Chapter 6

INVENTORIES

CHAPTER LEARNING OBJECTIVES

After studying this chapter, you should be able to:

1. Determine how to classify inventory and inventory quantities.

2. Explain the accounting for inventories and describe the inventory cost flow methods.

3. Explain the financial effects of the inventory cost flow methods.

4. Explain the lower-of-cost-or-market basis of accounting for inventories.

5. Indicate the effects of inventory errors on the financial statements.

6. Compute and interpret inventory turnover.

*7. Apply the inventory cost flow methods to perpetual inventory records.

*8. Describe the two methods of estimating inventories.

*9. Compare the accounting procedures for inventories under GAAP and IFRS.

![]()

*Note: All asterisked (*) items relate to material contained in the Appendix to the chapter.

PREVIEW OF CHAPTER 6

In this chapter we will explain the procedures for determining the cost of inventory on hand at the balance sheet date. In addition, we will discuss the effects of inventory errors on a company's financial statements. The content and organization of this chapter are as follows:

![]()

CHAPTER REVIEW

- (L.O. 1) Merchandise inventory has two common characteristics: (a) it is owned by the company and (b) it is in a form ready for sale in the ordinary course of business.

- A manufacturer's inventory is usually classified into three categories:

- Finished goods that are completed and ready for sale.

- Work in process that is in various stages of production but not yet completed.

- Raw materials that are on hand waiting to be used in production.

Determination of Inventory Quantities

3. The determination of inventory quantities involves (a) taking a physical inventory of goods on hand and (b) determining the ownership of goods.

4. Taking a physical inventory involves counting, weighing or measuring each kind of inventory on hand. Internal control procedures should be followed in taking the inventory in order to minimize errors.

5. For goods in transit, legal title is determined by the terms of sale. When the terms are:

a. FOB (free on board) shipping point, ownership of the goods passes to the buyer when the public carrier accepts the goods from the seller.

b. FOB destination, legal title to the goods remains with the seller until the goods reach the buyer.

6. Under a consignment arrangement, the holder of the goods (called the consignee) does not own the goods. Ownership remains with the shipper of the goods (consignor) until the goods are actually sold to a customer. Consigned goods should be included in the consignor's inventory—not the consignee's inventory.

Inventory Costing

7. (L.O. 2) After a company has determined the quantity of units of inventory, it applies unit costs to the quantities to determine the total cost of the inventory and the cost of goods sold.

Specific Identification

8. The specific identification method identifies the particular units sold so that the cost of the specific unit sold is charged to the cost of goods sold. This method is possible when a company sells a limited variety of high unit-cost items that can be clearly identified from the time of purchase through the time of sale.

9. The allocation of inventoriable costs may be made under any of the following assumptions as to the flow of costs (a) first-in, first-out (FIFO), (b) last-in, first-out (LIFO), or (c) average cost.

FIFO

10. The FIFO method assumes that the costs of the earliest goods purchased are the first to be sold.

a. This method often parallels the actual physical flow of the merchandise.

b. Under this method, the ending inventory is based on the latest units purchased.

LIFO

11. The LIFO method assumes that the costs of the latest units purchased are the first to be sold.

a. This method seldom coincides with the actual physical flow of inventory.

b. Under this method, all goods purchased during the period are assumed to be available for the first sale, regardless of the date of purchase.

c. The ending inventory is found by taking the unit cost of the oldest goods and working forward until all units of inventory are costed.

Average Cost

12. The average cost method assumes that the goods available for sale are similar in nature.

a. Under this method, the cost of goods available for sale is allocated on the basis of weighted average unit cost.

b. The formula for determining the weighted average unit cost is: Cost of goods available for sale divided by total units available for sale.

Financial Statement Effects

13. (L.O. 3) In periods of rising prices, FIFO produces a higher net income, LIFO the lowest, and average cost falls in the middle. The reverse is true when prices are falling.

14. Companies adopt different inventory costing methods because of:

a. Balance sheet effects: the inventory costs are closer to current costs under FIFO than under LIFO.

b. Income statement effects: in addition to the effects on net income in (13) above, LIFO enables the company to avoid reporting paper or phantom profit as economic gain.

c. Tax effects: in a period of inflation LIFO results in the lowest income taxes.

Lower of Cost or Market

15. (L.O. 4) When the value of inventory is lower than its cost, the inventory is written down to its market value. This is known as the lower of cost or market (LCM) method.

16. Market is measured by the current replacement cost of the goods, not selling price.

17. (L.O. 5) The effects of inventory errors on the current year's income statement are:

18. The effects of ending inventory errors on the balance sheet are:

19. In the financial statements:

a. Inventory is usually classified as a current asset after receivables in the balance sheet, and cost of goods sold is subtracted from sales in the income statement.

b. There should be disclosure of (1) the major inventory classifications, (2) the basis of accounting, and (3) the costing method.

Inventory Turnover Ratio

20. (L.O. 6) The inventory turnover ratio measures the number of times on average the inventory is sold during the period.

