Chapter 25

SELLING SECURITIES

Get 'em while they're hot!

Now that we have studied the properties of the various financial securities, let's see how companies sell them to investors. Bank finance was beautiful in its simplicity – whenever a company needed funds, it turned to its bank. Now that direct financing has become more common, companies can raise funds from a great many investors whom they do not necessarily know. That means they have to market their financing!

Section 25.1 GENERAL PRINCIPLES IN THE SALE OF SECURITIES

1/ THE PURPOSE OF OFFERINGS

The offering must be in line with this objective. The price of a security is equal to its present value, as long as all publicly available information has been priced in. This is the very basis of market efficiency. Conversely, asymmetric information is the main factor that can keep a company from selling an asset at its fair value.

Investors must therefore be given the information they need to make an investment decision. The company issuing securities and the bank(s) handling the offerings must provide investors with information. Depending on the type of offering, this can be in the form of:

- a mandatory legal written document called a prospectus, required by the exchange regulator (containing descriptive information: a reference document about the company, as well as a document detailing the transaction in question);

- presentations by management via meetings/conference calls with investors or electronic roadshows;

- valuations and comments by financial professionals on the deal and the issuer via notes by financial analysts and presentations to the bank's sales teams, for example.

A firm underwriting commitment by the bank(s) handling the transaction can provide additional reassurance to investors, because if the bank is willing to arrange and underwrite the offering, it must believe that the offering will succeed and that the price is “fair”. After all, investors are also clients to whom the bank regularly offers shares.

Investor information needs and the complexity of the deal depend on the following:

- The amount of information that is already available on the issuing company itself. Clearly, an initial public offering of shares in a company unknown to the market will require a big effort to educate investors on the company's strategy, business, financial profile and perhaps even the sector in which it operates. This information is already contained in the share price of a publicly traded company, as that price reflects investor anticipation. This is why it is generally easier to offer shares in a company that is already listed.

- Investor risk. Investors need more information for shares than for bonds, which are less risky.

- The type and number of investors targeted. In addition to regulatory restrictions, it is generally more difficult for a European company to sell its securities in the US than in Europe, especially if the company and its industry are not known outside its home country (sometimes the opposite can occur, as in the oil services sector, for example). Meanwhile, a private placement with a few investors is simpler than a public offering, market authorities imposing a lower level of information for transactions targeting only professional investors.

2/ THE ROLE OF BANKS

The bank(s) in charge of an offering have four roles, the complexity of which depends on the type of offering:

- Arranging the deal, i.e. choosing the type of offering on the basis of the goal sought: volume of securities to offer and in what form and timetable, choosing the market for the offering, contacts with market authorities, preparation of legal documents in liaison with specialised attorneys.

- Circulation of information: an offering is often an opportunity for an issuer to report on its recent activity, prospects and strategy. The consistency of this information is checked by the bank and the lawyers in charge of the deal during a phase called “due diligence”, which consists of interviews with the company's management. Information is also gathered by the brokerage arm of the bank and then put out in research notes written by the bank's financial analysts. The bank also organises meetings between the issuer and investors in one or more markets (roadshows or one-to-one meetings).

- Distribution of the paper: the bank's sales teams approach their regular clients, the investors, to market the securities and take orders. The issue price is then set by the bank in liaison with the issuer or seller, and the securities are allocated to investors. An equilibrium price is established in the “after-market” phase. In the days after that, the bank may intervene in the market in order to facilitate exchanges of blocks among investors.

- Underwriting: in some cases the bank provides the issuer (or seller) with a guarantee that the securities will find buyers at the agreed price. The bank thus assumes a certain market risk. The magnitude of this risk will depend on the type of guarantee and on the timing of the commitment.

Most offerings, especially public offerings,1 require a syndicate made up of several banks. Depending on how involved it is in the deal, and in particular the degree of guarantee, any one bank may play the role of:

- global coordinator, who coordinates all aspects of an offering; the global coordinator is also lead manager and usually serves as lead and book-runner as well. For fixed-income issues, the global coordinator is called the arranger;

- the lead manager is responsible for preparing and executing the deal. The lead helps choose the syndicate. One (or more) leads also serve as book-runners. The lead also takes part in allocating the securities to investors;

- joint-leads play an important role, but do not usually serve as book-runners;

- co-leads may underwrite a portion of the securities but have no role in structuring the deal;

- co-managers play a more limited role in the transaction, normally just underwriting a small portion of securities. Sometimes co-managers will provide no underwriting commitment and have no placement role, they will merely associate their names with the transaction. This being called “check collecting”.

For some transactions (a block trade of already existing shares or a bond issue), the banks may buy the securities from the seller (or issuer) and then sell them to investors. This is called a bought deal. Unsold securities go onto the bank's balance sheet.

A firm underwriting agreement carries less of a commitment than a bought deal. A firm underwriting is a commitment by the bank to buy the securities only if the offering fails to attract sufficient investor interest. In some cases, the bank may be released from its commitment in the event of force majeure like a market crash or a war declaration. A failure of the placement, not justified by a case of force majeure, is not a sufficient reason for the bank to withdraw.

