Chapter 49

MANAGING WORKING CAPITAL

Is it supply chain management or is it strategy? It's finance, General!

On aggregate in Continental Europe, working capital represents large amounts (c. 15% on capital employed). Customer credits (and symmetrically, supplier credits), which are commercial loans between companies, amount to nearly three times the amount of short-term loans granted to corporates.

The similarity between the amount of working capital and that of net debt is not completely coincidental, as often these two items behave in concert. An increase in working capital means an increase in net debt, as a large number of companies can testify following their experiences in late 2020. A drop in working capital often means a drop in net debt, as a large number of companies can testify following their experiences in mid-2020.

Finally, the problems and the amounts of working capital are not identical for all sectors. There is a world of difference between industry (management of work-in-progress, credit limits for major customers, etc.) and the services sector.

Section 49.1 A BIT OF COMMON SENSE

Working capital is an investment, like any other, even if on occasion there is less choice involved (for example, when a customer “forgets” to pay by the due date and turns the supplier into its unwilling banker). As an investment, it should be managed lucidly and properly. Reducing it in order to reduce the company's need for funds and to improve its earnings is a possibility, but it is not the only possibility.

1/ THE NUMEROUS ASPECTS OF WORKING CAPITAL

From the company's point of view, what is working capital?

- First and foremost, it's part of commercial conquest. We all know that payment periods form part of the terms of a commercial contract. Try to set up a business in Greece, where contractual payment periods are 53 days with average periods often stretching to 69 days, by asking to be paid at 25 days like in the Netherlands! Similarly, keeping stock levels high reduces the risk of losing an order because supplies are not available. Consumers will remember the sense of annoyance and frustration felt in March of 2020 at the empty toilet paper shelves of a number of retailers.1

- Next, it's a source of financing when it reduces and a source of financing requirement when it increases. One might be tempted to assume that the stakes are not the same when the very short-term interest rates stand at 0% or even negative, as they did in 2016–2021, or at 10% per year, as they did between 1990 and 1993.2 This is a false assumption. The problem is not so much the cost of money as it is making money available by reducing working capital in order to invest, to repay debt or to constitute a war chest. The problem is also not having money when the company needs it. In other words, managing working capital is a timeless problem, even if some situations are better than others for highlighting the issue.

- Finally, it is a source of risk: the risk that customers will pay late or will only pay partially or not at all because they have gone bankrupt, which could in turn create problems for the company and create a series of domino-like bankruptcies. It is to alleviate this risk that the European authorities have introduced statutory provisions to reduce payment periods to 60 days (or by way of exception 45 days end of month) after the invoice is issued. There is also the risk of the loss of value for obsolescence of certain goods (news journals, cut flowers, yoghurt, etc.).

From a more economic point of view, working capital can be:

- A tool for helping customers or suppliers who are already experiencing problems as a result of a liquidity crisis. For example, in March–April 2020, some large groups as L'Oréal, with ample cash resources, in turn helped their main subcontractors, who were experiencing a liquidity crisis, by reducing their payment periods. This was not only a question of altruism, it was also in their best interest, in order to avoid the bankruptcy of their suppliers, which would have threatened the continuity of their supplies.

- A source of value creation in periods of negative real interest rates and significant inflation, for sectors with high levels of inventories, through inflation gains.3 In other words, good management of working capital in this case means not managing it!

- A source of speculation (and hence of risk) when the company overstocks raw materials, the price of which it is expecting will rise substantially over the coming months (electronic components end 2020–beginning 2021).

Working capital results from the company's strategy. For example, when a company decides to get involved upstream in order to secure its supplies (ArcelorMittal owns iron-ore mines that provide it with 65% of its consumption), or downstream in order to fill the gaps in a retail network that is patchy or not yet established (SEB runs close to 1,300 shops in 45 emerging countries such as China, Turkey), then working capital is necessarily increased. Similarly, when the company decides, like Indesit did, to outsource part of its production to Eastern Europe, South East Asia or China, then margins rise (or don't fall), but working capital increases, since these subcontractors just don't have the financial structure necessary to grant Greek-style payment periods!4

The level of working capital is also the result of a financial arbitrage between margins and costs. We know of a magazine group that pays cash for its paper supplies. It is able to purchase its paper at a knock-down price, as it is in a very good position to negotiate discounts at a higher rate than that at which it could invest its cash, from suppliers whose need for cash is constant given the extent of their investments. Our magazine publisher's working capital is mediocre (practically no supplier credit), but its margins are outstanding!

