Appendix E

Solutions to the Exercises

Chapter 1

- 1.1

-

- (a) We have the stationary solution X t = ∑ i ≥ 00.5 i (η t − i + 1), with mean EX t = 2 and autocorrelations ρ X (h) = 0.5∣h∣ .

- (b) We have an ‘anticipative’ stationary solutionwhich is such that EX t = − 1 and ρ X (h) = 0.5∣h∣ .

- (c) The stationary solutionis such that EX t = 2 with ρ X (1) = 2/19 and ρ X (h) = 0.5 h − 1 ρ X (1) for h > 1.

- The compatible models are, respectively, ARMA(1, 2), MA(3) and ARMA(1, 1).

- The first noise is strong, and the second is weak because

Note that, by Jensen's inequality, this correlation is positive.

-

- 1.2 Without loss of generality, assume

for

t < 1 or

t > n

. We have

for

t < 1 or

t > n

. We have

which gives

, and the result follows.

, and the result follows. - 1.3 Consider the degenerate sequence (X

t

)

t = 0, 1, …

defined, on a probability space (Ω, 풜, ℙ), by

X

t

(ω) = (−1)

t

for all

ω ∈ Ω and all

t ≥ 0. With probability 1, the sequence {(−1)

t

} is the realisation of the process (X

t

). This process is non‐stationary because, for instance,

EX

0 ≠ EX

1

.

Let U be a random variable, uniformly distributed on {0, 1}. We define the process (Y t ) t = 0, 1, … by

for any ω ∈ Ω and any t ≥ 0. The process (Y t ) is stationary. We have in particular EY t = 0 and Cov(Y t , Y t + h ) = (−1) h . With probability 1/2, the realisation of the stationary process (Y t ) will be the sequence {(−1) t } (and with probability 1/2, it will be {(−1) t + 1}).

This example leads us to think that it is virtually impossible to determine whether a process is stationary or not, from the observation of only one trajectory, even of infinite length. However, practitioners do not consider {(−1) t } as a potential realisation of the stationary process (Y t ). It is more natural, and simpler, to suppose that {(−1) t } is generated by the non‐stationary process (X t ).

- 1.4 The sequence 0, 1, 0, 1, … is a realisation of the process

X

t

= 0.5(1 + (−1)

t

A), where

A

is a random variable such that

P[A = 1] = P[A = − 1] = 0.5. It can easily be seen that (X

t

) is strictly stationary.

Let Ω* = {ω ∣ X 2t = 1, X 2t + 1 = 0, ∀ t}. If (X t ) is ergodic and stationary, the empirical means

and

and  both converge to the same limit

P[X

t

= 1] with probability 1, by the ergodic theorem. For all

ω ∈ Ω*

these means are, respectively, equal to 1 and 0. Thus

P(Ω*) = 0. The probability of such a trajectory is thus equal to zero for any ergodic and stationary process.

both converge to the same limit

P[X

t

= 1] with probability 1, by the ergodic theorem. For all

ω ∈ Ω*

these means are, respectively, equal to 1 and 0. Thus

P(Ω*) = 0. The probability of such a trajectory is thus equal to zero for any ergodic and stationary process. - 1.5 We have

Eε

t

= 0, Var ε

t

= 1, and Cov(ε

t

, ε

t − h

) = 0 when

h ≠ 0, thus (ε

t

) is a weak white noise. We also have

, thus ε

t

and ε

t − 1

are not independent, which shows that (ε

t

) is not a strong white noise.

, thus ε

t

and ε

t − 1

are not independent, which shows that (ε

t

) is not a strong white noise.

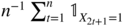

- 1.6 Assume

h > 0. Define the random variable

where

where  . It is easy to see that

. It is easy to see that  has the same asymptotic variance (and also the same asymptotic distribution) as

has the same asymptotic variance (and also the same asymptotic distribution) as  . Using

. Using  , stationarity, and Lebesgue's theorem, this asymptotic variance is equal to

, stationarity, and Lebesgue's theorem, this asymptotic variance is equal to

This value can be arbitrarily larger than 1, which is the value of the asymptotic variance of the empirical autocorrelations of a strong white noise.

- 1.7 It is clear that

is a second‐order stationary process. By construction, ε

t

and ε

t − h

are independent when

h > k

, thus

is a second‐order stationary process. By construction, ε

t

and ε

t − h

are independent when

h > k

, thus  for all

h > k

. Moreover,

for all

h > k

. Moreover,  , for

h = 0, …, k

. In view of Theorem 1.2,

, for

h = 0, …, k

. In view of Theorem 1.2,  thus follows an MA(k) process. In the case

k = 1, we have

thus follows an MA(k) process. In the case

k = 1, we have

where ∣b∣ < 1 and (u t ) is a white noise of variance σ 2 . The coefficients b and σ 2 are determined by

which gives

and

σ

2 = 2/b

.

and

σ

2 = 2/b

. - 1.8 Reasoning as in Exercise 1.6, the asymptotic variance is equal to

Since

, for

k ≠ h

the asymptotic variance can be arbitrarily smaller than 1, which corresponds to the asymptotic variance of the empirical autocorrelations of a strong white noise.

, for

k ≠ h

the asymptotic variance can be arbitrarily smaller than 1, which corresponds to the asymptotic variance of the empirical autocorrelations of a strong white noise. - 1.9

- We havewhen n > m and m → ∞. The sequence {u t (n)} n defined by

is a Cauchy sequence in

L

2

, and thus converges in quadratic mean. A priori,

is a Cauchy sequence in

L

2

, and thus converges in quadratic mean. A priori,

exists in ℝ ∪ + {∞}. Using Beppo Levi's theorem,

which shows that the limit

is finite almost surely. Thus, as

n → ∞,

u

t

(n) converges, both almost surely and in quadratic mean, to

is finite almost surely. Thus, as

n → ∞,

u

t

(n) converges, both almost surely and in quadratic mean, to  . Since

. Since

we obtain, taking the limit as n → ∞ of both sides of the equality, u t = au t − 1 + η t . This shows that (X t ) = (u t ) is a stationary solution of the AR(1) equation.

Finally, assume the existence of two stationary solutions to the equation X t = aX t − 1 + η t and u t = au t − 1 + η t . If

, then

, then

which entails

This is in contradiction to the assumption that the two sequences are stationary, which shows the uniqueness of the stationary solution.

- We have

X

t

= η

t

+ aη

t − 1 + ⋯ + a

k

η

t − k

+ a

k + 1

X

t − k − 1

. Since ∣a ∣ = 1,

as k → ∞. If (X t ) were stationary,

and we would have

This is impossible, because by the Cauchy–Schwarz inequality,

- The argument used in Part 1 shows thatalmost surely and in quadratic mean. Since

for all n , (

for all n , (

) is a stationary solution (which is called anticipative, because it is a function of the future values of the noise) of the AR(1) equation. The uniqueness of the stationary solution is shown as in Part 1.

) is a stationary solution (which is called anticipative, because it is a function of the future values of the noise) of the AR(1) equation. The uniqueness of the stationary solution is shown as in Part 1. - The autocovariance function of the stationary solution is

We thus have Eε t = 0 and, for all h > 0,

which confirms that ε t is a white noise.

- We have

- 1.10 In Figure 1.6a, we note that several empirical autocorrelations are outside the 95% significance band, which leads us to think that the series may not be the realisation of a strong white noise. Inspection of Figure 1.6b confirms that the observed series ε1, …, ε

n

cannot be generated by a strong white noise; otherwise, the series

would also be uncorrelated. Clearly, this is not the case, because several empirical autocorrelations go far beyond the significance band. By contrast, it is plausible that the series is a weak noise. We know that Bartlett's formula giving the limits

would also be uncorrelated. Clearly, this is not the case, because several empirical autocorrelations go far beyond the significance band. By contrast, it is plausible that the series is a weak noise. We know that Bartlett's formula giving the limits  is not valid for a weak noise (see Exercises 1.6 and 1.8). On the other hand, we know that the square of a weak noise can be correlated (see Exercise 1.7).

is not valid for a weak noise (see Exercises 1.6 and 1.8). On the other hand, we know that the square of a weak noise can be correlated (see Exercise 1.7).

- 1.11 Using the relation

, formula (B.18) can be written as

, formula (B.18) can be written as

With the change of index h = i − ℓ, we obtain

which gives (B.14), using the parity of the autocovariance functions.

