CHAPTER 14

A Strategic Approach to Enterprise Risk Management at Zurich Insurance Group

LINDA CONRAD

Director of Strategic Business Risk at Zurich Insurance Group

KRISTINA NARVAEZ

President and Owner of ERM Strategies, LLC

This case study describes how the Zurich Insurance Group has implemented and evolved its enterprise risk management (ERM) approach for more than 10 years across the globe. It describes how Zurich has organized its governance structures and ERM champions to help integrate ERM into the business model that focuses on promptly identifying, measuring, managing, monitoring, and reporting risks that affect the achievement of strategic, operational, and financial objectives. This includes adjusting their risk profiles to be in line with Zurich's stated risk tolerance to respond to new threats and opportunities in order to optimize returns.

ENTERPRISE RISK MANAGEMENT AT ZURICH

As a large global insurance carrier, Zurich Insurance Group has relied on its ERM program for more than 10 years as a means to help Zurich remain profitable. With over 60,000 employees around the world and serving customers in more than 170 countries and territories, Zurich is exposed to a wide range of risks from its customers to its own operations. Yet Zurich recognizes that taking the right risks at the right time is a necessary part of growing and protecting shareholder value. Naturally, Zurich aims to capitalize on appropriate market opportunities that could attract the best talent and investor capital. To achieve this, Zurich utilizes insight from its ERM program to help balance growth opportunities with the reality that it is operating in a complex world economy.

ERM not only is embedded in Zurich's business, but is also aligned with its strategic and operational planning and budgeting process. Zurich assesses risks systematically and from a strategic perspective through its proprietary tools that allow it to identify and then evaluate the probability of a risk scenario occurring, as well as the severity of the consequence should it occur. Zurich then develops, implements, and monitors appropriate improvement actions. Its ERM tools are integral to how Zurich deals with change, by helping to evaluate strategic risks as well as risks to its reputation. At the senior management level, the ERM process is annually reviewed and tied to the strategic planning process, but is also embedded in the ongoing business.

Listed here are Zurich's major ERM objectives, and a tangible proof point:

- Protect the capital base by monitoring that risks are not taken beyond Zurich's risk tolerance.

- Enhance value creation and contribute to an optimal risk/return profile by providing the basis for efficient capital deployment.

- Support Zurich's decision-making processes by providing consistent, reliable, and timely risk information.

- Protect Zurich's reputation and brand by promoting a sound culture of risk awareness and disciplined and informed risk taking.

Tangible Results

By aligning ERM with its business strategy, Zurich has been able to use certain tools to create new value to its organization in a variety of areas. Zurich's ERM program has sustained business growth throughout the recession, contributing to more than 40 consecutive quarters of growth. One way it added value through ERM was when Zurich introduced an enhanced operational risk management framework. One business unit reduced operational risk-based capital (RBC) consumption by 21.7 percent when Zurich moved from an asset-based to a risk-based approach for operational risk quantification. Tools such as Total Risk Profiling (TRP, described later in this chapter) and the business unit then identified high risk exposures, performed a deeper assessment and developed mitigation measures, The business unit experienced an additional reduction of 28.9 percent in operational risk capital consumption the following year. Operational risk capital not consumed was then available to fund profitable growth for Zurich

Optimizing the Risk and Reward Balance at Zurich

To consistently achieve the right balance between risk and reward to optimize capital, many corporate leaders around the world have adopted ERM within their organizations. Zurich has a well-established ERM program, which it sees as a critical component to its success. Zurich's comprehensive ERM and risk tolerance framework links risk taking, strategic planning, and operational planning with a comprehensive risk limit system. It enables active risk-taking within a consistent framework across the entire organization. It also allows for the flexibility to either increase or limit risk levels as appropriate for specific applications, geographies, or business units on a case-by-case basis, in accordance with Zurich's risk policy.

Global businesses like Zurich are increasingly focused on the challenge of mapping and managing their risk profiles, looking beyond a single dimension to understand the complex interactions between many different types of risks. Zurich's risk landscape outlines the number of risks, types of risks, and potential effects of those risks to the organization. This outline supports each business unit within Zurich as they strive to anticipate additional costs or disruption to its operations. Also, it describes the willingness of Zurich to take risks and how those risks will affect the operational strategy of the organization. Managing the vast scope of business exposures and growth initiatives requires taking a broader view on risks from a strategic perspective. In defining its desired risk profile, Zurich must determine which risks will optimize its returns. Its ERM mission is to promptly identify, measure, manage, report, and monitor the risks that affect the achievement of its strategic goals.

Risk Culture at Zurich

The risk culture at Zurich could be defined as the individual and group behavior within the organization that determines the way in which Zurich identifies, understands, discusses, and acts on the organization's risks and opportunities. Embedding a positive risk culture is the responsibility of the Zurich leadership team because it is critical to the effective management of the business.

The core characteristics expected from an effective risk culture include committed leadership, an effective governance structure with clear risk responsibilities and timely escalation procedures, continuous and constructive challenges, active learning from past mistakes, and incentives that reward consideration of risk management objectives and risk appetite in the organization's management of the business.

Zurich recognizes the need to constantly improve on its ERM program. Senior leadership also wishes to have an effective way of understanding and reporting on the risk culture and framework of the company, both to support internal management and oversight and to be able to report externally. In principle, the risk culture should not be seen as something separate from the overall culture of the organization, and, for risk to be truly embedded, it should be regarded as one element, albeit one that currently deserves specific attention.

ZURICH GROUP'S ENTERPRISE RISK MANAGEMENT FRAMEWORK

At the heart of Zurich's ERM framework is a governance process with clear responsibilities for taking, managing, monitoring, and reporting risks. (See Exhibit 14.1.) Zurich articulates the roles and responsibilities for risk management throughout the organization, from the board of directors and the chief executive officer (CEO) to its businesses and functional areas. In fact, each business and functional or project team will have someone designated as a risk owner to be responsible for identifying and addressing relevant risk exposures and to help embed ERM further in the business unit and build a more open, positive risk culture.

Exhibit 14.1 Zurich Risk Management Framework

One of the key elements of Zurich's ERM framework is to foster transparency by establishing risk reporting standards throughout the organization. Zurich regularly reports on its risk profile, current risk issues, adherence to its risk policies, and improvement actions both at a local and on a senior management level. Zurich has procedures in place for the timely referral of risk issues to senior management and the board of directors. Various governance and control functions coordinate to help ensure that objectives are being achieved, risks are identified and appropriately managed, and internal controls are in place and operating effectively.

Risk Governance Approach at Zurich with Three Lines of Defense

Zurich uses a “three lines of defense” model to help ensure governance and control. (See Exhibit 14.2.) This model consists of the following:

- The first line of defense in the business or functional areas involves the employees making day-to-day business decisions like underwriting, managing projects, developing information technology (IT) solutions, or managing human capital issues.

