CHAPTER 1

The Growth of Shariah Investments

Preparing the Next Generation

Permissibility is the original state.

INTRODUCTION

When I was a speaker at the Islamic Finance News (IFN) Europe Conference in London in June 2011, a young European participant asked, “Why would Japan join the bandwagon and issue Sukuk when it does not have a sizable Muslim population?” I explained that whilst Japan itself has ample liquidity, its involvement in Islamic finance is to show the world that the Japanese remain relevant and innovative and are able to grant value to investors with the latest investment trend. We have seen AEON Credit Services and Nomura Holdings issue Sukuk (Islamic bond) in 2007 and 2010, respectively, and Daiwa Asset listed its first Islamic ETF in Singapore in 2008.

What is being done by Japan is reflective of active market players envisioning that over the next 10 years, the landscape of institutions offering Islamic financial services, including banks, nonbanks and microfinance institutions, Takaful (insurance), Re-Takaful operators, and capital market players, will evolve into a full-fledged system of Islamic financial services that coexist effectively and efficiently with conventional financial institutions.

The rapid pace of economic growth and the accumulation of wealth in the Middle East and among the Muslim populations of the Far East are the catalysts that have driven and stimulated the developments in Islamic asset and wealth management. I have observed that the second and third generation of Muslim immigrants in the United States, the United Kingdom, and Europe care deeply about practicing Islam in all aspects of their lives, including their investments. In addition to Shariah compliance, this emerging demographic also demands similar investment performance to that of conventional investing. This growing group also wants the option of choosing from a wide range of Islamic investment solutions.

The idea of Islamic investing is gaining popularity as it also offers distinct risk management advantages. For example, several years ago Islamic funds were little affected by the scandal-afflicted companies such as Enron and WorldCom, as Shariah-compliant investment funds were prohibited under Shariah investing principles from holding these stocks given these companies’ highly leveraged balance sheets. The creation and improvement of international Islamic capital markets’ regulatory frameworks have contributed to an improvement of governance, which has increased international investors’ confidence.

In the wake of the 2007 U.S. credit crisis and subsequent global financial crisis in 2008, the Islamic financial system not only survived; it has also grown. The size of the Islamic financial services industry was USD 1.14 trillion of banking assets as of 2010, a 78 percent increase over 2007.1 What helped Islamic banking and finance during the financial crisis was the absence of exposure of derivatives, which ruined the balance sheets of most conventional banks. A situation like American Insurance Group (AIG), which had an unsustainably highly leveraged balance sheet due to high-risk debt instruments, is not likely to occur in Islamic finance. While many hedge funds and other financial instruments took significant risks and fell hard in the late 2000s, the Islamic finance, in many cases, remained conservative and generic in its product offerings and investments and as a result, became one of the fastest-growing segments in the global financial service sector.

The viability of Islamic finance is derived from its capability to meet the changing demand of the capital market. It is worth noting that the McKinsey Islamic World Conference 2008–2009 report highlighted that among the high-net-worth individuals, between 10 and 20 percent were ready to sacrifice investment return for Shariah compliance, thus providing a reasonable market demand to drive the development and expansion of Shariah-compliant investment products and solutions.

THE GLOBAL ISLAMIC FUNDS INDUSTRY: WHERE IS IT NOW?

Islamic finance is gaining importance in asset and wealth management. As of 2011, according to the data from the Global Islamic Finance Forum magazine, there are more than 700 Islamic investment funds managing total assets under management of USD60 billion to USD65 billion.2 These funds are dominated by equity funds, followed by money market funds.

Islamic investment funds are being offered by emerging asset management companies to meet the changing appetite of the investors. While equity funds remain most popular, Sukuk, money market, commodities trading, and real estate are also catching up. The available selection of Islamic funds has evolved from being domestically invested to being diversified regionally and internationally. Investors’ growing interest, added to the availability of diversified offerings across various asset classes, are no doubt creating choices for all investors, Muslim and non-Muslim. Currently, a broad spectrum of asset classes—including equity, Sukuk, real estate, commodities, leasing, trade finance, private equity, and hedge funds—are available. The number of global asset management companies offering a broad range of Shariah-compliant investment funds across the world demonstrates the increasing diversity of players. These companies are headquartered in the strategic Islamic finance hubs of Malaysia, Saudi Arabia, Kuwait, United Arab Emirates, Bahrain, and United Kingdom.

