CHAPTER 2

Equity and Personal Finance

You might be wondering why a chapter on equity comes before any of the financial how-to in a personal finance book. After reading this, I hope you'll wonder why it's not the first thing covered in every single personal finance book.

Because, when the minimum wage has been $7.25 since 2009 while prices of goods have gone up 27% since then,1 it doesn't matter how well you budget.

When you have an overall racial wealth disparity of 8 to 1,2 and a gender wealth disparity of 3 to 1 for women, 50 to 1 for Black women, and 100 to 1 for Latinas,3 explained by the enslavement of Black people and systemic oppression, that's not going to be resolved by investing alone.

When mothers are paid 30% less,4 just for being mothers, are offered no paid leave, and childcare prices are astronomical, women continue to struggle and those who can drop out of the workforce by the millions.

The Idea That You Can Pull Yourself Up by Your Bootstraps Is a Scam

Black people are paid less, the things they own are worth less, but then you tell me to pull myself up by my bootstraps.

—Tiffany Aliche, The Budgetnista

Oof. This quote stuck with me during our interview. Tiffany Aliche (a.k.a. The Budgetnista) is a financial educator, bestselling author of Get Good With Money, and a Black woman. You'll be hearing a lot more from her (you're welcome). I was very intentional about featuring different voices, ethnicities, economic backgrounds, perspectives, and expertise throughout this book. Know that these are people I respect immensely. These are people I was giddy to interview. These are people I consider my financial adulting leaders and friends. You can find a list of where to follow and connect with each of them in the Financial Adulting toolkit (financialadultingbook.com).

Okay, back to scams. I repeat, telling people to pull themselves up by their bootstraps is a scam.

Financial education is important and we'll get into why and what that needs to look like, but until we see real significant changes from the top – I'm talking changes in government and corporate policy – financial literacy can't and won't solve our problems.

Mehrsa Baradaran, author of The Color of Money and professor at UC Irvine, shares, “I wrote my book to debunk the myth that you can leave the systems of credit, banking, and federal policy intact and you alone or your community can accumulate wealth, work hard, save your money, and close the wealth gap. Of course it works in individual cases but we take these individual cases and exceptions and make rules of them.”

In our interview, Dasha Kennedy, financial activist and founder of The Broke Black Girl, shared about the link between politics and personal finance:

When people say leave politics out of money, there's no way to do that. When how I pay taxes is decided through policy, how much I'm going to pay in childcare is decided through policy, how my kids’ schools are funded is decided through policy, and how much I'm going to be paid is decided through policy, we can't leave that out. And to even think that that's possible comes from a place of privilege. If you have an overflow of money and access to capital, policy probably really doesn't matter to you because you have your saving grace. But for me, I have to care about those things because it impacts my money.

That's why when people say they educate about personal finance but “stay out of politics,” it's complete BS.* Policy is critical and completely intertwined with our financial lives.

Financial adults understand the smart money moves they can make, but they also understand and advocate for the changes that need to be made at the top.

I am a white, upper-middle-class, cisgender, heterosexual, nondisabled woman. And as a financial adult, I'm going to use that privilege to bring all other women up with me. I can't call myself a feminist or anti-racist if I don't believe and care about equality for all women.

Not to mention (and this is just icing on the cake), it's what's best for all people: our wallets, our planet, everything. As Sallie Krawcheck, the co-founder and CEO of Ellevest, says, “Nothing bad happens when women have more money.” And I bet she wouldn't disagree with me taking it a step further and saying, the world changes for the better. Much better.

The Racial Wealth Gap

Farnoosh Torabi, financial expert and host of the So Money podcast, calls the racial wealth gap a “wealth chasm,” because that's more reflective of the size of the gap.

So what is this wealth chasm? Mehrsa explains that “across every income and education level, there's a massive racial wealth gap.” The average white family has a median net worth of $188,200 compared with $24,100 for Black families, $36,100 for Hispanic families, and $74,500 for groups of all other races/ethnicities.5 Dasha shares that the richest 400 Americans have more wealth than all the Black households in the United States combined. That's the chasm.

