CHAPTER 8

LIMIT THEOREMS

The ability to draw conclusions about a population from a given sample and determine how reliable those conclusions are plays a crucial role in statistics. On that account it is essential to study the asymptotic behavior of sequences of random variables. This chapter covers some of the most important results within the limit theorems theory, namely, the weak law of large numbers, the strong law of large numbers, and the central limit theorem, the last one being called so as a way to assert its key role among all the limit theorems in probability theory (see Hernandez and Hernandez, 2003).

8.1 THE WEAK LAW OF LARGE NUMBERS

When the distribution of a random variable X is known, it is usually possible to find its expected value and variance. However, the knowledge of these two quantities do not allow us to find probabilities such as P (|X − c| > ∊) for ∊ > 0. In this regard, the Russian mathematician Chebyschev proved an inequality, appropriately known as Chebyschev’s inequality (compare with exercise 2.48 from Chapter 2), which offers a bound for such probabilities.

Even though in practice it is seldom used, its theoretical importance is unquestionable, as we will see later on.

Chebyschev’s inequality is a particular case of Markov’s inequality (compare with exercise 2.47 from Chapter 2), which we present next.

Lemma 8.1 (Markov’s Inequality) If X is a nonnegative random variable whose expected value exists, then, for all a > 0, we have:

Proof: Consider the random variable I defined by:

![]()

Since X ≥ 0, then ![]() , and taking expectations on both sides of this inequality we arrive at the desired expression.

, and taking expectations on both sides of this inequality we arrive at the desired expression. ![]()

From past experience, a teacher knows that the score obtained by a student in the final exam of his subject is a random variable with mean 75. Find an upper bound to the probability that the student gets the score greater than or equal to 85.

Solution: Let X be the random variable defined as follows:

X := “Score obtained by the student in the final exam”.

Since X is nonnegative, Markov’s inequality implies that:

P(X ≥ 85) ≤ 0.88235. ![]()

Suppose that X is a random variable having a binomial distribution with parameters 5 and ![]() . Use Markov’s inequality to find an upper bound to P(X ≥ 2). Compute P(X ≥ 2) exactly and compare the two results.

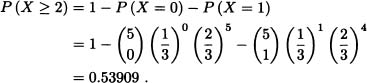

. Use Markov’s inequality to find an upper bound to P(X ≥ 2). Compute P(X ≥ 2) exactly and compare the two results.

Solution: We know that ![]() , and therefore, from Markov’s inequality:

, and therefore, from Markov’s inequality:

![]()

These results show that Markov’s inequality can sometimes give a rather rough estimate of the desired probability. ![]()

In many cases there is no specific information about the distribution of the random variable X and it is in those cases where Chebyschev’s inequality can offer valuable information about the behavior of the random variable.

Theorem 8.1 (Chebyschev’s Inequality) Let X be a random variable such that Var (X) < ∞. Then, for any ∊ > 0, we have:

![]()

Proof: Let Y := |X − E(X)|2 and a = ∊2. Markov’s inequality yields

which completes the proof. ![]()

Clearly, (8.2) is equivalent to:

![]()

Likewise, taking ∊ := σk, with k > 0 and ![]() , we obtain:

, we obtain:

![]()

If in (8.2) E(X) is replaced by a real number C, we obtain:

![]()

The above expression is also called “Chebyschev’s inequality” (see Meyer, 1970).

Note 8.1 In (8.1) and (8.2) we can replace P (X ≥ a) and P (|X − E(X)| ≥ ∊) with P (X > a) and P (|X − E(X)| > ∊), respectively, and the inequalities will still hold.

Is there any random variable X for which

where μX and σX are the expected value and standard deviation of X, respectively?

Solution: It follows from Chebyschev’s inequality that:

![]()

Hence, there cannot be a random variable X satisfying (8.3). ![]()

Show that if V ar (X) = 0, then P (X = E(X)) = 1.