During its infancy stage from 2003 to 2009, the global Islamic funds industry produced a commendable annualized growth rate of 25 percent.

Examining the trend of new launches over the last 10 years, there are two key inflection points. The first inflection point in 2002 saw the beginning of a five-year growth trend in the number of new fund launches which peaked in 2007. In 2008, the trend reversed sharply, with investors prioritizing capital preservation and fleeing the markets, bringing demand for new funds to a halt. There was healthy industry attrition and consolidation as asset management companies had to rationalize their range of offerings with the impact of the global financial crisis. Therefore, the year 2010 saw 23 fund closures, followed by 46 fund launches.3 Slow growth of 3.5 percent in 2011 has not deterred the establishment of new asset classes.4

A decade ago, investors who wanted to invest in Islamic funds had to turn to established markets with strong domestic market demand for Islamic investments, like Saudi Arabia and Malaysia. In 2011, Saudi Arabia led with a 33.2 percent market share of funds offered, followed by Malaysia, which domiciled 21.8 percent of funds (see Table 1.1). However, there is more asset class diversity in Malaysia versus other countries. Observing the rapid growth of new funds from 2002 to 2006, new market participants from different countries rallied to enter the industry to drive the establishment of the 180 new funds in 2007.

Table 1.1 Islamic Funds by Country (2011)

| Fund Manager Country | Percentage (%) |

| Saudi Arabia | 33.2 |

| Malaysia | 21.8 |

| Kuwait | 7.1 |

| United States | 6.4 |

| Cayman Islands | 5.5 |

| Luxembourg | 3.5 |

| Ireland | 3.3 |

| Jersey | 2.9 |

| Bahrain | 2.6 |

| Indonesia | 2.4 |

| Others | 11.3 |

| 100.00 | |

| Source: Global Islamic Finance Forum magazine (2012) | |

Malaysia and Saudi Arabia were pioneers in the development of Islamic funds. The world’s first Islamic fund, LembagaTabung Haji or The Pilgrims Fund, was created in 1963 by the Malaysian government to help Muslims save for their pilgrimage to Mecca. The first designated Shariah-compliant fund in Saudi Arabia was the Al-Ahli International Trade Fund, launched by National Commercial Bank in 1987. At their inception, the primary goal of these funds was to provide equities that comply with Shariah principles.

Since then, Shariah-complaint funds have demonstrated their perseverance by diversifying into various asset classes. In 2011, Malaysia and Saudi Arabia had a combined 55 percent market share, totaling USD26.8 billion out of almost USD60 billion in assets under management (see Table 1.1), but Islamic funds are also available on global platforms like Luxembourg, Ireland, and the Cayman Islands. Although funds registered in the Cayman Islands are largely distributed in the Middle East through Bahrain, funds registered in Luxembourg and Dublin are largely distributed by global banks in the respective jurisdictions, and they are also in compliance with Undertakings for Collective Investment in Transferable Securities (UCITS). This demonstrates that Shariah-complaint funds have evolved to meet the demands of sophisticated international investors, especially those from the United Kingdom and other parts of Europe. Due to these platforms’ robust risk framework, investors have a “window” with which to monitor the track records of these funds in Luxembourg and Dublin before deciding to invest.

As of 2011, the Cayman Islands offered 5.5 percent of the total universe of Islamic funds, and Luxembourg offered 3.5 percent, followed by 3.3 percent in Dublin, Ireland. The popularity of these Islamic investment funds in Luxembourg and Dublin has been spurred by sophisticated global investment managers who already have a sufficient track record on specific asset class capabilities in the conventional space.

