In this chapter we should like to present a sample of security analysis in operation. We have selected, more or less at random, four companies which are found successively on the New York Stock Exchange list. These are ELTRA Corp. (a merger of Electric Autolite and Mergenthaler Linotype enterprises), Emerson Electric Co. (a manufacturer of electric and electronic products), Emery Air Freight (a domestic forwarder of air freight), and Emhart Corp. (originally a maker of bottling machinery only, but now also in builders’ hardware).* There are some broad resemblances between the three manufacturing firms, but the differences will seem more significant. There should be sufficient variety in the financial and operating data to make the examination of interest.

In Table 13-1 we present a summary of what the four companies were selling for in the market at the end of 1970, and a few figures on their 1970 operations. We then detail certain key ratios, which relate on the one hand to performance and on the other to price. Comment is called for on how various aspects of the performance pattern agree with the relative price pattern. Finally, we shall pass the four companies in review, suggesting some comparisons and relationships and evaluating each in terms of the requirements of a conservative common-stock investor.

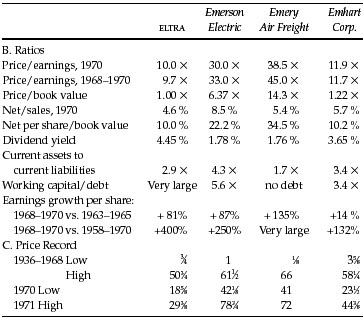

TABLE 13-2 A Comparison of Four Listed Companies

The most striking fact about the four companies is that the current price/earnings ratios vary much more widely than their operating performance or financial condition. Two of the enterprises—ELTRA and Emhart—were modestly priced at only 9.7 times and 12 times the average earnings for 1968–1970, as against a similar figure of 15.5 times for the DJIA. The other two—Emerson and Emery—showed very high multiples of 33 and 45 times such earnings. There is bound to be some explanation of a difference such as this, and it is found in the superior growth of the favored companies’ profits in recent years, especially by the freight forwarder. (But the growth figures of the other two firms were not unsatisfactory.)

For more comprehensive treatment let us review briefly the chief elements of performance as they appear from our figures.

1. Profitability. (a) All the companies show satisfactory earnings on their book value, but the figures for Emerson and Emery are much higher than for the other two. A high rate of return on invested capital often goes along with a high annual growth rate in earnings per share.* All the companies except Emery showed better earnings on book value in 1969 than in 1961; but the Emery figure was exceptionally large in both years. (b) For manufacturing companies, the profit figure per dollar of sales is usually an indication of comparative strength or weakness. We use here the “ratio of operating income to sales,” as given in Standard & Poor’s Listed Stock Reports. Here again the results are satisfactory for all four companies, with an especially impressive showing by Emerson. The changes between 1961 and 1969 vary considerably among the companies.

2. Stability. This we measure by the maximum decline in per-share earnings in any one of the past ten years, as against the average of the three preceding years. No decline translates into 100% stability, and this was registered by the two popular concerns. But the shrinkages of ELTRA and Emhart were quite moderate in the “poor year” 1970, amounting to only 8% each by our measurement, against 7% for the DJIA.

3. Growth. The two low-multiplier companies show quite satisfactory growth rates, in both cases doing better than the Dow Jones group. The ELTRA figures are especially impressive when set against its low price/earnings ratio. The growth is of course more impressive for the high-multiplier pair.

4. Financial Position. The three manufacturing companies are in sound financial condition, having better than the standard ratio of $2 of current assets for $1 of current liabilities. Emery Air Freight has a lower ratio; but it falls in a different category, and with its fine record it would have no problem raising needed cash. All the companies have relatively low long-term debt. “Dilution” note: Emerson Electric had $163 million of market value of low-dividend convertible preferred shares outstanding at the end of 1970. In our analysis we have made allowance for the dilution factor in the usual way by treating the preferred as if converted into common. This decreased recent earnings by about 10 cents per share, or some 4%.

5. Dividends. What really counts is the history of continuance without interruption. The best record here is Emhart’s, which has not suspended a payment since 1902. ELTRA’S record is very good, Emerson’s quite satisfactory, Emery Freight is a newcomer. The variations in payout percentage do not seem especially significant. The current dividend yield is twice as high on the “cheap pair” as on the “dear pair,” corresponding to the price/earnings ratios.