- The second line of defense is Group Risk Management, which oversees the company's efforts to apply appropriate risk identification and governance processes and provides tools and frameworks to manage decisions. Group Risk Management also coordinates very closely with the Compliance and Legal departments, Business Continuity Management, IT, Procurement, and other areas, to encourage better coordination across various silos to build an enterprise lens on risk management.

- The third line of defense is the independent internal audit function, which is responsible for verifying the functionality of the ERM and internal controls framework.

Exhibit 14.2 Zurich Risk Governance Overview

To support the governance process, Zurich relies on documented policies and guidelines. The Zurich Risk Policy is its risk governance document; it specifies Zurich's risk tolerance, risk limits and authorities, reporting requirements, procedures to approve any exceptions, and procedures for referring risk issues to senior management and the board of directors. The limits are specified per risk type, reflecting the willingness and ability to take risks, considering issues such as earnings stability, economic capital adequacy, financial flexibility and liquidity, franchise value, and reputation. Zurich's strategic direction and operational plan seeks to achieve a reasonable balance between risk and return, and to be aligned with economic and financial objectives.

An important element of Zurich's ERM framework is a well-balanced and effectively managed remuneration program. This includes a groupwide remuneration philosophy and robust short- and long-term incentive plans, with strong governance and links to the business planning, performance management, and risk policies. Based on Zurich's Risk Policy, the board establishes the structure and design of the remuneration arrangements so that they do not encourage inappropriate risk taking.

As an ongoing process, adherence to requirements stated in the Zurich Risk Policy is assessed. Zurich regularly enhances its Risk Policy to reflect new insights and changes in the environment and to reflect changes to the risk tolerance. For example, the Zurich Risk Policy was recently updated and strengthened for various areas, including actuarial reserving in General Insurance, reinsurance, receivables, operational risk management, and particularly outsourcing and business continuity management. Related procedures and risk controls were also strengthened or clarified for these areas.

Integrated Assessment and Assurance

Integrated Assessment and Assurance (IAA) is a coordinated view from the Assurance functions to provide greater confidence that risks are identified, those risks are appropriately managed, and mitigation actions are implemented and controls are operating effectively. The Assessment and Assurance functions include Group Risk Management, Group Compliance, and Group Audit. (See Exhibit 14.3.) Close coordination is also maintained with Group Legal, External Audit, and management's review functions such as underwriting or claims reviews and actuarial peer reviews.

Exhibit 14.3 Zurich's Core Assessment and Assurance Functions

Internal Control Framework

Swiss law prescribes the existence of an Internal Control System (OR 728a) to all “listed companies” and “companies of economic significance.” Zurich Insurance Group was one of the early firms to pioneer the industry with the establishment of its internal control system in 2004. The framework is of core importance in ensuring that company objectives are adhered to and that risks are controlled. The board of directors wants to have positive assurance that an effective internal control system is embedded in the business processes.

Zurich's Internal Control Framework (ICF) provides to the board the requested global overview of the risks in each business unit and how they are controlled. The evidence of these controls and its documentation serve as proof of the ICF's existence for regulatory and auditing purposes. Zurich's three lines of defense help ensure that the Internal Control Framework is enabled.

ROLE OF THE CHIEF RISK OFFICER AND GROUP RISK MANAGEMENT AT ZURICH

Zurich's chief risk officer (CRO) consults with the other assurance, control, and governance functions to provide the chief executive officer (CEO) with a review of risk factors to consider in the annual process to determine variable compensation. The CRO leads the Group Risk Management function, which develops methods and processes for identifying, measuring, managing, monitoring, and reporting risks throughout Zurich. The CRO is responsible for the oversight of risks across Zurich and regularly reports risk matters to the CEO, senior management committee, and the Risk Committee of the board.

The Group Risk Management organization at Zurich consists of central functions at the Corporate Center and a decentralized risk management network at all the segment, regional, business unit, and functional levels. At the Group level there are two centers of expertise: risk analytics and risk and control. The Risk Analytics department quantitatively assesses insurance, financial market, asset/liability, credit, and operational risks, and is Zurich's center of excellence for risk quantification and risk modeling. The Risk and Control department includes operational risk management, internal control framework, risk reporting, risk governance, and risk operations. Group Risk Management proposes changes to the risk management framework and Zurich's risk policies; it makes recommendations on the organization's risk tolerance and assesses the risk profile.

The risk management network consists of the chief risk officers (CROs) of the Group's segments and regions, and the local risk officers (LROs) of the business units and functions and their staff. While their primary focus is on operational and business-related risks, they are also responsible for providing a holistic view of all risks for their areas. The risk officers are part of the management teams in their respective businesses and therefore are embedded in the business units. The LROs also report to the segment or regional CROs, who in turn report to the Group's chief risk officer. The CROs of the Group's segments and regions are members of the leadership team of the Group's chief risk officer.

In addition to the risk management network, Zurich has audit and/or oversight committees at the major business and regional levels. These committees are responsible for providing oversight of the risk management and control functions. This includes monitoring adherence to policies and periodic risk reporting. At the local level, these oversight activities are conducted through risk and control committees or quarterly meetings between senior executives and the local heads of governance functions.

In 2012, Zurich strengthened the process through which the assurance, control, and governance functions provide risk and compliance information about each business unit as part of the annual individual performance assessment. Through these processes, Zurich encourages a culture of disciplined risk taking across the organization. It continues to consciously take carefully selected risks for which it expects an adequate return.

Board-Level Risk Committee and Executive Risk Committee Responsibilities

The board of directors of Zurich Insurance Group has ultimate oversight responsibility for Zurich's risk management program. The board approved the guidelines for the Group's risk management framework and key principles, particularly as articulated in the Zurich Risk Policy, and decides on changes to such guidelines and key principles, as well as transactions reaching specified thresholds.

The Risk Committee of the board serves as a focal point for oversight regarding Zurich's risk management. In particular its risk tolerance, including agreed limits that the board regards as acceptable for Zurich to bear, the aggregation of these limits across the entire organization, the measurement of adherence to risk limits, and its risk tolerance in relation to anticipated capital levels. The Risk Committee further oversees the organization-wide risk governance framework, including risk management and control, risk policies and their implementation, as well as risk strategy and the monitoring of operational risks.

The Risk Committee also reviews the methodologies for risk measurement and its adherence to risk limits. The Risk Committee further reviews, with business management and Zurich's Risk Management functions, its general policies and procedures and satisfies itself that effective systems of risk management are established and maintained. It receives regular reports from Zurich's Risk Management Group and assesses whether significant issues of a risk management and control nature are being appropriately addressed by management in a timely manner. The Risk Committee assesses the independence and objectivity of Zurich's Risk Management functions; approves its terms of reference; reviews the activities, plans, organization, and quality of the function; and reviews key risk management principles and procedures. To facilitate information exchange between the Audit Committee of the board and the Risk Committee of the board, at least one board member is a member of both committees. The Risk Committee generally meets seven times per year, including once jointly with the Remuneration Committee.

