The day-to-day operation of a fund will be driven by the type of fund. Actively managed and open-ended funds will potentially have more workflow than passive and closed funds. Portfolios of illiquid assets will be less active than retail funds operating in liquid assets. As we have seen earlier, the investment objectives, types of instruments, and products and strategies employed by the manager will also impact on the workflow within the fund operations and support. Likewise the investment process can involve the fund in a legal agreement with the investment manager and the services offered to the manager by the prime broker will be subject to a prime broker/broker agreement.

Keywords

open ended funds

retail funds

investment manager

illiquid assets

closed funds

Introduction

The day to day operation of a fund will be driven by the type of fund. Actively managed and open ended funds will potentially have more workflow than passive and closed funds. Portfolios of illiquid assets will be less active than retail funds operating in liquid assets.

As we have seen earlier, the investment objectives, types of instruments, and products and strategies employed by the manager will also impact on the workflow within the fund operations and support.

Likewise the investment process can involve the fund in a legal agreement with the investment manager and the services offered to the manager by the prime broker will be subject to a prime broker/broker agreement.

The service provision by the custodian and administrator will also be governed by legal agreements that establish the relationship and a service level agreement (SLA), which determines the provision and responsibilities in the service delivery by each party.

Key content of the SLA would include:

1. General scope of the service including types of assets to be processed by the administrator, key contacts for both parties, escalation routes etc.

2. Communication channels for receipt and delivery of data, for example, SWIFT messages, prime broker/broker proprietary systems, email, hard copy etc.

3. Timings and deadlines for provision of data between the parties.

4. Sources of data, for example, asset transactions, prices for valuation, subscriptions and redemptions (if administrator is providing the transfer agent service).

5. Internal and external reporting requirements including regulatory and investor communications.

6. Scope of secretarial services if being provided by the administrator.

7. Accounting policies and requirements.

8. Risk management and Compliance services. The administrator can provide assistance to the fund with risk management and compliance for the fund but the responsibility remains the funds.

9. Benchmarking of the service.

10. Waivers, indemnities etc.

This is clearly a key document and is covered again in Part 4.

Parts of the content of the SLA will be related to the process workflow.

Process workflow

The process workflow for a fund will fall into three areas:

1. Operations

2. Valuation and accounting

3. Transfer agency

As we have already seen in earlier chapters these areas are linked with the investment activity and the investor activity linked to the valuation and accounting processes.

Within each area there are specific tasks and functions the team will undertake and we can explore these now.

We saw earlier in the book the following diagram covering the workflow for a securities asset transaction in a fund:

The following provides examples of some of the key process workflow the administrator and/or custodian are involved in during the flow shown earlier.

Investment capital

1 Subscription and redemption in the shares and units of the fund

Investment process

2 Investment decisions

Asset servicing

3 Corporate actions

The administrator and custodian will incorporate these high level process blocks into their system capabilities and design procedures to deliver the operational process.

As data is such a key driver in the functions of administration and custody, a strong database capability is essential if the amount of manual process is to be minimized.

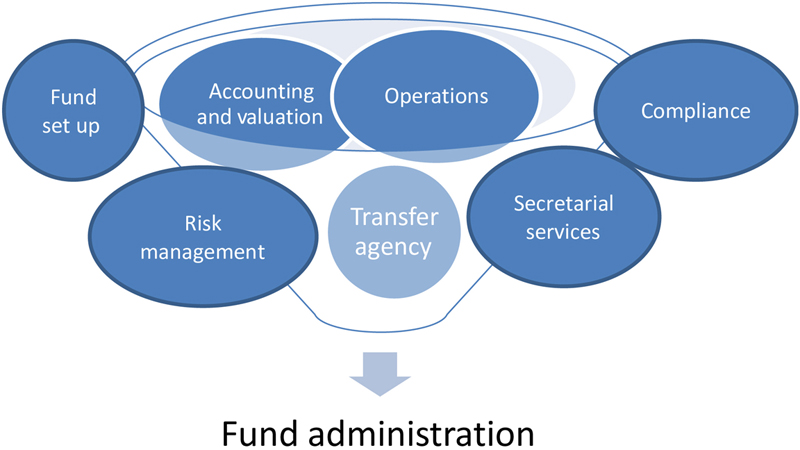

As we know generically there are several component parts of what is fund administration as the following diagram shows.

The precise nature of the service that a fund requires and an administrator can offer does of course depend on many factors.

As we have said this will include the assets the funds invest in, the strategies used, passive or actively managed, form the fund takes in terms of being regulated or unregulated, retail or alternative investment fund, and the requirements of the jurisdiction in which the fund is based. The requirement of the promoter/owner and the investors is also a key component of the relationship that will exist between the fund and its administrator.

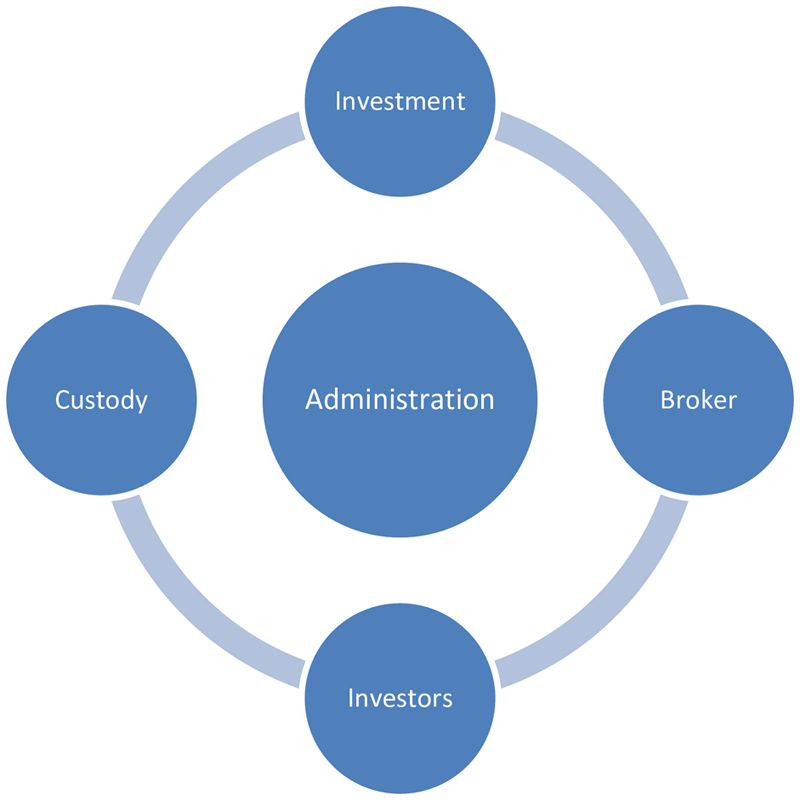

Where does fund administration sit in terms of the whole investment process?

Fig. 3.1 shows how the principle relationships are with the investment manager, brokers and prime brokers, custodians/depositaries, and the investors.

Figure 3.1

The other key parties the administrator may be involved with, include:

• Promoter/owner.

• Nonexecutive directors.

• Risk and compliance managers.