Let's break it down in numbers.

Disparities in Wealth Gap by Race and Ethnicity

*Other families – a diverse group that includes those identifying as Asian, American Indian, Alaska Native, Native Hawaiian, Pacific Islander, other race, and all respondents reporting more than one racial identification – have lower wealth than white families but higher wealth than Black and Hispanic families.

Source: Federal Reserve Board, 2019 Survey of Consumer Finances.

Because the “Other” category includes such a diverse group, it's important to note that there are large wealth disparities within the Asian American Pacific Islander (AAPI) community. A 2016 study of Los Angeles showed that while Japanese, Asian Indian, and Chinese households had a higher median wealth than white households, Koreans, Vietnamese, and Filipinos had 15×, 6×, and 1.5× less wealth, respectively.6 As of 2000, American Indian households had a wealth gap to white households of 11×.7

These numbers were taken before the onset of the COVID-19 pandemic, which disproportionately impacted communities of color financially, so these numbers are most likely worse than the study indicates. Reports say that with current policies in place, it will take 228 years to close the gap.8

A Very Quick History Lesson (That We Missed in School)

The racial wealth gap in our country dates back to enslavement, when white America built its economy (and wealth) with the free labor of people who had been kidnapped and enslaved and when Indigenous People were forced and displaced from their land, which was a tremendous loss of community wealth.

I didn't learn about most of this important history in school and I can only include a small glimpse in this book. To better understand the true scope of how policy after policy excluded and exploited BIPOC communities, I've included more resources in the Financial Adulting toolkit.

The 1862 Homestead Act

Through the Homestead Act, more than 270 million acres9 of land (10% of the United States),10 previously inhabited by Indigenous People, was sold (but really gifted for an extremely discounted price) to citizens and intended citizens for $1.2511 per acre (equivalent to about $3412 today!) in 1.6 million 160-acre plots. While there isn't much data on the race/ethnicity of homesteaders, it's believed that the overwhelming majority of plots went to white people. In the year 2000, the wealth of more than 46 million adults (25% of the United States) could be traced back to this policy.13

Freedman's Savings Bank

After the Civil War, in 1865, Freedman's Savings Bank was created by the U.S. government for those previously enslaved to deposit money and receive financial education. It's important to remember that previously enslaved Black people were starting with nothing, while white Americans had been building wealth for hundreds of years.

Henry Cooke, a white financier on the board of directors of the bank, used the bank's money to make speculative investments in railroads (Mehrsa calls it the “subprime market of that time”) and the bank eventually went under. More than 61,000 Black Americans lost $72 million14 in today's money (over half the Black community's accumulated wealth) that was never recovered, despite the bank being protected by the federal government. This incident starts a distrust of the financial system that gets reinforced and lingers for hundreds of years.

Tulsa Race Massacre of 1921

In 1921, a very segregated Tulsa had a thriving business district that was often called Black Wall Street. Kevin Matthews II, founder of BuildingBread and a Tulsa native, shares: “A white mob burned and bombed the nation's wealthiest Black neighborhood, killing an estimated 300 Black people, leaving 9,000 people homeless, destroying 1,200 businesses and causing between $50 and $100 million in property damage, all in 24 hours. The city then passed laws preventing people from building on land that was burned as a result of the massacre. Insurance companies labeled it a ‘riot’ to deny payments to Black people despite the fact that there were at least six airplanes used in the attack.”

The Federal Housing Administration (FHA)

The FHA was created as part of President Franklin D. Roosevelt's New Deal, and insured and guaranteed all federal approved mortgage loans, which Mehrsa explains made them “easy, risk free, and abundant.”15 Mehrsa shares in her book, “If you could save a few thousand dollars, you could buy a house, build wealth, and become middle class.” And your new mortgage payment in the suburbs would probably be lower than your rent in the city. This opportunity was only available to those who met the “gold standard” – people who were white, middle class, and male. “Between 1934 and 1968 98% of FHA loans went to white Americans,” creating white suburbs and leaving Black Americans renting in redlined neighborhoods.

Redlining

Redlining was the Home Owners Loan Corporation (HOLC) system of maps that rated neighborhoods on their perceived risk and stability. On the maps, green areas, rated A, were “homogeneous and white” while red neighborhoods, rated D, were predominantly Black. Neighborhoods with African Americans or Latinos were automatically rated D (red) and were ineligible for mortgages. The FHA used these maps for their own lending process.

Mehrsa acknowledges that the HOLC and FHA “were not creating these preferences, but reflecting the reality that white Americans preferred to live in segregated communities.”16 That said, “The FHA was unwilling to use the strength of the government and its leverage in the credit market to challenge racism.”

Redlining was just one of the many Jim Crow laws17 (a collection of state and local statutes that legalized racial segregation). Despite this history, Mehrsa believes that change is possible and that there is a lot of room for optimism around closing the gap. At the same time, many of the events mentioned were in response to progress, so she says we need to be “a little wary of celebrating before we're done.”

The Gender Wealth Gap

Then there's the gender wealth gap. Women own $0.32 for every $1.00 a white man owns. This gap is far greater for women of color. Black women and Latinas own $0.02 and $0.01, respectively, for the white man's dollar. $0.01!

The Gender and Racial Wealth Gap

Source: Data from Women and Wealth—Insights for Grantmakers. Asset Funders Network, 2015.

Where does this come from? Our personal finances are all interconnected. Each area of our money lives impacts each of the other areas. The wage gap combined with the pink tax (see Chapter 5) requires women to take out more debt. Even when women have the same credit profile as men, they pay higher interest rates (discrimination). This all leads to women investing less and buying less real estate (and the mortgages cost more for women when they do).

Then there's intersectionality, a term coined by lawyer and civil rights activist Kimberlé Crenshaw. Women of color, LGBTQ+, people with disabilities, and mothers experience these gaps in a compounding way. Kimberlé describes intersectionality as “a prism, for seeing the way in which various forms of inequality often operate together and exacerbate each other.”18 Yes, there is inequality based on gender identity, race/ethnicity, class, and sexual orientation, but many people are subject to some or all of these inequalities, not just one, and there's a cumulative effect.

Wait, you might be wondering why I included motherhood. A large part of the pay gap is due to motherhood. What? Mothers earn less for the same work than fathers do, experience workplace discrimination, and are pushed out of the workforce due to the lack of childcare and corporate support of parents, and this not only impacts their lifetime income but also their ability to invest, their access to retirement accounts, and their need to take on debt.

Not to mention, women live longer, which means they need more money in order to retire. It's enough to make you scream.

Another Gap That Has a History

In addition to all the current factors that play into the gender wealth gap, the world of money has historically been less accessible to women. The personal finance sector was created for and by men, leaving women out until very recently. These systemic barriers have set the stage for the gender wealth gap.

The Equal Credit Opportunity Act (ECOA) of 1974

Until 1974 when the ECOA passed, a woman couldn't take out a credit card in her own name without a male co-signer, like her husband or father. That's recent history. The act also granted women the ability to take out their own mortgage. Before then, many women seeking their own loans were laughed out of banks.

Women's wages were discounted by as much as 50% during the loan process when lenders decided how much they could borrow. You can imagine how that impacted what homes they could afford. Here's a hint – homes worth much less than those of their male counterparts.

The Equal Pay Act of 1963 and the Pregnancy Discrimination Act of 1978

At work things were similarly bleak. There was no requirement for equal pay until 1963 (still a big problem) and women could be legally fired for being pregnant until 1978 (it still happens illegally).

In addition, investing culture was dominated by white men. There wasn't one woman on the New York Stock Exchange until Muriel “Mickey” Siebert purchased a seat in 1967. Years earlier, women tried to make a stock exchange of their own in order to get a piece of the action.

The Double X Economy

Inequality has a real cost. Linda Scott, a professor emeritus at the University of Oxford and author of The Double X Economy, coined the phrase “Double X Economy” to address the systemic exclusion of women from the financial order (all over the world). Linda says “gender inequality causes poverty” – so it's not only the missed economic opportunity; “there's hunger that's attributable to this, there's war, there's disease. There's all types of terrible things.”19

I had the incredible opportunity to interview Linda for this book and she talked about the cost of not focusing on women, and gave the specific recent example of the pandemic Shecession of 2020.

From Linda:

From an economic perspective, those who run the world's economies are chasing growth (they want the economies to grow). Right now governments are trying to recover from the economic impact of the pandemic and for the most part they've ignored the special needs of women. It has been manifestly evident throughout the pandemic that women are suffering to a different degree and for different reasons than men, and obviously will need different solutions. And rather than deal with those needs, they are being pooh-poohed and set aside.

It's pretty ridiculous because on average, in the global economy, women contribute just under 40% of GDP and in the United States they contribute at least 40% of the GDP20 and make up more than half the workforce. In 41% of families, women are the primary breadwinner. And if women decided to form their own country, they'd immediately be big enough to join the G7 (the world's seven largest developed economies). When you're trying to kickstart an economy it doesn't make sense to ignore women!

Women are the world's most valuable wasted resource.

Linda's book starts with the Gloria Steinem quote, “The truth will set you free, but first it will piss you off.” Yep. Feeling that. But Linda shares some concrete actions we can take. We'll get to those shortly!

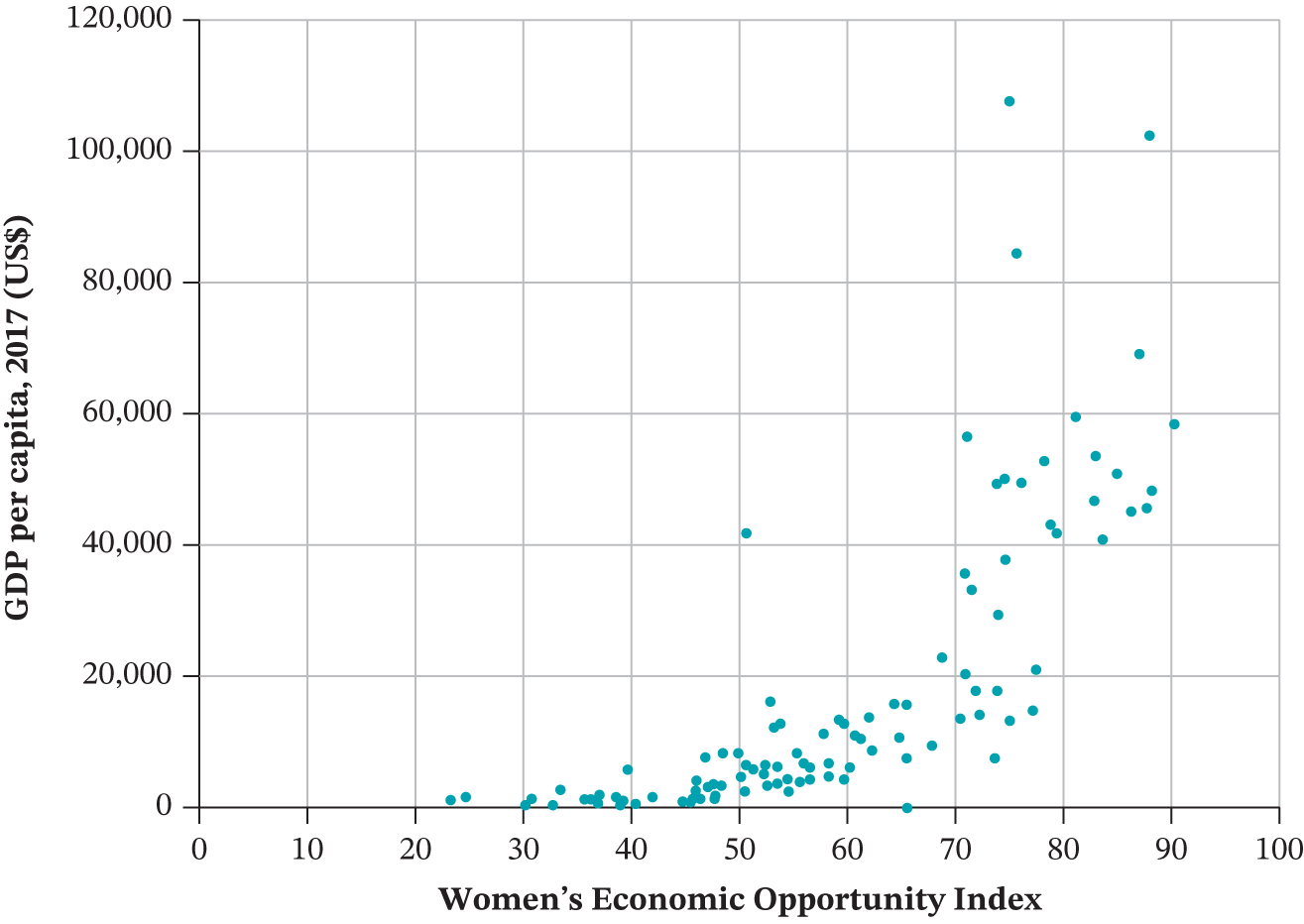

Women's Economic Opportunity and GDP

Each dot on the graph shown here represents a country's Women's Economic Opportunity Index score as related to GDP. There are approximately 100 nations shown in the graph; all those for which the data was available were included. In the graph, the upward-right direction of the dots indicates that more economic freedom for women corresponds positively to GDP per capita. Other data has converged to reach the same conclusion.

Sources: World Bank Database for GDP at purchasing power parity; Economist Intelligence Unit for the Women's Economic Opportunity Index; World Economic Forum for the National Competitiveness Index.

We Need Women to Be Wealthy

You know I believe this to my core. This is why I do the work that I do. I believe that getting more money into women's hands will solve many of the problems we see in the world today. A lot of brilliant experts (including Linda) agree with me.

Farnoosh weighs in: “When women are wealthy they have more financial agency. They can make decisions for themselves and get out of bad situations. We have to remember that we are still living in a sexist patriarchal world so we need money to help us combat those external headwinds.”

Women invest 90%21 of their income back into their families, compared with 35% for men. When women have more wealth it's better for children, it's better for families, it's better for companies, and it's better for the economy as a whole.

What Needs to Happen to Close These Gaps

The following are some of the proposed policy reforms that came up over and over again in my conversations with experts, but this list is by no means exhaustive. For more resources, head to the Financial Adulting toolkit.

Raise the Minimum Wage

80% of minimum wage workers22 are adults, two-thirds are women, and almost 25% are women of color (who make up 17% of the population). Raising the minimum wage to $15 would more than double the earnings of over 700,00023 women and give substantial raises to millions more. Now that's wage gap progress. In raising the minimum wage, it's critical to include people with disabilities. In most states, corporations are legally allowed to pay people with disabilities well below the minimum wage. Many politicians are working on eliminating this law.

Cancel Student Loan Debt

Student loans are a women's issue. Women have two-thirds of all student loan debt24 and the student loan debt burden disproportionately affects women of color. Linda says, “Women have to take out more debt in order to get the same jobs as men. And then they have to pay back the loans at a lower salary than men.” Alleviating some or all student debt is a way to remove the burden and level the playing field.

Tax the Super-Wealthy

I use the term super-wealthy because people are often worried that an increase in taxes will affect them. Most experts I spoke with were focused on taxing the richest people, people who bring home millions and millions or have net worths in the billions. This would allow for more programs to invest in underserved communities.

Farnoosh says, “I do find it problematic when the 50 richest Americans have as much wealth as half the U.S. I believe in the redistribution of the dollars in this country with the goal of supporting equity. I believe in taxing the rich more than others. I don't believe in trickle-down economics. I think the rich ought to pay a higher percentage in taxes and the government needs to give the working class a realistic opportunity to achieve wealth by reducing their taxes, and giving them more free access to things like healthcare, food, and housing.”25

Pay Reparations

In Mehrsa's book she writes about reparations: “An essential first step in dealing with the wealth gap is to acknowledge that it was created through racist public policy. Full justice demands a recognition of the historic breach of the social contract between America's constitutional democracy and Black Americans. And contract breach requires a remedy.” She doesn't recommend any remedy specifically but says we should encourage our policymakers to come up with “creative proposals that garner full and meaningful financial inclusion that reverse the effects of historic exclusions from wealth creation.”

Mandate Paid Leave

Caregiving responsibilities disproportionately fall to women and due to these responsibilities, combined with a lack of paid leave (almost one in four mothers have returned to work within two weeks of giving birth26), women are often forced to spend time out of the workforce. Research shows that workers can expect to lose up to three or four times their annual salary for each year out of the workforce due to the loss in future income and raises.27

Women who have paid leave are more likely to stay in the workforce the year following birth and are 54% more likely to report wage increases.28 Paid leave for fathers also plays an important role. For every month a father takes paternity leave, his partner's income increases by 6.7%.29,30

Build a System of Universal, Affordable, High-Quality Childcare

Linda argues that building a childcare system would actually be the most important and impactful intervention worldwide. She says it should be treated as “economic infrastructure” (meaning it's available to everyone) and because “it's the biggest barrier to women participating in the economy it would easily pay for itself.” She adds that “there's really no excuse for not doing it except for the stupid old fashioned idea that in some moral world women should be at home. And I try to make it clear in the book that that idea comes from a history of keeping women captive.” Burning rage!

Reform Our Healthcare System

Medical expenses are the number-one cause of personal bankruptcy in the United States and debt rates are much higher for those who are uninsured or underinsured, which are disproportionately people of color. As you can imagine, high medical expenses and resulting medical debt impact a family's ability to plan, save, and build wealth.

Build a Bigger Coalition

Linda says “we've allowed feminism to be cast as a left-wing issue. The left wing claims it and the right wing disdains it, but among the American public, treating women and men equally is just what decent people do. It's a core centrist value and we should start treating it that way.” She argues that “these issues, issues around capital and the economy, are things that in my experience, speak very strongly to republican, financially conservative women.” She believes we can build a bigger coalition from all political parties.

Equality versus Equity

The distinction between equality and equity is extremely important in personal finance. Dasha describes equality as giving everyone the exact same personal finance resources and saying “I provided you with tools, now it's up to you to use them,” whereas equity is giving people the resources that apply specifically to their experiences and needs, especially those in communities that are impacted by systemic gaps and discrimination.

Dasha explained:

Black women live at the intersection of race and gender so we're always fighting two battles. 81% of Black mothers are the primary breadwinners of their homes.31 That means four out of five Black families depend on the paycheck of a Black woman to survive. The conversation around personal finance will be different for us.

When I first started as a financial educator, I'd hear other educators swear off credit and say “Credit is bad. If you can't afford it now, don't get it.” But this is a very privileged and judgmental perspective. For Black women, and Black people as a whole, credit can be a saving grace because it fills the gap when we're not paid fairly and our families haven't had the opportunity to build wealth. Instead of swearing it off, equity is teaching people how to understand it and leverage it if it's needed.

Because personal finance systems look different for each of us depending on our privilege, race, gender, and sexuality, we need more nuance and perspective in financial education.

Your Education Matters

In talking to so many people, especially women, about their financial lives, I've found a common thread in many of our stories. So many of our financial successes come from someone who gave us a nudge. This might be a colleague who urged us to set up our 401(k), a friend who sat down with us to show us how she budgets, or the colleague who bravely shared what she's getting paid so we could compare.

When we get educated around our money, not only do we lift ourselves and our families up, we can be an example of what's possible and we can give others the nudge they need. We bring others up with us and that has a tremendous impact.

Your Financial Adulting Action Items

- Understand that politics and money are inseparable.

- Understand the racial and gender wealth gaps – where they come from, how they are perpetuated, and how they currently affect your own personal finances.

- Help close the gap. In addition to the resources here, you can learn more in the Financial Adulting toolkit. Build your knowledge, use your voice, and vote for leaders who believe in the changes you do.

- Support financial educators (and businesses) who share your values and are women and BIPOC-owned.

- Become a financial adult. As you learn and achieve more, you'll bring yourself and others up with you.

As you go through each of the following chapters covering different financial topics, you'll see that equity, privilege, and policy are integral parts of the big picture – no more financial advice in a silo. That's the first step to being a financial adult. First up, your money goals!

Notes

- 1. “CPI Inflation Calculator,” U.S. Bureau of Labor Statistics (July 2009–August 2021), https://www.bls.gov/data/inflation_calculator.htm.

- 2. “Disparities in Wealth by Race and Ethnicity in the 2019 Survey of Consumer Finances,” The Federal Reserve (September 28, 2020), https://www.federalreserve.gov/econres/notes/feds-notes/disparities-in-wealth-by-race-and-ethnicity-in-the-2019-survey-of-consumer-finances-accessible-20200928.htm#fig1.

- 3. Heather McCulloch, “Closing the Women's Wealth Gap” (January 2017), https://womenswealthgap.org/wp-content/uploads/2017/06/Closing-the-Womens-Wealth-Gap-Report-Jan2017.pdf (chart, p. 4). Original source: https://assetfunders.org/wp-content/uploads/Women_Wealth_-Insights_Grantmakers_brief_15.pdf.

- 4. “Moms Equal Pay Day 2021,” Equal Pay Today, http://www.equalpaytoday.org/moms-equal-pay-day-2021.

- * When I say BS, I mean bullshit.

- 5. “Disparities in Wealth by Race and Ethnicity.”

- 6. Melany De La Cruz-Viesca, Zhenxiang Chen, Paul M. Ong, Darrick Hamilton, William A. Darity Jr., “The Color of Wealth in Los Angeles,” The Federal Reserve Bank of Los Angeles (2016), http://www.aasc.ucla.edu/besol/Color_of_Wealth_Report.pdf (p. 5).

- 7. Mariko Chang, “Lifting as We Climb: Women of Color, Wealth, and America's Future,” Center for Community Economic Development (Spring 2010), https://static1.squarespace.com/static/5c50b84131d4df5265e7392d/t/5c5c7801ec212d4fd499ba39/1549563907681/Lifting_As_We_Climb_InsightCCED_2010.pdf (p. 14).

- 8. Dedrick Asante-Muhammed, Chuck Collins, Josh Hoxie, and Emanuel Neves, “The Ever-Growing Gap,” Institute for Policy Studies (August 2016), https://ips-dc.org/wp-content/uploads/2016/08/The-Ever-Growing-Gap-CFED_IPS-Final-2.pdf.

- 9. “The Homestead Act of 1862,” National Archives (June 2, 2021), https://www.archives.gov/education/lessons/homestead-act#:~:text=President%20Abraham%20Lincoln%20signed%20the,pay%20a%20small%20registration%20fee.

- 10. Ibid.

- 11. Ibid.

- 12. Ian Webster, “Value of $1.25 from 1862 to 2021,” CPI Inflation Calculator, https://www.in2013dollars.com/us/inflation/1862?amount=1.25.

- 13. Keri Leigh Merritt, “Land and the Roots of African-American Poverty,” Aeon (March 11, 2016), https://aeon.co/ideas/land-and-the-roots-of-african-american-poverty.

- 14. Mehrsa Baradaran, The Color of Money: Black Banks and the Racial Wealth Gap (Cambridge, MA: Belknap Press of Harvard University Press, 2017), p. 30 ($3 million lost in 1874); https://www.in2013dollars.com/us/inflation/1874?amount=3000000.

