Convertible bonds and preferred stocks have been taking on a predominant importance in recent years in the field of senior financing. As a parallel development, stock-option warrants—which are long-term rights to buy common shares at stipulated prices—have become more and more numerous. More than half the preferred issues now quoted in the Standard & Poor’s Stock Guide have conversion privileges, and this has been true also of a major part of the corporate bond financing in 1968–1970. There are at least 60 different series of stock-option warrants dealt in on the American Stock Exchange. In 1970, for the first time in its history, the New York Stock Exchange listed an issue of long-term warrants, giving rights to buy 31,400,000 American Tel. & Tel. shares at $52 each. With “Mother Bell” now leading that procession, it is bound to be augmented by many new fabricators of warrants. (As we shall point out later, they are a fabrication in more than one sense.)*

In the overall picture the convertible issues rank as much more important than the warrants, and we shall discuss them first. There are two main aspects to be considered from the standpoint of the investor. First, how do they rank as investment opportunities and risks? Second, how does their existence affect the value of the related common-stock issues?

Convertible issues are claimed to be especially advantageous to both the investor and the issuing corporation. The investor receives the superior protection of a bond or preferred stock, plus the opportunity to participate in any substantial rise in the value of the common stock. The issuer is able to raise capital at a moderate interest or preferred dividend cost, and if the expected prosperity materializes the issuer will get rid of the senior obligation by having it exchanged into common stock. Thus both sides to the bargain will fare unusually well.

Obviously the foregoing paragraph must overstate the case somewhere, for you cannot by a mere ingenious device make a bargain much better for both sides. In exchange for the conversion privilege the investor usually gives up something important in quality or yield, or both. 1 Conversely, if the company gets its money at lower cost because of the conversion feature, it is surrendering in return part of the common shareholders’ claim to future enhancement. On this subject there are a number of tricky arguments to be advanced both pro and con. The safest conclusion that can be reached is that convertible issues are like any other form of security, in that their form itself guarantees neither attractiveness nor unattractiveness. That question will depend on all the facts surrounding the individual issue.*

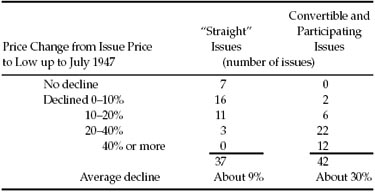

We do know, however, that the group of convertible issues floated during the latter part of a bull market are bound to yield unsatisfactory results as a whole. (It is at such optimistic periods, unfortunately, that most of the convertible financing has been done in the past.) The poor consequences must be inevitable, from the timing itself, since a wide decline in the stock market must invariably make the conversion privilege much less attractive—and often, also, call into question the underlying safety of the issue itself.† As a group illustration we shall retain the example used in our first edition of the relative price behavior of convertible and straight (nonconvertible) preferreds offered in 1946, the closing year of the bull market preceding the extraordinary one that began in 1949.

TABLE 16-1 Price Record of New Preferred-Stock Issues Offered in 1946

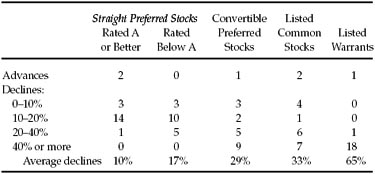

A comparable presentation is difficult to make for the years 1967–1970, because there were virtually no new offerings of nonconvertibles in those years. But it is easy to demonstrate that the average price decline of convertible preferred stocks from December 1967 to December 1970 was greater than that for common stocks as a whole (which lost only 5%). Also the convertibles seem to have done quite a bit worse than the older straight preferred shares during the period December 1968 to December 1970, as is shown by the sample of 20 issues of each kind in Table 16-2. These comparisons would demonstrate that convertible securities as a whole have relatively poor quality as senior issues and also are tied to common stocks that do worse than the general market except during a speculative upsurge. These observations do not apply to all convertible issues, of course. In the 1968 and 1969 particularly, a fair number of strong companies used convertible issues to combat the inordinately high interest rates for even first-quality bonds. But it is noteworthy that in our 20-stock sample of convertible preferreds only one showed an advance and 14 suffered bad declines.*

TABLE 16-2 Price Record of Preferred Stocks, Common Stocks, and Warrants, December 1970 versus December 1968

(Based on Random Samples of 20 Issues Each)

(Standard & Poor’s composite index of 500 common stocks declined 11.3%.)