Zurich's Executive Risk Committee, which consists of the CEO together with the Group Executive Committee (GEC), oversees the Group's performance with regard to risk management and control, strategic, financial, and business policy issues of organization-wide relevance. This includes monitoring adherence to and further development of the Group's risk management policies and procedures. The Group Balance Sheet Committee and the Group Finance and Risk Committee regularly review and make recommendations on the Group's risk profile and significant risk-related issues.

The chief risk officer is a member of the GEC and reports directly to the CEO and the Risk Committee of the board. The CRO is a member of each of the management committees listed below, in order to provide a common and integrated approach to risk management, to allow for appropriate quantification and, where necessary, mitigation of risks identified in these committees.

Emerging Risk Group

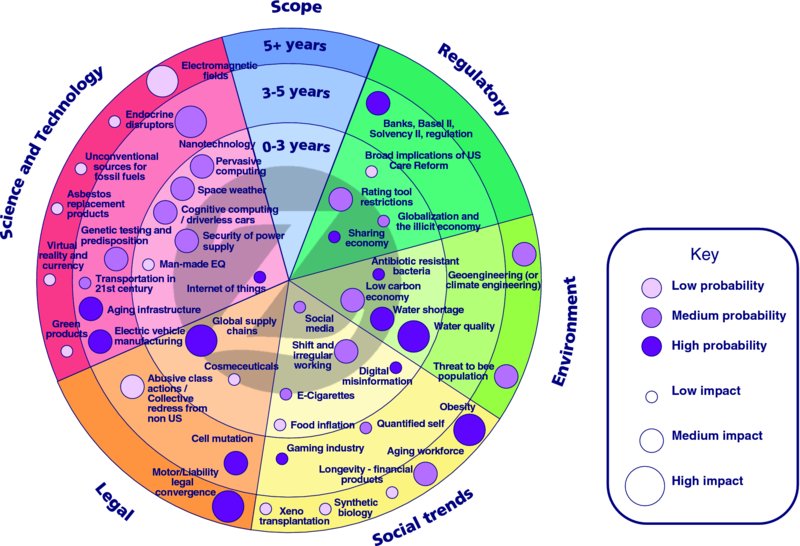

Zurich's Emerging Risk Group (ERG) seeks to preempt potential downsides of emerging risk and help its employees and customers understand and address them. The ERG looks to serve customers and society and build business opportunities to increase, not exclude, insurability of emerging risks. The ERG's remit is to respond to emerging risk threats and opportunities with strategies that help customers understand and protect themselves from risk and that drive profitable underwriting results.

The Zurich Emerging Risk Radar shows potential risks and opportunities that the ERG has currently identified. The online, internal version of Zurich Risk Radar is interactive, and one can roll the cursor over each threat to see a description of a risk and its potential harm—and each risk is classified by its primary scope (Science and Technology, Regulatory, Environmental, Social, or Legal), as well as the time over which the risk will potentially emerge (zero to three years, three to five years, five or more years), plus its potential impact on Group earnings. (See Exhibit 14.4 for a public version.)

Exhibit 14.4 Zurich Risk Radar

WORKING WITH EXTERNAL STAKEHOLDERS

Various external stakeholders, among them regulators, rating agencies, investors, and accounting bodies, have placed emphasis on the importance of a sound risk management program in the insurance industry. Regulatory requirements, such as the Swiss Solvency Test in Switzerland and the regulatory principles of Solvency III in the European Union, have emphasized a risk-based and economic approach, based on comprehensive quantitative and qualitative assessments and reports.

Rating agencies are now interested in enterprise risk management as a factor in evaluating companies' creditworthiness. Standard & Poor's, a rating agency with a separate rating for ERM, has rated Zurich's overall ERM as “strong.” Reinsurance and credit risk controls remain “excellent.” Market, asset/liability management (ALM), reserving, catastrophe, and operational risk controls, as well as strategic and emerging risk management, are seen as “strong.” Zurich is rated either “excellent” or “strong” in all of the Standard & Poor's dimensions for ERM.

Zurich also seeks external expertise from its International Advisory Council and Natural Catastrophe Advisory Council to better understand and assess risks, particularly regarding areas of complex change. In addition, the Investment Management Advisory Council provides feedback to Investment Management on achieving superior risk-adjusted returns versus liabilities for the Group's invested assets. Zurich also organizes various regional Risk Management Councils comprised of key customers, which engage to help identify and address issues together.

Zurich is involved in a number of international industry organizations engaged in advancing the regulatory dialogue and sound risk management practices pertaining to the insurance industry. It is also a standing member of and actively contributes to the Emerging Risk Initiative of the CRO Forum (an organization composed of the chief risk officers of major insurance companies and financial conglomerates that focuses on developing and promoting industry best practices in risk management).

Zurich actively participates in professional risk management bodies such as the Risk and Insurance Management Society (RIMS), the Institute of Risk Management (IRM), the Federation of European Risk Management Association (FERMA), and the Association of Insurance and Risk Managers in Industry and Commerce. For example, Zurich's staff serves on the RIMS ERM Committee and on the global Education Advisory Board of the IRM. It is also involved in various working groups in the Conference Board, supports the Red Cross in crisis recovery, and collaborates with other entities to help promote better risk identification, assessment, prevention, and mitigation.

Zurich is a main contributor to the Global Risk Report that is produced by the World Economic Forum in cooperation with other corporations (Swiss Re, Marsh & McLennan Companies, the Oxford Martin School [University of Oxford], the National University of Singapore, and the Wharton Risk Management and Decision Processes Center [University of Pennsylvania Center for Risk Management] [www.weforum.org/reports/global-risks-2012-seventhninth-edition]). The report's assessment of the most pressing global risks and the interconnections among them provides valuable information for risk mitigation worldwide. Supporting the report is also part of the Group's commitment to corporate responsibility by sharing Zurich's expertise to help businesses, nations, and society.

ZURICH'S PROPRIETARY TOOLS USED IN ERM FRAMEWORK

Zurich uses a variety of methodologies and tools to manage its business risk, with the following aims. More information on Zurich's Strategic Risk Management work can be found at www.zuricherm.com.

- Understand issues in enterprise strategy, resilience, supply chain, and business continuity.

- Identify scenarios that could—or should—be built into a strategic and/or operational resilience plan.

- Develop action points and risk responsibilities to help protect profitability.

Total Risk Profiling Tool

One of Zurich's key proprietary tools is called Total Risk Profiling (TRP); it is a workshop-based approach where a facilitator-led team develops a risk profile by determining relative ratings in probability and severity (likelihood and impact) for potential risk scenarios. (See Exhibit 14.5.) TRP is a structured approach to identifying, assessing, and monitoring holistic risks and improvement actions needed. By embedding its Total Risk Profiling methodology into its risk culture, this has helped ensure its risk management culture is consistent and effective across its various business units. It uses these risk scenarios to define the underlying issues and break them into components of vulnerability, trigger, and consequences. The TRP tool can also help a business unit define and quantify its risk tolerance limit. A short video explains more about Total Risk Profiling (http://zdownload.zurich.com/zna/TotalRiskProfiling.html).