Cost of Goods Sold ÷ Average Inventory = Inventory Turnover

*Applying Perpetual Inventory

*21. (L.O. 7) Each of the inventory cost flow methods may be used in a perpetual inventory system.

a. Under FIFO, the cost of the earliest goods on hand prior to each sale is charged to cost of goods sold.

b. Under the LIFO method, the most recent purchase prior to sale is allocated to the units sold.

c. When the moving average method is used, a new average is computed after each purchase by dividing the cost of goods available for sale by the units on hand.

Estimating Inventories

*22. (L.O. 8) Inventories may have to be estimated when (a) management wants monthly or quarterly financial statements or (b) a fire or other type of casualty makes it impossible to take a physical inventory.

*23. The gross profit method is widely used to estimate the ending inventory. Two steps are involved in using this method.

a. The estimated cost of goods sold is determined by subtracting the estimated gross profit from net sales.

b. The estimated cost of goods sold is subtracted from cost of goods available for sale to determine the estimated cost of the ending inventory.

Retail Inventory Method

*24. The retail inventory method is used by retail companies to estimate the cost of the inventory. The steps in using this method are:

A Look at IFRS

*25. (L.O. 9) The requirement for accounting for and reporting inventories are more principles – based under IFRS than GAAP which provides more detailed guidelines.

*26. IFRS and GAAP are similar with respect to defining inventory, determines who owns the goods, as well as costs to include in inventory.

*27. IFRS requires the specific identification method where inventory items are not interchangeable, GAAP does not specify situations in which specific identification must be used.

*28. GAAP permits the use of LIFO for inventory valuation, while IFRS prohibits its use. Only FIFO and average-cost are the two acceptable cash flow assumptions permitted under IFRS.

*29. IFRS requires companies to use the same cost flow assumption for all goods of a similar natures while GAAP has no specific requirements.

*30. In the lower-of-cost-or-market test for inventory valuation, IFRS defines market as net realizable value, while GAAP defines it as essentially replacement cost.

*31. Unlike property, plant, and equipment, IFRS does not permit the option of valuing inventories at fair value.

![]()

![]()

![]()

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

![]()

MULTIPLE CHOICE

Circle the letter that best answers each of the following statements.

- (L.O. 1) Inventory items on an assembly line in various stages of production are classified as:

- Finished goods.

- Work in process.

- Raw materials.

- Merchandise inventory.

- (L.O. 1) L. Pasteur Company's inventory at December 31, 2014, was $300,000 based on a physical count of goods made on December 31. The following items were in transit:

*Goods costing $5,000 were shipped FOB shipping point on December 29, 2014 to a customer and received by the customer on January 3, 2013.

*Goods costing $10,000 were shipped FOB destination on December 30, 2014 to a customer and received by the customer on January 4, 2015.

What amount should L. Pasteur report as inventory on its December 31, 2014 balance sheet?

- $290,000.

- $305,000.

- $310,000.

- $315,000.

- (L.O. 2) Rudolf Diesel Company's inventory records show the following data:

A physical inventory on December 31 shows 8,000 units on hand. Under the FIFO method, the December 31 inventory is:

- $56,000.

- $58,000.

- $64,000.

- $72,000.

- (L.O. 2) Fermat Company had 300 units of inventory on hand at January 1 costing $32 each. Purchases during the month of January were as follows:

A physical count on January 31 shows 450 units on hand. The cost of the inventory at January 31 under the LIFO method is:

- $15,400.

- $14,900.

- $14,550.

- $14,400.

Items 5 and 6 are based on the following data:

Sig Freud Bookstore had 200 electric pencil sharpeners on hand at January 1, costing $18 each. Purchases and sales of electric pencil sharpeners during the month of January were as follows:

Sig Freud does not maintain perpetual inventory records. According to a physical count, 150 electric pencil sharpeners were on hand at January 31.

- (L.O. 2) The cost of the inventory at January 31, under the FIFO method is:

- $400.

- $2,700.

- $3,100.

- $3,200.

- (L.O. 2) The cost of the inventory at January 31, under the LIFO method is:

- $400.

- $2,700.

- $3,100.

- $3,200.

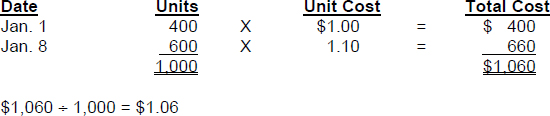

- (L.O. 2) Ampere Company recorded the following data:

The weighted average unit cost of the inventory at January 31 is:

- $1.00.

- $1.05.

- $1.06.

- $1.10.

- (L.O. 3) In a period of rising prices, FIFO will have a

- lower net income than LIFO.

- lower cost of goods sold than LIFO.

- lower income tax expense than LIFO.

- lower net purchases than LIFO.

- (L.O. 3) In a period of inflation, the use of the LIFO method will result in:

- a more realistic inventory value than FIFO.

- a better matching of costs and revenues than FIFO.

- higher income taxes than FIFO.

- higher net income than FIFO.

Items 10 and 11 are based on the following data:

Langmuir, Inc. has 5 personal computers which have been part of the inventory for over two years. Each personal computer cost $800 and originally retailed for $1,100. At the statement date, each personal computer has a current replacement cost of $450.