- 1.12 We can assume

i ≥ 0 and

j ≥ 0. Since

γ

X

(ℓ) = γ

ε(ℓ) = 0 for all ℓ ≠ 0, formula (B.18) yields

for (i, j) ≠ (0, 0) and

Thus

In formula (B.15), we have

ij

= 0 when

i ≠ j

and

ij

= 0 when

i ≠ j

and  ii

= 1. We also have

ii

= 1. We also have  when

i ≠ j

and

when

i ≠ j

and  for all

i ≠ 0. Since

for all

i ≠ 0. Since  , we obtain

, we obtain

For significance intervals C h of asymptotic level 1 − α , such that

, we have

, we have

By definition of C h ,

Moreover,

We have used the convergence in law of

to a vector of independent variables. When the observed process is not a noise, this asymptotic independence does not hold in general.

to a vector of independent variables. When the observed process is not a noise, this asymptotic independence does not hold in general. - 1.13 The probability that all the empirical autocorrelations stay within the asymptotic significance intervals (with the notation of the solution to Exercise 1.12) is, by the asymptotic independence,

For m = 20 and α = 5%, this limit is equal to 0.36. The probability of not rejecting the right model is thus low.

- 1.14 In view of (B.7), we have

r

X

(1) = ρ

X

(1). Using step (B.8) with

k = 2 and

a

1, 1 = ρ

X

(1), we obtain

Then, step (B.9) yields

Finally, step (B.8) yields

- 1.15 The historical data from 3 January 1950 to 24 July 2009 can be downloaded via the URL: http://fr.finance.yahoo.com/q/hp?s = %5EGSPC. We obtain Figure E.1 with the following R code:

> # reading the SP500 data set> sp500data <- read.table("sp500.csv",header=TRUE,sep=",")> sp500<-rev(sp500data$Close) # closing price> n<-length(sp500)> rend<-log(sp500[2:n]/sp500[1:(n-1)]); rend2<-rend∧2> op <- par(mfrow = c(2, 2)) # 2 × 2 figures per page> plot(ts(sp500),main="SP 500 from 1/3/50 to 7/24/09",+ ylab="SP500 Prices",xlab="")> plot(ts(rend),main="SP500 Returns",ylab="SP500 Returns",+ xlab="")> acf(rend, main="Autocorrelations of the returns",xlab="",+ ylim=c(-0.05,0.2))> acf(rend2, main="ACF of the squared returns",xlab="",+ ylim=c(-0.05,0.2))> par(op)

Figure E.1 Closing prices and returns of the S&P 500 index from 3 January 1950 to 24 July 2009.

Chapter 2

- 2.1 This covariance is meaningful only if

and

Ef 2(ε

t − h

) < ∞. Under these assumptions, the equality is true and follows from

E(ε

t

∣ ε

u

, u < t) = 0.

and

Ef 2(ε

t − h

) < ∞. Under these assumptions, the equality is true and follows from

E(ε

t

∣ ε

u

, u < t) = 0.

- 2.2 In case (i) the strict stationarity condition becomes

α + β < 1. In case (ii) elementary integral computations show that the condition is

- 2.3 Let

λ

1, …, λ

m

be the eigenvalues of

A

. If

A

is diagonalisable, there exists an invertible matrix

P

and a diagonal matrix

D

such that

A = P

−1

DP

. It follows that, taking a multiplicative norm,

For the multiplicative norm ‖A‖ = ∑ ∣ a ij ∣, we have

The result follows immediately.

The result follows immediately.When A is any square matrix, the Jordan representation can be used. Let n i be the multiplicity of the eigenvalue λ i . We have the Jordan canonical form A = P −1 JP , where P is invertible, and J is the block‐diagonal matrix with a diagonal of m matrices J i (λ i ), of size n i × n i , with λ i on the diagonal, 1 on the superdiagonal, and 0 elsewhere. It follows that A t = P −1 J t P , where J t is the block‐diagonal matrix whose blocks are the matrices

. We have

. We have  , where

N

i

is such that

, where

N

i

is such that  . It can be assumed that ∣λ

1 ∣ > ∣ λ

2 ∣ > ⋯ > ∣ λ

m

∣ . It follows that

. It can be assumed that ∣λ

1 ∣ > ∣ λ

2 ∣ > ⋯ > ∣ λ

m

∣ . It follows that

as t → ∞, and the proof easily follows.

- 2.4 We use the multiplicative norm ‖A‖ = ∑ ∣ a

ij

∣. Thus log‖Az

t

‖ ≤ log ‖A‖ + log ‖z

t

‖; therefore, log+‖Az

t

‖ ≤ log+ ‖A‖ + log+ ∣ z

t

∣, which admits a finite expectation by assumption. It follows that

γ

exists. We have

and thus

Using Eq. (2.21) and the ergodic theorem, we obtain

Consequently, γ < 0 if and only if ρ(A) < exp(−E log ∣ z t ∣).

- 2.5 To show 1, first note that, by stationarity, we have

. The replacement can thus be done in (2.22). To show that it can also be done in (2.23), let us apply Theorem 2.3 to the sequence

. The replacement can thus be done in (2.22). To show that it can also be done in (2.23), let us apply Theorem 2.3 to the sequence  defined by

defined by  . Noting that

. Noting that  , we have

, we have

which completes the proof of 1.

We have shown that, for any

, the stationary sequences

, the stationary sequences  and

and  have the same top Lyapunov exponent, i.e.

have the same top Lyapunov exponent, i.e.

The convergence follows by showing that

.

. - 2.5 For the Euclidean norm, multiplicativity follows from the Cauchy–Schwarz inequality. Since

, we have

, we have

To show that the norm N 1 is not multiplicative, consider the matrix A whose elements are all equal to 1: we then have N 1(A) = 1 but N 1(A 2) > 1.

- 2.6 We have

and

- 2.7 We have

, therefore, under the condition

α

1 + α

2 < 1, the moment of order 2 is given by

, therefore, under the condition

α

1 + α

2 < 1, the moment of order 2 is given by

(see Theorem 2.5 and Remark 2.6(1)). The strictly stationary solution satisfies

in ℝ ∪ {+∞}. Moreover,

which gives

Using this relation in the previous expression for

, we obtain

, we obtain

If

, then the term in brackets on the left‐hand side of the equality must be strictly positive, which gives the condition for the existence of the fourth‐order moment. Note that the condition is not symmetric in

α

1

and

α

2

. In Figure E.2, the points (α

1, α

2) under the curve correspond to ARCH(2) models with a fourth‐order moment. For these models,

, then the term in brackets on the left‐hand side of the equality must be strictly positive, which gives the condition for the existence of the fourth‐order moment. Note that the condition is not symmetric in

α

1

and

α

2

. In Figure E.2, the points (α

1, α

2) under the curve correspond to ARCH(2) models with a fourth‐order moment. For these models,

Figure E.2 Region of existence of the fourth‐order moment for an ARCH(2) model (when μ 4 = 3).

- 2.8 We have seen that

admits the ARMA(1, 1) representation

admits the ARMA(1, 1) representation

where

is a (weak) white noise. The author correlation of

is a (weak) white noise. The author correlation of  thus satisfiesE.1

thus satisfiesE.1

Using the MA(∞) representation

we obtain

and

It follows that the lag 1 autocorrelation is

The other autocorrelations are obtained from (E.1) and

. To determine the autocovariances, all that remains is to compute

. To determine the autocovariances, all that remains is to compute

which is given by

- 2.9 The vectorial representation

is

is

We have

The eigenvalues of A (2) are 0, 0, 0 and 3α 2 + 2αβ + β 2 , thus I 4 − A (2) is invertible (0 is an eigenvalue of I 4 − A (2) if and only if 1 is an eigenvalue of A (2) ), and the system (2.63) admits a unique solution. We have

The solution to Eq. (2.63) is

As first component of this vector, we recognise

, and the other three components are equal to

, and the other three components are equal to  . Equation (2.64) yields

. Equation (2.64) yields

which gives

, but with tedious computations, compared to the direct method utilised in Exercise 2.8.

, but with tedious computations, compared to the direct method utilised in Exercise 2.8. - 2.10 It suffices to show that

for all fixed

for all fixed  . Let

. Let  and

and  for

for  . For all

. For all  , write

, write  with

with  . We have

. We have

and the result follows.

- 2.10

- Subtracting the (

q + 1)th line of (λI

p + q

− A) from the first, then expanding the determinant along the first row, and using Eq. (2.32), we obtainand the result follows.

- When

the previous determinant is equal to zero at

λ = 1. Thus

ρ(A) ≥ 1. Now, let

λ

be a complex number of modulus strictly greater than 1. Using the inequality ∣a − b ∣ ≥ ∣ a ∣ − ∣ b∣, we then obtainIt follows that ρ(A) ≤ 1 and thus ρ(A) = 1.

the previous determinant is equal to zero at

λ = 1. Thus

ρ(A) ≥ 1. Now, let

λ

be a complex number of modulus strictly greater than 1. Using the inequality ∣a − b ∣ ≥ ∣ a ∣ − ∣ b∣, we then obtainIt follows that ρ(A) ≤ 1 and thus ρ(A) = 1.

