12

Supply of Money

After studying this topic, you should be able to understand

- In India, the RBI publishes data on the alternative measures of money supply.

- In fractional reserve banking system, banks utilize some of their deposits for making loans and keep some as reserves for withdrawals by the depositors.

- High-powered money is money produced by the government and the central bank and held in the hands of the public and the banks.

- The lending and the borrowing activities of the commercial banks lead to credit creation.

INTRODUCTION

As already discussed in the previous chapter, there is no single definition of what constitutes money in any economy. But the problem is that money is a very important variable and, hence, cannot be just ignored. In this chapter, we discuss the theory of money supply or what is often called the H theory of money supply. We also examine the measures of money supply in India. We will discuss in detail that the money supply in an economy is determined not only by the monetary authorities but also by the banking system through the creation of credit.

MEASURES OF MONEY SUPPLY IN INDIA

Before we embark on the measures of money supply, it is imperative to make certain important observations regarding money:

- The supply of money is a stock variable (as compared to, say income which is a flow variable) and refers to the stock of money at a point in time.

- When we measure the supply of money, it is the money in the hands of the ‘public’, by which we mean the households, firms and institutions (like the non-bank financial institutions). The government (including the Central and the State governments) and the banking system are not a part of the ‘public’, and are in fact the producers of money. The Central Bank and all banks that accept demand deposits form a part of the banking system.

As the measurement of money may differ from country to country, we here analyse the different measures of money supply published by the Reserve Bank of India, the RBI.

Until the year 1967–68, the RBI used to publish data only on what is called the narrow measure of money supply. As this definition laid emphasis on the medium of exchange function of money, only currency and demand deposit held by the public were included in the narrow measure of money supply.

From the year 1967–68, RBI started publishing data on the broader measure of money supply in addition to the earlier narrow measure. This is also known as ‘aggregate monetary resources’ or the AMR. The AMR is based on the liquidity approach, which emphasizes the store of value function of money. Hence, the AMR includes the time deposits of commercial banks held by the public, in addition to currency and demand deposits.

The RBI publishes data on the following four alternative measures of money supply:

| M1 = | C + DD + OD | |

| M2 = | M1 + Saving Deposits with Post Offices | |

| M3 = | M1 + Net Time Deposits of Banks | |

| M4 = | M3 + Total Deposits with Post Office Savings Organization (including NSC) | |

| where, | C = | Currency |

| DD = | Demand deposits of banks | |

| OD = | Other deposits of the RBI | |

| NSC = | National saving certificates |

Before analysing the above measures of money supply, it is necessary to throw some light on the different components included in the measures of money supply. They are:

Currency: Currency includes both the coins and paper notes, though paper notes are the more predominant of the two. Coins and one rupee notes are issued by the Government of India whereas the currency notes of rupees two and higher denominations (including rupees five, ten, twenty, fifty, hundred, five hundred and thousand notes) are issued by the RBI. However, all the currency is put into circulation by the RBI.

Currency includes both the coins and paper notes, though paper notes are the more predominant of the two.

Demand deposits of banks: These are current account deposits, which are payable on demand either by cheque (with no restrictions) or otherwise. There is no interest payment on these deposits, which are generally held by the business firms for their transactions. However, the banks do provide various kinds of services to their account holders. Hence, they serve as a medium of exchange and are therefore included under the narrow definition of money side by side with currency.

Demand deposits of banks are current account deposits, which are payable on demand either by cheque (with no restrictions) or otherwise.

Time deposits of banks: These are fixed term deposits where the term of the deposit may vary. Unlike demand deposits, time deposits are not payable on demand. Also, cheques cannot be issued against them. They are interest earning deposits where the interest rises as the term of the deposit increases. They can be withdrawn before the maturity period but only with a loss of interest.

Time deposits of banks are fixed term deposits where the term of the deposit may vary and, in addition, they are not payable on demand.

Savings account deposits: These combine features of both the demand deposits and the time deposits. Like demand deposits, they are payable on demand and withdrawable by cheques, though the chequing facilities are limited. Like time deposits, they earn an interest. Because of these very characteristics that they possess, saving deposits are held only by households for their short term savings. Business firms cannot hold a savings account.