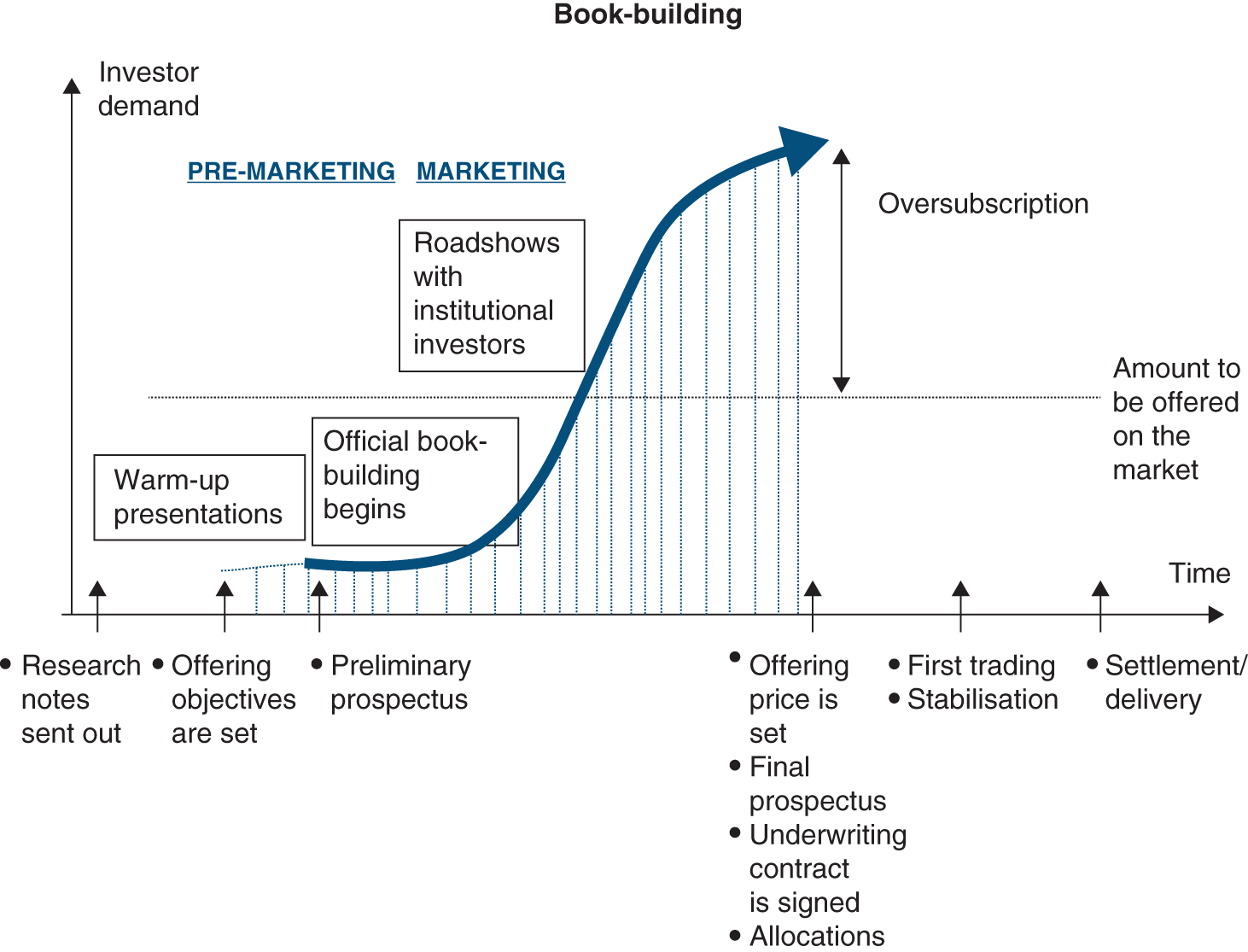

Before agreeing to underwrite more complex deals, banks may wish to have some idea of investors' intentions. They do so via a process called book-building, which occurs at the same time that information is sent out and the securities are marketed. Volumes and potentially prices from potential investors are listed in the book. This helps determine if the transaction is feasible and, if so, at what price. Only after the book-building process do banks choose whether or not to underwrite the deal. Book-building allows the banks running the transaction to limit significantly their risk, by assuring them that investors are willing to buy the securities.

In simpler transactions such as the placement of blocks or the issue of convertible bonds, the bank will almost always get feedback from a limited number of investors on their interest in the transaction and on the pricing. Market soundings are regulated by a European Directive (market abuse regulation, MAR).

In some cases, the bank does not pledge that the transaction will go through successfully, only that it will make its best efforts to ensure that this happens. This is rare in a formal documented offer, as investor confidence could be sapped if there is no formal pledge that the deal will go through. As a result, best efforts is the rule only in offerings by smaller companies or in very special cases (companies in financial distress, for example).

In some transactions, the bank's commitment is halfway between an initial bought deal and a post-book-building bought deal. When a block of existing shares is being sold, a bank may make a “back-stop” or floor underwriting commitment, i.e. go through the book-building process but guarantee the seller a minimum price.

There are three techniques for adjusting the offering to investor actual behaviour during (or just after) the transaction: extension clause, greenshoe and clawback.

The extension clause allows shareholders wanting to sell shares or the company issuing new shares to sell more shares than initially planned if demand turns out to be strong. The option is disclosed in the prospectus and can be exercised at the time of the allocation. The size of the transaction can be increased by 15% in the case of a share issue and 25% in the case of a secondary placement.

To stabilise the price after the transaction, the issuer or seller may give the bank the option of buying a number of shares over and above the shares offered to investors (as many as 15% more in a capital increase and 25% more for block trades of existing shares). This is called a greenshoe (named after the first company to use it). The bank allocates all the securities to investors, including the greenshoe shares, i.e. more than the official offering. These additional shares are borrowed by the bank:

- If the price falls after the offering, the bank buys shares on the market up to the limit of the greenshoe. This supports the price. It then has 30 days to resell these shares if the price moves back up. If the price doesn't rise, the bank repays the loan using the shares it bought to support the price. In this case the greenshoe is not exercised.

- If the price moves up, the bank can resell the shares or, if the price rises immediately after the transaction, the bank no longer has the shares so it will pay back the loan by exercising the greenshoe. The company will thus have sold more shares than originally planned.

Greenshoes are used for secondary offerings (i.e. sale of existing shares), new share issues (the lead bank receives, free of charge, warrants that it may or may not exercise) or convertible bond issues (when it takes the form of a simple extension of the issue, decided two or three days after its launch).