• Auditors.

• Agents and intermediaries—for example, derivative brokers/counterparties as well as property management companies (real estate funds), specialist accountants (private equity funds), and parties involved in the transaction and warehousing of alternatives like art, collectibles, and commodities.

• Banks—that is, custodian banks.

And, possibly, although on probably an infrequent basis,

• Tax advisers

• Lawyers

We will now look at the work flow that each component of the administration service undertakes.

At a high level the possible structure for a full service administrator is as shown in the following diagram.

Fund operations

The fund operations team will be dealing with the asset transactions, which are made for the portfolio of the fund. The transactions are typically in one of the following:

• Securities—equities, bonds.

• Derivatives—futures, forwards, options, swaps.

• Commodities—agricultural, energy, metals, etc.

• Property—retail (housing) or commercial (offices, warehouses, shops).

• Investment funds—retail funds and alternative investment funds (hedge funds, private equity funds, property funds). Funds like fund of funds and some retail funds are able to invest in the shares or units of other investment funds.

• Alternatives—art, antiques, structured products, infrastructure etc.

In addition we have cash, like deposits (overnight money) and short term money market instruments (Treasury Bills, Certificate of Deposit (CDs), Commercial Paper) as well as trades in currencies (foreign exchange).

The role of the operations team is to interact with the investment manager to obtain the asset trades undertaken and to then reconcile the successful finality of settlement of these transactions. In this book, unless otherwise stated, this means the party involved in the investment process including a manager, committee etc.

As part of this process the administrator will reconcile positions and cash movements in the fund portfolio with the custodian, broker, or counterparty.

Any discrepancies will be immediately relayed to the investment manager for resolution and may need reporting internally to the risk manager and/or senior management depending on the terms of the SLA between the fund and the administrator.

The details of the transaction will be posted into the fund records and accounts.

•Source

• Broker—executed trades

• Prime Broker—executed trades

• Manager—placed and completed orders

• Data received from manager and brokers through statements, confirmations etc.—note this is likely to be an automated process but may also be manual

•Update portfolio

• Validation of manager versus broker data

• Position/exposure limits check versus mandate/offering document/regulation

• Transaction details posted to fund records

•Settlement

• Custodian settlement details/ positions in the assets in their account at CSD or clearing house/broker is reconciled to the data for the portfolio—unsettled trades are managed by the custodian but monitored by the administrator and included in the positions and NAV calculations. Note—unmatched transactions cannot proceed to settlement and cannot be included in the funds records and NAV calculations, however pending the resolution by the manager and counterparty they will be provisionally included in the cash forecast.

•Corporate actions

• Managing the outcome of any corporate actions announced on assets held by the fund (fund can lose money or other benefits if this process (carried out by the custodian and monitored by the administrator) is not managed properly.

• Cash movements resulting from corporate actions will need to be included in the cash forecast.

Summary of the workflow

• Portfolio trade capture—ensuring that all transactions are properly detailed in the records of the fund.

• Booking into the fund’s records—allocating all transactions to the relevant fund.

• Reconciliation to brokers/custodian—primary control for ensuring that the portfolio agrees with the positions from the market/counterparties.

• Portfolio position reports to investment manager—advising the investment manager that the portfolio is reconciled of any discrepancies that the manager needs to resolve/remain unresolved.

• Corporate actions—ensuring that any corporate action has been managed and the outcome updated in the fund’s records.

• Mandate checks—ensuring the fund is complying with its offering documents.

• Possibly broker/third-party agreements in conjunction with legal/compliance, that is, ISDA documents for over the counter (OTC) derivatives—ensuring the fund has agreed and signed agreements for services, settlement of products/assets, etc.

Valuation and accounting

The valuation and accounting team are responsible for maintaining the full accounts of the fund, carrying out valuations of the assets of the fund and incorporating the realized and accruals for income and expenses so that the NAV and if required the NAV per share/unit can be calculated.

The frequency of this NAV calculation will depend on the fund and as we have already seen this could be daily, weekly, monthly, or quarterly. Remember some funds operating in illiquid assets and closed funds with a stated investment period, that is, private equity funds may have a less frequent NAV calculation.

The following are the tasks of the team:

•General ledger

The fund’s accounting records will be maintained in the general ledger (G/L) and in most cases the GL will have sub ledgers for the recording of specific items like investments, expenses, income, tax, commissions etc.

The entries to the GL are usually on a double entry bookkeeping basis.

The control over and reconciliation of entries to the ledgers is vitally important and is part of the risk management process of the fund and the administrator.

•Valuing the funds property (investments)

This is needed for the measuring of the performance of the fund, contributes to the NAV calculation and may also relate to subscription and redemption values as well as performance fees, where applicable.

•Income and expenses

The team will identify and post realized and accrued income and expenses to the ledgers.

•Publishing the price of funds

This will usually be based on the NAV and shares/units in issue and will be carried out in accordance with the offering documents. The team will need to make sure that the relevant sign offs have been done before publication.

Usually a senior manager in the administrator will sign off the NAV and pass it to the fund where the investment manager or other designated party will also sign off on the value. The responsibility for the correctness and publication of the NAV lies with the fund.

•Impact of incorrect pricing of investments

Should this situation arise, the regulators and/or offering documents and agreements establish how and when compensation is due on incorrect pricing and the team will need to follow the relevant procedure.

The compensation is due to investors who have subscribed or redeemed their shares or units at an incorrect value. Note—investors that have benefited from the error will be unlikely to have to repay the gain.

On identification of such a mispricing it must be escalated to senior management in the administrator and to the fund manager and governance.

•Pricing controls and policy

The fund will need to have clearly laid down controls and policies for the pricing and valuing of assets. This is essential if the risks associated with the valuation process are to be managed and will be followed by the team when calculating the NAV.

It should be compiled by the fund in conjunction with the administrator and any deviation from the policy needs to be logged.

The pricing policy is likely to be linked into an overall valuation policy such as the following:

Extracts on pricing and valuation

The following are extracts from the CLT Advanced Certificate & Diploma in Fund Administration.

Pricing models

Pricing models can be very important but there must also be recognition of their limitations in some cases. Nonetheless, the use of models plus subjective analysis can produce a reasonable and meaningful value.

Models work on data so the access to a data source is critical, but even then a model cannot tell you exactly what will happen to a price unless it is based on all the relevant detail. Pricing models can also be expensive to buy or build and to maintain. Does the fund administrator spend large sums on models only to see a decline in the use of the products the models can now value?

It may also be that the investment manager has developed a pricing model and is not keen to have anyone else access how it works. As part of the pricing policy, accepting a value for pricing purposes from such a model would have to be confirmed as acceptable.

What is a reasonable price or value?

One way of working out what a reasonable value might be for the CMO we have been talking about is to look first at the rate of defaults in sub-prime mortgages of the kind held in the CMO and second at the credit default swaps market for Bear Stearns.

The first should allow a judgement on the likelihood that the tranche will default, while the second could show the probability of a default by Bear Stearns.

Don’t forget that hedging the risk will be a cost to the fund and therefore a lower return of interest and or capital than expected if the default occurs.

