CHAPTER 8

Become an Investor for Good

We've covered retirement; now it's time to talk about investing for everything else. We can also choose to invest our money in ways that (mostly) aren't harmful and can even support the values we believe in.

Investing is an important part of being a financial adult because remember our friend, compound interest? It enables our money to grow exponentially. That can provide freedom in our choices and help us reach our goals. Not to mention, we won't miss out on thousands, tens of thousands, or even millions of dollars over the course of our lifetime.

Only half the people1 in the United States invest, and women tend to invest 40% less than men, on average.2 These numbers are even lower for communities of color. In 2019 only 34% of Black people and 24% of Latinos owned stocks, compared with 61% of white people.3

The Opportunity to Invest Is a Privilege

The problem is manyfold. It's not just that the stock market has been inaccessible for women and communities of color for centuries (although that's a big part of it). In order to invest, you need to have funds to invest. When 54% of the country is living paycheck to paycheck and 40% have less than $400 saved, investing is not something that's reasonable or feasible for most.4 When Black and Latino families have eight times and five times, respectively, less net worth than white families,5 that has a tremendous impact on their ability to invest. Having the opportunity to invest is a privilege.

And for the time being, if you have the privilege to be able to invest or expect to in the future, this chapter is going to get you set up. Not only do we need you set up to invest and grow your wealth, we want you talking about it. You're modeling it for others.

The Culture of Investing

What comes to mind when you hear the word “investor”?

If you think Warren Buffett or [insert other gray-haired white guy], it's not surprising. The investing world has been created for and by men. “Look at the brand symbol of the industry, it's a bull,” says Sallie Krawcheck, the co-founder and CEO of Ellevest. That says a lot in itself.

The investment industry is very white and very male; 79% of financial advisors are white6 and only 23% of certified financial planners (CFPs) are women.7 That's a problem. If you look at bank CEOs, they are all white men, now with the exception of the first woman CEO at a large bank, Jane Fraser at Citigroup.

Emily Green, the director of Private Wealth at Ellevest, explained, “The banks are talking about diversity but white men are still slated to be the next CEOs. Banks and financial companies are going to need to hire people at all ranks who will be able to help create products and services that work for people other than white men.” Instead of the industry working to fix how women are, they need to change what the banks do to serve women, and people of color. And that's not going to happen until there are women and people of color at all levels working in these organizations.

My Investing Story

Despite all my privilege and finance background, I still didn't feel like an investor. I wasn't part of the club. I felt like I should know more before starting. When I heard a colleague talking about his brilliant investing idea, I didn't think twice (or listen to my gut) and jumped on the opportunity. Turns out, he didn't know what he was talking about and I lost thousands of dollars (a large part of my net worth at the time).

I decided – never again. Never again will I depend on someone else to understand and invest my money. I'm going to figure this out.

I'll let you in on a little secret. Many people (even the very confident-sounding ones) don't know what they're talking about when it comes to investing. People are very quick to share their investing wins without sharing their investing losses.

Yet investing doesn't have to be that complicated. I mean, I'm going to break it all down for you in one chapter of a book. Plus, studies show that women are actually better investors when we do invest because we tend to trade less and have a more long-term focus. A Fidelity study showed that women investors earn 0.4% more per year than men (others show higher numbers).8 Compounded year after year, this can amount to a big difference.

The best way to change investing culture is to get more BIPOC, women, and especially BIPOC women investing. And why do we want to change investing culture? It will make investing truly inclusive, so more women and BIPOC women will be able to build wealth. And we know what it means when more women are wealthy. All good things for everyone. So that's what we're going to do.

Before You Get Started

Before you put money toward investing goals, you want to make sure you've checked some important financial boxes:

- You have cash on hand in case of an emergency (i.e., a rainy-day fund; see Chapter 3).

- You have maximized your company 401(k) matching (covered in Chapter 7).

- You are investing for retirement in tax-advantaged accounts (Chapter 7).

- You've paid off high-interest credit card debt (more about other debt later in this chapter).

If you haven't checked these boxes, that doesn't mean you can't put some money aside to learn to invest. We learn by doing. Just like you would buy a ticket to a conference to learn more about a certain topic, you can set aside $5, $10, or even $100 to learn about investing.

I just wouldn't prioritize investing as part of your savings on a regular basis over the aforementioned goals. It comes down to security and protection (i.e., the rainy-day fund) and what's actually costing and earning you the most money.

What Is Investing?

Investing just means buying something with the goal of selling it later for more money. Investing in stocks, bonds, and real estate is just one way to do that. With retirement investing, the goal is to save up enough money to retire (not need to work). Any investing outside of that could be to grow your money for a specific goal like buying a house or sending your kid to college, or you might not even be sure.

Your return or profit on an investment is how much it earned. If you bought an investment for $100 and sold it for $150, you earned $50 or a 50% return on your original investment.

A 50% return sounds awesome but the timeline is also important. Did you earn that in one year or over 30 years? This is where annualized return comes in. This makes it easier to compare what you earned with other investments. A good return is relative. Yes, it's great to earn a 10% return but if the market went up 25% that year, it's not as great because you could have done much better.

Realized versus Unrealized Gains

When the value of your investment goes up, your profit (or the amount it went up) is called a gain. If you haven't sold the investment, that amount is called an unrealized gain. It's not realized because it's actually not your money yet. The investment value can still go up and down.

When you sell the investment and the profit (plus the original amount) is in cash in your account, that's a realized gain. Currently, you only pay taxes on realized gains.

