Chapter 7

ACCOUNTING INFORMATION SYSTEMS

CHAPTER LEARNING OBJECTIVES

After studying this chapter, you should be able to:

1. Identify the basic concepts of an accounting information system.

2. Describe the nature and purpose of a subsidiary ledger.

3. Explain how companies use special journals in journalizing.

*4. Indicate how companies post a multi-column journal.

*5. Compare the procedures for accounting information systems under GAAP and IFRS.

![]()

PREVIEW OF CHAPTER 7

Whether you use pen, pencil, or computers in maintaining accounting records, certain principles and procedures apply. The purpose of this chapter is to explain and illustrate these features. The content and organization of this chapter are as follows:

![]()

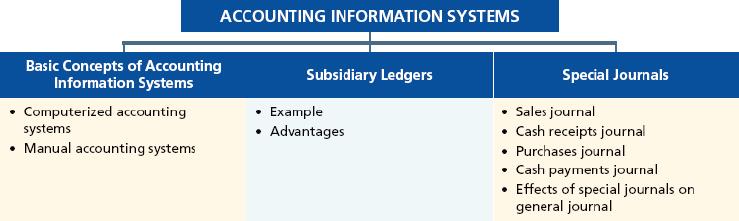

Accounting Information Systems

- (L.O. 1) An accounting information system involves collecting and processing data and disseminating financial information to decision makers. It includes each step of the accounting cycle.

- The basic principles of an accounting information system are:

- Cost effectiveness. The system must be cost effective--the benefits of the information disseminated must outweigh the cost of providing it.

- Usefulness. To be useful the information must be understandable, relevant, reliable, timely, and accurate.

- Flexibility. The system should be able to accommodate a variety of users and changing information needs.

Computerized Accounting Systems

3. General ledger accounting systems are software programs that integrate the various accounting functions related to sales, purchases, receivables, payables, cash receipts and disbursements, and paycoll. They also generate financial statements.

4. Companies with revenues of less than $5 million and up to 20 employees generally use entry-level programs. Quality entry-level packages include easy data access and report preparation, provide an “audit trail,” have internal controls, enable customization, and provide network-compatibility.

5. Enterprise resource planning (ERP) systems are typically used by manufacturing companies with more than 500 employess and $500 million in sales. ERP systems go far beyond the functions of an entry-level general ledger package by integrating all aspects of the organization, including accounting, sales, human resource management, and manufacturing.

Manual Systems

6. In a manual accounting system, each of the steps in the accounting cycle is performed by hand.

Subsidiary Ledgers

7. (L.O. 2) A subsidiary ledger is a group of accounts with a common characteristic, assembled together to facilitate the recording process by freeing the general ledger from details concerning individual balances.

8. Two common subsidiary ledgers are:

a. The accounts receivable (or customers') ledger which collects transaction data with individual customers.

b. The accounts payable (or creditors') ledger which collects transaction data with individual creditors.

9. The summary account in the general ledger is called a control account and the balance in the control account must equal the composite balance of the individual accounts in the subsidiary ledger at the end of the period.

10. The advantages of using subsidiary ledgers are that they:

a. Show transactions affecting one customer or one creditor in a single account, thus providing up-to-date information on specific account balances.

b. Free the general ledger of excessive details. As a result, a trial balance of the general ledger does not contain vast numbers of individual account balances.

c. Help locate errors in individual accounts by reducing the number of accounts in one ledger and by using control accounts.

d. Make possible a division of labor in posting by having one employee post to the general ledger while a different employee(s) post to the subsidiary ledgers.

Special Journals

11. (L.O. 3) To expedite journalizing and posting transactions, most companies use special journals in addition to the general journal. A special journal is used to group similar types of transactions, such as all sales of merchandise on account or all cash receipts.

12. The following are types of special journals:

a. Sales journal—all sales of merchandise on account.

b. Cash receipts journal—all cash received (including cash sales).

c. Purchases journal—all purchases of merchandise on account.

d. Cash payments journal—all cash paid (including cash purchases).

