estate taxes and insurance, of £119,224. Payments are due on December 31.

Instructions

- Prepare an installment payments schedule for the first 4 years.

- Prepare the entries for (1) the loan and (2) the first installment payment.

- Show how the total mortgage liability should be reported on the statement of financial position at December 31, 2017.

Prepare entries to record issuance of bonds, payment of interest, and amortization of bond discount using effective-interest method.

P10-5B On January 1, 2017, Witherspoon Satellites issued £4,500,000, 9%, 10-year bonds at £4,219,600. This price resulted in an effective-interest rate of 10% on the bonds. Witherspoon uses the effective-interest method to amortize bond premium or discount. The bonds pay annual interest January 1.

Instructions

(Round all computations to the nearest pound.)

- Prepare the journal entry to record the issuance of the bonds on January 1, 2017.

- Prepare an amortization table through December 31, 2018 (2 interest periods) for this bond issue.

- Prepare the journal entry to record the accrual of interest and the amortization of the discount on December 31, 2017.

- Prepare the journal entry to record the payment of interest on January 1, 2018.

- Prepare the journal entry to record the accrual of interest and the amortization of the discount on December 31, 2018.

Prepare entries to record issuance of bonds, payment of interest, and amortization of premium using effective--interest method.

P10-6B On January 1, 2017, Ashlock Chemical AG issued €4,000,000, 10%, 10-year bonds at €4,543,627. This price resulted in an 8% effective-interest rate on the bonds. Ashlock uses the effective-interest method to amortize bond premium or discount. The bonds pay annual interest on each January 1.

Instructions

(Round all computations to the nearest euro.)

- Prepare the journal entries to record the following transactions.

- The issuance of the bonds on January 1, 2017.

- Accrual of interest and amortization of the premium on December 31, 2017.

- The payment of interest on January 1, 2018.

- Accrual of interest and amortization of the premium on December 31, 2018.

- Show the proper non-current liabilities statement of financial position presentation for the bond liability at December 31, 2018.

- Provide the answers to the following questions in narrative form.

- What amount of interest expense is reported for 2018?

- Would the bond interest expense reported in 2018 be the same as, greater than, or less than the amount that would be reported if the straight-line method of amortization were used?

Prepare entries to record issuance of bonds, interest accrual, and straight-line amortization for 2 years.

P10-7B Wu Ltd. sold ¥6,000,000, 8%, 20-year bonds on January 1, 2017. The bonds were dated January 1 and pay interest annually on January 1. Wu uses the straight-line method to amortize bond premium or discount. The bonds were sold at 96.

Instructions

- Prepare the journal entry to record the issuance of the bonds on January 1, 2017.

- Prepare a bond discount amortization schedule for the first 4 interest periods.

- Prepare the journal entries for interest and the amortization of the discount in 2017 and 2018.

- Show the statement of financial position presentation of the bond liability at December 31, 2018.

Prepare entries to record issuance of bonds, interest, and straight-line amortization of bond premium and discount.

P10-8B Rosewell Ltd. sold £4,000,000, 7%, 10-year bonds on January 1, 2017. The bonds were dated January 1, 2017, and pay interest annually on January 1. Rosewell uses the straight-line method to amortize bond premium or discount.

Instructions

- Prepare all the necessary journal entries to record the issuance of the bonds and bond interest expense for 2017, assuming that the bonds sold at 103.

- Prepare journal entries as in part (a), assuming that the bonds sold at 96.

- Show the statement of financial position presentation for the bond liability at December 31, 2017, for both parts (a) and (b).

Prepare entries to record interest payments, straight-line discount amortization, and redemption of bonds.

P10-9B The following is taken from the Sinjh ASA statement of financial position.

| SINJH ASA Statement of Financial Position December 31, 2016 |

|||

| Non-current liabilities | |||

| Bonds payable (face value €2,400,000), 9%, due January 1, 2027 | €2,310,000 | ||

| Current liabilities | |||

| Interest payable (for 12 months from January 1 to December 31) | 216,000 | ||

Interest is payable annually on January 1. The bonds are callable on any annual interest date. Sinjh uses straight-line amortization for any bond premium or discount. From December 31, 2016, the bonds will be outstanding for an additional 10 years (120 months).