Long-Term Investing Wins the Tax Game

In your retirement accounts (and other tax-advantaged accounts like a 529 plan – we covered them in the previous chapter– and an HSA, discussed in Chapter 10) you don't pay taxes on your capital gains (which is a huge gain for us, pun intended). In our nonretirement accounts we do. When we buy and sell an investment within a year, we pay short-term capital gains tax on the growth, which is the equivalent of our income tax rate. So if I earned $50 on an investment when I sold it, and my income tax rate is 30%, I'd owe $15 when I file my taxes.

If we hold our investments for over a year before selling, we pay long-term capital gains tax, which is 0% if you are single and earn under $41,675, 15% if you earn $41,676 to 459,750, and 20% if you earn over $459,750 in 2022. Let's say I earn $50,000; my $50 capital gain is now taxed at 15%. I'll owe an additional $7.50 at tax time.

What If You Lose Money?

I know, I'm so optimistic. So far I've only talked about making money. When your investment goes down in value, that's a loss. If you still own the investment, that's an unrealized loss. Once you sell your investment at a loss, the amount your investment went down is a realized loss. Losses decrease our taxes.

Okay, cool-cool-cool. But you might be wondering, where does this magical investing happen?

The Three Ways to Invest (from Least to Most Expensive)

When it comes to actually investing your money, there are three ways you can do it. Here's the high-level overview, along with pros and cons of each.

On Your Own

To get started, you'll need a brokerage account, some money (it can be a very small amount), and your investment choices. That's only three things. Not too bad, right? You are the one who logs into your brokerage account and buys and sells the investments.

PRO: It is the least expensive option. You are not paying an advisor's management fee. Georgia Lee Hussey says that up until you hit about a million dollars in investments, doing it on your own works great and can keep your costs low, letting the magic of compound growth work for you.

PRO: It is great for control freaks. You can choose from any and all investments available to you under the sun. Nothing happens to your money without you initiating it.

PRO: It is accessible to those who are ready to invest. As long as you meet the account minimum (which can be very low), you're in.

CON: We're not always rational with money. Having some barrier, like a person we can call or software we can trust, between us and our money can keep us from making emotional decisions. Talking to a person doesn't mean you have to hire a financial advisor. I talk about other financial professionals you can hire to mitigate this con later.

CON: You're doing the work. Rebalancing is on you. Checking in is on you. The truth is, you should be checking in regardless of how you invest, but with the other ways you have some more support.

With a Robo-Advisor

A robo-advisor is a digital platform that invests your money for you for a management fee (usually 0.25–0.35%). Typically, you'll open an account, answer some questions about your goals, timeline, and risk tolerance, and the robo-advisor will invest accordingly. Some you might have heard of are Ellevest, Wealthfront, Betterment, and SoFi.

PRO: They do the work. You answer the questionnaire and voilà! Your money is managed for you. Set up some automatic contributions and you can be very hands-off.

PRO: Most robo-advisors invest your money in low-fee index fund investments. I'm a fan!

PRO: Robo-advisors are accessible to those who are ready to invest. Your money is being handled by “expert” software for a low price and that can give you peace of mind.

PRO: They may offer the opportunity to talk to a CFP. You may have a person to reach out to if you get nervous during a market dip or have a question.

PRO: Many offer tax-loss harvesting, which can save you money in taxes. Tax-loss wha? Remember capital gains and losses? Well, robo-advisors sell your investments for a loss and buy similar securities (jargon for tradable investments) to keep your overall portfolio composition the same for the lower price. This locks in the loss (now a realized loss) and saves you money in taxes while not sacrificing your investments. This is something that happens digitally – it's not something you'd want to spend your time replicating on your own.

While this sounds very cool, I have been skeptical about how much savings this actually generates. Tony Molina was able to share that “while there is no way to quantify what tax-loss harvesting is going to do for someone (it depends on market movement and specific investments),” for Wealthfront, “the average client typically gets back at least three times the value of our 0.25% fee in the benefits of tax-loss harvesting – about 0.75%.” If you harvested losses of $3,000 and your income tax rate is 30%, you are now paying $900 less in taxes.

CON: That fee. It's small but it's a fee nonetheless. What does that mean in real dollars? Take 0.25% (.0025) and multiply it by the amount of money you have invested. If you have $10,000 invested, that's $25 per year.

CON: You could replicate the portfolio on your own. Many robo-advisors choose simple low-fee investment options for you, which is great and one of the reasons I'm a fan of them. But at the same time, you can also replicate what they are doing on your own. It just takes more work on your end.

CON: There may be no person to talk to (this is a pro for some and a con for others). If there is support available, you are probably not going to be talking to the same person every time.

CON: There is not much of a barrier to emotional investing decisions (very similar to investing on our own). Having a better understanding of how investing works can really help with this (for investing on your own, too!). Tony says, “Know that you will have to deal with the downturn as well as the upturns in passive investing. You'll get hit hard in the downturn but know that you're going to come out ahead.” It helps to keep this in mind.

Hiring a Financial Advisor

Hiring a human (vs. software) to manage your investments for you.

PRO: There is more support. Some people really want to be able to call their person up and talk about their investments or calm their fears when the market is down. And they are happy to pay more for that (four to five times more).

PRO(ish): They can help you get more nuanced. You might think that hiring an individual (which costs more money) will mean you get more nuanced financial planning to meet your needs. You might even expect the advice to include your holistic financial picture. This is the ideal scenario and usually only happens once you have some very considerable wealth. You'll want to get clear on what support you will be getting when you interview potential advisors.

CON: This is the most expensive option. Advisors typically charge a percentage fee to manage your funds (usually 0.5–1.5%). If you have $100,000 invested with a financial advisor and their fee is 1.5.%, that's $1,500 per year. Another way to look at it? If your portfolio earned 6% and you paid a 1.5% fee, you're now only keeping 4.5% of that profit. That being said, it's best to work with a fee-only advisor who doesn't sell you products to earn commission.

Tony shares, “If you are high net worth, some advisors will be able to put you into alternative assets not available to everyone else. Otherwise, you're paying a higher fee just to talk to someone. There's no competitive advantage.” Georgia says that “investment management is highly replicable. We have all the evidence we need to know how to invest well. There are some differences in philosophy but they are just nuances.”

CON: This option is inaccessible to most. Many advisors only take on clients who have a certain amount of money to invest (they call this their minimum). Minimums can range from $50,000 to $1,000,000 so for most, hiring a financial advisor is not a possibility.

CON: They may try to sell you expensive products you don't need. Another thing that gives advisors a bad rep is that fee-based (different from fee-only) or commission-based advisors can hawk products – specifically, products that earn them commissions (a conflict of interest that I've had an issue with for the entirety of my career). These products might be in the form of insurance products (more on this in Chapter 10) or expensive funds with high expense ratios, load fees (a percentage fee you pay to purchase the fund), exit fees (a percentage fee you pay to sell the fund), and 12b-1 fees. This is another con that can be eliminated by working with a fee-only fiduciary.

Regardless of which option you choose, you want to understand what's happening with your investments. If you are working with an advisor, you want them to be open to educating and listening to you.

But Wait, What's a Financial Planner?

A CFP or certified financial planner is technically a type of financial advisor (I know, it's confusing). Financial planners do not always manage your investments and usually have a more holistic view of your finances (outside of just your investments and insurance). They go into the details of your entire financial plan. Brian Walsh, a CFP with SoFi you met a few chapters back, calls financial planners the quarterback or coordinator of your finances. They can offer second opinions when you talk to specialists in any given personal finance area like investing, insurance, or tax and estate planning.

Even for those early in their careers and money journeys, Georgia believes a financial planner is still valuable. She says, “It's really beneficial to see somebody for a couple hours just to give you the lay of the land and tell you which benefits to choose. And then you're good for two years.” Financial planners have different models. Some meet with you to make a plan for a few hours and you're set. And others serve more as long-term accountability partners throughout the year (and everything in between).

You want your financial planner to be a CFP, fee-only, and a fiduciary. I've included my favorites in the Financial Adulting toolkit.

“Fun” fact: These titles aren't cut and dry. There can be overlap between financial advisors and financial planners. Some CFPs are also financial advisors (who invest your money for you) and others are strictly financial planners (who put together a financial plan but don't invest your money for you). I say this over and over but regardless of what option(s) you choose, you always want to know how the people who are educating you are getting paid and what you are paying in fees. There are some resources in the Financial Adulting toolkit that will help you vet financial professionals.

TLDR (just kidding, definitely read the whole thing): The personal finance and investing spaces are continually changing and becoming more accessible for new investors. If you want more support, you can also hire financial or money coaches – someone to help you create goals, overcome setbacks, and break through the barriers holding you back from those goals – as well as a financial planner to support you in investing and looking at your entire financial picture.

What You Need to Get Started

If you are interested in getting started on your own or are curious about what it would entail, you'll need to open a brokerage account.

What Is a Brokerage Account?

A brokerage company is a firm that enables you to buy and sell investments. When you open up a brokerage account, you can then transfer money into the account and buy and sell investments there. There are many brokerage companies. Some you might have heard of are Vanguard, Fidelity, Charles Schwab, TD Ameritrade, E-trade, and there are many more (this list is by no means exhaustive).

How Much Money Should I Invest?

If you've never invested before, you might have a chunk of savings you want to invest and/or a monthly amount you'd like to put toward your investments. You can go back to Chapter 3 for help in prioritizing which goals should come first and how to break down your goals into monthly targets. You can test out different amounts in your financial plan (or happiness allocation). There's a common investing myth that you need a lot of money to invest. Depending on how you decide to do it (coming soon), you can start with as little as $5.

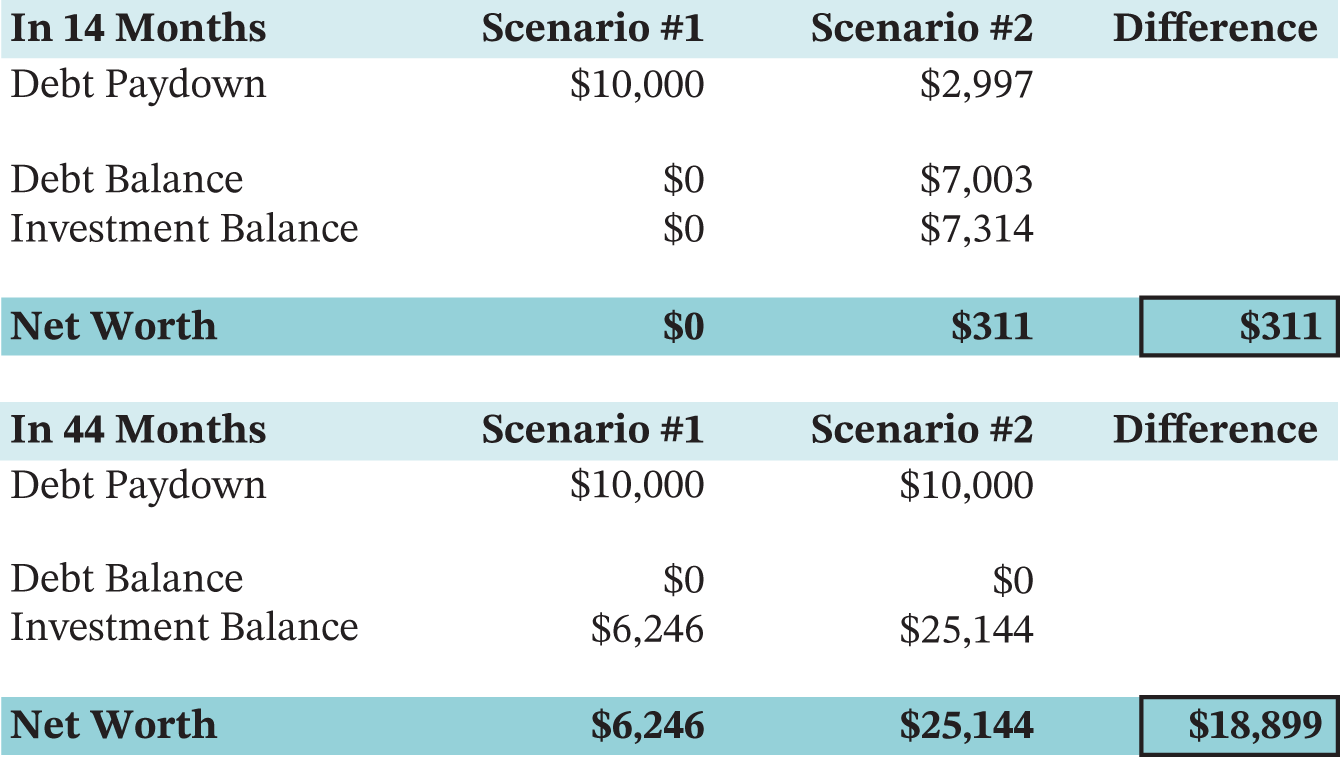

Can I Invest Before I Pay Off My Student Loans (or other debt)?

The short answer is yes. A few things to consider here. First, what's the best use of your money? If you can expect to earn 7%, on average, adjusted for inflation in the market, and your student loans have an interest rate of less than that, then it makes more sense financially to invest than to aggressively pay down your student loans. Lauren Anastasio and Brian agree with this 7% cutoff and Rachel Sanborn Lawrence prefers 5%.

The tricky part is, we have no way of knowing what the market will look like in the years you invest instead of paying down your debt, so it's not a cut-and-dried answer. Is it ever? To make decisions easier, I like to look at the numbers. The following chart shows what kind of trade-off we are talking about.

Let's say you have $10,000 in student loans, with an interest rate of 5% and a $250 monthly payment. In scenario #1, you pay $750 toward student loans and in scenario #2 you pay $250 toward student loans and invest $500 with an interest rate of 7%. You can run a similar comparison with your own debt information (there's a template in the Financial Adulting toolkit).

Another important thing to consider is your relationship toward your debt. Some feel very comfortable and happy having student loans and making the monthly payments, where others want to pay them down as soon as possible.

Time Is Very Important

Understanding your goals for the money you are investing is important because of time. When you need the money will determine whether you should be investing it in the first place and how risky those investments should be. For any money you need in the short term (the next one to three years), you will want to keep that in cash (like a high-yield savings account).

After we're covered for the next three years, Brian recommends breaking down the remaining investments into goals for the next three to seven years (a medium-term bucket) and longer than seven years (a long-term bucket). For medium-term goals he says, “It's a balancing act. There's no perfect answer because it's long enough where I want it to grow, but it's short enough where a market decline could have a bad impact. It's typically a mix of stocks and bonds.” For the long-term goals, he usually recommends that everything (or almost everything) be invested in stocks because that's the best for long-term growth.

When we invest for the long term we have the opportunity to wait out the market dips because we don't need the money for anything pressing. It's a much more powerful and much less stressful place to be. In some cases we may not even know what the money we are investing is for. That can be a good sign that we don't need the money in the near future. Can you hear the major privilege in this? I hope so.

Are You Ready to Level Up Your Risk Knowledge?

There are two types of risk, systematic and unsystematic. Systematic risk is the risk that the entire market can go down. This can happen when there's a recession, a global pandemic (oh, hey, 2020), or even when there's bad news. Following is a chart showing the total stock market over the past 30 years. Overall, the trend is far upward (yay long-term investing) but there are days or months where the market is down. Systematic risk is inevitable, unsystematic risk is not.

Unsystematic risk is the risk of loss in a certain industry or for a specific company (during the pandemic when no one was traveling, airline stocks took a big hit). Or when a company announces that their profit will be lower than expected, their stock price may go down. By investing in many industries and even more companies, we can mitigate this risk. And this is why investing in one company's stock is more risky than buying a fund that holds 3,000 companies, where the movement of one company or industry won't have too much of an impact on the whole.

S&P 500 Index

Source: Yahoo! Finance.

The Types of Investments

In our brokerage accounts we can invest in anything that's publicly traded (jargon alert), meaning an investment that the general public can buy and sell via their brokerage accounts. Each investment that is publicly traded has a ticker symbol.

Funds are a great way to diversify because they are invested in all different things (each has their own mandate or description of what they invest in). By buying a share of a fund, we can be invested in hundreds of stocks or bonds, or a mix of both. You can separate funds into two categories: actively and passively managed.