Solution: Chebyschev’s inequality implies that for any n ≥ 1:

![]()

Taking the limit when n → ∞, we get:

In other words, P (X = E(X)) = 1 . ![]()

The weak law of large numbers can be obtained as an application of Chebyschev’s inequality. This is one of the most important results in probability theory and was initially demonstrated by Jacob Bernoulli for a particular case. The weak law of large numbers states that the expected value E(X) of a random variable X can be considered an “idealization”, for “large enough” n, of the arithmetic mean ![]() , where X1, · · ·, Xn are independent and identically distributed random variables with the same distribution of X.

, where X1, · · ·, Xn are independent and identically distributed random variables with the same distribution of X.

In order to state this law, we need the following concept:

Definition 8.1 (Identically Distributed Random Variables) Xl, X2, · · · is said to be a sequence of independent and identically distributed random variables if:

1. For any ![]() we have that X1, · · ·, Xn are independent random variables.

we have that X1, · · ·, Xn are independent random variables.

2. For any ![]() , Xi and Xj have the same distribution.

, Xi and Xj have the same distribution.

Note 8.2 The previous definition can be generalized to random vectors as follows: It is said that X1, X2, · · · is a sequence of independent and identically distributed random vectors if:

1. For any ![]() we have that X1, · · · , Xn are independent random vectors.

we have that X1, · · · , Xn are independent random vectors.

2. For any ![]() , Xi and Xj have the same distribution.

, Xi and Xj have the same distribution.

Theorem 8.2 (The Weak Law of Large Numbers (WLLN)) Let X1, X2, · · · be a sequence of independent and identically distributed random variables with mean μ and finite variance σ2. Then, for any ∊ > 0, we have that

![]()

from which we obtain that for any ∊ > 0:

![]()

Proof: Let ![]() be the arithmetic mean of the first n random variables. Clearly

be the arithmetic mean of the first n random variables. Clearly ![]() and V ar

and V ar ![]() . Chebyschev’s inequality implies that for any ∊ > 0 we must have:

. Chebyschev’s inequality implies that for any ∊ > 0 we must have:

![]()

which is exactly what we wanted to prove. ![]()

Note 8.3 It is possible to prove the weak law of large numbers without the finite variance hypothesis. That result, due to the Russian mathematician Alexander Khinchin (1894-1959), states the following [see Hernandez (2003) for a proof]:

If X1, X2, · · · is sequence of independent and identically distributed random variables with mean μ, then, for any ∊ > 0, we have that:

![]()

As a special case of the weak law of large numbers we obtain the following result:

Corollary 8.1 (Bernoulli’s Law of Large Numbers) Let X1, X2, · · · be a sequence of independent and identically distributed random variables having a Bernoulli distribution with parameter p. Then, for any ∊ > 0, we have

Proof: The weak law of large numbers implies that:

![]()

Since p ∈ (0,1), then ![]() and consequently (8.4) holds.

and consequently (8.4) holds. ![]()

Note 8.4 Bernoulli’s law states that when a random experiment with only two possible results, success or failure, is carried out for a number of times large enough, then, for any ∊ > 0, the set of results for which the proportion of successes is at a distance greater than ∊ of the probability of success p tends to zero. Observe that Bernoulli’s law does not assert that the relative frequency of successes converges to the success probability as the number of repetitions increases. Even when the latter is true, it cannot be directly inferred from Bernoulli’s law.

Note 8.5 Bernoulli’s law was proved by means of the weak law of large numbers, which in turn rests upon Chebyschev’s inequality. However, the original proof given by Bernoulli states that, for arbitrary ∊ > 0 and 0 < δ < 1, we have

![]()

where ![]() In

In ![]() For example, if ∊ = 0.03 and δ = 0.00002, then n ≥ 12416 implies:

For example, if ∊ = 0.03 and δ = 0.00002, then n ≥ 12416 implies:

![]()

That is, if the experiment is repeated at least 12,416 times, we can be at least 99.998% sure that the success ratio will be less than 3% away from the success probability p.