An offering targeted at several categories of investors (institutional, retail, employees, etc.) will be split into several tranches reserved for each of them. The clawback clause gives the company some flexibility in the size of each tranche. Hence, if institutional demand is very heavy and retail demand very light, the clawback allows the shares initially allocated to retail investors to be reallocated to institutional investors.

If a large shareholder sells part of his shares through the transaction, the placement will be eased if this shareholder commits not to sell additional shares over a certain period of time (unless the bank coordinating the transaction gives the green light). This is called a lock up and lasts between a few months and a year.

To simplify the transaction, the bank may advise the company to target a limited number of investors, thus avoiding the rules governing a public offering, including supervision by market authorities, obligation to present information, etc. This is called a private placement and is possible on all types of products. Private placements are in particular often used in offerings to US investors (generally under rule 144A), as the offering would otherwise be subject to extremely strict restrictions. They are also used in Europe for some bond placements.

3/ ISSUE DISCOUNTS

Studies show that when a company is floated, its stock often rises by an average of about 10–15% over its issue price, depending on the country, the timing and how the rise is calculated. Meanwhile, shares in a company that is already listed are usually offered at a discount ranging from 2–5%, although the range varies profoundly according to different countries.

This discount is theoretically due to the asymmetry of information between the seller and the investors or intermediaries. One side knows more about the company's prospects, while the other side knows more about market demand. The transaction is therefore possible. It's all a matter of price! Selling securities generally sends out a negative signal, so the seller has to price his securities slightly below their true value to ensure the deal goes through and that investors are satisfied.

The IPO discount could be due to the fact that there are both informed and uninformed investors. Uninformed investors cannot distinguish which issues are really attractive and thus are exposed to the winner's curse. This is why an average discount is offered, to guarantee an appropriate return for uninformed investors who will be receiving many shares of a “bad deal” and few shares of a “good deal”. Others suggest that the discount is a way of remunerating the banks underwriting the deal. The discount makes the issue easier to market, reduces risk and allows them to meet institutional client demand.

The issue discount is another way to persuade investors to invest in a transaction that appears to carry some risk.

For bonds, the investor will generally get a slightly better yield to maturity (5 to 20 basis points) on a new issue than on the secondary market of an existing issue with similar conditions. This premium will be called the new issue premium (NIP), a premium in rate being equivalent to a discount in price.

So much for the major principles. Let's now look at how the main types of securities are offered. As you will see, the methods converge towards two main techniques: bought deals and book-building.

Section 25.2 INITIAL PUBLIC OFFERINGS

The purpose of this section is not to analyse the motivations, strategic or otherwise, of an IPO (that will be seen in Chapter 44) but simply to describe how it works.

1/ HOW AN IPO WORKS

IPOs are surely the most complex of transactions, taking many months to put in place. They involve selling securities, about which prior information is extremely limited, to a large number of investors, including institutional and retail investors and employees.

An IPO can include a primary tranche (i.e. shares newly issued by the company) and/or a secondary tranche (i.e. disposal of existing shares by an existing shareholder). The techniques are the same for both tranches and, in fact, existing shares and new shares are bundled up in the same lot of shares to be offered. They are fungible.

However, the techniques vary depending on whether the shares are being offered to institutional investors, retail investors or employees.

2/ HOW IPOS ARE MADE

A number of techniques exist for floating a company. However, in the past few years, IPOs on regulated markets have almost all been in the same form: that of an underwritten deal with institutional investors and a retail public offering with retail investors.

(a) Book-building

Offerings of securities to institutional investors are most often implemented through a book-building. This is the main tranche in almost all IPOs. Under this system, one or more banks organise the marketing and sale of securities to investors via a phase of book-building. The price set after book-building will serve as a basis for setting the price of the retail public offering. Other techniques are used for the other tranches (employees and retail investors, in particular).

The initial review phase is handled by the banks. This consists of assessing and preparing the legal and regulatory framework of the deal (choice of market for listing, whether to offer shares in the US, etc.); structuring the deal; supervising documentation (due diligence, prospectus) and underwriting and execution agreements; preparing financial analysis reports; designing a marketing campaign (i.e. the type and content of management presentations, programme of meetings between management and investors).

Then comes the execution phase, with the publishing of financial analysis notes by syndicate banks. This is a pre-marketing period lasting one to two weeks prior to the effective launch of the operation. The notes are presented to investors during “warm-up” meetings, which help test investor sentiment. Analysts' research notes cannot be published during the blackout period that precedes the launch. The terms of the transaction, particularly the price range or maximum price, are set on the basis of conclusions from this pre-marketing exercise.

The marketing campaign itself then begins, and the offering is under way. During this period, full information is distributed via draft prospectuses (certified by market authorities), which may be national or international in scope. The prospectus includes all information on the company and the transaction. The offering is marketed within a price range of about 15% or with a maximum price. Company managers are mobilised during this period for numerous meetings with investors (roadshows) or for one-on-one meetings. The information given to investors is mainly on company results, markets and strategy.

In the meantime, investor intentions to subscribe in terms of volumes and prices are recorded in an order book, on the basis of the preliminary price range.

After this period, which can last 5–15 days, the sale price of the existing shares and/or newly issued shares is set. The price reflects market conditions, overall demand as reflected in the order book and the price sensitivity that investors may have expressed.

Not until after this phase might banks enter into a firm underwriting agreement. The shares are then immediately allocated, thus limiting the bank's risk. After allocation, investors are theoretically committed. However, up to the actual settlement and delivery of the shares (three days after the transaction), banks still face counterparty risk. There is also business risk in the form of an institutional investor who decides not to take delivery of the shares after all (an agreement is normally found between the bank and the investor). In sum, the only risks the syndicate takes is that of a market crash between the moment the price is set and the moment when the shares are allocated, and that of stabilising the price for around a month after the transaction by buying shares on the market.

