CHAPTER 10A

Studies in Cost Management

Earned Value—An Integrated Project Management Approach

Earned Value Management (EVM), often referred to simply as earned value, is a productive technique for the management of cost and schedule that is required on many U.S. government contracts. In recent years, EVM has shown itself to be equally valuable when applied to other complex projects, whether in private, commercial, or government environments.

In the world of EVM, the role of the Control Account Manager (CAM) is pivotal in the process. The project manager and all of the other traditional project management contributors are active participants and have significant responsibilities that can’t be underestimated. However, because of the critical role of the CAM, this material is targeted at helping the CAM plan and manage assigned tasks.

The EVM process is essentially the same at all levels of the project or organization. Individual components of the EVM approach addresses work authorization through status reporting. Descriptions of cost accounts, authorized work packages, and planned work packages are emphasized because of their significance in the EVM approach in general and, specifically, because of the role they play in helping the CAM to be successful at the difficult job of balancing the many project management requirements and tasks.

PROCESS OVERVIEW

The first EVM concept (then known as Cost Schedule Control System Criteria or C/SCSC) was introduced in the 1960s, when the Department of Defense Instruction 7000.2-Performance Measurement of Selected Acquisitions exploded on the management scene. The criteria included in the instruction defined standards of acceptability for defense contractor management project control systems. The original 35 criteria were grouped into 5 general categories—organization, planning and budgeting, accounting, analysis, and revisions—and were viewed by many, government and contractor personnel alike, as a very positive step toward helping to solve management problems, while achieving some much needed consistency in the general project management methods used throughout the Department of Defense and, eventually, most major U.S. government agencies.

Today, many highly respected organizations around the world work within the boundaries of the criteria. Hundreds have received validation or certification by the U.S. government. These organizations represented thousands of government and private projects and programs. Thousands of other contractors have been using the basic principles of EVM without any formal requirements to do so. These organizations have clearly found the concepts and techniques useful on all work, not just that being done for the U.S. government.

It should be noted that not everyone agrees that EVM is the best project management approach. However, in this author’s experience, these same critics subtly adapt various components of the EVM concept on their projects and find them extremely valuable and productive management tools. After all, it is hard to argue with the sound business management concepts upon which EVM is based.

Numerous abbreviations and terms are employed in a description of EVM; these are explained in Figure 10A-1.

CRITICAL DATA ELEMENTS OF EVM

There are three critical data elements involved in EVM: Planned Value (PV), Actual Cost (AC), and Earned Value (EV).

Planned Value

The PV is the amount of resources, usually stated in terms of dollars, that are expected to be consumed to accomplish a specific piece of work scope. The PV is more commonly known as the spend plan or cost estimate and has long been employed in the world of project management. In EVM applications, the emphasis is placed on achieving the closest possible correlation between the scope of work to be completed (work content) and the amount of resources actually required to deliver that scope.

Actual Cost

The AC is the amount of resources, usually stated in terms of dollars, were expended in a specified time period to accomplish a specific scope of work. The AC is more commonly known as the actual incurred cost or simply actuals, and it has also been employed in the world of project management since its beginning. In EVM applications, the emphasis is placed on expending and recording resource expenditures with a direct correlation to the scope of work that has been planned to be completed at the same point in time.

Earned Value

The EV is a measure of the amount of work accomplished, stated in terms of all or a portion of the budget assigned to that specific scope of work. The work accomplishment status, as determined by those responsible for completion of the work, is converted to dollar form and becomes the focal point of all status and analysis activities that follow. The EV is the only nontraditional data element required when utilizing EVM management techniques. The EV, when compared with the PV and AC, provides the foundation for comprehensive management evaluations, projections, and (if necessary) corrective action planning and implementation.

FIGURE 10A-1. ABBREVIATIONS AND TERMS

What’s in It for the User?

In-the-trenches experience has resulted in two separate observations on utilizing EVM: good news and bad news. Let’s take the good news first. The EVM approach:

• Provides information that enables managers and contributors to take a more active role in defining and justifying a “piece of the project pie.”

• Alerts you to potential problems in time to be proactive instead of reactive.

• Allows you to demonstrate clearly your timely accomplishments.

• Provides the basis for significant improvement in internal and external communications.

• Provides a powerful marketing tool for future projects and programs that require high management content.

• Provides the basis for consistent, effective management system-based training and education.

• Provides a more definitive indication of the cost and schedule impact of project problems.

