CHAPTER 18 APPLICATIONS IN INVESTMENT PLANNING

CASE STUDY

Roberta Stephens of the Faraway Gap Food Pantry has reached out to you as a personal financial planner and investment adviser representative. Faraway is a 501(c)(3) charitable organization that provides groceries to county residents who have fallen on hard times. The charity was established more than 30 years ago by Jean Roberts, a local businesswoman who made it big selling reclaimed wood from old factories. Jean wanted to give back to her local community, and the charity was established to honor those who had given her a helping hand.

Sadly, Jean Roberts recently passed away. She left her entire estate, valued at $2 million, to Faraway, all in cash. It was a generous bequest—equivalent to more than 10 years of the nonprofit’s annual operating expenses. Having never dealt with this kind of money before, the board of directors is at a loss as to what to do with it. Already, there is a bit of contentiousness among board members. Some would like to purchase a building in order to save on rent. Some would like to create an ad campaign to encourage increased contributions. Others would like to increase the director’s salary and provide retirement benefits in order to attract a qualified replacement for Jean.

A delay in making a decision as to how to best manage the bequest has several disadvantages—losing investment earnings (due to the entire amount being in cash); using operating funds for rent while the decision is being made whether to buy a building; and not being able to attract a new director because the current benefits package is below market.

Roberta’s question for you is: “How do we begin to address the issues associated with Faraway’s new resources?”

LEARNING OBJECTIVES

After completing this chapter, you should be able to do the following:

![]() Identify and apply appropriate tools to measure the performance of a personal financial planning client’s investment portfolio.

Identify and apply appropriate tools to measure the performance of a personal financial planning client’s investment portfolio.

![]() Use income tax planning concepts and applications within investment planning.

Use income tax planning concepts and applications within investment planning.

![]() Evaluate how investment planning concepts interrelate to other areas of personal financial planning.

Evaluate how investment planning concepts interrelate to other areas of personal financial planning.

![]() Formulate an investment policy statement (IPS) for a client.

Formulate an investment policy statement (IPS) for a client.

Introduction

We introduced the basic concepts of investing in chapter 10 and discussed investment planning and investment vehicles in chapter 11. We now return to examine investing and investment planning through the lens of integrative personal financial planning.

As you may recall from chapter 10, a personal financial planner does not always manage a client’s investment assets. However, investment planning is an essential part of the personal financial planning engagement even when the personal financial planner does not manage the investment assets. It is important the personal financial planner understand the integration of the various elements of investing, as well as how investing affects all the other areas of personal financial planning. The best way for a personal financial planner to understand this integration is through the client’s IPS. The IPS is in itself an abbreviated version of a personal financial plan, covering many of the same topics such as income needs, tax considerations, and specific financial goals. As you will see, the IPS is not only the primary link between investment planning and overall financial planning, it is also the centerpiece of investment planning.

This chapter focuses primarily on the creation of an IPS, but we also cover the concepts of investment risk and the analysis of an investment portfolio, measurement of investment returns, and applications to the other areas of personal financial planning.

Perform Financial Analysis

We introduced the concept of the investment planning process in chapter 10. There we focused primarily on the first phase of the process—planning. As we noted then, careful planning is essential in investing. But what happens when you can’t be a part of the initial planning phase? In many cases, a client will come to a personal financial planner with an investment strategy and portfolio already in place. When this happens, the planner should perform an analysis of the portfolio. This analysis will allow the planner to become acquainted with the client’s investing needs and evaluate the portfolio in terms of investment risk, income taxes, investment constraints, and asset allocation.

INVESTMENT RISK

A critical component of analyzing an investment portfolio is investment risk management. Risk can be defined in the following ways:

•The uncertainty that the actual or realized return will not equal the expected return

•The likelihood of an adverse outcome (for example, loss in the value of an investment portfolio)

•The volatility of an asset’s returns over time

Investment risk may be divided into one of two categories: diversifiable risk (also known as nonsystematic or nonmarket risk) or nondiversifiable risk (also known as systematic or market risk).