Instructions

(Round all computations to the nearest euro).

- Journalize the payment of bond interest on January 1, 2017.

- Prepare the entry to amortize bond discount and to accrue the interest due on December 31, 2018.

- Assume that on January 1, 2018, after paying interest, Sinjh calls bonds having a face value of €800,000. The call price is 102. Record the redemption of the bonds.

- Prepare the adjusting entry at December 31, 2018, to amortize bond discount and to accrue interest on the remaining bonds.

COMPREHENSIVE PROBLEMS

CP10-1 James Ltd.’s statement of financial position at December 31, 2016, is presented below.

During 2017, the following transactions occurred.

- James paid £2,500 interest on the bonds on January 1, 2017.

- James purchased £241,100 of inventory on account.

- James sold for £450,000 cash inventory which cost £250,000. James also collected £31,500 sales taxes.

- James paid £230,000 on accounts payable.

- James paid £2,500 interest on the bonds on July 1, 2017.

- The prepaid insurance (£5,600) expired on July 31.

- On August 1, James paid £12,000 for insurance coverage from August 1, 2017, through July 31, 2018.

- James paid £24,000 sales taxes to the government.

- Paid other operating expenses, £91,000.

- Redeemed the bonds on December 31, 2017, by paying £47,000 plus £2,500 interest.

- Issued £90,000 of 8% bonds on December 31, 2017, at 104. The bonds pay interest every December 31.

- Recorded the insurance expired from item 7.

- The equipment was acquired on December 31, 2016, and will be depreciated on a straight-line basis over 5 years with a £3,000 residual value.

- The income tax rate is 30%. (Hint: Prepare the income statement up to income before taxes and multiply by 30% to compute the amount.)

Instructions

(You may want to set up T-accounts to determine ending balances.)

- Prepare journal entries for the transactions listed above and adjusting entries.

- Prepare an adjusted trial balance at December 31, 2017.

- Prepare an income statement and a retained earnings statement for the year ending December 31, 2017, and a classified statement of financial position as of December 31, 2017.

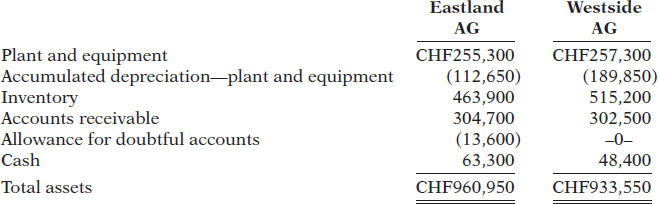

CP10-2 Eastland AG and Westside AG are competing businesses. Both began operations 6 years ago and are quite similar in most respects. The current statements of financial position data for the two companies are shown below.

You have been engaged as a consultant to conduct a review of the two companies. Your goal is to determine which of them is in the stronger financial position.

Your review of their financial statements quickly reveals that the two companies have not followed the same accounting practices. The differences and your conclusions regarding them are summarized below.

Eastland has used the allowance method of accounting for bad debts. A review shows that the amount of its write-offs each year has been quite close to the allowances that have been provided. It therefore seems reasonable to have confidence in its current estimate of bad debts.

Westside has used the direct write-off method for bad debts, and it has been somewhat slow to write off its uncollectible accounts. Based upon an aging analysis and review of its accounts receivable, it is estimated that CHF18,000 of its existing accounts will probably prove to be uncollectible.

Eastland estimated a useful life of 12 years and a residual value of CHF30,000 for its plant and equipment. It has been depreciating them on a straight-line basis.

Westside has the same type of plant and equipment. However, it estimated a useful life of 10 years and a residual value of CHF10,000. It has been depreciating its plant and equipment using the double-declining-balance method.

Based upon engineering studies of these types of plant and equipment, you conclude that Westside’s estimates and method for calculating depreciation are the more appropriate.

Among its current liabilities, Eastland has included the portions of non-current liabilities that become due within the next year. Westside has not done so.

You find that CHF16,000 of Westside’s CHF82,000 of non-current liabilities are due to be repaid in the current year.

Instructions

- Revise the statements of financial position presented above so that the data are comparable and reflect the current financial position for each of the two companies.

- Prepare a brief report to your client stating your conclusions.