Savings account deposits are payable on demand and withdrawable by cheques, though the chequing facilities are limited and in addition they earn an interest.

Time deposits with post offices: These include recurring deposits and cumulative time deposits. The depositor makes a regular deposit of a fixed sum for over a certain time period.

Saving deposits with post offices: These are deposits with the post offices, which are withdrawable on demand though that can only be done by withdrawal slips on which there are restrictions and also limits. Hence, the encashability of these deposits is very restricted and therefore they do not serve as a medium of exchange.

Other deposits of the RBI: These are deposits of the RBI other than those held by the government (both the Central and the State governments) and the banks. These deposits include demand deposits of quasi government institutions, IMF, World Bank, foreign central banks and governments, and others. As these other deposits form a very small proportion of the total money supply, they are often ignored.

National Saving Certificates (NSC): NSC is a tax saving instrument available at all post offices in India. It is a saving instrument for purposes of investing long-term savings. It is a combination of both high safety and adequate returns. It is also often used by the middle class families in India for saving on their tax. NSCs are available in denominations of Rs. 100, Rs. 500, Rs. 1000, Rs. 5000 and Rs. 10,000. There are no maximum limits on the purchase of the NSCs.

National saving certificates is a tax saving instrument for purposes of investing long-term savings available at all post offices in India being a combination of both high safety and adequate returns.

A look at the new series by the RBI brings us to certain conclusions:

- What we call M1 in the new series is actually the old M or what we called the narrow measure of money supply. The only difference between the two is that the new series includes into the picture the net demand deposits of state co-operative banks, central co-operative banks and a part of primary co-operative banks.

- What we call M3 in the new series is actually the AMR or what we called the broad measure of money supply. The only difference between the two is that the new series gives a better treatment to the co-operative banking sector.

- In the new series, M2 and M4 aim at including into the picture the post office deposits. M2 includes only the saving deposits with post offices whereas M4 includes total (saving and time) deposits with post offices.

- It is interesting to note that in the new series, the four measures of money supply are in descending order of liquidity with M having the highest liquidity and M4 having the lowest liquidity.

The RBI publishes data on all the four measures of money supply as they all are useful for purposes of monetary policy.

RECAP

- When we measure the supply of money, it is the money in the hands of the ‘public’.

- The new series on the four measures of money is in descending order of liquidity.

THE THEORY OF MONEY SUPPLY

We have assumed till now that the supply of money in any economy is policy determined. But, actually, the supply of money is determined not only by the monetary authorities but also the public and the banks that play an important, if not the major, role in the determination of the supply of money. To simplify the analysis, we assume that there exists a fractional reserve system.

In a hundred per cent reserve banking system (which is just a theoretical concept), banks do not make any loans; in a fractional reserve banking system, banks utilize some of their deposits for making loans on which they charge an interest and keep some as reserves for withdrawals by the depositors. This system is based on the presumption that not all the depositors come at the same time to withdraw their deposits and also in case there are outflows there are inflows also. Hence, a bank needs to keep aside only a fraction of the total deposits as reserves and it gives out the rest in the form of loans.

To understand the theory of money supply (also called the H theory of money supply or the money multiplier theory of money supply), it is imperative to understand the difference between money and what we call high-powered money (or the monetary base).

We can define money by using the narrow definition of money as

In the US, the money supply is measured as four categories in ascending order M0, M1, M2 and M3. M0 represents base money and includes coins, bills and deposits of the central bank whereas M3 represents all the different forms of money, including credit. In the US, the Federal Reserve is responsible for controlling the money supply, in Japan it is the Bank of Japan, in China the People’s Bank of China and in UK the Bank of England are the central banks of the respective countries.

| where, | M | = Money |

| C | = Currency | |

| DD | = Demand deposits of banks |

High-powered money is the money, which is produced by the government and the central bank and held in the hands of the public and the banks. It can be defined as:

| where, | H | = High-powered money |

| C | = Currency held by the public | |

| R | = Cash reserves held by banks |

High-powered money is the money, which is produced by the government and the central bank and held in the hands of the public and the banks. It can be defined as H = C + R.

