CHAPTER 9

The Sukuk Portfolio

A Broader Investment Universe for Mainstream Investors

O ye who believe! Fulfill your undertakings.

(Al Maeda: 1)13

INTRODUCTION

According to Global Islamic Finance Report (2012), it is regrettable that the Goldman Sachs global Sukuk, which was assigned by Moody’s a (P)A1 rating on November 3, 2011, and assigned an A+/F1+ rating by Fitch on October 19, 2011, was not acceptable as a Shariah-investible asset. It appeared to adopt a controversial structure geared toward the conventional finance needs of the investment bank, which involve opportunities for riba, or interest.1 This is a unique case because it seemed that the proceeds of the Sukuk would be used in a noncompliant manner. This has yet to be accepted and offered.

However, investors should take comfort that all existing approved Sukuks in the market are deemed Shariah compliant from the standpoint that all Sukuk proceeds are used for purposes of productive economic activities, which benefit mankind. Put simply, Sukuk refers to fixed-income instruments (or bonds) that are structured based on Shariah principles. As the earning of interest is forbidden in Islam, therefore traditional interest-paying bonds structures are unacceptable in Islamic investing.

Sukuks are investment certificates consisting of ownership claims in a pool of assets, whereas bonds are interest-bearing securities. The claim embodied in Sukuk is a claim to both cash flow and ownership. A bond is a debt obligation, meaning the issuer is expected to pay bondholders on certain specified dates, interest and principal amounts.

Sukuk holders are entitled to share in the revenues generated by the Sukuk assets, as well as in the proceeds of the sale of the Sukuk assets, as they can claim an undivided beneficial ownership of the assets.

Similar to conventional fixed income, the structuring and pricing of Sukuks will still be assessed by international rating agencies for investors to refer to in assessing the risk/return parameters of a Sukuk issue.

Sukuk as a financing instrument has shown a track record of growth. As of the second quarter of 2012, Sukuks outstanding totaled USD243.4 billion within Europe.2 The United Kingdom is well positioned to become the international hub for Islamic capital markets, worth USD271.0 million Sukuks outstanding.3 Ireland and France are close behind, with both governments passing a law enabling the issuance of Sukuks in 2009.

The 2009 Dubai debt crisis erroneously gave the global investment community a poor impression of Sukuk (Shariah-compliant fixed-income) investing. Having fully recovered from this, the Sukuk market performance has proved resilient for the past two years. Sukuk investing not only enhances potential returns relative to conventional fixed-income investing but also reduces portfolio volatility.

This chapter will shed light on how Sukuk investing offers diversification benefits by examining the investment universe, sector weightings, and country spread. It will conclude with a case study of how investors who have limited themselves to investing in the conventional fixed-income asset class can definitively add value to their portfolios by allocating a portion to the Sukuk investment universe.

Although Gulf Cooperation Council (GCC) countries such as the United Arab Emirates, Bahrain, and Qatar have become regional Islamic finance hubs, the evolution of Sukuk structures was pioneered by Malaysia, which remains the main issuer of Sukuk with USD 129.43 billion in 2012.4

EMERGENCE OF DIFFERENT SUKUK STRUCTURES

Supported by the right regulatory framework and favorable tax systems, Malaysia emerged as the global leader in Sukuk issuance with 71.6 percent of the global issuance originating from Malaysia during the third quarter of 2011 followed by MENA, which contributed 16 percent.5 Malaysia’s dominance in the global Sukuk market is reflected by its contribution of 65 percent to the total global outstanding Sukuk issuance.6

In 2001, Malaysia issued the first global corporate Sukuk and first Ijarah Sukuk. In 2002, Malaysia issued the first global sovereign Ijarah Sukuk followed by the first tradable Istisna Sukuk in 2003. Malaysian exemplary pioneering in the global Sukuk industry is further demonstrated in Table 9.1.

Table 9.1 List of Malaysia’s Significant Issuances

| Year | Amount | Sukuk Structures |

| 1990 | RM125 million (USD33 million) | The world’s first corporate Sukuk and the world’s first BBA Sukuk by Shell MDS Sdn Bhd |

| 1994 | RM30 million (USD8 million) | The world’s first Islamic mortgage-backed securities (with recourse) via Sukuk Mudharabah by Cagamas. Bhd |

| 2001 | USD150 million | The world’s first global corporate Sukuk and the world’s first Ijarah Sukuk by Kumpulan Guthrie Bhd |

| 2002 | USD600 million | The world’s first global sovereign Sukuk by the Government of Malaysia |

| 2003 | RM5.6 billion (USD1.5 billion) | The world’s first tradable Sukuk Istisna by SKS Power Sdn Bhd |

| 2004 | RM500 million (USD540 million) | The world’s first Sukuk issuance by a supranational agency, the International Finance Corporation |

| 2005 | RM2.5 billion | The world’s first Islamic Asset-Backed Securitization via Sukuk Musharakah by Musharakah One Capital Bhd |

| 2005 | RM2.05 billion (USD540 million) | The world’s first Islamic mortgage-backed securities (without recourse) by Cagamas MBS Bhd |

| 2006 | USD750 million | The world’s first Exchangeable Sukuk by Khazanah Nasional Bhd |

| 2007 | USD300 million | The world’s first Islamic US dollar subordinated debt using Ijarah principle by Malayan Banking Bhd |

| 2007 | RM8 billion (USD 2.4 billion) | The world’s first hybrid Sukuk by Malakoff Corporation Bhd |

| 2007 | RM15.4 billion (USD4.6 billion) | The world’s single largest corporate Sukuk by Binariang GSM Sdn. Bhd |

| 2007 | RM3.5 billion (USD1.06 billion) | The world’s first Sukuk program by a British-owned multinational company, Tesco Stores (M) Sdn. Bhd |

| 2007 | RM400 million (USD125 million) | The world’s first Sukuk program by a Japanese owned multinational company, AEON Credit Service (Malaysia) Bhd |

| 2008 | RM300 million (USD83 million) | The world’s first redeemable Sukuk Musharakah with warrants by WCT Engineering Bhd |

| 2008 | USD550 million | First exchangeable Sukuk to use Hong Kong listed shares by Khazanah Nasional Bhd |

| 2009 | RM20 billion (USD5.4 billion) | First innovative structure using Musharakah & Ijarah principles by Pengurusan Aset Air Bhd |

| 2009 | USD1.5 billion | The world’s first Emas Sukuk by Petroliam Nasional Bhd (Al-Ijarah Sukuk) |

| 2011 | USD2 billion | Malaysia’s first Wakala issue by the Government of Malaysia |

| 2012 | CNY500 million (USD160 million) | The first quasi sovereign issuance in renminbi by Khazanah Nasional Berhad |

| Source: Securities Commission Malaysia. www.sc.com.my, PWC Publication 2010, “Gateway to Asia: Malaysia, International Islamic Finance Hub,” CIMB-Principal Islamic Asset Management Sdn Bhd, CIMB Islamic Bank Bhd. The table is reproduced from: N. Kamso, “2011 Sukuk Growth-The Malaysian Experience,” in: ed. S. Jaffer, Global Growth, Opportunities and Challenges in the Sukuk Market (UK: Euromoney Books, 2011), 43–55. |

||

The Asian financial crisis of 1997 did not deter the country from ranking first in issuance in the global Sukuk industry. Though the crisis dampened the entire financial industry, including the Sukuk market, Malaysia emerged as a vibrant player only within four years of recovery. Since then issuers from other regions, notably Asia (Singapore, Indonesia, Japan), Europe (Turkey, Germany), and the Middle East (United Arab Emirates, Bahrain, and Saudi Arabia), have also made strides to deepen and widen the global Sukuk supply.

The Sukuk investment universe, though small compared to conventional fixed income, has now progressed to a point where investible asset classes of Sukuk funds are available to international investors. That said, investors are relatively unfamiliar with the diversification benefits of a Sukuk investment portfolio, which are made apparent by examining a global Sukuk index.

EXAMINING SUKUK INVESTMENT RESULTS

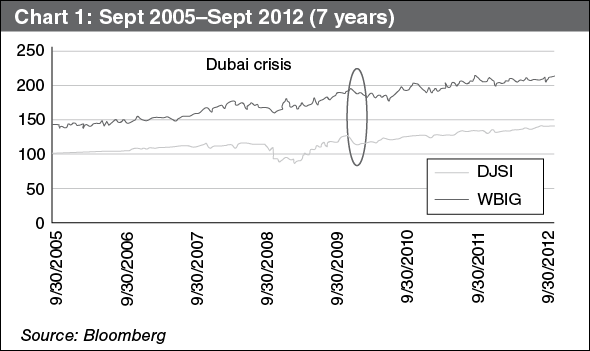

The Dow Jones Sukuk Index (DJSI), designed to measure the performance of global Sukuk, comprised merely seven constituents when it was first introduced in October 2005. At that time, the index lacked breadth and depth in comparison to the conventional bond index, the World Broad Investment Grade Bond Index (WBIG). The 2008 global financial crisis and 2009 Dubai debt crisis were the first real tests for Sukuk. The combined headwinds proved damaging to the nascent Sukuk market, and several issuances slumped to their lowest level during these crises. However, in spite of the challenges, or because of them, the Sukuk investment universe has staged a strong comeback since 2009, and has reestablished itself as a vibrant and attractive new asset class today. The DJSI has not only improved from the unimpressive performance of its 5 and 7 year returns, but it also went on to produce superior returns by outperforming the conventional index over a 2-year time period as at the end of September 2012. See Table 9.2.

Table 9.2 Annualized Returns of DJSI and WBIG

Repeat of the Dubai Debt Crisis Unlikely

With Dubai and state-controlled Dubai corporates being early entrants as issuers in the Sukuk market, Dubai’s 2009 crisis reverberated forcefully in the Sukuk space. With the onset of the global financial crisis that adversely affected economies everywhere, Dubai’s real estate market declined after a six-year boom. On November 24, 2009, state-controlled Dubai World rattled financial markets by announcing that it was seeking to delay payments on USD59 billion of debt.7 The collapse of the real estate market in Dubai severely affected the mortgage sector and hence, the broader Dubai economy. Uncertainties surrounding how the Sukuk securities would fare caused many global investors to flock to what they viewed as the comparative safety of conventional fixed income. See Figure 9.1.

However, investor fears in the 2009 Sukuk market proved to be unfounded. Dubai did not actually default on its public debt. In fact, Dubai received financial assistance from Abu Dhabi, the “patriarch” of the United Arab Emirates. In similar fashion to what investors had seen related to the global banking firms a year earlier, Abu Dhabi stepped in to support Dubai with a USD20 billion bailout.8 Following the extension of financial support to Dubai from Abu Dhabi, the government of Dubai made concerted efforts to strengthen its banking system by implementing a scoring system to evaluate individual borrowers’ creditworthiness. In addition, the Gulf Cooperation Council banks have made a variety of efforts to strengthen their balance sheets to protect against declines in loan recovery rates and asset prices. The banks’ tier 1 capital adequacy ratios have steadily increased over the last four years and were in the region of 15 percent at end-2011. More importantly, equity forms the bulk of the banks’ capital base, and their equity-to-assets ratios are high, ranging from 10 percent in Bahrain to 16 percent in Qatar.9

Global Sukuk Makes a High-Quality Recovery

The DJSI has recovered completely from the crisis. The index has matured with respect to both the quality and quantity of its constituents. This has led to markedly lower volatility, given the higher creditworthiness of the investment universe. The volatility of DJSI returns has fallen significantly to 2.08 percent for the 2-year period, compared to the 5 and 7 year periods of 10.13 percent and 8.58 percent, respectively. At 2.08 percent, the return volatility in the Sukuk space is less than half of that in the conventional space over the same period, which registered at 5.16 percent for the WBIG. This lower volatility is coupled with a tripling of the number of constituents in the index, meaning that a severe fluctuation of any one constituent has less singular effect on the overall index. See Table 9.3.

Table 9.3 Returns Volatility of DJSI and WBIG

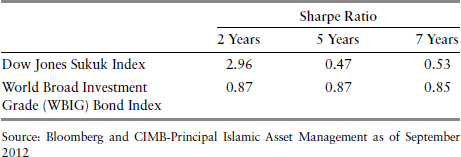

A further examination of the DJSI’s returns reveals a significant increase in the Sharpe ratio, a measure commonly used to better analyze performance by taking risk into consideration. A portfolio with a higher Sharpe ratio is considered to have exhibited better performance, as the Sharpe ratio measures how well the return of an asset compensates the investor for the risk taken. The Sharpe ratio for the DJSI is 2.96 over the most recent 2-year period, versus 0.47 and 0.53 over the 5 and 7 year periods, respectively. In contrast, the Sharpe ratio of the WBIG remained similar over the 2-, 5-, and 7-year periods at average of 0.86. Therefore, in examining the quality of the Sukuk index performance while considering both return and risk, we find that its superior performance is further enhanced with lower volatility and a higher Sharpe ratio. See Table 9.4.