The conclusion to be drawn from these figures is not that convertible issues are in themselves less desirable than nonconvertible or “straight” securities. Other things being equal, the opposite is true. But we clearly see that other things are not equal in practice and that the addition of the conversion privilege often—perhaps generally—betrays an absence of genuine investment quality for the issue.

It is true, of course, that a convertible preferred is safer than the common stock of the same company—that is to say, it carries smaller risk of eventual loss of principal. Consequently those who buy new convertibles instead of the corresponding common stock are logical to that extent. But in most cases the common would not have been an intelligent purchase to begin with, at the ruling price, and the substitution of the convertible preferred did not improve the picture sufficiently. Furthermore, a good deal of the buying of convertibles was done by investors who had no special interest or confidence in the common stock—that is, they would never have thought of buying the common at the time—but who were tempted by what seemed an ideal combination of a prior claim plus a conversion privilege close to the current market. In a number of instances this combination has worked out well, but the statistics seem to show that it is more likely to prove a pitfall.

In connection with the ownership of convertibles there is a special problem which most investors fail to realize. Even when a profit appears it brings a dilemma with it. Should the holder sell on a small rise; should he hold for a much bigger advance; if the issue is called—as often happens when the common has gone up considerably—should he sell out then or convert into and retain the common stock?*

Let us talk in concrete terms. You buy a 6% bond at 100, convertible into stock at 25—that is, at the rate of 40 shares for each $1,000 bond. The stock goes to 30, which makes the bond worth at least 120, and so it sells at 125. You either sell or hold. If you hold, hoping for a higher price, you are pretty much in the position of a common shareholder, since if the stock goes down your bond will go down too. A conservative person is likely to say that beyond 125 his position has become too speculative, and therefore he sells and makes a gratifying 25% profit.

So far, so good. But pursue the matter a bit. In many cases where the holder sells at 125 the common stock continues to advance, carrying the convertible with it, and the investor experiences that peculiar pain that comes to the man who has sold out much too soon. The next time, he decides to hold for 150 or 200. The issue goes up to 140 and he does not sell. Then the market breaks and his bond slides down to 80. Again he has done the wrong thing.

Aside from the mental anguish involved in making these bad guesses—and they seem to be almost inevitable—there is a real arithmetical drawback to operations in convertible issues. It may be assumed that a stern and uniform policy of selling at 25% or 30% profit will work out best as applied to many holdings. This would then mark the upper limit of profit and would be realized only on the issues that worked out well. But, if—as appears to be true—these issues often lack adequate underlying security and tend to be floated and purchased in the latter stages of a bull market, then a goodly proportion of them will fail to rise to 125 but will not fail to collapse when the market turns downward. Thus the spectacular opportunities in convertibles prove to be illusory in practice, and the overall experience is marked by fully as many substantial losses—at least of a temporary kind—as there are gains of similar magnitude.

Because of the extraordinary length of the 1950–1968 bull market, convertible issues as a whole gave a good account of themselves for some 18 years. But this meant only that the great majority of common stocks enjoyed large advances, in which most convertible issues were able to share. The soundness of investment in convertible issues can only be tested by their performance in a declining stock market—and this has always proved disappointing as a whole.*

In our first edition (1949) we gave an illustration of this special problem of “what to do” with a convertible when it goes up. We believe it still merits inclusion here. Like several of our references it is based on our own investment operations. We were members of a “select group,” mainly of investment funds, who participated in a private offering of convertible 4½% debentures of Eversharp Co. at par, convertible into common stock at $40 per share. The stock advanced rapidly to 65½, and then (after a three-for-two split) to the equivalent of 88. The latter price made the convertible debentures worth no less than 220. During this period the two issues were called at a small premium; hence they were practically all converted into common stock, which was retained by a number of the original investment-fund buyers of the debentures. The price promptly began a severe decline, and in March 1948 the stock sold as low as 7 3/8. This represented a value of only 27 for the debenture issues, or a loss of 75% of the original price instead of a profit of over 100%.

