Chapter 5

ACCOUNTING FOR MERCHANDISING OPERATIONS

CHAPTER LEARNING OBJECTIVES

After studying this chapter, you should be able to:

1. Identify the differences between service and merchandising companies.

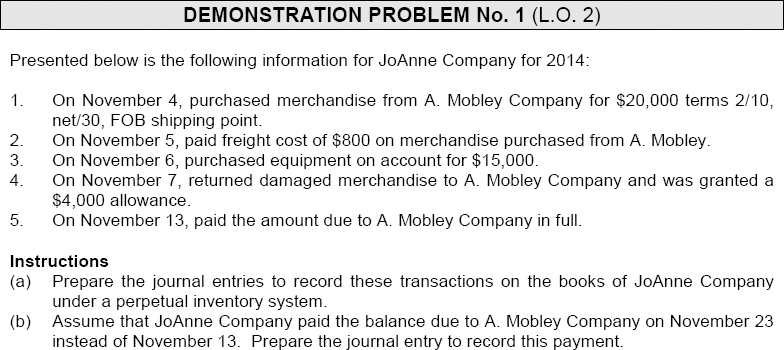

2. Explain the recording of purchases under a perpetual inventory system.

3. Explain the recording of sales revenues under a perpetual inventory system.

4. Explain the steps in the accounting cycle for a merchandising company.

5. Distinguish between a multiple-step and a single-step income statement.

*6. Explain the recording of purchases and sales of inventory under a periodic inventory system.

*7. Prepare a worksheet for a merchandising company.

*8. Compare the accounting procedures for merchandising under GAAP and IFRS.

*Note: All asterisked (*) items relate to material contained in the Appendices to the chapter.

![]()

PREVIEW OF CHAPTER 5

The steps in the accounting cycle for a merchandising company are the same as the steps for a service enterprise. However, merchandising companies use additional accounts and entries which are required in recording merchandising transactions. The content and organization of this chapter are as follows:

![]()

Measuring Net Income

- (L.O. 1) A merchandiser is an enterprise that buys and sells goods to earn revenue. Merchandisers that purchase and sell directly to consumers are retailers, and those that sell to retailers are known as wholesalers.

- The primary source of revenue for a merchandiser is sales revenue. Expenses are divided into two categories: (1) cost of goods sold and (2) operating expenses.

- Sales less cost of goods sold is called the gross profit (or gross margin) on sales. For example, if sales are $5,000 and cost of goods sold is $3,000, gross profit is $2,000.

- After gross profit is calculated, operating expenses are deducted to determine net income (or loss).

- Operating expenses are expenses incurred in the process of earning sales revenue.

Operating Cycles

6. The operating cycle of a merchandiser is as follows:

Flow of Costs

7. A merchandiser may use either a perpetual or a periodic inventory system in determining cost of goods sold.

a. In a perpetual inventory system, detailed records of the cost of each inventory item are maintained and the cost of each item sold is determined from the records when the sale occurs.

b. In a periodic inventory system, detailed inventory records are not maintained and the cost of goods sold is determined only at the end of an accounting period.

Purchase Transactions

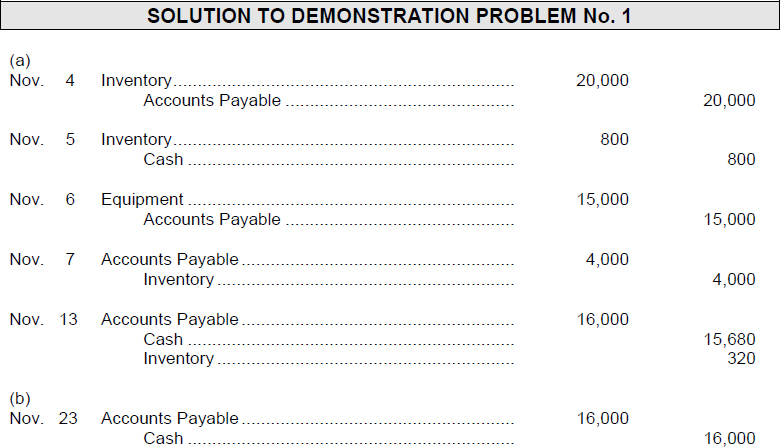

8. (L.O. 2) Under the perpetual inventory system, purchases of merchandise for sale are recorded in the Inventory account. For a cash purchase, Cash is credited; for a credit purchase, Accounts Payable is credited.