Actively managed means that there is an investment professional (really a team of professionals) choosing the investments. Passively managed means that the fund mimics an index so it's essentially managed by a computer (there are people too but far fewer). Examples of indexes are the S&P 500 (the largest 500 publicly traded companies in the United States) and the Dow Jones Industrial Average (a.k.a. “The Dow,” which tracks 30 large companies). Actively managed funds have higher expenses because you are paying for the team and expertise. You might assume that the investment professionals (actively managed funds) would earn higher returns, but it's actually really hard to beat the market.

“Fun” very important fact: Passively managed funds typically outperform their actively managed counterparts. Research shows that over the past 15 years, 86% of actively managed stock funds underperformed their respective benchmarks. Passively managed funds are less expensive and typically earn more profit – it's a win-win.

Rachel concurred and said that with equity (or stock) funds, passively managed is the way to go. She said that with some types of bonds you can argue that there can be added value with active management, but she still recommends passive management for bond funds. Rachel also shared that in “alternative assets” (anything outside of stocks, bonds, and cash), which are typically more of a focus for high-net-worth individuals, active management can be a differentiator.

What's in These Funds?

Outside of bonds versus equities, funds are often broken down by sector (industry) and/or size of the companies in the fund. As you can imagine, with a fund that's only invested in one sector, you are much more exposed (jargon alert) to anything happening in that sector, but at the same time, if it does really well, you will also earn more return than if you were invested in a bunch of other sectors at the same time.

Georgia says, “Invest in passively managed, low cost, broadly diversified funds – keep it super-unsexy.”

What Does Broadly Diversified Mean?

It means that your portfolio is invested across a lot of sectors (e.g., tech, healthcare, etc.), geographic regions, and companies of different sizes.

Geographic locations are often broken down by U.S./domestic, international developed (e.g., Australia, Sweden, and Germany), and emerging markets (e.g., India, Mexico, and China).

Company size is determined by market capitalization, often shortened to “market cap.”

Large-cap companies are large companies that are typically viewed as more stable and less risky, like Apple, Microsoft, and Johnson & Johnson. Small-cap companies tend to be more volatile but have a larger opportunity for growth (many you probably haven't heard of), and mid-cap are somewhere in the middle.

A broadly diversified portfolio will likely also include bonds and a bit of cash. It can include diversity in who issues the bond (e.g., government or corporate bonds) and the length of the term of the bond (short or long term). There's also a subsection of government bonds called “munis,” which is short for municipal bonds issued by local governments.

Where Does Investing for Good Come In?

Emily says, “If you're not thinking about the impact of your investments, you're still making an impact, it's just a negative impact.” That means thinking about where you're investing your money, and how that aligns with what you value personally. Think consumer activism for your investments.

Let's talk about options. ESG stands for environmental, social, and governance, and reflects criteria used to screen companies for their policies, the idea being that ESG funds are index funds and ETFs that only include companies that meet a certain level of criteria. Some funds exclude fossil fuels, gun manufacturers, tobacco companies, and companies that have had human rights violations. Others only include companies that have a certain number of women on the board and management team. And while there still isn't a governing third party, you can go to MSCI's (Morgan Stanley Capital International's) analysis tool to see how funds and companies rank on ESG factors.

Georgia shares that the most important thing to remember with ESG investing is that “it is not going to be perfect. It is actually going to be deeply, deeply imperfect. So bet on that. It's going to involve a lot of gray area.”

Cleona Lira, the founder of Conscious Money, says, “Do not worry so much about the labels. Look more at the underlying companies that the fund is investing in. The top 10 holdings on a fund factsheet provide a lot of information.” Other experts echoed this. Tanja Hester says it's important to be skeptical of ESG labels. You want to do your research to see what's actually in any given fund.

Georgia says that having a focus can help. At Modernist Financial, the primary portfolio has an environmental focus, predominantly centered on greenhouse gas emissions (and reducing them). She says if you add too many filters or factors you're considering, you're going to filter everything out and not have much left to invest in, which creates much more risk due to less diversification.

What's really cool is that a number of studies show that ESG funds are outperforming their non-ESG counterparts – so investing in them is a win-win. As there is more and more demand for these types of funds (from us financial adults), we'll see a lot more options come into the horizon. I keep a list of my favorites (and tools to research them) in the Financial Adulting toolkit.

What About Socially Responsible or Values-Based Investing?

Georgia shares, “It's important to understand that the movement for socially-conscious (a.k.a. values-based) investing comes out of religious institutions. We at Modernist don't offer “socially responsible” investment filters (though the name sounds like it would be a good thing) because, due to religious beliefs, these filters generally disinvest from companies that engage in stem cell research or produce abortion/contraceptives for women's healthcare. As a progressive investor, that is not ‘socially responsible’ to me.” She adds that “some elements of that analysis are really helpful,” like screening for munition companies and companies that use child labor. “I really am grateful that religious communities laid that groundwork for contemporary ESG investing, I just don't subscribe to all of their recommended filters.”

How to Choose a Brokerage Account

As you do your research, you'll find that not all brokerage accounts are the same and some will be a better fit than others. But again, at the end of the day, it's better to make a choice than not take action and miss out on time for your money to grow.

Read through this list, then set a timer for 30–60 minutes to do some research. When the timer goes off, make your choice. Nothing like a deadline! Here's how to choose a brokerage account.