While a fund that accepts risk might accept the possible default (lower return of interest and/or capital than expected) in favor of the potentially much higher yield, one could still possibly expect to see them hedge part of the counterparty risk, at least, and probably the CMO risk too if things started to happen in the market.

It would be wrong to have the CMO showing in the fund as still valued at $60m, unless the manager and advisers can give a very good reason or can demonstrate that there are offsetting products hedging the exposure.

Would the scenario described above constitute an “easy” or “difficult” position to value? The answer could be that it is easy, if the components and the issuer can be assessed in terms of risk and yield, or difficult, because the precise interpretation of the degree of risk, ability to sell on or novate and the options to hedge out the risk are themselves fairly volatile, for example, the prime broker might agree to novate the position today and refuse or massively increase the discount tomorrow. Likewise, the cost of buying protection through a CDS on Bear Stearns might jump 200 points overnight.

Of course the CMO might be redeemed perfectly OK and all interest paid as expected (assuming the mortgages don’t default) because the issuer is taken over by a strong party, as in fact happened when J P Morgan Chase acquired Bear Stearns.

Pricing and value issues

The less transparent the product the greater the degree of caution in valuing it: many highly complex CDOs or so-called toxic assets have a range of value from 0% to 100%. Some may and probably will be near to zero but many may yet deliver much if not all their value.

One possibility is that there will be gradual write-downs and write-ups in value, which are preferable to huge swings in value. The exception to this would be if something highly significant triggers such a change in value, which needs to be reflected immediately.

Accounting rules may also affect how a position is valued and indeed the concept of mark to market and fair value can cause the value to be shown as zero if there is poor liquidity, even though the product in reality does have some potential value.

Valuation in practice

It is important that the process of valuation is thought through carefully on a product-by-product basis.

Valuations of complex products will be based on the issues shown earlier and while this may not be an exact science it should still be possible for auditors and regulators to look for evidence of reasonableness in the interpretation of the “real” value and the “probable” value, taking into account the market situation, hedges, etc. with suitable pricing and valuation then applied. This concept, with some adjustment, should be applicable across private equity and property funds. The issues specific to private equity and property are naturally related to the characteristic of the assets.

Private equity can be venture capital or buy out related.

Venture capital is in turn related to small, medium sized businesses that are start ups or growing entities.

These unlisted companies are in need of capital and this can sometimes be achieved through private equity funds. The PE fund invests in the companies mainly in equity but sometimes in debt instruments.

For the administrator the key issues are how to value the unlisted company and also how income such as dividends or interest is received from the investee company.

For example, dividends could be in the form of shares rather than cash and interest on debt may be paid on maturity and not at regular intervals as would happen with a government bond. Indeed, the interest amount may also be paid in shares rather than cash.

There are very few issues with the on-exchange products. In the on-exchange markets and products while there can be volatility in prices, because the price is derived from the exchange there is a readily available, independent and robust source of pricing.

Valuation checklist

It is always useful for control purposes to have procedures and checklists that can be used operationally and to demonstrate adequate control to auditors and regulators.

Example for Valuation Checklist

Following is an example of such a checklist:

Use of asset and strategy

Meets the mandate/offering documents

Use authorized

Relevant board meeting, committee minutes, etc.

Operational awareness

Check to see that adequately resourced and knowledgeable operational support is in place

Risk awareness

Management controls over exposure and counterparty risk in place

Valuation processes and methodology

Clearly defined, workable pricing policy

Designated pricing agent

Escalation procedures for issues

Documented pricing sources and approved methodologies

Approved hedging products and strategies

Comparison usage and benchmarks to assess reasonableness of value

“Difficult to value” assets

Identification of types of asset and strategy

Documented valuation and pricing policy

Source: CLT International Advanced Certificate in Fund Administration

Income and expense

The team will need to identify all income and expenses of the fund and post these to the relevant ledgers.

Income can be from a variety of sources, for example, from:

1. Income generating assets like bonds.

2. Distributions of share of profits from dividends.

3. Interest on cash deposits.

4. Fees from securities financing.

Expenses can be generated by the following:

1. Invoices for services from parties such as the custodian, administrator etc.

2. Director’s, Trustee, General Partner fees.

3. Commissions and fees associated with assets trades.

4. Fees associated with securities financing.

5. Start-up fees and costs.

6. Performance fees payable.

7. Regulatory fees and costs.

These lists are not exhaustive and unique costs and income might be generated for certain types of funds. For example, withholding tax may occur on income from assets but may be reclaimable. Ledgers will need to reflect this.

Margin and collateral

Some funds may become involved in margin calls and collateral and this must be reflected in the relevant ledgers in the accounts.

In addition some income and fees will be periodic and some may be one off.

It is vitally important that the Capital and Income elements of the fund are kept separate in the accounts of the fund.

Distributions

The team will calculate the available amounts for distribution funds over the relevant period.

Once the gross amount is calculated the amount per share or unit is then applied to the investor’s holding.

We can look at an example here:

Income for the period calculated incorporating any deductions = £1,000,000

Fund accumulation shares = 50,000

Fund distribution shares = 75,000

Total shares in issue = 125,000

Distribution = £1,000,000/125000 = £8 per share

NAV per share of the fund = £12

Fund accumulation shares receive 1.5 shares

Fund distribution shares receive £8 per share

Impact—accumulation shares now = 75,000

Distribution shares = 75,000

The team may need to seek advice from the tax expert in respect of a deduction of tax, if any.

Performance fee calculation

The team will most likely be involved in the calculation of performance fees where these are payable to the investment manager under the IMA.

The basis for calculation of the fee will be in the offering documents and the administrator will also need to apply any equalization process if this applicable. See Appendices for flows in relation to performance fee and carried interest calculations.

Management Information

The team may need to produce management information for the fund.

This will be contained in the Agreement and the SLA between the fund and the administrator and could include data on:

• Change in NAV

• Commissions and fees paid

• Distributions

• Performance and performance fees

• Errors

Summary of accounting issues and controls

• Key accounting issues.

• Valuation

• Profit and loss

• Cash flows

• Verification

• Disclosure

• Key controls.

• Reconciliation of all cash movements is primary accounting control in any business.

• Independent verification of existence (and value) of assets and liabilities.

• Application of relevant accounting policies and standards.

Regulation and disclosure

•Capital markets highly regulated

• European banking laws & directives (MiFID/MiFID II, Basel II, AIFM)

•UK—FCA/PRA, Europe—EMIR/ESMA, United States—SEC, CFTC

• Industry associations; best practice

• National accounting standards

Accounting procedures must comply

Summary

•Consistent valuation policy

•Accurate profit and loss measurement

•Reconciliation of cash flows

•Verification of assets/liabilities

•Compliance re disclosure

Transfer agency

The transfer agency team will be involved in several key areas of the operation of the fund.

Naturally a major function is that of dealing with the subscriptions and redemptions by investors in the fund but it is not the only key task.

Other important aspects of the transfer agency role are:

•The role of the maintaining of the stakeholders register for units or shares:

• Issuing acknowledgement

• Certificated and book entry record to the fund Register

• Amending records

• Dividend payments

• Power of Attorney

•International transactions—Ensuring comprehensive KYC and AML checks are carried out, identifying any constraints and ensuring correct share class has been applied.