- Subtracting the (

q + 1)th line of (λI

p + q

− A) from the first, then expanding the determinant along the first row, and using Eq. (2.32), we obtain

- 2.11 For all ε > 0, noting that the function

f(t) = P(t

−1 ∣ X

1 ∣ > ε) is decreasing, we have

The convergence follows from the Borel–Cantelli lemma.

Now, let (X n ) be an iid sequence of random variables with density f(x) = x −2

x ≥ 1

. For all

K > 0, we have

x ≥ 1

. For all

K > 0, we have

The events {n −1 X n > K} being independent, we can use the counterpart of the Borel–Cantelli lemma: the event {n −1 X n > K for an infinite number of n} has probability 1. Thus, with probability 1, the sequence (n −1 X n ) does not tend to 0.

- 2.12 First note that the last

r − 1 lines of

B

t

A

are the first

r − 1 lines of

A

, for any matrix

A

of appropriate size. The same property holds true when

B

t

is replaced by

E(B

t

). It follows that the last

r − 1 lines of

E(B

t

A) are the last

r − 1 lines of

E(B

t

)E(A). Moreover, it can be shown, by induction on

t

, that the

i

th line ℓ

i, t − i

of

B

t

…B

1

is a measurable function of the

η

t − j

, for

j ≥ i

. The first line of

B

t + 1

B

t

…B

1

is thus of the form

a

1(η

t

)ℓ1, t − 1 + ⋯ + a

r

(η

t − r

)ℓ

r, t − r

. Since

the first line of EB t + 1 B t …B 1 is thus the product of the first line of EB t + 1 and of EB t …B 1 . The conclusion follows.

- 2.13

- For any fixed

t

, the sequence

converges almost surely (to

converges almost surely (to  ) as

K → ∞. Thusand the first convergence follows. Now note that we have

) as

K → ∞. Thusand the first convergence follows. Now note that we have

The first inequality uses (a + b) s ≤ a s + b s for a, b ≥ 0 and s ∈ (0, 1]. The second inequality is a consequence of

. The second convergence then follows from the dominated convergence theorem.

. The second convergence then follows from the dominated convergence theorem. - We have

. The convergence follows from the previous question, and from the strict stationarity, for any fixed integer

K

, of the sequence

. The convergence follows from the previous question, and from the strict stationarity, for any fixed integer

K

, of the sequence  .

. - We have

for any i ′ = 1, …, ℓ, j ′ = 1, …, m . In view of the independence between X n and Y , it follows that

almost surely as

n → ∞. Since

almost surely as

n → ∞. Since  is a strictly positive number, we obtain

is a strictly positive number, we obtain  almost surely, for all

i

′, j

′

. Using (a + b)

s

≤ a

s

+ b

s

once again, it follows that

almost surely, for all

i

′, j

′

. Using (a + b)

s

≤ a

s

+ b

s

once again, it follows that

- Note that the previous question does not allow us to affirm that the convergence to 0 of

entails that of

E(‖A

k

A

k − 1…A

1‖

s

), because

entails that of

E(‖A

k

A

k − 1…A

1‖

s

), because  has zero components. For

k

large enough, however, we have

has zero components. For

k

large enough, however, we have

where

is independent of

A

k

A

k − 1…A

N + 1. The general term

a

i, j

of

A

N

…A

1

is the (i, j)th term of the matrix

A

N

multiplied by a product of

is independent of

A

k

A

k − 1…A

N + 1. The general term

a

i, j

of

A

N

…A

1

is the (i, j)th term of the matrix

A

N

multiplied by a product of  variables. The assumption

A

N

> 0 entails

a

i, j

> 0 almost surely for all

i

and

j

. It follows that the

i

th component of

Y

satisfies

Y

i

> 0 almost surely for all

i

. Thus

variables. The assumption

A

N

> 0 entails

a

i, j

> 0 almost surely for all

i

and

j

. It follows that the

i

th component of

Y

satisfies

Y

i

> 0 almost surely for all

i

. Thus  . Now the previous question allows to affirm that

E(‖A

k

A

k − 1…A

N + 1‖

s

) → 0 and, by strict stationarity, that

E(‖A

k − N

A

k − N − 1…A

1‖

s

) → 0 as

k → ∞. It follows that there exists

k

0

such that

. Now the previous question allows to affirm that

E(‖A

k

A

k − 1…A

N + 1‖

s

) → 0 and, by strict stationarity, that

E(‖A

k − N

A

k − N − 1…A

1‖

s

) → 0 as

k → ∞. It follows that there exists

k

0

such that

- If

α

1

or

β

1

is strictly positive, the elements of the first two lines of the vector

are also strictly positive, together with those of the (

q + 1)th and (

q + 2)th lines. By induction, it can be shown that

are also strictly positive, together with those of the (

q + 1)th and (

q + 2)th lines. By induction, it can be shown that  under this assumption.

under this assumption. - The condition

can be satisfied when

α

1 = β

1 = 0. It suffices to consider an ARCH(3) process with

α

1 = 0, α

2 > 0, α

3 > 0, and to check that

can be satisfied when

α

1 = β

1 = 0. It suffices to consider an ARCH(3) process with

α

1 = 0, α

2 > 0, α

3 > 0, and to check that  .

.

- For any fixed

t

, the sequence

- 2.14 In the case

p = 1, the condition on the roots of 1 − β

1

z

implies ∣β ∣ < 1. The positivity conditions on the

φ

i

yield

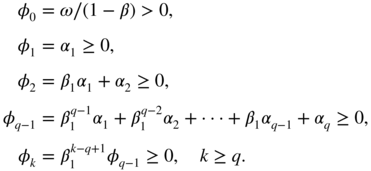

The last inequalities imply β 1 ≥ 0. Finally, the positivity constraints are

If q = 2, these constraints reduce to

Thus, we can have α 2 < 0.

- 2.15 Using the ARCH(

q

) representation of the process (

), together with Proposition 2.2, we obtain

), together with Proposition 2.2, we obtain

- 2.16 Since

,

h > 0, we have

,

h > 0, we have  where

λ, μ

are constants and

r

1, r

2

satisfy

r

1 + r

2 = α

1

,

r

1

r

2 = − α

2

. It can be assumed that

r

2 < 0 and

r

1 > 0, for instance. A simple computation shows that, for all

h ≥ 0,

where

λ, μ

are constants and

r

1, r

2

satisfy

r

1 + r

2 = α

1

,

r

1

r

2 = − α

2

. It can be assumed that

r

2 < 0 and

r

1 > 0, for instance. A simple computation shows that, for all

h ≥ 0,

If the last equality is true, it remains true when h is replaced by h + 1 because

. Since

. Since  , it follows that

, it follows that  for all

h ≥ 0. Moreover,

for all

h ≥ 0. Moreover,

Since

, if

, if  then we have, for all

h ≥ 1,

then we have, for all

h ≥ 1,  We have thus shown that the sequence

We have thus shown that the sequence  is decreasing when

is decreasing when  . If

. If  , it can be seen that for

h

large enough, say

h ≥ h

0

, we have

, it can be seen that for

h

large enough, say

h ≥ h

0

, we have  , again because of

, again because of  . Thus, the sequence

. Thus, the sequence  is decreasing.

is decreasing. - 2.17 Since

X

n

+ Y

n

→ − ∞ in probability, for all

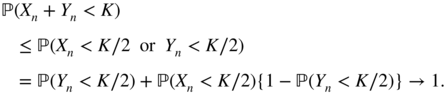

K

we have

Since

in probability, there exist

K

0 ∈ ℝ and

n

0 ∈ ℕ such that

P(X

n

< K

0/2) ≤ ς < 1 for all

n ≥ n

0

. Consequently,

in probability, there exist

K

0 ∈ ℝ and

n

0 ∈ ℕ such that

P(X

n

< K

0/2) ≤ ς < 1 for all

n ≥ n

0

. Consequently,

as n → ∞, for all K ≤ K 0 , which entails the result.