10. (L.O. 4) What value should Langmuir, Inc., have for the personal computers at the end of the year balance sheet?

a. $1,750.

b. $2,250.

c. $4,000.

d. $5,500.

11. (L.O. 4) How much loss should Langmuir, Inc., record the for year ended?

a. $1,500.

b. $1,750.

c. $1,800.

d. $2,250.

12. (L.O. 5) On December 31, 2014, Cavendish, Inc. overstated its ending inventory by $4,000. Assuming no correcting entry was made, the effects on the following 2015 income statement items are :

13. (L.O. 5) Euler Company made an inventory count on December 31, 2014. During the count, one of the clerks made the error of counting an inventory item twice. For the balance sheet at December 31, 2014, the effects of this error are:

Items *14-*16 relate to the perpetual inventory system of the Zollmer Company. During May, the following purchases and sales were made for Product X298. There was no beginning inventory.

*14. (L.O. 7) Under the FIFO method, the cost of goods sold for each sale is:

*15. (L.O. 7) Under the LIFO method, the cost of goods sold for each sale is:

*16. (L.O. 7) Under the average cost method, the cost of goods sold for each sale is:

*17. (L.O. 8) Doppler Company wishes to prepare an income statement for the month of March when its records show Net Sales, $300,000; Beginning Inventory, $59,000; and Cost of Goods Purchased, $155,000. The company realizes a 30% gross profit rate. The estimated cost of the ending inventory at March 31 under the gross profit method is:

a. $4,000.

b. $55,000.

c. $63,000.

d. $72,000.

*18. (L.O. 8) Oppenheimer Company's records indicate the following information for the year:

| Merchandise inventory, 1/1 | $ 550,000 |

| Purchases | 2,250,000 |

| Net Sales | 3,000,000 |

On December 31, a physical inventory determined that ending inventory of $600,000 was in the warehouse. Oppenheimer's gross profit on sales has remained constant at 30%. Oppenheimer suspects some of the inventory may have been taken by some new employees. At December 31, what is the estimated cost of missing inventory?

a. $100,000.

b. $200,000.

c. $300,000.

d. $700,000.

Items *19 and *20 are based on the following data: On December 31, Gottlieb Retailers has the following information under the retail inventory method.

*19. (L.O. 8) The cost to retail ratio is:

a. 71%.

b. 78%.

c. 75%.

d. 80%.

*20. (L.O. 8) The estimated cost of the ending inventory is:

a. $41,210.

b. $45,286.

c. $43,500.

d. $22,500.

![]()

Match each term with its definition by writing the appropriate letter in the space provided.

![]()

EX. 6-1 (L.O. 2) On January 1, Fermi Company had a beginning inventory of 200 units that cost $30 each. The following purchases were made during the year.

Fermi Company uses a periodic inventory system. The count of the ending inventory was 500 units at December 31.

Instructions

Compute the cost of the ending inventory and the cost of goods sold for Fermi Company for the year ended December 31 for each of the following methods: (a) FIFO, (b) LIFO, and (c) average cost (round to two decimals)

*EX. 6-2 (L.O. 8) The records of A.G. Bell Company show the following data for the month of October:

| Net sales | $230,000 |

| Inventory at cost, October 1 | 122,500 |

| Inventory at retail, October 1 | 175,000 |

| Goods purchased at cost | 149,600 |

| Goods purchased at retail | 220,000 |

Instructions

(a) Using the retail inventory method, compute the estimated cost of the inventory at October 31. (Round to two decimals.)

(b) Assuming a gross profit rate of 30%, compute the estimated cost of the inventory at October 31 using the gross profit method.

(a)

(b)

![]()

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

| 1. (F) | Merchandise inventory has two common characteristics: (1) it is owned by the company and (2) it is in a form ready for sale to customers in the ordinary course of business. |

| 2. (T) | |

| 3. (T) | |

| 4. (F) | Under the terms, FOB destination, legal title to the goods remains with the seller until the goods are delivered to the buyer by the transportation company. |

| 5. (F) | The primary basis of accounting for inventories is cost. |

| 6. (T) | |

| 7. (T) | |

| 8. (T) | |

| 9. (T) | |

| 10. (T) | |

| 11. (F) | Under the lower of cost or market basis, market is defined as current replacement cost, not selling price. |

| 12. (T) | |

| 13. (F) | This basis may also be applied to major categories of inventory or to total inventory. |

| 14. (F) | If beginning inventory is overstated, net income will be understated in the same year. |

| 15. (T) | |

| *16. (F) | The cost of goods sold is based on the earliest goods on hand prior to the sale. |

| *17. (T) | |

| *18. (T) | |

| *19. (F) | The cost to retail ratio is applied to the ending inventory at retail. |

| *20. (T) |

MULTIPLE CHOICE

MATCHING

- g

- a

- b

- d

- c

- e

- i

- f

- j

- h

EX. 6-1

For each of the inventory methods, the number of units available for sale and cost of goods available for sale should be computed as follows: