TAXALERT

The deduction for expenses related to a storage unit in the taxpayer’s home that is regularly used for inventory of the taxpayer’s business of selling products in which the home is the sole fixed location of the business has been expanded to cover product samples as well as inventory.

Taxpayers are not required to use the space exclusively for the storage of inventory or product samples in order to be eligible for the deduction. The new rule adds “product samples” to clarify the current rule, so taxpayers need not attempt to distinguish between inventory and product samples.

Example. Joe Smith is in the business of selling cosmetics. Joe’s residence is the only location of his business. He uses space in the study of his home to store cosmetic samples. Joe may deduct the expenses related to the portion of his residence used to store the product samples. It does not matter if Joe uses the study for additional purposes.

Direct expenses. Direct expenses benefit only the business part of your home. They include a separate phone line installed for the business, painting, or repairs made to the specific area or room used for business. You can deduct direct expenses in full.

Indirect expenses. Indirect expenses are for keeping up and running your entire home. They benefit both the business and personal parts of your home. Examples of indirect expenses include:

-

- Real estate taxes

- Deductible mortgage interest

- Casualty losses

- Rent

- Utilities and services

- Insurance

- Repairs

- Security systems

- Depreciation

You can deduct the business percentage of your indirect expenses.

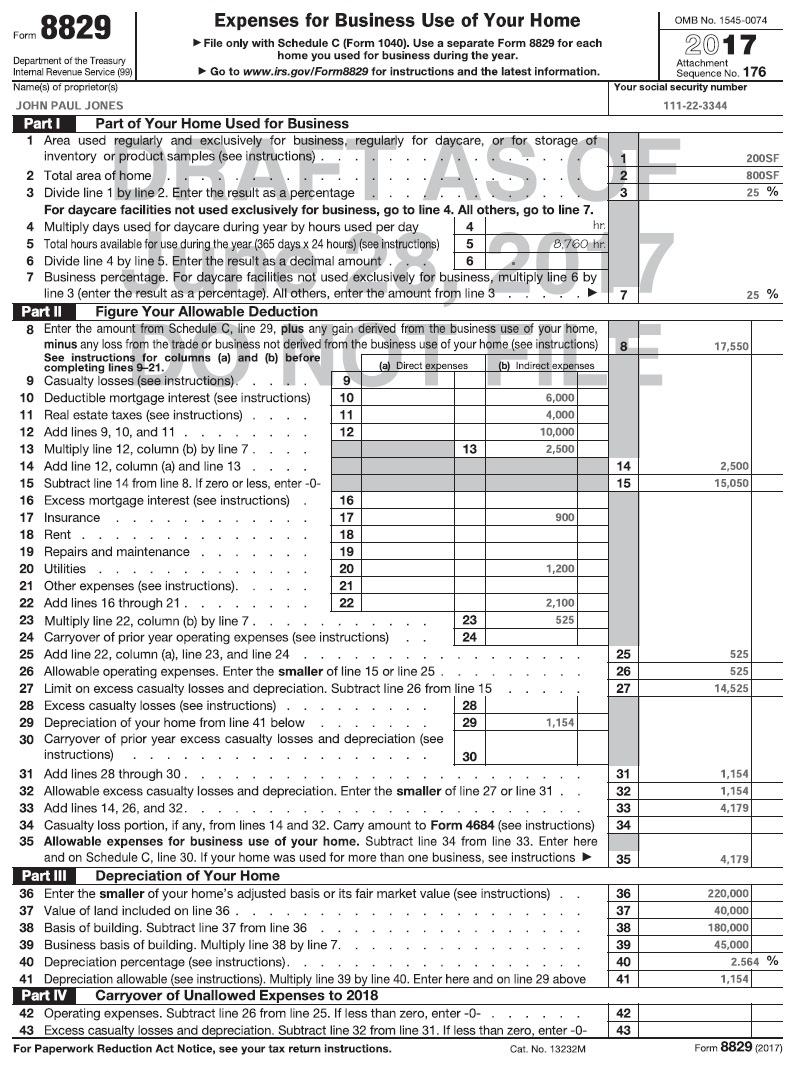

Figuring the business percentage. To figure deductions for the business use of your home, find the business percentage. You can do this by dividing the area used for business by the total area of your home. You may measure the area in square feet. To figure the percentage of your home used for business, divide the number of square feet of space used for business by the total number of square feet of space in your home. If the rooms in your home are about the same size, figure the business percentage by dividing the number of rooms used for business by the number of rooms in the home. You can also use any other reasonable method to determine the business percentage.

Example 1. Your home measures 1,200 square feet. You use one room that measures 240 square feet for business.

Therefore, you use one-fifth (240 ÷ 1,200), or 20%, of the total area for business.

Example 2. If the rooms in your home are about the same size, and you use one room in a 5-room house for business, you use one-fifth, or 20%, of the total area for business.

Real estate taxes. If you own your home, you can deduct part of the real estate taxes on your home as a business expense. To figure the business part of your real estate taxes, multiply the real estate taxes paid by the percentage of your home used for business.

Deductible mortgage interest. If you pay deductible mortgage interest, you can generally deduct part of it as a business expense. To figure the business part of your deductible mortgage interest, multiply this interest by the percentage of your home used in business. You can include interest on a second mortgage in this computation.

Casualty losses. If you have a casualty loss on your home or other property you use in business, you can deduct the business part of the loss as a business expense. Treat a casualty loss as an unrelated expense, a direct expense, or an indirect expense depending on the property affected.

In a partial destruction, the deductible loss is the decrease in fair market value of the property or the adjusted basis of the property, whichever is less. You must reduce this amount by any insurance or other reimbursement received.

If your business property is completely destroyed (becomes totally worthless), your deductible loss is the adjusted basis of the property, minus any salvage value and any insurance or other reimbursement you receive or expect to receive. Figure the loss without taking into account any decrease in fair market value.

Rent. If you rent, rather than own, a home and meet the requirements for business use of the home, you can deduct part of the rent you pay. To figure your deduction, multiply your rent payments by the percentage of your home used for business.

Utilities and services. Expenses for utilities and services, such as electricity, gas, trash removal, and cleaning services, are primarily personal expenses. However, if you use part of your home for business, you can deduct the business part of these expenses.

Telephone. The basic local telephone service charge, including taxes, for the first telephone line into your home is a nondeductible personal expense. However, charges for business long-distance phone calls on that line, as well as the cost of a second line into your home used exclusively for business, are deductible business expenses for the business use of your home. Deduct these charges separately on the appropriate schedule. Do not include them in your home office deduction.

Insurance. You can deduct the cost of insurance that covers the business part of your home.

Repairs. The cost of repairs and supplies that relate to your business, including labor (other than your own labor), is a deductible expense. For example, a furnace repair benefits the entire home. If you use 10% of your home for business, you can deduct 10% of the cost of the furnace repair.

Repairs keep your home in good working order over its useful life. Examples of common repairs are patching walls and floors, painting, wallpapering, repairing roofs and gutters, and mending leaks.

Security system. If you install a security system that protects all the doors and windows in your home, you can deduct the business part of the expenses you incur to maintain and monitor the system. You can also take a depreciation deduction for the part of the cost of the security system relating to the business use of your home.

Depreciation. The cost of property that can be used for more than 1 year, such as a building, a permanent improvement, or furniture, is a capital expenditure.

Land is not depreciable property. You generally cannot recover the cost of land until you dispose of it.

Permanent improvements. A permanent improvement increases the value of property, adds to its life, or gives it a new or different use. Examples of improvements are replacement of electric wiring or plumbing, a new roof, an addition, paneling, remodeling, or major modifications.

Depreciating your home. If you use part of your home for business, depreciate that part as nonresidential real property under the Modified Accelerated Cost Recovery System (MACRS). Under MACRS, nonresidential real property is depreciated using the straight-line method over 39 years.

To figure depreciation on the business part of your home, you need to know:

- The business-use percentage of your home;

- The first month in your tax year for which you can deduct business use of your home expenses;

- The adjusted basis and fair market value of your home at the time you qualify for a deduction.

Adjusted basis of home. The adjusted basis of your home is generally its cost plus the cost of any permanent improvements that you made to it minus any casualty losses deducted in earlier tax years.

When you change part of your home from personal to business use, your basis for depreciation is the business-use percentage times the lesser of:

-

- The adjusted basis of your home (excluding land) on the date of change; or,

- The fair market value of your home (excluding land) on the date of change.

Unrelated expenses benefit only the parts of your home that you do not use for business. These include repairs to personal areas of your home, lawn care, and landscaping. You cannot deduct unrelated expenses. For more information, also see chapter 29, Miscellaneous deductions.

Recordkeeping. You do not have to use a particular method of recordkeeping, but you must keep records that provide the information needed to figure your deductions for the business use of your home. Your records must show the following:

- The part of your home you use for business;

- That you use this part of your home exclusively and regularly for business as either your principal place of business or as the place where you meet or work with clients or customers in the normal course of your business;

- The depreciation and expenses for the business part of your home.

Generally, you must keep your records for at least 3 years from the date the return was filed or 2 years from the date the tax was paid, whichever is later. Keep records that support your basis in your home for as long as they are needed to figure the correct basis of your home.

Deduction limit. If your gross income from the business use of your home equals or exceeds your total business expenses (including depreciation), you can deduct all of your expenses for the business use of your home. But if your gross income from the business is less than your total business expenses, your deduction for certain expenses for business use of your home is limited. The total of your deductions for otherwise nondeductible expenses, such as utilities, insurance, and depreciation (with depreciation taken last) cannot be more than your gross income from the business use of your home minus the sum of:

- The business percentage of the otherwise deductible mortgage interest, real estate taxes, and casualty and theft loss; and

- The business expenses that are not attributable to the business use of your home (e.g., salaries or supplies).

If you are self-employed, do not include in (2) above your deduction for half of your self-employment tax.

You can carry forward to your next tax year deductions over the current year’s limit. These deductions are subject to the gross income limit from the business use of your home for the next tax year. The amount carried forward will be allowable only up to your gross income in the next tax year from the business in which the deduction arose, whether or not you live in the home during the year.