The guarantee given by the bank to the company is also implicitly a comforter for the market. The bank determines a value after review of internal information. This partly resolves the problem of asymmetry of information. The signal is no longer negative, because a bank with access to internal information is taking the risk of buying the shares at a set price if the market does not.

A standardised press release (with the issue price) is sent out after the price is set and the subscription period is closed. The lead bank knows the quantity and quality of demand. The book-runner allocates the new shares to investors in concert with the issuer and/or seller, who can thus “choose” its shareholders to a certain extent.

The shares are allocated on the basis of certain criteria determined in advance. Allocation is discretionary but not arbitrary. The goal may be to favour US, European or local investors. Generally, the main goal in allocation is to have a balance between investors with different investment timing in order to ensure a stable aftermarket. The banks may steer the issuer to what it believes are quality investors, thus limiting excessive flowback, i.e. the massive sale of securities immediately after the offering.

Book-building offers several advantages, including greater flexibility. For one thing, the price can be adjusted as necessary during the marketing phase, which can sometimes last several weeks. Moreover, shareholders can still be chosen via discretionary allocation of shares.

(b) How shares are offered to retail investors

In an underwritten deal, shares are allocated at the discretion of the lead, based on the order book, as well as on criteria announced in advance. However, when shares are being sold to retail investors, the issue is centralised by the market itself.

- The retail public offering

In a retail public offering, a price range is set before the offering, but the exact price is set after the offering. The final price reflects market demand. French market authorities, for example, require a marketing period lasting at least three days, after which a draft prospectus is issued with the characteristics of the deal. Based on a price range, financial intermediaries collect orders from investors. The issue price is set jointly by the issuer and the syndicate lead, and is generally equal to the underwriting price.2 The final prospectus is then approved by the market authorities.

With the agreement of the market authorities, the banks can adjust the price if they have previously reserved the right to do so but, in general, they must begin the process anew if the new price is outside of the initial range. Shares are allocated on the basis of orders if supply is equivalent to demand and can be reduced on the basis of predetermined criteria. Allocation of shares to the various categories of buyers is done on the same basis as the fixed-price offer.

Normally, at least 1% of the order is filled, but there may be provision for a minimum number of shares per order, so that broker fees do not end up swallowing any potential gain. Similarly, there are sometimes several categories of orders with different allocation priorities.

- Fixed-price offering

Under a fixed-price offering, a certain number of shares are offered to the public at a pre-set price, which is generally identical to the price offered to institutional investors. The price is set after the book-building phase and is independent of market conditions. It is applied regardless of the number of shares requested. If it is far below what the market is willing to pay, the price will rise sharply in the days after the IPO and primary market buyers will have a capital gain to show for their initiative.

The only difference between a fixed-price offering and a retail public offering is how the price is set.

- Minimum-price offering

Under this technique, a number of shares are offered to the public at a certain price, under which they will not be sold. The local stock exchange centralises orders, in which buyers must specify a floor price, and tries to find a sufficiently wide price range at which orders can be allocated in a certain proportion (about 6%) if there is sufficient demand.

In a minimum-price offering, some orders may be shut out entirely, and orders at very high prices are paradoxically eliminated. This explains why the first quoted price is above the pre-set minimum price. If demand is too strong to quote the shares, trading is declared “limit up” and resumes at a higher price, or another technique is used for the initial quotation.

- An ordinary full listing

The principle of an ordinary full listing is simple: the shares are offered on the basis of the market's normal trading and quoting conditions. A minimum sale price is set, but buy orders are not centralised by the local stock exchange. Quotation is possible at a price normally no higher than 110% of the minimum price; at least 6% of the buy orders are filled (4% in exceptional cases). As in a minimum-price offering, trading may be suspended “limit up” and resumed at a higher price. In addition, orders may have to be covered by sufficient funds (the goal being to discourage speculation).

3/ US LISTINGS FOR NON-US COMPANIES

Companies normally list their shares on their domestic stock market, where they are better known. However, they may wish to tap foreign investors to widen their shareholder base and could thus seek a foreign listing.

This decision is not so unusual – over 3,000 foreign companies are listed in the US!

Since the American markets (NYSE and Nasdaq) are traditionally the preferred alternative for companies wanting to list, we focus our attention on US listing.

(a) Private placements

Under rule 144A, companies may opt for private placement of their shares, but they may only do so with US qualified institutional buyers (QIBs). QIBs are then prohibited from selling their shares on the open market for two years, but can trade with other QIBs via the PORTAL system. Private placements are simply a means of gaining access to US investors, but do not allow a company to register its shares with the Securities and Exchange Commission (SEC, the US market regulator) or to quote them in the US.

This is the least restrictive way to raise capital on US markets, as private placements are not registered with the SEC and come under the 12g3-2(b) waiver. All the issuing company has to do is translate the information that it has provided to its domestic market.

(b) Indirect listing via ADR

ADRs, also known as DRs or GDRs,3 are negotiable instruments issued by a US bank and representing the shares that it has acquired in a foreign company listed on a non-US market – something like tracking stocks, except they are not issued by the company itself. ADRs are traded on a regulated market (Nasdaq or NYSE) or an over-the-counter (OTC) market.

The ADR shares can be established either for existing shares already trading in the secondary market of the home country, or as part of a global offering of new shares.

There are three types of ADR depending on whether the company wishes to be listed on an organised market and raise funds in the US. The disclosure requirements will be more or less onerous depending on the type of ADR.

Nearly 3,000 ADRs are listed from 90 countries, including Sanofi, Telefónica, Korea Electric Power, ArcelorMittal, BP, Alibaba, JD.com, Teva and many others.

(c) Full listing

Companies can also list their ordinary shares in both their home countries and directly in the US. This gives them access to institutional investors whose by-laws do not allow them to buy shares outside the US.