• Allows tremendous flexibility in its application.

On the downside, EVM also most likely:

• Results in the customer asking for more detail.

• Results in greater time spent organizing and analyzing data by someone in the organization, although this is becoming less and less of an issue with today’s automated project management support capabilities.

• Requires more structure and discipline than usual.

• Costs money and organizational resources to develop and implement.

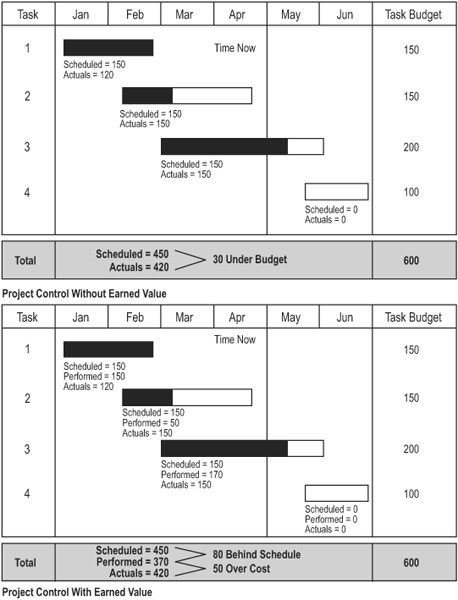

Experience clearly shows the net result to be significantly in favor of utilizing the EVM approach. Figure 10A-2 shows the benefits in graphic form. Without earned value, the example shows an “under budget” situation. Using EVM, the real status of the project is revealed, showing a project behind schedule and over budget.

But even with EVM, the management user must remember at all times that using EVM will not:

• Solve technical problems.

• Solve funding problems, although it might help.

• Make decisions for you, although it will help.

• In any way “manage” your program, project, or work package.

EVM will, however, provide sound, timely information—the most useful commodity for today’s managers faced with making extremely difficult decisions.

PROCESS DESCRIPTION

EVM can be successful only if the user recognizes the need for a hierarchical relationship among all the units of work to be performed on a project. This hierarchical relationship is established through the work breakdown structure (WBS). Work is done at the lowest levels of the WBS (work packages); therefore, these critical elements have particular significance when it comes to achieving the most beneficial results from using EVM.

The EVM process involves numerous specific tasks and efforts, which are described in detail below.

Control Account

The control account (CA) is the focus for defining, planning, monitoring, and controlling because it represents all the work associated with a single WBS element, and it is usually the responsibility of a single organizational unit. EVM converges at the control account level, which includes budgets, schedules, work assignments, cost collection, progress assessment, problem identification, and corrective actions.

Day-to-day management is accomplished at the CA level. Most management actions taken at higher levels are on an “exception” basis in reaction to significant problems identified in the CA.

FIGURE 10A-2. BENEFITS OF USING EVM

The level selected for establishment of a CA must be carefully considered to ensure that work is properly defined in manageable units (work packages) with responsibilities clearly delineated.

Authorized Work Package

An authorized work package (AWP) is a detailed task that is identified by the control account manager for accomplishing work within a CA. An AWP has the following characteristics:

• It represents units of work at the levels where the work is performed (lowest level of the WBS).

• It is clearly distinct from all other work packages and is usually performed by a single organizational element.

• It has scheduled start and completion dates (with interim milestones, if applicable), which represent physical accomplishment.

• It has a budget or assigned PV usually expressed in terms of dollars and/or labor hours.

• Its duration is relatively short unless the AWP is subdivided by discrete value milestones that permit objective measurement of work performed over long periods of time.

• Its schedule is integrated with all other schedules.

Planning Work Package

If an entire control account cannot be subdivided into detailed AWPs, far-term effort is identified in larger planned work packages (PWPs) for budgeting and scheduling purposes. The budget for a PWP is identified specifically according to the work for which it is intended. The budget is also time-phased and has controls, which prevent its use in performance of other work. Eventually, all work in PWPs is planned to the appropriate level of detail for authorized work packages.

Work Authorization

All project work, regardless of origin, should be described and authorized through the work authorization process, an integral part of EVM. The EVM relates not only to work authorization, but also to planning, scheduling, budgeting, and other elements of project control, which reflect the flow of work through the functional organizations.