6. Price History. The reader should be impressed by the percentage advance shown in the price of all four of these issues, as measured from the lowest to the highest points during the past 34 years. (In all cases the low price has been adjusted for subsequent stock splits.) Note that for the DJIA the range from low to high was on the order of 11 to 1; for our companies the spread has varied from “only” 17 to 1 for Emhart to no less than 528 to 1 for Emery Air Freight.* These manifold price advances are characteristic of most of our older common-stock issues, and they proclaim the great opportunities of profit that have existed in the stock markets of the past. (But they may indicate also how overdone were the declines in the bear markets before 1950 when the low prices were registered.) Both ELTRA and Emhart sustained price shrinkages of more than 50% in the 1969–70 price break. Emerson and Emery had serious, but less distressing, declines; the former rebounded to a new all-time high before the end of 1970, the latter in early 1971.

General Observations on the Four Companies

Emerson Electric has an enormous total market value, dwarfing the other three companies combined.* It is one of our “good-will giants,” to be commented on later. A financial analyst blessed (or handicapped) with a good memory will think of an analogy between Emerson Electric and Zenith Radio, and that would not be reassuring. For Zenith had a brilliant growth record for many years; it too sold in the market for $1.7 billion (in 1966); but its profits fell from $43 million in 1968 to only half as much in 1970, and in that year’s big selloff its price declined to 22½ against the previous top of 89. High valuations entail high risks.

Emery Air Freight must be the most promising of the four companies in terms of future growth, if the price/earnings ratio of nearly 40 times its highest reported earnings is to be even partially justified. The past growth, of course, has been most impressive. But these figures may not be so significant for the future if we consider that they started quite small, at only $570,000 of net earnings in 1958. It often proves much more difficult to continue to grow at a high rate after volume and profits have already expanded to big totals. The most surprising aspect of Emery’s story is that its earnings and market price continued to grow apace in 1970, which was the worst year in the domestic air-passenger industry. This is a remarkable achievement indeed, but it raises the question whether future profits may not be vulnerable to adverse developments, through increased competition, pressure for new arrangements between forwarders and airlines, etc. An elaborate study might be needed before a sound judgment could be passed on these points, but the conservative investor cannot leave them out of his general reckoning.

Emhart and ELTRA. Emhart has done better in its business than in the stock market over the past 14 years. In 1958 it sold as high as 22 times the current earnings—about the same ratio as for the DJIA. Since then its profits tripled, as against a rise of less than 100% for the Dow, but its closing price in 1970 was only a third above the 1958 high, versus 43% for the Dow. The record of ELTRA is somewhat similar. It appears that neither of these companies possesses glamour, or “sex appeal,” in the present market; but in all the statistical data they show up surprisingly well. Their future prospects? We have no sage remarks to make here, but this is what Standard & Poor’s had to say about the four companies in 1971:

ELTRA—“Long-term Prospects: Certain operations are cyclical, but an established competitive position and diversification are offsetting factors.”

Emerson Electric—“While adequately priced (at 71) on the current outlook, the shares have appeal for the long term…. A continued acquisition policy together with a strong position in industrial fields and an accelerated international program suggests further sales and earnings progress.”

Emery Air Freight—“The shares appear amply priced (at 57) on current prospects, but are well worth holding for the long pull.”

Emhart—“Although restricted this year by lower capital spending in the glass-container industry, earnings should be aided by an improved business environment in 1972. The shares are worth holding (at 34).”

Conclusions: Many financial analysts will find Emerson and Emery more interesting and appealing stocks than the other two—primarily, perhaps, because of their better “market action,” and secondarily because of their faster recent growth in earnings. Under our principles of conservative investment the first is not a valid reason for selection—that is something for the speculators to play around with. The second has validity, but within limits. Can the past growth and the presumably good prospects of Emery Air Freight justify a price more than 60 times its recent earnings?1 Our answer would be: Maybe for someone who has made an in-depth study of the possibilities of this company and come up with exceptionally firm and optimistic conclusions. But not for the careful investor who wants to be reasonably sure in advance that he is not committing the typical Wall Street error of overenthusiasm for good performance in earnings and in the stock market.* The same cautionary statements seem called for in the case of Emerson Electric, with a special reference to the market’s current valuation of over a billion dollars for the intangible, or earning-power, factor here. We should add that the “electronics industry,” once a fair-haired child of the stock market, has in general fallen on disastrous days. Emerson is an outstanding exception, but it will have to continue to be such an exception for a great many years in the future before the 1970 closing price will have been fully justified by its subsequent performance.