- 2.18 We have

as n → ∞. If γ < 0, the Cauchy rule entails that

converges almost surely, and the process (ε t ), defined by

, is a strictly stationary solution of model (2.7). As in the proof of Theorem 2.1, it can be shown that this solution is unique, non‐anticipative and ergodic. The converse is proved by contradiction, assuming that there exists a strictly stationary solution

, is a strictly stationary solution of model (2.7). As in the proof of Theorem 2.1, it can be shown that this solution is unique, non‐anticipative and ergodic. The converse is proved by contradiction, assuming that there exists a strictly stationary solution  . For all

n > 0, we have

. For all

n > 0, we have

It follows that a(η −1)…a(η −n )ω(η −n − 1) converges to zero, almost surely, as n → ∞ , or, equivalently, that

E.2

We first assume that E log {a(η t )} > 0. Then the strong law of large numbers entails

almost surely. For (E.2) to hold true, it is then necessary that log ω(η

−n − 1) → − ∞ almost surely, which is precluded since (η

t

) is iid and

ω(η

0) > 0 almost surely. Assume now that

E log {a(η

t

)} = 0. By the Chung–Fuchs theorem, we have

almost surely. For (E.2) to hold true, it is then necessary that log ω(η

−n − 1) → − ∞ almost surely, which is precluded since (η

t

) is iid and

ω(η

0) > 0 almost surely. Assume now that

E log {a(η

t

)} = 0. By the Chung–Fuchs theorem, we have  with probability 1 and, using Exercise 2.17, the convergence (E.2) entails log ω(η

−n − 1) → − ∞ in probability, which, as in the previous case, entails a contradiction.

with probability 1 and, using Exercise 2.17, the convergence (E.2) entails log ω(η

−n − 1) → − ∞ in probability, which, as in the previous case, entails a contradiction. - 2.19 Letting

a(z) = λ + (1 − λ)z

2

, we have

Regardless of the value of

, fixed or even random, we have almost surely

, fixed or even random, we have almost surely

using the law of large numbers and Jensen's inequality. It follows that

almost surely as

t → ∞.

almost surely as

t → ∞. - 2.20

- Since the φ i are positive and A 1 = 1, we have φ i ≤ 1, which shows the first inequality. The second inequality follows by convexity of x ↦ x log x for x > 0.

- Since

A

1 = 1 and

A

p

< ∞, the function

f

is well defined for

q ∈ [p, 1]. We haveThe function q ↦ log E|η 0|2q is convex on [p,1] if, for all λ ∈ [0, 1] and all q, q * ∈ [p, 1],

which is equivalent to showing that

with X = |η 0|2q ,

. This inequality holds true by Hölder's inequality. The same argument is used to show the convexity of

. This inequality holds true by Hölder's inequality. The same argument is used to show the convexity of  . It follows that

f

is convex, as a sum of convex functions. We have

f(1) = 0 and

f(p) < 0, thus the left derivative of

f

at 1 is negative, which gives the result.

. It follows that

f

is convex, as a sum of convex functions. We have

f(1) = 0 and

f(p) < 0, thus the left derivative of

f

at 1 is negative, which gives the result. - Conversely, we assume that there exists

p

* ∈ (0, 1] such that

and that condition (2.52) is satisfied. The convexity of

f

on [p

*, 1] and (2.52) implies that

f(q) < 0 for

q

sufficiently close to 1. Thus condition (2.41) is satisfied. By convexity of

f

and since

f(1) = 0, we have

f(q) < 0 for all

q ∈ [p, 1]. It follows that, by Theorem 2.6,

E|ε

t

|

q

< ∞ for all

q ∈ [0, 2].

and that condition (2.52) is satisfied. The convexity of

f

on [p

*, 1] and (2.52) implies that

f(q) < 0 for

q

sufficiently close to 1. Thus condition (2.41) is satisfied. By convexity of

f

and since

f(1) = 0, we have

f(q) < 0 for all

q ∈ [p, 1]. It follows that, by Theorem 2.6,

E|ε

t

|

q

< ∞ for all

q ∈ [0, 2].

- 2.21 Since

, we have

a = 0 and

b = 1. Using condition (2.60), we can easily see that

, we have

a = 0 and

b = 1. Using condition (2.60), we can easily see that

since the condition for the existence of

is

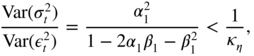

is  . Note that when the GARCH effect is weak (that is,

α

1

is small), the part of the variance that is explained by this regression is small, which is not surprising. In all cases, the ratio of the variances is bounded by 1/κ

η

, which is largely less than 1 for most distributions (1/3 for the Gaussian distribution). Thus, it is not surprising to observe disappointing

R

2

values when estimating such a regression on real series.

. Note that when the GARCH effect is weak (that is,

α

1

is small), the part of the variance that is explained by this regression is small, which is not surprising. In all cases, the ratio of the variances is bounded by 1/κ

η

, which is largely less than 1 for most distributions (1/3 for the Gaussian distribution). Thus, it is not surprising to observe disappointing

R

2

values when estimating such a regression on real series.

Chapter 3

- 3.1

Given any initial measure, the sequence (X

t

)

t ∈ ℕ

clearly constitutes a Markov chain on (ℝ, ℬ(ℝ)), with transition probabilities defined by

P(x, B) = ℙ(X

1 ∈ B ∣ X

0 = x) = P

ε

(B − θx).

- (a) Since

P

ε

admits a positive density on ℝ, the probability measure

P(x, .) is, for all

x ∈ E

, absolutely continuous with respect to

λ

and its density is positive on ℝ. Thus any measure

ϕ

which is absolutely continuous with respect to

λ

is a measure of irreducibility: ∀x ∈ E

,

Moreover, λ is a maximal measure of irreducibility.

- (b) Assume, for example, that ε t is uniformly distributed on [−1, 1]. If θ > 1 and X 0 = x 0 > 1/(θ − 1), we have x 0 < X 1 < X 2 < …, regardless of the ε t . Thus there exists no irreducibility measure: such a measure should satisfy ϕ([ − ∞ , x]) = 0, for all x ∈ ℝ, which would imply ϕ = 0.

- (a) Since

P

ε

admits a positive density on ℝ, the probability measure

P(x, .) is, for all

x ∈ E

, absolutely continuous with respect to

λ

and its density is positive on ℝ. Thus any measure

ϕ

which is absolutely continuous with respect to

λ

is a measure of irreducibility: ∀x ∈ E

,

- 3.2 If (X

n

) is strictly stationary,

X

1

and

X

0

have the same distribution,

μ

, satisfying

Thus μ is an invariant probability measure.

Conversely, suppose that μ is invariant. Using the Chapman–Kolmogorov relation, by which ∀t ∈ ℕ, ∀ s, 0 ≤ s ≤ t, ∀ x ∈ E, ∀ B ∈ ℰ,

we obtain

Thus, by induction, for all t , ℙ[X t ∈ B] = μ(B) (∀B ∈ ℬ ). Using the Markov property, this is equivalent to the strict stationarity of the chain: the distribution of the process (X t , X t + 1, …, X t + k ) is independent of t , for any integer k .

- 3.3 We have

Thus π is invariant. The third equality is an immediate consequence of the Fubini and Lebesgue theorems.

- 3.4 Assume, for instance,

θ > 0. Let

C = [−c, c],

c > 0, and let

δ = inf {f(x); x ∈ [−(1 + θ)c, (1 + θ)c]} We have, for all

A ⊂ C

and all

x ∈ C

,

Now let B ∈ ℰ . Then for all x ∈ C ,

The measure ν is non‐trivial since ν(E) = δλ(C) = 2δc > 0.

- 3.5 It is clear that (X

t

) constitutes a Feller chain on ℝ. The

λ

‐irreducibility follows from the assumption that the noise has a density which is everywhere positive, as in Exercise 3.1. In order to apply Theorem 3.1, a natural choice of the test function is

V(x) = 1 + ∣ x∣. We have

Thus if K 1 < 1, we have, for K 1 < K < 1 and for g(x) > (K 2 + 1 − K 1)/(K − K 1),

If we put A = {x; g(x) = 1 + ∣ x ∣ ≤ (K 2 + 1 − K 1)/(K − K 1)}, the set A is compact and the conditions of Theorem 3.1 are satisfied, with 1 − δ = K .

- 3.6 By summing the first

n

inequalities of (3.11) we obtain

It follows that

because V ≥ 1. Thus, there exists κ > 0 such that

Note that the positivity of δ is crucial for the conclusion.

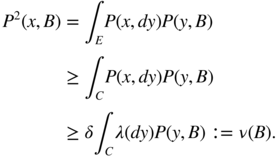

- 3.7 We have, for any positive continuous function

f

with compact support,

The inequality is justified by (i) and the fact that P f is a continuous positive function. It follows that for f =

C

, where

C

is a compact set, we obtain

C

, where

C

is a compact set, we obtain

which shows that,

(that is, π is subvarient) using (ii). If there existed B such that the previous inequality were strict, we should have

and since π(E) < ∞ we arrive at a contradiction. Thus

which signifies that π is invariant.

- 3.8 See Francq and Zakoïan (2006b).