Diversifiable Risk (Nonsystematic)

Diversifiable or nonsystematic risk is risk that may be reduced or eliminated through security diversification in an investment portfolio. Diversification in a portfolio of securities can substantially reduce the variability of returns without an equivalent reduction in expected returns for the portfolio. The reduction in risk is achieved because, on average, worse-than-expected returns from one security are offset by better-than-expected returns from another security. Nonsystematic risk is generally the result of market fluctuations due to such things as a new competitor in the marketplace, a regulatory change, employee turnover, a product recall, or the introduction of new technology.

Nondiversifiable Risk (Systematic)

Investment risk cannot be entirely eliminated through the diversification of an investment portfolio. This risk remaining after diversification is called systematic risk. It cannot be reduced or eliminated by increasing the number of different types of securities because it permeates the entire economic system and is inescapable. Economic activity, monetary and fiscal policy, the level of interest rates, and market sentiment are all impossible to diversify away. The risk of the market as a whole cannot be avoided.

SYSTEMATIC RISK IS PRIME

A helpful acronym for remembering the types of systematic risk is PRIME.

Purchasing power risk

Reinvestment risk

Interest rate risk

Market risk

Exchange rate risk

Total Risk (Standard Deviation)

Total risk, or portfolio risk, is the combination of systematic and nonsystematic risk that is inherent in a security or portfolio of securities. This is also called the standard deviation. The standard deviation measures the volatility or total risk of a portfolio. The computation of the standard deviation is based on the average historic return for a similar portfolio.

TAXATION AND INCOME TAX PLANNING

It is not what an investor earns that counts, but rather how much an investor keeps after taxes are paid on his or her earnings that really matters. Income taxes are a critical component of the financial analysis, so investments should be classified according to how they will be taxed—either as ordinary income investments or capital gain investments. Generally, investments taxed as ordinary income (such as dividends from bonds, interest, and short term gains) should populate tax qualified accounts because distributions from these accounts, regardless of the underlying investments, will be taxed as ordinary income. Capital gain assets should be in taxable accounts to take advantage of the current lower long-term capital gains rates and the possibility of offsetting gains with losses, which could result in zero taxable income.

ASSESS IMPACT OF CONSTRAINTS

Constraints may affect the selection, purchase, and sale of securities. For example, if a client’s time horizon is less than 10 years, then an investment portfolio would be skewed toward more cash and cash equivalents in order to protect against the risk of a market downturn. This is because the client has fewer years to recover any systematic risk.

Additional constraints may include the client’s need for liquidity in order to provide capital for a future event such as children’s education or the purchase of a vacation home. Also, some clients prefer not to invest in specific industries such as tobacco, gaming, or weapons manufacture.

ASSET CLASS ALLOCATION STRATEGY

A review of the asset allocation is essential in the analysis of the portfolio. The decision to rebalance the asset class allocation strategy is usually made once each year, using simulation procedures to determine the likely range of outcomes associated with the specific asset mix. The investment adviser and the client consider the new allocation based upon updated data for the returns in each asset class selected for the client’s portfolio, as well as risk tolerance, investment constraints, and long-term goals.

The Investment Policy Statement

We introduced the IPS in chapter 10 as the main component of the planning phase of the investment planning process. As a refresher, table 18-1 shows the components of an IPS.

| TABLE 18-1 | COMPONENTS OF AN IPS |

COMPONENT |

DESCRIPTION |

| Objectives | In addition to client-specific goals, the objectives section will also include anticipated return and risk assumptions for the investment portfolio. |

| Constraints | The constraints section will provide mutually agreed-upon constraints for the investment portfolio. Examples of constraints include the following:

•Time horizon—short, intermediate or long-term •Liquidity—upcoming events that will require cash or cash equivalent assets not subject to market risk •Taxes—specific parameters for the amount of taxable income that can be generated by the investment portfolio •Legal issues of client’s situation— irrevocable trusts, requirements for alimony and child support |

| Asset class allocation strategy | This includes the agreed-upon asset allocation strategy, as well as appropriate benchmarks against which to measure portfolio performance |

| Duties and responsibilities | The duties and responsibilities of both the client and the investment adviser are codified. |

| Monitoring and review policy | A specific program of monitoring and review is agreed upon. The rebalancing of the investment portfolio, as well as an update to objectives and constraints, is outlined. |

| Acknowledgement by all parties | Signatures attest to the mutual understanding of both parties to the investment policy statement. |

When a personal financial planner also acts as an investment manager, the planner will work closely with the client to create an IPS that codifies the client’s specific goals and creates an investment strategy. In those cases in which the personal financial planner isn’t acting as an investment manager—or, as in the previous section, is engaging a client with an existing portfolio and presumably an existing IPS—the planner should review the IPS to ensure it is properly integrated with the client’s overall PFP goals.