Although the control account manager is most concerned with the work authorization process at the authorized work package and control account levels, the total process is presented to provide the CAM with a sense of specific responsibilities within the total system. The authorization flow is traced from customer authorization through contractual change authorization using the following five steps:

1. Authorization for contracted work consists of two parts: the basic contract and the contractual scope changes.

2. Work authorization for contracted work is provided as follows: The organization’s general manager, in coordination with the finance director, provides authorization to the project manager to start work through a contract directive (CD). This directive approves total project scope of work and funding

3. WBS planning target authorization is as follows:

• The WBS manager prepares the WBS planning target authorization.

• The project manager approves the WBS target goal for expansion to the functional control account.

• The WBS target is later replaced by the completed WBS-package budget rollup of CAs.

4. The procedure for control account planning target authorization is as follows:

The control account manager prepares a target control account goal for expansion to work packages. The CA target is later replaced by CA-package budget rollup of all planned work packages.

5. Change control is processed as follows: The CAM submits or signs a modified work package form to the EVM information department. These modified work package forms show any internal replanning or customer contractual baseline change that:

• Alters work by addition/deletion, causing CA budget adjustments.

• Causes adjustment of work or budget between CAs.

• The processing department completes a package change record (PCR) for audit trail of baseline revisions (baseline maintenance).

• The project manager or delegated WBS manager approves the add/delete transactions to the management reserve/contingency account controlled by management if the budget adjustment is outside the single cost account. (Note: Parties to the original budget agreements must approve revisions.)

• The CA budget cannot be changed by such actions as cost overruns or under runs; changes that affect program schedules or milestones because of work acceleration or work slippage; or retroactive adjustments.

Planning and Scheduling

This description of planning and scheduling from the project level down gives the CAM an overall view of specific responsibilities. Eight factors are involved.

1. Planning and scheduling must be performed in a formal, complete, and consistent way. The customer-provided project master schedule and related subordinate schedules through the control account/work package levels provide a logical sequence from summary to detailed work packages. The EVM logic network schedule works as the tool to make certain that work package schedules are compatible with contract milestones, since the networks are derived from the work package database.

2. Network logic must be established for all interfaces within the framework of the contract work breakdown structure (CWBS).

3. The responsibility assignment matrix (RAM) is an output of WBS planning. It extends to specific levels in support of internal and customer reports. The RAM merges the WBS with the organization structure to display the intersection of the WBS with the control account-responsible organizations.

4. When work plans are detailed, the lower-level work packages are interfaced and scheduled. These work packages are usually identified as either:

• Discrete effort: Effort that can be scheduled in relation to clearly definable start and completion dates, and which contains objective indicator milestones against which performance can be realistically measured

• Level of effort (LOE): Support effort that is not easily measured in terms of discrete accomplishment; it is characterized by a uniform rate of activity over a specific period of time.

Where possible, work packages should be categorized in terms of discrete effort. LOE should be minimized—typically not more than ten percent.

5. The general characteristics of schedules are as follows:

• Schedules should be coordinated (with all other performing organizations) by the EVM manager.

• Commitment to lower-level schedules provides the basis for the project schedule baselines.

• All work package schedules are directly identifiable as related to CA packages and WBS elements.

After a baseline has been established, schedule dates must remain under strict revision control, changing only with the appropriate EVM manager’s approval.

6. Two categories of project schedules are used. Project-level schedules are master phasing/milestone schedules, program schedules, or WBS intermediate schedules. Detailed schedules are either control account schedules or work package schedules.

• Control account schedules: (1) have milestones applicable to responsible organizations; (2) are developed by the organizations to extend interfaces to lower work package items; (3) are at the level at which status is normally determined and reported monthly to the project CA level for updating of higher-level schedule status and performance measurement; (4) have planned and authorized packages that correlate to the CA, WBS, and scope of work (SOW) and which is reported to the customer; and (5) document the schedule baseline for the project.

• Work package schedules: (1) provide milestones and activities required to identify specific measurable work packages; (2) supply the framework for establishing and time-phasing detailed budgets, various status reports, and summaries of cost and schedule performance; (3) are the level at which work package status is normally discussed and provide input for performance measurement; (4) are the responsibility of a single performing organization; (5) provide a schedule baseline against which each measurable work package must be identified; and (6) require formal authorization for changes after work has started and normally provide three months’ detail visibility.

7. Regarding schedule change control, the control account managers can commit their organization to a revised schedule only after formal approval by at least the WBS manager.

8. Work package schedule statusing involves the following:

• Objective indicators or milestones are used to identify measurable intermediate events.