13. If a transaction cannot be recorded in a special journal, it is recorded in the general journal. Special journals permit greater division of labor and reduce the time necessary to complete the posting process.

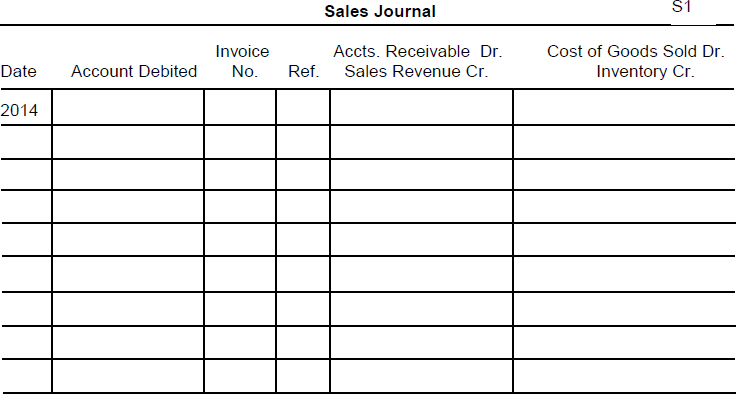

Sales Journal

14. For the sales journal,

a. Each entry results in a debit to Accounts Receivable and a credit to Sales Revenue at selling price; and a debit to Cost of Goods Sold and a credit to Inventory at cost.

b. Only one line is needed to record each transaction.

c. All entries are made from sales invoices.

d. Postings are made daily to the individual accounts receivable in the subsidiary ledger and monthly, in total, to Accounts Receivable, Sales Revenue, Cost of Goods Sold and Inventory in the general ledger.

Cash Receipts Journal

15. The cash receipts journal is a columnar journal with debit columns for cash and sales discounts, and credit columns for accounts receivable, sales, and “other” accounts. In addition there is a separate column for a debit to Cost of Goods Sold and a credit to Inventory. In journalizing cash receipts transactions:

a. Only one line is needed for each entry.

b. Each sale entry is accompanied by another entry that debits Cost of Goods Sold and credits Inventory for cost.

*16. (L.O. 4) The posting of a columnar journal such as the cash receipts journal involves the following procedures:

a. All column totals except the total for the Other Accounts column are posted once at the end of the month to the account title or titles specified in the column heading.

b. The total of the Other Accounts column is not posted. Instead, the individual amounts comprising the total are posted separately to the general ledger accounts specified in the Accounts Credited column.

c. The individual amounts in a column, posted in total to a control account, are posted daily to the subsidiary ledger account specified in the Accounts Credited column.

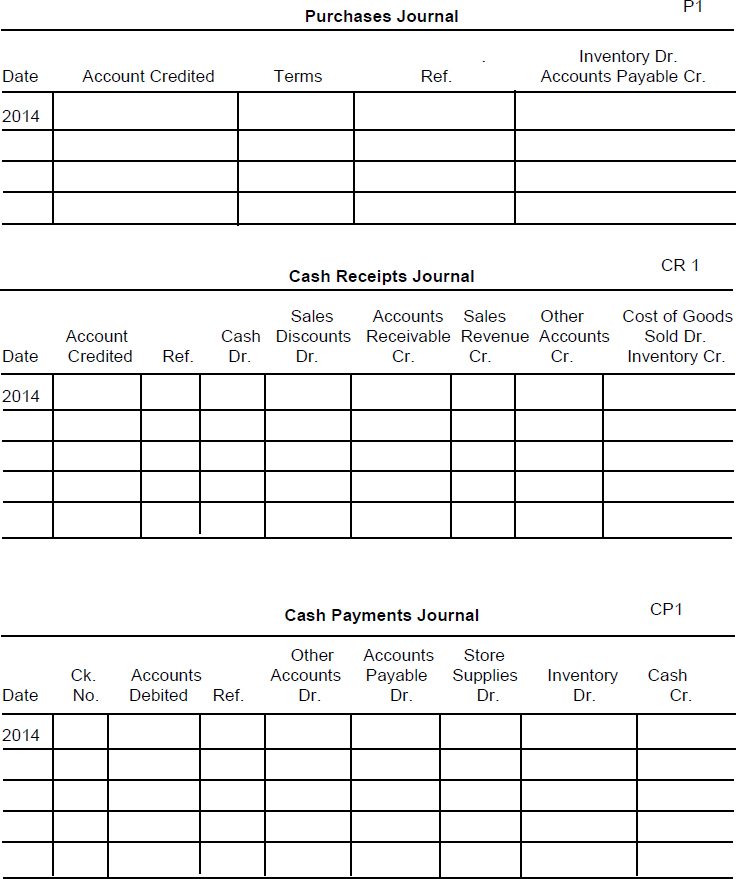

Purchases Journal

*17. For the purchases journal,

a. Each entry results in a debit to Inventory and a credit to Accounts Payable.

b. Only one line is needed to record each transaction.

c. All entries are made from purchase invoices.

d. Postings are made daily to the individual creditor accounts in the accounts payable subsidiary ledger and monthly, in total, to Inventory and Accounts Payable in the general ledger.

*18. The purchases journal can be expanded into a columnar journal by adding columns for office supplies, store supplies, and other accounts.

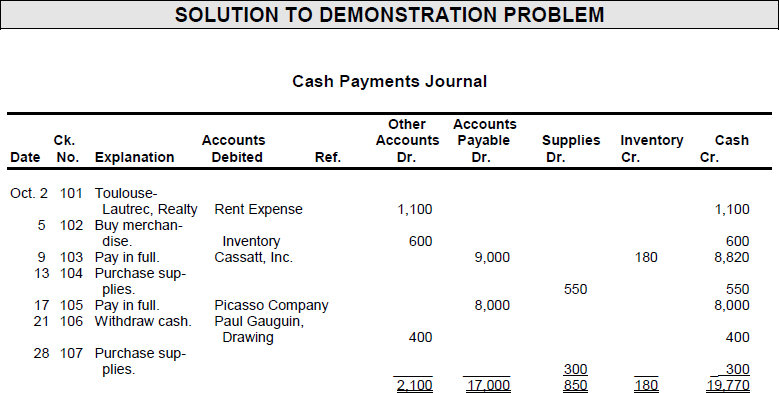

Cash Payments Journal

*19. The cash payments journal has multiple columns because cash payments may be made for a variety of purposes.

a. The journalizing procedures are similar to those described earlier for the cash receipts journal.

b. All entries are made from prenumbered checks.

c. The posting procedures are similar to those described earlier for the cash receipts journal.

Effects of Special Journals on the General Journal

*20. Only transactions that cannot be entered in a special journal are recorded in the general journal. When the entry involves both control and subsidiary accounts the following modifications are required:

a. In journalizing, both the control and subsidiary accounts must be identified.

b. In posting, there must be a dual posting to the control account and subsidiary account.

A Look at IFRS

*21. The basic concepts related to an accounting information system, the use of subsidiary ledgers and control accounts, as well as the system for recording transactions, are the same under GAAP and IFRS.

*22. The overriding principle in converting to IFRS is full retrospective application of IFRS.

*23. When a company converts to IFRS, it must decide on a transition date and a reporting date.

![]()

![]()

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

![]()

MULTIPLE CHOICE

Circle the letter that best answers each of the following statements.

- (L.O. 1) Which of the following statements is incorrect?

- A major consideration in developing an accounting system is cost awareness.

- When an accounting system is designed, no consideration needs to be given to the needs and knowledge of the various users.

- The accounting system should be able to accommodate a variety of users and changing information needs.

- To be useful, information must be understandable, relevant, reliable, timely, and accurate.

- (L.O. 2) Which of the following accounts may a business not use as a controlling account and subsidiary ledger?

- Inventory.

- Accounts Payable.

- Selling and Administrative Expenses.

- A business may use all of the above as controlling accounts and subsidiary ledgers.

- (L.O. 2) Which of the following is not an advantage of a subsidiary ledger?

- Shows transactions affecting one customer or one creditor in a single account.