The main difference between ordinary registered shares and ADRs is that ordinary registered shares carry lower transaction costs as there is no depositary. They are also more liquid and less subject to arbitrage trading between domestic shares and ADRs.

Full listing is a relatively long and complex process suitable only for very large companies (UBS, Deutsche Telekom, Repsol YPF, etc.).

Section 25.3 ICOS

An ICO, or initial coin offering, is a fund-raising process for a start-up, frequently in the technology sector and linked to blockchain cryptography. The name is derived from IPO (initial public offering) for marketing purposes, and is similar only in name as it differs quite significantly from the IPO process. To avoid scams, of which there were many during the initial ICO buzz of 2017/2018, market authorities have actively implemented regulations to govern the ICO process.

Start-ups seeking to raise capital will provide in exchange not shares but “tokens”, issued with blockchain technology, which can then be traded on specialised platforms. There are several categories of tokens:

- Utility tokens (the most widespread today) that will give access to a good or service in development by the company raising the funds.

- Security tokens that resemble financial securities in that they give access to all or part of the company's income and/or dividends.

- Community tokens (the first to appear) that give their holders the opportunity to participate in the governance of the project financed by the company.

- Asset tokens that represent rights over underlying assets.

A company wishing to carry out an ICO presents its project and the characteristics of its tokens in a document entitled a “white paper” (the equivalent of the prospectus for an IPO). One of the difficulties with ICOs is the valuation of the token. Depending on the characteristics of the token, its value will depend more on the use that will be made of it, or on the income derived from this use.

Section 25.4 CAPITAL INCREASES

A financial approach to capital increases is developed in Chapter 38.

1/ THE DIFFERENT METHODS

The method chosen for a capital increase depends:

- on whether or not the company is listed;

- on how willing current shareholders are to subscribe.

(a) Listed companies

When the large majority of current shareholders are expected to subscribe to the capital increase and it is not particularly necessary or desirable to bring in new shareholders, the transaction comes with pre-emptive subscription rights (the transaction is then called a rights issue). The issue price of the new shares is set and announced in advance and the offering then unfolds over several days. The price is set at a significant discount to the market price, so that the transaction will go through even if the share price drops in the run up to the listing of new shares. To avoid penalising existing shareholders, the issue comes with pre-emptive subscription rights, which are negotiable throughout the transaction period.

However, when current shareholders are not expected to subscribe or when the company wants to widen its shareholder base, there is no issue of pre-emptive subscription rights. The issue price is then not set until a marketing and pre-placement period has been completed, with a very slight discount to the share price at the end of this period. There are no pre-emptive subscription rights, but there may be a period during which current shareholders are given priority in subscribing.

(b) Unlisted companies

In this case, the issue price's discount will not be dictated by the fear that the share price will fluctuate during the operation (as the company is not listed), but rather by the wish of current shareholders to raise cash by selling the subscription rights they may have received.

If current shareholders do not wish to raise cash, then the company will issue pre-emptive subscription rights at a price about equal to the share price, or may issue shares to identified investors that have been found via a private placement.4

WHICH METHOD SHOULD BE USED FOR A CAPITAL INCREASE?

| Rights issue subscribed to mainly by: | Listed company | Unlisted company |

|---|---|---|

| Current shareholders | Pre-emptive subscription rights Steep discount to the market price | Pre-emptive subscription rights with a steep discount if current shareholders wish to raise cash Pre-emptive subscription rights with no discount or no pre-emptive rights if current shareholders do not want to raise cash |

| New shareholders | Offer without pre-emptive subscription rights (at a slight discount to the current share price) In some cases, a reserved rights issue | Pre-emptive subscription rights with a steep discount if shareholders want to raise cash Reserved rights issue if shareholders do not want cash |

Shares cannot be issued below par value (this is also the case for listed companies). If the share price is below par value, the par value could be reduced by offsetting it against past losses.

2/ RIGHTS ISSUE

A fixed-price rights issue with pre-emptive subscription rights (also called privileged subscription or rights issues) is the traditional issue preferred by small investors (or their representatives). Such issues acknowledge their loyalty or, conversely, allow them to raise a little cash by selling their subscription rights.

In some countries, such as the US and Japan, rights issues are quite rare, while in Continental Europe they generally have to be sold by rights.

Such issues remain open for at least 10 trading days. Banks underwrite them at a price well below the current share price, generally at a discount of 15–30%, but up to 30–50% when a financial crisis increases the volatility of stocks. No bank will guarantee a price near the current market price, because the longer the subscription period, the greater the risk of a drop in price. It is at this price that the banks will buy up any shares that have not found takers.

A steep discount would be a considerable injustice to existing shareholders, as the new shareholders could buy shares at 20% below the current market price. Rights issues resolve this problem by allowing existing shareholders to buy a number of shares proportional to the number they already have. If existing shareholders use all their pre-emptive rights, i.e. buy the same proportion of new shares as they possess of existing shares, they should not care what price the new shares are offered at.

Even when existing shareholders do not wish to subscribe, the pre-emptive subscription rights keep them from being penalised, as they can sell the right on the first day it is detached.

(a) Definition

The subscription right offers the existing shareholder:

- the certainty of being able to take part in the capital increase in proportion with their current stake;

- the option of selling the right (which is listed separately for listed companies) throughout the operation. This negotiable right adjusts the issue price to the current share price.

The subscriber may, thanks to their subscription rights, subscribe unconditionally to an amount equivalent to the pro rata of their holdings in the company. Should they wish to subscribe in a greater quantity, they may do so conditionally, provided that other shareholders do not take up their own rights to the subscription. Otherwise, should they seek certainty with regard to their intentions, they will have to purchase the subscription rights from shareholders who do not wish to participate.

The subscription right is similar to a call option whose underlying asset is the share, whose strike price is the issue price of the new shares and whose exercise period is that of the capital increase. Hence, its theoretical value is similar to that of a call option whose time value is very low, given its short maturity.