Start with Recommendations

Now that you have a better idea of how you want to invest, keep that in mind in your research – meaning, you plan to focus on highly rated ESG funds, or funds in general. You want to start with a list of a few names. You can google, look to experts, or ask friends. We also have a list for you in the toolkit. When googling, be wary of top-10 lists. Sometimes companies pay to be on those, so you'll still want to do your own research.

When you have a list of names, take a look at customer reviews. It's important to see what people are saying who are actually using and experiencing the platform. Is it easy to get in touch with customer service? Do they have text support or do you have to hop on the phone? Do the investment options match how you plan to invest? Do customers like the website/app? How do you prefer to communicate? A lot of this is personal preference.

Look for a Low or No Minimum

Depending on how much money you are starting with, certain account minimums will be a dealbreaker. Many accounts have low or no minimums.

Make Sure There Are No Trading Fees

Back in the day when I started investing, you had to walk up the hill barefoot both ways to make a trade. Just kidding. But many brokerage accounts did charge a fee or commission each time you made a trade (unless you were trading their securities). The good news is, it's now easy to find accounts with $0 commissions, all the time. Trading fees are a dealbreaker.

Say No to Other Fees

Are there any other fees like a monthly or annual account maintenance fee? There are plenty of account options that don't charge any other fees, so this one is also a dealbreaker for me.

Do They Pass Your Consumer Activist Criteria?

Back in Chapter 6, you made your own consumer activist criteria. The financial services space is evolving (albeit more slowly than I'd like). There are new companies being founded and the more established brands are implementing changes to do better. You might not be able to find a perfect fit but you can definitely factor this in.

SIPC Insurance

Any reputable brokerage firm will be SIPC insured. This is similar to the FDIC insurance that we talked about in Chapter 6 in that if the brokerage firm goes under for any reason, your money is protected. That being said, it's very important to understand that being insured doesn't protect your investments from losses as far as ups and downs in the market.

Once you choose, you'll follow the brokerage firm's process for opening an account. It will feel very similar to opening a bank account.

What If I Don't Want to Do It Myself?

If you go the robo-advisor route, you'll open up your account through the robo-advisor (not through a separate brokerage), but your research will look similar. Research:

- The fees and other costs

- Investment options

- How they stack up with your consumer activist criteria

If you hire a financial advisor, your brokerage account will typically be through their company. You can open an account with them directly or, if you already have an account, you will transfer your investments over to them. Before hiring a financial advisor you'll want to ask or find out:

- Are they an RIA/fiduciary?

- Do they have any other credentials?

- Are they a fee-only advisor or do they get paid to sell you products?

- What's their investment philosophy?

- What does your gut say about the interaction? Did you feel heard? Was it a judgment-free conversation?

- Did they take the time to explain what's happening with your money?

What About the Apps?

Apps can be added to your research – you'll want them to meet the same criteria (i.e., no fees). They are another type of brokerage account that may add some different features, education, and gamification, like investing your spare change or social media components to encourage conversations around investing.

Another thing you'll see in many of the apps is the opportunity to invest in fractional shares, meaning instead of spending $1,000 for a share of Tesla stock, you can buy a portion of a share for $5. The goal of many of these apps is to make investing more accessible and fun, and you know I'm all for that.

Choosing Your Investments

There isn't one perfect investment choice for you. There are thousands of books, millions of articles, and entire TV channels that talk about investing 24/7. Two people can completely disagree on strategy and both make good money. At the end of the day, you want to be invested and have your money growing.

Start with Asset Allocation

We calculated your asset allocation for your retirement investments in Chapter 7. The asset allocations for your other investments are a different story. In the Financial Adulting toolkit you can find some of my favorite resources for finding your ideal asset allocation.

Answer the questions in the calculators with the specific money you are looking to invest in mind. You'll probably answer the questions differently if you are investing the money you plan to use to buy your house in 7 years than your retirement money that you don't need for over 20 years.

Now On to the Funds

You're ready to choose some investments. Some of the calculators in the Financial Adulting toolkit give specific fund recommendations or genres to get you started. You researched funds for your retirement in Chapter 7. You'll do the same thing here (just with lots more options) and if you decide to, you can now add your ESG criteria. If you need some funds to get you started, I have a list in the toolkit.

Great! Now research these criteria for three to seven funds.

A Couple of Things to Note

- If the fund is tracking an index, Tony recommends looking at the tracking error. How good of a job is it doing at tracking the index it's supposed to track?

- If adding the ESG component feels overwhelming and will keep you from getting started, no judgment. This is something you can come back to later.

Purchasing or Selling an Investment

You've come so far! To purchase or sell an investment, you might think you just hit buy or sell. Maybe in some of the apps, but it might not be that easy. Here's how to purchase an investment and some frequently asked questions.

The Ways You Can Purchase and Sell

The easiest way is to make a market order. That just means you'll purchase (or sell) the investment at the market price at that time. This is what I now do and I recommend it for everyone, unless you find it fun to try to earn a few extra cents per share.

Only if you're interested: You can also use stop and limit orders to name your price. Specifically, a limit order has you purchase a share at a named price or better and a stop order activates a market order when the investment hits a certain price. To make it more “fun” you can combine them in a stop limit order. At the levels most of us are investing, it's not worth the extra work and time to do these fancy orders for a few cents.

Choosing the Number of Shares

When you purchase an investment you typically have to enter in the number of shares you want to buy. Take the amount you want to invest and divide it by the share price. If you have $100 to invest and the share price is $35, then you can buy two shares. The extra cash waits until next time.