(We are not including OD, other deposits of the central bank in our analysis as they are a very small proportion of the total money supply.)

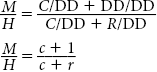

A comparison of the above two equations, Eqs. (1) and (2), reveals that currency (C) is common to both the equations, the difference is due to the presence of DD in the equation of money and that of R in the equation of high-powered money. This difference is of great importance in the theory of money supply. DD are created by the banks. But to be able to create them, banks have to maintain an R. In fact in a fractional reserve system, DD are a certain multiple of R. It is this, which gives H a quality of high power, because of which it serves as the basis for the creation of demand deposits.

Dividing Eqs. (1) by (2), we get

Dividing both the numerator and the denominator of the above equation on the right hand side by DD, we get

M = mH

where,

![]() is the money multiplier

is the money multiplier![]() is the currency demand deposit ratio

is the currency demand deposit ratio![]() is the reserve deposit ratio

is the reserve deposit ratio

Currency deposit ratio: It is the currency held by the public as a fraction of their demand deposits. Both the currency and the demand deposits are a function of the income level and the rate of interest. Hence, they are highly correlated. The currency deposit ratio is determined by the payment practices of the public, and the cost and convenience with which cash can be made available. In addition, this ratio is affected to a large extent by the seasonal patterns; for example, in India it is highest around the Diwali festival.

Currency deposit ratio is the currency held by the public as a fraction of their demand deposits.

Reserve deposit ratio: It is the reserves held by the banks as a fraction of their deposits. (As here D = DD, the reserves will be a fraction of demand deposits.)These reserves of the banks are usually divided under two headings which are as follows:

Reserve deposit ratio is the reserves held by the banks as a fraction of their deposits.

- Required reserves: These are those reserves, which every bank is statutorily required to hold. They are also called the Cash Reserve Ratio (CRR).

- Excess reserves: These are reserves in excess of the required reserves. Banks hold them voluntarily as ‘cash on hand’ or ‘vault cash’ for purposes of meeting currency drains and clearing drains. As these reserves do not earn any interest banks, try to minimize them.

Introduction of Time Deposits: A Broader View

Until now we have only included demand deposits in our analysis, while in practice time deposits are also very important. Hence, we define

D = DD + TD

where,

TD = time deposits

t = ![]() is the time deposit ratio

is the time deposit ratio

Time deposit ratio This is the ratio of time deposits to demand deposit. The division between these two deposits is a decision, which is made by the public depending on the terms and conditions offered by the banks on the two deposits.

Time deposit ratio is the ratio of time deposits to demand deposit.

| We have | D | = DD + TD |

| Thus, | R | = r (DD + TD) |

| = r (DD + t DD) | ||

| = r (1 + t) DD |

We have Eq. (3) as,

Substituting for R, we get

Dividing both the numerator and the denominator of the above Eq. (4) on the right-hand side by DD, we get

BOX 12.2

In the UK, the behaviour of the money multiplier has undergone a spectacular change in the recent years. During the period 1870–1970, it was quite stable and fluctuated within very narrow limits. However, from the 1970s, the magnitude of the money multiplier has more than doubled.

We get the final equation of the H theory of money supply as

We can put it in the form M = mH

where,

This is the money multiplier equation when time deposits are included in the analysis.

We can put it in the form M = m (c, t, r) H.

The above equation shows that the determinants of money supply can be grouped under the following two headings:

Those That Influence The High-Powered Money, H

It is important to realize that the changes in H are mainly controlled through policies and determined by the public and the banks.

As already discussed, H or high-powered money is the money which is produced by the monetary authorities and held by the public and the banks. In India, the central government and the RBI constitute the monetary authorities. Thus money produced by the government, or government currency and money produced by the RBI, or Reserve Bank money constitute the supply of high-powered money. Among the two, government currency and reserve bank money, the more important component of high-powered money is the latter, namely, Reserve Bank money. Hence, the changes in the Reserve Bank money (RBM) are largely responsible for the changes in high-powered money.