UCITS are synonymous with strong capability and wider scope. Any Islamic investment fund established as a UCITS vehicle would have adhered to two of its important guidelines: namely, risk diversification and liquidity. UCITS funds are heavily regulated, ensuring effective and uniform investor protection. Global UCITS fund platforms are structured to appeal to international investors, given the robust risk framework and strict governance. The UCITS structure is flexible enough that it can be offered in multiple asset classes and multiple currencies to a broader investor base. As such, it can more easily build scale internationally and not be limited to the domestic sandbox. Such platforms are popular in the conventional space, and Shariah asset managers would do well to take full advantage to structure these types of funds and utilize them to service the integrated world.

In essence, an UCITS-compliant fund is regarded as a European passport whereby if a fund is authorized in one European Union (EU) member state, the fund can be distributed in any other EU member state without any additional authorization.5

Table 1.2 above shows that equity Islamic funds lead in terms of assets under management, contributing to 46.9 percent of the total Islamic funds universe. Over the years, investors’ appetites have tended to favor Islamic equity funds when compared to the rest of the asset classes launched. This might be related to the fact that investors know that equity investing potentially generates higher return than fixed income. It is worth noting that Islamic equity investing avoids indulging in excessively risky and high-debt company stocks, leading to reduced volatility. Since money market and commodities fund are generally more stable in an uncertain market, there has been an increase in the number of funds launched since 2007. It must also be noted here that although the Sukuk market represents 5.8 percent of the funds asset class, it is currently the most visible Islamic finance instrument to various global investors.

Table 1.2 Funds by Asset Class

| MANDATE | Percentage Contribution | Amount USD (Billion) |

| Equity | 46.9 | 28.14 |

| Money markets | 22.2 | 13.3 |

| Mixed assets | 11.8 | 7.0 |

| Real estate | 9.0 | 5.4 |

| Sukuk | 5.8 | 3.4 |

| Commodities | 3.4 | 2.04 |

| Others | 0.9 | 0.54 |

| Trade finance | 0.1 | 0.060 |

| Structured products/ Hedge funds | 0.1 | 0.060 |

| TOTAL | 100 | 60 |

| Source: Global Islamic Finance Forum magazine (2012) | ||

Analysis of these global developments of Islamic funds industry and fund managers showed that 67 percent of the funds are invested in Asia Pacific and Middle East/Africa. Considering that investors were initially based in Asia-Pacific, the Middle East, and Africa, it makes commercial sense that these funds are invested in their backyards, the markets they are most familiar with.

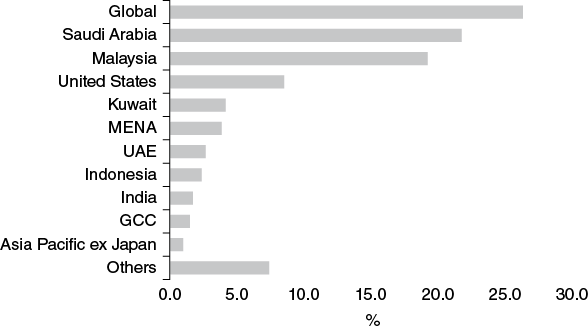

Figure 1.1 shows where the funds were geographically invested. Global funds contributed a maximum weightage of 26.3 percent. Saudi Arabia is second with 21.8 percent, followed by 19.2 percent concentration in Malaysia; almost a majority of the funds raised in these two regions are distributed locally.

Figure 1.1 Funds by investment geography (2011)

Source: Global Islamic Finance Forum magazine (2012)

Generally, the popularity of the investment locations has to do with where the funds were launched. For instance, Malaysia launched numerous Asia-Pacific investment funds because Malaysia is part of the Asia-Pacific region, and the fund managers and investors there were more familiar with the investments. Likewise, Saudi Arabia and Kuwait were more likely to have launched Middle East funds as they are more comfortable with investing close to where they are.

