CHAPTER 9

Buying a Home

Whether you're thinking of buying your first home or a rental property, you're investing in real estate. There are many things to consider and navigate as you decide whether it makes sense for you to buy a home and then go through the process. Here we go!

Buying a Home – How It Works

Most of us won't be able to (or want to) pay the entire price of the home in full (commonly referred to as paying in cash). Most home buyers pay a chunk of money up front (in the form of a down payment) and finance the rest using a specific type of loan called a mortgage.

Before we talk about the home-buying process, it's important to answer a few questions.

Rent versus Buy?

Ah, the “American Dream.” Own a home with a two-car garage and a white picket fence and you're on your way to happiness, right? Not quite. There are many misconceptions about homeownership. A big one is that it makes financial sense for everyone to own a home and paying rent is a “waste of money.” Homeownership doesn't make sense for everyone and there are many factors to consider before taking the leap.

Timing

Consider how long you plan to stay in this home. There are costs involved with buying and selling a home. The longer we own a home, the longer we give it time to appreciate (or increase) in value and the longer we give it to lessen the burden of those up-front and back-end costs.

Your Budget

Your budget can determine how long you want or are able to stay in a certain home. If there's a neighborhood you really want to live in but it doesn't work with your budget yet, you might want to wait to purchase so that when you do, you can see yourself living there for a long time. Or if you plan to have kids or expect parents or other family to move in with you, you may want to wait to purchase a home that can accommodate your growing family.

Your Goals

The financial piece of the home purchase is really important, but it's not everything. A lot of people purchase a home not because it's the best use of their capital (i.e., cash) but because it's something they want. It's important to them. Maybe they want to have a place to call and make their own. Or maybe it provides a sense of financial security to not depend on the rental market.

How Much Will This Cost?

Have you heard the term “house poor”? It's a sad phrase for a very common situation where homeowners spend all (or most) of their savings to purchase their home, plus a large portion of their income goes to their mortgage (and other home-related expenses). It's not fun or comfy, so we want to go in with our eyes wide open.

The Down Payment

This is the most well-known expense associated with buying a home. It's also the largest and most daunting (by far), which explains why it gets so much attention.

With a conventional mortgage, if your down payment is below 20%, you'll likely pay private mortgage insurance (PMI), which is usually 0.5–1.5% of the cost of the mortgage each year. Not having to pay PMI is ideal, but putting 20% down also makes purchasing a home potentially out of reach for many, especially in the short term.

There are some other reasons you might want to consider a larger down payment. Putting more money down can:

- Make your offer look more competitive, especially in a hot real estate market

- Mean a lower monthly payment, which can make monthly costs more affordable

- Typically mean a lower interest rate, which will save you in interest costs

- Make it easier to secure a mortgage (the loan is viewed as less risky)

Mortgage Closing Costs

Closing costs are the expenses associated with the mortgage and closing on (finalizing) the purchase or sale of the home. The exact amounts will vary by state, the cost of your home, the mortgage, and whom you hire. Head to the Financial Adulting toolkit for a closing cost calculator, which will give you an idea of what they will be in your area, given your mortgage size. Some closing costs may include:

- Title insurance

- Prepaid expenses (interest and taxes)

- Wire fees

- Loan origination fees

- Additional taxes and fees

- Escrow fees

- Broker fees (for sale of a home only)

Wait, what are escrow fees? Escrow fees are fees that go toward setting up your escrow account. An escrow account is an account created and held by a third party where you put your earnest money (also called a deposit) until your home purchase closes. These funds are applied toward your down payment. Then, a separate escrow account managed by the company servicing your mortgage can be set up (and may be required). It will usually use part of every monthly payment to fund property taxes and insurance out of the account.

Other Closing Costs

But that's not all … here are some other potential closing costs.

- Home inspection

- Homeowners insurance

- Real estate attorney

- Private mortgage insurance (PMI)

Life Insurance

This one might come as a surprise but if you are buying a home with a partner, life insurance can be an important purchase if one person wouldn't be able to afford the payments on their own. Life insurance can protect them from having to sell the home or default on the mortgage if something were to happen to their partner.

