Building VCMS in to the Organization

Method is like packing things in a box; a good packer will get in half as much again as a bad one.

Cecil1

One of the major challenges in any new approach to managing an organization is the decision to build the new information into the ongoing information system or to simply use it as a study that provides new insights. In the case of the value-based cost management system (VCMS), it makes the most sense to build it in because the VCMS keeps important information for strategic and incremental analysis current and ready to use in a variety of decision settings. Creating an actionable basis for making changes to the organization, the VCMS provides all of the benefits of activity-based costing with the additional insights that are provided by tying activities to specific value attributes. It is a comprehensive cost analysis tool.

The VCMS has been used for different purposes by the companies that have been studied in our field work. Since each site was unique, with specific problems that needed to be addressed, the model has been tested in a wide variety of situations and found to be useful. Let’s look at some of the evidence of VCMS usefulness from our field work.

Strategic Analysis and the VCMS

The VCMS model is a strategic tool first and foremost. Providing a mapping of the company’s efforts against the value attributes preferred by customers, it helps direct attention to those areas where the firm is under- or over-performing. The result is a more tightly defined set of change actions that are needed to improve a firm’s competitiveness.

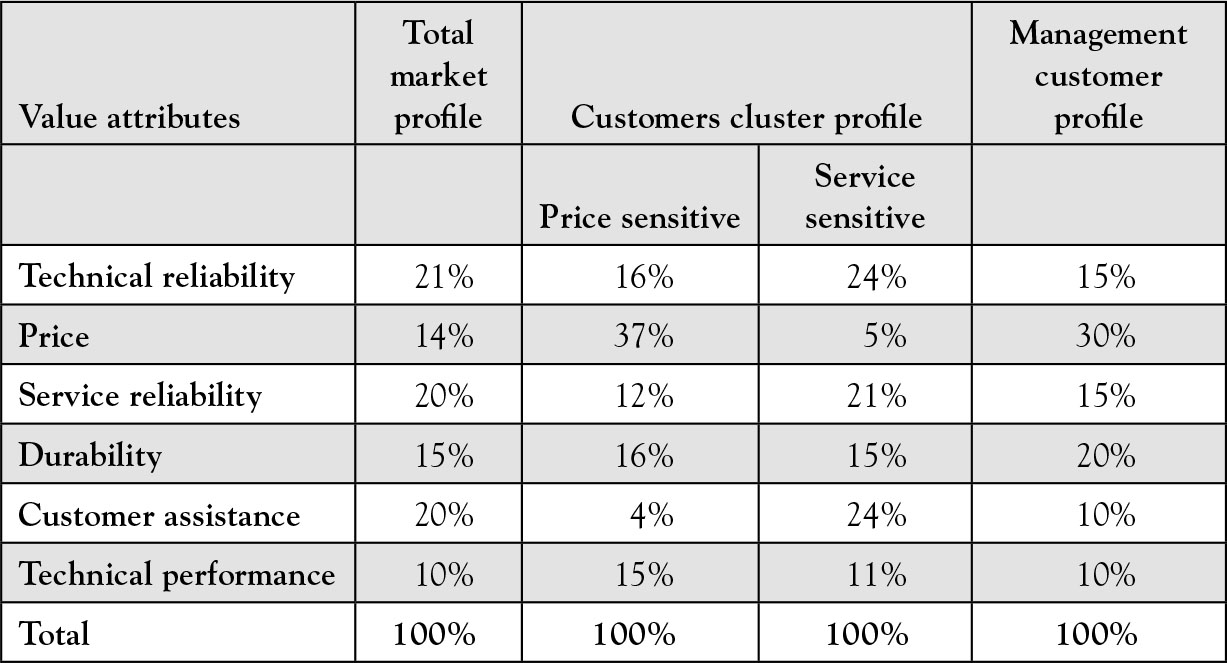

Frangor was one of the early implementations of our model. A farm implements manufacturer in Italy, it employed strategic cost analysis to help it understand its overall position in the industry. This information was useful, but was not as actionable as the company had hoped. It then turned to the VCMS to gain a more precise understanding of where and how the firm was meeting customer needs and where it was falling short. As can be seen in Figure 11.1, our work identified two customer segments using data collected with customer surveys. Additionally, what Frangor’s customers valued did not correspond to attributes identified by management as most important, making this valuable new information for the firm and its decision-making.