Changes in the RBM occur due to changes in the following factors:

- Net reserve bank credit to the government

- Reserve Bank credit to banks

- Reserve Bank credit to development banks

- Net foreign exchange assets of the Reserve Bank

- Net non-monetary liabilities of the Reserve Bank

Of the above, an increase in the first four factors leads to an increase in the RBM whereas an increase in the last factor will lead to a decrease in the RBM.

Those That Influence The Money Multiplier, m

The changes in ‘m’ are mainly endogenous as c, t and r all are behavioural ratios.

The determinants of the money multiplier can be divided under two heads:

- The proximate determinants of the money multiplier include the behavioural ratios c, t and r.

In general, there will occur an increase in the money multiplier and hence the money supply when:

- there is a decrease in the c, currency deposit ratio. This means that if the public prefers to hold a smaller proportion of H in the form of currency and a larger proportion as deposits, then the banks will be able to hold more in the form of reserves and hence they will be able to create more money.

- there is a decrease in the r, reserve deposit ratio. This implies that with a lower reserve deposit ratio, the ability of the banks to extend credit increases and hence they will be able to create more money.

- there is a decrease in t, time deposit to demand deposit ratio.

- The ultimate determinants of the money multiplier include those factors, which influence the proximate determinants of the money multiplier. They are as follows:

- As far as the c and t ratios are concerned, they are determined by the public’s preferences between currency, demand deposits and time deposits. These factors further depend on the income level, the interest rate, development of the banking system, payments habit of the public and many more factors.

- As far as the r ratio is concerned, while the fixation of the cash reserve ratio is a policy decision at the behest of the central bank, the maintenance of excess reserves is an internal decision made by the banks themselves.

The Money Multiplier Process

A discussion relating to the H theory would be incomplete if the actual money multiplier process is not discussed in detail.

Here we discuss as to how a given increase in H leads, over time, to a multiple expansion in bank credit and in the supply of money in the economy.

To analyse the process, some assumptions are necessary, which are as follows:

- The only type of deposits with the banks are demand deposits, i.e., D = DD.

- Commercial banks assets take the form of loans and advances only.

- The c ratio is 0.5 whereas the r ratio is 0.1 (where the r ratio includes both the required reserve ratio and the excess reserve ratio).

- At the going rate of interest, there is a large demand for bank loans.

- There exists a fractional reserve system because of which banks have to maintain only a fraction of its total deposits as cash reserves while the rest can be used for making loans.

Suppose that the government purchases goods worth Rs 600 crores from the public. The payment is made through cheques drawn on the RBI. The public on receipt of the cheques deposits them with their banks, who after the collection, credit the accounts of the depositors. Hence, there is an increase in the deposits of the public as also in the reserves of the banks of an amount of Rs 600 crores. The public withdraws Rs 200 crores as currency (the c ratio is 0.5) and leaves the rest with the banks whose reserves go up by Rs 400 crores. These new reserves are known as primary deposits and it is with these reserves that the credit creation commences.

Out of these additional reserves, the banks keep aside just the required reserves and lends out the rest (the r ratio is 0.1). The process of expansion continues leading to a multiple creation of deposits, credit and money.

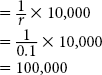

The crucial question is to what will be the total increase in the supply of money. To calculate it, we need to first find the value of the money multiplier.

We know that m

but

c = 0.5 and r = 1.

BOX 12.3

Since the year 1995, the money multiplier in China showed an upward trend. However, in 1998 there occurred some major financial reforms which led to significant changes. Though initially the money multiplier remained stable, later on it became unstable and difficult to control, with the money multiplier and high-powered money moving in opposite directions. An attempt at increasing the high-powered money to bring about changes in the money supply was accompanied by a decrease in the money multiplier. These developments presented immense challenges and opportunities to the central bank and the framers of the monetary policy.

The total increase in the supply of money = 2.5 × ΔH

= 2.5 × Rs. 600 crores

= Rs. 1500 crores.

It is important to note that the smaller are the c and the r ratios the larger is the value of the multiplier.