MATCHA CREATIONS

(Note: This is a continuation of the Matcha Creations problem from Chapters 1–9.)

MC10 Recall that Matcha Creations sells fine European mixers that it purchases from Kzinski Supply Co. Kzinski warrants the mixers to be free of defects in material and workmanship for a period of one year from the date of original purchase. If the mixer has such a defect, Kzinski will repair or replace the mixer free of charge for parts and labor.

Go to the book’s companion website, www.wiley.com/college/weygandt, to see the completion of this problem.

BROADENING YOUR PERSPECTIVE

Financial Reporting and Analysis

Financial Reporting Problem: TSMC, Ltd. (TWN)

BYP10-1 The financial statements of TSMC appear in Appendix A. The notes to consolidated financial statements appear in the 2013 annual report, which can be found in the Investors section of the company’s website, www.tsmc.com.

Instructions

Refer to TSMC’s financial statements and answer the following questions about liabilities.

- What were TSMC’s total current liabilities at December 31, 2013? What was the increase/decrease in TSMC’s total current liabilities from the prior year?

- What were the components of total current liabilities on December 31, 2013?

- What was TSMC’s total non-current liabilities at December 31, 2013? What was the increase/decrease in total non-current liabilities from the prior year? What were the components of total non-current liabilities on December 31, 2013?

Comparative Analysis Problem: Nestlé SA (CHE) vs. Petra Foods Ltd. (SGP)

BYP10-2 Nestlé’s financial statements are presented in Appendix B. Financial statements of Petra Foods are presented in Appendix C.

Instructions

- At the end of the most recent fiscal year reported, what was Nestlé’s largest current liability account? What were its total current liabilities? What was Petra Foods’ largest current liability account? What were its total current liabilities?

- Based on information contained in those financial statements, compute the following for each company for the most recent fiscal year reported.

- Working capital.

- Current ratio.

- What conclusions concerning the relative liquidity of these companies can be drawn from these data?

- Based on the information contained in those financial statements, compute the following ratios for each company for the most recent fiscal year reported.

- Debt to assets ratio.

- Times interest earned.

- What conclusions concerning the companies’ long-run solvency can be drawn from these ratios?

Real-World Focus

BYP10-3 Purpose: Bond or debt securities pay a stated rate of interest. This rate of interest is dependent on the risk associated with the investment. Fitch Ratings provides ratings for companies that issue debt securities.

Address: www.fitchratings.com, or go to www.wiley.com/college/weygandt

Instructions

Answer the following questions.

- In what year did Fitch introduce its bond rating scale? (See Our Organization.)

- What letter values are assigned to debt investments that are considered “investment grade” and “speculative grade”? (See Ratings Definitions.)

- Search the Internet to identify two other major credit rating agencies.

Critical Thinking

Decision-Making Across the Organization

*BYP10-4 On January 1, 2015, Fleming Ltd. issued £2,400,000 of 5-year, 8% bonds at 95; the bonds pay interest annually on January 1. By January 1, 2017, the market rate of interest for bonds of risk similar to those of Fleming had risen. As a result, the market value of these bonds was £2,000,000 on January 1, 2017—below their carrying value. Debra Fleming, president of the company, suggests repurchasing all of these bonds in the open market at the £2,000,000 price. To do so, the company will have to issue £2,000,000 (face value) of new 10-year, 11% bonds at par. The president asks you, as controller, “What is the feasibility of my proposed repurchase plan?”

Instructions

With the class divided into groups, answer the following.

- What is the carrying value of the outstanding Fleming 5-year bonds on January 1, 2017? (Assume straight-line amortization.)

- Prepare the journal entry to redeem the 5-year bonds on January 1, 2017. Prepare the journal entry to issue the new 10-year bonds.

- Prepare a short memo to the president in response to her request for advice. List the economic factors that you believe should be considered for her repurchase proposal.

Communication Activity

BYP10-5 Ron Seiser, president of Seiser AG, is considering the issuance of bonds to finance an expansion of his business. He has asked you to (1) discuss the advantages of bonds over equity financing, (2) indicate the types of bonds he might issue, and (3) explain the issuing procedures used in bond transactions.

Instructions

Write a memo to the president, answering his request.