• Milestone schedule status and EV calculations are normally performed monthly.

Budgeting

In accordance with the scope of work negotiated by the organization with the customer, the budgets for elements of work are allocated to the control account manager through the EVM process. These budgets are tied to the work package plans, which have been approved in the baseline. The following top-down outline, with five factors, gives the CAM an overview of the EVM budgeting process.

1. Project-to-function budgeting involves budget allocations and budget adjustments.

Budget allocations involve the following:

• The project manager releases the WBS targets to the WBS managers, who negotiate control account targets with the control account managers. The CAMs then provide work package time-phased planning.

• When all project effort is time-phased, the EVM information is produced and output reports are provided for the project manager’s review. When the performance measurement baseline (PMB) is established, the project manager authorizes WBS packages, which are summarized from the control accounts.

• The WBS manager authorizes the control account packages, which are summed from work package planning. The time-phased work package budgets are the basis for calculating the EV each month.

Regarding budget adjustments, the performance measurement baseline can be changed with the project manager’s approval when either of the following occurs:

• Changes in SOW (additions or deletions) cause adjustments to budgets.

• Formal rebaselining results in a revised total allocation of budget.

2. PMB budgets may not be replanned for changes in schedule (neither acceleration nor slips) or cost overruns or underruns.

3. Management Reserves (MRs) are budgets set aside to cover unforeseen requirements (unknown/unknowns). The package change record is used to authorize add/delete transactions to these budgets.

4. Undistributed Budgets (UBs) are budgets set aside to cover identified, but not yet detailed or assigned SOW. As these scopes of work are incorporated into the detail planning, a PCR is used to authorize and add to the performance measurement baseline.

5. Regarding detailed planning, the planned work package is a portion of the budget (the PV) within a CA that is identified to the CA, but is not yet defined into detailed AWPs.

Cost Accumulation

Cost accumulation provides the CAM with a working knowledge of the accounting methods used in EVM. There are six things involved in cost accumulation accounting (for actual costs).

1. Timekeeping/cost collection for labor costs uses a labor distribution/accumulation system. The system shows monthly expenditure data based on labor charges against all active internal work packages.

2. Three factors are involved in nonlabor costs.

• Material cost collection accounting shows monthly expenditure databased on purchase order/subcontract expenditure.

• The cost collection system for subcontract/integrated contractor costs uses reports received from the external source for monthly expenditures.

• Regarding the funds control system (commitments):

—The funds control system records the total value of purchase orders/subcontracts issued, but not totally funded.

—The cumulative dollar value of outstanding orders is reduced as procurements are funded.

3. Regarding the accounting charge number system:

• The accounting system typically uses two address numbers for charges to work packages: (1) the work package number, which consists of WBS-department-CA-work package; and (2) the combined account number, which consists of a single character ledger, three-digit major account, and five-digit subaccount number.

• Work package charge numbers are authorized by the control account manager’s release of an AWP.

4. Regarding account charge number composition, an example of an internal charge number is 181-008-1-01. External charge numbers are alphabetized work package numbers. An example is 186-005-2-AB.

5. Regarding direct costs:

• All internal labor is charged to AWP charge numbers.

• Other direct costs are typically identified as: (1) Purchase services and other; (2) travel and subsistence; (3) computer, and (4) other allocated costs.

6. Indirect costs are elements defined by the organization.

• Indirect costs are charged to allocation pools and distributed to internal work packages. They may also be charged as actuals to work packages.

• Controllable labor overhead functions may be budgeted to separate work packages for monthly analysis of applied costs.

Note that actual cost categories and accounting system address numbers vary by organization. Extra care must be taken to integrate EVM requirements with other critical management information processes within the specific organization.

Performance Measurement

Performance measurement for the control account manager consists of evaluating work package status, with EV determined at the work package level. Comparison of planned value (PV) versus earned value (EV) is made to obtain schedule variance. Comparison of EV to actual cost (AC) is made to obtain cost variance. Performance measurement provides a basis for management decisions by the organization and the customer. Six factors must be considered in performance measurement.

1. Performance measurement provides:

• Work progress status.

• Relationship of planned cost and schedule to actual accomplishment.

• Valid, timely, auditable data.

• The basis for estimate at completion (EAC), or latest revised estimates (LRE) summaries developed by the lowest practical WBS and organizational level.