According to Hernandez (2003), Italian mathematician Francesco Paolo Cantelli (1875−1966) proved an even stronger result, namely, that if n ≥ ![]() In

In ![]() then

then

![]()

and thus, for ∊ = 0.03 and δ = 0.00002, n ≥ 42711 implies that:

![]()

8.2 CONVERGENCE OF SEQUENCES OF RANDOM VARIABLES

Let X, X1, X2, · · · be real-valued random variables all defined over the same probability space. In this section three important and common modes of convergence of the sequence ![]() to X will be defined. It is important, however, to clarify that there exist other modes of convergence different from those studied here (in this regard, see, Bauer, 1991).

to X will be defined. It is important, however, to clarify that there exist other modes of convergence different from those studied here (in this regard, see, Bauer, 1991).

Definition 8.2 (Convergence in Probability) Let X, X1, X2, · · · be realvalued random variables defined over the same probability space ![]() . It is said that

. It is said that ![]() converges in probability to X and write

converges in probability to X and write

![]()

if, for any ∊ > 0, the following condition is met:

![]()

Note 8.6 Making use of the last definition, we can express the weak law of large numbers as follows: If X1, X2, · · · is a sequence of independent and identically distributed random variables with mean μ and finite variance σ2, then

![]()

where ![]() represents the arithmetic mean of the first n random variables.

represents the arithmetic mean of the first n random variables.

Let ![]() be a sequence of random variables such that

be a sequence of random variables such that ![]() and

and ![]() for n = 1,2, · · ·. Let ∊ > 0.

for n = 1,2, · · ·. Let ∊ > 0.

Then:

![]()

Therefore:

![]()

Thus:

![]()

A fair dice is thrown once. For each n = 1,2, · · ·, we define the random variable Xn by

![]()

and let X be the random variable given by:

![]()

Clearly, for all n = 1,2, · · ·, we have:

|Xn − X| = l.

Hence

![]()

and therefore:

![]()

A useful result to establish the convergence of a sequence of random variables is the following theorem, whose proof is omitted. We encourage the interested reader to see Jacod and Protter (2004) for a proof.

Theorem 8.3 Let X, X1, X2 · · · be real-valued random variables defined over the same probability space ![]() . Then

. Then ![]() if and only if the following expression holds:

if and only if the following expression holds:

![]()

Definition 8.3 (Convergence in Lr) Let X, X1, X2, · · · be real-valued random variables defined over the same probability space ![]() . Let r be a positive integer such that E (|X|r) < ∞ and E(|Xn|r) < ∀n. Then

. Let r be a positive integer such that E (|X|r) < ∞ and E(|Xn|r) < ∀n. Then ![]() if and only if the following expression holds:

if and only if the following expression holds:

![]()

Let X1, X2, · · · be a sequence of independent and identically distributed random variables with mean μ and finite variance σ2. Let

![]()

where Sn = X1 + · · · + Xn. Now:

Hence:

![]()

Consider Example 8.5. Since ![]() and

and ![]() for n = 1,2, · · ·, we get E(Xn) = 1. Hence,

for n = 1,2, · · ·, we get E(Xn) = 1. Hence, ![]() whereas

whereas ![]() .

. ![]()

Theorem 8.4 Let r > 0, X, X1, X2,· · · be a sequence of random variables such that ![]() . This implies

. This implies ![]() .

.

Proof: Chebyschev’s inequality implies that for any ∊ > 0 we must have:

![]()

Hence, the proof. ![]()

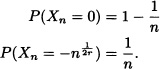

Let ![]() where

where ![]() is the Borel σ-algebra on [0,1] and

is the Borel σ-algebra on [0,1] and ![]() ([0,1]) is the Lebesgue measure on [0,1]. Let

([0,1]) is the Lebesgue measure on [0,1]. Let

![]()

![]()

That is, ![]() . But:

. But:

![]()

Another mode of convergence that will be covered in this section is almost sure convergence, a concept defined below.