If you are buying a home on your own, you may still want to purchase life insurance. If something were to happen to you, whoever you leave the house to would be responsible for the mortgage payments (and all other costs). If you want them to be able keep the home and not have to sell it, life insurance might be needed for them to do that. We talk life insurance in detail in Chapter 10.

Home Emergency Fund

When we own our own homes, we can no longer call the landlord when something breaks. This is a big adjustment (at least it was for me). If your dishwasher breaks or something happens with the AC, you're going to have to foot the bill. To prepare for these inevitable home repairs, you will want to create a new rainy-day fund for your home in addition to your regular rainy-day fund, or you can increase the amount you keep in your original rainy-day fund to cover unexpected home costs.

Property Taxes

Property taxes are an annual tax that will vary by where you live and the assessed value of your property. The assessed value of your home is often not the price you paid for it (which is called the appraised or market value), but a value placed on it by the local government for calculating taxes.

The amount you owe in property taxes will change every certain number of years when the property is reassessed or if there is an increase in property taxes in your town. How often your taxes will be reassessed varies by city.

Updates, Renovations, and Decor

When you purchase a home, you'll likely want to start adding your personal touches or notice that some aspect (or many) of the home wants some love and attention. Updates (like painting), decor costs (like lighting and furniture), and any renovation expenses should be included in your home plan. These costs can be significant if you are investing in a fixer-upper or if many things arise from the home inspection.

Maintenance Expenses

If you are buying a co-op or condo, or live in a development, you'll likely have a monthly maintenance fee or HOA (homeowner's association) fee. This is money that the building or community uses each month for cleaning, staff, amenities, and reserves for larger projects. Even if you are buying a house, there can be monthly or quarterly maintenance fees associated with neighborhood upkeep, such as maintenance of common lawn areas, sidewalks, sewer lines, or streetlights.

When you see a price that feels too good to be true, check out these fees. Sometimes they are so high it's like adding a rent payment on top of your mortgage.

If you are moving from an apartment to a house or even to a larger home, it's important to account for any additional costs that you didn't have before. Will your utilities be higher? Do you now have a lawn to take care of? An annual chimney cleaning? Will you need to buy more furniture?

Costs of the Move Itself

Once you've purchased your home, you'll need to figure out how to get all your stuff there. This is an expense we often forget about or underestimate. Depending on how far you have to move and how much stuff you have, moving costs will vary. When making your plan, get estimates from some reputable movers in your area to see how much you should save up or account for.

Incorporate These Costs into Your Plan

Add Up the One-Time Costs

If you decide to buy a home, this is your home savings goal. If it feels astronomical and far away, I get it. If it's important for you to become a homeowner sooner, adjust your expectations. Or if your wishlist is nonnegotiable, you can increase the time it will take to reach the goal (for now).

Incorporate the Ongoing Costs

For the ongoing expenses, we go back to our friendly financial plan (or happiness allocation). You can estimate the ongoing costs and enter them into your plan to see if they're workable with your current (or estimated) income and other expenses.

“Try On” Your Estimated Homeowner Expenses

This is brilliant (if I do say so myself) and often skipped over. One of the easiest ways to see how being a homeowner will feel financially is to “try on” your new expenses for size. Take the estimated monthly costs you calculated, including your mortgage, property taxes, insurance, and HOA, if applicable. If this is more than you are paying now for housing, transfer the difference to savings each month. For example, if the total will be $2,000 per month and you are currently paying $1,500, pay your bills as usual and transfer an additional $500 to savings. It's a win-win because you'll be saving up for your new home while also getting an idea of how this home will affect your spending plan.

Wait, I'm Discouraged; This Is Much More Expensive Than I Thought

I know. Saving up for a home is a really big goal. Know that your progress toward your goals doesn't have to be linear and it won't be. Just because I'm saving $5 or $20 per paycheck right now doesn't mean that it will take me 10,000 years to save up for a home. Our progress can be exponential, especially as we learn new skills and get motivated by our results. And it's okay if it takes you some time to reach this goal! It's a big one.

Also, if you earn a commission or receive a bonus or lump-sum payment, putting aside a significant portion of that (if possible) can help you reach your homeownership goal.

Stay motivated: Keep an image handy of your home (or the home you want) on your phone or in your wallet. Look at it often. Before we bought our home I was working in a windowless basement in our apartment on the Upper West Side. I really wanted to work in an office with a big sunny window. This is the image I kept on my desk and in my mind as we searched for our new home. When we bought our condo there was a room with a big window and that's right where I put my desk!

Organize Your Finances Before Starting the Process

There are a couple things you can do in advance that will make your life much easier during this process. Believe me, I know. I didn't do them.

Check Your Credit Score and Get Credit Ready

Our credit score is typically one of the most important factors lenders consider when we're applying for a mortgage. Not only does it determine if we qualify for a loan (more details on this later), it can also impact the interest rate we're offered (which can matter a lot on a big loan). We'll talk credit scores in detail in Chapter 12. Increasing your score can take time, so the earlier you start making moves, the better.

Simplify Your Accounts

During the mortgage process, you'll be sending over lots (and lots) of financial information, and then more follow-up financial information and then more follow-up financial information and … you get the idea. It's painful. The simpler your financial life, the easier this will be. Consolidate accounts where you can. Make a list of everything you have (and owe) and where, and know your logins and passwords.

Important: Do this before you apply for a mortgage. Moving money around and making account changes during the mortgage process will lead to much more paperwork and even more of a headache.

Go on a Buyer's Budget

Fee Gentry, MBA real estate professional, founder of the Black eXp Network (a network of 3,700 Black real estate professionals and allies) and co-creator of the Agent Accelerator Academy, a 60-day course teaching agents to work with communities of color, recommends reducing expenses before the home-buying process; it is a win-win because it makes your spending look good for your lender and you'll also be saving more money. Not only that, don't make any major purchases and don't open a credit card, take out other debt, or refinance your student loans (which will affect your credit). This buyer's budget is all about keeping spending down and keeping yourself credit ready.

Understand the Types of Mortgages Available

Your mortgage is a big deal. For many of us, it's the largest loan we've ever received. Here are the key details of the different options.

- Conventional loans. A conventional mortgage is a mortgage with a bank rather than with the government. You will typically need a credit score of 620 or higher to qualify but exceptions can be made depending on your personal finance profile (like how much income you earn and cash you have in the bank). Below are some common types of conventional mortgages. “Jumbo” mortgages are larger than conventional loans and come in these same types.

- Fixed-rate mortgages. These mortgages have the same interest rate for the entire life of the loan. You might see 30-year, 15-year, 10-year, and even 7-year fixed-rate mortgages. You don't have to worry about interest rate fluctuations. What you sign is what you get. It's typically more expensive (interest-rate-wise) to lock in an interest rate for a long period of time. Depending on how long you plan to live in your home or how quickly you plan to pay off your mortgage, it may be worth getting a mortgage for less time.

- Adjustable-rate mortgages (ARMs). These mortgages have a fixed rate for a certain period of time and then the rate adjusts depending on where interest rates are at the time. A 10/1 ARM is an example of an adjustable-rate mortgage. The rate is fixed for 10 years and then adjusts each year going forward.

- Interest-only mortgage. This is exactly what it sounds like. You're only required to pay off the monthly interest and don't have to make payments toward principal. This one requires a lot of discipline to pay down any of the mortgage principal – discipline I don't have.

- FHA loan. These loans are backed by the Federal Housing Administration (FHA). You can generally qualify for an FHA loan with a credit score of 580 or above and your down payment can be as low as 3.5%. The catch with a down payment below 20% is that you'll usually be required to pay an MIP (mortgage insurance premium), which typically costs 0.45–1.05% of the cost of the mortgage each year and 1.75% for upfront MIP. If you are using the rent vs. buy calculator, make sure it factors in MIP, or you can add that to your mortgage interest rate as a proxy. You'll also want to add it into your ongoing costs in your budget. There are size limits on the loan, which will depend on your location.

- USDA and VA mortgages. These are two other mortgage options for those who qualify in rural areas or are military-qualified borrowers, respectively. Neither requires a down payment and the VA mortgage doesn't require mortgage insurance.

Outside of mortgages there are financial assistance programs available for first-time homebuyers.

- Housing Choice Voucher (HCV) homeownership program. This program provides monthly payment and down payment assistance to first-time homebuyers who meet specific income and employment requirements. You can learn more at hud.gov.

- There are also state and local programs that provide first-time home-buying assistance to veterans, those in specific industries (like teachers and service members), specific locations (like in rural areas), and at specific income levels. What's available varies by state (and county) but it's worth looking into!

Fee encourages us to ask the mortgage bankers lots of questions and to deep-dive watching mortgage tutorials on YouTube. I understand the tendency to want to get the process over and done with but I promise it's worth taking the time to really understand what's available.

Should You Go Digital or Analog?

Fee says that sometimes the digital mortgage companies work really well (they're convenient and can remove bias from the mortgage process) and that there are also benefits to working with a local provider (they're more familiar with how loans are written in that specific community and they work to compete with the “big” mortgage companies). I'm a fan of trying both and seeing where you get the best rate.

Fee says that in the same way you ask questions of your agent (I have a list for you in the toolkit), you can also ask questions of your lender, such as: “I'm concerned because I've heard that women or those in the AAPI community or senior citizens get discriminated against. Can you walk me through the process?” You can learn a lot from how they respond.

An Important Ratio to Lenders

Each lender has their own metrics they look for in a borrower. In addition to your credit score, lenders will also look at your debt-to-income (DTI) ratio. Your DTI ratio is calculated by taking the total amount of money you put toward debt payments each month and dividing that by your gross monthly income. Gross monthly income means your income before taxes and deductions are taken out. If you earn commissions or bonuses, those can go in there too. You can calculate your gross monthly income by taking your annual income and dividing it by 12.

Lenders look at two DTI ratios during the mortgage approval process. First, they look at the ratio of all your new housing costs to your gross income (front-end DTI ratio). These costs include your mortgage principal and interest, insurance, property taxes, and HOA dues (if applicable). Then they look at your new mortgage and all other monthly debt payments you make as a percentage of your gross monthly income (back-end DTI ratio).

Some lenders may have a DTI ratio limit with restrictions on lending to people above that limit. For example, a lender may want to see a DTI ratio below 35%, with no more than 28% going to your mortgage. That means that if you earn $50,000, your annual debt payments will need to be below $17,500 and only $14,000 of that can go toward mortgage payments. But lenders also take credit score and cash reserves into account and can make exceptions.

If you are looking to improve your DTI, a great way to do that is to pay down debt. We'll make a plan to pay off your debt in Chapter 13.

What About Discrimination in Lending?

Fee shared, “I see it every single time. Single women and people of color go through a different level of scrutiny by underwriters than let's say any married, straight white couple. I've had clients who are single women with an 800 credit score and $250,000 cash in the bank and then another million in assets saved, and the lender will come back with a higher interest rate than for some married dude who has a 650 credit score.” And the same pattern is repeated with people of color.

It's the unfortunate reality and Fee says that all you can do is prepare for the extra level of scrutiny and have responses planned for any questions or pushback you get. For example, if you have student loans, be ready to share when they will be completely paid off and how you've never missed or had a late payment. She says a good agent should be able to help you prepare for this as well.

Understand Key Mortgage Jargon

Here is some jargon you'll want to know for the interest rate conversations:

- Interest rate. The amount you'll pay in interest each year on the mortgage. It does not include any fees or other mortgage costs you pay.

- APR (annual percentage rate). The total cost of borrowing money. It includes the interest rate, points (more on this next), mortgage broker fees, and any other charges.

- Points (short for discount points). Allow you to pay more upfront (in the form of a fee) to lower your interest rate. Credits are the opposite. They allow you to pay less up front in closing costs in exchange for a higher interest rate. Which should you choose? I always recommend running the numbers. If you pay $500 now to pay $15 less each month, it will take 33 months (2.75 years) to break even. If you are moving into a long-term home, it could be worth paying points up front to have that lower interest rate. If it's a shorter-term purchase, it might be worth it to pay less now and have a higher interest rate.