- 3.9 If

were infinite then, for any

K > 0, there would exist a subscript

n

0

such that

were infinite then, for any

K > 0, there would exist a subscript

n

0

such that  . Then, using the decrease in the sequence, one would have

. Then, using the decrease in the sequence, one would have  . Since this should be true for all

K > 0, the sequence would not converge. This applies directly to the proof of Corollary A.3 with

u

n

= {α

X

(n)}

ν/(2 + ν)

, which is indeed a decreasing sequence in view of point (v) on Section A.3.1.

. Since this should be true for all

K > 0, the sequence would not converge. This applies directly to the proof of Corollary A.3 with

u

n

= {α

X

(n)}

ν/(2 + ν)

, which is indeed a decreasing sequence in view of point (v) on Section A.3.1.

- 3.10 We have

where

Inequality (A.8) shows that d 7 is bounded by

By an argument used to deal with d 6 , we obtain

and the conclusion follows.

- 3.11 The chain satisfies the Feller condition (i) because

is continuous at x when g is continuous.

To show that the irreducibility condition (ii) is not satisfied, consider the set of numbers in [0,1] such that the sequence of decimals is periodic after a certain lag:

For all h ≥ 0,

if and only if

if and only if  . We thus have,

. We thus have,

and,

This shows that there is no non‐trivial irreducibility measure.

The drift condition (iii) is satisfied with, for instance, a measure φ such that φ([−1, 1]) > 0, the energy V(x) = 1 + ∣ x∣ and the compact set A = [−1, 1]. Indeed,

provided

Chapter 4

- 4.1

Note that

is a measurable function of

is a measurable function of  and of

and of  , that will be denoted by

, that will be denoted by

Using the independence between

and the other variables of

and the other variables of  , we have, for all

, we have, for all  ,

,

when the distribution

is symmetric.

is symmetric. - 4.2 A sequence

of independent real random variables such that

of independent real random variables such that  with probability

with probability  and

and  with probability

with probability  is suitable, because

is suitable, because  ,

,  ,

,  and

and  . We have used

. We have used  for any decreasing sequence of events, in order to show that

for any decreasing sequence of events, in order to show that

- 4.3 By definition,

and, by continuity of the exponential,

is finite if and only if the series of general term

converges. Using the inequalities

converges. Using the inequalities  , we obtain

, we obtain

Since the

tend to 0 at an exponential rate and

tend to 0 at an exponential rate and  , the series of general term

, the series of general term  converges absolutely, and we finally obtain

converges absolutely, and we finally obtain

which is finite under condition (4.12).

- 4.4 Note that (4.13) entails that

with probability 1. The integral of a positive measurable function being always defined in

, using Beppo Levi's theorem and then the independence of the

, using Beppo Levi's theorem and then the independence of the  , we obtain

, we obtain

which is of course finite under condition (4.12). Applying the dominated convergence theorem, and bounding the variables

by the integrable variable

by the integrable variable  , we then obtain the desired expression for

, we then obtain the desired expression for  .

. - 4.5 Denoting by

the density of

the density of  ,

,

and

. With the notation

. With the notation  , it follows that

, it follows that

It then suffices to use the fact that

is equivalent to

is equivalent to  , and that

, and that  is thus equivalent to

is thus equivalent to  , in a neighborhood of 0.

, in a neighborhood of 0. - 4.6 We can always assume

. In view of the discussion on pages 79–80, the process

. In view of the discussion on pages 79–80, the process  satisfies an ARMA

satisfies an ARMA representation of the form

representation of the form

where

is a white noise with variance

is a white noise with variance  . Using

. Using  and

and

the coefficients

and

and  are such that

are such that

and

When, for instance,

,

,  ,

,  and

and  , we obtain

, we obtain

- 4.7 In view of Exercise 3.5, an AR

process

process  ,

,  , in which the noise

, in which the noise  has a strictly positive density over

has a strictly positive density over  , is geometrically

, is geometrically  ‐mixing. Under the stationarity conditions given in Theorem 4.1, if

‐mixing. Under the stationarity conditions given in Theorem 4.1, if  has a density

has a density  and if

and if  (defined in (4.10)) is a continuously differentiable bijection (that is, if

(defined in (4.10)) is a continuously differentiable bijection (that is, if  ) then

) then  is a geometrically

is a geometrically  ‐mixing stationary process. Reasoning as in step (iv) of the proof of Theorem 3.4, it is shown that

‐mixing stationary process. Reasoning as in step (iv) of the proof of Theorem 3.4, it is shown that  , and then

, and then  , are also geometrically

, are also geometrically  ‐mixing stationary processes.

‐mixing stationary processes.

- 4.8 Since

and

and  , we have

, we have

If the volatility

is a positive function of

is a positive function of  that possesses a moment of order 2, then

that possesses a moment of order 2, then

under conditions (4.34). Thus, condition (4.38) is necessarily satisfied. Conversely, under (4.38) the strict stationarity condition is satisfied because

and, as in the proof of Theorem 2.2, it is shown that the strictly stationary solution possesses a moment of order 2.

- 4.9 Assume the second‐order stationarity condition (4.39). Let

and

Using

, we obtain

, we obtain

We then obtain the autocovariances

and the autocorrelations

. Note that

. Note that  for all

for all  , which shows that

, which shows that  is a weak ARMA

is a weak ARMA process. In the standard GARCH case, the calculation of these autocorrelations would be much more complicated because

process. In the standard GARCH case, the calculation of these autocorrelations would be much more complicated because  is not a linear function of

is not a linear function of  .

. - 4.10 This is obvious because an APARCH

with

with  ,

,  and

and  corresponds to a TGARCH

corresponds to a TGARCH .

.

- 4.11 This is an EGARCH

with

with  ,

,  ,

,  and

and  . It is natural to impose

. It is natural to impose  and

and  , so that the volatility increases with

, so that the volatility increases with  . It is also natural to impose

. It is also natural to impose  so that the effect of a negative shock is more important than the effect of a positive shock of the same magnitude. There always exists a strictly stationary solution

so that the effect of a negative shock is more important than the effect of a positive shock of the same magnitude. There always exists a strictly stationary solution

and this solution possesses a moment of order 2 when

which is the case, in particular, for

. In the Gaussian case, we have

. In the Gaussian case, we have

and

using the calculations of Exercise 4.5 and

Since

is an increasing function, provided

is an increasing function, provided  , we observe the leverage effect

, we observe the leverage effect  .

. - 4.12 For all

ε > 0, we have

and the conclusion follows from the Borel–Cantelli lemma.

- 4.13 Because the increments of the Brownian motion are independent and Gaussian, we have

and

as h → 0. The conclusion follows.

- 4.14 We have

Using the indication, one can check that

and

and

We thus conclude by noting that

Chapter 5

- Let (ℱ

t

) be an increasing sequence of

σ

‐fields such that ε

t

∈ ℱ

t

and

E(ε

t

∣ ℱ

t − 1) = 0. For

h > 0, we have ε

t

ε

t + h

∈ ℱ

t + h

and

The sequence (ε t ε t + h , ℱ t + h ) t is thus a stationary sequence of square integrable martingale increments. We thus have

where

. To conclude,

1

it suffices to note that

. To conclude,

1

it suffices to note that

in probability (and even in L 2 ).

- 5.2 This process is a stationary martingale difference, whose variance is

Its fourth‐order moment is

Thus,

Moreover,

Using Exercise 5.1, we thus obtain

- 5.3 We have

By the ergodic theorem, the denominator converges in probability (and even a.s.) to γ ε(0) = ω/(1 − α) ≠ 0. In view of Exercise 5.2, the numerator converges in law to

. Cramér's theorem

2

then entails

. Cramér's theorem

2

then entails

The asymptotic variance is equal to 1 when α = 0 (that is, when ε t is a strong white noise). Figure E.3 shows that the asymptotic distribution of the empirical autocorrelations of a GARCH can be very different from those of a strong white noise.

Figure E.3 Comparison between the asymptotic variance of

for the ARCH(1) process (5.28) with (η

t

) Gaussian (solid line) and the asymptotic variance of

for the ARCH(1) process (5.28) with (η

t

) Gaussian (solid line) and the asymptotic variance of  when ε

t

is a strong white noise (dashed line).

when ε

t

is a strong white noise (dashed line). - 5.4 Using Exercise 2.8, we obtain

In view of Exercises 5.1 and 5.3,

for any h ≠ 0.

- 5.5 Let ℱ

t

be the

σ

‐field generated by {η

u

, u ≤ t}. If

s + 2 > t + 1, then

Similarly, Eε t ε t + 1ε s ε s + 2 = 0 when t + 1 > s + 2. When t + 1 = s + 2, we have

because ε t − 1 σ t ∈ ℱ t − 1 ,

,

E(η

t

∣ ℱ

t − 1) = Eη

t

= 0 and

,

E(η

t

∣ ℱ

t − 1) = Eη

t

= 0 and  . Using (7.24), the result can be extended to show that

Eε

t

ε

t + h

ε

s

ε

s + k

= 0 when

k ≠ h

and (ε

t

) follows a GARCH(p, q), with a symmetric distribution for

η

t

.