Table 9.4 Sharpe Ratios of DJSI and WBIG

Sukuk Investing Offers an Enlarged Investment Universe

Unlike Shariah-compliant equity investing, which is a subset of global equity, Sukuk investing is unique in that it enlarges the existing conventional fixed-income investment universe to grant conservative investors attractive opportunities in a completely separate class of fixed-income assets. The number of constituents in the DJSI has tripled in two years, largely due to active participation by governments and corporations that have facilitated numerous Sukuk offerings. The number of constituents in DJSI has increased from 13 in June 2010 to 36 as of September 2012.10 In addition, the constituents of the DJSI have similar ratings to those of the WBIG. Both indices require a minimum quality of BBB- or Baa3 by the rating agencies.11 Moving forward, we anticipate that more issuers will participate in the Sukuk market. Today, Sukuk investors are seeing several first-time issuers come to issue in their market. For instance, the Republic of Turkey issued a USD750 million benchmark issuance in September with Citigroup and HSBC included as book runners. Further, following on the sovereign issuance, Turkey’s Sukuk market is gathering even more momentum as companies from the national airline to the biggest telephone operator plan Sukuk offerings.12

Sukuk Investing Offers Strong International Diversification

The performance of the DJSI has remained resilient despite political unrest in pockets of the Middle East. The stability of the index is a reflection of the geographical diversification it offers. The sovereign representation of Sukuk issuers in the DJSI leads with Malaysia, and is followed by Saudi Arabia, Qatar, and Indonesia.

Table 9.5 Percentage of Sovereign Debt in Dow Jones Sukuk Index

| COUNTRY | Percentage |

| Malaysia | 17.08% |

| Saudi Arabia | 16.21% |

| Qatar | 13.60% |

| Indonesia | 6.04% |

| Dubai | 5.53% |

| Abu Dhabi | 3.60% |

| TOTAL | 62.06 |

| Source: Bloomberg and CIMB-Principal Islamic Asset Management | |

In addition to the benefits of diversification, these jurisdictions have strong macroeconomic fundamentals and offer exposure to oil- and gas-related revenue streams, which offer deep reserves support to issuers. In addition, more than 60 percent of the investment universe of DJSI is composed of investment-grade Sukuk funds from countries, which may not register significantly, if at all, inside the conventional index.

Sukuk Investing Offers Shariah-Compliant Exposure to Financials

Investment exposure to the financial sector is considered a proxy for the growth of an economy since banking prospers with an economic expansion. However, the Shariah-compliant equity portfolio will typically filter out the financial sector, as they tend to be conventional banking and financial services entities. Shariah-sensitive investors who want exposure to the financial sector can still access the sector through the Sukuk asset class. Table 9.6 shows the sector weightings of both indices.

Table 9.6 WBIG and DJSI Sector Weightings

As shown in Table 9.5, financials constitute the second-largest sector of about 30 percent in the DJSI. This is also an investment opportunity for conventional investors who want to diversify the quality of their overall portfolio’s exposure to the financial sector, as they can gain exposure to Islamic banks such as QIB Sukuk Funding (Qatar), IDB Trust SVCS (Saudi Arabia), and Abu Dhabi Islamic Bank (UAE).

CASE STUDY: SUKUK INVESTING AS A DIVERSIFICATION STRATEGY

The benefits of diversification with Sukuk securities are not just theoretical, they are demonstrable. For example, one can examine the results of the following two scenarios to determine whether investing in Sukuk serves as a good diversification strategy without compromising investment returns:

For the two-year period ending September 28, 2012, the annualized returns of the second portfolio resulted in a slightly enhanced return of 4.88 percent, versus 4.52 percent in the first portfolio. In addition, the second portfolio’s Sharpe ratio was increased significantly to 1.14 versus 0.87. See Table 9.7.