Definition 8.4 (Almost Sure Convergence) Let X, X1, X2, · · · be real-valued random variables defined over the same probability space ![]() . We say that

. We say that ![]() converges almost surely (or with probability 1) to X and write

converges almost surely (or with probability 1) to X and write

![]()

if the following condition is met:

![]()

In other words, if ![]() , then:

, then:

![]() if and only if p (A) = 1.

if and only if p (A) = 1.

Let ![]() be an arbitrary probability space and let (Xn)n be the sequence random variables defined over

be an arbitrary probability space and let (Xn)n be the sequence random variables defined over ![]() as follows:

as follows:

![]()

Clearly, for all ![]() , we have:

, we have:

![]()

Therefore,

![]()

which implies:

![]()

8.3 THE STRONG LAW OF LARGE NUMBERS

The following result, known as the strong law of large numbers, states that the average of a sequence of independent and identically distributed random variables converges, with probability 1, to the mean of the distribution.

The proof of this law requires the following lemma [see Jacod and Protter (2004) for a demonstration]:

Lemma 8.2 Let X1,X2, · · · be a sequence of random variables. We have that:

1. If all the random variables Xi are positive, then

where the expressions in (8.5) are either both finite or both infinite.

2. If ![]() , then

, then ![]() converges almost surely and (8.5) holds.

converges almost surely and (8.5) holds.

Theorem 8.5 (The Strong Law of Large Numbers (SLLN)) Let X1,X2,· · · be a sequence of independent and identically distributed random variables with finite mean μ and finite variance σ2. Then:

![]()

Proof: (Jacod and Protter, 2004) Without loss of generality, we can assume that μ = 0.

Since ![]() ,

,

and E (XjXk) = 0 for j ≠ k, then (9.7) equals:

Therefore:

![]()

![]()

From Lemma 8.2, we have

![]() with probability 1

with probability 1

and consequently lim ![]() with probability 1.

with probability 1.

Let ![]() and kn be an integer such that:

and kn be an integer such that:

![]() .

.

Then

![]() ,

,

so that:

.

.

Accordingly,

and another application of Lemma 8.2 yields

with probability 1

with probability 1

from which:

![]() with probability 1.

with probability 1.

Since lim ![]() and

and ![]() , then, with probability 1, we conclude that

, then, with probability 1, we conclude that ![]() , which completes the proof for the case μ = 0. If μ ≠ 0, it suffices to consider the random variables defined, for i = 1,2, · · ·, by

, which completes the proof for the case μ = 0. If μ ≠ 0, it suffices to consider the random variables defined, for i = 1,2, · · ·, by

Zi := Xi – μ

and apply the result to the sequence thus obtained. ![]()

The last mode of convergence presented in this text, known as convergence in distribution, is most widely used in applications.

Definition 8.5 (Convergence in Distribution) Let X, X1, X2, · · · be realvalued random variables with distribution functions F, F1, F2, · · ·, respectively. It is said that ![]() converges in distribution to X, written as

converges in distribution to X, written as

![]()

if the following condition holds:

![]() for any point x where F is continuous

for any point x where F is continuous

or, equivalently,

![]() if and only if

if and only if ![]()

for any point x where F is continuous.

Note that convergence in distribution, just like the other modes of convergence previously discussed, reduces itself to the convergence of a sequence of real numbers and not to the convergence of a sequence of events.

Let ![]() be a probability space,

be a probability space, ![]() be the sequence of random variables over

be the sequence of random variables over ![]() defined as

defined as

![]()

and X = 0. Assume:

![]()

In other words:

![]()

Note 8.7 If X, X1, X2, · · ·are random variables with values in ![]() , then:

, then:

![]() X if and only if

X if and only if ![]() for all

for all ![]() .

.

The following theorem relates convergence in distribution with convergence of the characteristic functions. Its proof is beyond the scope of this text and the reader may refer to Hernandez (2003) or Rao (1973).

Theorem 8.6 (Lévy and Cramer Continuity Theorem) Let X, X1, X2,· · ·be real-valued random variables defined over the same probability space ![]() and having the characteristic functions

and having the characteristic functions ![]() · · · respectively. Then:

· · · respectively. Then:

![]() if and only if

if and only if ![]() for all

for all ![]() .