It Won't Happen Immediately

I share this so you don't freak out while your money is in limbo. It takes time for an order to execute and the shares to show up in your account. Don't fret when it's not immediate. You can come back and check in a day or two (depending on the platform) and the shares will be there.

Should I Choose to Reinvest Dividends?

Some companies pay dividends, which means they share profits (in cash) with their investors (a certain amount per share). If you don't choose to reinvest your dividends, the cash will sit in your account. If you choose to reinvest your dividends, the cash will be used to purchase more shares. Dividends are great if you are looking for some income (side note: they are taxed as income!) so they are a great tool in retirement. While we're growing our money, it typically makes sense to reinvest.

How Do I Know What's a Good Price?

Want to know a little secret? No one really knows. Not even people who do this for a living. Yes, you'll hear buy low and sell high. Sounds easy enough, right? But in practice you can't know when the market is at its peak or low. Constant investing over time (either per month or per paycheck) is the way to go.

Am I Buying at the Right Time?

This is pretty similar to the last question in that no one really knows, but it's helpful to understand some terms you'll hear thrown around. A bull market means stocks are going up or whoever said it thinks stocks will go up. A bear market is the opposite; things are going down. A bubble means that prices are high (things are overvalued) and will eventually “pop” or go back to a much lower level. A correction is when there's a drop in prices because things were overvalued or too high.

Do I Invest All My Money at the Same Time?

If you have a chunk of money, should you invest it all at once? There are mixed reviews. Dollar-cost averaging means that instead of investing all of your money at once (and getting one price), investing over time at different prices will reduce your risk of buying in when the stock price is high. This happens naturally when we invest on a regular basis, like every month or every paycheck, which is great.

To do this with a chunk of money, you could, as an example, invest a quarter of it (25%) every week until it's all invested. This takes some extra work. But research shows that it usually turns out better to get all of it invested at once because over time markets tend to go up.9 When something is easier and better for our money, that's a win-win. Plus, you're less likely to forget to invest.

When Do I Sell My Investments?

Sell your investments when you're ready to use the money for whatever goal you've been saving for. Yay! Or maybe you are no longer a fan of an investment and are looking to make a switch to a different one. Just know that with investments outside of your retirement accounts, selling is a taxable event. If you made money (which I hope you did if you're selling it), you will pay capital gains tax.

Learn from Some Investing Experts

What better way to learn than to see how the experts are investing their own money? You're welcome.

Georgia Lee Hussey, CFP and founder of Modernist Financial: Georgia says, “I invest in passively managed, low-cost, and broadly diversified index-like funds and ETFs. I keep it super-unsexy.” She recommends you do the same. “Keep it fast, easy, cheap, and automated and then move on to something more interesting like your giving plan or how to spend your money more intentionally” (like we covered in Chapter 6). Pretty cool that you know what all that means now, right?

Farnoosh Torabi, money expert and host of the So Money podcast: Farnoosh uses a robo-advisor for her personal investing and recently revisited her portfolio because her investments were keeping her up at night. She shared that “traditional financial advice says set it and forget it. But no, because when life happens, you need to check yourself and that includes your investment portfolio.” When she set up her portfolio 10 years ago, she wasn't the breadwinner, she didn't have kids, and she was in a different place. Her emotions served her in that they led her to revisit her investments and rebalance her portfolio.

Emily Green, Director of Private Wealth at Ellevest: Even though she invests other people's money all day, every day, Emily has her money invested in a robo-advisor and has automatic contributions set up to her impact (or ESG) portfolio. Since she's 34 (at the time of the interview), her retirement accounts are mostly invested in equity funds and she said her nonretirement investments are pretty “aggressive” as well.

Tony Molina, Product Evangelist at Wealthfront: Tony shared a personal story of how his investing strategy changed. Before the pandemic, he and his wife were saving for a home as a more long-term goal. Then their priorities shifted, work from home became the norm, they had a baby on the way, and they realized they wanted to buy much sooner. They sold their investments earlier than they had expected (luckily the market was up) and took a tax hit on their realized gains. I share this story because we make plans, but plans change. Even though investing is for the long term, it's still your money and it's liquid. Our plans don't have to be perfect to get started.

How Your Investing Can Change as You Build Wealth

I spoke with Alex Lieberman, co-founder of Morning Brew (one of the daily newsletters I get and love). They also have a great personal finance newsletter called Money Scoop. Alex shared his personal investment strategy:

I've historically invested my money in a very practical way that fit my lifestyle. Meaning, I didn't have time to spend researching investments. Plus I have zero competitive advantage. I invested in funds that track the S&P 500. And over time, odds are that they would grow at 7 or 8% return each year, on average.

More recently, since selling a portion of the Brew, and being fortunate to accumulate some wealth, I've moved to working with dedicated financial advisors who manage the bulk of my money. I have a close relationship with them where they update me on how they are putting my money to work in a balanced portfolio that I would describe as pretty aggressive (as it should be for a 28 year old).

Now that Alex has more time, he enjoys coming up with investment ideas (for a small portion of his portfolio) and talking through them with his advisors. He views them not only as managing his money but also as educating him about investing. He dedicates about 10% of his portfolio to alternative investments like real estate, private equity, angel investing, and crypto.

We talked about the higher fees he pays for a financial advisor. Here's how Alex thinks of them:

The average financial advisor charges somewhere between 0.5% and 1% of assets under management. To me, it becomes very clear over a period of time (let's call it a few years), whether they are able to outperform net of their fees. And if they're not, then that's when I start thinking about working with someone else. If they are, then that's great because I've created a space where I can feel confident that I am preserving my wealth, growing my wealth, and I have the space to learn.”