The best way to understand an IPS is to see one and read through it. Exhibit 18-1 provides a sample IPS for you to examine. The first thing you should notice about it is that it’s quite long. An IPS shouldn’t be succinct—note the following sections:

•Confirming Your Objectives—This section identifies the personal financial planning client’s goals and objectives for investments.

•Summary Information—This is a high level overview of the client: family, employment, tax status, and the like.

•Performance Benchmarks—This is an agreed upon list of investment benchmarks against which the investment manager’s performance will be measured.

•Income and Liquidity Needs—This includes how much income, if any, the client will need from the investment portfolio on an annual basis.

| EXHIBIT 18-1 | INVESTMENT POLICY STATEMENT EXAMPLE |

Investment Policy Statement

Elizabeth and Charles Wilson

January 1, 2016

Confirming Your Objectives

This investment policy statement (IPS) has been created to confirm a clear and concise understanding between Elizabeth and Charles Wilson and Hometown Wealth Management, LLC, a registered investment adviser, regarding the objectives and strategy for the management of the accounts within the relationship. In addition, this statement is intended to establish the parameters within which Hometown will exercise discretion on your behalf in the management of your accounts. Adherence to the IPS encourages discipline and continuity of strategy throughout market cycles. The IPS is based on your unique client-specific factors, such as your attitude toward investment risk, return objectives, time horizon, liquidity and cash flow needs, and income tax considerations. This document should be reviewed whenever material changes occur in your personal circumstances or, at a minimum, at least annually to assess changes to your situation that would warrant modification.

Summary Information

| Client Name(s) | Date of Birth | State of Residence |

| Dr. Elizabeth M. Wilson | 3/8/19xx | GA |

| Charles L. Wilson, III | 6/5/19xx | GA |

Dr. Elizabeth and Charles Wilson were introduced to Hometown by their personal financial planner, Stephanie Crane, CPA/PFS, a registered investment adviser representative of Best Financial, Inc. The Wilsons reside in Kennesaw, Georgia, with their daughter Ann Marie Wilson. Elizabeth is a partner with Cardiology Specialists of North West Georgia, and Charles is a stay-at-home father after practicing law for 15 years. They are currently making modifications to their home in Kennesaw with the addition of four new stables and a riding arena to encourage Ann Marie’s equestrian interests.

What Another?, LLC, a Wyoming entity, was organized on 3/26/XX and is owned 50 percent by the Elizabeth M. Wilson revocable trust, dated 02/09/XX; and 50 percent by the Charles L. Wilson, III revocable trust, dated 02/10/XX. It is anticipated that at some point in the future a gift trust for the benefit of Ann Marie will be formed, and the trust will have a membership interest in What Another?, LLC.

Financial Goals and Investment Objectives

General Financial Goals

To provide for the growth of principal and to fund future financial independence needs.

Time Horizon

The time horizon is 20 or more years.

Investment Objectives

To meet these financial goals, it is mutually agreed that the investment objective for the overall relationship is growth of principal over time through exposure to equities. Current income is of lesser importance. Fixed income assets are used to provide some income and to reduce portfolio volatility. Additional sources of return and diversification are added through an allocation to alternative investments.

The following table details the accounts included in your relationship with Hometown. Though the objectives listed for each account may differ from that of the overall relationship, the accounts as a group are managed toward your overall relationship’s objective. The allocation ranges for each account are provided as a guide and may vary based on factors such as our asset class outlook over time and any specific circumstances that may arise.

With consideration of the two primary factors that affect an investor’s risk tolerance (the financial ability to accept risk within an investment program and the willingness to accept return volatility), this portfolio’s risk tolerance is above average. It is anticipated that the portfolio will have some volatility due to fluctuations in interest rates and equity valuations. A diversified allocation to alternative investments may help mitigate this volatility.