. Using (7.24), the result can be extended to show that

Eε

t

ε

t + h

ε

s

ε

s + k

= 0 when

k ≠ h

and (ε

t

) follows a GARCH(p, q), with a symmetric distribution for

η

t

. - 5.6 Since

Eε

t

ε

t + 1 = 0, we have Cov{ε

t

ε

t + 1, ε

s

ε

s + 2} = Eε

t

ε

t + 1ε

s

ε

s + 2 = 0 in view of Exercise 5.5. Thus

- 5.7 In view of Exercise 2.8, we have

with ω = 1, α = 0.3 and β = 0.55. Thus γ ε(0) = 6.667,

,

,  . Thus

. Thus

for i = 1, …, 5. Finally, using Theorem 5.1,

- 5.8 Since

γ

X

(ℓ) = 0, for all ∣ℓ ∣ > q

, we clearly have

Since

,

γ

ε(0) = ω/(1 − α) and

,

γ

ε(0) = ω/(1 − α) and

(see, for instance, Exercise 2.8), we have

Note that

as

i → ∞.

as

i → ∞. - 5.9 Conditionally on initial values, the score vector is given by

where ε t (θ) = Y t − F θ (W t ). We thus have

and, when σ 2 does not depend on θ ,

- 5.10 In the notation of Section 5.4.1 and denoting by

the parameter of interest, the log‐likelihood is equal to

the parameter of interest, the log‐likelihood is equal to

up to a constant. The constrained estimator is

, with

, with  . The constrained score and the Lagrange multiplier are related by

. The constrained score and the Lagrange multiplier are related by

On the other hand, the exact laws of the estimators under H 0 are given by

and

with

For the case

, we can estimate

I

22

by

, we can estimate

I

22

by

The test statistic is then equal to

E.3

with

and where R 2 is the coefficient of determination (centred if X 1 admits a constant column) in the regression of

on the columns of

X

2

. For the first equality of (E.3), we use the fact that in a regression model of the form

Y = Xβ + U

, with obvious notation, Pythagoras's theorem yields

on the columns of

X

2

. For the first equality of (E.3), we use the fact that in a regression model of the form

Y = Xβ + U

, with obvious notation, Pythagoras's theorem yields

In the general case, we have

Since the residuals of the regression of Y on the columns of X 1 and X 2 are also the residuals of the regression of

on the columns of

X

1

and

X

2

, we obtain LM

n

by:

on the columns of

X

1

and

X

2

, we obtain LM

n

by:- computing the residuals

of the regression of

Y

on the columns of

X

1

;

of the regression of

Y

on the columns of

X

1

; - regressing

on the columns of

X

2

and

X

1

, and setting LM

n

= nR

2

, where

R

2

is the coefficient of determination of this second regression.

on the columns of

X

2

and

X

1

, and setting LM

n

= nR

2

, where

R

2

is the coefficient of determination of this second regression.

- computing the residuals

- 5.11 Since

, it is clear that

, it is clear that  , with

, with  and

R

2

defined in representations (5.29) and (5.30).

and

R

2

defined in representations (5.29) and (5.30).Since T is invertible, we have

, where Col(Z) denotes the vectorial subspace generated by the columns of the matrix

Z

, and

, where Col(Z) denotes the vectorial subspace generated by the columns of the matrix

Z

, and

If e ∈ Col(X) then

and

and

Noting that

, we conclude that

, we conclude that

Chapter 6

- From the observations ε1, …, ε

n

, we can compute

and

and

for h = 0, …, q . We then put

and then, for k = 2, …, q (when q > 1),

With standard notation, the OLS estimators are then

- 6.2 The assumption that

X

has full column rank implies that

X

′

X

is invertible. Denoting by 〈⋅, ⋅〉 the scalar product associated with the Euclidean norm, we have

and

with equality if and only if

, and we are done.

, and we are done. - 6.3 We can take

n = 2,

q = 1, ε0 = 0, ε1 = 1, ε2 = 0. The calculation yields

.

.

- 6.4 Case 3 is not possible, otherwise we would have

for all t , and consequently

, which is not possible.

, which is not possible.Using the data, we obtain

, and thus

, and thus  . Therefore, the constrained estimate must coincide with one of the following three constrained estimates: that constrained by

α

2 = 0, that constrained by

α

1 = 0, or that constrained by

α

1 = α

2 = 0. The estimate constrained by

α

2 = 0 is

. Therefore, the constrained estimate must coincide with one of the following three constrained estimates: that constrained by

α

2 = 0, that constrained by

α

1 = 0, or that constrained by

α

1 = α

2 = 0. The estimate constrained by

α

2 = 0 is  , and thus does not suit. The estimate constrained by

α

1 = 0 yields the desired estimate

, and thus does not suit. The estimate constrained by

α

1 = 0 yields the desired estimate  .

. - 6.5 First note that

. Thus

. Thus  if and only if

η

t

= 0. The nullity of the

i

th column of

X

, for

i > 1, implies that

η

n − i + 1 = ⋯ = η

2 = η

1 = 0. The probability of this event tends to 0 as

n → ∞ because, since

if and only if

η

t

= 0. The nullity of the

i

th column of

X

, for

i > 1, implies that

η

n − i + 1 = ⋯ = η

2 = η

1 = 0. The probability of this event tends to 0 as

n → ∞ because, since  , we have

P(η

t

= 0) < 1.

, we have

P(η

t

= 0) < 1.

- 6.6 Introducing an initial value

X

0

, the OLS estimator of

φ

0

is

and this estimator satisfies

Under the assumptions of the exercise, the ergodic theorem entails the almost sure convergence

and thus the almost sure convergence of

to

φ

0

. For the consistency, the assumption

to

φ

0

. For the consistency, the assumption  suffices.

suffices.If

, the sequence (ε

t

X

t − 1, ℱ

t

) is a stationary and ergodic square integrable martingale difference, with variance

, the sequence (ε

t

X

t − 1, ℱ

t

) is a stationary and ergodic square integrable martingale difference, with variance

We can see that this expectation exists by expanding the product

The CLT of Corollary A.1 then implies that

and thus

When

, the condition

, the condition  suffices for asymptotic normality.

suffices for asymptotic normality. - 6.7 By direct verification, A −1 A = I .

- 6.8

- Let

Then

Then  solves the modelThe parameter ω 0 vanishing in this equation, the moments of

solves the modelThe parameter ω 0 vanishing in this equation, the moments of

do not depend on it. It follows that

do not depend on it. It follows that

- and 3. Write

to indicate that a matrix

M

is proportional to

to indicate that a matrix

M

is proportional to  . Partition the vector

. Partition the vector  into

Z

t − 1 = (1, W

t − 1)′

and, accordingly, the matrices

A

and

B

of Theorem 6.2. Using the previous question and the notation of Exercise 6.7, we obtain

into

Z

t − 1 = (1, W

t − 1)′

and, accordingly, the matrices

A

and

B

of Theorem 6.2. Using the previous question and the notation of Exercise 6.7, we obtain

We then have

Similarly,

It follows that C = A −1 BA −1 is of the form

- Let

- 6.9

- Let

Let us show the existence of

x

*

. Let (x

n

) be a sequence of elements of

C

such that, for all

n > 0, ‖x − x

n

‖2 < α

2 + 1/n

. Using the parallelogram identity ‖a + b‖2 + ‖a − b‖2 = 2‖a‖2 + 2‖b‖2

, we havethe last inequality being justified by the fact that (x m + x n )/2 ∈ C , the convexity of C and the definition of α . It follows that (x n ) is a Cauchy sequence and, E being a Hilbert space and therefore a complete metric space, x n converges to some point x * . Since C is closed, x * ∈ C and ‖x − x *‖ ≥ α . We have also ‖x − x *‖ ≤ α , taking the limit on both sides of the inequality which defines the sequence (x n ). It follows that ‖x − x *‖ = α , which shows the existence.

Let us show the existence of

x

*

. Let (x

n

) be a sequence of elements of

C

such that, for all

n > 0, ‖x − x

n

‖2 < α

2 + 1/n

. Using the parallelogram identity ‖a + b‖2 + ‖a − b‖2 = 2‖a‖2 + 2‖b‖2

, we havethe last inequality being justified by the fact that (x m + x n )/2 ∈ C , the convexity of C and the definition of α . It follows that (x n ) is a Cauchy sequence and, E being a Hilbert space and therefore a complete metric space, x n converges to some point x * . Since C is closed, x * ∈ C and ‖x − x *‖ ≥ α . We have also ‖x − x *‖ ≤ α , taking the limit on both sides of the inequality which defines the sequence (x n ). It follows that ‖x − x *‖ = α , which shows the existence.