2. Regarding cost and schedule performance measurement:

• The elements required to measure project progress and status are: (1) work package schedule/work accomplished status; (2) the PV or planned expenditure; (3) the EV or earned value; and (4) the AC or recorded (or accrued) cost.

• The sum of AWP and PWP budget values (PV) should equal the control account budget value.

• Development of budgets provides these capabilities: (1) the capability to plan and control cost; (2) the capability to identify incurred costs for actual accomplishments and work in progress; and (3) the control account/work package EV measurement levels.

3. Performance measurement recognizes the importance of project budgets.

• Measurable work and related event status form the basis for determining progress status for EV quantification.

• EV measurements at summary WBS levels result from accumulating EV upward through the control account from work package levels.

• Within each control account, the inclusion of LOE is kept to a minimum to prevent distortion of the total EV.

• There are three basic “claiming techniques” used for measuring work package performance: (1) Short work packages are less than three months long. Their earned value (EV) equals PV up to an 80 percent limit of the budget at completion until the work package is completed. (2) Long work packages exceed three months and use objective indicator milestones. The earned value (EV) equals PV up to the month-end prior to the first incomplete objective indicator. (3) Level of effort: Planned value (PV) is earned through passage of time.

• The measurement method to be used is identified by the type of work package. Note that EV must always be earned the same way the PV was planned. (See Figure 10A-3 for alternate methods of establishing PV and calculating EV.)

4. To develop and prepare a forecast to complete (FTC), the control account manager must consider and analyze:

• Cumulative actuals/commitments

• The remaining CA budget

• Labor sheets and grade/levels

• Schedule status

• Previous quarterly FTC

• EV to date

• Cost improvements

• Historical data

• Future actions

• Approved changes.

5. The CAM reports the FTC to the EVM information processing organization each quarter.

6. The information processing organization makes the entries and summarization of the information to the reporting level appropriate for the project manager’s review. [Ed. Note: Further information on measurement of aspects of project management performance beyond intra-project metrics can be found in Chapter 24.]

Variance Analysis

If performance measurement gives results in schedule or cost variances in excess of preestablished thresholds, comprehensive analyses must be made to determine the root cause of the variance. The CAM is mainly concerned with variances that exceed thresholds established for the project. Analyses of these variances provide information needed to identify and resolve problems or take advantage of opportunities. Three factors are involved in variance analysis.

0/100 |

Take all credit for performing work when the work package is complete. |

50/50 |

Take credit for performing one-half of the work at the start of the work package; take credit for performing the remaining one-half when the work package is complete. |

Discrete Value Milestones |

Divide work into separate, measurable activities and take credit for performing each activity during the time period it is completed. |

Equivalent Units |

If there are numerous similar items to complete, assume each is worth an equivalent portion of the total work package value; take credit for performance according to the number of items completed during the period. |

Percentage Complete |

Associate estimated percentages of work package to be completed with specific time periods; take credit for performance if physical inspection indicates percentages have been achieved. |

Modified Milestone/Percentage Complete |

Combines the discrete value milestone and percent complete techniques by allowing some “subjective estimate” of work accomplishment and credit for the associated earned value during reporting periods where no discrete milestone is scheduled to be completed. The subjective earning of value for nonmilestone work is usually limited to one reporting period or up to 80 percent of the value of the next scheduled discrete milestone. No additional value can be earned until the scheduled discrete milestone is completed. |

Level of Effort |

Based on a planned amount of support effort, assign value per period; take credit for performance based on passage of time. |

Apportioned Effort |

Milestones are developed as a percentage of a controlling discrete work package; take credit for performance upon completion of a related discrete milestone. |

FIGURE 10A-3. ALTERNATE METHODS OF ESTABLISHING PV AND CALCULATING EV

1. Preparation

• The cost-oriented variance analyses include a review of current, cumulative, and at-completion cost data. In-house performance reports are used by the CAM to examine cost and schedule dollar plan vs. actual differences from the cost account plan.

• The calendar-schedule analyses include a review of any (scheduling subsystem) milestones that cause more than one-month criticality to the contract milestones.

• Variances are identified to the CA level during this stage of the review.

• Both cost variance and schedule variance are developed for the current period and cumulative as well as at-completion status.

• Determination is made whether a variance is cost-oriented, schedule-oriented, or both.

• Formal variance analysis reports are developed on significant CA variances.