By contrast, both ELTRA at 27 and Emhart at 33 have the earmarks of companies with sufficient value behind their price to constitute reasonably protected investments. Here the investor can, if he wishes, consider himself basically a part owner of these businesses, at a cost corresponding to what the balance sheet shows to be the money invested therein.* The rate of earnings on invested capital has long been satisfactory; the stability of profits also; the past growth rate surprisingly so. The two companies will meet our seven statistical requirements for inclusion in a defensive investor’s portfolio. These will be developed in the next chapter, but we summarize them as follows:

- Adequate size.

- A sufficiently strong financial condition.

- Continued dividends for at least the past 20 years.

- No earnings deficit in the past ten years.

- Ten-year growth of at least one-third in per-share earnings.

- Price of stock no more than 1½ times net asset value.

- Price no more than 15 times average earnings of the past three years.

We make no predictions about the future earnings performance of ELTRA or Emhart. In the investor’s diversified list of common stocks there are bound to be some that prove disappointing, and this may be the case for one or both of this pair. But the diversified list itself, based on the above principles of selection, plus whatever other sensible criteria the investor may wish to apply, should perform well enough across the years. At least, long experience tells us so.

A final observation: An experienced security analyst, even if he accepted our general reasoning on these four companies, would have hesitated to recommend that a holder of Emerson or Emery exchange his shares for ELTRA or Emhart at the end of 1970—unless the holder understood clearly the philosophy behind the recommendation. There was no reason to expect that in any short period of time the low-multiplier duo would outperform the high-multipliers. The latter were well thought of in the market and thus had a considerable degree of momentum behind them, which might continue for an indefinite period. The sound basis for preferring ELTRA and Emhart to Emerson and Emery would be the client’s considered conclusion that he preferred value-type investments to glamour-type investments. Thus, to a substantial extent, common-stock investment policy must depend on the attitude of the individual investor. This approach is treated at greater length in our next chapter.

Commentary on Chapter 13

In the Air Force we have a rule: check six. A guy is flying along, looking in all directions, and feeling very safe. Another guy flies up behind him (at “6 o’clock”—“12 o’clock” is directly in front) and shoots. Most airplanes are shot down that way. Thinking that you’re safe is very dangerous! Somewhere, there’s a weakness you’ve got to find. You must always check six o’clock.

—U.S. Air Force Gen. Donald Kutyna

E-Business

As Graham did, let’s compare and contrast four stocks, using their reported numbers as of December 31, 1999—a time that will enable us to view some of the most drastic extremes of valuation ever recorded in the stock market.

Emerson Electric Co. (ticker symbol: EMR) was founded in 1890 and is the only surviving member of Graham’s original quartet; it makes a wide array of products, including power tools, air-conditioning equipment, and electrical motors.

EMC Corp. (ticker symbol: EMC) dates back to 1979 and enables companies to automate the storage of electronic information over computer networks.

Expeditors International of Washington, Inc. (ticker symbol: EXPD), founded in Seattle in 1979, helps shippers organize and track the movement of goods around the world.

Exodus Communications, Inc. (ticker symbol: EXDS) hosts and manages websites for corporate customers, along with other Internet services; it first sold shares to the public in March 1998.

This table summarizes the price, performance, and valuation of these companies as of year-end 1999:

Electric, Not Electrifying

The most expensive of Graham’s four stocks, Emerson Electric, ended up as the cheapest in our updated group. With its base in Old Economy industries, Emerson looked boring in the late 1990s. (In the Internet Age, who cared about Emerson’s heavy-duty wet-dry vacuums?) The company’s shares went into suspended animation. In 1998 and 1999, Emerson’s stock lagged the S & P 500 index by a cumulative 49.7 percentage points, a miserable underperformance.