.

We proceed now to establish the major links between the convergence modes defined so far, namely, we will see that:

![]() .

.

Theorem 8.7 Let X, X1, X2, · · · be real-valued random variables defined over the same probability space ![]() . Then:

. Then:

![]() .

.

Proof: Let ∊ > 0. The sets

![]()

form an increasing sequence of events whose union

![]()

contains the set

![]()

By hypothesis P(A) = 1, from which we infer that P (A∞) = 1. On the other hand, it follows from the continuity of P that:

![]()

Since

![]()

and

![]()

we conclude that:

![]()

![]()

Theorem 8.8 Let X, X1, X2, · · · be real-valued random variables defined over the same probability space ![]() with distribution functions F, F1, F2, · · · respectively. Then:

with distribution functions F, F1, F2, · · · respectively. Then:

![]() .

.

Proof: Let x be a point of continuity of F. We need to prove that ![]() . Since F is continuous at x, then, for any ∊ > 0, there exists a δ > 0 0 such that:

. Since F is continuous at x, then, for any ∊ > 0, there exists a δ > 0 0 such that:

.

.

On the other hand, since ![]() , then there exists

, then there exists ![]() such that, for n ≥ n (∊), the following condition is satisfied:

such that, for n ≥ n (∊), the following condition is satisfied:

![]() .

.

Furthermore, we have that:

![]() .

.

Analogously:

![]() .

.

Figure 8.1 Relationship between the different modes of convergence

Thus:

That is, for all n ≥ n(![]() ), we have that

), we have that

![]()

and consequently:

![]()

Note 8.8 The converse of the above theorem is not, in general, true. Consider, for example, the random variables given in Example 8.6. In that case, we have ![]() , but

, but ![]() .

.

Figure 8.1 summarizes the relationship between the different modes of convergence. In this figure, the dotted arrow means that the convergence in probability does not imply the convergence in almost surely. However, we can prove that there is a subsequence of the original sequence that converges almost surely.

All the definitions given so far can be generalized to random vectors in the following way:

Definition 8.6 (Convergence of Random Vectors) Let X, X1, X2, · · · be k-dimensional random vectors, ![]() , having the distribution functions Fx, Fx1, Fx2, · · ·, respectively. Then, it is said that:

, having the distribution functions Fx, Fx1, Fx2, · · ·, respectively. Then, it is said that:

1. ![]() converges in probability to X, written as

converges in probability to X, written as ![]() , if the ith component of Xn converges in probability to the ith component of X. for each i = 1,2, · · ·, k.

, if the ith component of Xn converges in probability to the ith component of X. for each i = 1,2, · · ·, k.

2. ![]() converges almost surely (or with probability 1) to X, written as

converges almost surely (or with probability 1) to X, written as ![]() , if the ith component of Xn converges almost surely to the ith component of X for each i = 1, 2, · · ·, k.

, if the ith component of Xn converges almost surely to the ith component of X for each i = 1, 2, · · ·, k.

3. ![]() converges in distribution to X, written as

converges in distribution to X, written as ![]() , if limn → ∞FXn(x) = FX(x) for all points

, if limn → ∞FXn(x) = FX(x) for all points ![]() of continuity of FX (·).

of continuity of FX (·).

8.4 CENTRAL LIMIT THEOREM

This section is devoted to one of the most important results in probability theory, the central limit theorem, whose earliest version was first proved in 1733 by the French mathematician Abraham DeMoivre. In 1812 Pierre Simon Laplace, also a French mathematician, proved a more general version of the theorem. The version known nowadays was proved in 1901 by the Russian mathematician Liapounoff.

The central limit theorem states that the sum of independent and identically distributed random variables has, approximately, a normal distribution whenever the number of random variables is large enough and their variance is finite and different from zero.