Assume that there exist two solutions of the minimisation problem in C ,

and

and  . Using the convexity of

C

, it is then easy to see that

. Using the convexity of

C

, it is then easy to see that  satisfies

satisfies

This is possible only if

(once again using the parallelogram identity).

(once again using the parallelogram identity). - Let

λ ∈ (0, 1) and

y ∈ C

. Since

C

is convex, (1 − λ)x

* + λy ∈ C

. Thus

and, dividing by λ ,

Taking the limit as λ tends to 0, we obtain inequality (6.17).

Let z such that, for all y ∈ C , 〈z − x, z − y〉 ≤ 0. We have

the last inequality being simply the Cauchy–Schwarz inequality. It follows that ‖x − z‖ ≤ ‖x − y‖, ∀ y ∈ C . This property characterising x * in view of part 1, it follows that z = x * .

- Let

- 6.10

- It suffices to show that when C = K , (6.17) is equivalent to (6.18). Since 0 ∈ K , taking y = 0 in (6.17) we obtain 〈x − x *, x *〉 ≤ 0. Since x * ∈ K and K is a cone, 2x * ∈ K . For y = 2x * in (6.17) we obtain 〈x − x *, x *〉 ≥ 0, and it follows that 〈x − x *, x *〉 = 0. The second equation of (6.18) then follows directly from (6.17). The converse, (6.18) ⇒ (6.17), is trivial.

- Since

x

* ∈ K

, then

z = λx

* ∈ K

for

λ ≥ 0. By (6.18), we haveIt follows that (λx)* = z and (a) is shown. The properties (b) are obvious, expanding ‖x * + (x − x *)‖2 and using the first equation of (6.18).

- 6.11 The model is written as

Y = X

(1)

θ

(1) + X

(2)

θ

(2) + U. Thus, since

M

2

X

(2) = 0, we have

M

2

Y = M

2

X

(1)

θ

(1) + M

2

U. Note that this is a linear model, of parameter

θ

(1)

. Noting that

, since

M

2

is an orthogonal projection matrix, the form of the estimator follows.

, since

M

2

is an orthogonal projection matrix, the form of the estimator follows.

- 6.12 Since

J

n

is symmetric, there exists a diagonal matrix

D

n

and an orthonormal matrix

P

n

such that

. For

n

large enough, the eigenvalues of

J

n

are positive since

. For

n

large enough, the eigenvalues of

J

n

are positive since  is positive definite. Let

λ

n

be the smallest eigenvalue of

J

n

. Denoting by ‖ ⋅ ‖ the Euclidean norm, we have

is positive definite. Let

λ

n

be the smallest eigenvalue of

J

n

. Denoting by ‖ ⋅ ‖ the Euclidean norm, we have

Since

and

and  , it follows that

, it follows that  , and thus that

X

n

converges to the zero vector of ℝ

k

.

, and thus that

X

n

converges to the zero vector of ℝ

k

. - 6.13 Applying the method of Section 6.3.2, we obtain

X

(1) = (1, 1)′

and thus, by Theorem 6.8,

Chapter 7

-

- When j < 0, all the variables involved in the expectation, except ε t − j , belong to the σ ‐field generated by {ε t − j − 1, ε t − j − 2, …}. We conclude by taking the expectation conditionally on the previous σ ‐field and using the martingale increment property.

- For

j ≥ 0, we note that

is a measurable function of

is a measurable function of  and of

and of  Thus

Thus  is an even function of the conditioning variables, denoted by

is an even function of the conditioning variables, denoted by  .

. - It follows that the expectation involved in the property can be written asThe latter equality follows from of the nullity of the integral, because the distribution of η t is symmetric.

- 7.2 By the Borel–Cantelli lemma, it suffices to show that for all real

δ > 0, the series of general terms

converges. That is to say,

converges. That is to say,

using Markov's inequality, strict stationarity and the existence of a moment of order s > 0 for

.

. - 7.3 For all

κ > 0, the process

is ergodic and admits an expectation. This expectation is finite since

is ergodic and admits an expectation. This expectation is finite since  and

and  . We thus have, by the standard ergodic theorem,

. We thus have, by the standard ergodic theorem,

When κ → ∞, the variable

increases to

X

1

. Thus by Beppo Levi's theorem

increases to

X

1

. Thus by Beppo Levi's theorem  converges to

E(X

1) = + ∞. It follows that

converges to

E(X

1) = + ∞. It follows that  tends almost surely to infinity.

tends almost surely to infinity. - 7.4

- The assumptions made on

f

and Θ guarantee that

is a measurable function of

η

t

, η

t − 1, …. By Theorem A.1, it follows that (Y

t

) is stationary and ergodic.

is a measurable function of

η

t

, η

t − 1, …. By Theorem A.1, it follows that (Y

t

) is stationary and ergodic. - If we remove condition (7.94), the property may not be satisfied. For example, let Θ = {θ

1, θ

2} and assume that the sequence (X

t

(θ

1), X

t

(θ

2)) is iid, with zero mean, each component being of variance 1 and the covariance between the two components being different when

t

is even and when

t

is odd. Each of the two processes (X

t

(θ

1)) and (X

t

(θ

2)) is stationary and ergodic (as iid processes). However,

is not stationary in general because its distribution depends on the parity of

t

.

is not stationary in general because its distribution depends on the parity of

t

.

- The assumptions made on

f

and Θ guarantee that

- 7.5

- In view of (7.30) and of the second part of assumption A1, we haveE.7almost surely. Indeed, on a set of probability 1, we have for all ι > 0,

E.8

E.8

Note that

and (7.29) entail that

and (7.29) entail that  . The limit superior (E.5) being less than any positive number, it is null.

. The limit superior (E.5) being less than any positive number, it is null. - Note that

is the strong innovation of

is the strong innovation of  . We thus have orthogonality between

ν

t

and any integrable variable which is measurable with respect to the

σ

‐field generated by θ0

:with equality if and only if

. We thus have orthogonality between

ν

t

and any integrable variable which is measurable with respect to the

σ

‐field generated by θ0

:with equality if and only if

‐almost surely, that is,

θ = θ

0

(by assumptions A3 and A4; see the proof of Theorem 7.1).

‐almost surely, that is,

θ = θ

0

(by assumptions A3 and A4; see the proof of Theorem 7.1). - We conclude that

is strongly consistent, as in (d) in the proof of Theorem 7.1, using a compactness argument and applying the ergodic theorem to show that, at any point

θ

1

, there exists a neighbourhood

V(θ

1) of

θ

1

such that

is strongly consistent, as in (d) in the proof of Theorem 7.1, using a compactness argument and applying the ergodic theorem to show that, at any point

θ

1

, there exists a neighbourhood

V(θ

1) of

θ

1

such that

- Since all we have done remains valid when Θ is replaced by any smaller compact set containing

θ

0

, for instance Θ

c

, the estimator

is strongly consistent.

is strongly consistent.

- In view of (7.30) and of the second part of assumption A1, we have

- 7.6 We know that

minimises, over Θ,

minimises, over Θ,

For all c > 0, there exists

such that

such that  for all

t ≥ 0. Note that

for all

t ≥ 0. Note that  if and only if

c ≠ 1. For instance, for a GARCH(1, 1) model, if

if and only if

c ≠ 1. For instance, for a GARCH(1, 1) model, if  we have

we have  . Let

. Let  The minimum of

f

is obtained at the unique point

The minimum of

f

is obtained at the unique point

If

, we have

, we have  . It follows that

c

0 = 1 with probability 1, which proves the result.

. It follows that

c

0 = 1 with probability 1, which proves the result. - 7.7 The expression for

I

1

is a trivial consequence of (7.74) and Cov

. Similarly, the form of

I

2

directly follows from (7.38). Now consider the non‐diagonal blocks. Using (7.38) and (7.74), we obtain

. Similarly, the form of

I

2

directly follows from (7.38). Now consider the non‐diagonal blocks. Using (7.38) and (7.74), we obtain

In view of (7.41), (7.42), (7.79) and (7.24), we have

and

It follows that

E.6

and ℐ is block‐diagonal. It is easy to see that 풥 has the form given in the theorem. The expressions for J 1 and J 2 follow directly from (7.39) and (7.75). The block‐diagonal form follows from (7.76) and (E.6).

