APPENDIX TO CHAPTER 4

DV01, Duration, and Convexity

A4.1 DV01, DURATION, AND CONVEXITY OF PORTFOLIOS

Let ![]() denote the price of asset

denote the price of asset ![]() and

and ![]() the price of a portfolio of those assets. By definition,

the price of a portfolio of those assets. By definition,

Let ![]() be the single factor generating changes in rates. Then, taking the derivative of both sides of (A4.1) with respect to

be the single factor generating changes in rates. Then, taking the derivative of both sides of (A4.1) with respect to ![]() ,

,

Then, divide both sides of (A4.2) by ![]() 10,000 and apply Equation (4.5) of the text to see that,

10,000 and apply Equation (4.5) of the text to see that,

Or, in words, the DV01 of a portfolio equals the sum of the individual asset DV01s.

To derive the duration of a portfolio, start from Equation (A4.2), dividing both sides by ![]() ,

,

Equation (A4.5) multiplies each term in the summation by one, in the form of ![]() . Equation (A4.6) follows from the definition of duration in the text, Equation (4.11). In words, Equation (A4.6) says that the duration of a portfolio equals the weighted average of the durations of the individual assets, where the weights are the fraction of value of each asset in the portfolio.

. Equation (A4.6) follows from the definition of duration in the text, Equation (4.11). In words, Equation (A4.6) says that the duration of a portfolio equals the weighted average of the durations of the individual assets, where the weights are the fraction of value of each asset in the portfolio.

The proof for the convexity of a portfolio can be derived along the same lines as the duration of a portfolio. The result, given here without proof, is,

A4.2 ESTIMATING PRICE CHANGE WITH DURATION AND CONVEXITY

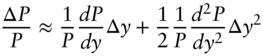

Let ![]() be the price of an asset as a function of the single factor that describes changes in rates. Then, a second‐order Taylor approximation of the price rate function is given by,

be the price of an asset as a function of the single factor that describes changes in rates. Then, a second‐order Taylor approximation of the price rate function is given by,

Subtracting ![]() from both sides of (A4.8) and denoting the change in price,

from both sides of (A4.8) and denoting the change in price, ![]() , by

, by ![]() ,

,

where (A4.11) – which is Equation (4.16) – follows from the definitions of duration and convexity, that is, from Equation (4.10) and a discrete version of Equation (4.14).