The real point of this story is that some of the original purchasers converted their bonds into the stock and held the stock through its great decline. In so doing they ran counter to an old maxim of Wall Street, which runs: “Never convert a convertible bond.” Why this advice? Because once you convert you have lost your strategic combination of prior claimant to interest plus a chance for an attractive profit. You have probably turned from investor into speculator, and quite often at an unpropitious time (because the stock has already had a large advance). If “Never convert a convertible” is a good rule, how came it that these experienced fund managers exchanged their Eversharp bonds for stock, to their subsequent embarrassing loss? The answer, no doubt, is that they let themselves be carried away by enthusiasm for the company’s prospects as well as by the “favorable market action” of the shares. Wall Street has a few prudent principles; the trouble is that they are always forgotten when they are most needed.* Hence that other famous dictum of the old-timers: “Do as I say, not as I do.”

Our general attitude toward new convertible issues is thus a mistrustful one. We mean here, as in other similar observations, that the investor should look more than twice before he buys them. After such hostile scrutiny he may find some exceptional offerings that are too good to refuse. The ideal combination, of course, is a strongly secured convertible, exchangeable for a common stock which itself is attractive, and at a price only slightly higher than the current market. Every now and then a new offering appears that meets these requirements. By the nature of the securities markets, however, you are more likely to find such an opportunity in some older issue which has developed into a favorable position rather than in a new flotation. (If a new issue is a really strong one, it is not likely to have a good conversion privilege.)

The fine balance between what is given and what is withheld in a standard-type convertible issue is well illustrated by the extensive use of this type of security in the financing of American Telephone & Telegraph Company. Between 1913 and 1957 the company sold at least nine separate issues of convertible bonds, most of them through subscription rights to shareholders. The convertible bonds had the important advantage to the company of bringing in a much wider class of buyers than would have been available for a stock offering, since the bonds were popular with many financial institutions which possess huge resources but some of which were not permitted to buy stocks. The interest return on the bonds has generally been less than half the corresponding dividend yield on the stock—a factor that was calculated to offset the prior claim of the bondholders. Since the company maintained its $9 dividend rate for 40 years (from 1919 to the stock split in 1959) the result was the eventual conversion of virtually all the convertible issues into common stock. Thus the buyers of these convertibles have fared well through the years—but not quite so well as if they had bought the capital stock in the first place. This example establishes the soundness of American Telephone & Telegraph, but not the intrinsic attractiveness of convertible bonds. To prove them sound in practice we should need to have a number of instances in which the convertible worked out well even though the common stock proved disappointing. Such instances are not easy to find.*

Effect of Convertible Issues on the Status of the Common Stock

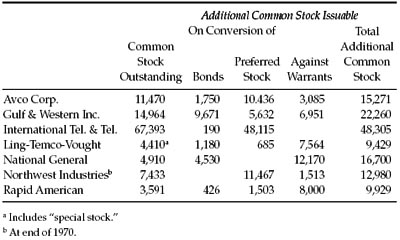

In a large number of cases convertibles have been issued in connection with mergers or new acquisitions. Perhaps the most striking example of this financial operation was the issuance by the NVF Corp. of nearly $100,000,000 of its 5% convertible bonds (plus warrants) in exchange for most of the common stock of Sharon Steel Co. This extraordinary deal is discussed below pp. 429–433. Typically the transaction results in a pro forma increase in the reported earnings per share of common stock; the shares advance in response to their larger earnings, so-called, but also because the management has given evidence of its energy, enterprise, and ability to make more money for the shareholders.* But there are two offsetting factors, one of which is practically ignored and the other entirely so in optimistic markets. The first is the actual dilution of the current and future earnings on the common stock that flows arithmetically from the new conversion rights. This dilution can be quantified by taking the recent earnings, or assuming some other figures, and calculating the adjusted earnings per share if all the convertible shares or bonds were actually converted. In the majority of companies the resulting reduction in per-share figures is not significant. But there are numerous exceptions to this statement, and there is danger that they will grow at an uncomfortable rate. The fast-expanding “conglomerates” have been the chief practitioners of convertible legerdemain. In Table 16-3 we list seven companies with large amounts of stock issuable on conversions or against warrants.†

Indicated Switches from Common into Preferred Stocks

For decades before, say, 1956, common stocks yielded more than the preferred stocks of the same companies; this was particularly true if the preferred stock had a conversion privilege close to the market. The reverse is generally true at present. As a result there are a considerable number of convertible preferred stocks which are clearly more attractive than the related common shares. Owners of the common have nothing to lose and important advantages to gain by switching from their junior shares into the senior issue.