- 7.8

- We have

The parameters to be estimated are

a

and

α

,

ω

being known. We haveIt follows that

The parameters to be estimated are

a

and

α

,

ω

being known. We haveIt follows that

Letting ℐ = (ℐ ij ),

and

and  , we then obtain

, we then obtain

- In the case where the distribution of

η

t

is symmetric we have

μ

3 = 0 and, using (7.24),

. It follows that

. It follows that

The asymptotic variance of the ARCH parameter estimator is thus equal to

: it does not depend on

a

0

and is the same as that of the QMLE of a pure ARCH(1) (using computations similar to those used to obtain (7.1.2)).

: it does not depend on

a

0

and is the same as that of the QMLE of a pure ARCH(1) (using computations similar to those used to obtain (7.1.2)). - When

α

0 = 0, we have

, and thus

, and thus  . It follows that

. It follows that

We note that the estimation of too complicated a model (since the true process is AR(1) without ARCH effect) does not entail any asymptotic loss of accuracy for the estimation of the parameter a 0 : the asymptotic variance of the estimator is the same,

, as if the AR(1) model were directly estimated. This calculation also allows us to verify the ‘

α

0 = 0’ column in Table 7.3: for the

, as if the AR(1) model were directly estimated. This calculation also allows us to verify the ‘

α

0 = 0’ column in Table 7.3: for the  law we have

μ

3 = 0 and

κ

η

= 3; for the normalized

χ

2(1) distribution we find

law we have

μ

3 = 0 and

κ

η

= 3; for the normalized

χ

2(1) distribution we find  and

κ

η

= 15.

and

κ

η

= 15.

- We have

- 7.9 Let

ε > 0 and

V(θ

0) be such that (7.95) is satisfied. Since

almost surely, for

n

large enough

almost surely, for

n

large enough  almost surely. We thus have almost surely

almost surely. We thus have almost surely

It follows that

and, since ε can be chosen arbitrarily small, we have the desired result.

In order to give an example where (7.95) is not satisfied, let us consider the autoregressive model X t = θ 0 X t − 1 + η t where θ 0 = 1 and (η t ) is an iid sequence with mean 0 and variance 1. Let J t (θ) = X t − θX t − 1 . Then J t (θ 0) = η t and the first convergence of the exercise holds true, with J = 0. Moreover, for all neighbourhoods of θ 0 ,

almost surely because the sum in brackets converges to +∞, X t being a random walk and the supremum being strictly positive. Thus (7.95) is not satisfied. Nevertheless, we have

Indeed,

converges in law to a non‐degenerate random variable (see, for instance, Hamilton 1994, p. 406) whereas

converges in law to a non‐degenerate random variable (see, for instance, Hamilton 1994, p. 406) whereas  in probability since

in probability since  has a non‐degenerate limit distribution.

has a non‐degenerate limit distribution. - 7.10 It suffices to show that

is positive semi‐definite. Note that

is positive semi‐definite. Note that  . It follows that

. It follows that

Therefore

is positive semi‐definite. Thus

is positive semi‐definite. Thus

Setting x = Jy , we then have

which proves the result.

- 7.11

- In the ARCH case, we have

. It follows thator equivalently

. It follows thator equivalently

, that is,

, that is,  We also have

We also have  , and thus

, and thus

- Introducing the polynomial

, the derivatives of

, the derivatives of  satisfyIt follows that

satisfyIt follows that In view of assumption A2 and Corollary 2.2, the roots of ℬ θ (L) are outside the unit disk, and the relation follows.

In view of assumption A2 and Corollary 2.2, the roots of ℬ θ (L) are outside the unit disk, and the relation follows.

- It suffices to replace

θ

0

by

in 1.

in 1.

- In the ARCH case, we have

- 7.12 Only three cases have to be considered, the other ones being obtained by symmetry. If

t

1 < min {t

2, t

3, t

4}, the result is obtained from (7.24) with

g = 1 and

t − j = t

1

. If

t

2 = t

3 < t

1 < t

4

, the result is obtained from (7.24) with

t = t

2

and

t − j = t

1

. If

t

2 = t

3 = t

4 < t

1

, the result is obtained from (7.24) with

t = t

2

and

t − j = t

1

. If

t

2 = t

3 = t

4 < t

1

, the result is obtained from (7.24) with  j = 0,

t

2 = t

3 = t

4 = t

and

j = 0,

t

2 = t

3 = t

4 = t

and  .

.

- 7.13

- It suffices to apply (7.38), and then to apply Corollary 2.1.

- The result follows from the Lindeberg central limit theorem of Theorem A.3.

- Using Eq. (7.39) and the convergence of

to +∞,

to +∞,

- In view of Eq. (7.50) and the fact that

, we have

, we have

- The derivative of the criterion is equal to zero at

. A Taylor expansion of this derivative around

α

0

then yieldswhere α * is between

. A Taylor expansion of this derivative around

α

0

then yieldswhere α * is between

and

α

0

. The result easily follows from the previous questions.

and

α

0

. The result easily follows from the previous questions. - When

ω

0 ≠ 1, we havewith

Since d t → 0 almost surely as t → ∞, the convergence in law of part 2 always holds true. Moreover,

with

which implies that the result obtained in Part 3 does not change. The same is true for Part 4 because

Finally, it is easy to see that the asymptotic behaviour of

is the same as that of

is the same as that of  , regardless of the value that is fixed for

ω

.

, regardless of the value that is fixed for

ω

. - In practice ω 0 is not known and must be estimated. However, it is impossible to estimate the whole parameter (ω 0, α 0) without the strict stationarity assumption. Moreover, under condition (7.14), the ARCH(1) model generates explosive trajectories which do not look like typical trajectories of financial returns.

- 7.14

- Consider a constant

. We begin by showing that

. We begin by showing that  for

n

large enough. Note thatWe have

for

n

large enough. Note thatWe have

In view of the inequality x ≥ 1 + log x for all x > 0, it follows that

For all M > 0, there exists an integer t M such that

for all

t > t

M

. This entails that

for all

t > t

M

. This entails that

Since M is arbitrarily large,

E.7

provided that

. If

. If  is chosen so that the constraint is satisfied, the inequalities

is chosen so that the constraint is satisfied, the inequalities

and (E.7) show that

E.8

We will define a criterion O n asymptotically equivalent to the criterion Q n . Since

a. s. as

t → ∞, we have for

α ≠ 0,

a. s. as

t → ∞, we have for

α ≠ 0,

where

On the other hand, we have

when α 0/α ≠ 1. We will now show that Q n (α) − O n (α) converges to zero uniformly in

. We have

. We have

Thus for all M > 0 and any ε > 0, almost surely

provided n is large enough. In addition to the previous constraints, assume that

. We have

. We have  for any

for any  , and

, and

for any α ≥ α 0 . We then have

Since M can be chosen arbitrarily large and ε arbitrarily small, we have almost surely

E.9

For the last step of the proof, let

and

and  be two constants such that

be two constants such that  . It can always be assumed that

. It can always be assumed that  . With the notation

. With the notation  , the solution of

, the solution of

is

This solution belongs to the interval

This solution belongs to the interval  when

n

is large enough. In this case

when

n

is large enough. In this case

is one of the two extremities of the interval

, and thus

, and thus

This result, (E.9), the fact that min α Q n (α) ≤ Q n (α 0) = 0 and (E.8) show that

Since

is an arbitrarily small interval that contains

α

0

and

is an arbitrarily small interval that contains

α

0

and  , the conclusion follows.

, the conclusion follows. - It can be seen that the constant 1 does not play any particular role and can be replaced by any other positive number

ω

. However, we cannot conclude that

almost surely because

almost surely because  , but

, but  is not a constant. In contrast, it can be shown that under the strict stationarity condition

is not a constant. In contrast, it can be shown that under the strict stationarity condition  the constrained estimator

the constrained estimator  does not converge to

α

0

when

ω ≠ ω

0

.

does not converge to

α

0

when

ω ≠ ω

0

.

- Consider a constant

Chapter 8

- Let the Lagrange multiplier

λ ∈ ℝ

p

. We have to maximise the Lagrangian

Since at the optimum

the solution is such that

Since

Since  we obtain

we obtain  , and then the solution is

, and then the solution is

- 8.2 Let

K

be the

p × n

matrix such that

K(1, i

1) = ⋯ = K(p, i

p

) = 1 and whose the other elements are 0. Using Exercise 8.1, the solution has the formE.10

Instead of the Lagrange multiplier method, a direct substitution method can also be used.

The constraints

can be written as

can be written as

where H is n × (n − p), of full column rank, and x * is (n − p) × 1 (the vector of the non‐zero components of x ). For instance: (i) if n = 3, x 2 = x 3 = 0 then x * = x 1 and

; (ii) if

n = 3,

x

3 = 0 then

x

* = (x

1, x

2)′

and

; (ii) if

n = 3,

x

3 = 0 then

x