Chapter 12

Conclusion

In March 2020, popular opinion – spearheaded by the media – might deem it beside the point to write a book about geopolitics and investing. A book on epidemiology and investing may be more appropriate.

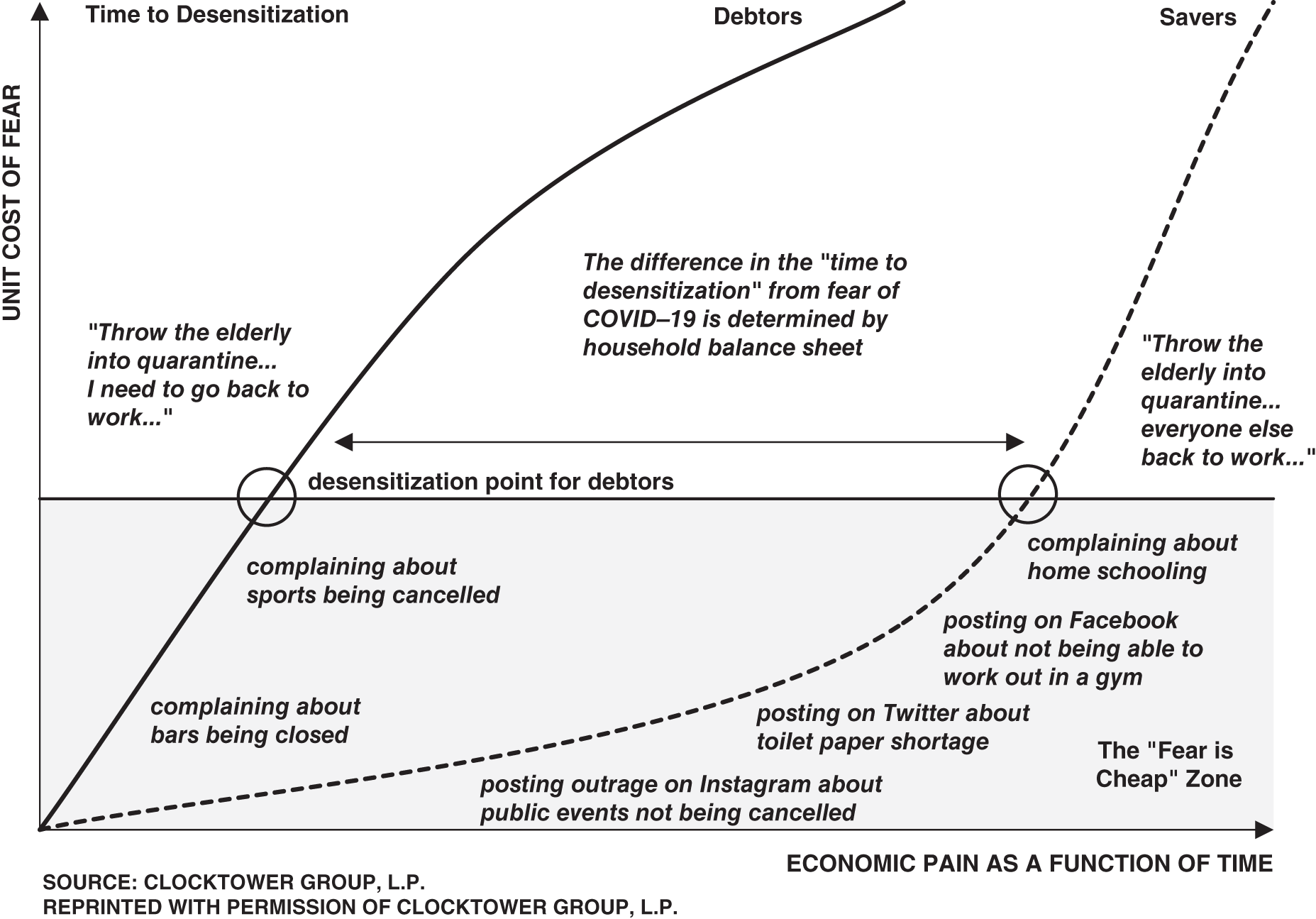

But geopolitics is central to the COVID-19 pandemic and its ultimate effect on the economy and markets. In Chapter 8, I argued the curve-flattening narrative will ultimately succumb to economic constraints: the pressure to restart the economy. Figure 12.1 summarizes that chapter's conclusions, and only half-jokingly.

As a reminder of my main thesis in Chapter 8, most voters are not savers. Or, if they are, their savings is not enough to nurse them through a depression-level economic dislocation. Therefore, investors should expect a revolt against the indefinite curve-flattening narrative to occur sooner rather than later – at the “desensitization point for debtors” in Figure 12.1. While your sample may be skewed if your friends, family, and colleagues are “savers” – certainly if you are an investor they are – most people are “debtors” on the diagram. Twitter and Instagram are not representative of the median voter in this respect.

Figure 12.1 Constraints to flatten-the-curve narrative will grow.

This book has little to teach about pandemics, but it does provide a framework to forecast policy reactions to anything. A recession, terrorism, trade war, pandemic, alien invasion. It does not matter. A correct read of constraints will always beat a forecast based on preferences or one that extrapolates the current narrative and dominant sentiment linearly into the future. Such reductionist linearity might be common in abstract models, but it is harder to find in material reality.

Though COVID-19 is on everyone's minds at the time of writing, I want to end with a broader conclusion and highlight what this book has to teach investors and non-investors alike: leave ideology and unfounded bias out of policy discussions. Even if you run a think tank or a political advocacy interest group, you can find something useful in the constraint framework. Its unique perspective enables you to perceive reality – without the rose-colored glasses of personal preference. If you know where things stand materially and where they are going, your efforts to change them for the better will be more successful.

Take climate change. If you think it is a dire scenario, then you need to understand the constraints on reducing carbon emissions.1 Once you develop a clear, nonideological, constraint-based forecast of policy, you will discover the fulcrum constraint that must change to generate the outcomes you want.

Personally, I will not be the agent of any change, only its observer. I posited in Chapter 3 that a special circle of forecasting hell is reserved for the self-important, op-ed-writing forecaster. I spend a lot of time meditating on my biases and bathing myself in nihilism. I would probably make a terrible motivational speaker. And I try, really hard, not to become outraged by stupid policymaking.

I wrote this book because my framework has allowed me to make sense of the world and occasionally generate alpha. I hope others who use it will find similar success, but it won't work for everyone, and it is definitely not a foolproof method. As I illustrated with COVID-19 – only the most important investment matter of 2020– a too-rigid focus on material constraints does have its pitfalls. Sometimes collective psychology can create a material reality of its own.

But in the long-term, like old age, material constraints are undefeated. The problem for investors is that, before the long-term arrives, you can lose all your money. As Keynes remarked in the 1930s, “markets can stay irrational longer than you can remain solvent.” Betting against time is the Achilles' heel of any investment framework and why investing is an art, not a science. As is the case for the practitioner of any art form, I may strive for perfection, but I can only hope to approach it asymptotically.

From one artist to another, I hope this book helps you add the hue of geopolitical analysis to your palette.

Note

- 1 You may be wondering what these constraints are. Too bad. It's Chapter 12, folks, and I will not expand on climate change here.