TABLE 16-3 Companies with Large Amounts of Convertible Issues and Warrants at the End of 1969 (Shares in Thousands)

EXAMPLE: A typical example was presented by Studebaker-Worthington Corp. at the close of 1970. The common sold at 57, while the $5 convertible preferred finished at 87½. Each preferred share is exchangeable for 1½ shares of common, then worth 85½. This would indicate a small money difference against the buyer of the preferred. But dividends are being paid on the common at the annual rate of $1.20 (or $1.80 for the 1½ shares), against the $5 obtainable on one share of preferred. Thus the original adverse difference in price would probably be made up in less than a year, after which the preferred would probably return an appreciably higher dividend yield than the common for some time to come. But most important, of course, would be the senior position that the common shareholder would gain from the switch. At the low prices of 1968 and again in 1970 the preferred sold 15 points higher than 1½ shares of common. Its conversion privilege guarantees that it could never sell lower than the common package.2

Stock-Option Warrants

Let us mince no words at the outset. We consider the recent development of stock-option warrants as a near fraud, an existing menace, and a potential disaster. They have created huge aggregate dollar “values” out of thin air. They have no excuse for existence except to the extent that they mislead speculators and investors. They should be prohibited by law, or at least strictly limited to a minor part of the total capitalization of a company.*

For an analogy in general history and in literature we refer the reader to the section of Faust (part 2), in which Goethe describes the invention of paper money. As an ominous precedent on Wall Street history, we may mention the warrants of American & Foreign Power Co., which in 1929 had a quoted market value of over a billion dollars, although they appeared only in a footnote to the company’s balance sheet. By 1932 this billion dollars had shrunk to $8 million, and in 1952 the warrants were wiped out in the company’s recapitalization—even though it had remained solvent.

Originally, stock-option warrants were attached now and then to bond issues, and were usually equivalent to a partial conversion privilege. They were unimportant in amount, and hence did no harm. Their use expanded in the late 1920s, along with many other financial abuses, but they dropped from sight for long years thereafter. They were bound to turn up again, like the bad pennies they are, and since 1967 they have become familiar “instruments of finance.” In fact a standard procedure has developed for raising the capital for new real-estate ventures, affiliates of large banks, by selling units of an equal number of common shares and warrants to buy additional common shares at the same price. Example: In 1971 CleveTrust Realty Investors sold 2,500,000 of these combinations of common stock (or “shares of beneficial interest”) and warrants, for $20 per unit.

Let us consider for a moment what is really involved in this financial setup. Ordinarily, a common-stock issue has the first right to buy additional common shares when the company’s directors find it desirable to raise capital in this manner. This so-called “preemptive right” is one of the elements of value entering into the ownership of common stock—along with the right to receive dividends, to participate in the company’s growth, and to vote for directors. When separate warrants are issued for the right to subscribe additional capital, that action takes away part of the value inherent in an ordinary common share and transfers it to a separate certificate. An analogous thing could be done by issuing separate certificates for the right to receive dividends (for a limited or unlimited period), or the right to share in the proceeds of sale or liquidation of the enterprise, or the right to vote the shares. Why then are these subscription warrants created as part of the original capital structure? Simply because people are inexpert in financial matters. They don’t realize that the common stock is worth less with warrants outstanding than otherwise. Hence the package of stock and warrants usually commands a better price in the market than would the stock alone. Note that in the usual company reports the per-share earnings are (or have been) computed without proper allowance for the effect of outstanding warrants. The result is, of course, to overstate the true relationship between the earnings and the market value of the company’s capitalization.*