Exhibit 14.5 Zurich Total Risk Profiling Tool

A risk tolerance limit is defined as part of the risk appetite, and action plans are developed to improve the prioritized risks and bring them within the business unit's tolerance for risk. The structure of the TRP risk identification process provides a sound basis for detailed quantification of more complex risks. TRP has helped Zurich's business units set the agenda for internal audit or enterprise risk management to monitor risks at or just below the risk tolerance boundary.

By being able to define multiple risk triggers with different potential consequences, the TRP tool has helped Zurich to identify the true drivers of risk by undertaking various stress tests or even to define new risk exposures. A facilitator-led team develops a relative rating for each risk scenario, often without a predefined scale of impact and likelihood, to improve the business unit's understanding of the risk.

Another main aim of the flexible TRP tool is to help embed a risk culture that will sustain shareholder value through better enterprise risk management practices and strategic planning processes. Zurich performs nearly 200 TRP workshops per year, ranging from assessing strategy execution, project management, human resources (HR), mergers and acquisitions (M&A), or business interruption (BI) exposures to new product development. In fact, completion of a TRP is a requisite part of the submission for a project budget or operational plan. The TRP tool helps to enable the following:

- Assessment of current and emerging risks to business resilience and profitability

- Alignment of business strategy with key performance indicators

- Communication of board discussion on risk appetite to investors and other stakeholders

- Reviewing the environmental scanning tool for corporate or competitive business strategy development

- Embedding of ERM in the strategic planning process

- Product launches, acquisitions or divestitures, and project management

- Considering the vulnerabilities in the supply chain

- Evaluation of business interruption risk scenarios

- Testing of existing strategies in the context of unrealized/underrealized risks and opportunities

- Use in the objective-setting stage of the business cycle to determine the budget

Zurich Hazard Analysis Tool

The Zurich Hazard Analysis is a powerful methodology to systematically identify, address, and manage various types of hazards or vulnerabilities and to address and manage the corresponding risks. The methodology is closely related to Total Risk Profiling, and is helpful in defining “pathways” of risks. Zurich has been successfully applying and using it within its operations and with customers for over 20 years in various industries, commercial enterprises, and, more recently, in the financial services industry, as well as public entities.

Zurich's Risk Room

Another of Zurich's proprietary tools, called the Zurich Risk Room, helps the organization and its customers to systematically explore major global risks, investigating how they are expressed on a country-by-country basis. (See Exhibit 14.6.) It shows on a 3-D screen how risks and geographies combine (sometimes unexpectedly) to be relevant to Zurich's business concerns. This tool allows one to see which countries reflect similar profiles, and which risks begin to stand out on mapping various risk correlations. By working across different types of risks, risk correlations are identified that illustrate whether relevant risk connections exist and which ones are the strongest.

Exhibit 14.6 Zurich's Risk Room

The Zurich Risk Room creates a statistical, fact-based assessment of global threats as they relate to business planning and implementation. Its output can complement departmental, regional, or consultant-based research and data, providing an additional objective lens to risk evaluation and reducing the issues related to silo-based risk assessments. Using a consistent global framework, the Zurich Risk Room can help identify threats that may cross boundaries and provide key decision makers with relevant risk information that can help them make more informed business decisions, even if they are not experts in risk analysis.

By examining risks and interconnections in detail, Zurich is able to compare both individual issues and overall country risk characteristics of one country to those of another. This allows Zurich to see whether a country's risk profile is unique or it shares similarities with other countries. For international businesses, it is vital to form a picture of where operations and investments are vulnerable and where these vulnerabilities may reside. Zurich is then able to identify how risks are bundled, or where a threat in one area might cascade to another.

A demo version of the Zurich Risk Room software for an iPad or Android tablet can be downloaded by searching for Zurich Risk Room in iTunes or Google Play. In addition, this is a link to a short video that will give a brief overview of the Zurich Risk Room application: www.youtube.com/watch?v=_UMaYJtDu6Q.

CATEGORIZING VARIOUS RISKS AT ZURICH

In order to enable a consistent, systematic, and disciplined approach to ERM, Zurich categorizes its main risks. (See Exhibit 14.7.) This grouping assists Zurich in monitoring any aggregation of exposures that may be accumulating across the enterprise and could, therefore, have a greater impact on the company.

Exhibit 14.7 Categorizing Various Risks at Zurich

Strategic Risks

Strategic risks are the unintended risks that can result as a by-product of planning or executing a strategy. For example, they can arise from the following:

- Inadequate assessment of strategic plans

- Improper implementation of strategic plans

- Unexpected changes to assumptions underlying plans

Risk considerations are a key element in the strategic decision-making process. The senior leadership team assesses the implications of strategic decisions on risk-based return measures and risk-based capital in order to optimize the risk/return profile and to take advantage of economically profitable growth opportunities as they arise.

Zurich works on reducing the unintended risks of strategic business decisions through its risk assessment processes and tools. The Group Executive Committee regularly assesses key strategic risk scenarios for the Group as a whole, including scenarios for emerging risks and their strategic implications.

An example of this is when Zurich evaluates the risks of mergers and acquisitions (M&A) transactions from both a quantitative and a qualitative perspective. Zurich conducts risk assessments of M&A transactions to evaluate risk, especially related to the integration of acquired businesses, to help increase the likelihood of successfully attaining the expected benefits. They may also review country-level exposures using the Zurich Risk Room tool.

Insurance Risks

Insurance risk is the inherent uncertainty regarding the occurrence, amount, and timing of insurance liabilities. The exposure is usually transferred to Zurich through the underwriting process. Zurich assumes certain customer risks and aims to manage that transfer of risk and to minimize unintended underwriting risks through the following:

- Establishing limits for underwriting authority

- Requiring specific approvals for transactions involving new products or where established limits of size and complexity may be exceeded

- Using a variety of reserving and modeling techniques to address the various insurance risks inherent in the insurance business

- Ceding insurance risks through proportional, nonproportional, and specific risk reinsurance treaties

Market Risks

Market risks can be associated with the Group's balance sheet positions where the value or cash flow depends on financial markets. Fluctuating risk drivers resulting in market risk may include:

- Equity market prices

- Real estate market prices

- Interest rates and credit spreads

- Currency exchange rates

Zurich has policies and limits to manage market risk. Zurich aligns its strategy asset allocation to its risk-taking capacity. The Group centralizes the management of certain asset classes to help control aggregation of risk, and provides a consistent approach to constructing portfolios and selecting external asset managers. Zurich also diversifies portfolios, investments, and asset managers. It regularly measures and manages market risk exposure. Zurich has established limits on concentration in investments by single issuers and certain asset classes, as well as deviations of asset interest rate sensitivities from liability interest rate sensitivities, and also has limits on investments that are illiquid.