Three Scenarios of How Points Affect Interest Rate

Source: ConsumerFinance.gov.

Should I Pay Down My Mortgage?

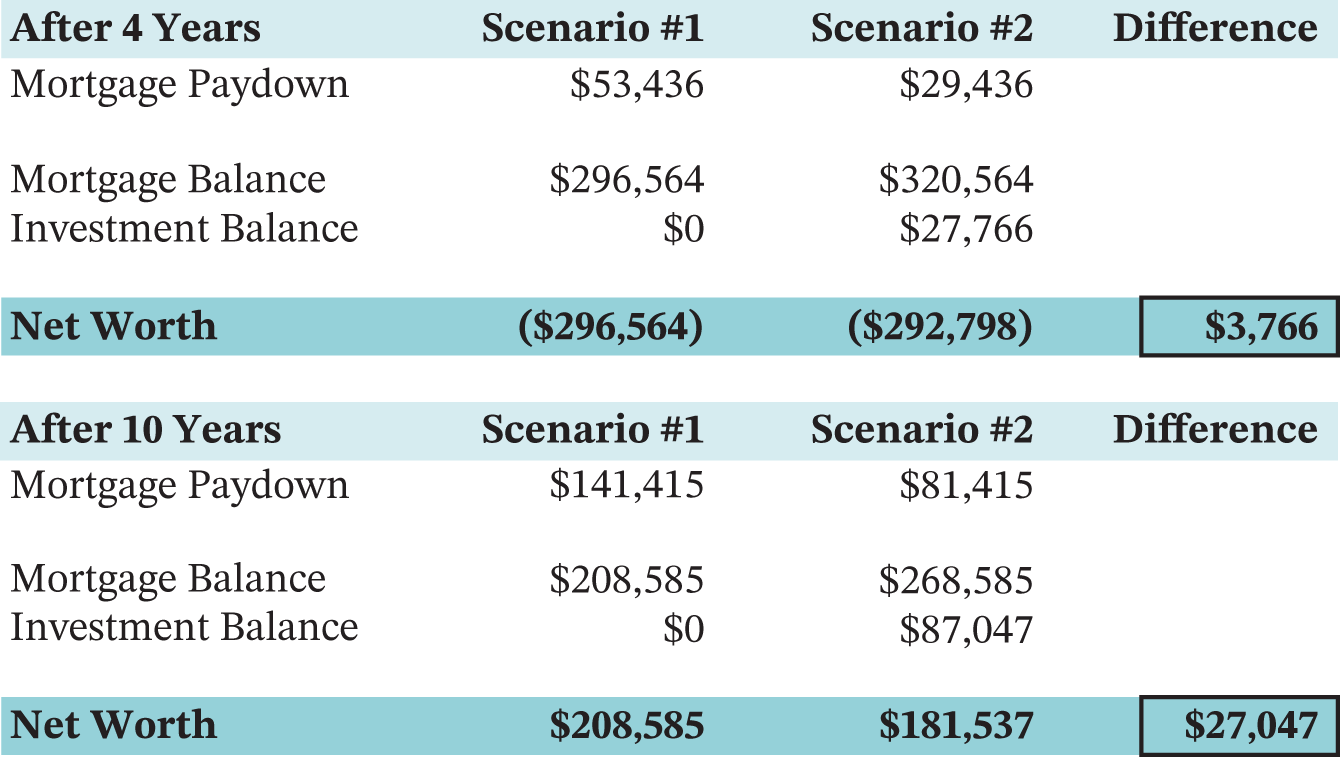

Mortgage paydown will definitely come after building your rainy-day fund, 401(k) matching, paying down debt with a higher interest rate, and saving for retirement, but after that, it comes down to the opportunity cost of that money and your level of comfort with debt. This example can help you think it through:

Let's say you have a $350,000 mortgage, with an interest rate of 3.25% and a $1,523 monthly payment. In scenario #1, you pay an additional $500 per month toward your mortgage and in scenario #2 you pay your mortgage and invest the additional $500 with an interest rate of 7%. You can run a similar comparison with your own mortgage information (there's a template in the Financial Adulting toolkit).