How will he know if they outperform net of fees? He'll compare his portfolio with the advisor to a scenario where he invested in an S&P 500 fund or used a robo-advisor. I'm excited to check in with him on this in 2023. Maybe I'll include a follow-up in my next book.

Protect Yourself from Yourself

We're usually the number-one threat to our own investing success. Here are some ways to protect yourself from yourself:

- Remember – you haven't lost (or earned) money on your investments until you sell them.

- Don't watch your investments all day.

- Automate if you can.

- Don't try to time the market.

Some Other Things That Might Be on Your Mind

What the Heck Is Bitcoin?

Understanding Bitcoin is not necessary to understand investing, but it's everywhere, so you might still want to know what it is. Bitcoin is a form of cryptocurrency (the most popular form of “crypto”), which is digital currency not tied to any banks or government (traditional money is part of the fiat system). Bitcoin is created and trades on a decentralized system known as blockchain.

You can invest in different cryptocurrencies like Bitcoin and Ethereum, but you can also invest in diversified crypto ETFs. Farnoosh got started investing in the space by investing in an ETF of companies that work in the space more tangentially or that support crypto technology. Even though she chose a more diversified crypto investment rather than choosing one of the currencies, she shared that it's still very risky and only makes up a very small piece of her investing portfolio.

You might have also heard the term NFT, which stands for nonfungible token and is a photo, video, or other digital file stored on a digital ledger that people trade.

Is Individual Stock Picking Like Gambling?

Individual stock picking (also called speculative investing) can be fun for some investors but it doesn't have to be part of your strategy. While I sometimes have FOMO when people make it big off of a certain stock, I also remember the big losses we don't hear about but that happen more often. I am happy with my long-term 8% return I get with diversified index funds.

Brian says you should only consider speculative investing once you have your financial foundation in place (those boxes checked!) and even then he recommends keeping it to 5% or less of your portfolio. Georgia calls this “hunches and fun” and recommends keeping it to 2–5%. She says, “Let's not bet your whole future on whether you think Tesla or Bitcoin is going to make it or not, because these markets are too small and volatile to make them a large part of your portfolio. You want this to be money you are okay with losing.”

Your Financial Adulting Action Items

- Understand that investing is a privilege.

- Check some important financial boxes before you get started investing.

- Start to get comfortable with investing lingo (this takes time!).

- Choose how you want to invest – on your own, with a robo-advisor, or if you want to hire a financial professional.

- If you want more support, look into hiring a financial planner or money coach.

- Research, choose, and open your brokerage account or robo-advisor account (if applicable).

- Research and choose your investments (including ESG funds).

- Decide how much you can and want to invest.

- Learn strategies from investing experts.

- Start investing. Make it automatic when possible.

- Use strategies to protect yourself from yourself.

- Adjust your financial plan for the amounts you are now investing.

Huge congrats! You are now an investor who not only grows their money but also does good (or you're ready to start as soon as you check those financial boxes). Your money is officially working for you! This is just the beginning of your investing journey. Continue to ask questions, get support, and normalize investing conversations with friends. That's how we'll change investing culture.

Next up, we're going to talk about a different type of investment, a real estate investment – a.k.a., buying a home.

Notes

- 1. “Survey of Consumer Finances, 1989–2019,” The Federal Reserve (September 28, 2020), https://www.federalreserve.gov/econres/scf/dataviz/scf/chart/#series:Stock_Holdings;demographic:all;population:1;units:have.

- 2. Jean Chatzky, “Why Women Invest 40 Percent Less Than Men (and How We Can Change It),” NBC News (September 25, 2018), https://www.nbcnews.com/better/business/why-women-invest-40-percent-less-men-how-we-can-ncna912956 (Survey by Wealth Simple).

- 3. “Survey of Consumer Finances, 1989–2019,” The Federal Reserve (September 28, 2020), https://www.federalreserve.gov/econres/scf/dataviz/scf/chart/#series:Stock_Holdings;demographic:racecl4;population:all;units:have.

- 4. “Nearly 40 Percent of Americans with Annual Incomes over $100,000 Live Paycheck-to-Paycheck,” PR Newswire (June 15, 2021), https://www.prnewswire.com/news-releases/nearly-40-percent-of-americans-with-annual-incomes-over-100-000-live-paycheck-to-paycheck-301312281.html.

- 5. “Disparities in Wealth by Race and Ethnicity in the 2019 Survey of Consumer Finances,” The Federal Reserve (September 28, 2020), https://www.federalreserve.gov/econres/notes/feds-notes/disparities-in-wealth-by-race-and-ethnicity-in-the-2019-survey-of-consumer-finances-accessible-20200928.htm#fig1.

- 6. “Labor Force Statistics from the Current Population Survey,” U.S. Bureau of Labor Statistics (January 22, 2021), https://www.bls.gov/cps/cpsaat11.htm.

- 7. “Making More Room for Women in the Financial Planning Profession,” CFP Board, https://www.cfp.net/-/media/files/cfp-board/knowledge/reports-and-research/womens-initiative/cfp-board_win_web.pdf?la=en&hash=614591F5084FDE519B27B7A2D3CA3AC6.

- 8. “Who's the Better Investor: Men or Women?” Fidelity Investments (May 18, 2017), https://www.fidelity.com/about-fidelity/individual-investing/better-investor-men-or-women/.

- 9. “How to Invest a Lump Sum of Money,” Vanguard, https://investor.vanguard.com/investing/online-trading/invest-lump-sum.