9. FOB shipping point means that goods are placed free on board the carrier by the seller, and the buyer must pay the freight costs. FOB destination means that goods are placed free on board at the buyer's place of business, and the seller pays the freight.

10. When the purchaser pays the freight, Inventory is debited and Cash is credited. When the seller pays the freight, Delivery Expense or Freight-out is debited and cash is credited. This account is classified as an operating expense by the seller.

11. A purchaser may be dissatisfied with the merchandise received because the goods may be damaged or defective, of inferior quality, or not in accord with the purchaser's specifications. The purchaser may return the merchandise, or choose to keep the merchandise if the supplier is willing to grant an allowance (deduction) from the purchase price. When merchandise is returned, Inventory is credited.

12. When the credit terms of a purchase on account permits the purchaser to claim a cash discount for the prompt payment of a balance due, this is called a purchase discount. If a purchase discount has terms 3/10, n/30, then a 3% discount is taken on the invoice price (less any returns or allowances) if payment is made within 10 days. If payment is not made within 10 days, then there is no purchase discount, and the net amount of the bill is due within 30 days.

13. When an invoice is paid within the discount period, the amount of the discount is credited to Inventory. When an invoice is not paid within the discount period, then the usual entry is made with a debit to Accounts Payable and a credit to Cash.

Sales Transactions

14. (L.O. 3) In accordance with the revenue recognition principle, sales revenues are recorded when the performance obligation is satisfied. Typically the performance obligation is satisifed when the goods are transferred from the seller to the buyer.

15. All sales transactions should be supported by a business document. Cash register documents provide evidence of cash sales; sales invoices provide support for credit sales.

16. A sale on credit is recorded as follows:

A cash sale is recorded by a debit to Cash and a credit to Sales Revenue, and a debit to Cost of Goods Sold and a credit to Inventory.

17. A sales return results when a customer is dissatisfied with merchandise and is allowed to return the goods to the seller for credit or for a cash refund. A sales allowance results when a customer is dissatisfied with merchandise and the seller is willing to grant an allowance (deduction) from the selling price.

18. To give the customer a sales return or allowance, the seller normally makes the following entry if the sale was a credit sale (the second entry is made only if the goods are returned):

For a sales return or allowance on a cash sale, a cash refund is made and Cash is credited instead of Accounts Receivable. The second entry is the same as above.

19. Sales Returns and Allowances is a contra revenue account and the normal balance of the account is a debit.

Sales Discounts

20. A sales discount is the offer of a cash discount to a customer for the prompt payment of a balance due. If a credit sale has terms 2/10, n/30, then a 2% discount is taken on the invoice price (less any returns or allowances) if payment is made within 10 days. If payment is not made within 10 days, then there is no sales discount, and the net amount of the bill, without discount, is due within 30 days. Sales Discounts is a contra revenue account and the normal balance of this account is a debit.

21. Both Sales Returns and Allowances and Sales Discounts are subtracted from Sales Revenue in the income statement to arrive at net sales.

The Accounting Cycle

22. (L.O. 4) Each of the required steps in the accounting cycle applies to a merchandising company.

Adjusting Entries and Closing Entries

23. A merchandising company generally has the same types of adjusting entries as a service company but a merchandiser using a perpetual inventory system will require an additional adjustment to reflect the difference between a physical count of the inventory and the accounting records. In addition, like a service company, a merchandising company makes closing entries to and from Income Summary.

Multiple-Step vs. Single-Step Income Statement

24. (L.O. 5) A multiple-step income statement shows two steps in determining net income: (1) cost of goods sold is subtracted from net sales for determining gross profit and (2) operating expenses are deducted from gross profit to determine net income. In addition, there may be nonoperating sections for:

a. Revenues and expenses that result from secondary or auxiliary operations, and

b. Gains and losses that are unrelated to the company's operations.

Gross Profit and Operating Expenses

25. Gross profit is net sales less cost of goods sold. The gross profit rate is expressed as a percentage by dividing the amount of gross profit by net sales. Operating expenses are the third component in measuring net income for a merchandising company.

26. Nonoperating sections are reported in the income statement after income from operations and are classified as (a) Other revenues and gains and (b) Other expenses and losses.