Figure 11.1. Frangor’s value profiles.

Looking at the information in Figure 11.1, we see that across the board management did not have a good understanding of the value profile for their company. The fact that two segments were identified had also eluded the company during the years. Since each segment wanted and valued different attributes, it made it quite a challenge for the firm. Should they focus on the price-sensitive customers and change their current differentiation strategy to a price strategy, or should they continue to differentiate themselves, placing more emphasis on service reliability and customer assistance than they did in the past? The decision was made to enhance service and also to look within the firm to try to find ways to reduce costs so they could also be more price-competitive.

Based on this information, changes were made to the design and development process to focus on a family of products using one stable platform rather than the one-up designs that had been developed in the past. This allowed the company to cut its inventory of raw materials by one-third, a major cost reduction. A second change was described in Chapter 10. The firm invested more in its service profile so that they could meet the demands of the service-sensitive customers. Not all customers would place equal value on service, but in a differentiation strategy it was critical that Frangor choose a path that would separate them from their major competitors who were competing predominantly on cost.

In strategic analysis, then, the VCMS model helps the company understand the differences in attributes valued by customer segments and what path forward makes the most sense. Since a differentiation strategy allows the company more room to innovate, it is often preferred once customer data enters the analysis. Competing on cost constantly pushes the profit margins of the firm, placing ever greater pressure on finding waste and BVA-Administrative costs and removing or limiting them. The firm that uses VCMS as their strategic model knows where not to cut costs—they protect value-add and BVA-Future expenditures. This makes cost cutting a surgical rather than a chainsaw operation.

This was the experience at Windows, Inc. also, as noted in Chapter 10. They found that there were differences in the preferences between their trading partners and the final customer. Since the costs created by the trading partners were not truly value-add in nature, but more likely BVA-Administrative, there was significant impetus to find a way to meet trading partner requests with minimal outlay of new funds.

We’ve also seen that Impact Communications had a significant strategic revelation when using the VCMS approach. They found out that they had three very different segments of customers, and they were only servicing one segment well. This led to changes in the way jobs were designed and executed. The VCMS-based information also led to internal structural changes in the firm, with the pure publicity work (smile and dial) being placed higher in importance than the research work that only a small segment of its customer population valued.

GTI made major changes in its strategic profile once it realized that a large proportion of its total income and profit were coming from traditional “dial tone is great” customers. The company had been trying to compete with Internet providers and spending less and less time and money servicing its basic customers. The company was ultimately bought out by a major phone service provider, where the major investments necessary to thrive in the Internet-dominated market could be justified based on scale. For a small local telephone company, though, the profits simply weren’t there. At the time of the study, basic services for basic customers was the source of majority of its profit. It was a lesson in not taking the loyal customer for granted.

Identifying the value profile of different customer segments is one of the primary benefits of the VCMS approach. Tying the company’s costs to the value profile is an added benefit, one that allows for targeted changes in the way the company is managed. It helps make the decisions that management undertakes have a greater focus and become more reflective of what the market really wants from their product or service. And, for a trading partner farther back in the value stream, it helps them better understand what elements of their work contribute to the value of the final product—communication is enhanced because it is built on customer value data, not management opinion or perception of customer wants.

The VCMS, then, is a valuable strategic tool, one that can be used on an ongoing basis to track the preferences of customers in the marketplace and to keep the firm constantly fine-tuning its operations to better meet these expectations. It is a growth-oriented model because it emphasizes removing waste and reducing the cost of BVA-administrative tasks, refocusing the savings into areas the customer values. The result is a multiplication of the value delivered by the firm and the enhancement of its strategic position. In every firm that employed the VCMS, then, improved strategic decision-making was the result of the pilot study. The proof that VCMS is a strategic tool lies in the results of this fieldwork.

Incremental Analysis and the VCMS

There has also been a significant use of the information acquired during the VCMS study to support incremental analysis in the firms that have been studied. Incremental analysis is short-term operational analysis that emphasizes making shifts to how work is currently being done. For instance, Frangor used the results of the study to determine whether or not it should directly manufacture more of the parts that went into its farm implements. The company had traditionally been a final assembly shop, outsourcing all of its parts to other manufacturers. This placed it in a profit squeeze situation, where suppliers would raise their prices but Frangor couldn’t simply pass these price increases along. Making more parts allowed Frangor to recoup more of the profits that came from their final products. It was a decision based on VCMS information.