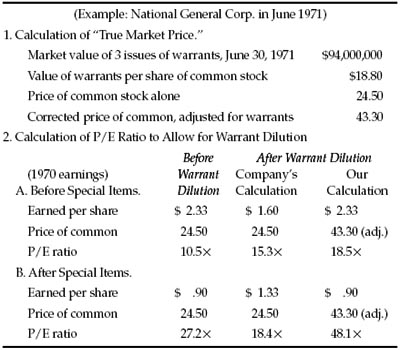

The simplest and probably the best method of allowing for the existence of warrants is to add the equivalent of their market value to the common-share capitalization, thus increasing the “true” market price per share. Where large amounts of warrants have been issued in connection with the sale of senior securities, it is customary to make the adjustment by assuming that the proceeds of the stock payment are used to retire the related bonds or preferred shares. This method does not allow adequately for the usual “premium value” of a warrant above exercisable value. In Table 16-4 we compare the effect of the two methods of calculation in the case of National General Corp. for the year 1970.

Does the company itself derive an advantage from the creation of these warrants, in the sense that they assure it in some way of receiving additional capital when it needs some? Not at all. Ordinarily there is no way in which the company can require the warrant-holders to exercise their rights, and thus provide new capital to the company, prior to the expiration date of the warrants. In the meantime, if the company wants to raise additional common-stock funds it must offer the shares to its shareholders in the usual way—which means somewhat under the ruling market price. The warrants are no help in such an operation; they merely complicate the situation by frequently requiring a downward revision in their own subscription price. Once more we assert that large issues of stock-option warrants serve no purpose, except to fabricate imaginary market values.

The paper money that Goethe was familiar with, when he wrote his Faust, were the notorious French assignats that had been greeted as a marvelous invention, and were destined ultimately to lose all of their value—as did the billion dollars worth of American & Foreign Power warrants.* Some of the poet’s remarks apply equally well to one invention or another—such as the following (in Bayard Taylor’s translation):

TABLE 16-4 Calculation of “True Market Price” and Adjusted Price/Earnings Ratio of a Common Stock with Large Amounts of Warrants Outstanding

Note that, after special charges, the effect of the company’s calculation is to increase the earnings per share and reduce the P/E ratio. This is manifestly absurd. By our suggested method the effect of the dilution is to increase the P/E ratio substantially, as it should be.

FAUST: Imagination in its highest flight Exerts itself but cannot grasp it quite.

MEPHISTOPHELES (the inventor): If one needs coin the brokers ready stand.

THE FOOL (finally): The magic paper…!

Practical Postscript

The crime of the warrants is in “having been born.”* Once born they function as other security forms, and offer chances of profit as well as of loss. Nearly all the newer warrants run for a limited time—generally between five and ten years. The older warrants were often perpetual, and they were likely to have fascinating price histories over the years.

EXAMPLE: The record books will show that Tri-Continental Corp. warrants, which date from 1929, sold at a negligible 1/32 of a dollar each in the depth of the depression. From that lowly estate their price rose to a magnificent 75 3/4 in 1969, an astronomical advance of some 242,000%. (The warrants then sold considerably higher than the shares themselves; this is the kind of thing that occurs on Wall Street through technical developments, such as stock splits.) A recent example is supplied by Ling-Temco-Vought warrants, which in the first half of 1971 advanced from 2½ to 12½—and then fell back to 4.

No doubt shrewd operations can be carried on in warrants from time to time, but this is too technical a matter for discussion here. We might say that warrants tend to sell relatively higher than the corresponding market components related to the conversion privilege of bonds or preferred stocks. To that extent there is a valid argument for selling bonds with warrants attached rather than creating an equivalent dilution factor by a convertible issue. If the warrant total is relatively small there is no point in taking its theoretical aspect too seriously; if the warrant issue is large relative to the outstanding stock, that would probably indicate that the company has a top-heavy senior capitalization. It should be selling additional common stock instead. Thus the main objective of our attack on warrants as a financial mechanism is not to condemn their use in connection with moderate-size bond issues, but to argue against the wanton creation of huge “paper-money” monstrosities of this genre.

* Graham detested warrants, as he makes clear on pp. 413–416.

* Graham is pointing out that, despite the promotional rhetoric that investors usually hear, convertible bonds do not automatically offer “the best of both worlds.” Higher yield and lower risk do not always go hand in hand. What Wall Street gives with one hand, it usually takes away with the other. An investment may offer the best of one world, or the worst of another; but the best of both worlds seldom becomes available in a single package.