RECAP

- The determinants of money supply can be grouped under two headings: those that influence high-powered money and those that influence the money multiplier.

- A given increase in H leads, over time, to a multiple expansion in bank credit and in the supply of money in the economy.

THE PROCESS OF CREDIT CREATION AND THE DEPOSIT MULTIPLIER

One of the most important functions performed by a commercial bank is the creation of credit. In fact, it is the lending and the borrowing activities of the commercial banks that lead to the credit creation.

Bank deposits can be grouped into two categories:

- Primary deposits: These are deposits that bring in new reserves to the banks.

- Secondary deposits: They are also called derivative deposits; they are deposits that do not bring in new reserves to the banks. They are created out of the credit extended by the banks.

Credit Creation in a Single Bank Model

We assume that:

- There exists a single bank in the banking system.

- The bank is only accepting demand deposits.

- The c ratio is 0.5 whereas the r ratio is 0.1 (where the r ratio includes both the required reserve ratio and the excess reserve ratio).

- The bank’s assets include reserves and the loans on which they charge an interest.

In continuation of the earlier example, the government purchases goods worth Rs. 600 crores from the public and makes a payment by a cheque drawn on the RBI. This cheque is deposited by the public with the bank, which collects the payment. The deposits of the public and the reserves of the bank increase by an amount of Rs. 600 crores.

As we have assumed that the currency deposit ratio is 0.5, the public makes a withdrawal of only Rs. 200 crores and leaves the rest Rs. 400 crores with the bank. Thus, Rs. 400 crores worth of deposits is created with the bank. As these deposits bring in new reserves to the bank, they are called primary deposits.

These do not earn any interest. Thus as per the desired reserve ratio of 0.1, the bank keeps aside an amount of Rs. 40 crores and lends out the rest Rs. 360 crores to the borrowers at an interest. Actually, this lending is not in the form of cash. All that happens is that the borrower’s account is credited for this particular amount and he can draw cheques for that amount. This is the first round of credit creation.

When the borrower spends the amount, he actually withdraws only a part of the total amount (as per the c ratio). Thus, the borrower withdraws Rs. 120 crores and Rs. 240 crores continue to remain with the bank representing an addition to the secondary deposits. It represents a second round increase in deposits and in money.

Out of this amount, the bank again keeps aside a certain amount and lends out the rest. As the proceeds of the loans are spent, the recipients of the payments again deposit them with the bank, leading to another round of credit creation and deposits and money. However, it is to be noted that in each successive round the amount of money involved becomes smaller and smaller. This can be put in the form of an infinite geometric series, which is the same as in the case of the multiple bank model discussed below.

It is felt that the economic growth in the recent years all over the world has occurred due to the liberal creation of credit and the liquidity injects at low rates of interests by the central banks. The lenders have been no less instrumental in perpetuating the lending aggressively by offering innovative credit instruments such as credit default swaps (CDS), commercial mortgage backed securities (CMBS), residential mortgage backed securities (RMBS) and others. However, the recent spurt in defaults in the mortgage market, erratic rating issues, etc. have led to a fall in the demand for these instruments and the potential investors no longer take fancy to such investments. This may perhaps be the start of a vicious cycle of liquidity crisis and credit reversal and is capable of significantly impacting the economic growth of the different nations.

Credit Creation in a Multiple Bank Model

Till now, we have assumed that there exists a single bank. However, in reality there exist several banks in the banking system.

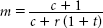

Suppose the first bank receives Rs. 10,000 as primary deposits. With a reserve ratio of 10 per cent, the bank will make a loan of Rs. 9000 and keep Rs. 1000 of the deposits as reserves. Hence, there will be a creation of credit. The balance sheet of the first bank will be as shown below:

Balance sheet of the first bank

The credit creation process will continue as the borrowers deposit the loan amount of Rs. 9,000 with another bank and make use of the loan amount of Rs. 9,000 to make a payment to a creditor who then deposits it with another bank, the second bank. The balance sheet of the second bank will be as shown below:

Balance sheet of the second bank

The amount of Rs. 8100, which is given out as loan by the second bank may eventually get deposited in a third bank whose balance sheet will be as shown below:

Balance sheet of the third bank

This process continues in the same manner as in the case of the single bank model. The total amount of money created by the banking system can be calculated as follows:

Original Deposit with the first bank = Rs. 10,000

| Lending by the first bank | = (1 – r) × 10,000 |

| Lending by the second bank | = (1 – r)2× 10,000 |

| Lending by the third bank | = (1 – r)3 × 10,000 |

Total money supply

= 10,000 + (1 – r) × 10,000 + (1 – r)2 × 10,000 + (1 – r)3 × 10,000 + …

= [1 + (1 – r) + (1 – r)2 + (1 – r) 3 + …] × 10,000

This is the sum of an infinite geometric series and can be expressed as

| Total money supply |  |

(as we have assumed r = 10% = 0.1)

Thus, the original deposit of Rs. 10,000 will generate a total amount of money equal to Rs. 100,000. It is of extreme importance to understand that under the fractional reserve system, although there is creation of money, there is no creation of wealth as such. Thus there is an increase in the liquidity in the economy, but there is certainly no increase in the economy’s wealth.

The Deposit and the Credit Multipliers (in a Simple Model Where There are Only Demand Deposits)

Deposit Multiplier

We have observed that starting with a primary deposit, the banking system is able to create secondary deposits, which are in fact a multiple of the primary deposits. This multiple will depend on the value of the deposit multiplier, Dm.

The deposit multiplier is the ratio of the change in deposits to the change in reserves. Thus

Deposit multiplier is the ratio of the change in deposits to the change in reserves.

where,

ΔD = change in deposits

ΔD = change in reserves

Thus, we have

Deposit Multiplier,

In our example, as c is 0.5 and r is 0.1, the value of the deposit multiplier will be

The value of the deposit multiplier depends on the following factors:

- The reserve ratio: Given the currency deposit ratio, the higher the reserve ratio the lower will be the value of the deposit multiplier.

- The currency deposit ratio: Given the reserve deposit ratio, the higher the currency deposit ratio the lower will be the value of the deposit multiplier. In the extreme case, where there is no currency drain, then the whole of the initial amount of Rs. 600 crores will be deposited with the banking system and the deposit multiplier will be

Credit Multiplier

Credit multiplier is the ratio of the change in the amount of credit to the change in reserves.

This is a concept, which is akin to the deposit multiplier. The credit multiplier is the ratio of the change in the amount of credit to the change in reserves. Thus,

where,

ΔCr = change in credit

ΔR = change in reserves

Thus, we have

Credit Multiplier,

In our example, as c is 0.5 and r is 0.1, the value of the deposit multiplier will be

The value of the credit multiplier also depends on the two ratios, the reserve ratio and the currency deposit ratio.

A comparison of the deposit and the credit multiplier shows that while the denominator is the same in both of them, the deposit multiplier has a change in deposits, ∆D in the numerator and the credit multiplier has a change in credit, ∆C in the numerator. Thus what is required is to distinguish between a change in deposits, ∆D and change in credits, ∆C. Although a change in deposits can occur due to change in both the primary deposits and in the secondary deposits, a change in credit occurs only when there is a change in the secondary deposits.

RECAP

- Bank deposits can be grouped into two categories: primary deposits and secondary deposits.

- By starting with a primary deposit the banking system is able to create secondary deposits, which are in fact a multiple of the primary deposits.

SUMMARY

INTRODUCTION

In this chapter, we discussed the theory of money supply or what is often called the H theory of money supply, the measures of money supply in India and the creation of credit.

MEASURES OF MONEY SUPPLY IN INDIA

- The supply of money is a stock variable.

- When we measure the supply of money, it is the money in the hands of the ‘public’.

- Until the year 1967–68, the RBI used to publish data only on what is called the narrow measure of money supply.

- From the year 1967–68, RBI started publishing data on the broader measure of money supply or the AMR in addition to the earlier narrow measure.