Subscriptions and Redemptions

The life cycle of the subscription and redemption process can be illustrated by the following:

This diagram shows the process for the subscription to a fund. This could be via a public offering, placement, advertising, or through an intermediary. The T/A will need to carry out relevant KYC and AML checks. The KYC involves checking that the applicant has the right status for the fund they are applying to invest in, particularly for restricted investor funds and also that the investor is meeting and maximum/minimum application or position and is not for any reason unacceptable to the owners/managers.

AML checks are important and becoming more so, even to the extent of nonregulated funds having to do AML due diligence as matter of law rather than regulation.

If all is in order the cash is received and the register is updated with any acknowledgement, certificate or contract note sent to the investor.

The manager may want to see any significant applications in terms of name and amount as large subscriptions and redemptions can potentially create problems.

Redemptions also require due diligence in terms of who is authorized to request redemption, are the proceeds to go to the same place as the source of incoming capital etc.

Switches are somewhat different as in an umbrella fund the investor may switch between funds without any payment involved but checks are still necessary.

Distributions

We have seen in the section on the work of the valuation and accounting team that for some classes of shares a fund may be making distributions of income either reinvested for accumulation shares or distributed for distribution shares.

Once the available amount per share has been calculated, the transfer agency will prepare the statement for the investor showing the additional shares now in their name or the amount payable.

On the due date the register will be updated accordingly and payments made where relevant.

The statement will make reference to any tax that may be deductible.

Custody and depositary

Now let us look at the role and work of the custodian.

In the day to day operations of the fund the custodian is performing some key tasks.

The custodian holds and manages, in their name, the assets that belong to the fund. At all times the custodian is holding the title to assets in their name but “beneficially” for the client. The custodian has no interest in the assets of the client and they are held segregated away from the assets of the custody firm.

Clients like funds can benefit from having the settlement and postsettlement processes managed by a specialist custodian. The safekeeping of the assets of the fund are a major issue for investors in a fund as loss of the fund’s assets through fraud, theft, or uninsured destruction of assets can collapse a fund and lose the investors all their capital.

Typically a custodian has core services and added value services it can offer its fund client.

Core services would potentially comprise:

• Status reporting (matched/unmatched)

• Settlement of trades

• Safekeeping of physical assets

• Income collection

• Managing corporate actions

• Proxy voting

• Withholding tax reclaims

We can see that these services are built around the fact that the custodian is holding the assets of the fund in its name and is therefore well positioned to manage processes like settlement and income selection.

We can see here the detail of what the custodian is doing.

•Status reporting

• As the link between the CSD the custodian can report on the status of the fund’s transaction with the market.

•Settlement of trades

• The custodian ensures the receipt and payment of shares or cash in settlement of the transactions the manager has undertaken.

•Safekeeping of physical assets

• Where assets are in paper or physical format the custodian will hold the assets securely in a vault.

• Where assets are in dematerialized form the custodian holds an electronic record in their books which is reflected in their record with the relevant CSD.

•Income collection

• The custodian can calculate the dividend, interest or other income due from a position and receive and report on the successful receipt of the payment from the source.

• If the payment is not direct, for example, because of a late settlement of a transaction, the custodian will make a claim from the party concerned.

•Managing corporate actions

• The custodian can calculate the outcome of a corporate action and manage the results/adjust the records/make and receive payments etc.

•Proxy voting

• The custodian can vote on behalf of the fund where the regulations permit.

•Withholding tax reclaims

• If investments are in overseas locations where tax is deducted at source, the custodian can, if the fund qualifies and the jurisdiction permits, reclaim the tax paid.

Then there are the added value services that a client of the custodian can opt to use and pay for on the basis of the usage, for example:

• Management, client, and regulatory reporting

• Stock lending and borrowing

• Cash management

• FX services

• Portfolio pricing and valuation

• Derivatives clearing and settlement

• Market information

Custodians have developed these services in order to offer a comprehensive service to clients like funds. For example, some portfolio pricing and valuation are typically part of the services offered by a fund administrator. It therefore follows that a custodian could also be the administrator for some types of fund.

We can see here the detail of these added value services:

•Management, client, and regulatory reporting

• The custodian maintains extensive data and information related to markets, trades, positions, etc. and can provide an extensive suite of reporting to the fund.

•Stock lending and borrowing

• Custodians can manage both the lending and borrowing requirements of securities for the fund, assuming the fund wishes to lend or borrow securities.

•Cash management

• Custodians receive and pay out cash in settlement of transactions or income from dividends etc., and offer management services to ensure funding requirements and excess cash is managed efficiently for the fund.

•FX services

• Custodians can provide foreign exchange services to the fund if required.

•Portfolio pricing and valuation

• The positions held by the fund can be independently valued using the custodian’s sources of market prices.

•Derivatives clearing and settlement

• Custodians can provide information, settlement, and position maintenance for many types of derivatives often involving another Group entity.

•Market information

• The custodian is an important source of price information, data on corporate actions, exchange rates etc.

Core services are usually paid for by an assets under management (AUM) formula while added value services are charged on a usage basis.

The fees are negotiated and core service fees will have both a floor (minimum charge) and a tapering charged on high value AUM.

Custody fees are usually accrued in the accounts to avoid a spike affecting the fund’s net asset value, which will occur if the total cost of the custodian’s invoice hits the fund accounts on a single day.

Global custody

A global custodian provides clients with multicurrency custody, settlement, and reporting services, which extend beyond the global custodian’s and client’s base region and currency; and encompass all classes of financial instruments.

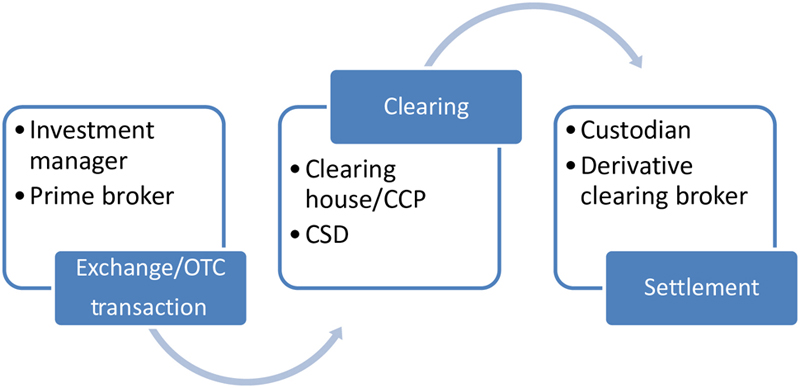

The workflow for an asset transaction is as shown:

The life cycle of the trade starts with the order being placed by the investment manager to the broker and execution of the trade.

The trade will enter into the clearing phase and is recorded at the CSD and or clearing house/CCP.

This is followed by the data capture and validation process by the fund’s administrator and then settlement processing by the custodian of the fund at the CSD.

Key reconciliations will take place at various stages in the process including the primary reconciliation by the administrator of the portfolio positions and those held at the custodian and brokers.