27. The income statement is referred to as a single-step income statement when all data are classified under two categories: (a) Revenues and (b) Expenses, and only one step is required in determining net income or net loss.

Classified Balance Sheet

28. A merchandiser generally has the same type of balance sheet as a service company except inventory is reported as a current asset.

Determining Cost of Goods Sold Under a Periodic System

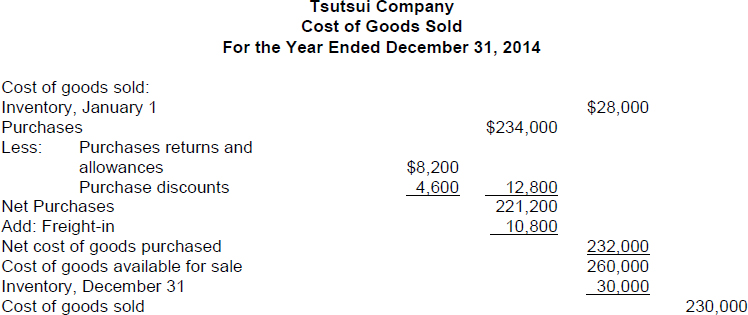

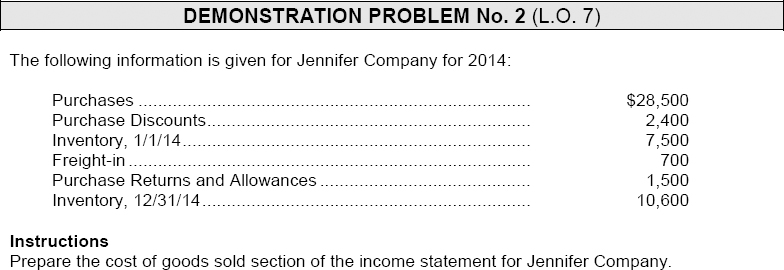

*29. (L.O. 6) Under a periodic system separate accounts are used to record freight costs, returns, and discounts. In addition, a running account of changes in inventory is not maintained. Instead, the balance in ending inventory, as well as cost of goods sold for the period, is calculated at the end of the period. The determination of cost of goods sold for Tsutsui Co. using a periodic inventory system, is as follows:

Periodic Inventory System

*30. In a periodic inventory system revenues from the sale of merchandise are recorded when sales are made in the same way as in a perpetual system. But, no attempt is made on the date of sale to record the cost of the merchandise sold. Instead, a physical inventory count is taken at the end of the period to determine (1) the cost of the merchandise then on hand and (2) the cost of the goods sold during the period.

*31. Under the periodic inventory system, purchases of merchandise for sale are recorded in a Purchases account. For a cash purchase, Cash is credited; for a credit purchase, Accounts Payable is credited.

*32. A purchase return and allowance is recorded by debiting Accounts Payable or Cash and crediting the account Purchase Returns and Allowances. Purchase Returns and Allowances is a temporary account whose normal balance is a credit.

*33. If payment is made within a discount period, the amount of the discount is credited to the account Purchases Discounts. When an invoice is not paid within the discount period, then the usual entry is made with a debit to Accounts Payable and a credit to Cash.

Cost of Goods Sold

*34. To determine the cost of goods sold under a periodic inventory system, three steps are required: (1) Record purchases of merchandise; (2) Determine the cost of goods purchased; and (3) Determine the cost of goods on hand at the beginning and end of the accounting period.

Cost of Goods Purchased

*35. In determining cost of goods purchased, (a) contra-purchase accounts are subtracted from purchases to produce net purchases, and (b) freight-in is then added to net purchases.

*36. Cost of inventory on hand under the periodic inventory method is obtained from a physical inventory. Taking a physical inventory involves:

a. Counting the units on hand for each item of inventory.

b. Applying unit costs to the total units on hand for each item.

c. Totaling the costs for each item of inventory, to determine the total cost of goods on hand.

Cost of Goods Sold

*37. Cost of goods sold is determined by two steps:

a. The cost of goods purchased is added to the cost of goods on hand at the beginning of the period to obtain the cost of goods available for sale.

b. The cost of goods on hand at the end of the period is subtracted from the cost of goods available for sale.

*38. The income statement for retailers and wholesalers under a periodic inventory system will generally contain more detail listing the above calculations.