- Since April 1977, the RBI has started publishing data on four alternative measures of money supply:

M1 = C+ DD + OD

M2 = M1+ Saving deposits with post offices

M3 = M1 + Net time deposits of banks

M4 = M3 + Total deposits with post office savings organization (including NSC)

- What we call M1 in the new series is actually the narrow measure of money supply; what we call M3 in the new series is actually the AMR.

- In the new series, the four measures of money supply are in descending order of liquidity.

THE THEORY OF MONEY SUPPLY

- The supply of money is determined by the monetary authorities, the public and the banks.

- In a fractional reserve banking system, banks need to keep aside only a fraction of the total deposits as reserves and give out the rest in the form of loans.

- The theory of money supply is also called the H theory of money supply or the money multiplier theory of money supply, where

is the money multiplier.

is the money multiplier. - With the introduction of time deposits, D = DD+TD. The money multiplier equation becomes

- In the money multiplier equation, c is the currency demand deposit ratio, r is the reserve deposit ratio and t is the time deposit ratio.

- The equation M = m(c, t, r) H shows that the determinants of money supply can be grouped under two headings: those that influence the high-powered money, H and those that influence the money multiplier, m.

- H or High-powered money is money, which is produced by the monetary authorities and held by the public and the banks. Changes in the RBM are largely responsible for the changes in high-powered money.

- The determinants of the money multiplier can be divided under two heads: the proximate determinants and the ultimate determinants.

THE PROCESS OF CREDIT CREATION AND THE DEPOSIT MULTIPLIER

- It is the lending and the borrowing activities of the commercial banks that lead to the credit creation.

- Bank deposits can be grouped into two categories: primary deposits, which are deposits that bring in new reserves to the banks and secondary deposits, which are deposits that do not bring in new reserves to the banks. They are created out of the credit extended by the banks.

- Credit creation in a single bank model shows the process of how, with successive rounds of credit creation, the single bank is able to create credit.

- Credit creation in a multiple bank model shows the process of how, with successive rounds of credit creation, the several banks in the banking system are able to create credit.

- The deposit multiplier is the ratio of the change in deposits to the change in reserves and given as

and the credit multiplier is the ratio of the change in the amount of credit to the change in reserves and given as,

and the credit multiplier is the ratio of the change in the amount of credit to the change in reserves and given as,

REVIEW QUESTIONS

TRUE OR FALSE QUESTIONS

- The supply of money is a flow variable.

- Until the year 1967–68, the RBI used to publish data only on what is called the broad measure of money supply.

- Coins and one rupee notes are issued by the RBI.

- High-powered money is money, which is produced by the government and the central bank.

- New reserves are known as secondary deposits.

VERY SHORT-ANSWER QUESTIONS

- What is the meaning of money in the hands of the ‘public’?

- What are ‘aggregate monetary resources’ or the AMR?

- What is high-powered money?

- What is the fractional reserve banking system?

- Explain the difference between money and high-powered money.

SHORT-ANSWER QUESTIONS

- Mention the four measures of money supply (with their components) published by the RBI.

- Write short notes on the following:

- Time deposits of banks

- Savings account deposits

- What is the money multiplier? Explain.

- Write short notes on the following:

- Currency deposit ratio

- Reserve deposit ratio

- What is the difference between the deposit and the credit multipliers?

LONG-ANSWER QUESTIONS

- Discuss the various measures of money supply in India.

- The theory of money supply is also called the H theory of money supply or the money multiplier theory of money supply. Discuss.

- Write a short note on the working of the money multiplier process.

- Elucidate the process of credit creation when there exists only a single bank in the banking system.

- Credit creation in a multiple bank model shows how, with successive rounds of credit creation, the several banks in the banking system are able to create credit. Discuss.

ANSWERS

TRUE OR FALSE QUESTIONS

- False. The supply of money is a stock variable and refers to the stock of money at a point in time.

- False. Until the year 1967–68, the RBI used to publish data only on the narrow measure of money supply.

- False. Coins and one rupee notes are issued by the Government of India whereas currency notes of rupees two and higher denominations are issued by the RBI.

- True. High-powered money is money, which is produced by the government and the central bank and held in the hands of the public and the banks.

- False. New reserves are known as primary deposits and it is with these reserves that the credit creation commences.