The diagram earlier follows on from the one we saw at the beginning of this section.

The shown flows are based on securities transactions and yet there will be some important and subtle differences dependent on the actual assets. For example, for a property fund that is operating in physical property, there will be no paper share certificate or dematerialized security but instead there will be the Title Deeds of the property, which will be the evidence of ownership.

We can now look at the life cycle of derivatives transactions.

Life Cycle of Derivatives Transactions

Derivatives are either traded on-exchange or off-exchange OTC and can settle via CCP or directly between parties, although since 2008 regulatory change means that many OTC derivatives now settle via a CCP.

We can look again at the relationships in Fig. 3.2:

Figure 3.2

Contractual parties to derivative contracts trade as principal; both on-exchange and OTC.

Exchange traded derivatives (eg, futures) have the benefit of a central clearing house, which greatly reduces counterparty risk exposure within the market by providing multilateral netting among the clearing house members. Today as noted above, many OTC products now also benefit from the central clearing process.

The CCP has various protective procedures in place—especially the margining process and the daily settlement of losses through the variation margin process. Students should study Chapter 5 which explains derivatives further.

Clients or end users as they are known will still have credit risk exposure to their clearing bank or broker.

The life cycle of a derivatives trade follows some of the routing that occurs for some kinds of securities.

Settlement of On-Exchange Derivatives

On-exchange derivatives settle via a CCP/Clearing House and are in the form of a standardized contract. Standardized contracts are designed by the exchange and the product detail is contained in the contract specification issued by the exchange.

Principal on-exchange products are futures and option contracts on a wide range of what is called the underlying such as equities, debt and interest rate instruments, commodities, credit and currencies.

The life cycle of a trade moves through the phases we are by now familiar with so we have execution, trade capture, and then the middle and back office process.

We can see the main processes in the phases in the Fig. 3.3 and we then look at the OTC scenario.

Figure 3.3

The post execution phase for futures and options will involve the clearing of the trades and the maintenance of the open positions by the CCP/Clearing House in the name of a clearing member as shown in Fig. 3.3.

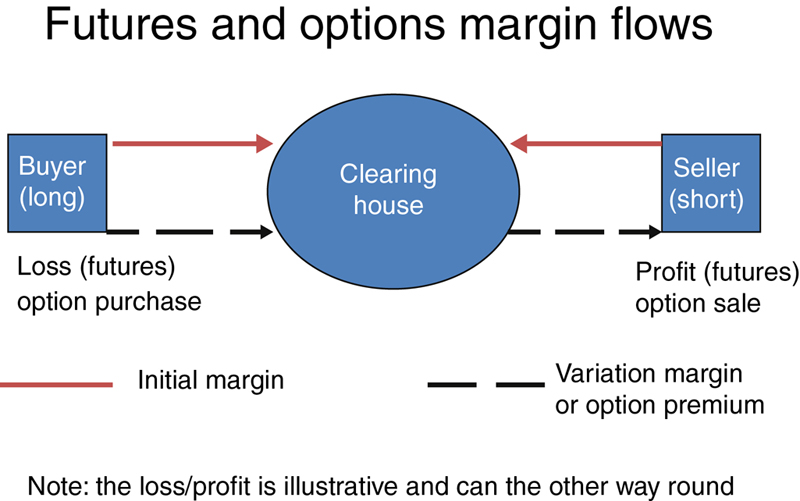

For futures contracts there is a daily variation margin calculation (a revaluation process) and the amount generated by the calculation is for settlement.

In addition there is a security deposit that is called initial margin that must be covered by collateral lodged at the CCP/Clearing House until all obligations have been met and the open position closed, delivered, or matured.

The daily settlement components are summarized in Fig. 3.4:

Figure 3.4

In Fig. 3.4, we see the main settlement processes and to this we can also add monitoring the initial margin and collateral management process.

The daily workflow in this part of the life cycle is illustrated in Fig. 3.5.

Figure 3.5

As we can see the settlement process is carried out with a convention of T + 1 with the preparatory workflow on trade day.

This workflow may well involve the same positioning process that we find in securities settlement but related to collateral and payments.

The post settlement phase of on-exchange derivatives involves both the management of the variation and initial margin flows but also the potential exercise, assignment, and tendering for delivery process as well.

The latter can occur on maturity or depending on the contract specification at times during the life of the contract, an example being that American style options can be exercised any busy day by the buyer.

In the appendices, there are diagrams that should be studied carefully as they are related to these exercise, assignment, and tendering for delivery processes.

Life Cycle of the Settlement of OTC Derivatives

As noted earlier many OTC trades are today settled via a CCP rather than directly between the counterparties, for example interest rate and credit default swaps.

Therefore there are two distinct process flows associated with OTC derivatives, one centralized the other not.

We can see the main workflow illustrated in Fig. 3.6.

Figure 3.6

In Fig. 3.7, we can see that although there may be a variation type process, that is, a mark to market revaluation this may only be for P/L calculations and not a settlement amount.

Figure 3.7

Exercise

Now let us do an exercise related to the calculation of variation and initial margins, fees, and change to the cash balance of a series if trades (Fig. 3.8).

Figure 3.8

You need to calculate the initial and variation margin, commission, and the change to the cash balance at the broker as a result of these trades.

The answer can be found in Part 5 of the book.

Securities lending and borrowing

Securities Lending

Now let us look at securities lending and explore what it is and the life cycle of what is a very important part of the financial markets.

Introduction

Securities Lending Defined

Securities lending is the lending of equities and bonds by or on behalf of an investor to counterparties who are authorized to borrow securities in return for a fee.

Securities lending provides liquidity to the market by utilizing securities that would otherwise be “side-lined” by being held in safekeeping thus providing yield enhancement in the form of the fee received.

A major industry organization, The Group of Thirty, recognized the importance of securities lending and made a recommendation which stated that:

Securities lending and borrowing should be encouraged as a method of expediting the settlement of securities transactions. Existing regulatory and taxation barriers that inhibit the practice of lending and borrowing securities should be removed.

The “...expedition of securities transactions” is not the only reason why securities lending and borrowing takes place. Furthermore, not every market or regulatory jurisdiction implements appropriate measures to “...encourage...” the practice. Indeed post the market crash, many regulators and markets had serious concerns that securities lending had contributed to volatility and share price declines primarily associated with short selling strategies used by some hedge funds.

Some regulators introduced prohibitions on short selling and/or securities lending although many have realized that securities lending itself is a crucially important facility in the efficient operation of the markets, particularly, in terms of settlement on due date.

Characteristics of securities lending

Legal title to the securities passes from the lender to the borrower but the benefits of ownership are retained by the lender.

This is important as it means that the lender continues to receive income and retains the right to sell the securities in the stock market although this may be subject to any constraints in respect of the terms of the loan. The lender, however, loses the right to vote.

In terms of the income like dividends or interest this will not be paid direct to the lender as their name will have been removed from the issuer or company’s register; instead the income is claimed from and paid by the borrower.

Uses of securities lending

Market participants borrow for a variety of reasons, which include to:

• Cover short positions (where participants, for example, some hedge funds and market makers sell securities which they do not hold).