Another example is the public works sector, which is structured around customer advances that more or less cover the cost of the works, and more, for the best of them. Working capital is low, but then so are margins. You can't expect your customer to give you everything!

The company grants discounts so that customers will pay quickly, which means that working capital level is low and that cash is quite plentiful but also that margins will decline. This is why in the USA it is standard to offer customers the option of paying at 30 days or of paying at 10 days and getting a 2% discount. As the yield to maturity of this commercial offer is 44.6%, very few buyers are able to resist the temptation! (And those who do send out a signal of a pitiful financial situation which may alarm suppliers.) Sales, when they are exceptional, are also a way of buying cash.

2/ MANAGING WORKING CAPITAL

There are four ways of approaching working capital management:

- tighten control over waste: stop the payments department from paying suppliers early, sell off stocks with low turnover rates and consider phasing out the production of such items. These measures are relatively easy to put in place and will not require a major overhaul of the company;

- take a close look at more structural elements that will require a change in behaviour or organisation. This could mean indexing the variable compensation of sales reps, not to orders taken but to actual payments or margins made, reorganising production chains in order to reduce buffer stocks, shifting from a mass procedure to a process procedure,5 introducing made-to-order production for slow-moving products, but also to optimise administrative procedures (paperless invoices, automated reminders) etc. Such changes are complex to put in place, and will require the active cooperation of a number of departments, which more often than not will mean the involvement of general management;

- carry out an arbitrage between margins and working capital in order to buy or sell cash;

- create a false appearance, by reducing working capital on the balance sheet using factoring, securitisation, discounting, reverse factoring etc. But let's not fool ourselves, working capital has not really been reduced, it has only been partly financed, and this part disappears from view in the same way that poverty is invisible in Potemkin villages. These are financing techniques that are discussed in Section 21.3.

Only the first two of the above ways of approaching working capital management will lead to the generation of cash without weighing heavily on the cost structure.

Working capital management is also a cultural issue. We saw in Section 11.3 that payment periods in Europe differ widely from one country to the next.

Some companies have a more developed cash culture than others, either because of the financial difficulties they have had to face in the past (carmakers in the 1980s), the influence of their shareholders (LBO funds make cash an essential lever of their culture6) or the approach of a manager (former financial director), which have made them sensitive to cash from a very early stage. Other firms have less of a cash culture because financial conditions make cash less of a pressing problem or because their culture is far removed from such preoccupations (engineering firms, firms involved primarily in research and development, etc.).

In other words, if a cash culture is to take hold within a company, as an add-on to other cultures rather than a replacement, it will require a long learning period, patience, diplomacy and, above all, the support of general management, as it often leads to a root-and-branch overhaul of established practices with which staff are familiar and comfortable.

Finally, even though all employees can be expected to try to enhance their performance and improve their weak points, we can't help being a bit sceptical. Division managers are rarely superhuman. If we set division managers multiple targets of growing the market shares of their products, increasing margins, ensuring good relationships between labour and management and seeing to it that their divisions comply with corporate culture, not forgetting to innovate along the way, and then we also ask them to reduce their working capital over and above the obvious waste that needs to be avoided, we are perhaps asking too much of them. These multiple objectives could hamper managers in the performance of their tasks, with the risk that they are unable to perform properly and fail to achieve any of their goals.

We know of a multinational firm that has become a leader in its field as a result of innovation and highly effective marketing. Its margins are enviable and its after-tax return on capital employed is just under 20%, yet its working capital can hardly be described as good. Is it possible to be good at everything all of the time?

This rather existential question has, unfortunately, to give way to the more mundane. The following sections look at the operational and more concrete ways of reducing working capital. This may seem a bit dull, but it is the nuts and bolts of the field. Stay with us and be patient.

Section 49.2 MANAGING RECEIVABLES

Managing receivables involves:

- negotiating better payment terms (general terms and conditions);

- securing the actual payment of receivables as closely as possible to the original contractual terms and conditions;

- securing the payment of receivables in order to avoid bad debts.

The last two points are intertwined, as the risk of default increases in direct proportion to the length of the payment period. Payment periods for Spanish, Italian, Portuguese and Greek groups are twice as long as in Scandinavia, and, here, the default rate is twice as high.

1/ SPEEDING UP THE PAYMENT OF TRADE RECEIVABLES

Altares estimates that 45% of invoices remain unpaid on their due date and that 3.2% of them are still unpaid 90 days later.

