Enterprise leadership management

In its development process management science has developed with the creation of human consumption and the process of consumption creation. Before scientific management was put forward by Frederick Winslow Taylor, an American writer, the management of enterprise production and operation fell into experimental management. After the steam engine was invented, enterprise production became an intensive, large-scale production. Taylor summarized practices in his scientific management theory, The Principles of Scientific Management, published in 1911. Then in 1916, Henri Fayol, a Frenchman, summarized his practical experience in General and Industrial Management on the basis of Taylor’s scientific management. By then, enterprise management had developed from management of production processes into management of operation processes.

Max Weber, a German who established the theoretical administrative organization system, is called the father of organization theory. In the 1920s, scientific management developed into management science, which was represented by George Elton Mayo, Abraham Maslow, and Douglas McGregor in America.

The development of contemporary management mainly involves the social system school, the decision-making theory school, and the contingency theory school. The social system school is represented by the American scholar Chester Barnard; the decision-making theory school is represented by American scholars Herbert Simon and James March; the system management school is represented by Fremont Kast and James Rosenzweig; the empirical school is represented by Drucker and Dale; the contingency management theory was established by F. E. Fiedler, an American who put forward the contingency leadership theory in the 1970s. Management science is sure to keep on developing with the development process of the three important consumptions practices.

Consumption and enterprise management matter a lot to enterprise. In order to straighten out their relations and function, we need first to be clear about the concepts of enterprise and management.

Section 1 The concept of enterprise

Enterprise is a cell of a social economy and an organizing form by which mankind asks nature for consumption materials and creates the movement process of consumption materials. Enterprise runs with dissipative structure. The process by which enterprises produce products is a consumption process. An enterprise’s production activity is a process during which it has a relation with nature, and it is a reflection of the relationship between people or between people and society, which must adapt to the complicated natural and social living environment. Consumption is the traction force for the production, marketing, and operation of the enterprise.

There is a boundary between the entrepreneur and capitalist. The operational philosophy and behavioral features of an entrepreneur are to bear the responsibility of the enterprise operation, and to produce maximum enterprise benefit with minimum consumption expenditure. The interests of an enterprise are divided into two: profit interests and social interests, including producing and selling useful and popular products, to generate tax, settle social employment, take care and make contributions to public welfare, and make contributions to extended reproduction for the enterprise’s development.

The operational philosophy and behavior of a capitalist

The only purpose of operating an enterprise is for profit. Any means can be applied to earn interest and profit, including harming the interest of many consumers and the public. An entrepreneur and a capitalist have the same purpose of achieving profit through careful operations, but a capitalist does not have a sense of social responsibility.

An entrepreneur’s purpose to pursue profit is not for the sake of profit. An entrepreneur regards the operation of an enterprise as a social business. The enterprise must make profit since it is the life-blood unit for social economy. Without profit, an enterprise would go bankrupt, not to mention its social responsibility and interests. The social responsibility assumed by entrepreneurs should be based on the enterprise’s profit, or else entrepreneurs couldn’t realize their social responsibility.

Although capitalists hold mercenary operation ideas, objectively, they still assume a certain social responsibility. The maximization of profit itself is equaled to the realization of social responsibility. Without social interests, an enterprise cannot realize profit interests, which is the contradictory unity of the opposites. The operation concept of an enterprise determines its behavior. The overlooking of social responsibility in the pursuit of profit hurts consumers and other social interests. Enterprise is bound to belong to society, so is the money. Nobody could bring in fortune at their birth or bring it out at death. Fortune comes from society, to society it will finally return. Therefore, the enterprise operation ideas of a capitalist should be the same as those of entrepreneurs. We need to learn from Japanese Panasonic and other entrepreneurs and strive to be excellent entrepreneurs.

Section 2 The concept of enterprise leadership management

Modern enterprise management is a people-oriented scientific management process, during which the research, development, production, marketing, and service of an enterprise are systematically integrated by functional elements with technical tools, working methods, enterprise culture, and management modes. Lower consumption costs are applied to produce more high-quality consumption products, so as to achieve better double-purposes.

The functional elements of enterprise leadership management include organization, decision-making, the consumption objective, planning profit targets, resources allocation, enterprise rules, discipline, allocation decision-making, strategy, tactics, stratagems, monitoring, safety assessment, and so on.

We should discuss the future direction of the modern enterprise from two perspectives: the correct relations of the enterprise and the individual, and the future evolution of the enterprise’s organizational form.

The enterprise and the individual are equal. The enterprise should meet the needs of the individual; meanwhile it influences the individual through its resources, responsibility, and effectiveness, as shown in Figure 15.1.