There is a gradual growth trend in the emerging market investment. Emerging market strategy first appeared in 2006, and two funds were each launched in 2006 and 2007. One of the notable emerging market products is the iShares UCITS-compliant MSCI emerging market Islamic ETF. It was listed in December 2007. The existing net total assets are a respectable USD28.8 million as of November 2012.6

GLOBAL PRODUCT INNOVATION OF ISLAMIC INVESTMENT PRODUCTS

Islamic investment funds started much later, in the early 1990s. Although the evolution of Islamic financial markets started 30 years earlier, Islamic investment funds growth has been phenomenal since 2000. The evolution was influenced by investors from Europe and the United States, as well as the global offshore market. Sophisticated products—namely, private equity and Islamic REITs, hedge funds, derivatives, Islamic asset-backed securities, and global Islamic bonds—are all being added. As a result, new institutions such as Islamic investment banks have joined the club in offering Islamic funds.7

Islamic funds have evolved into the wealth management space to cater to investors who want market exposure in conjunction with ethical, responsible investing. Investors can obviously benefit from the broad spectrum of Islamic funds.

Islamic investment products have progressed over the period from 1990 to 2005. Beginning in 1990, investment products were largely equity and Murabaha funds. Islamic investment products now include a wide spectrum of funds, ranging from generic funds to even hedge funds. There was an inflection point from year 2005 onward where there was an active influx of new funds (see Table 1.3).

Table 1.3 Range of Global Islamic Investment Products

| 2005 and Onward |

| Equity funds Murabaha funds Ijarah funds Lifestyle funds Balanced funds Sukuk funds Private equity funds Real estate funds Commodity funds Funds of funds Hedge funds Index funds Structured products Listed REITs Exchange-traded funds (ETFs) |

| Source: International Organization of Securities Commission (IOSCO)’s Islamic Capital Market Task Force Report 2004 and CIMB Islamic Research |

PROGNOSIS FOR ISLAMIC FINANCIAL MARKETS: WHERE ARE THEY GOING?

The global market for Islamic banking assets was valued at USD1.357 trillion at the end of 2011. That year also saw tremendous growth in one of the asset classes, which contributed to further progress in the Islamic banking and financial services in an otherwise depressed environment for financial services. Sukuk saw a 77 percent growth totaling USD85.0 billion in issuance. The growth in global Islamic banking and services industry was 16.04 percent. One potential scenario shows global Islamic banking assets with commercial banks to reach USD1.8 trillion in 2013, representing an average annual growth of 17 percent.8

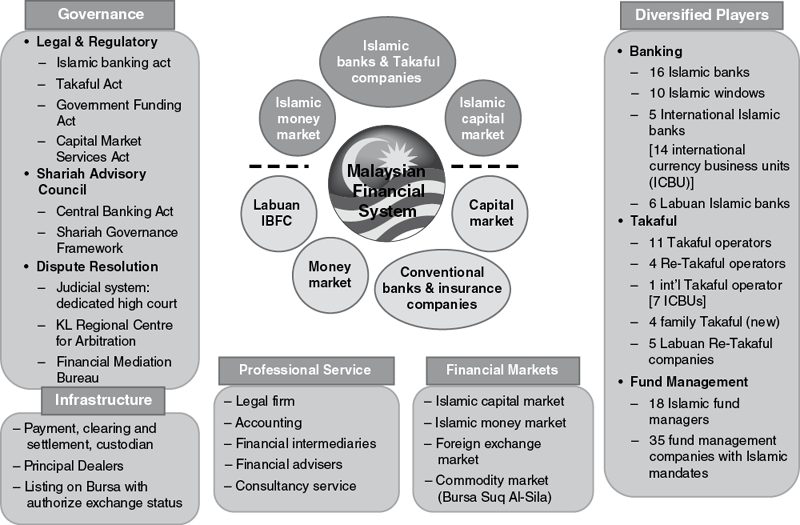

It is believed that Malaysia not only continues to dominate the Sukuk market but also intends to lead the internalization of Islamic finance so that it can grow into the largest marketplace. Malaysia’s proclaimed vision and facilitative legal framework has attracted companies from countries that are assessing the viability of Islamic finance. It has continued to raise the bar with landmark issuances and developments over the last three years. To achieve its aspiration to be a hub for global Islamic finance, Malaysia has established a comprehensive value chain of market players supported by services providers in a comprehensive legal and regulatory framework, as shown by Figure 1.2.

