To keep our faces toward change and behave like free spirits in the presence of fate is strength undefeatable.

Helen Keller1

It is often noted that there are very few modern models that work as well in service companies as they do in manufacturing firms. The value-based cost management system (VCMS) is an exception to this rule—it works equally well in both settings and it is often easier to implement in service organizations. The reason for this is that the VCMS does not use cost drivers, so there is no need to worry about the challenge of measuring the outcome of a service in a definable way. Since the analysis emphasizes activities and value attributes rather than activity drivers, it can manage service-based data with ease. Some of the best implementations of the VCMS have been in service firms that operate as job shops.

In this chapter, we focus on job shop structures and how they can use the information generated by the VCMS to discipline the spending on a specific customer’s job. Since customization of service is sometimes a key to increased customer satisfaction and loyalty, it can serve as a valuable tool to help a job shop retain its current customers and gain new ones. Putting the customer in the driver’s seat in defining the activities they want performed for them immediately can make the customer feel as though their unique needs are being met. It is a recipe for success. It is a process that starts with explaining to customers what the VCMS means to them, continues with using the information gathered from customers to discipline the spending in the organization, and ends with reporting back to customers that their money has been spent as they wanted it to be. Let’s start with explaining the VCMS to customers.

Explaining the VCMS to Customers

Most customers know what they are expecting from a company when they purchase its services. They can identify value attributes and create their unique value proposition with little prompting from the sales force. The key point to understand is what the customers want versus what value attributes the company is currently able to provide. A systematic customer value analysis such as conjoint analysis will provide an opportunity for customers to make choices between products that are similar and will lead to a result where the importance of the various attributes in customer decision-making process is clear. Remember, though, to support the VCMS, the sum of all the value attributes has to add up to 100%.

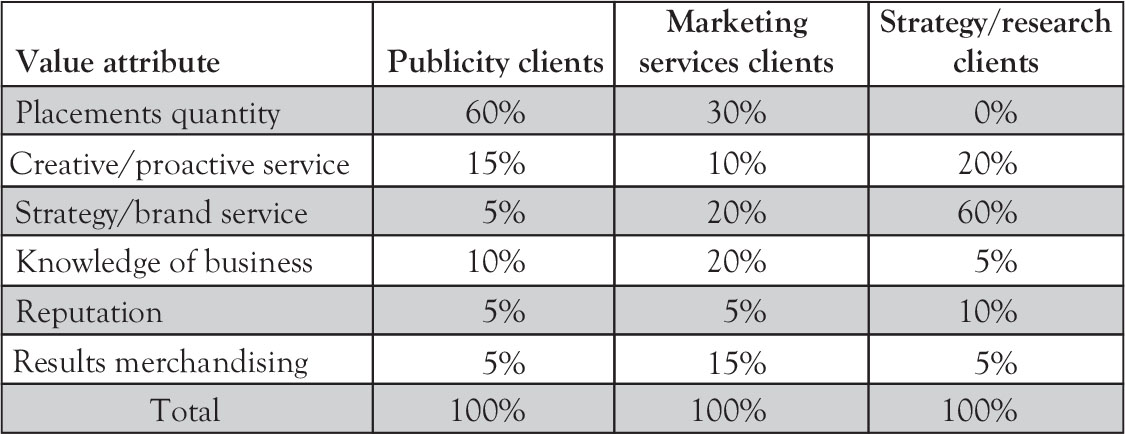

The attribute data and their importance in choices made by customers can be collected in a survey type of format, or sometimes by presenting customers with choices between sets of similar products, which contain different combinations and levels of attributes. The customer information collected can sometimes be surprising, as we saw at Impact Communications. Returning to the value profiles for the three different customer segments, we see that there are very different expectations in regard to service attributes across customer segments (see Figure 9.1). For instance, the data suggests that publicity clients place 60% of their value for an engagement on getting placements, while research clients place no value on this attribute. Without customer data, a firm can end up with a generic service strategy for all its clients. Since this is not the best strategy in this case, using the VCMS to ensure that each customer segment can have the type of activities and outcomes that they most desire can be critical for competitive survival and success.

Figure 9.1. Impact communications’ value propositions.