Theorem 8.9 (Univariate Central Limit Theorem (CLT)) Let X1, X2, · · · be a sequence of independent and identically distributed random variables with mean μ and finite variance σ2. Let ![]() and Yn :=

and Yn := ![]() . Then, the sequence of random variables Y1, Y2, · · · converges in distribution to a random variable Y having a standard normal distribution. In other words:

. Then, the sequence of random variables Y1, Y2, · · · converges in distribution to a random variable Y having a standard normal distribution. In other words:

![]()

Proof: Without loss of generality, it will be assumed that μ = 0. Let ![]() be the characteristic function of the random variables X1, X2, · · ·. Since the random variables are independent and identically distributed, we have that:

be the characteristic function of the random variables X1, X2, · · ·. Since the random variables are independent and identically distributed, we have that:

Expansion of ![]() in a Taylor series about zero yields:

in a Taylor series about zero yields:

Thus:

Taking the limit when n → ∞ we get:

![]()

The Lévy-Cramer continuity theorem implies that

![]()

where Y is a random variable having a standard normal distribution. ![]()

Note 8.9 The de Moivre-Laplace theorem (4.6) is a particular case of the central limit theorem. Indeed, if X1, X2, · · · are independent and identically distributed random variables having a Bernoulli distribution of parameter p, then the conditions given in (8.9) are satisfied.

Note 8.10 Let X1, X2, · · · be a sequence of independent and identically distributed random variables with mean μ and finite positive variance σ2. The central limit theorem asserts that, for large enough n, the random variable ![]() has, approximately, a normal distribution with parameters nμ and nσ2.

has, approximately, a normal distribution with parameters nμ and nσ2.

Note 8.11 The central limit theorem can be applied to most of the classic distributions, namely: binomial, Poisson, negative binomial, gamma, Weibull, etc., since all of them satisfy the hypotheses required by the theorem. However, it cannot be applied to Cauchy distribution since it does not meet the requirements of the central limit theorem.

Note 8.12 There are many generalizations of the central limit theorem, among which the Lindenberg-Feller theorem stands out in that it allows for the sequence X1, X2, · · · of independent random variables with different means E(Xi) = μi and different variances ![]() .

.

Note 8.13 (Multivariate Central Limit Theorem) The central limit theorem can be generalized to sequences of random variables as follows:

Let X1, X2, · · · be a sequence of k-dimensional independent and identically distributed random vectors, with ![]() , having mean vector μ and variance- covariance matrix

, having mean vector μ and variance- covariance matrix ![]() , where

, where ![]() is positive definite. Let

is positive definite. Let

![]()

be the vector of arithmetic means. Then

![]()

where X is a k-dimensional random vector having a multivariate normal distribution with mean vector 0 and variance-covariance matrix ![]() . (See Hernandez, 2003).

. (See Hernandez, 2003).

Some applications of the central limit theorem are given in the examples below.

A fair dice is tossed 1000 times. Find the probability that the number 4 appears at least 150 times.

Solution: Let X := “Number of times that the number 4 is obtained”. We know that ![]() . Applying the de Moivre-Laplace theorem, we can approximate this distribution with a normal distribution of mean

. Applying the de Moivre-Laplace theorem, we can approximate this distribution with a normal distribution of mean ![]() and variance

and variance ![]() . Therefore:

. Therefore:

Suppose that for any student the time required for a teacher to grade the final exams of his probability course is a random variable with mean 1 hour and standard deviation 0.4 hours. If there are 100 students in the course, what is the probability that he needs more than 110 hours to grade the exam?

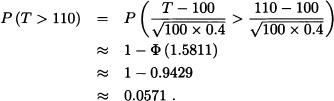

Solution: Let Xi be the random variable representing the time required by the teacher to grade the ith student of his course. We need to calculate the probability that ![]() greater than 110. By the central limit theorem, we have:

greater than 110. By the central limit theorem, we have:

(Wackerly et al., 2008) Many raw materials, like iron ore, coal and unrefined sugar, are sampled to determine their quality by taking small periodic samples of the material as it moves over a conveyor belt. Later on, the small samples are gathered and mixed into a compound sample which is then submitted for analysis. Let Yi be the volume of the ith small sample in a particular lot, and assume that Y1, Y2, · · ·, Yn is a random sample where each Yi has mean μ (in cubic inches) and variance σ2. The average volume of the samples can be adjusted by changing the settings of the sampling equipment. Suppose that the variance σ2 of the volume of the samples is approximately 4. The analysis of the compound sample requires that, with a 0.95 probability, n = 50 small samples give rise to a compound sample of 200 cubic inches. Determine how the average sample volume μ must be set in order to meet this last requirement.