Alternative investments may be purchased through the use of mutual funds offering daily liquidity. These mutual funds offer strategies designed to complement and diversify a traditional stock and bond allocation and include, but are not limited to, real estate, commodities, long or short equity, managed futures, or absolute return.

To reduce cost and enhance tax efficiencies, mutual funds and exchange-traded funds may be used in the portfolios.

Performance Benchmarks

Global Reference Benchmark—A blend of the components listed here with weights based on the portfolio’s longer term neutral targets to equities (domestic and international), fixed income, and alternative investments. The global reference benchmark is used as an overall index for your entire portfolio.

| Asset Class | Index |

| Domestic Equities | S&P 1500 (Includes stocks of S&P 500, S&P |

| (Large Cap, Mid-Cap, Small Cap) | 400 and S&P 600) |

| International Equities (Developed and Emerging Markets) | MSCI ACWI ex-U.S. |

| Fixed Income (Taxable or Tax-Free) | Barclay’s Aggregate or S&P Intermediate Muni |

| Alternative Investments | CPI – U + 2 percent |

Income and Liquidity Needs

At the present time, there are no income or liquidity needs for Elizabeth and Charles Wilson. Elizabeth is in practice as a cardiologist earning $650,000–$800,000 annually. The Wilson’s intent is to make regular annual contributions of $250,000 to the investment management account with after-tax earnings. Additionally, Elizabeth is making maximum annual contributions to her SEP based on income from the practice. Finally, the Wilsons are making maximum annual exclusion gifts into the 529 plan for Ann Marie.

Other Important Information

Tax Considerations and Sensitivity

Elizabeth and Charles are currently in the 39 percent marginal federal income tax bracket. Interest, dividends, and capital gains in the investment management account will be reported to you for your personal income tax return. The Wilsons have indicated moderate sensitivity to short-term capital gains.

Other Assets

Assets held outside of Hometown are taken into consideration for overall asset allocation purposes. These include the following:

•529 plan with Vanguard: $147,566

•Educational savings plan with T. Rowe Price: $32,209

•Estimated home value: $800,000

•Life insurance policy cash value(s): $184,491

Elizabeth and Charles have a $287,171 mortgage on their home. They will establish an investment credit line through What Another?, LLC, to fund modifications for the new stables and riding arena. Costs are estimated to be $300,000–$350,000.

Investment Constraints

No special investment constraints have been indicated.

Low Cost Basis Assets

Exxon Mobil Corporation inherited by Elizabeth from her mother.

Information Sharing

Hometown is authorized to share information with Best Financial, Inc., Morris, William & Jennings, CPAs, and the members of the Small Law Group, LLC led by the Wilson’s trust and estate attorney, Rob Post.

Morris William & Jennings, CPAs

Michael Jefferies, CPA/PFS

24 Big Pond Drive

Chicago, IL 60601

Stephanie Crane, CPA/PFS

Best Financial, Inc.

1 Financial Plaza

Kennesaw, GA 30152

Small Law Group, LLC

Rob Post, J.D., MBA, LLM

5 Adams St

Savannah, GA 31401

Confirming Our Responsibilities

Detailed here are the general responsibilities of Hometown Wealth Management, LLC, in striving toward successfully meeting your wealth management objectives. This is not intended to be an exhaustive list, but rather a broad guideline of how Hometown will approach managing your relationship on an ongoing basis.

Hometown Wealth Management, LLC

•Implement the investment plan.

•Inform you of any substantive changes to the investment management organization, including but not limited to changes in personnel, ownership structure, and investment philosophy.

•Meet with you, at your convenience, to review your portfolio and objectives on a regular basis. Informal, periodic updates are welcome and will be provided at your request.

•Monitor, rebalance, and manage the portfolio as necessary for income tax planning.

•Provide assistance and guidance for initial determination and ongoing review of appropriate investment objectives and asset allocation strategy based on your specific needs, objectives, and considerations.

•Report portfolio performance on a periodic basis.

Your Crucial Role

In order for Hometown Wealth Management, LLC to provide meaningful and appropriate wealth management guidance and assistance, you should provide all relevant information pertaining to risk tolerance, return objectives, income needs, financial stability, tax status, goals, and other objectives and considerations and notify us of any significant changes. We ask that you please carefully review this IPS and bring to our attention any details not consistent with your goals and objectives.