If the issue price and the current share price are the same, the subscription right's market value will be zero and its only value will be the priority it grants.

If the share price falls below the issue price, the rights issue will fail, as nobody will buy a share at more than its market price. The right then loses all value. Fortunately, the reverse occurs more frequently.

(b) Calculating the theoretical value of the subscription right

Let's take a company that has 1,000,000 shares outstanding, trading at €50 each. The company issues 100,000 new shares at €40 each, or one new share for each 10 existing ones. Each existing share will have one subscription right, and to buy a new share for €40, 10 subscription rights and €40 will be required.

After the new shares have been issued, an existing shareholder who holds one share and has sold his pre-emptive subscription rights must be in the same situation as an investor who has bought 10 pre-emptive subscription rights and one new share. So the share price after the deal should be equal to:

but also:

In our example:

Hence:

The post-deal share price should be equal to:

It is easy to calculate the theoretical value of the subscription right:

where V is the pre-issue share price, E the issue price of the new shares, N′ the number of new shares issued and N the number of existing shares.

We can see that this formula can be used to find the previous result.

The detachment of subscription rights is conceptually similar to a bonus share award. Hence, the existing shareholder may, if they wish, sell some pre-emptive rights and use the cash and remaining rights to subscribe to new shares, without laying out new cash (see the exercise at the end of this chapter).

(c) Advantages and drawbacks of pre-emptive rights

The subscription right is valid for at least 10 trading days – a relatively lengthy amount of time. The issue price therefore has to be well below the share price, so that if the share price does fall during the period, the deal can still go through. In such case, the value of the right (i.e. the difference between the share price and the issue price) will fall but will remain positive, as long as the share price, ex-rights, is above the issue price.

This is a double-edged sword as, once the deal is launched and the rights issued, nothing can delay the capital increase, even if the share price drops significantly during the deal. This is why the initial discount is so significant.

Complicating the transaction further is the fact that shareholders who do not possess a number of shares divisible by the subscription parity must sell or buy rights on the market so that they do. This can be difficult to do on international markets.

Another potential complication is the large proportion of US investors among current shareholders who are sometimes unable to exercise their pre-emptive subscription rights as some are not authorised to invest in options, which subscription rights are.

3/ ISSUE OF SHARES WITHOUT PRE-EMPTIVE SUBSCRIPTION RIGHTS

In issues of shares without subscription rights, the company also turns to a bank or a banking syndicate for the issue. But their role is more important in this case, as they must market the new shares to new investors. They generally underwrite the issue, as described above for IPOs. A retail public offering can be undertaken simultaneously. Alternatively, the bank can simply launch the transaction and centralise the orders without having gone through a book-building phase. The company may issue 10–15% more shares than expected, via a greenshoe, under which warrants are issued to the banks (see 25.1, 2/).

Local regulations tend to limit the flexibility to issue shares without subscription rights, so that the shareholder will not be diluted at an absurdly low price. Therefore, in most countries, regulation fixes a maximum discount to the last price or a minimum issue price as a reference to a price average.

When new shares are issued with no pre-set price, current shareholders can be given first priority without necessarily receiving pre-emptive rights. Indeed, such a priority period is the rule when pre-emptive rights are not issued. However, priority periods have the disadvantage of lengthening the total transaction period, as they generally last a few trading days (this is the minimum amount of time to allow individual shareholders the time to subscribe).

Legally speaking, a public issue of new shares, with or without pre-emptive rights, is considered to have been completed when the banks have signed a contract on a firm underwriting the transaction, regardless of whether or not the shares end up being fully subscribed.

Such issues of shares can be implemented in the form of a private placement to qualified investors (usually for a minor portion of capital).

4/ EQUITY LINES

The way an equity line works is that a company issues warrants to a bank that exercises them at the request of the company when it needs to raise equity. Equity lines smooth the impact of a capital increase over time. The shares issued when the warrants are exercised are immediately resold by the bank.

Equity lines are suitable for young businesses where the stock performance history does not allow conventional rights issues. However, it opens the way to many uncertainties, particularly on the terms imposed on the banks in exercising warrants and reselling the shares.

5/ RESERVED CAPITAL INCREASE

The placement of securities is infinitely simplified if the capital increase is reserved for a single identified investor. The challenge is then simply to reassure shareholders about the fairness of the issue price of the securities, as the reserved capital increase must be voted on at an EGM with, of course, cancellation of preferential subscription rights.

6/ EMPLOYEE STOCK OWNERSHIP PLANS

Employee Stock Ownership Plans (ESOPs) enable employees to acquire shares in the company they work for via a share placement process. The placement of securities is made directly with employees, generally at the same time as the payment of profit-sharing and incentive schemes, which makes it possible to finance all or part of the subscription. The company may also offer more structured share subscription mechanisms (downside protection of the share, upside multiplier).

Section 25.5 BLOCK TRADES OF SHARES

A block is a large number of shares that a shareholder wishes to sell on the market. Normally, only a small fraction of a company's shares are traded during the course of a normal day. Hence, a shareholder who wants to sell, for example, 5% of a company's shares cannot do so directly on the market. If he did, he could only do so over a long period and with the risk of driving down the share price. Blocks are sold via book-building and/or bought deals, which were described above.

1/ BOOK-BUILDING AND ACCELERATED BOOK-BUILDING

Like a rights issue or an IPO, a block trade can be done via book-building. However, block trades are “simpler” deals than capital increases or IPOs, the company is already known to the investors as already public and the amount to be placed is smaller. Hence block trades require less marketing. Book-building is faster, top management is less involved or not involved at all, and the deal can sometimes be done within a few hours.

Bigger transactions involving a strategic shift (exit by a controlling shareholder, etc.) may require an intense marketing campaign, and the deal will be managed as if it were a rights issue.