Credit Risks

Credit risks are associated with a loss or potential loss from counterparties failing to fulfill their financial obligations. Zurich's exposure to credit risks may be derived from the following main categories of assets:

- Cash and cash equivalents

- Debt securities

- Reinsurance assets

- Mortgage loans and mortgage loans given as collateral

- Other loans

- Receivables

- Derivatives

Zurich strives to manage individual exposures as well as credit risk concentrations. Its objective in managing credit risks is to maintain them within parameters that reflect its strategic objectives and risk tolerance. Sources of credit risks are assessed and monitored, and Zurich has policies to manage special risks within various subcategories of credit risk. To assess counterparty credit risk, Zurich uses the rating assigned by external rating agencies, qualified third parties such as asset managers, and internal rating assessments. When there is a difference among external rating agencies, Zurich assesses the reason for the inconsistencies and applies the lowest of the respective ratings unless other indicators of credit quality justify the assignment of alternative internal credit ratings. Zurich maintains counterparty credit risk databases that record external and internal sources of credit intelligence.

Liquidity Risks

Risks that Zurich may not have sufficient liquidity to meet its obligations when they fall due, or would have to incur excessive costs to do so, are categorized as liquidity risks. Zurich's policy is to maintain adequate liquidity and contingent liquidity to meet its liquidity needs under both normal and stressed conditions.

Zurich has groupwide liquidity management policies and specific guidelines as to how local businesses have to plan, manage, and report their local liquidity. These include regularly conducting stress tests for all major carriers within Zurich. The stress tests use a standardized set of internally defined stress events and are designed to provide an overview of the potential liquidity drain that Zurich would face if it had to recapitalize local balance sheets.

Operational Risks

Operational risks can be associated with Zurich's people, processes, and systems, and external events such as outsourcing, catastrophes, legislation, or external fraud. Zurich has a comprehensive framework with a common approach to identify, assess, quantify, mitigate, monitor, and report operational risks within the scenario-based assessments, internal controls evaluations, and loss event data.

In the area of information security, Zurich continues to focus on its global improvement program with special emphasis on protecting customer information, improving security with its suppliers, and monitoring that access to information is properly controlled. This helps Zurich better protect information assets and ensure greater alignment with regulation and policies. A key consideration is maintaining and developing the capability of Zurich's business continuity with an emphasis on recovery from possible risk events such as natural catastrophe or pandemic. Zurich continues to develop its existing business continuity capability by further implementing a more globally consistent approach to business continuity and crisis management.

Focusing on the risk of claims fraud and nonclaims fraud continues to be of great importance to Zurich. Zurich continues its global antifraud initiative to further improve Zurich's ability to prevent, detect, and respond to fraud. While claims fraud is calculated as part of insurance risk and nonclaims fraud is calculated as part of operational risk for risk-based capital, both are part of the common framework for assessing and managing operational risks. Zurich considers risk controls to be key instruments for monitoring and managing operational risks. The operational effectiveness of key controls is assessed by self-assessments and independent testing of controls supporting the financial statements.

Reputation Risks

Reputation risks are risks that might arise from an act or omission by Zurich or any of its employees that could result in damage to the Group's reputation or loss of trust among its stakeholders. Every risk type could have potential consequences for Zurich's reputation, and therefore effectively managing its exposures holistically and systematically helps Zurich reduce threats to its reputation.

CAPITAL MANAGEMENT

Capital and solvency are managed through an integrated and comprehensive framework of principles and governance structures as well as methodology, monitoring, and reporting processes. The capital management process is illustrated in Exhibit 14.8. At the group executive level, the Group Balance Sheet Committee defines the capital management strategy and sets the principles, standards, and policies for the execution of the strategy. Group Treasury and Capital Management are responsible for the execution of the capital management strategy within the mandate set by the Group Balance Sheet Committee.

Exhibit 14.8 Zurich's Capital Management Strategy

Within these defined principles, the group manages its capital using a number of different capital models, taking into account regulatory, economic, and rating agency constraints. The capital and solvency position is monitored and reported on a regular basis. Based on the results of the capital models and the defined standards and principles, Group Treasury and Capital Management has a set of measures and tools available to manage capital within the defined constraints. This tool set is referred to as the Capital Management Program.

The Capital Management Program comprises various measures to optimize shareholders' return and to meet capital needs, while enabling Zurich to take advantage of growth opportunities as they arise. Such measures are used as and when required and could include efficient balance sheet structuring as well as cash dividends, share buy-backs, special dividends, issuances of shares or senior and subordinated debt, and purchase of reinsurance.

The group seeks to maintain the balance between higher returns for shareholders on equity raised, which may be possible with higher levels of borrowing, and the security provided by a sound capital position. The payment of dividends, share buy-backs, and issuances and redemption of debt can have an important influence on Zurich's capital levels.

Zurich Economic Capital Model

In addition to a qualitative approach to measuring risks, Zurich regularly measures and quantifies material risks to which it is exposed through both TRP and the Zurich Economic Capital Model (Z-ECM). This model provides a key input into the strategic planning process, as it allows an assessment as to whether its risk profile is in line with its risk tolerance level. In particular, Z-ECM forms the basis for optimizing Zurich's risk/return profile by providing consistent risk measurement across the Group.

Zurich uses Z-ECM to assess the economic capital consumption of its business with a balance sheet approach. Under the balance sheet approach one looks at the change in stockholders' or owners' equity to determine the amount of net income during the period between balance sheets. The Z-ECM framework is embedded in Zurich's risk culture and plays a critical role in decision making, and is used in capital allocation, business performance management, pricing, reinsurance purchasing, transaction evaluation, and risk optimization, as well as regulatory, investor, and rating agency communication. Z-ECM quantifies the capital required for insurance-related risk (including premium and reserve, natural catastrophe, business, and life insurance), market risk (market/ALM [asset/liability management]), credit risk (including reinsurance credit and investment credit), and operational risks.

At the Group level, Zurich compares Z-ECM capital required to the Z-ECM available financial resources (Z-ECM AFR) to derive an economic solvency ratio (Z-ECM ratio). Z-ECM AFR reflects financial resources available to cover policyholder liabilities in excess of their expected value. It is derived by adjusting the International Financial Reporting Standards (IFRS) shareholders' equity to reflect the full economic capital base available to absorb any unexpected volatility in Zurich's business activities. As part of Z-ECM, Zurich uses a scenario-based approach to assess, model, and quantify the capital required for operational risk for business units under extreme circumstances and a very small probability of occurrence (internal model calibrated to a confidence level of 99.95 percent over a one-year time horizon).