But that was Emerson the stock. What about Emerson the company? In 1999, Emerson sold $14.4 billion worth of goods and services, up nearly $1 billion from the year before. On those revenues Emerson earned $1.3 billion in net income, or 6.9% more than in 1998. Over the previous five years, earnings per share had risen at a robust average rate of 8.3%. Emerson’s dividend had more than doubled to $1.30 per share; book value had gone from $6.69 to $14.27 per share. According to Value Line, throughout the 1990s, Emerson’s net profit margin and return on capital—key measures of its efficiency as a business—had stayed robustly high, around 9% and 18% respectively. What’s more, Emerson had increased its earnings for 42 years in a row and had raised its dividend for 43 straight years—one of the longest runs of steady growth in American business. At year-end, Emerson’s stock was priced at 17.7 times the company’s net income per share. Like its power tools, Emerson was never flashy, but it was reliable—and showed no sign of overheating.

Could EMC Grow PDQ?

EMC Corp. was one of the best-performing stocks of the 1990s, rising—or should we say levitating?—more than 81,000%. If you had invested $10,000 in EMC’s stock at the beginning of 1990, you would have ended 1999 with just over $8.1 million. EMC’s shares returned 157.1% in 1999 alone—more than Emerson’s stock had gained in the eight years from 1992 through 1999 combined. EMC had never paid a dividend, instead retaining all its earnings “to provide funds for the continued growth of the company.”1 At their December 31 price of $54.625, EMC’s shares were trading at 103 times the earnings the company would report for the full year—nearly six times the valuation level of Emerson’s stock.

What about EMC the business? Revenues grew 24% in 1999, rising to $6.7 billion. Its earnings per share soared to 92 cents from 61 cents the year before, a 51% increase. Over the five years ending in 1999, EMC’s earnings had risen at a sizzling annual rate of 28.8%. And, with everyone expecting the tidal wave of Internet commerce to keep rolling, the future looked even brighter. Throughout 1999, EMC’s chief executive repeatedly predicted that revenues would hit $10 billion by 2001—up from $5.4 billion in 1998.2 That would require average annual growth of 23%, a monstrous rate of expansion for so big a company. But Wall Street’s analysts, and most investors, were sure EMC could do it. After all, over the previous five years, EMC had more than doubled its revenues and better than tripled its net income.

But from 1995 through 1999, according to Value Line, EMC’s net profit margin slid from 19.0% to 17.4%, while its return on capital dropped from 26.8% to 21%. Although still highly profitable, EMC was already slipping. And in October 1999, EMC acquired Data General Corp., which added roughly $1.1 billion to EMC’s revenues that year. Simply by subtracting the extra revenues brought in from Data General, we can see that the volume of EMC’s existing businesses grew from $5.4 billion in 1998 to just $5.6 billion in 1999, a rise of only 3.6%. In other words, EMC’s true growth rate was almost nil—even in a year when the scare over the “Y2K” computer bug had led many companies to spend record amounts on new technology.3

A Simple Twist of Freight

Unlike EMC, Expeditors International hadn’t yet learned to levitate. Although the firm’s shares had risen 30% annually in the 1990s, much of that big gain had come at the very end, as the stock raced to a 109.1% return in 1999. The year before, Expeditors’ shares had gone up just 9.5%, trailing the S & P 500 index by more than 19 percentage points.

What about the business? Expeditors was growing expeditiously indeed: Since 1995, its revenues had risen at an average annual rate of 19.8%, nearly tripling over the period to finish 1999 at $1.4 billion. And earnings per share had grown by 25.8% annually, while dividends had risen at a 27% annual clip. Expeditors had no long-term debt, and its working capital had nearly doubled since 1995. According to Value Line, Expeditors’ book value per share had increased 129% and its return on capital had risen by more than one-third to 21%.

By any standard, Expeditors was a superb business. But the little freight-forwarding company, with its base in Seattle and much of its operations in Asia, was all-but-unknown on Wall Street. Only 32% of the shares were owned by institutional investors; in fact, Expeditors had only 8,500 shareholders. After doubling in 1999, the stock was priced at 39 times the net income Expeditors would earn for the year—no longer anywhere near cheap, but well below the vertiginous valuation of EMC.

The Promised Land?