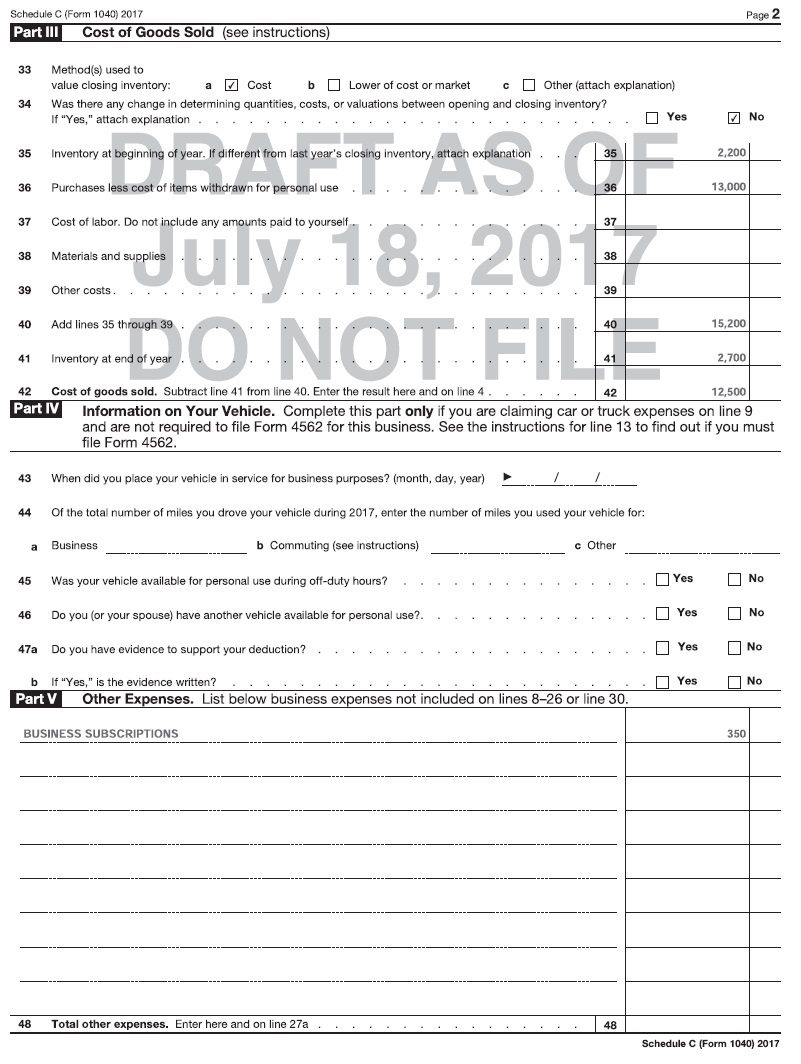

Figuring deduction limit and carryover. If you file Schedule C (Form 1040), figure your deduction limit on Form 8829, Expenses for Business Use of Your Home. Enter the amount from line 35 of Form 8829 on Schedule C, line 30.

Deductible mortgage interest. After you have figured the business portion of the mortgage interest on Form 8829, subtract that amount from total mortgage interest. The remainder is deductible on Schedule A; do not deduct any of the business portion on Schedule A. If the amount of interest allowed on Schedule A for home mortgage is limited, because it exceeds the maximum allowed (see chapter 24, Interest expense), the portion of the disallowed interest allocable to the business use of the home may be taken on Form 8829 (see instructions to line 16 of Form 8829 for further explanation).

Real estate taxes. If you file Schedule C, enter all your deductible real estate taxes on Form 8829. After you have figured the business portion of your taxes on Form 8829, subtract that amount from your total real estate taxes. The remainder is deductible on Schedule A; do not deduct any of the business part of real estate taxes on Schedule A.

Daycare facility. You can deduct expenses for using part of your home on a regular basis to provide daycare services if you meet the following requirements:

- You must be in the trade or business of providing daycare for children, for persons age 65 or older, or for persons who are physically or mentally unable to care for themselves.

- You must have applied for, been granted, or be exempt from having a license, certification, registration, or approval as a daycare center or as a family or group daycare home under applicable state law. You do not meet this requirement if your application was rejected or your license or other authorization was revoked.

Meals. If you provide food for your daycare business, do not include the expense as a cost of using your home for business. Claim it as a separate deduction on your Schedule C. You can deduct 100% of the cost of food consumed by your daycare recipients and 50% of the cost of food consumed by your employees as a business expense. You cannot deduct the cost of food consumed by you and your family.

Do not deduct the cost of meals for which you were reimbursed under the Child and Adult Care Food Program administered by the U.S. Department of Agriculture. The reimbursements are not included in your income to the extent you used them to provide food for the eligible recipients.

Chapter 39: Self-employment income: How to file Schedule C

by

Ernst & Young Tax Guide 2018, 33rd Edition

Chapter 39: Self-employment income: How to file Schedule C

by

Ernst & Young Tax Guide 2018, 33rd Edition