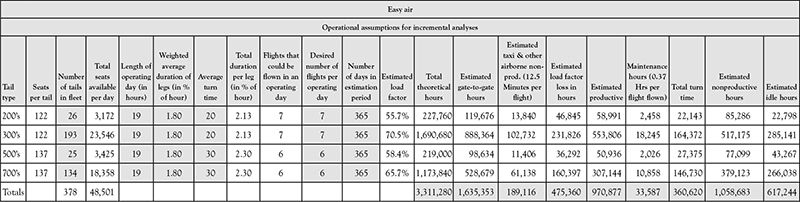

At Easy Air, an entire study of the impact of long haul flights on overall costs and profits of the firm was completed. Figure 11.2 shows part of how this analysis was done. The shaded data boxes were where management could made changes to model assumptions, while the unshaded boxes were calculated based on the results of the activity analysis underlying the VCMS approach. Several revenue and cost scenarios were developed as part of the study, resulting in a change to the structure of the sector model used to schedule the planes. Specifically, the long haul flights were made into a separate sector, resulting in changes in management of that segment of flights. Decoupling the long haul flights from the regional networks reduced the impact of variation in the long haul operations on the effectiveness and efficiency of the short haul regional networks.

Figure 11.2. Easy Air incremental analysis template.

This effort resulting in an operational a change that helped the company improve its on-time performance statistics, an important measure of quality of service in the airline industry. It was also an illustration of the value of keeping the VCMS data current. With current information, the study could automatically estimate the impact of changes to the operational assumptions of the firm. This was a result of the VCMS being based in activity-based analysis, while not going to the level of activity-based costing. Since activity-based costing estimates assume a volume, it was important to separate the analysis of costs from existing activities and simply make estimates of how much impact the change would have on the capacity available.

At Windows, Inc. the entire management of vacuum-forming some of the window components came under study due to the VCMS analysis. Since capacity cost analysis2 was used to conduct the costing of the machine centers in the company, very precise data was available to analyze how much it would cost if a change in the vacuum forming department was made. Once again, gathering the information to support the VCMS project resulted in information that could be used in a variety of ways internally to improve the quality and consistency of the incremental capacity utilization analysis done in the company. The results of a part of this analysis are demonstrated in Figure 11.3.

Figure 11.3. Windows, Inc. capacity analysis.

So what is the total information required to support the VCMS? First, if the company is a service company, the data includes the following:

• Activity analysis

• Customer profile data

• Mapping of activities to value-add, BVA-Indirect, BVA-Future, BVA-Administrative, and Waste categories

• Mapping of activities to value attributes.

If the company has manufacturing as part of its basic operations, capacity analysis needs to be added to the cost analysis segment to ensure that the data internal to the firm matches the activity analysis in a comprehensive way. In capacity analysis, the value-add portion of the capacity utilization is clearly outlined, with various forms of BVA-Administrative and waste activities clearly outlined. Since it takes more resources to collect the capacity data, even though it is minimized in nature, this is why VCMS works so well in service firms—the data collection is greatly minimized.

Whether in manufacturing or service, the VCMS supports consistent incremental analysis where the data is based on actual operations, not assumed relationships. This is a marked improvement over most existing incremental analysis where cost analysts assume new conditions for every decision. The VCMS results in a total costing approach that is driven by customer concerns first and foremost, but which can also be used to identify and isolate internal operational improvements with no, or minimal, new data collection needed.

Collecting and Using Data for Performance Evaluation

Supporting decision analysis, whether strategic or incremental in nature, is a natural outgrowth of using the VCMS approach to measure and manage a firm’s cost and value structure. The question that immediately gets raised in most companies, though, is how to use the information to evaluate performance. The Windows, Inc. analysis noted above was done for all of the cost centers in the organization. This approach allowed management to compare the performance of the various cost centers to see where capacity utilization was high and where it needed to be addressed. The greater the amount of productive time on a machine, given what it produces is actually needed by the firm to meet customer demand, the greater the value-add component. Windows, Inc. relied heavily upon profit sharing with its employees to manage its workforce commitment to superior performance. The results of this type of reward’s ability to motivate employees were seen in the very high utilizations of machinery across the company. No one was motivated to buy excess machinery.