Book-building can come with a public offer of sale when the company wants to allow retail investors to acquire shares, but only for the larger issues. Barring a waiver from Euronext, a retail offering is possible only if it involves at least 10% of the total outstanding shares or at least 20 times the average daily volumes during the previous six months.

Block trades use techniques that are similar to those of IPOs. For example, prices can be set in advance or on the basis of terms set when the offering begins. However, in the latter case, no price range is required (but the price-setting mechanism and the maximum price must be spelled out). In the requisite filings with Euronext, the initiator can reserve the right to withdraw the offer if take-up is insufficient or increase the number of shares on offer by as much as 25% if demand is greater than expected.

2/ BOUGHT DEALS AND BACK-STOPS

When the seller initiates book-building or accelerated book-building, he has no guarantee that the transaction will go through. Nor does he know at what price the deal will be done. To solve this problem, he can ask the bank to buy the shares itself. The bank will then sell them to investors. This is called a “bought deal”.

The bank is then taking a significant risk and will only buy the shares at a discount to the market price. In recent bought deals involving liquid stocks, this discount ranges from 2% to 5%; it was between 10% and 20% mid-2009.

The way it works is this: the seller contacts a few banks one late afternoon after the markets close. They may have mentioned to some banks a few days or weeks beforehand that they might be selling shares, thus ensuring better-quality replies. The seller asks each bank the price it is willing to offer for the shares. Bids must be submitted within a few hours. The seller chooses the bank solely on the basis of price, and the shares are sold that very night. The bank must then organise its sales teams to resell the shares during the night in North America or Asia, taking advantage of the time difference, and then the following morning in Europe.

For the seller, bought deals offer the advantage of being certain that the deal will go through and at the price stated at the moment when it decides whether to sell. There are some disadvantages, however:

- the deal will generally be at a greater discount than in accelerated book-building;

- share performance can suffer, as the bank that has acquired the shares will want to sell them as quickly as possible, even if that means making the price fall.

In a very hot market, the seller may have the best of both worlds in transactions with a back-stop.

- The bank sets up an order book so that the firm can benefit from an increase in share price.

- The bank guarantees a minimum price. If all or part of the placement cannot be made at that price, the bank will buy the shares at the back-stop price.

Banks can be very aggressive when seeking to gain the right to execute such transactions in order to build credentials and comfort their ranking in league tables. A number of large transactions (in particular when governments are sellers) have led to heavy losses for investment banks in charge, leading some banks to leave this market altogether, deemed too risky.

Section 25.6 BONDS

As the bond market develops and becomes more international, investors need benchmarks to measure the risk of default by issuers they do not always know very well. Ratings have thus become crucial in bond offerings. The market for companies that do not have a rating from at least one agency is more complex to tap, as it can be closed from time to time (the market for unrated issuers was also closed for several weeks during the Covid-19 crisis). For an offering in the US, the issuer will need to have at least two ratings.

As we mentioned in Chapter 20, the corporate bond market can be separated between companies having a rating of at least BBB (investment grade) and companies rated BB or lower (below investment grade). When they want to issue bonds, the latter must offer higher interest rates. Such bonds are called “high yield”. The investment grade and high yield markets are separate, not just for the issuers, but also for investors and for the investment banks handling the offering. It should be noted, however, that depending on the situation, some issuers rated BB+ or even BB (known as crossovers) may issue with investment grade type documentation.

1/ INVESTMENT GRADE BONDS

The euro switchover naturally gave rise to a pan-European bond market, and has allowed much larger issues than were previously possible on national markets. €1bn issues are no longer rare, and only issues of €10bn or more are exceptional.

Bond offering techniques have thus evolved towards those used for shares, and market regulations have followed suit. For example, competitive bidding has gradually given way to book-building. Competitive bidding consists of a tender from banks. The issuer chooses the establishment that will head up the offering on the basis of the terms offered (mainly price). It thus takes the risk of giving the lead mandate to a bank that is overly aggressive on price. The reason this is risky is that prices of bonds on the secondary market may fall after the operation begins. Buyers will not like this. Competitive bidding is similar to a bought deal and is often used by state-owned companies.

Other placement techniques exist (but they are usually used by sovereign issuers): Dutch auctions (“reverse auctions”) are one example.

Book-building helps avoid price weakness after launch, as the issue price (or spread) is not pre-set. The lead bank suggests a price range and sounds out investors to see what price they are willing to pay. Presentations to investors, one-on-one meetings and electronic roadshows over the Internet or Bloomberg allow management to present its strategy.

The lead then builds a book of volumes and prices (either rate or spread) offered by each investor interested in the issue. There is little risk of miscalculation, as the issue price is set by the market. The period between when the price is set and the effective delivery of the shares is called the grey market (this is also the case for IPOs and rights issues). Bonds are traded on the grey market without, technically, even existing. Transactions on the grey market are unwound after settlement and delivery and the first official quotations. The lead intervenes on the grey market to maintain the spread at which the issue has been priced.

So there are some similarities between share and bond offerings. However, the process is much shorter for bonds and can be extremely short, especially if a company is an investment grade frequent issuer, and if the issue is on its local market. In such case, the placement will be implemented in a few hours with no marketing efforts. The process is longer for a first issue or if the company is targeting a large proportion of international investors.

The role of the lead is not just to market the paper, but to advise the client, where applicable, in the obtaining of a rating. It determines the spread possible through comparisons with issuers having a similar profile and chooses the members of the syndicate to help sell the bonds to the largest number possible of investors.

When the company plans several issues in the medium term, it can put out an umbrella prospectus to cover all of them, under an issue of EMTNs (euro medium-term notes). This allows the company to tap the markets very rapidly when it needs to, or when the market is attractive, at least to qualified investors, as issues to individual investors are much more cumbersome in terms of documentation.