- Help locate errors in individual accounts.

- Puts greater detail in the general ledger.

- Makes possible a division of labor.

- (L.O. 3) Which of the following is a journal that most merchandising enterprises will not use?

- Cash payments journal.

- Purchases journal.

- Sales journal.

- Equipment journal.

- (L.O. 3) When the totals of the sales journal are posted at the end of the month there will be credits to:

- Sales Revenue and Inventory and debits to Accounts Receivable and Cost of Goods Sold.

- Accounts Receivable and Cost of Goods Sold and debits to Sales Revenue and Inventory.

- Sales Revenue and debits to each individual customer account.

- the Sales Revenue account only, and no debits.

- (L.O. 3) The entries in the sales journal must be posted daily to the:

- Sales Revenue Account.

- Accounts Receivable subsidiary ledger.

- the Accounts Payable subsidiary ledger.

- none of the above.

- (L.O. 3) A cash receipts journal will be used for:

- (L.O. 3) Which of the following transactions will not involve the cash receipts journal?

- Cash sales of merchandise totaling $2,000.

- Cash is received by signing a note for $3,000.

- The owner makes a cash investment in the business.

- A company gives a purchase refund to a purchaser following a cash purchase.

- (L.O. 3) The Other Accounts column of a columnar journal is often referred to as the:

- Sundry Accounts column.

- Controlling Account column.

- Credit Account column.

- Debit Account column.

- (L.O. 3) In the cash receipts journal, debits are made in which columns?

- Cash, Sales Discounts, and Cost of Goods Sold.

- Accounts Receivable, Cash, and Cost of Goods Sold.

- Sales Discounts, Sales Revenue, and Inventory.

- Accounts Receivable, Sales Revenue, and Inventory.

*11. (L.O. 4) The purchases journal will include:

*12. (L.O. 4) In the expanded purchases journal, debits are made in which columns?

a. Accounts Payable, Inventory, and Supplies.

b. Inventory, and Supplies.

c. Cash, and Supplies.

d. Accounts Payable, Cash, and Inventory.

*13. (L.O. 4) The cash payments journal may include a column for:

a. store supplies.

b. accounts receivable.

c. sales revenue.

d. sales discounts.

*14. (L.O. 4) If a customer returns goods for credit, an entry is normally made in the:

a. cash receipts journal.

b. sales journal.

c. cash payments journal.

d. general journal.

*15. (L.O. 4) If a customer takes a sales discount, an entry is made in the:

a. cash receipts journal.

b. sales journal.

c. cash payments journal.

d. general journal.

*16. (L.O. 4) Totaling the columns of a multi-column journal and proving the equality of the totals is called:

a. totaling and balancing.

b. footing and cross-footing.

c. totaling and cross-footing.

d. footing and balancing.

![]()

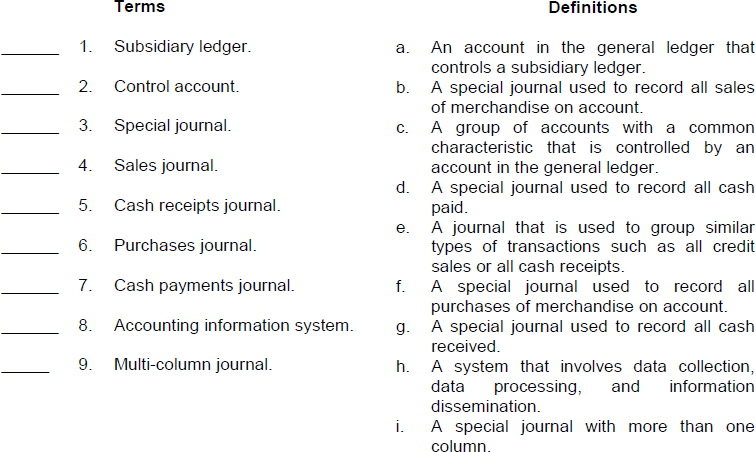

Match each term with its definition by writing the appropriate letter in the space provided.