As the previous framework lays out, there is no doubt that Malaysia is at the forefront of the industry and continues to raise the bar with landmark issuances and developments taking place the last three years. It is an industry leader in structuring Islamic funds when compared to other countries.

Other key clusters of countries—namely, the Middle East and South East Asia—are actively developing the Islamic investment funds business as one of their organizational goals. Other jurisdictions are clearly joining the bandwagon to take advantage of their benefits. Islamic funds will be a fundamental tool to capture the wealth of opportunity. Rampant development of knowledge and soft skills will be optimized. Talents will be deployed to ensure that the backroom, system integration, prime broker, custodian, and trustees are aligned to Islamic principles. Progress of product development will deepen into Islamic ETFs, structured products, and hedge funds. Asset securitization is promising because current market operations are restricted by the dearth of liquidity in enhancing products—hence, the small Islamic secondary markets currently lack depth and breadth. A favorable tax regime will be introduced to address this.

Islamic investment funds are expected to grow at a considerable rate due to the fact that global middle-class investors are looking for alternatives to generate higher return combined with responsible investment. The Islamic banking sector is projected to grow at a compound annual growth rate (CAGR) of 21.1 percent until 2020. This was the same projection used from 2007 to 2011.9 Figure 1.3 illustrates the projected global Islamic banking assets growth until 2020.

Figure 1.3 Global Islamic banking assets growth trends

Source: Global Islamic Finance Forum magazine (2012)

In a dynamic industry, the global Islamic funds market is trending upward. It is notable that this is spanning beyond the “captive” market of the sizable global Muslim population. Others are being drawn to the ethics and principles that form the basis of these funds.

The conducive regulatory environment and the size of market in the Middle East/North Africa is expected to support the rapid growth. New investment firms are established each year, and the funds in this region have increased fivefold in less than 10 years. Although most managers handle few mutual funds, some institutional mandates and some discretionary portfolios, banks in Abu Dhabi, Kuwait, and Saudi have started to separate their investment banking from commercial banking. From the standpoint of progress in distributing investment products, the international fund managers offer offshore funds in the Middle East by using Bahrain, UAE, and Qatar as a distribution platform.

Today, there is greater focus on Saudi Arabia, which has the longest-standing record of foreign–local teamwork, than in previous years. New licenses have allowed more foreign banks to tie with local Saudi financial institutions, notably Morgan Stanley Saudi Arabia and Credit Suisse/Saudi Swiss Securities, Merrill Lynch Saudi Arabia, HSBC-Saudi British Bank/Al Amana, and Citibank-Saudi American Bank. JP Morgan is licensed in Saudi Arabia under its own name. Deutsche Bank has both a local venture and a license under its own name.

The market players are keen to squash the feeling that Shariah is a retail story and that petrodollars do not care about whether a fund is Shariah compliant. They are intent on meeting investor demand and providing the requested diversity. Many international institutions already provide distinct Shariah-compliant businesses (e.g., HSBC Amanah, Citi Islamic and BNP Paribas Investment Partners).

There is growing interest in Asia’s growth potential. Middle Eastern investors are eyeing opportunities in emerging markets, particularly India, China, and Pakistan. Despite being perceived as “new kids on the block,” most experts believe it wouldn’t be too difficult for both Singapore and Hong Kong to establish themselves as Islamic wealth centers due to their long association as financial hubs in Asia. All they need to do right now is to get the necessary infrastructure and regulation, followed by a jump start into the sector, and then build critical mass based on their Islamic finance expertise. Case-in-point: Hong Kong Airport Authority has expressed an interest in taking the lead in issuing its first Islamic bonds of up to USD 1.0 billion in 2013.10 Hong Kong can even provide a getaway for investors interested in mainland China (especially Gulf Cooperation Council investors) by constructing Shariah-compliant products with underlying Chinese assets. While Indonesia and Japan are not forgotten, Malaysia is still most favored.

The United Kingdom is now the leading center for Islamic finance outside the Gulf Confederation Council and Malaysia. The United Kingdom seems poised to establish and maintain London as Europe’s gateway to international Islamic finance.