A discussion with customers that is centered around value attributes signals the fact that the company’s goal is truly to become customer-driven. It is important that the value attribute data collection instrument includes and properly defines all relevant value attributes. It is often recommended to conduct focus groups with customers in advance of data collection in order to properly identify all attributes in the relevant market. When the original list of attributes was first discussed at Impact Communications, for instance, the results merchandising—the quality of presentation to management that reflected positively on the manager who had chosen Impact—was overlooked. It became obvious that this was missing when customers were first polled for their input. So, a firm always has to be open to the fact that new value attributes may emerge as the industry develops new products and new players enter the market.

It is, in fact, one of the more valuable aspects of using the VCMS that the customer data enters the process explicitly and thereby forces the organization to be externally focused. Incorporating customer data explicitly into the VCMS provides critical education to all stakeholders in the organization about what the market values and how and if attributes and their importance in the product or service is changing. Since customer preferences are a dynamic element in the value creation process, staying in touch with the market using the VCMS as a communications tool is vitally important.

To summarize these points, then, when the salesperson meets with a potential customer to discuss a job or a purchase of goods or services, they should focus on the discussion of value attributes embedded in the product sold and articulate how the specific combination of features provides value to this customer. A service or a product with a different combination and importance of the features needs to be offered to the customer in case the customer belongs to a segment whose valuation of features is different.

Our field work shows that the VCMS model fosters effective communication between the salesperson and the customers in regard to the value attributes delivered rather than incentivizing the salesperson to solely compete on price. The VCMS model creates a new language for communicating with customers that expands beyond simple task or activity offerings to a deeper understanding of the value profile—what will make the customer happy with the outcomes of the engagement.

Creating a Job-Specific Value Profile

Having gathered the customer data, the organization next needs to develop a job-specific value profile. This profile is as important as the physical description of the work to be completed because it directs attention to exactly what the customer (or a segment) expects from the organization. It defines best practice for a successful job. Figure 9.2 shows an example of value attributes in an accounting firm, where each client has different needs.

Figure 9.2. Example of a value attribute listing.

Some clients of an accounting firm are most concerned with the advice and reputation of the firm, while others place more importance on reasonable fees and accurate analysis. Each engagement is likely different, with clients placing more or less weight on these various attributes. And, some customers may add things such as friendly service to this list. The final list of value attributes and weightings depends on how each customer views their relationship with the firm.

Directing Resources Where They Matter

Once the value profile has been collected for a specific customer, it comes back to the firm to guide the engagement planning process. If the customer cares about friendly service, it may suggest that an accountant that is more outgoing might be chosen to be the direct contact for the customer. The engagement has to be planned so that the resources of the firm are directed toward the things that matter most to the customer. Since probably all customers of an accounting firm expect accurate analysis, it goes without saying that the job plan should ensure that the right people are assigned to the tasks that need to be completed. A partner may be chosen as the direct contact for the customer, signaling to the customer that their job is important to the firm.

The resources must be planned, then, to ensure that the customer value proposition is met. For Impact Communications, this meant that many more people had to be assigned to the basic “dial and smile” activities required to gain placements since publicity clients were a majority of the firm’s business and this is what they valued. It was a culture change for the organization, where a successful career path in the past had been to avoid direct publicity placements activities and to emphasize research tasks. In this case, this was what the founder valued, but not what was found to be valued by the publicity customers. When company resources are aligned with customer preferences, a reconfiguration of internal processes might be required so that the right attributes are delivered in every job. It doesn’t matter what the firm cares most about—it is customer preferences that should drive performance.

Keeping Tabs on Spending

Once the job has been planned and resources assigned, a tracking system needs to be put in place that ensures that the customer’s value profile is used to prioritize actions and resource use for each job. This means that the VCMS becomes part of the organization’s management control system, being used to evaluate the success of jobs and the efforts of the managers who run them.

Let’s return to our accounting firm example and look at how this type of reporting mechanism might be set up (see Figure 9.3). As you can see, the engagement dollars have been split up amongst the value attributes, creating the revenue equivalents that drive the model. A cost projection has then been developed, ensuring that the engagement is profitable. Company expectations for this engagement, given the level of competition in the industry and given its customer value in the market, is that 50% of the spending should be directed to the value profile, leaving 25% for administration and 25% for profit. The engagement is estimated to be worth $10,000. This report would be used as a guide to the project manager, ensuring that the funds get spent in line with customer needs and their defined value.