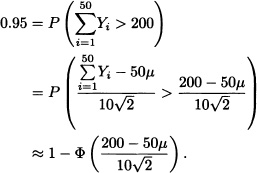

Solution: The random variables Y1, Y2, · · ·, Y50 are independent and identically distributed having mean μ and variance σ2 = 4. By the central limit theorem, ![]() has, approximately, a normal distribution with mean 50μ and variance 200. We wish to find μ such that

has, approximately, a normal distribution with mean 50μ and variance 200. We wish to find μ such that ![]() = 0.95. Accordingly:

= 0.95. Accordingly:

That is,

![]()

which in turn implies

![]()

from which we obtain:

![]()

EXERCISES

8.1 Suppose that 50 electronic components say D1, D2, · · ·, D50, are used in the following manner. As soon as D1 fails, D2 becomes operative. When D2 fails, D3 becomes operative, etc. Assume that the time to failure of Di is an exponentially distributed random variable with parameter 0.05 per hour. Let T be the total time of operation of the 50 devices. Compute the approximate probability that T exceeds 500 hours using the central limit theorem?

8.2 Let X1, X2, · · ·, Xn be n independent Poisson distributed random variables with means 1,2, · · ·, n, respectively. Find an x in terms of t such that

![]() for sufficiently large n

for sufficiently large n

where ![]() is the cdf of

is the cdf of ![]() (0,1).

(0,1).

8.3 Suppose that Xi, i = 1,2, · · ·, 450, are independent random variables each having a distribution ![]() (0,1). Evaluate

(0,1). Evaluate ![]() approximately.

approximately.

8.4 Let Y be a gamma distributed random variable with pdf

![]()

Find the limiting distribution of ![]() as p → ∞.

as p → ∞.

8.5 Let ![]() . Use the CLT to find n such that:

. Use the CLT to find n such that:

P[X > n/2] ≥ 1 − α.

Calculate the value of n when α = 0.90 and p = 0.45.

8.6 A fair coin is flipped 100 consecutive times. Let X be the number of heads obtained. Use Chebyschev’s inequality to find a lower bound for the probability that ![]() differs from

differs from ![]() by less than 0.1.

by less than 0.1.

8.7 Let X1, X2 · · ·, X50 be independent and identically distributed random variables having a Poisson distribution with mean 2.5. Compute:

![]()

8.8 (ChernofF Bounds) Suppose that the moment generating function mX(t) of a random variable X exists. Use Markov’s inequality to show that for any ![]() the following holds:

the following holds:

a) P(X ≥ a) ≤ exp(−ta) mX(t) for all t > 0.

b) P(X ≤ a) ≤ exp(−ta) mX(t) for all t < 0.

8.9 (Jensen Inequality) Let f be a twice-differentiable convex real-valued function, that is, f″ (x) ≥ 0 for all x. Prove that if X is a real-valued random variable, then

E(f(X)) ≥ f(E(X))

subject to the existence of the expected values.

Hint: Consider the Taylor polynomial of f about μ = E(X).

8.10 If X is a nonnegative random variable with mean 2, what can be said about E(X3) and E(In X).

8.11 Let X, X1, X2, · · · be real-valued random variables defined over the same probability space ![]() . Show the following properties about convergence in probability:

. Show the following properties about convergence in probability:

a) ![]() if and only if

if and only if ![]() .

.

b) If ![]() and

and ![]() , then P(X = Y) = 1.

, then P(X = Y) = 1.

c) If ![]() , then

, then ![]() .