Using a Worksheet

*39. (L.O. 7) As indicated in CHAPTER 4, a worksheet enables financial statements to be prepared before the adjusting entries are journalized and posted. The steps in preparing a worksheet for a merchandiser are the same as they are for a service enterprise except the additional merchandising accounts are included.

A Look at IFRS

*40. (L.O. 8) Under both GAAP and IFRS a company can choose to use either a perpetual or a periodic system.

*41. Under GAAP, companies generally classify income statement items by function. Under IFRS, Companies must classify expenses by either nature or function.

*42. Under IFRS, revaluation of land, buildings, and intangible assets is permitted, which are initially adjusted to equity, often referred to as other comprehensive income.

*43. IFRS requires that two years of income statement information be presented, whereas GAAP requires three years.

![]()

![]()

![]()

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

![]()

Circle the letter that best answers each of the following statements.

- (L.O. 1) A merchandising company sells goods to:

- (L.O. 1) Brent Company has sales revenue of $13,000, cost of goods sold of $8,000 and operating expenses of $3,000 for the year ended December 31. Brent's gross profit is:

- $10,000.

- $ 5,000.

- $ 2,000.

- $ 0.

- (L.O. 1) For the year ended 2012, Degas Co. has the following amounts: Sales Revenue $350,000; Gross Profit $120,000; and Operating Expenses $90,000. What are the amounts of Cost of Goods Sold and Net Income (Loss)?

- $260,000 and $140,000.

- $230,000 and $30,000.

- $230,000 and $140,000.

- $130,000 and $90,000.

- (L.O. 1) Which of the following is not associated with a perpetual inventory system?

- Detailed records of the cost of each inventory purchase and sale are maintained.

- The system is usually more expensive.

- Shrinkage and lost or stolen goods are more readily determined.

- The cost of goods sold is determined only at the end of the accounting period.

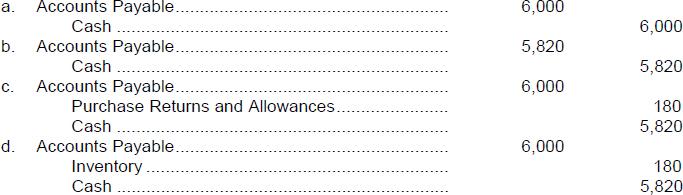

- (L.O. 2) Monet Company made a purchase of merchandise on credit from Claude Corporation on August 3, for $3,000, terms 2/10, n/45. On August 10, Monet makes the appropriate payment to Claude. The entry on August 10 for Monet Company is:

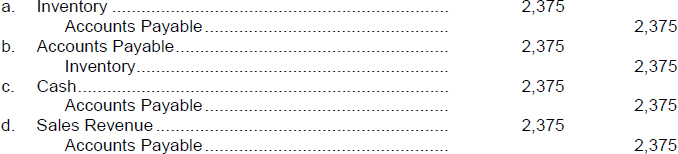

- (L.O. 2) On August 28, Renoir Company purchased merchandise from Sisley Company for $2,375 on credit. Under the perpetual system, the entry by Renoir Company is:

- (L.O. 2) Cezanne Co. returned defective goods costing $5,000 to the Bazille Company on March 19, for credit. The goods were purchased March 10, on credit, terms 3/10, n/30. The entry by Cezanne Co. on March 19, in receiving full credit is:

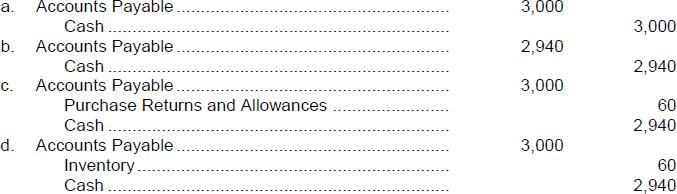

- (L.O. 2) Seurat Company made a purchase of merchandise on credit from Van Gogh Company on August 3, for $6,000, terms 3/10, n/30. On August 17, Seurat makes the appropriate payment to Van Gogh. The entry on August 17 for Seurat Company is:

- (L.O. 2) Caillebotte Company purchased inventory from Pissaro Company. The shipping costs were $400 and the terms of the shipment were FOB shipping point. Caillebotte would have the following entry regarding the shipping charges:

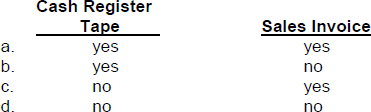

- (L.O. 3) Every credit sale should be supported by a:

- (L.O. 3) El Greco Co. made a credit sale to Rubens Company when terms were n/30. Upon payment by Rubens, El Greco Co. should debit Cash and credit:

- Sales Revenue.