• Support derivatives activities (where participants may be subjected to an option exercise).

• Cover settlement fails (where participants do not have sufficient securities available to settle a delivery).

• Obtain securities that are acceptable as collateral.

Market participants lend securities for one purpose; that is, to earn fee income. This has two benefits:

• Fee income enhances the investment performance of the securities portfolio.

• As securities lending decreases the size of the portfolio, there is a corresponding reduction in safekeeping charges, however if the lender is not operating via a lending pool, which we will look at in a moment, they will be taking collateral against the lent securities and may incur custody charges in this respect

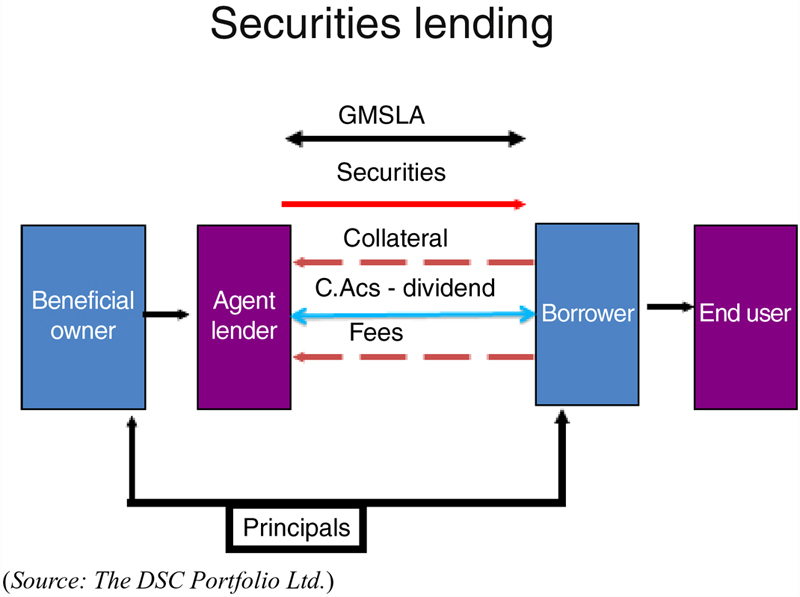

Prime brokers and global custodians (often linked) take advantage of securities lending and borrowing by acting as intermediaries or as a conduit in the process by managing the securities lending pool, which utilizes client’s assets that are available to lend by providing these securities to the clients wishing to borrow.

The global custodians benefit by:

• Retaining a share of the fee income while running a discretionary lending program (note a custodians client is not obliged to make their securities available for lending) for their client, and/or

• Charging a transaction fee for every movement across their client’s securities account where the custodian is unaware of the reasons for the securities movements, that is, they are not moving as part of the settlement of a transaction.

As a global custodian holds sizeable quantities of any particular issue, it is able to play an important role by providing liquidity to the market. Furthermore, lenders and borrowers benefit from increased operational reliability and reduced risk by utilizing the range of the global custodian’s services such as:

• Clearance

• Payment

• Settlement

• Pledging (of assets as collateral)

• Valuation (mark-to-market)

Securities lending precautions and controls

The Risks

The lender is primarily concerned with the safe return of his securities by the borrower and that there are adequate means of recompense in the event that the securities are not returned.

There are four situations each of which could place the lender at a disadvantage:

1. The most serious situation is where a borrower defaults with no chance of the lender retrieving the securities.

2. Timing differences between delivery of the loaned securities and the corresponding receipt of sufficient collateral.

3. The late/delayed return of securities due to settlement and securities liquidity problems experienced by the borrower.

4. Settlement inefficiencies or a systemic collapse within the local market itself.

Various countermeasures are taken in order to reduce the risk associated with each of the earlier mentioned situations.

Borrower default

Loans of securities are delivered by the lender on a “free of payment” basis to the borrower. For their part, the borrower covers the loan by delivering collateral to the lender.

It is of utmost importance that the collateral should be of such quality and quantity that it must be readily exchangeable into cash in the event that the borrower defaults. This enables the lender to be able to replace the missing securities by using the collateral proceeds to acquire the securities in the market.

To satisfy an adequate collateral requirement, the borrower must deliver collateral with a market value, which exceeds the market value of the loaned securities (the outstanding loans) by a predetermined margin; typically between 5% and 15%.

This margin allows for any variation in the value of the outstanding loans. The securities out on loan are “marked-to-market” (priced at the current market value) at least daily and intraday in volatile markets using the previous business day’s closing prices or the current market price. Any resulting shortfall in the amount of collateral is called from and made good by the borrower. Conversely, any excess collateral can be returned to the borrower.

Day-light exposure

Day-light exposure is the intraday settlement risk that loan securities may be delivered before the collateral is received. If the borrower should then default during the intervening period, the lender would be unsecured. The reverse is also true for a loan return.

For example, a lender who delivers securities to the borrower at 10:00 but does not receive the collateral until 15:00 has a day-light exposure of 5 h. There is a particular problem when the parties to a loan transaction and the domicile of the securities are all in different time zones. For example, lender in London, borrower in New York, securities in Tokyo.

Loan transaction for value Wednesday; securities delivered on Wednesday (Tokyo time zone).

Collateral due for delivery value Wednesday: collateral delivered Wednesday (New York time zone).

In the lender’s time zone, there is an exposure of at least 14 h, that is, from the time the securities are delivered (before close of business in Tokyo) to the receipt of collateral (after start of business in New York).

Settlement delays

Delays can be caused by the usual settlement failure types:

• Insufficient securities to satisfy the total delivery.

• Lender or borrower gives late or incorrect delivery/receipt instructions.

Market inefficiencies

Investors will always want to invest in countries where there are opportunities for capital gain and income growth and with scant attention to the efficient operation of the settlements systems.

Effective securities lending does however depend on the ability to deliver securities without delays and complications. For this reason, securities lending is only undertaken in the established markets with reliable and robust settlements.

Collateral

To satisfy the quality requirement, the following types of collateral are generally acceptable:

1. Cash

The lender places the cash out into the money markets and agrees to pay interest (a rebate) to the borrower at a rate lower than the market rate. The difference in rates reflects the lending fee payable to the lender.

Advantages of accepting cash as collateral:

• Acceptance of cash collateral allows the securities to move on a DVP basis and thus eliminates the risk that the securities delivery and collateral receipt do not occur simultaneously.

• Cash is regarded as the safest form of collateral in domestic markets including the United States of America where it is used in the majority of cases.

Disadvantages of accepting cash as collateral:

• Operational issues—many institutional lenders are not prepared or able to undertake the extra administrative burden of reinvesting the cash.

• The tax and regulatory situations in countries can make the use of cash impractical and or unattractive.

• There can be the added problems of foreign currencies, which require one or two days notice prior to placing funds.

• There is an exposure to adverse exchange rates when using foreign currencies.

Securities

Collateral in the form of other securities can be acceptable however there are issues that need to be considered.

The market value of the collateral must also be monitored and be easily realizable into cash in the event of borrower default.