![]()

EX. 7-1 (L.O. 3 and *4) Cartoonist Inc., had the following transactions during the month.

- Merchandise is sold on credit to Gary Trudeau for $2,500.

- Merchandise is sold to Charles Schulz for $1,000 cash.

- Merchandise purchased by Charlie Brown on account is returned for credit.

- A check for $2,940 is received from Al Capp in payment of invoice no. 101 for $3,000 less 2% discount.

- Merchandise is purchased on credit from Disney Company for $2,000, terms 1/20, n/30.

- Check no. 101 for $3,100 is issued for store supplies bought from Jim Davis.

- Check no. 102 for $1,980, $2,000 less the 1% discount is mailed to Disney Company to pay for merchandise purchased on credit.

- Merchandise is purchased for $1,000 (check no. 103) cash from Mary Worth.

- Equipment is purchased from Mort Walker for $4,000 on credit.

- Cash is received from R. Dagwood in payment of a $5,000 note receivable, plus $75 of accrued interest.

Instructions

(a) Indicate the journal in which each transaction should be entered using the following letters:

G = General journal

S = Sales journal

P = Purchases journal (one-column)

CR = Cash receipts journal

CP = Cash payments journal

(b) For each journal selected in (a) above, indicate by inserting a check mark in the appropriate column whether the journalized data should be posted (1) only at the end of the month, (2) daily and at the end of the month, or (3) only daily. (Note: Assume that the columnar journals have the same columns as those in the chapter and subsidiary and control accounts are used.)

*EX. 7-2 (L.O. 4) The following transactions were made by George Baker Company during the month of October 2014.

| Oct. 3 | Received a $3,000 payment from Chic Young in full for invoice no. 101 when terms were n/30. |

| 6 | Bought store supplies from Chester Gould Co. for $500—used check no. 101. |

| 9 | Purchased merchandise from Harold Gray Company for $3,500—used check no. 102. |

| 13 | Received $2,000 cash from Harold Gray Company as an allowance for defective goods purchased on Oct. 9. |

| 16 | Purchased merchandise from Hank Ketcham Company for $1,500 on credit. |

| 20 | Sold merchandise to Jack Kirby for $2,250 on credit—used sales invoice no. 10. The cost of goods sold was $1,600. |

| 23 | Purchased merchandise from Bob Montana, Inc. for $6,000 on credit. |

| 25 | Received $2,205 from Jack Kirby for the sale made on Oct. 20 less a 2% discount. |

| 27 | Paid Hank Ketcham Company $1,485 cash for the purchase on Oct. 16 less a 1% discount--used check no. 103. |

Instructions

In the journals provided, enter the transactions for the George Baker Company for the month ended October 31, 2014.

![]()

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

TRUE-FALSE

| 1. (T) | |

| 2. (F) | The last principle is flexibility, not fixed structure. |

| 3. (T) | |

| 4. (T) | |

| 5. (F) | The summary account in the general ledger is called a control account. |

| 6. (T) | |

| 7. (T) | |

| 8. (F) | A special journal is used to group similar types of transactions. |

| 9. (F) | If a transaction cannot be recorded in a special journal, it is recorded in the general journal. |

| 10. (F) | When special journals are employed, daily postings are usually made to the subsidiary ledgers and monthly postings to the general ledger. |

| 11. (F) | An advantage of the sales journal is that one-line entry for each sales transaction saves time. |

| 12. (F) | The column totals of the Sales journal are posted to the Sales Revenue account and the Accounts Receivable account, and the Cost of Goods Sold account and the Inventory account. |

| 13. (T) | |

| 14. (T) | |

| 15. (T) | |

| 16. (T) | |

| 17. (F) | Entries in the purchases journal are made from purchase invoices. Sales invoices are used to make entries in the sales journal. |

| 18. (T) | |

| 19. (F) | The total of the Other Accounts column is not posted because each individual transaction is posted to the appropriate account affected. |

| 20. (T) |

MULTIPLE CHOICE

- c

- a

- e

- b

- g

- f

- d

- h

- i.

EXERCISES

EX. 7-1

EX. 7-2