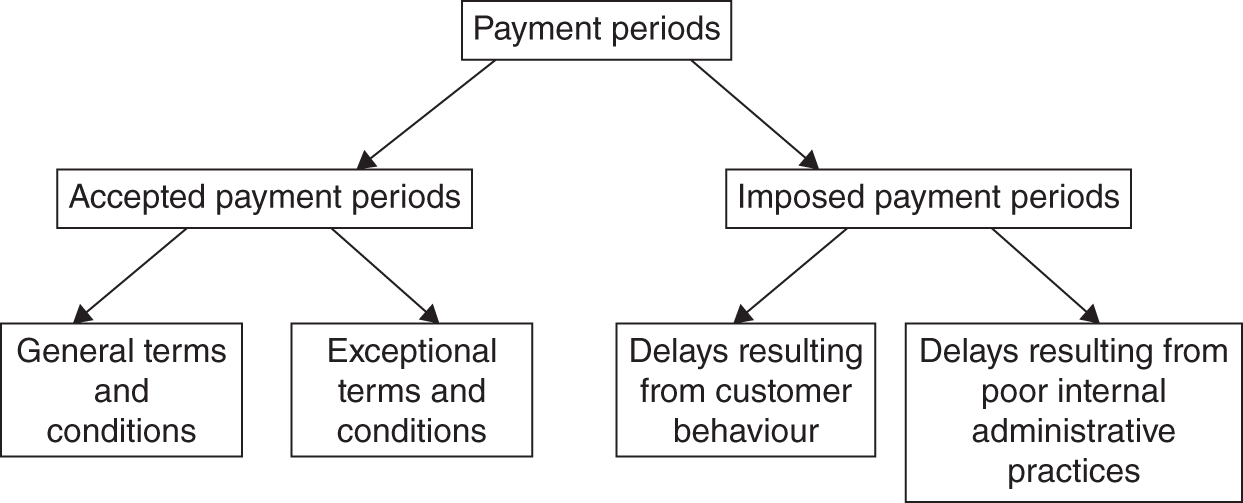

Payment periods are often described as the result of four factors:

The general terms and conditions of sale make provision for payment periods that are set by the company and are in line with its strategy, standard industry practice and local customs.

When sales reps offer exceptional terms and conditions of payment, this means that the financial manager has made sure that they come with a commercial gain (higher price, larger volumes). If this is not the case, then sales reps will have to go back on their word, which is never easy with a customer who has been allowed to slide into bad habits! This is why it is best not to let sales reps make decisions on exceptional terms and conditions.

When customers fail to meet payment in full and on time, they are bending the rules and stretching the terms and conditions of sale which they signed up to. The EU Directive on the reduction of payment periods makes provisions for penalties for such infringements: late payment interest calculated at the Central European Bank rate plus 10 points (10% in mid-2020). In certain countries, the law also makes provision for civil and criminal penalties (fines). Even though suppliers are under an obligation to apply them, they may think twice before doing so, given the potential negative consequences of such action.

In order to avoid ending up in this situation, it is in the company's best interests to:

- contact customers 15 to 30 days before invoices are due in order to remind them that payment is due and to check that there are no problems with the invoice. If there are any problems, corrective measures should be taken immediately (for example, a new invoice with the correct purchase order number should be issued). Such reminders should preferably be made by telephone if they are to be more effective. They must be adapted to the type of customer (large companies vs. small businesses) and should target the largest outstanding amounts. Payment reminders also provide an opportunity to check that all invoices sent to a particular client are up to date;

- identify customers that are systematically late payers or that regularly come up with stalling tactics in order to delay payment;

- identify customers who have long and complicated internal invoice payment approval systems, for example a customer with multiple delivery sites for payments that are centralised and paid by batch (invoices approved for payment received after the 20th of the month are paid on the 10th of the following month, etc.);

- set up a procedure for identifying swift and efficient dispute settlement. Customers that dispute invoices don't pay them. It is estimated that it takes, on average, 30 minutes to settle a dispute and that two-thirds of disputes are settled as soon as the first action is taken. Dispute settlement is all the more necessary since an unpaid invoice will often be an obstacle to new orders from the same customer, even if nothing is being done to understand and resolve the cause of the dispute;

- send out written reminders at the latest 15 days after the invoice is due, followed by a second reminder 15 days after that, and a final reminder 15 days after the second reminder, before taking legal action or handing over the debt to a debt collection agency.