Impact Communications also built the VCMS data into its performance evaluation process. Engagement managers were evaluated based on how closely they held the expenditures and efforts on a project to the value profile the customer had defined. This was a major change to the performance evaluation process, one that focused everyone’s attention on the need to tailor each engagement so that individual customers would be satisfied with the outcomes. Since the firm needed to build up a loyal customer base, building the VCMS logic into performance evaluation helped ensure that satisfied customers would come back to the firm in the future.

There are many ways, then, that the VCMS data can be built into performance management systems. Cost centers can be held accountable for maximizing the value add component of their work and using continuous improvement methods to drive out waste and minimize BVA-administrative activities. Goals can be set for these cost reductions. If the resulting savings are reinvested into activities and outcomes that the customer base values, the firm can grow its value profile in ways that increase its competitiveness.

Elements of the VCMS puzzle can also be built into the performance evaluation system, as was seen at Windows, Inc. In this situation, the benefits gained can once again be used to create new funds for value-creating work. Identifying waste and eliminating it is always a good management approach. Knowing what to do with the funds that are freed up is a benefit of using the VCMS framework to manage the business.

One warning needs to be voiced at this stage, though. When the VCMS is used as a management control tool it becomes open to the same level of dysfunctional consequences as are seen in any control situation. While it is difficult to game the capacity analysis, it is possible that a cost center would overproduce to make its capacity utilization numbers look good. But, if the overproduction results in increased inventories and downstream damage or obsolescence of parts, it is not a win for the company. That means the information provided by the VCMS must be balanced off against other performance goals for the company or cost center.

Given its reliance on manager input to develop the activity analysis, using the VCMS for performance evaluation can also lead to managers claiming higher percentages of value-add activities even if their performance has not really changed. Since there are very few ways to verify this information, short of closely monitoring daily activities in a department, little is gained if the system leads to data manipulation or false reporting by cost center managers.

As with all information systems, then, the VCMS walks a fine line between positive and negative impacts when it is used for management control purposes. It is a reality faced in all organizations that people hate being controlled and will do many undesirable things to meet their goals if they feel pressure to meet preset standards. Using VCMS data for control purposes, then, must be done carefully or the integrity of the whole system can be impaired.

So, the question that results is: Should the VCMS be used for management control purposes at all? The answer is that clearly the information needs to be used at a high level to guide decisions that make the firm better at creating value for its customers. Pushing the control element lower in the organization, though, can lead to faulty information or other dysfunctional results that may damage the reliability of the information. It is the researchers’ view, then, that using the VCMS for internal management control purposes should be done with great care or not at all. It is a decision support tool, not a management control one. There are many ways that performance can be monitored. If, for instance, managers feel that there is a reward for continuous improvement, this can result in distortions in the VCMS-reported results.

Taking a Temperature or Ongoing Monitoring?

A second question that often arises when the VCMS study is completed is whether or not the effort should be a one-time event or whether the reporting of VCMS data should become part of the regular monthly reporting package for cost centers. The answer to this question lies in what benefits the organization wishes to obtain from the VCMS. If it is done just to test the validity of the current strategy, it clearly can be done as a one-time study.

The results of a one-time study will be time sensitive, though, so the VCMS loses a lot of its ability to guide future actions. Since it becomes simpler for managers to provide the needed data the more often they actually perform the needed data collection and calculations, it makes some sense to build the VCMS into the monthly or quarterly reporting package for the firm. This is especially true if the data is to be used for incremental analysis. This is short-term decision-making, which means that data needs to be up-to-date and reliable.

If the firm only wishes to use the VCMS data for strategic planning, the data can probably be collected on an annual basis. In this case the focus would be on how much improvement there has been in meeting customer expectations. The study would also provide management with insights into whether customer preferences have changed over the past year. The combination of the two streams of VCMS-based data supports a fine-tuning of the firm’s strategy to keep it constantly focused on meeting new and existing customer demands. If done yearly, the study should be handled by the internal control group of the organization as they are usually the most trusted and trained in the art of doing an information-gathering interview.