Analysis of Capital Adequacy

Zurich maintains interactive relationships with three global rating agencies: Standard & Poor's, Moody's, and A.M. Best. The Insurance Financial Strength Rating (IFSR) of Zurich's main operating entity is an important element of its competitive position. Moreover, Zurich's credit ratings that are derived from its financial strength rating do, in fact, affect its cost of capital, just like any other credit-rated company.

In each country in which Zurich operates, the local regulator specifies the minimum amount and type of capital that each of the regulated entities must hold in relation to its liabilities. In addition to maintaining the minimum capital required to comply with the solvency requirements, Zurich targets holding an adequate buffer of capital reserves to ensure that each of its regulated subsidiaries meets the local capital requirements. Zurich is subject to different capital requirements depending on the country in which it operates. The main areas are Switzerland and European Economic Area countries, and the United States.

Since January 1, 2011, the Swiss Solvency Test (SST) capital requirements are binding in Switzerland. The Group uses an adaptation of its internal Risk-Based Capital (RBC) model to comply with the SST requirements and runs a full SST calculation twice a year. The model is still subject to Swiss Financial Market Supervisory Authority (FINMA) approval.

ZURICH'S BUSINESS RESILIENCE TOOLS

Business resilience management helps provide Zurich with the structure for dealing with risks systematically, holistically, and successfully. Zurich's Business Resilience program is supported by an enterprise risk management framework that identifies particular events or circumstances relevant to its business objectives, assesses them in terms of likelihood and magnitude of impact, and then determines a response strategy. (See Exhibit 14.9.) A resilient enterprise is better able to anticipate surprises, recover more quickly from disruptions, adapt to changing conditions, and leverage emerging opportunities.

Exhibit 14.9 Zurich's Business Resilience Program

The objective of Zurich's Business Resilience program is “Prepared, Informed, and Resilient.” This tagline is regularly communicated to staff, especially during Business Resilience Awareness week. Some of Zurich's proprietary Business Resilience tools are listed here.

Business Interruption Modeling allows Zurich the capability to better manage its risks based on an in-depth understanding of the value chain, with a main focus on the business critical value flow, followed by identification, assessment, and quantification of business interruption exposures and optional mitigations. Like all organizations, a business interruption for Zurich could have the potential to inhibit productivity and could have multiple negative impacts on its organization. Some examples of business interruption impacts could include loss of customers, diminished customer service, legal and/or regulatory issues, lower employee morale, and even delays in projects, products, or other strategic growth. Thus, it is essential that organizations try to map and quantify how they serve customers, in order to proactively protect where they generate value.

Key stages of Business Interruption Modeling include:

- Defining scope by identifying the business-critical part(s) of the value chain

- Building an interdependency framework of business-critical value flows

- Identifying relevant business interruption vulnerabilities as loss of resources such as supplier, production, storage, and customer

- Assessing the extent based on interruption scenarios, and modeling the effects quantitatively

- Prioritizing risks based on financial impact of scenarios, with focus on unacceptable risks in order to develop a beneficial mitigation plan

- Assessing the effectiveness of current business continuity plans and identifying improvement actions

Supply Chain Risk Assessment allows Zurich to improve its reliability and minimize the effects of a supply chain disruption on its capital and earnings. Zurich's supplier risk assessment should help address vulnerabilities that could inhibit Zurich's ability to respond to a changing risk landscape. Its supply chain risk evaluation, mapping, and grading are designed to assess and quantify the broad areas of exposures and risk controls in its supply chain. This gives Zurich actionable insights to help facilitate mitigation strategies that can address the characteristics of each supplier individually, including risk transfer options.

The stages of a Supply Chain Risk Assessment include:

- Develop a supply chain/value chain map.

- Gather key supply/supplier details.

- Evaluate risk factor information.

- Define and evaluate potential risk or loss scenarios.

- Develop risk grading for each critical supplier.

- Determine risk strategies.

Business Continuity Management (BCM) includes the mitigation strategies used to minimize the impact after an incident, with the possible scope of risks coming from supply chain risks, strategic risks, operational risks, technological risks, or natural hazards. BCM is very useful in identifying gaps in risk mitigation strategies and improving risk controls to manage those exposures more effectively. As part of Zurich's business resilience process, BCM is important for managing the multitude of risk exposures and potential interruptions scenarios and thus strengthening Zurich's business resilience program.

Zurich's Six-Stage Business Continuity Management Life Cycle

- Modeling key business processes

- Business impact analysis

- BCM strategy and processes

- Business continuity planning

- Crisis management

- Training, exercise, maintenance, and assessment

Zurich is able to undertake a regular gap analysis of its business continuity plans against best practices and common BCM-related standards such as International Standards Organization (ISO), National Fire Protection Association (NFPA) and the British Standard. It also routinely tests its crisis response activities. For example, it has planned or completed simulation exercises such as:

- Eurostar trains caught in tunnel

- India: Bomb explosion in hotel where Zurich has employees, impacting the country where company has operations in Pune, Bangalore, and Chennai

- Fire in Home Office location injuring employees, impacting critical processes, and possibly preventing occupancy in location for up to three to four months

- Los Angeles earthquake

- Kansas tornado

- Political demonstration in New York City

Business Impact Analysis is designed to provide the method to identify the systems that, when absent, would create a danger to the survival of the organization. This analysis can also ensure that these systems receive the correct priority in any subsequent business continuity plan.

Key stages of Zurich's Business Impact Analysis include:

- Prioritize the key business services or processes.

- Identify the internal and external risks to the continuity of these business processes.

- Assess the importance of each risk in terms of both the likelihood and the financial impact of potential outcomes.

- Establish priorities for mitigating the critical risks.

- Develop a management plan of action.

- Assess the business continuity plan and management plan of action.

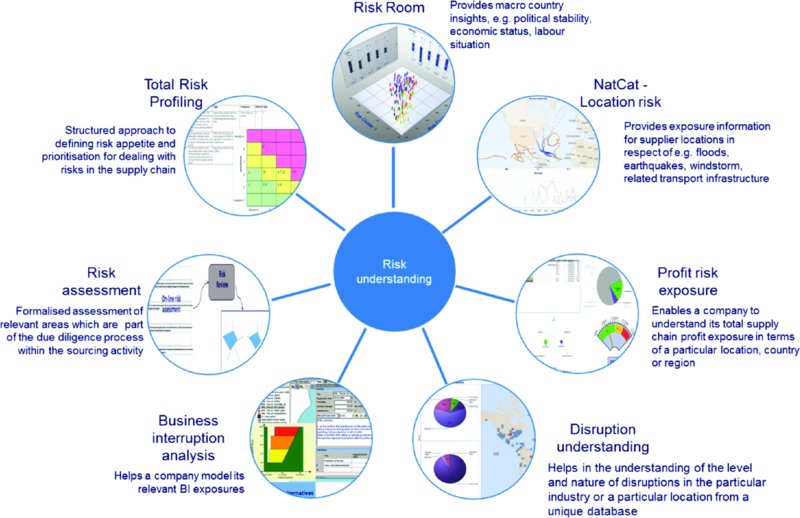

HOW ZURICH USES ITS ERM TOOLS TO CREATE NEW VALUE

In the area of mergers and acquisitions, Zurich may use two opportunity analysis tools to supplement traditional due diligence practices. Both the Total Risk Profiling tool and the Zurich Risk Room can be used to simulate various risk scenarios and investigate potential outcomes. (See Exhibit 14.10.) When Zurich acquired holdings in Asia and Latin America, these tools served to help identify and understand the risks associated with the strategy, so they could be managed accordingly and increase the likelihood of success on these opportunities.