† According to Goldman Sachs and Ibbotson Associates, from 1998 through 2002, convertibles generated an average annual return of 4.8%. That was considerably better than the 0.6% annual loss on U.S. stocks, but substantially worse than the returns of medium-term corporate bonds (a 7.5% annual gain) and long-term corporate bonds (an 8.3% annual gain). In the mid-1990s, according to Merrill Lynch, roughly $15 billion in convertibles were issued annually; by 1999, issuance had more than doubled to $39 billion. In 2000, $58 billion in convertibles were issued, and in 2001, another $105 billion emerged. As Graham warns, convertible securities always come out of the woodwork near the end of a bull market—largely because even poor-quality companies then have stock returns high enough to make the conversion feature seem attractive.

* Recent structural changes in the convertible market have negated some of these criticisms. Convertible preferred stock, which made up roughly half the total convertible market in Graham’s day, now accounts for only an eighth of the market. Maturities are shorter, making convertible bonds less volatile, and many now carry “call protection,” or assurances against early redemption. And more than half of all convertibles are now investment grade, a significant improvement in credit quality from Graham’s time. Thus, in 2002, the Merrill Lynch All U.S. Convertible Index lost 8.6%—versus the 22.1% loss of the S & P 500-stock index and the 31.3% decline in the NASDAQ Composite stock index.

* A bond is “called” when the issuing corporation forcibly pays it off ahead of the stated maturity date, or final due date for interest payments. For a brief summary of how convertible bonds work, see Note 1 in the commentary on this chapter (p. 418).

* In recent years, convertibles have tended to outperform the Standard & Poor’s 500-stock index during declining stock markets, but they have typically underperformed other bonds—which weakens, but does not fully negate, the criticism Graham makes here.

* This sentence could serve as the epitaph for the bull market of the 1990s. Among the “few prudent principles” that investors forgot were such market clichés as “Trees don’t grow to the sky” and “Bulls make money, bears make money, but pigs get slaughtered.”

* AT&T Corp. no longer is a significant issuer of convertible bonds. Among the largest issuers of convertibles today are General Motors, Merrill Lynch, Tyco International, and Roche.

* For a further discussion of “pro forma” financial results, see the commentary on Chapter 12.

† In recent years, convertible bonds have been heavily issued by companies in the financial, health-care, and technology industries.

* Warrants were an extremely widespread technique of corporate finance in the nineteenth century and were fairly common even in Graham’s day. They have since diminished in importance and popularity—one of the few recent developments that would give Graham unreserved pleasure. As of year-end 2002, there were only seven remaining warrant issues on the New York Stock Exchange—only the ghostly vestige of a market. Because warrants are no longer commonly used by major companies, today’s investors should read the rest of Graham’s chapter only to see how his logic works.

* Today, the last remnant of activity in warrants is in the cesspool of the NASDAQ “bulletin board,” or over-the-counter market for tiny companies, where common stock is often bundled with warrants into a “unit” (the contemporary equivalent of what Graham calls a “package”). If a stockbroker ever offers to sell you “units” in any company, you can be 95% certain that warrants are involved, and at least 90% certain that the broker is either a thief or an idiot. Legitimate brokers and firms have no business in this area.

* The “notorious French assignats” were issued during the Revolution of 1789. They were originally debts of the Revolutionary government, purportedly secured by the value of the real estate that the radicals had seized from the Catholic church and the nobility. But the Revolutionaries were bad financial managers. In 1790, the interest rate on assignats was cut; soon they stopped paying interest entirely and were reclassified as paper money. But the government refused to redeem them for gold or silver and issued massive amounts of new assignats. They were officially declared worthless in 1797.

* Graham, an enthusiastic reader of Spanish literature, is paraphrasing a line from the play Life Is a Dream by Pedro Calderon de la Barca (1600–1681): “The greatest crime of man is having been born.”

Commentary on Chapter 16

That which thou sowest is not quickened, except it die.

—I. Corinthians, XV:36.