Figure 9.3. Putting resources where customers want them.

The question that naturally comes to mind is how to match the activities that are being performed to these value attributes. This is where it is important to have completed the VCMS study inside the firm. The results of that study can create a taxonomy of activities that are classified by value attribute. For reasonable fees, which serve as a table stakes issue, the decision might be made to add this dollar amount ($750) to the accuracy attribute as this is a basic feature expected of all well-run accounting engagements. It could also be spread across several attributes if that is deemed to be the basic features an engagement should have.

With the communication attribute, the billings that align with client meetings would be mapped there. Individuals engaged on a specific job would then use the activity taxonomy to bill their hours to attributes. Anything that is done that doesn’t pass the value-add test during the VCMS internal study would be charged to administration. Clearly, if too much of the total cost ends up in administration, the job won’t earn its targeted 25% profit.

The entire point of this discussion is that the original VCMS study provides a list of value-adding activities by value attribute. It even goes so far as to split an activity out against multiple attributes. Internal personnel have to become conversant with this activity list and be able to use it to make judgments about how much time and resources should be dedicated to specific tasks. The VCMS approach, then, replaces traditional engagement budgeting, substituting a customer-driven approach for one that is firm-defined.

Reporting Back to Customers

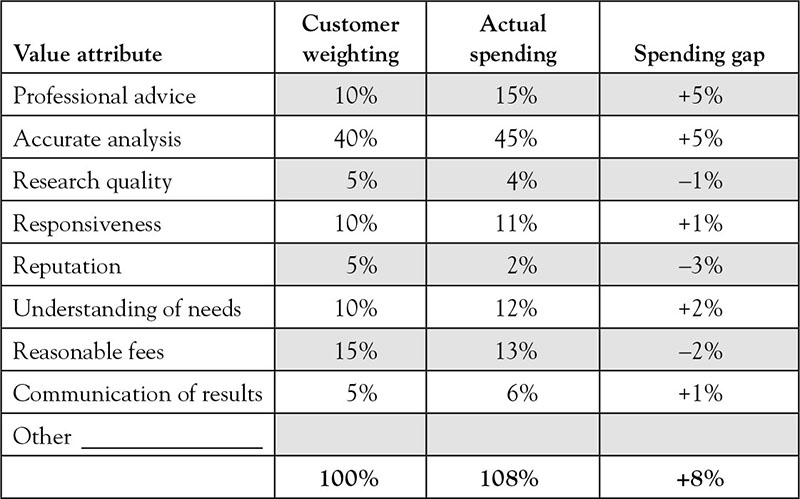

Closing the loop on a customer-driven job structure requires that the firm report back to customers about where spending is taking place. Here we return to the original percentages and use the internal tracking information to match spending against the defined value attributes. This is what was done at Impact Communications. For our accounting firm example, the report back to the customer might look like the following (see Figure 9.4).

Figure 9.4. Reporting back to customers.

It is clear that in this engagement, more time has been spent providing professional advice to the customer and actually performing the engagement calculations and worksheets than were originally planned. The shortfall on reputation can be explained by noting that this engagement required more hands-on than planned, which might mean that the reputation of the firm should be positively impacted if the customer is pleased with the outcomes—the related value multiplier should go up. Six percent more time has been spent in direct communications (professional advice and communication of results) than planned, suggesting that the customer may have understated how much interaction they desired on the job. For research quality, the engagement may have proven to be easier than originally planned, requiring less research to result in a positive outcome.

These calculations are made using the internal reports and calculating the percentage of spending by category as a percent of the total nonadministrative tasks. Since this was planned originally to be 50% of the total spend, it is clear that this job made 4% less profit than planned. Why 4%? The percentages reported back to the customer are against the 50% benchmark, so an 8% overage actually converts to only 4% of the job’s total. As long as administration didn’t exceed its 25% target, the job should be profitable.