- Accounts Receivable and Sales Discounts.

- Accounts Receivable.

- None of the above.

- (L.O. 3) On October 2, 2014, DaVinchi Company has cash sales of $3,200 from merchandise having a cost of $2,500. The entries to record the day's cash sales will include:

- a $2,500 debit to Cost of Goods Sold.

- a $3,200 credit to Cash.

- a $2,500 debit to Inventory.

- a $2,500 debit to Accounts Receivable.

- (L.O. 3) On October 4, 2014, Terry Corporation had credit sales transactions of $2,500 from merchandising having cost $1,900. The entries to record the day's credit transactions include:

- a debit of $2,500 to Inventory.

- a credit of $2,500 to Sales Revenue.

- a debit of $1,900 to Inventory.

- a credit of $1,900 to Cost of Goods Sold.

- (L.O. 3) A customer, Zurbaran, is dissatisfied with merchandise purchased for $2,000 cash from the Rembrandt Company. Rembrandt Company gives Zurbaran a cash refund of $2,000. The journal entry by Rembrandt Company for the refund will include a:

- debit to Sales Returns and Allowances.

- credit to Accounts Receivable.

- debit to Accounts Receivable.

- credit to Sales Returns and Allowances.

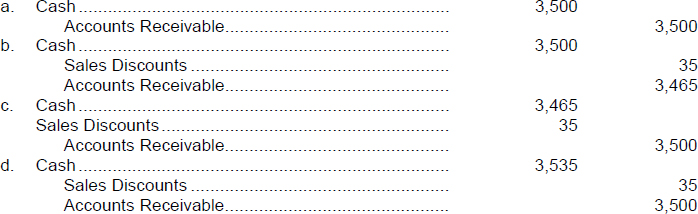

- (L.O. 3) On July 9, Goya Company sells goods on credit to Ed Manet for $3,500, terms 1/10, n/60. Goya receives payment on July 18. The entry by Goya on July 18 is:

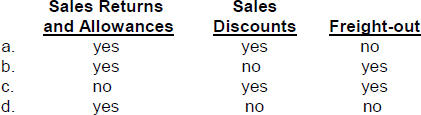

- (L.O. 3) Which of the following are contra revenue accounts?

- (L.O. 4) In the Clark Company, sales were $320,000, sales returns and allowances were $20,000 and cost of goods sold was $180,000. The gross profit rate was:

- 60%.

- 40%.

- 37.5%.

- 56.3%.

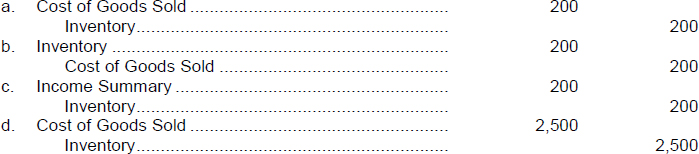

- (L.O. 4) When the physical count of BIM company inventory had a cost of $2,700 at year end and the unadjusted balance in Merchandise Inventory was $2,500, BIM will have to make the following entry:

- (L.O. 5) The nonoperating sections of the income statement will include a section entitled other:

- revenues and losses.

- revenues and gains.

- expenses and gains.

- expenses and casualty losses.

- (L.O. 5) In the balance sheet, ending inventory is reported:

- in current assets immediately following accounts receivable.

- in current assets immediately following prepaid expenses.

- in current assets immediately following cash.

- under property, plant, and equipment.

*21. (L.O. 6) Which of the following is true concerning Freight-in?

a. Freight-in is subtracted from net purchases in determining cost of goods purchased.

b. Freight-in is added to net purchases in determining cost of goods purchased.

c. Freight-in is a selling expense.

d. Freight-in is an administrative expense.

*22. (L.O. 6) On December 31, Degas Co. has the following account balances: Purchases $307,000; Purchase Returns and Allowances $34,000; Purchase Discounts $26,000; and Freight-in $18,000. The cost of goods purchased for Degas Co. is:

a. $265,000.

b. $281,000.

c. $349,000.

d. $229,000.