Ethics Case

BYP10-6 Dylan Horn is the president, founder, and majority owner of Wesley Medical Ltd., an emerging medical technology products company. Wesley is in dire need of additional capital to keep operating and to bring several promising products to final development, testing, and production. Dylan, as owner of 51% of the outstanding shares, manages the company’s operations. He places heavy emphasis on research and development and on long-term growth. The other principal shareholder is Mary Sommers who, as a non-employee investor, owns 40% of the shares. Mary would like to deemphasize the R&D functions and emphasize the marketing function, to maximize short-run sales and profits from existing products. She believes this strategy would raise the market price of Wesley’s shares.

All of Dylan’s personal capital and borrowing power is tied up in his 51% share ownership. He knows that any offering of additional shares will dilute his controlling interest because he won’t be able to participate in such an issuance. But, Mary has money and would likely buy enough shares to gain control of Wesley. She then would dictate the company’s future direction, even if it meant replacing Dylan as president and CEO.

The company already has considerable debt. Raising additional debt will be costly, will adversely affect Wesley’s credit rating, and will increase the company’s reported losses due to the growth in interest expense. Mary and the other minority shareholders express opposition to the assumption of additional debt, fearing the company will be pushed to the brink of bankruptcy. Wanting to maintain his control and to preserve the direction of “his” company, Dylan is doing everything to avoid a share issuance. He is contemplating a large issuance of bonds, even if it means the bonds are issued with a high effective-interest rate.

Instructions

- Who are the stakeholders in this situation?

- What are the ethical issues in this case?

- What would you do if you were Dylan?

Answers to Insight and Accounting Across the Organization Questions

p. 491 How About Some Green Bonds? Q: Why might standardized disclosure help investors to better understand how proceeds from the sale or issuance of bonds are used? A: By requiring transparency as to how a bond’s proceeds are to be used and how they will affect a company’s sustainable profitability, investors will make better financial decisions.

p. 499 Bonds versus Notes? Q: Why might companies prefer bond financing instead of short-term financing? A: In some cases, it is difficult to get loans from banks. In addition, low interest rates have encouraged companies to go more long-term and fix their rates. Recently, short-term loans suddenly froze, leading to liquidity problems for certain companies.

p. 501 “Covenant-Lite” Debt Q: How can financial ratios such as those covered in this chapter provide protection for creditors? A: Financial ratios such as the current ratio, debt to assets ratio, and times interest earned provide indications of a company’s liquidity and solvency. By specifying minimum levels of liquidity and solvency, as measured by these ratios, a creditor creates triggers that enable it to step in before a company’s financial situation becomes too dire.

A Look at U.S. GAAP

Learning Objective 12

Compare the accounting for liabilities under IFRS and U.S. GAAP.

IFRS and GAAP have similar definitions of liabilities. IFRSs related to reporting and recognition of liabilities are found in IAS 1 (revised) (“Presentation of Financial Statements”) and IAS 37 (“Provisions, Contingent Liabilities, and Contingent Assets”). The general recording procedures for payroll are similar although differences occur depending on the types of benefits that are provided in different countries. For example, companies in other countries often have different forms of pensions, unemployment benefits, welfare payments, and so on. The accounting for various forms of compensation plans under IFRS is found in IAS 19 (“Employee Benefits”) and IFRS 2 (“Share-based Payments”). IAS 19 addresses the accounting for a wide range of compensation elements, including wages, bonuses, post-employment benefits, and compensated absences. Both of these standards were recently amended, resulting in significant convergence between IFRS and GAAP.

Key Points

Similarities

- The basic definition of a liability under GAAP and IFRS is very similar. Liabilities may be legally enforceable via a contract or law but need not be; that is, they can arise due to normal business practice or customs.

- Both GAAP and IFRS classify liabilities as current or non-current on the face of the statement of financial position. IFRS specifically states, however, that industries where a presentation based on liquidity would be considered to provide more useful information (such as financial institutions) can use that format instead.

- The basic calculation for bond valuation is the same under GAAP and IFRS. In addition, the accounting for bond liability transactions is essentially the same between GAAP and IFRS.

Differences

- Under IFRS, companies sometimes show liabilities before assets. Also, they will sometimes show non-current liabilities before current liabilities. Neither of these presentations is used under GAAP.