This IPS was created by:

Peter N. Talbot, CPA/PFS

Hometown Wealth Management, LLC

1/15/15

The Monitoring and Updating Phase

The creation of the IPS is of the utmost importance because that’s when the investment planner performs a deep discovery to determine a client’s financial goals, present financial condition, risk tolerance, unique needs, liquidity constraints, and time horizon. However, one could argue that the monitoring and updating phase is just as important, because it is in this phase that the financial planner determines how the plan is working and what changes, if any, need to be made to keep the client on track to achieving his or her goals.

Monitoring a portfolio isn’t as simple as checking investment valuations and yields. The financial planner must determine whether those yields represent an appropriate or desirable return. In order to properly monitor an investment portfolio, there are various measurements of returns used to evaluate performance.

MEASURING PERFORMANCE AND GOAL ACHIEVEMENT

Simple Versus Compound Return

Just as there is simple and compound interest, there are also simple and compound returns for investments. A simple return is obtained by dividing the sum of two or more items by the number of items. A compound return adds interest to the principal sum from the previous year in order to calculate the interest in the next compounding period (n / N).

Arithmetic Mean Versus Geometric Mean

There are two methods to determine the average return of an investment: the arithmetic mean and the geometric mean. When should personal financial planners use the arithmetic mean, and when should they use the geometric mean to measure returns from financial assets? The arithmetic mean is best used when compounding is of little or no consequence (for example, investments held for short periods of time and with little or no ongoing cash flows). The arithmetic mean takes into account the compounding effect of returns over time. It is the sum of all of the investment returns divided by the number of periods over which the sum total is calculated. The geometric mean is a superior measure of the change of value over multiple periods with uneven cash flows. These were discussed in chapter 3.

Holding Period Return

The holding period return (HPR) is the total return (income plus price appreciation plus dividends less margin interest) over the period from purchase to sale divided by the price of the investment (the out-of-pocket cost). The weakness of the HPR is that it fails to consider the timing of when the cash flows occur for the investment. If the period of time the investment is held is greater than one year, the HPR overstates the annualized return. If the period of time the investment is held is less than one year, then the HPR understates the annualized return.

EXAMPLE

An investor purchased a security for $10,000. The security paid cumulative dividends of $3,000 over the years until it was sold. What is the holding period return if the investor sold the security for $20,000?

Without knowing the period of time for which the investment is held or the timing of the dividend payments, there is no way to know whether an HPR of 130 percent for this investment is good or bad.

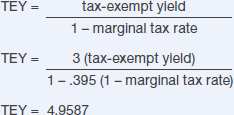

Taxable Equivalent Yield

The taxable equivalent yield (TEY) calculates the required interest rate for a taxable bond to provide the same after-tax return as a municipal bond. Generally, a municipal bond is exempt from federal income tax but is subject to state and local tax, unless purchased by a resident of the issuing state.

EXAMPLE

Nathan and Alice Johnson own a municipal bond that has a 3 percent coupon. The Johnsons are in the 39.5 percent marginal tax bracket. What coupon rate is required by a corporate bond to make it comparable to the yield on the Johnson’s municipal bond?

REEVALUATION OF THE IPS

What happens if, in the course of measuring performance, the investment adviser finds some underperforming investments, or that the original investment plan isn’t meeting the client’s goals? It’s then time to change course and update the IPS.

The IPS contains language on how and when it will be reviewed and updated. It is essential to review the IPS periodically and to make its review part of each meeting with the investment adviser. In addition, a review is needed whenever elements of the original agreement need to be updated or changed. One of the more frequent changes to an IPS is the asset allocation. For some investors, the target allocation will change over time, especially at the beginning of financial independence, as the client moves from the wealth accumulation phase to the wealth distribution phase.