Other commonly acceptable types of collateral used are:

Certificates of deposit

A popular security type used as collateral is a Certificate of Deposit. CDs are certificates, which give ownership of a deposit at a bank and for which there is an established market.

The advantages of using CDs as collateral:

• Considered to be of high quality and “near-cash” they are guaranteed by the banks on which they are drawn. The lender is able to specify the creditworthiness of the banks by only accepting paper with a rating of, say, “A” or better.

• CDs are straightforward to sell should the need arise.

The disadvantages of CDs as collateral:

• The nominal amount of CDs tends to be in shapes of £1,000,000 or $1,000,000 and this makes it difficult to ensure that the margined collateral value matches the value of outstanding loans.

• CDs have a limited lifespan and borrowers must ensure that CDs are substituted as old CDs mature.

Government bonds

High-quality securities such as government bonds of the G7 countries, which also benefit from high credit ratings and ease of sale are acceptable.

Equities

Equities are used but the issuer creditworthiness and the high-risk nature mainly volatility of the security type itself are not generally acceptable to lenders. In addition, as some equities can have longer settlement periods (T + 3 or more against T + 1 for say government bonds) can delay the time from borrower default to receipt of the collateral sale proceeds.

Irrevocable letters of credit (L/Cs)

A once popular method of providing collateral cover, L/Cs are nevertheless under threat as the cost of a L/C during the credit crunch and still today is making borrowing against them unprofitable.

Advantages of taking L/Cs as collateral:

• Lender does not need to reinvest or revalue the L/C.

• Day-light exposure is eliminated if receipt of a L/C is preadvised to the lender before the securities are released to the borrower.

• Face amount of L/C is more than adequate to cover the margined value of the outstanding loans and this results in less collateral movement to maintain the margin levels.

Disadvantages of taking L/Cs as collateral:

• Credit risk of bank that issued the L/C. (Lenders will limit the amount of L/Cs they will accept from one issuer.)

• (For the borrower) the high cost of obtaining a L/C from the bank.

Securities lending agreements

In order to protect the interests of the lending parties, the borrowing parties and when applicable the intermediaries, agreement forms are drawn up to clearly define the rights, duties, and liabilities of those concerned.

An agreement will contain references to, inter alia, the following topics:

• Interpretation definitions of the terms used in the agreement—Rights and title includes reference to the protection of lender’s entitlements.

• Collateral—Loans should be secured with collateral.

• Equivalent securities—Securities and collateral should be returned in an equivalent form to the original deliveries.

• Lenders’ and borrower’s warranties—Statement that both parties are permitted to undertake the lending/borrowing activities.

• Default—Remedies available in the event that one or other party defaults on its obligations.

• Arbitration and Jurisdiction—How and where disputes will be submitted for resolution and under which governing law.

Role of the prime brokers/global custodians

The extent to which the prime brokers/global custodian is involved in securities lending depends on the type of service offered. The global custodian typically operates a lending pool where the whole process of securities lending is managed by the custodian in return for taking a portion of the fee generated. For example, the custodian may receive 50 bps for lending the security but may only pay the owner of the loaned securities 30 bps.

However, some large lending institutions may decide to do direct lending in which case the custodian is only involved in moving assets.

Direct lending will suit the bigger institutions like large investment funds, pension funds etc., who are able to offer portfolios with large and varied holdings to potential borrowers.

They are therefore able to earn larger fees by going direct to the market rather than paying part of the fee earned to the custodian.

The key points are:

• The institution negotiates loan agreements and recalls/returns with the intermediaries or borrowers.

• The institution controls the movement of collateral and ensures that margins are maintained.

• The institution assumes the counterparty risk of the intermediary.

• The global custodian delivers and receives securities on a “free of payment” basis on instructions taken from the institution.

The risks for the institution are:

Investor assumes all risks associated with securities lending including:

• Intraday exposure—They must ensure that securities are not released until adequate margined securities are under their control (directly in-house or indirectly through a global custodian or settlement agent).

• Settlement risk—They must ensure that deliveries of securities for loans are made on time.

• Deliveries of securities “free of payment” demand a higher level of authorization and control than deliveries made on a DVP basis.

• The operations teams must be able to identify in sufficient time situations where securities on loan are required to settle a sale transaction and to initiate timely recalls.

• Market risk—They must ensure collateral is revalued more frequently in volatile markets.

• Legal risk—They are responsible for arranging and monitoring the legal arrangements of the loan, that is, stock-lending agreements, for example, the ISLA Global Master Securities Lending Agreement.

The rewards are:

• Fee income—They will receive the full amount of the fees.

• Exposure—They are able to choose the counterparties they lend to.

Nondiscretionary program

Nondiscretionary lending differs from direct lending insofar as the global custodian takes a more active role in the process.

The key points are:

• The custodian seeks approval from the client for each loan request.

• The custodian receives collateral from the borrowers and ensures that the margins/collateral are adequate.

• A fee is charged by the custodian for this service.

• The client assumes the risk of the borrowers.

The extra advantage for the client is:

• The custodian ensures that the collateral is matched to the movement of securities.

• The custodian is better placed to initiate timely loan recalls to cover the sales that their client might make.

The disadvantage is:

That the client’s relationship with the intermediaries might suffer now that they approach the custodian for loan requests and returns.

Discretionary (or managed) program

Discretionary programs tend to suit the small/medium-sized lenders whose individual holdings are not always large and varied enough to attract borrowers.

The stock lending is delegated entirely to the custodian in the following key ways:

• The custodian actively seeks to place securities out on loan with the intermediaries.

• The custodian takes collateral and monitors the margins.

• A portion of the risk of the borrower is transferred from the client to the custodian.

• Depending on the level of risk assumed by the custodian, anything from 50% to 60% of the fee income is retained by the custodian.

The advantages for the lender are:

• The service is totally linked into the custodian’s settlement systems thus ensuring that the risk of settlement failure through late recalls is almost eliminated.

• The investor benefits from being a part of substantially larger holdings in the “pool,” which may be more attractive to potential borrowers.

The disadvantages for the investor are:

• Depending on the method of loan allocation adopted by the custodian the investor’s assets may not be fully utilized.

• The investor receives only a portion of the fee income. However, as noted earlier this may be offset by reductions in transaction charges and safekeeping fees.

Operating the pool

There is an issue, which affects the ability of a lender to participate in securities lending on an equitable basis. This is the problem of ensuring that loans and fee income are allocated fairly across all participants in the pool. To manage this, the global custodians use sophisticated algorithms to allocate loans and fee accruals fairly.

Benefits and entitlements

As stated in the introduction, the lender loses legal ownership and voting rights of the securities but retains the benefits of ownership.

It is important to appreciate that the lender is treated as if he had not lent the securities; any shortfalls are made good by the borrower who, as is considered the “temporary legal owner” of the securities (in reality the securities will almost certainly have been used for settlement and are not with the borrower), will be considered to have received any benefits. It is the responsibility of the intermediary or global custodian to ensure that the lender is not disadvantaged through securities lending activities.

Any corporate action of a lent security can be an issue but certainly dividends or interest payments create a need for the borrower or intermediary to “make good” the lender.