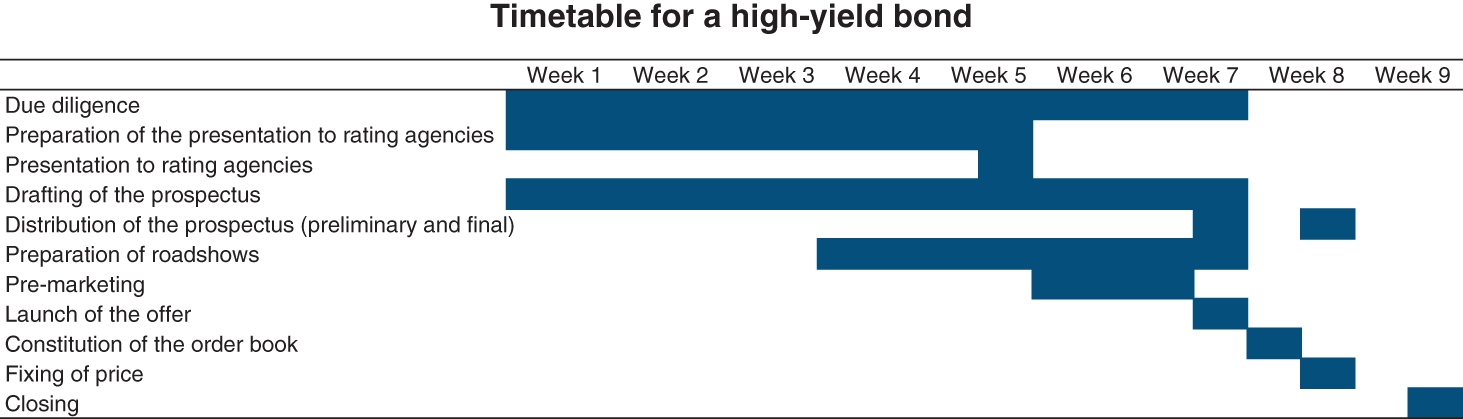

2/ HIGH YIELD BONDS

By definition, high yield or non-investment grade bonds are risky products. High yield issues take longer and require more aggressive marketing than a standard issue, as there are fewer potential buyers.

3/ PRIVATE PLACEMENT

As explained previously, private placements are an alternative to regular bond issues and allow issues of smaller amounts.

Placement techniques for private placements are much closer to placements of syndicated loans (see Section 25.8) than to standard bond issues. Investors are generally contacted in anticipation of the transaction to gauge their appetite for the transaction and the type of issuer that they could consider. The transaction is then proposed to firms that meet the criteria defined by the investors. Investors are typically insurance companies or pension funds looking for long-term investment and not caring much about the liquidity of their investment.

The placement requires the drafting of a prospectus as in a standard transaction.

Obviously, each local market (US, European, Schuldschein in Germany) has its specificities. Signs of a structuring market, standard issue contracts are now available for European private placements.

Section 25.7 CONVERTIBLE AND EXCHANGEABLE BONDS

Convertible bonds (CBs) (examined in Section 24.2) are a very specific product. From a placement point of view, the investor of a convertible bond will benefit from all the information given by the firm to the equity market. In addition, the share price allows the investor to value precisely the option part of the instrument that he will buy.

The only factor that could make an investor hesitate to invest in a convertible bond is the product's complexity. However, CBs are now well known to professional investors, and are sold mainly to specialised investors or hedge funds.

Section 25.8 SYNDICATED LOANS

Syndicated loans are not securities in their own right, but merely loans made to companies by several banks.

A syndicated loan offering is nonetheless similar to a bond issue. The company first receives a proposal from different banks to put in place or (refinance) a syndicated loan. On the basis of these proposals, the firm will retain one (or several) bank(s) that will arrange the transaction (the mandated lead arrangers, or MLAs). MLAs also usually have the role of bookrunners. This bank may do a bought deal of the entire loan and then syndicate it afterwards. The arranger is paid specifically for its advisory and placement role. When a large number of MLAs are retained, some will have a specific role to coordinate the transaction and facilitate the negotiation of the documentation (they are the facilitators, coordinators or agents of the documentation).

The main terms are negotiated between the documentation agent and the company and are put into a term sheet. Meanwhile, the bank and company choose a syndication strategy along with the banks (or financial institutions) that will be members of the syndicate.

After meetings with the company and a memorandum of information is drawn up (which can be avoided if the company is public), the banks contacted will decide whether or not to take part in the syndicated loan. Once the syndicate is formed, the legal documentation is finalised.

The entire process can take two months between the choice of arranger and the release of funds.

Syndicated loans are closely dependent on the quality of the company's relationship with its banks. Syndicated loans do not often make much money for the banks, and they take part only as they wish to develop or maintain good relations with a client, to whom they can later market more lucrative transactions (called “side business”). Membership of a syndicate sometimes even comes with the stipulation that it will be remunerated through an implicit or explicit pledge from the company to choose the bank as the lead on its next market transaction or as an advisor on its next M&A deal.

SUMMARY

QUESTIONS

EXERCISES

ANSWERS

BIBLIOGRAPHY

NOTES

- 1 That is, for a flotation on a regulated market or a public retail offer.

- 2 Retail investors are generally offered a discount or are exempt from certain fees.

- 3 American depositary receipts may also be called – generically – depositary receipts (DRs), or Rule 144A depositary receipts or global depositary receipts (GDRs), which are the “private placement” discussed in the text. However, different names typically identify the market in which the depositary receipts are available: ADRs are publicly available to US investors on a national stock exchange or in the OTC market; Rule 144A ADRs are privately placed and resold only to QIBs in the US QIB PORTAL market; GDRs are generally available in one or more markets outside the foreign company's home country, although these may also be known as ADRs.

- 4 In the rare case of a capital increase with no subscription rights and not reserved for identified investors, the price is based on an expert appraisal or is set at book value.