If the client is happy with the service received, the job report should help provide input to the next engagement between the firm and the customer. Both sides of the client–firm relationship learn from this process, gaining a better understanding of what the customer really wants in a successful engagement. It is clear that this customer wants more communication than was originally planned, so future engagements should budget more time for this important activity. The completed job reporting package shows the customer that the firm is listening, and also that their preferences may be slightly different than they originally thought if they are satisfied with the job.

What happens if the customer is dissatisfied with the outcomes of the engagement? The salesperson or partner, whoever is doing the debriefing at the end of the job, needs to isolate exactly what the customer didn’t value. Perhaps they wanted even more direct communication. In that case, the firm might need to enlist a staff accountant to do some of the communication as their billing rate would be lower, keeping the job within its price structure while increasing the intensity of communications. The whole point is that there is now precise information that can be used in planning future engagements to bring them closer to delivering the right level of customer value. It is a communication process and a learning process, one that begins and ends with direct communication with the customer.

Assessing the Impact of VCMS-driven Customer Support

In marketing, loyalty of a customer is often recognized as one of the important aspects of an organization’s relationship with its customers. Loyal customers do repeat business with the firm, increasing the profitability of jobs as the firm learns how to meet customer expectations in more efficient and effective ways. So, one possible way to assess the impact of VCMS-driven customer support is through changes in the loyalty ratings for the firm’s customer base.

Why does loyalty matter? The answer to this lies in the amount of money that is spent to gain a new customer. It often takes significant financial and other investments to acquire a new customer. All of these costs have to be borne by the jobs the firm secures from the customer. If there is only one job secured because the customer was dissatisfied with the outcome, then all of this cost has to be borne by one job, quite likely turning it from a profitable engagement to one where losses occur. This was the situation facing Impact Communications before they turned to the VCMS approach to plan and monitor their performance on specific engagements.

So, connecting the impact of the VCMS approach with customer loyalty and satisfaction is a recommended step in ensuring that performance and profit improvements are attained by the organization. Monitoring every job to ensure that spending corresponds as closely as possible to the predefined customer expectations is critical. Adjusting expectations as more data become available is also important. The VCMS is a learning system, one where the firm is constantly absorbing more data about how its work affects the value proposition and where the customer comes to better understand what they really expect from the organization.

If job overruns continue, it may be necessary to negotiate changes in the fee structure with the client. These conversations are easier to have when the customer can see that they are actually demanding more service from the firm than was originally planned. This discussion also leaves room for the customer to alter their behavior in order to help the engagement remain on financial track while still providing the desired outcomes. Either way, the VCMS once again serves as a very important communication tool, one that removes ambiguity from the analysis and decisions surrounding a job and explicitly connects customer value with internal resource consumption.

Summary

In this chapter, we have shown how the VCMS can be used to help discipline the planning process and actual activities that take place when a job is taken by a job-shop firm. Using two examples from service organizations, the discussion provided a look at the engagement document as the first place where the firm and customer come to a clearer definition of what defines success in terms of job completion.

The engagement agreement serves as the basis for planning and monitoring internal activities. Using the VCMS coding scheme originally developed, the firm’s employees map their activities against the value attributes defined by customer data. For Impact Communications, we saw that the publicity clients wanted 60% of the effort of the firm to be directed toward gaining publicity placements. Since this had not been the focus of the firm prior to the VCMS study, it required a change in culture and expectations in the firm itself. Since publicity clients were generally leaving the firm after one engagement, there was no loyalty to the firm. This meant that a lot of money was spent getting new customers on an ongoing basis. The VCMS helped diagnose and isolate the cause of this customer churn and provided the organization with a clear path forward. Serving as a communication tool both internally and externally, the VCMS provides a clear signal about how success is defined in an engagement.

The VCMS approach includes the firm reporting back to the customer about how funds were spent on their job. This is a time where communication of satisfaction or concerns can take place, using precise definitions of expectations and actions. Some firms, such as Impact Communications, have developed monthly reports to customers that track the spending to date against the engagement plan. The more communication that takes place between the customer and the firm, the more likely the customer will be satisfied and become a more loyal customer, one who engages the firm multiple times, potentially improving the firm’s profit. Customer loyalty is one of the critical measures of an organization’s success. Sound, effective communication of expectations and results is the means to this end.

Decide what you want, decide what you are willing to exchange for it. Establish your priorities and go to work.

H. L. Hunt2