Exhibit 14.10 Zurich Business Resilience Tools

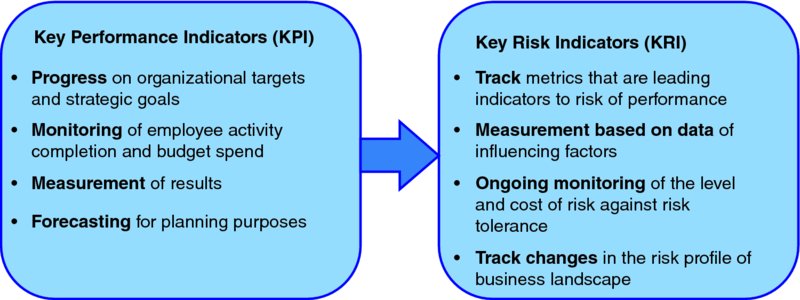

While key performance indicators (KPIs) can help an organization understand how well it is performing in relation to its strategic objectives, key risk indicators (KRIs) are leading indicators of risks to business performance. (See Exhibit 14.11.)

Exhibit 14.11 Zurich Key Performance Indicators and Key Risk Indicators

Zurich's ERM tools can add value by helping to determine and embed KRIs within an operations to provide an early warning that potential risks are on the rise. Some examples of Zurich using KRIs to monitor risks are in the areas of natural catastrophe risks (percentage of group shareholder equity), asset-liability matching (duration mismatch), strategic asset allocation (mix of investment across categories), and credit risk (weighted average credit rating).

Zurich has the opportunity to create value through business resiliency as well, which addresses disruption to business operations. It can use a combination of modeling software, supply chain risk assessment software, and business continuity gap analysis techniques to evaluate its exposure. It has recently appointed a supply chain risk officer, who reports into Zurich's CRO organization and is tasked with finding the appropriate balance between cost and reliability. It has a business continuity planning team throughout its operating regions, and maintains a robust network of champions within the business, trained to return the business to operation quickly and efficiently after a disruption. The business continuity team regularly exercises a variety of plans to ensure that Zurich can be ready for many potential risk situations. Stress-testing activities take place in parallel to ensure that the network is prepared to shift workload, deploy contingencies, and remain operational, particularly when customers may have suffered from the same event.

With new projects or product development opportunities, Zurich can also use its Total Risk Profiling (TRP) tool to evaluate risk scenarios that may prevent it from delivering on time, on budget, and with the expected results. Completion of a TRP analysis is normally required as part of most requests for project approval and budget. Improvement actions are assigned to risk owners during TRP sessions, and monitored regularly to ensure risk reduction. The TRP tool can also help with quantifying the potential exposure and risk tolerance level. For example, TRP was used as an analysis tool before considering outsourcing IT services, helping to vet the solution as a viable alternative. The risk assessment team assigned risk improvement actions to individuals, and proceeded with the project. The TRP was regularly updated and benchmarked throughout the course of the project, as risks changed and new ones surfaced. The TRP assessment can even be used as a yes/no decision gate during the project phases to help determine that the expected project benefits still outweigh the risks.

The TRP methodology can also be used at the board and senior management levels to help develop strategic (top-down) scenarios that can be applied consistently during operational (bottom-up) assessments across the enterprise. This has helped to ensure uniform handling of certain systemic issues and exposures to better balance the risks and rewards of new opportunities. It is very important to Zurich to set financial parameters around managing current risk issues and guiding key business decisions going forward. The TRP process can build team commitment and focuses management expertise on dedicating resources to mitigate those risks that are outside the risk tolerance level and pose the greatest barriers to achieving corporate objectives.

Another use of the TRP methodology is its employment in a risk tolerance workshop. Establishing a corporate risk tolerance is a critical step in helping increase business controls and profitability across an enterprise. The corporate risk boundary provides a clear indication of both an acceptable risk appetite for new opportunities and an unacceptable risk threshold for downside cost on potential exposures. Risk tolerance is often defined as the level of variability that an organization is willing to accept in its aggregate earnings and capital value at risk (VaR) limits. It is essential to both define and apply corporate risk tolerance in order to prioritize the most critical areas for risk improvement. The risk appetite at Zurich is set by senior management, and then broadly articulated and followed by business and functional areas.

Zurich's ERM program also contributes to its core business through the processes and procedures to review customer risks. Zurich performs credit checks to monitor collateral and financial viability of many of its customers and suppliers. Its cross-divisional Emerging Risk Group is tasked with scanning the horizon for new exposures that may impact Zurich and its customers. Zurich reviews customers' loss control techniques and provides best practices guidance through nearly 1,000 risk engineers who specialize in safety and operational risks around the world, serving the dual purpose of supporting customers' needs as well as protecting Zurich's own portfolio. Last, accumulations within Zurich's risk portfolio are monitored via a database to identify areas of disproportionate exposure to a single company, industry, supplier, or geographic location.

CONCLUSION

Every organization's directors and officers will approach ERM differently in order to achieve their unique objectives. Zurich has taken many steps to help develop a strong and effective ERM program. This program did not emerge overnight, but today Zurich views its ERM program as a competitive advantage well worth the investment. Despite having embedded a robust program into the fabric of its business, Zurich does not rest on its laurels. The program is constantly scrutinized in search of better ways to identify, assess, manage, and monitor Zurich's key risks. The company has even developed an ERM Gap Analysis that can be done yearly to help determine risk maturity and focus on its top areas for improvement. The organization's management continuously looks for opportunities to create a closer partnership between ERM and the core business, so that its ERM team is ready to consult and assist the business in understanding risk in pursuit of profit. ERM is certainly a long journey defined by many paths, but one that can continue to yield tremendous benefits for the organization.

APPENDIX

Internally, Zurich uses its Risk-Based Capital (RBC) model, which also forms the basis of the SST model. The RBC model targets a total capital level that is calibrated to an AA-rated financial strength. Zurich defines RBC as being the capital required to protect the Group's policyholders in order to meet all of their claims with a confidence level of 99.95 percent over a one-year time horizon.

While the Group's RBC model and the SST model are broadly the same, the following is a summary of the main differences between the three approaches:

- Model calibration. The RBC calibration is based on a value at risk at a 99.95 percent confidence level, whereas SST calibration is based on an expected shortfall at a 99 percent confidence level. The Group thereby sets itself a higher financial strength target than the SST regulatory requirement.