Table 9.7 Two-Year Returns and Sharpe Ratios Improved with 20% Sukuk Allocation

| Annualized Returns | Sharpe Ratio | |

| Portfolio 1: 100% tracking the World Broad Investment Grade Bond Index | 4.52% | 0.87 |

| Portfolio 2: 20% tracking the Dow Jones Sukuk Index and 80% tracking the World Broad Investment Grade Broad Index | 4.88% | 1.14 |

| Source: Bloomberg and CIMB-Principal Islamic Asset Management Sdn Bhd as of September 2012 | ||

Given low-yield markets worldwide, a differential of 36 basis points in and of itself is not an insignificant improvement. Equally as important, the improvement in the Sharpe ratio shows that the strategy can generate alpha or additional returns that better compensate for risk.

CONCLUSION

As one can see, investment exposure to Sukuk assets can offer diversification benefits. In addition, Sukuk prices generally hold up well because they are often treated as a “buy and hold” investment. This grants an additional layer of insulation against volatility relative to conventional fixed incomes. With additional information and enhanced knowledge, investors are becoming more comfortable with Sukuk investing. One of the most convenient and easiest ways to access the Sukuk asset class is via a fund that invests in diversified portfolio of global investment-grade Sukuks such as the Al Hilal Global Sukuk Fund. Launched in early 2012, the Al Hilal Global Sukuk Fund has delivered a strong performance of 4.3 percent in only six months since its March debut. The fund invests in a diversified portfolio of Shariah-compliant Sukuks issued by sovereign, quasi-sovereign, and corporations and aims to generate regular income as well as capital appreciation. There are clear signs that the Sukuk market is maturing and spurring a growing interest in gaining investment exposure to the asset class. Over the two-year period, we found similar investment results with lower volatility, compared to the conventional fixed incomes. These similar investment results also showed a clear improvement in the Sharpe ratio over the conventional index. Closer examination of the Sukuk investment space revealed further diversification benefits for investors who have, until now, invested only in the traditional fixed-income space. From its ability to enlarge the total fixed-income investment universe to offering international diversification with credit quality and Shariah-compliant financial sector exposure, there is evidence that diversifying a portion of one’s overall investment portfolio to Sukuk investments away from traditional fixed income will show an improvement in the Sharpe ratio without diminishing investment returns.

NOTES

1. Humayon Dar, ed., “Goldman Sachs Milestone Global Sukuk,” in Global Islamic Finance Report 2012 (London: Edbiz Consulting, 2012), 99–104.

2. Securities Commission Malaysia (2012, August 2). “SC Scorecard: Robust fund raising activities in Q2 2012” www.sc.com.my/main.asp?Pageid=379&linkid=3138&yearno=2012&mod=paper.

3. “Global Islamic Finance Forum (GIFF),” prepared by KFH Research Ltd., in conjunction with the Global Islamic Finance Forum (GIFF), September 18–20, 2012. Kuala Lumpur, Malaysia.

4. Ibid.

5. Zawya Sukuk Quarterly Bulletin, Issue 11, 3Q11 (2011).

6. Bloomberg Professional Services Terminal as at end-2010.

7. Arif Sharif and Laura Cochrane, “Dubai World Seeks to Delay Debt Payments as Default Risk Soars.” Bloomberg (November 25, 2009). www.bloomberg.com/apps/news?pid=newsarchive&sid=aoFe12bwzZ2M

8. Liz Alderman, “After Crisis, Dubai Keeps Building, but Soberly.” New York Times (September 30, 2010). www.nytimes.com/2010/09/30/business/global/30dubai.html?pagewanted=all&_r=0

9. Standard Chartered Bank, “Middle East Credit Compendium 2012” (May 2, 2012).

10. S&P Dow Jones Indices, LLC.

11. “Citigroup Global Fixed Income Index Catalog—2012 Edition” (January 17, 2012), 17.

12. Ercan Ersoy and Alaa Shahine, “Sukuk Taking Flight as Airline Readies Debut Sale: Turkey Credit,” Bloomberg (October 3, 2012). www.bloomberg.com/news/2012-10-03/sukuk-taking-flight-as-airline-readies-debut-sale-turkey-credit.html

13. The verse is a call to use various contracts in financial transactions; every contract in Shariah is permissible unless it is proven otherwise, through explicit or implicit provision. The wider structure of the provision captures the full range of permissible instruments and products used in the investment.

General Reading

Dar, Humayon, Rizwan Rahman, Rizwan Malik, and Asim Kamal, Global Islamic Finance Report (GIFR). Edbiz Consulting, 2012.

Jaffer, Sohail, Islamic Wealth Management: A Catalyst for Global Change and Innovation. Euromoney Books, 2009.