*23. (L.O. 6) On December 31, Seurat Company has the following amounts in the determination of cost of goods purchased: Purchases $60,000; Freight-in $10,000; Net purchases $48,000; Purchase returns and allowances $7,000; and Cost of goods purchased $58,000. What is the amount of purchase discounts?

a. $2,000.

b. $3,000.

c. $5,000.

d. $15,000.

*24. (L.O. 6) On December 31, Van Gogh Company has the following data: Cost of goods purchased $184,500; Beginning Inventory $19,000, Ending inventory $25,000, and Sales Revenue $300,000. The cost of goods sold for Van Gogh Corporation is:

a. $121,500.

b. $190,500.

c. $178,500.

d. $109,500.

*25. (L.O. 6) Caillebotte Company has the following amounts in the determination of cost of goods sold: Cost of Goods Purchased $76,000; Ending Inventory $34,000; Cost of Goods Sold $82,000. The dollar amount of beginning inventory is:

a. $28,000.

b. $40,000.

c. $42,000.

d. $48,000.

![]()

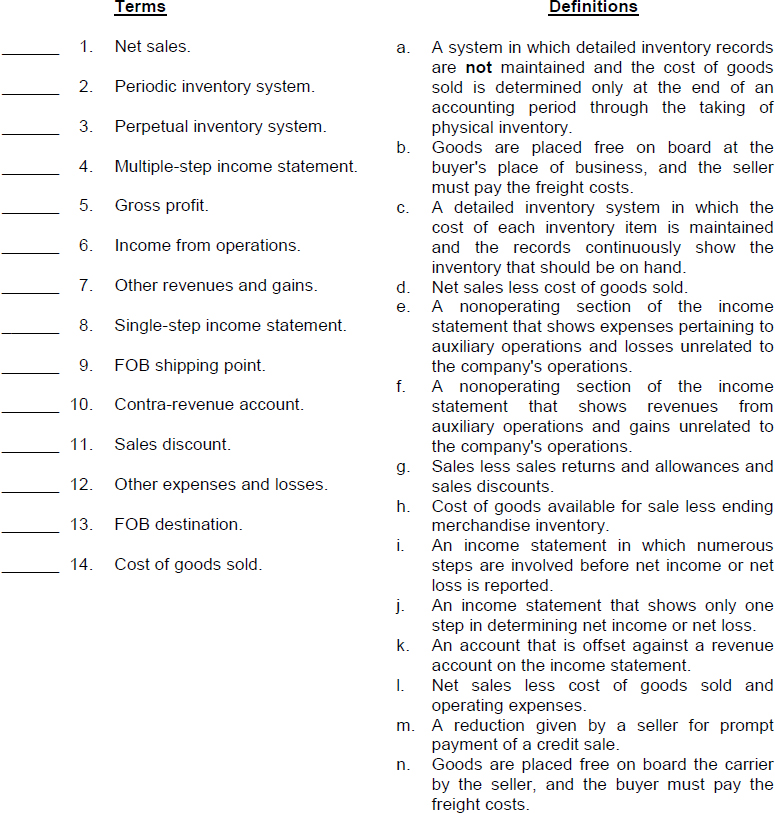

Match each term with its definition by writing the appropriate letter in the space provided.

![]()