Regardless of whether the data is used solely for strategic analysis, or also put to use in incremental analysis, decisions need to be made about whose responsibility it should become to maintain the data files and resulting database. While the initial team might seem the best group to tap for this, the managers on the team will clearly have other tasks that they are expected to perform. It can be very difficult to maintain the initial implementation team as the organization goes through natural changes. This is why it is recommended that once the initial study is completed, the responsibility for maintaining the VCMS database fall to a group, such as the lean management or internal control organization, to ensure that it remains a top priority.

So the answer to the question about whether the VCMS should be a one-time study or become part of the ongoing reporting requirements in the organization is “it depends.” It takes a significant amount of work to complete the initial data collection. Managers across the organization need to be trained in how to answer the questions and fill in the data forms. Capacity analysis needs to be undertaken if the organization has a manufacturing component. This is a lot of work to do to only use the results one time. Since it gets simpler to maintain the database the more frequently cost centers report on their activities, it seems logical to maintain the database with monthly or quarterly data collection so the greatest value can be obtained from the data embedded in the VCMS.

Making Value-Add a Mindset

If the VCMS becomes part of the regular reporting requirements of an organization, it helps to make value-add a mindset as part of the internal culture. Since meeting customer expectations on an ongoing basis is the key to gaining loyal customers, it is very important for the firm to do some form of value monitoring on an ongoing basis. Marketing clearly needs to be constantly polling the customer base to determine what their preferences are. If the industry is highly cost-competitive, there will be more and more of the organization’s product or service features that will be folded into competitive price (table stakes). Competition constantly eats away at the benefits of a differentiation strategy. Only by staying on top of customer preferences can a firm stay ahead of the competition.

It is also important to make value-add a mindset because it helps guide internal decision-making. Instead of pushing for new equipment or personnel to gain personal power, the guiding question becomes “will this new expenditure improve our firm’s value profile.” A new logic, then, is created for making investments in the firm when value-add becomes part of the organizational mindset.

Ongoing use of the VCMS supports the embedding of a value-add mindset in an organization. By constantly drawing the conversation back to whether or not an activity or asset will improve the organization’s ability to meet customer expectations, the VCMS makes value-add a visible part of the organization’s daily functioning. Just as adding quality monitoring to the plant floor has served to improve quality in adopting organizations, the VCMS approach can improve the firm’s ability to meet or exceed customer expectations. It supports the creation of a customer-centered organization.

Summary

In this chapter we’ve seen how the VCMS can be used in both strategic and incremental analysis. The information collected as part of the VCMS study is very useful in a variety of contexts. By tying everything constantly back to customer value-add the VCMS makes the concept of customer value visible and actionable within the organization. Ongoing maintenance of the VCMS database increases the reliability of the data, especially if it is used as a decision support tool rather than a management control tool.

In making value-add visible and actionable, the VCMS helps the organization stay focused on those value attributes preferred by its customers. Serving as a disciplining device, the VCMS makes it easier to make decisions about where investments should take place and where costs should be trimmed or controlled. While these benefits can come from a one-time study, the VCMS gains more power in the organizational culture if it becomes part of the ongoing reporting package.

Marketing or marketing intelligence clearly should be tasked with keeping their finger on the pulse of the customers and of the marketplace. By transforming the collected information into VCMS-friendly formats, the customer value expectations can be used to drive internal operations. An ongoing group, such as the lean management or internal control organization, should be placed in charge of the upkeep of the VCMS database. Whether updated monthly or quarterly, the VCMS has its greatest power if it is maintained. For companies that have manufacturing activities, monthly reporting makes the most sense. If the firm is purely service-oriented, quarterly reporting may suffice. The more frequently the data is collected, the greater its value as an information system.

Regardless of the use made of the VCMS data, it provides new insights and helps a company build a customer value-add mindset that can help differentiate it from its competitors. Strategic by design, and operational in nature, the VCMS is a valuable new form of reporting and decision support that can help transform a company into a value leader in its industry. It is a tool with many uses, creating a reliable, repeatable, and verifiable storehouse of decision support data.

Economy is half the battle of life; it is not so hard to earn money as to spend it well.

Spurgeon3