.

d) If ![]() and

and ![]() , then

, then ![]() .

.

e) If ![]() and k is a real constant, then

and k is a real constant, then ![]() .

.

f) If ![]() and

and ![]() , then

, then ![]() .

.

8.12 Let X, X1, X2, · · · be real-valued random variables defined over the same probability space ![]() . Prove that:

. Prove that:

a) If ![]() and

and ![]() , then

, then ![]() .

.

b) If ![]() and

and ![]() , then

, then ![]() .

.

8.13 Let f be a continuous real-valued function and let X, X1, X2, · · · be real-valued random variables over the same probability space ![]() . Show that if

. Show that if ![]() , then

, then ![]() .

.

Note: The result still holds if almost sure convergence is replaced by convergence in probability.

8.14 Let X, X1, X2, · · · be real-valued random variables defined over the same probability space ![]() . Show that if

. Show that if ![]() , where k is a real constant, then

, where k is a real constant, then ![]() .

.

8.15 Suppose that a Bernoulli sequence has length equal to 100 with a success probability of p = 0.7. Let X := “Number of successes obtained”. Compute P(X ∈ [65,80]).

8.16 A certain medicine has been shown to produce allergic reactions in 1% of the population. If this medicine is dispensed to 500 people, what is the probability that at most 10 of them show any allergy symptoms?

8.17 A fair dice is rolled as many times as needed until the sum of all the results obtained is greater than 200. What is the probability that at least 50 tosses are needed?

8.18 A Colombian coffee exporter reports that the amount of impurities in 1 pound of coffee is a random variable with mean 3.4 mg and standard deviation 4 mg. In a sample of 100 pounds of coffee from this exporter, what is the probability that the sample mean is greater than 4.5 mg?

8.19 (Ross, 1998) Let X be a random variable having a gamma distribution with parameters n and 1. How large must n be in order to guarantee that:

![]()

8.20 How many tosses of a fair coin are needed so that the probability that the average number of heads obtained differs at most 0.01 from 0.5 is at least 0.90?

8.21 Let X be a nonnegative random variable. Prove:

![]()

8.22 Let (Xn)n≥1 be a sequence of random variables, and let c be a real constant verifying, for any ∊ > 0, the following condition:

![]()

Prove that for any bounded continuous function g we have that:

![]()

8.23 Examine the nature of convergence of {Xn} defined below for the different values of k for n = 1,2, · · · :

8.24 Show that the convergence in the rth mean does not imply almost sure convergence for the sequence {Xn} defined below:

8.26 Let ![]() be a sequence of random variables such that

be a sequence of random variables such that ![]() . Show that

. Show that ![]() .

.

8.27 For each n ≥ 1, let Xn be an uniformly distributed random variable over set ![]() , that is:

, that is:

![]()

Let U be a random variable with uniform distribution in the interval [0,1]. Show that ![]() .

.

8.28 Let ![]() be a sequence of i.i.d. random variables with E(X1) = V ar(X1) =

be a sequence of i.i.d. random variables with E(X1) = V ar(X1) = ![]() ∈ (0, ∞) and P(X1 > 0) = 1. Show that, for n → ∞ ,

∈ (0, ∞) and P(X1 > 0) = 1. Show that, for n → ∞ ,

![]()

where:

![]()

8.29 Let ![]() be a sequence of random variables such that

be a sequence of random variables such that ![]() . Show that

. Show that ![]() .

.

8.30 Let ![]() . Prove the following statements:

. Prove the following statements:

a) If ![]() is a sequence of random variables with

is a sequence of random variables with ![]() , then

, then ![]() with

with ![]() .

.

b) The sequence ![]() with

with ![]() converges in distribution but does not converge in probability to

converges in distribution but does not converge in probability to ![]() .

.

8.31 Let ![]() be a sequence of i.i.d. random variables with P(Xn = 1) = P(Xn = −1) =

be a sequence of i.i.d. random variables with P(Xn = 1) = P(Xn = −1) = ![]() . Show that

. Show that

![]()

converges in probability to 0.