Delays resulting from the internal malfunctioning of the company are, in theory, the easiest to remedy, even though this often involves overhauling the company's administrative processes, while always keeping in mind the playoff between costs and efficiency. It's also a good idea to look at the time it takes for invoices to be issued because the payment period starts as of the date of the invoice, even if the product or service has already been provided. Checks should be carried out to ensure that the invoice bears the correct address and that the quantity invoiced is identical to the quantity ordered.

2/ SECURING THE PAYMENT OF TRADE RECEIVABLES

As a defaulting customer can cause a company to go bankrupt, it is in the company's best interests to protect its receivables from any risk in this regard.

There are several simple measures that can be put in place:

- setting of a maximum credit limit for each major customer. In practice, two credit limits are often put in place, with the lower one triggering an alarm when it is breached, leading to an investigation into the customer's solvency. If the second credit limit is breached, then orders will no longer be taken from this customer, unless it agrees to pay on delivery or agrees to reservation of ownership clauses7 for as long as it has not paid its commercial debt;

- spot checks on the solvency of customers because a customer that is solvent today may not be solvent tomorrow. Such checks can be carried out by analysing the customer's accounts and checking its rating with professionals involved in commercial information (Ellisphere, Altares, Dun & Bradstreet, Creditsafe, etc.);

- preparation of sales reps' prospecting campaigns by carrying out advance checks on the solvency of targets. This is good practice in order to avoid payment problems in the short term, but also from a long-term point of view as the most solvent companies often turn out to be the best customers with the best payment practices;

- use of the most secure payment methods such as confirmed export letters of credit8 or requirement of a down payment on ordering.

This is the province of the credit manager, generally attached to the finance department, who is responsible for trade receivables, customer risks and collection and is also required to optimise performance, working alongside the sales departments.

At a later stage, the credit manager may have to make use of the services of collection firms (Intrum, Ellisphere, Pouey, etc.), which handle the recovery of unpaid debts on behalf of companies, either amicably or through the courts.

In order to avoid such situations, the company can take out credit insurance. This is an insurance policy which guarantees the reimbursement of the unpaid debt by the credit insurer (Coface, Atradius, Euler Hermes, Zurich, SACE) in exchange for an insurance premium of between 0.10% and 2% of sales covered.9 It is rare that full compensation is paid out as the company will still have to pay the insurance excess, which will be between 10% and 30% of the amount of the debt. The insurance payout is made either when the purchaser of the company's goods is declared insolvent or at the end of the waiting period before payment. In order to avoid carrying only the risks that the company knows are bad risks (adverse selection), insurance companies often insist on covering the whole of the company's customer portfolio.

Credit insurers provide three services:

- the prevention of receivables risk through solvency analyses and the provision of centralised commercial information which they update on an ongoing basis;

- recovery of unpaid invoices;

- compensation on guaranteed debts it has not been possible to recover.

Credit managers also have other tools at their disposal to protect the company against defaulting customers:

- bank guarantees: the banks of certain problem customers are sometimes prepared to provide a bank guarantee that they will meet their payments;

- techniques used in trade finance such as the irrevocable and confirmed documentary credit (very popular in high-risk countries);

- non-recourse factoring,10 allowing a company to sell trade receivables.

Section 49.3 MANAGING TRADE PAYABLES

This item is often neglected as company buyers are often more keen to negotiate good prices than to negotiate advantageous payment periods.

But this is a pressing need with the development of credit insurance. If a company's supplier has taken out credit insurance to cover its receivables, and if the company pays after the contractual payment period and the supplier declares a default on payment to the insurance company, the company will be identified as a bad payer by the insurance company and this news will spread very quickly on the market.

Management of trade payables will mainly involve:

- a review of payment periods negotiated with each supplier. The company will often discover that it has a wide range of payment periods as a result of decentralisation. Even at companies where purchasing negotiations are centralised, payment periods are not dealt with as the focus is often only on prices fixed for the whole of the group. In such cases, the company should negotiate with its biggest suppliers and try to align all payment periods with the longest periods that are already in place. The company can try and force smaller suppliers to accept such longer payment periods;

- a comparison of theory (contractual payment periods) and practice (the actual period after which the company pays) will highlight situations in which the company pays earlier than it should. Often, if lack of discipline and incompetence are eliminated as causes, the reason for this is that different dates appear in the terms of payment in the contract, on the order and even on the invoice. Sometimes companies pay on the 15th of the month amounts that are due between the 15th and the 30th, and on the 30th of the month amounts that are due between the 1st and the 15th of the following month. There are other times when the supplier delivers the goods or service earlier than planned, and sends off the invoice immediately;

- a review of the procedure for validating the receipt of deliveries will help to prevent late validation of deliveries which, in the best of cases, generates delays in invoice accounting and hence payment delays, which could result in heavy penalties. In the worst of cases, new orders will be triggered as the stocks in the system could appear to be abnormally low!;

- finally, disputes should be dealt with quickly as they will not result in any extension of the contractual payment period.