Additional reasons to update an IPS include the following:

•Changes in the economy or capital markets

•Changes in types of securities or asset classes to be used

•Changes to previously agreed-upon investment policies and procedures

•Clarification of previously agreed-upon policies and procedures

•Substantive changes to the client’s personal circumstances

In addition to updates as a result of changes in circumstance, the IPS should be reviewed annually for information that has become stale or outdated. Also, the IPS should be rewritten every three to five years to reinforce the living and dynamic nature of the document. A client’s behavior and circumstances naturally change and evolve over the course of time. The IPS is updated in order to validate both the client’s and the investment manager’s understanding of the IPS.

Integration and Application of Investment Planning with PFP

RISK MANAGEMENT AND INSURANCE PLANNING

Annuity and life insurance contracts should be addressed in an IPS for several reasons, such as the following:

•The investment accounts may be needed to provide a source of funds to pay the life insurance premium payments.

•Guaranteed annuity and life insurance cash values provide a source of funds for emergency needs.

•If already not earmarked for a specific purpose, these funds may be considered a cash or cash equivalent in the asset allocation.

Annuities can provide guaranteed cash flow. Guaranteed cash flow helps to mitigate volatility in an investment portfolio by reducing exposure to sequence-of-returns risk, which is the risk of receiving negative returns early in the distribution phase. This type of risk is a major concern for retirees. The guaranteed income from an annuity contract creates a buffer from this type of risk by providing an alternate source of income when markets are down.

PLANNING FOR FINANCIAL INDEPENDENCE

No task is more challenging for the personal financial planner than investment planning for financial independence. Investment planning for specific goals, like college funding, is fairly straightforward. College begins in X years and will last for four or five years. Financial independence may begin in X years. However, neither the personal financial planner nor the client knows when the plan will end. It is this unknown that makes planning difficult. If a capital depletion model is used and the presumption is for age 95 mortality and the client lives to age 100, the results could be catastrophic.

This unknown terminal point in the financial timeline also affects the asset allocation plan. Common wisdom dictates that exposure to equity investments should be reduced over time because there are fewer years to make up a market decline. However, if the client demonstrates longevity, then a premature decision to reduce equity holdings in the client’s portfolio could be detrimental.

ESTATE PLANNING

Estate planning adds another layer of complexity to an IPS. The roles of the trustee, the grantor, and the beneficiaries of a trust need to be addressed in a separate IPS for the trust. The trust’s IPS will serve as evidence that careful consideration has been given by both the grantor and the trustee to the formulation and implementation of a prudent course of investment management. The trust document serves as a guide to the trustee and outlines the procedures for prudent administration of trust assets invested for the sole interest of the trust beneficiaries, and establishes the responsibilities of outside advisers, including the personal financial planner, in the trust operations. The IPS is revised and modified as appropriate on a periodic basis to reflect changes in trust objectives, asset performance and suitability, trustee risk management procedures, beneficiary objectives, and current tax laws.

CHARITABLE PLANNING

An IPS for a charitable remainder trust or charitable lead trust will tend to follow the same set of parameters as an IPS for a trust for estate planning. However, the directors of a private foundation or members of a board for a nonprofit entity have a fiduciary responsibility to protect the assets of the foundation or nonprofit entity. They are charged with the task of using the investment assets to further the mission of the organization.

Prior to investing, the charitable organization should develop an IPS. The IPS should define the organization’s objectives for investing and establish the nonprofit’s risk tolerance, as well as its liquidity needs. Often, depending on the size of the charitable organization, the duties of investment management are delegated to a subcommittee or an investment committee.

Chapter Review

Investing affects all areas of a personal financial plan, and investment planning is an essential part of the PFP engagement, even when the personal financial planner does not manage the investment assets. The IPS integrates the client’s investments with the client’s personal financial plan. The personal financial planner needs a basic understanding of what an IPS is, what metrics are being applied to measure the investment manager’s performance, and the various means of measuring an investment portfolio’s returns.

CASE STUDY REVISITED

Roberta’s question for you is: “How do we begin to address the issues associated with Faraway’s new resources?”

1. Identify Faraway’s goals and objectives—short, intermediate, and long-term.

2. Perform an analysis of purchase versus lease for Faraway’s office needs.

3. Review the current director’s benefit package and provide recommendations for improvements or modifications.

4. Create an investment policy statement, including the following:

•Objectives—In addition to the specific goals and objectives of Faraway, what are anticipated return and risk assumptions for the investment portfolio?