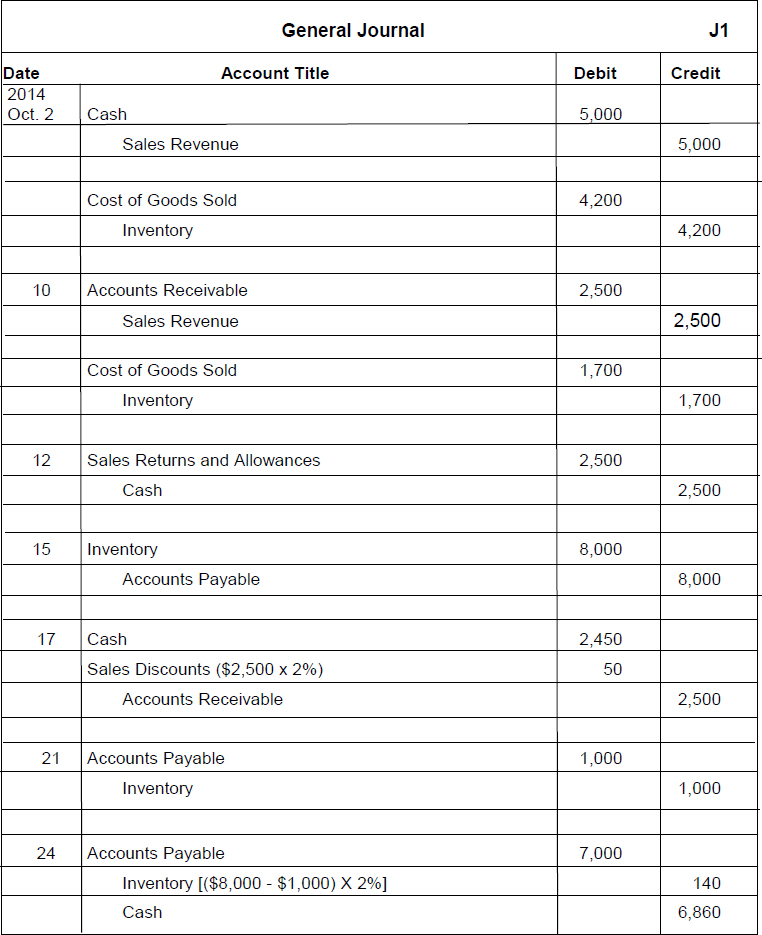

EX. 5-1 (L.O. 2 and 3) During the month of October, 2014, the American Fiction Merchandising Company had the following transactions:

| Oct. 2 | Sold $5,000 of goods that originally cost $4,200 to Jim Michener for cash. |

| 10 | Sold goods to Irving Stone for $2,500 on credit, terms 2/10, n/30. The goods originally cost $1,700. |

| 12 | Gave a cash refund of $2,500 to Jim Michener because half of the goods purchased on October 2 were defective. The goods were not returned. |

| 15 | Purchased $8,000 of merchandise from L'Amour Company on credit, terms 2/10, n/30. |

| 17 | Received cash from Irving Stone in full payment of the sale on October 10, less the sales discount. |

| 21 | Received an allowance from L'Amour Company of $1,000 because the goods purchased on October 15 did not meet specifications. |

| 24 | Paid L'Amour Company the amount due less the purchase discount. |

Instructions

Journalize the transactions. (Omit explanations.)

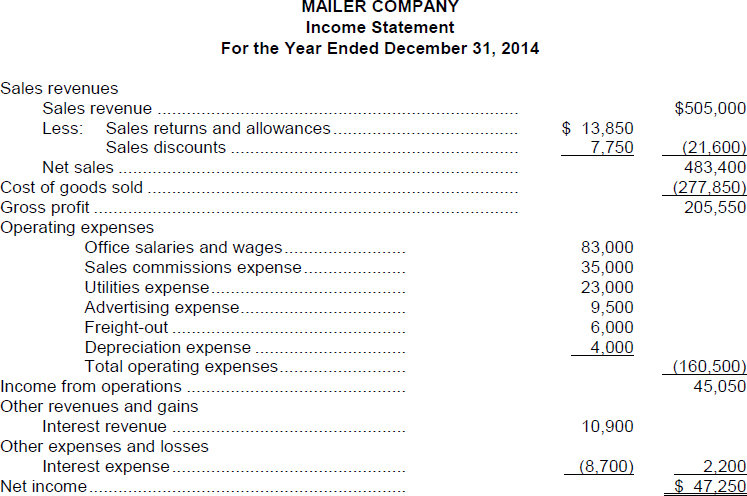

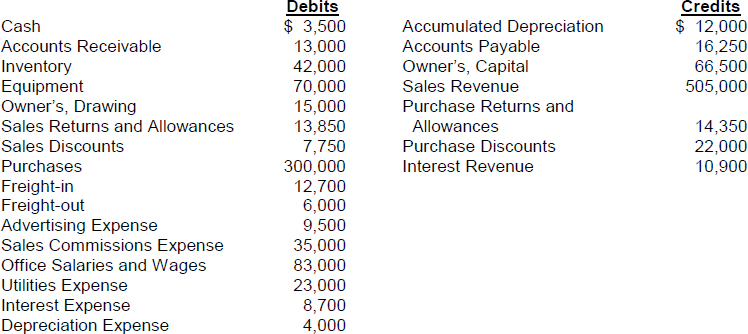

EX. 5-2 (L.O. 5) On December 31, 2014, the adjusted trial balance of the Mailer Company was as follows:

Instructions

Prepare a multiple-step income statement for the year ended December 31, 2014.