The relationship between the individual and the enterprise

The relationship between the individual and the enterprise is:

1. Demand-oriented. The individual asks the enterprise for pay, wages or salaries, status, opportunity.

2. Resource-oriented. The individual can provide the enterprise with intelligence, imagination, creativity.

3. Responsibility-oriented. The individual is responsible to the enterprise for active force, influence, power of organization.

4. Effect-oriented. The individual desires from the enterprise promotion opportunity, leadership capacity, a sense of achievement.

The enterprise’s influence on the individual

Similarly, the enterprise’s influence on the individual is:

1. Demand-oriented. The enterprise asks the individuals for proper profit for the company, practical contribution to the company, the elimination of anyone not beneficial for the company.

2. Resource-oriented. The enterprise can provide the individual with a working environment to satisfy the individual’s social demand, pay to the individual from enterprise profit, assistance for individual growth.

3. Responsibility-oriented. The enterprise desires that individuals can display leadership capacity to drive working, effectively utilize enterprise resources, bear all responsibilities within the range of rights to balance rights and responsibilities.

4. Effect-oriented. The enterprise hopes that, in a team, individuals can enable the company to grow constantly, gain more profit for the company, grow together with the company.

When we compare these orientations one by one, we may clearly define the correct relations of the enterprise and the individual. The future enterprise has five orientations:

1. Hugeness. Enterprises must focus their efforts on establishing management status in the fiercely competitive international market, while the diversified organization can easily lose. Only the centralized huge enterprise can make profit. That is why mergers and acquisitions at present are so popular.

2. Specialization. The future operation of the enterprise will be oriented to experts and professionals. Outsiders cannot deal with professional business any more. The rich hire experts to operate enterprises for them. The expert is responsible for making a proper profit. Only to separate investors from actual operators can rights and responsibilities be measured separately, and supervision must be strengthened to avoid deviation from proper enterprise orientation.

3. Cross-border operation. The shortcoming of a single country is that the survival of enterprise can be threatened when there is turmoil in the domestic market. Therefore, a modern enterprise should explore overseas markets to balance risks.

The future development of modern enterprises should depend on the five above-mentioned orientations. The success of an enterprise will depend on whether the five orientations can be met.

In the above analysis, the enterprise knows the demand of employees, and employees know the demands of an enterprise; this is very important to the leadership and strategic decision making of the enterprise.

Section 3 The philosophy of enterprise leadership management

These are some of the characteristics of the philosophy of enterprise leadership management:

1. Values. Enterprise effectiveness and consumers prevail. Everything will center on consumers’ demand and will serve consumption, with consumer satisfaction as the supreme goal.

3. Market-orientation. To pursue consumers’ demands, enterprises should create new needs of consumption, serve consumers, and satisfy them.

4. Social responsibility. The enterprise comes from society, serves society, contributes to society, and returns to society.

5. Enterprise development and management philosophy. Enterprise development is emphasized while management is applied for balance; this is the rule emphasis–balance, balance–emphasis.

Enterprise renovation and renaissance requires:

• cutting off non-profitable units

• revitalizing derelict assets

• reforming the institution and carry out restructuring

• developing new sales modes by developing new high-tech products to win the favor of direct consumers in the road to rebirth for enterprises.

Enterprises should be human-oriented, respect human rights and dignity, and manage people according to national law and enterprise regulation. People are masters, managing things, material, and property to realize community integration of society, enterprise, and individuals.

In enterprise development consumers will prevail. Everything will center on consumption and serve the consumer. The demand and trust of consumers is life for an enterprise’s existence.

Highlight enterprise development: without innovation, the enterprise will fail. Balance is management regulation, improvement, and reform to conform to enterprise development. Enterprise development and management are a dynamic process and a unity of opposites.

Information screening is essential as consumption determines everything in the modern enterprise. It is very important to investigate and collect extensive and complex consumer information and screen scientific intelligence to provide accurate, refined, and detailed information to leaders so that decision-making mistakes can be avoided.

Enterprise leaders combine strategies and tactics according to the information of targeted consumers, formulate a series of decisions, organize trials to gain experience, and then launch large-scale development.

Gradually modify mistakes to conform to market development rules: carry out executive monitoring on the enterprise’s plan; modify the plan by inspecting it to correct mistakes to ensure there is balance–emphasis and emphasis–balance in development.

Use various convenient and fast communication networks for information screening: establish basic information databases and the latest information database. The most valuable information is the most recent information.