By the end of 1999, Exodus Communications seemed to have taken its shareholders straight to the land of milk and honey. The stock soared 1,005.8% in 1999—enough to turn a $10,000 investment on January 1 into more than $110,000 by December 31. Wall Street’s leading Internet-stock analysts, including the hugely influential Henry Blodget of Merrill Lynch, were predicting that the stock would rise another 25% to 125% over the coming year.

And best of all, in the eyes of the online traders who gorged on Exodus’s gains, was the fact that the stock had split 2-for-1 three times during 1999. In a 2-for-1 stock split, a company doubles the number of its shares and halves their price—so a shareholder ends up owning twice as many shares, each priced at half the former level. What’s so great about that? Imagine that you handed me a dime, and I then gave you back two nickels and asked, “Don’t you feel richer now?” You would probably conclude either that I was an idiot, or that I had mistaken you for one. And yet, in 1999’s frenzy over dot-com stocks, online traders acted exactly as if two nickels were more valuable than one dime. In fact, just the news that a stock would be splitting 2-for-1 could instantly drive its shares up 20% or more.

Why? Because getting more shares makes people feel richer. Someone who bought 100 shares of Exodus in January watched them turn into 200 when the stock split in April; then those 200 turned into 400 in August; then the 400 became 800 in December. It was thrilling for these people to realize that they had gotten 700 more shares just for owning 100 in the first place. To them, that felt like “found money”—never mind that the price per share had been cut in half with each split.4 In December, 1999, one elated Exodus shareholder, who went by the handle “givemeadollar,” exulted on an online message board: “I’m going to hold these shares until I’m 80, [because] after it splits hundreds of times over the next years, I’ll be close to becoming CEO.”5

What about Exodus the business? Graham wouldn’t have touched it with a 10-foot pole and a haz-mat suit. Exodus’s revenues were exploding—growing from $52.7 million in 1998 to $242.1 million in 1999—but it lost $130.3 million on those revenues in 1999, nearly double its loss the year before. Exodus had $2.6 billion in total debt—and was so starved for cash that it borrowed $971 million in the month of December alone. According to Exodus’s annual report, that new borrowing would add more than $50 million to its interest payments in the coming year. The company started 1999 with $156 million in cash and, even after raising $1.3 billion in new financing, finished the year with a cash balance of $1 billion—meaning that its businesses had devoured more than $400 million in cash during 1999. How could such a company ever pay its debts?

But, of course, online traders were fixated on how far and fast the stock had risen, not on whether the company was healthy. “This stock,” bragged a trader using the screen name of “Launch_Pad 1999,” “will just continue climbing to infinity and beyond.”6

The absurdity of Launch_Pad’s prediction—what is “beyond” infinity?—is the perfect reminder of one of Graham’s classic warnings. “Today’s investor,” Graham tells us,

is so concerned with anticipating the future that he is already paying handsomely for it in advance. Thus what he has projected with so much study and care may actually happen and still not bring him any profit. If it should fail to materialize to the degree expected he may in fact be faced with a serious temporary and perhaps even permanent loss.”7

Where the Es Ended Up

How did these four stocks perform after 1999?

Emerson Electric went on to gain 40.7% in 2000. Although the shares lost money in both 2001 and 2002, they nevertheless ended 2002 less than 4% below their final price of 1999.

EMC also rose in 2000, gaining 21.7%. But then the shares lost 79.4% in 2001 and another 54.3% in 2002. That left them 88% below their level at year-end 1999. What about the forecast of $10 billion in revenues by 2001? EMC finished that year with revenues of just $7.1 billion (and a net loss of $508 million).

Meanwhile, as if the bear market did not even exist, Expeditors International’s shares went on to gain 22.9% in 2000, 6.5% in 2001, and another 15.1% in 2002—finishing that year nearly 51% higher than their price at the end of 1999.

Exodus’s stock lost 55% in 2000 and 99.8% in 2001. On September 26, 2001, Exodus filed for Chapter 11 bankruptcy protection. Most of the company’s assets were bought by Cable & Wireless, the British telecommunications giant. Instead of delivering its shareholders to the promised land, Exodus left them exiled in the wilderness. As of early 2003, the last trade in Exodus’s stock was at one penny a share.