You'll see that over time, investing outpaces the mortgage paydown, and in scenario #2, you'd have a net worth of $27,047 more after 10 years. Note: To keep things simple, I only included the mortgage and investment balance from new investments in the net worth calculation.

“Fun” fact: Some lenders offer free recasting of your mortgage once you've paid down a certain amount of additional principal on the loan. This means they recalculate (or recast) your payments using the lower loan balance. For example, if you have a $150,000 mortgage balance and pay down an extra $20,000 in principal, your payments after recasting are now based on a mortgage of $130,000. This allows your total monthly payment to go down. Not hating that.

Another “Fun” fact: If you have a 30-year mortgage, your mortgage is amortized over 30 years. Your payments stay the same each month but what the payments go toward changes over time. At first, your payments are more interest than principal because your loan is at its highest balance. Over time, as you pay down your principal, the payments go more and more toward paying down the loan balance than interest. You can check out an amortization calculator for more details in the Financial Adulting toolkit.

When Should I Refinance?

The short answer is, when the numbers make sense. If you can refinance for a lower rate, that's great. It costs money to refinance – sometimes thousands of dollars – so it's also helpful to calculate how long it will take for the monthly savings to pay off or break even with the fees. For example, if you are spending $1,000 to refinance and it will save you $200 a month on your mortgage, you break even in five months. There are some handy calculators to help in the toolkit! Refinancing can also help you lock in a lower interest rate if your mortgage is moving to an adjustable rate in the nearish future.

Another Way to Invest in Real Estate – REITs

If buying real estate feels too far out of reach or it's not quite a fit, there are other ways to get the benefits without a lot of the risk or costs. Real estate investment trusts (REITs) are companies that invest in real estate. By owning a share of a REIT (essentially a real estate fund) you own the properties in that REIT. Instead of purchasing a property of your own, you can buy a share of a REIT for $100 and own a piece of hundreds of properties.

Your Financial Adulting Action Items

- If you are a woman or BIPOC, know that you will most likely encounter discrimination during the homebuying process.

- Decide whether it makes sense for you to purchase a home financially, but don't forget to weigh subjective factors as well.

- Estimate the one-time cost to buy a home as well as the ongoing costs.

- Incorporate the estimated costs into your financial plan. Are they workable?

- “Try on” your estimated monthly homeowner expenses to see how they feel.

- Start saving (if you haven't already) for the larger one-time expenses.

- If you are buying a home with a partner, protect yourself with a prenup or cohabitation agreement.

- Add your mortgage to your goal priority lists, if it's not there already.

- Run a refinance calculator and/or see if it makes sense to recast your mortgage.

- Research some REITs.

This chapter was a biggie. You are now clear on whether or not it makes sense for you to buy a home. If it does, you now know the true cost and you are also a whiz on everything related to mortgages. Whew!

Retirement investor – check! Investor for good – check! Real estate investor – check! The next section of the book is critical, yet something we tend to want to glaze over. First up, we'll talk about protecting yourself. I'm talking protecting your income, protecting your chosen family, protecting your health, protecting your home, protecting your car – all the protecting.

Notes

- 1. “Disparities in Wealth by Race and Ethnicity in the 2019 Survey of Consumer Finances,” The Federal Reserve (September 28, 2020), https://www.federalreserve.gov/econres/notes/feds-notes/disparities-in-wealth-by-race-and-ethnicity-in-the-2019-survey-of-consumer-finances-accessible-20200928.htm#fig4.

- 2. Stefanos Chen, “The Resilience of New York's Black Homeowners,” New York Times (August 17, 2021), https://www.nytimes.com/2021/08/17/realestate/new-york-black-homeowners.html.

- 3. Andre M. Perry, Jonathan Rothwell, and David Harshbarger, “The Devaluation of Assets in Black Neighborhoods,” The Brookings Institution (November 27, 2018), https://www.brookings.edu/research/devaluation-of-assets-in-black-neighborhoods/.

- 4. Ibid.