Section 49.4 INVENTORY MANAGEMENT

The ability of a company to manage its inventories well is dependent on several parameters and on how well the company manages these:

- its ability to correctly forecast the level of activity in advance, which is highly dependent on the sector;

- its ability to carry out cross-analyses between product families and customer families in order to be able to work out suitable supplies and storage policies;

- its ability to reduce its supply periods;

- its ability to transform its stocks rapidly from raw materials into finished products, and then to sell them (called optimisation of the production process);

- its ability to monitor stock levels;

- its ability to obtain a service rate11 high enough to avoid stockouts.

Experience has shown that when a company takes a serious look at its inventory levels, it can achieve impressive results. We know of a company that has been able to reduce its inventories by 23%, cutting them from 70 to 54 days of sales. Progress in logistics and IT management have played a large role in these improvements. However, it would be fallacious to believe that it is always best to keep inventories low. Inventories remain an investment which results from a playoff of financial cost versus the flexibility gained.

As for the management of receivables, managing inventories involves action to combat waste and more structural action.

Action to combat waste includes:

- selling off dormant inventories for which orders have not been placed for more than a year;

- systematically using the Wilson formula for determining the optimal quantity to order. The Wilson formula12 consists in playing off the cost of placing the order (administrative cost, discount in line with size of order) against the cost of storage (financial cost of tying up capital, storage and risk);

- reducing uncertainty over supplies by analysing delivery periods and the reliability of the various suppliers or even setting up partnerships with some suppliers (as is the case in the automotive industry);

- integrating sales forecasts into the stock management tool;

- determining the inventories policy on the basis of service rates to be provided to customers.

Structural measures include:

- shifting from a mass production mode to a process mode,13 which is not without cost as the firm will lose flexibility and run the risk of breaks in production; or shifting from a workshop production mode to a mass production mode;

- shifting from a mass production mode to made-to-order unit production. This will mean sacrificing economies of scale but with technological development (e.g. 3D printing), production costs may still be reasonable and a build-up of unsold stock or lost sales can be avoided;

- including performance-based targets in the calculation of the variable remuneration of stock managers (only 20% of groups have such systems in place);

- optimising the location of stock and of picking processes at factories, in order to reduce in-transit inventory;

- working on sales forecasts so as to reduce buffer stocks and anticipation inventories, which may involve working more closely with the firm's main customers or working out precise statistics in order to be in a better position to determine the seasonality or the cyclical nature of sales;

- simplifying the range of products offered by reducing varieties which increase the number of unit stocks.

Section 49.5 CONCLUSION

Financial managers will not be able to put in place measures for managing working capital without the close collaboration of operational managers responsible for purchasing, stocks, logistics, production, sales and human resources, over whom financial managers have no authority. Over and above the fight against waste, managing working capital often quickly leads to strategic decisions involving the firm's commercial, production and logistics policies.

Financial managers will, this time internally, have an opportunity to demonstrate their teaching skills and negotiating talents.

SUMMARY

QUESTIONS

EXERCISES

ANSWERS

BIBLIOGRAPHY

NOTES

- 1 And ours when we see that the Vernimmen is only available for delivery in 10 days on Amazon!

- 2 See Section 35.1, 3/.

- 3 See Section 35.1, 3/.

- 4 Without taking into account the fact that purchases are made by whole container or that more is bought in order to avoid stock outs (more than one month's delay).

- 5 Which often means rebalancing part of the company's stocks, like the carmakers did in the 1980s. See Section 8.2, 2/.

- 6 See Chapter 47.

- 7 Enabling the company that has not yet been paid to automatically recover its asset if the customer goes bankrupt, without having to join the queue of creditors.

- 8 See Section 21.3.

- 9 Excluding very risky export regions and excluding very long periods for major export works.

- 10 See Section 21.3.

- 11 Calculated as the number of error-free orders delivered on time/number of orders.

- 12 Which you can download from www.vernimmen.com.

- 13 See Section 8.2.