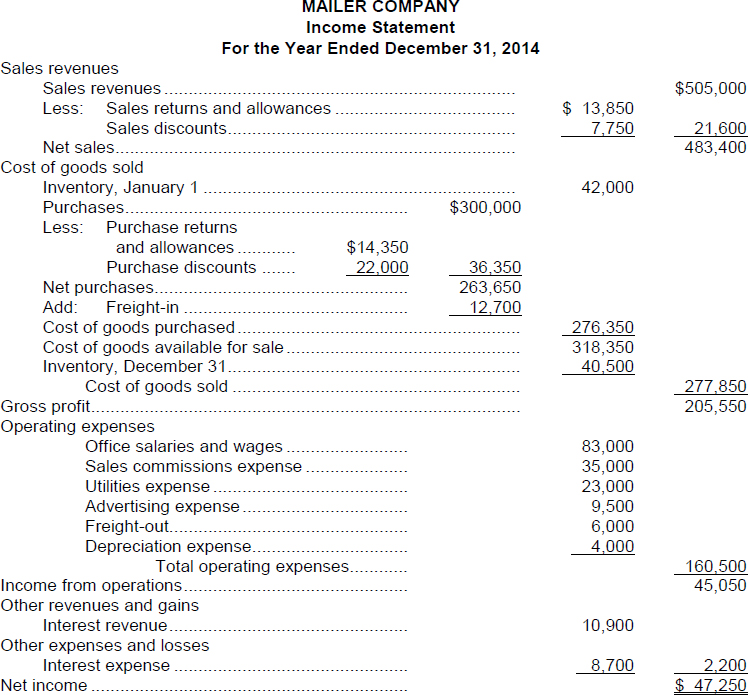

*EX. 5-3 (L.O. 6) Mailer Company uses a periodic inventory system. On December 31, 2014, the adjusted trial balance of the Mailer Company was as follows:

Other data:

Merchandise inventory December 31, 2014 is $40,500.

Instructions

Prepare a multiple-step income statement for the year ended December 31, 2014.

![]()

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

TRUE-FALSE

| 1. (F) | Merchandisers that sell to retailers are known as wholesalers; retailers are merchandising companies that purchase and sell directly to consumers. |

| 2. (F) | Inventory is reported as a current asset on the balance sheet. |

| 3. (F) | In a perpetual inventory system detailed records of the cost of each inventory purchase and sale are maintained and continuously (perpetually) show the inventory that should be on hand for every item. |

| 4. (T) | |

| 5. (F) | Under a perpetual inventory system, purchases of merchandise for sale are recorded by a debit to the Inventory account. |

| 6. (F) | A purchase return is where the purchaser returns the goods to the supplier for credit if the sale was made on credit, or for a cash refund if the purchase was originally for cash. |

| 7. (F) | The terms 2/10, n/30 state that a 2% discount is available if the invoice is paid within 10 days of the invoice date otherwise the net balance, without cash discount, is due 30 days from the invoice date. |

| 8. (F) | When the terms are FOB shipping point, the buyer pays the freight costs; when the terms are FOB destination, the seller pays the freight costs. |

| 9. (T) | |

| 10. (F) | Sales Revenue should be recorded in accordance with the revenue recognition principle. |

| 11. (T) | |

| 12. (T) | |

| 13. (F) | Sales Returns and Allowances is a contra revenue account. It is subtracted from Sales Revenue in the computation of Net Sales. |

| 14. (T) | |

| 15. (T) | |

| 16. (T) | |

| 17. (F) | The difference between the amounts is income (loss) from operations, not net income (or loss). |

| 18. (F) | If a merchandiser sells land at more than its cost, the gain should be reported in the other revenues and gains section. |

| 19. (T) | |

| 20. (T) | |

| *21. (T) | |

| *22. (F) | Freight-in is added to net purchases; Freight-out is a selling expense. |

| *23. (T) | |

| *24. (F) | The cost of ending inventory is subtracted from the cost of goods available for sale to determine the cost of goods sold. |

| *25. (F) | Under a periodic inventory system, when the purchaser directly incurs freight costs, the account Freight-in is debited. |

MATCHING

- g

- a

- c

- i

- d

- l

- f

- j

- n

- k

- m

- e

- b

- h

EX. 5-1