Lenders’ rights

Lenders retain the right to participate in all dividends, interest payments, and other benefits on securities that are on loan. The one exception as mentioned earlier is that the lenders lose the right to vote.

Manufactured dividends

If securities are on loan over the record date, the issuing company will pay the dividend to the party at the end of the borrowing chain. The lender will therefore be paid an amount of cash in lieu of the actual dividend. In other words, the borrower manufactures a dividend payment in order to make the lender good.

The regulations and tax situation regarding loaned securities where there is a manufactured dividend created must be fully understood. If there is any likelihood of the lender being disadvantaged then the loan needs to be recalled in time for the lender to be on the company register by record date.

There may be issues related to the deduction of the withholding tax (WHT) applicable to the country of issue of the securities.

Role of the custodian or intermediary

The lending intermediary’s prime role is to ensure that the lender is “made whole” and this can be achieved in the following ways by:

• Gathering information on actions from numerous sources.

• Comparing information from one source with another to ensure consistency.

• Rearranging the information (including any translations) into a form from which the lender can make a decision.

• Ensuring that all expected instructions are received from the lenders.

• Giving accurate and timely instructions to the correct destination, that is, borrowers agent/custodian.

• Informing the lender of the successful management of the corporate action results.

The need for the intermediaries to receive the lender’s instructions in advance of the issuing company’s own deadlines can cause problems with the lender. The lender might wish to delay a decision until the last possible moment; sometimes past the intermediary’s deadline. Nevertheless the intermediary should, in this situation, attempt to comply with the instructions on a “best efforts” basis.

Importance of accuracy and timeliness

The intermediary is responsible for managing the corporate action event related to the lenders securities (as well as on any collateral held from the borrower).

The way in which the lender receives information depends very much on the nature of the event itself and the manner in which the lender chooses to hold the securities in safekeeping.

All corporate actions have deadlines, especially those which require a decision (the optional events). Unfortunately, differing worldwide standards do not make the task of monitoring corporate actions any easier. For this reason, it is important for the intermediaries and/or their agents to ensure that:

• The information received is accurate.

• Any instructions are given in the form and within the deadlines specified by the company.

Failure to settle situations such as market purchases and sales on time will result in delays and inconvenience. There might be occasions when penalty interest is payable and both counterparties will be exposed to an element of risk while the trade remains unsettled.

However, the obligation to settle the trades remains until such time as the delivery of securities (together with the underlying cash payment) takes place.

With an optional corporate action, however, failure to give and act upon accurate and timely instructions could result in a loss of entitlement to the benefit. The party involved will have to purchase securities (if securities were to be the benefit, for example, a rights issue) in the market and pay the extra costs.

Actions required

1.Voting rights

Lenders who wish to exercise their right to vote must arrange for the loans to be recalled in sufficient time to comply with local voting rules. These rules might call for the reregistration of the securities into the lender’s (or their appointed nominee’s) name or might necessitate the blocking of the shares until the Annual (or Extraordinary) General Meeting has taken place. Sufficient time should be allowed for this to happen.

2.Corporate actions

It is the responsibility of the borrower to ensure that the lender is made whole with respect to corporate actions. The borrower can either unwind the loan returning the securities to the lender or can take up any entitlements on behalf of the lender making any extra cash payments as and when required.

Implications for collateral

There are two points to note with respect to collateral:

The amount of collateral pledged may have to increase or decrease in order to maintain the required (margined) levels of cover. This applies equally to collateral that is taken in the form of cash or other securities (whether in the same currency or different currencies).

If other securities are used, there will be a time when corporate actions will affect the collateral itself. In this case, the collateral can either be substituted or treated in much the same way as the loaned securities.

Repurchase agreement (repo)

A repo is a purchase or sale of a security now, with an opposite transaction later. The first deal is a purchase or sale of a security for immediate settlement. The second deal is a reversal of the first deal. It is a temporary rather than permanent transfer of securities and cash.

The difference in cash value is the cost of borrowing the cash secured against the security (usually high quality bonds).

Securities lending relationship structure

The loan will be covered by an agreement such as the International Securities Lending Association Global Master Securities Lending Agreement (GMSLA).

Summary

A firm needing to borrow cash that has bonds available will use a repo whereas a fund needing to borrow securities will be involved in a stock or securities loan against either cash or security collateral.

Since the market crash and following subsequent regulatory reviews, there has been the introduction of more reporting of loans and particularly in connection with short selling by hedge funds.

There is some talk of securities lending being subject to reporting to trade repositories and lending is also included in the proposed Financial Transaction Tax.

As we have seen earlier in this part, a fund may be involved in derivative transactions, which generate margin calls. In addition hedge funds may trade on margin with the prime broker.

In both cases we know it is essential that the accounting team record this correctly in the accounts.

The custodian will be very much involved in the collateral process moving assets that will be collateral and receiving or delivering assets that have been lent and borrowed.

For derivatives we have the variation margin process, which if you recall may involve the payment or receipt of monies with the broker. This must be recorded in the variation margin ledger but also in the cash flow process and the forecast.

Compliance

In Part 2 of the book, we looked at the regulatory environment for funds and the role of the compliance officer is to ensure that the fund complies with external regulation and internal controls and policies.

We can summarize the compliance role in terms of the fund and the administrator/custodian as follows:

• Mandates, scheme particulars, and prospectus.

• Approved clients and antimoney laundering procedures.

• Valuations and pricing.

• Errors and corrections.

• Reporting to clients.

• Interaction with the prime broker.

• Interaction with clients.

• Formal and periodic reporting.

• Process for partial fills.

• Process for reevaluating original order.

• Order reentered or cancelled.

• Procedure for dealing overseas.

• Instructions to the brokers.

• Allocation across funds.

• Execution.

• Reporting completed fills.

• Exposure limits and restrictions.

• Asset allocation policy.

• Use of derivatives policy.

• Monitoring instruments used.

• Monitoring implementation of policy.

• Authorized personnel.

Some of these areas are related to the activity of the investment manager, some to the operational process of the fund and some to the regulatory requirements.

Now we can look at the areas the compliance officer of the administrator/custodian will be responsible for:

• Structure for administration operation.

• Creating the fund administration and service level agreements.

• Procedures and controls for fund set up services.

• Procedures for monitoring fund’s—broker agreements, trustees arrangements, marketing and sales policy.

• Establishing procedures for valuations and publishing prices, creation/redemption of shares, client transaction records.

• Fund transaction records.

• Funding records.

• Asset valuations.

• Distributions.

• Reports to manager.

• Reports to clients.

• Reports to regulator.

Again some of these areas will relate to the services being provided and some will be internal control issues.

In both cases, it is essential that the procedures are set out in the manual and that they are complied with. There must also be an adequate escalation process to senior management when breaches occur.

It must also be reiterated that while the administrator can assist the fund with compliance, the responsibility remains with the fund.

Summary

In this part of the book, we have looked at the operation of the fund and the roles and tasks the teams and parties like custodians and compliance play in the process.

The efficiency with which the teams carry out these tasks will impact on the overall performance of the fund and crucially in some areas the reputation of the fund.

In Part 4, we look at another very important issue for a fund and its support service suppliers and that is risk.