- Scope. Operational and business risks for General Insurance are reflected in RBC, but are not required in SST.

- Market/ALM risk. The extreme scenario for market/ALM risk in RBC is directly attributed to that risk, whereas extreme scenarios in SST are aggregated to the combination of all risk types. This treatment of the extreme scenario in the RBC model leads to a more conservative result than in the SST model.

- Available financial resources (AFR). Senior debt is included in AFR for RBC purposes, but not included in AFR for the SST calculation.

Zurich uses RBC to assess the economic capital consumption of its business in a one-balance-sheet approach. The RBC framework is an integral part of how Zurich is managed. The RBC framework is embedded in Zurich's organization and decision making, and is used in capital allocation, business performance management, pricing, reinsurance purchasing, transaction evaluation, and risk optimization, as well as regulatory, investor, and rating agency communication.

Zurich compares RBC to its AFR to derive an economic solvency ratio. AFR reflects financial resources available to cover policyholder liabilities in excess of their expected value. It is derived by adjusting the IFRS shareholders' equity to reflect the full economic capital base available to absorb any unexpected volatility in the Group's business activities.

At a Group level, the management committees dealing with risks are:

- The Group Balance Sheet Committee (GBSC) acts as a cross-functional body whose main function is to control the activities that materially affect the balance sheets of the Group and its subsidiaries. The GBSC is charged with setting the annual capital and balance sheet plans for the Group based on the Group's strategy and financial plans, as well as recommending specific transactions or unplanned business changes to the Group's balance sheet. The GBSC has oversight of all main levers of the balance sheet, including capital management, reinsurance, asset/liability management, and liquidity. The GBSC reviews and recommends the Group's overall risk tolerance. It is chaired by the CEO.

- The Group Finance and Risk Committee (GFRC) acts as a cross-functional body for financial and risk management matters in the context of the strategy and the overall business activity of the Group. The GFRC oversees financial implications of business decisions and the effective management of the Group's overall risk profile, including risks related to insurance, financial markets and asset/liability, and credit and operational risks, as well as their interactions. The GFRC proposes remedial actions based on regular briefings from Group Risk Management on the risk profile of the Group. It reviews and formulates recommendations for future courses of action with respect to potential mergers and acquisitions (M&A) transactions, changes to the Zurich Risk Policy, internal insurance programs for the Group, material changes to the Group's risk-based capital methodology, and the overall risk tolerance. The GFRC is chaired by the chief financial officer, while the chief risk officer acts as deputy.

The management committees rely on output provided by technical committees, including:

- The Asset/Liability Management and Investment Committee (ALMIC) deals with the Group's asset/liability exposure and investment strategies and is chaired by the chief investment officer.

- The General Insurance Global Underwriting Committee (GUC) acts as a focal point for underwriting policy and related risk controls for General Insurance and is chaired by the Global Chief Underwriting Officer for General Insurance.

- The Group Reinsurance Committee (GRC) defines the Group's reinsurance strategy in alignment with its risk framework and is chaired by the Global Head of Group Reinsurance.

ABOUT THE CONTRIBUTORS

Linda Conrad is Director of Strategic Business Risk Management for Zurich. She leads a global team responsible for delivering tactical solutions to Zurich and to customers on strategic issues such as business resilience, supply chain risk, enterprise risk management (ERM), risk culture, and Total Risk Profiling. Linda also addresses enterprise resiliency issues in print and television appearances, including CNBC, Fox Business News, and the Financial Times, and is featured in a Wall Street Journal microsite at www.supplychainriskinsights.com.

Linda holds a Specialist designation in ERM, and serves on the global Education Advisory Board of the Institute of Risk Management in London. Linda is deputy member of the ERM Committee of the Risk and Insurance Management Society (RIMS), sits on the Supply Chain Risk Leadership Council, and was chairwoman of the Asian Risk Management Conference. She taught at the University of Delaware Captive program and in the Master's on Supply Chain Management program at the University of Michigan's Ross School of Business, where she serves on the Corporate Advisory Council. Linda studied at the Graduate Institute of International Studies in Geneva, Switzerland, and Fox Business School.

Kristina Narvaez is the president and owner of ERM Strategies, LLC, which offers ERM research and training to organizations on various ERM-related topics. She graduated from the University of Utah in environmental risk management and then received her MBA from Westminster College. She is a two-time Spencer Education Foundation Graduate Scholar from the Risk and Insurance Management Society and has published more than 30 articles relating to enterprise risk management and board risk governance. She has given many presentations to various risk management associations on topics of ERM. She teaches a Business Strategy class at Brigham Young University.

QUESTIONS

- How do Zurich ERM tools help them better understand their existing and emerging risks?

- How are Zurich's risk roles and responsibilities impacting their risk culture?

- Why is it important to include a Business Resilience program in your organization's ERM program?

- How is Zurich's Capital Management program helping their ERM program?

- Give some examples on how Zurich has created new value through their ERM program?

REFERENCES

- Bugalla, John, Linda Conrad, and Kristina Narvaez. 2013. Presentation given at Risk and Insurance Management Society Annual Conference in Los Angeles, April 22.

- Conrad, Linda. 2013. Presentation given at Risk and Insurance Management Society ERM Conference in San Francisco, November 4.

- Zurich Insurance Group. 2012. Zurich Risk Report.

ABOUT THE CONTRIBUTORS

Linda Conrad is Director of Strategic Business Risk Management for Zurich. She leads a global team responsible for delivering tactical solutions to Zurich and to customers on strategic issues such as business resilience, supply chain risk, enterprise risk management (ERM), risk culture, and Total Risk Profiling. Linda also addresses enterprise resiliency issues in print and television appearances, including CNBC, Fox Business News, and the Financial Times, and is featured in a Wall Street Journal microsite at www.supplychainriskinsights.com.

Linda holds a Specialist designation in ERM, and serves on the global Education Advisory Board of the Institute of Risk Management in London. Linda is deputy member of the ERM Committee of the Risk and Insurance Management Society (RIMS), sits on the Supply Chain Risk Leadership Council, and was chairwoman of the Asian Risk Management Conference. She taught at the University of Delaware Captive program and in the Master's on Supply Chain Management program at the University of Michigan's Ross School of Business, where she serves on the Corporate Advisory Council. Linda studied at the Graduate Institute of International Studies in Geneva, Switzerland, and Fox Business School.

Kristina Narvaez is the president and owner of ERM Strategies, LLC, which offers ERM research and training to organizations on various ERM-related topics. She graduated from the University of Utah in environmental risk management and then received her MBA from Westminster College. She is a two-time Spencer Education Foundation Graduate Scholar from the Risk and Insurance Management Society and has published more than 30 articles relating to enterprise risk management and board risk governance. She has given many presentations to various risk management associations on topics of ERM. She teaches a Business Strategy class at Brigham Young University.