Variance analyses should be prepared when one or more of the following exceed the thresholds established by the project manager: (1) schedule variance (EV to PV); (2) cost variance (EV to AC); or (3) at-completion variance (budget at completion to latest revised estimate, or LRE).

3. Operation

• Internal analysis reports document variances that exceed thresholds: schedule problem analysis reports for “time-based” linear schedule, or control account variance analysis reports for dollar variances.

• Explanations are submitted to the customer when contractual thresholds are exceeded.

• Emphasis should be placed upon corrective action for resolution of variant conditions.

• Corrective action should be assigned to specific individuals (control account managers) and closely tracked for effectiveness and completion.

• Internal project variance analyses and corrective action should be formally reviewed in regularly scheduled management meetings.

• Informal reviews of cost and schedule variance analysis data may occur daily, weekly, or monthly, depending on the nature and severity of the variance.

Figure 10A-4 presents some sample comparisons of PV, EV, and AC.

Reporting

The two basic report categories are customer and in-house. Customer performance reports are contractually established with fixed content and timing. In-house reports support internal projects with the data that relate to lower organizational and WBS levels. The CAM is mainly concerned with these lower-level reports.

1. Customer reporting

• A customer requires summary-level reporting, typically on a monthly basis.

• The customer examines the detailed data for areas that may indicate a significant variance.

FIGURE 10A-4. COMPARISONS OF PLANNED VALUE, EARNED VALUE, AND ACTUAL COST

• The cost performance report (CPR) is the vehicle used to accumulate and report cost and schedule performance data.

2. In-house reporting

• Internal management practices emphasize assignment of responsibility for internal reports to an individual CAM.

• Reporting formats reflect past and current performance and the forecast level of future performance.

• Performance review meetings are held: (1) monthly for cost and schedule; and (2) as needed for review of problem areas.

• The CAM emphasizes cumulative to-date and to-go cost, schedule, and equivalent person power on the CA work packages.

• It is primarily at the work package level that review of performance (EV), actuals (AC), and budget (PV) is coupled with objective judgment to determine the FTC.

• The CAM is responsible for the accuracy and completeness of the estimates.

Internal Audit/Verification and Review

The control account manager is the most significant contributor to the successful operation of a EVM process and to successful completion of any subsequent internal audits or customer reviews. Day-to-day management of the project takes place at the control account level. If each CA is not managed competently, project performance suffers regardless of the sophistication of the higher-level management system. The organization and the customer should place special emphasis on CAM performance during operational demonstration reviews.

The EV approach to project management may be the most comprehensive and effective method of developing plans and providing decision-making information ever conceived. But to achieve maximum potential benefit, the extensive use of an automated support program becomes inevitable. Software especially developed to support EVM applications is currently available for nearly every computer hardware configuration.

When considering which computer hardware/software combination will best satisfy your needs, carefully evaluate your specific project application; i.e., size of projects, frequency of reporting, ease of modification, potential for expansion, and graphic output requirements. This computer hardware/software decision could be the difference between success and failure in an EVM application, so don’t rush it! Make your selection only after a thorough investigation and evaluation. Don’t let anyone sell you something you don’t need or want.

![]() If you are using EVM data to project the “future state” of a project, at what stage of the project would this data become useful in the decision making process?

If you are using EVM data to project the “future state” of a project, at what stage of the project would this data become useful in the decision making process?

![]() How important is the duration of a work package in successfully utilizing the Earned Value approach? Are there any alternatives?

How important is the duration of a work package in successfully utilizing the Earned Value approach? Are there any alternatives?

![]() During the status/reporting stage (50% complete) you note that one of the key Cost Accounts on the project has an SPI of .83. What does this mean and what would you propose doing about it?

During the status/reporting stage (50% complete) you note that one of the key Cost Accounts on the project has an SPI of .83. What does this mean and what would you propose doing about it?

REFERENCES

1 Defense Contract Management Command (DCMC), Earned Value Management Implementation Guide; www.ntsc.navy.mil/Resources/Library/Acqguide/evmig.doc.

2 Earned Value Management Standard, Project Management Institute, 2004; www.pmi.org.

3 Industry Standard Guidelines for Earned Value Management Systems; www.ntsc.navy.mil/Resources/Library/Acqguide/evms_gde.doc.

4 Project Management: The Common Sense Approach—Using Earned Value to Balance the Triple Constraint, Lee R. Lambert, PMP/Erin Lambert, MBA, Lambert Consulting Group, Inc., 2000.