The Zeal of the Convert

Although convertible bonds are called “bonds,” they behave like stocks, work like options, and are cloaked in obscurity.

If you own a convertible, you also hold an option: You can either keep the bond and continue to earn interest on it, or you can exchange it for common stock of the issuing company at a predetermined ratio. (An option gives its owner the right to buy or sell another security at a given price within a specific period of time.) Because they are exchangeable into stock, convertibles pay lower rates of interest than most comparable bonds. On the other hand, if a company’s stock price soars, a convertible bond exchangeable into that stock will perform much better than a conventional bond. (Conversely, the typical convertible—with its lower interest rate—will fare worse in a falling bond market.)1

From 1957 through 2002, according to Ibbotson Associates, convertible bonds earned an annual average return of 8.3%—only two percentage points below the total return on stocks, but with steadier prices and shallower losses.2 More income, less risk than stocks: No wonder Wall Street’s salespeople often describe convertibles as a “best of both worlds” investment. But the intelligent investor will quickly realize that convertibles offer less income and more risk than most other bonds. So they could, by the same logic and with equal justice, be called a “worst of both worlds” investment. Which side you come down on depends on how you use them.

In truth, convertibles act more like stocks than bonds. The return on convertibles is about 83% correlated to the Standard & Poor’s 500-stock index—but only about 30% correlated to the performance of Treasury bonds. Thus, “converts” zig when most bonds zag. For conservative investors with most or all of their assets in bonds, adding a diversified bundle of converts is a sensible way to seek stock-like returns without having to take the scary step of investing in stocks directly. You could call convertible bonds “stocks for chickens.”

As convertibles expert F. Barry Nelson of Advent Capital Management points out, this roughly $200 billion market has blossomed since Graham’s day. Most converts are now medium-term, in the seven-to-10-year range; roughly half are investment-grade; and many issues now carry some call protection (an assurance against early redemption). All these factors make them less risky than they used to be.3

It’s expensive to trade small lots of convertible bonds, and diversification is impractical unless you have well over $100,000 to invest in this sector alone. Fortunately, today’s intelligent investor has the convenient recourse of buying a low-cost convertible bond fund. Fidelity and Vanguard offer mutual funds with annual expenses comfortably under 1%, while several closed-end funds are also available at a reasonable cost (and, occasionally, at discounts to net asset value).4

On Wall Street, cuteness and complexity go hand-in-hand—and convertibles are no exception. Among the newer varieties are a jumble of securities with acronymic nicknames like LYONS, ELKS, EYES, PERCS, MIPS, CHIPS, and YEELDS. These intricate securities put a “floor” under your potential losses, but also cap your potential profits and often compel you to convert into common stock on a fixed date. Like most investments that purport to ensure against loss (see sidebar on p. 421), these things are generally more trouble than they are worth. You can best shield yourself against loss not by buying one of these quirky contraptions, but by intelligently diversifying your entire portfolio across cash, bonds, and U.S. and foreign stocks.

UNCOVERING COVERED CALLS

As the bear market clawed its way through 2003, it dug up an old fad: writing covered call options. (A recent Google search on “covered call writing” turned up more than 2,600 hits.) What are covered calls, and how do they work? Imagine that you buy 100 shares of Ixnay Corp. at $95 apiece. You then sell (or “write”) a call option on your shares. In exchange, you get a cash payment known as a “call premium.” (Let’s say it’s $10 per share.) The buyer of the option, meanwhile, has the contractual right to buy your Ixnay shares at a mutually agreed-upon price—say, $100. You get to keep the stock so long as it stays below $100, and you earn a fat $1,000 in premium income, which will cushion the fall if Ixnay’s stock crashes.

Less risk, more income. What’s not to like?

Well, now imagine that Ixnay’s stock price jumps overnight to $110. Then your option buyer will exercise his rights, yanking your shares away for $100 apiece. You’ve still got your $1,000 in income, but he’s got your Ixnay—and the more it goes up, the harder you will kick yourself.1

Since the potential gain on a stock is unlimited, while no loss can exceed 100%, the only person you will enrich with this strategy is your broker. You’ve put a floor under your losses, but you’ve also slapped a ceiling over your gains. For individual investors, covering your downside is never worth surrendering most of your upside.