CONCLUSION

Saudi Arabia and Malaysia have been quick to capitalize on the emerging sector of Islamic financial instruments, and are now jointly recognized as world leaders in Islamic finance development. These countries played a crucial role in upgrading awareness, first on Islamic finance itself and consequently on Islamic asset management. While these two nations have led the charge toward the growth of the sector, other countries are following suit.

Today in the Asia Pacific, the Islamic asset management industry has grown immensely in many countries, including Malaysia, Brunei, Singapore, Japan, South Korea, China, and Indonesia.

Demand-driven results speak for themselves. Global investment houses today continue to aggressively develop products to provide for investors of all levels with varying needs. Boutique investment companies are also becoming an increasingly popular business model for global houses, to capture their share of the market in different countries.

Demand for product diversification has never been stronger, as institutional fund managers are heeding the call from clients to provide new investment exposures in their portfolios. As such, the number of Islamic asset managers and the amount of total assets under management has multiplied tremendously. This is most welcome in the industry, as it helps to promote new talent, better product quality, and greater competition.

As Islamic asset management continues to spread over multiple geographical regions and across new customer classes, it is only a matter of time before Islamic asset management stands head-to-head with conventional investing. In the Asia Pacific ex-Japan region, the industry is burgeoning in a dynamic, prohibited manner, with growing awareness and investor acceptance around the world. This is also the region with the greatest number of Shariah-compliant investment opportunities.

The amount of products and instruments available in the market makes the investor spoilt for choice. The future development of Islamic asset management in the region is supported by various factors—an overall positive growth in its component economies, growing population, and increasing wealth and increasing government support for the industry.

The Shariah-compliant investing approach has been proven to investors. This approach is able to form a balanced portfolio while reducing disparities and offering a socially and morally conscious alternative—thereby making it a valid and irresistible investment choice.

NOTES

1. “The Global Islamic Financial Services Industry,” in Global Islamic Finance Report 2011, 35.

2. KFH Research Ltd. and the Global Islamic Finance Forum (GIFF). “Global Islamic Finance Forum (GIFF).” Kuala Lumpur, Malaysia: September 18–20, 2012.

3. Ernst & Young, 5th Edition Islamic Funds and Investment Report (IFIR 2011): Achieving Growth in Challenging Times, 2011.

4. KFH Research Ltd. and the Global Islamic Finance Forum (GIFF). “Global Islamic Finance Forum (GIFF).” Kuala Lumpur, Malaysia: September 18–20, 2012.

5. Tony Goh. “The Next Frontier” Smart Investor, 264 (April 2012): 14–17.

6. “iShares MSCI Emerging Markets Islamic” Factsheet. iShares by Blackrock, November 2012.

7. International Organization of Securities Commission (IOSCO) Islamic Capital Market Task Force Report 2004.

8. IMF, The Banker, Central Bank Reports, and EY Universe, The World Islamic Banking Competitiveness Report 2012–2013.

9. KFH Research Ltd. and the Global Islamic Finance Forum (GIFF). “Global Islamic Finance Forum (GIFF).” Kuala Lumpur, Malaysia: September 18–20, 2012.

10. Bernardo Vizcaino. “Hong Kong’s sukuk bill on track but local interest dim.” Reuters, 2012. http://www.reuters.com/article/2012/11/14/islamic-finance-sukuk-idUSL5E8LU7Y920121114

11. For further explanations please refer to the Glossary of Quotations.

12. The legal maxim indicates that everything is permissible unless it is proven otherwise by Shariah; hence it is permissible to grow business and expand Islamic asset management provided that the motivating factors for the growth are Shariah compliant and driven by values and principles of Shariah.

General Reading

Ernst & Young. The World Islamic Banking Competitiveness Report, Growing Beyond: DNA of Successful Transformation (Report 2012–2013), December 2012.

Jaffer, Sohail. Islamic Asset Management: Forming the Future of Shariah Complaint Investment Strategies. Euromoney Books, 2004.

Jaffer, Sohail. Islamic Wealth Management: A Catalyst for Global Change and Innovation. Euromoney Books, 2009.