- 15. Ibid., p. 108 (entire section).

- 16. Ibid., p. 109.

- 17. History.com editors, “Jim Crow Laws,” History.com (March 26, 2021), https://www.history.com/topics/early-20th-century-us/jim-crow-laws.

- 18. “Intersectional Feminism: What It Means and Why It Matters Right Now,” UN Women (July 1, 2020), https://www.unwomen.org/en/news/stories/2020/6/explainer-intersectional-feminism-what-it-means-and-why-it-matters.

- 19. Linda Scott, “Gender Inequality Causes Poverty,” Double X Economy (March 29 2021), https://www.doublexeconomy.com/post/gender-inequality-causes-poverty.

- 20. “The Power of Parity: Advancing Women's Equality in the United States,” McKinsey Global Institute (April 2016), https://www.mckinsey.com/~/media/mckinsey/featured%20insights/employment%20and%20growth/the%20power%20of%20parity%20advancing%20womens%20equality%20in%20the%20united%20states/mgi-power-of-parity-in-us-full-report-april-2016.ashx#:~:text=Yet%20women%20in%20the%20United,women%20make%20to%20the%20economy, p. 9.

- 21. “Empowering Girls & Women,” Clinton Global Initiative, https://www.un.org/en/ecosoc/phlntrpy/notes/clinton.pdf.

- 22. “Minimum Wage,” Women Employed, https://womenemployed.org/minimum-wage/.

- 23. Ibid. (for total minimum wage workers); “Characteristics of Minimum Wage Workers, 2020,” U.S. Bureau of Labor Statistics (February 2021), https://www.bls.gov/opub/reports/minimum-wage/2020/home.htm.

- 24. “Deeper in Debt: Women & Student Loans,” AAUW (2021), https://www.aauw.org/resources/research/deeper-in-debt/.

- 25. Ben Steverman and Alexandre Tanzi, “The 50 Richest Americans Are Worth as Much as the Poorest 165 Million,” Bloomberg (August 10, 2020), https://www.bloomberg.com/news/articles/2020-10-08/top-50-richest-people-in-the-us-are-worth-as-much-as-poorest-165-million.

- 26. “Report: 1 in 4 Mothers Go Back to Work Less Than 2 Weeks After Giving Birth,” Abt Associates (August 20, 2015), https://www.abtassociates.com/who-we-are/news/in-the-news/report-1-in-4-mothers-go-back-to-work-less-than-2-weeks-after-giving.

- 27. “Calculating the Hidden Cost of Interrupting a Career for Child Care,” Center for American Progress (June 21, 2016), https://www.americanprogress.org/issues/early-childhood/reports/2016/06/21/139731/calculating-the-hidden-cost-of-interrupting-a-career-for-child-care/.

- 28. Linda Houser and Thomas P. Vartanian, “Pay Matters: The Positive Economic Impacts of Paid Family Leave for Families, Businesses and the Public,” Rutgers Center for Women and Work (January 2012), https://www.nationalpartnership.org/our-work/resources/economic-justice/other/pay-matters.pdf.

- 29. Rosie Colosi, “Paternity Leave Is a Lifesaver for Working Moms … But Are Dads Taking It?” CBS News (July 20, 2019), https://www.nbcnews.com/know-your-value/feature/paternity-leave-life-saver-working-moms-are-dads-taking-it-ncna1036226.

- 30. Elly Ann-Johansson, “The Effect of Own and Spousal Parental Leave on Earnings,” Institute for Labour Market Policy Evaluation (March 22, 2010), https://www.ifau.se/globalassets/pdf/se/2010/wp10-4-The-effect-of-own-and-spousal-parental-leave-on-earnings.pdf (p. 28).

- 31. Julie Anderson, “Breadwinner Mothers by Race/Ethnicity and State,” Institute for Women's Policy Research (September 2016), https://iwpr.org/wp-content/uploads/2020/08/Q054.pdf.