•Constraints—Will Faraway have any investment constraints? Factors to consider include the following:

![]() Time horizon

Time horizon

![]() Liquidity

Liquidity

![]() Legal issues

Legal issues

•Asset class allocation strategy—What is the proper balance?

•Duties and responsibilities—Which belong to Faraway and which belong to you as the investment adviser?

•Monitoring and review—A policy to rebalance the investment portfolio should be agreed to, as well as an update to objectives and constraints as outlined.

5. What other areas should be addressed?

ASSIGNMENT MATERIAL

REVIEW QUESTIONS

1. What type of investment risk is associated with an S&P index fund?

A. Diversifiable risk.

B. Nondiversifiable risk.

C. Nonmarket risk.

D. Nonsystematic risk.

2. A self-assessed risk-averse client wants to accumulate wealth. Of the following, which is the most critical action the personal financial planner should accomplish to assist the client in the achievement of the goal of wealth accumulation?

A. Invest the portfolio in 100 percent cash equivalent securities because it is the most risk-averse strategy.

B. Invest the portfolio in diversified mutual funds because diversity provides reduction in risk.

C. Invest the portfolio in securities which will bring the highest return to the client, regardless of risk.

D. Invest the portfolio only after determining the client’s risk tolerance.

3. Components of an investment policy statement include all of the following except:

A. Asset allocation strategy.

B. Client constraints.

C. Duties and responsibilities of the client and the personal financial planner.

D. Schedule pages of insurance contracts.

4. Susan Adams’s marginal tax rate is 25 percent. She is contemplating the purchase of either a corporate bond that has a 3.5 percent coupon or a newly issued tax-exempt municipal bond paying 2.5 percent. What is Susan’s taxable equivalent yield if she were to purchase the tax-exempt municipal bond?

A. 1.9125.

B. 2.5000.

C. 3.3333.

D. 3.5000.

5. Hunter Martin is considering the purchase of a bond to round out the asset allocation for his investment portfolio. Hunter is in the 25 percent marginal tax bracket. Which bond provides the highest after-tax return for Hunter?

A. Municipal bond paying 3 percent.

B. Corporate bond paying 3.5 percent.

C. Ginnie Mae 1 MBS paying 3.5 percent.

D. High yield corporate bond paying 4.5 percent.

For questions 6–10, refer to the IPS for Elizabeth and Charles Wilson.

6. What is the investment objective for Elizabeth and Charles Wilson?

A. Education funding.

B. Growth.

C. Liquidity.

D. Tax minimization.

7. Alternative investments are obtained through the use of

A. Commodities.

B. Exchange traded funds.

C. Hedge funds.

D. Mutual funds.

8. Which are performance benchmarks for the IPS of Elizabeth and Charles Wilson?

I. Barclay’s aggregate.

II. CPI – U + 2 percent.

III. MSCI ACWI ex-US.

IV. S&P 1500.

A. III, IV.

B. I, III, IV.

C. IV.

D. I, II, III, IV.

9. Who is the investment manager for Ann Marie’s 529 college savings plan?

A. Hometown Wealth Management, LLC.

B. Paraklete® Financial, Inc.

C. T. Rowe Price.

D. Vanguard.

10. Which accounts are managed by Hometown Wealth Management, LLC for Charles L. Wilson?

I. Rollover IRA.

II. Roth IRA.

III. SEP.

IV. Traditional IRA.

A. I, II.

B. II, III.

C. II, IV.

D. III, IV.

INTERNET RESEARCH ASSIGNMENTS

1. List three Internet resources to aid in the creation of an investment policy statement.

2. The SEC has an investor publication, Beginners’ Guide to Asset Allocation, Diversification, and Rebalancing. Download the publication. Which two elements of investing are “inextricably entwined”?

3. The development of online investment advice tools has generated discussions about the role of investment adviser representatives and the evolving relationship between financial intermediaries, such as personal financial planners, and their clients. Download “Report on Digital Investment Advice” from the Financial Industry Regulatory Authority (FINRA). What conclusions can be drawn about the role of the personal financial planner in the investment planning process?

4. What resources are available for the creation of an IPS for a charitable organization?

5. What online calculators are available to determine holding period return and taxable equivalent yield?