Create an information screening database through comparative, historical, and forward analysis and by building value information.

Information without value is a disaster to the decision maker. Information authenticity is the guarantee for successive decision making, otherwise decision-making mistakes will be made, causing catastrophe and failure of the enterprise.

Section 4 Consumption, control, and management of enterprise operation planning budget benefits

The whole process of the enterprise’s operation activities is the process of consumption and consumption generation. The enterprise is a social economic cell. Enterprise operation is a process of creating benefit, which is influenced by environment and competition.

The enterprise’s double benefits are the social benefits and the enterprise’s profit benefit. Double benefits are generated during the process of production consumption and the final product consumption by consumers. Social benefits include products with use value (including consumption during the production process) directly consumed by consumers, taxes, employment, and so on. The transformation of scientific results into the productivity of the consumption society create civilized progress, generating new technological products with use value during the production consumption process. Consumption by consumers indicates social civilization and progress.

The enterprise’s benefit is profit, which is why it is called profit benefit. During the creation of social benefits, the enterprise creates surplus labor value or surplus product wealth, which is in a relation of the unity of opposites. Without social benefits, there won’t be enterprise profit benefit. Without enterprise profit benefit, the enterprise will go bankrupt, failing to create social benefits. Besides, investors enjoy a little portion of enterprise profit benefits; the rest is transformed into consumption funds for reproduction, generating social interests. During production, the enterprise creates a commodity with use value that is consumed by consumers. The generated surplus labor value – surplus product wealth, which is called the rule of profit benefits and social benefits – functions in any society.

By scientific budgeting, the enterprise will define operation results, financial status, and achievements in the future operation in the form of a monetary amount and quantity, so as to monitor and control operational activities of the enterprise and various business divisions, and accomplish comprehensive management of the entire enterprise. In utilizing this tool, we should conduct an integrated analysis of the social environment, natural conditions, and internal environment of the enterprise for the production consumption, operation planning, and budget and profit management. The overall process of enterprise planning and profit estimating should focus on benefits, which are the internal driving force for enterprise development. Enterprise development and marketing are external factors for competition and development, which is an indication of the fundamental rules of enterprise.

Operation planning and budget management has a strong causal relationship with enterprise operation effectiveness. As a saying in China goes: ‘Eating cannot impoverish us, wearing clothes cannot impoverish us, without planning, we will always be poor.’ It just illustrates the importance of plan management and summarizes income, operation, and saving.

We can summarize the purpose of operation management in the following way. During the operation process, we use minimum expenditure to create maximum income benefits. However, enterprise consumption and operation management are not simple theoretical topics, most importantly, they are practical topics. Theory comes from and is superior to practice, guiding practice. Theory is not the repetition of practice, which should be tested by practice and improved and developed in practice. Practice always prevails. Most entrepreneurs who achieve large or small success are not theoreticians at the beginning. During practice, their successful experience conforms to economic rules. Sticking to these rules, they gradually achieve success. The rule belongs to theory. However, most successful entrepreneurs fail to summarize and sublimate their practice to draw theoretical conclusions. Experience is very practical, guiding you to create higher income benefits with minimum input consumption in the operation process.

My explanation of the relationship between consumption and the budget control, operation planning and effectiveness management of the enterprise, based on theory and practice, has a practical implication. It should not be static or unchangeable management theory, and should develop in practice since the management model is confirmed by operation purpose, advanced production tools, process, and mode.

The management mode of sales service is confirmed by the budget mode of the purpose of sales service. Due to constant development of high-tech productivity, the constant change of the production modes, the operation management mode also constantly changes. Change is absolute, which better conforms to the development of the productivity of the consumption society. Invariance is relative, the need for stage balance, which safeguards the need for the development of productivity of consumption society.

Formulating a plan

An enterprise’s consumption, budget control, and operation planning management will be formulated in accordance with the long-term, mediumterm, and short-term strategies and tactics of the enterprise. The long-term plan usually covers more than five years, the medium-term plan covers two to five years while the short-term plan usually covers one year. The shortterm plan is subdivided into monthly plans. It is the general method and rule for plan formulation. Middle and short-term plans are implementation plans; in particular, the yearly plan is the specific implementation plan. Sometimes, some part of the long-term and medium-term plan will be juxtaposed with the short-term plan. Although the operation plan budget and control benefit management are formulated based on objective reality, they still belong to the subjective scope while the objective practice is in motion every minute. The plan should be tested by reality. Therefore, during the implementation of the plan, leaders should monitor and control the implementation process, summarize experiences, and correct problems. They should carry out a plan check every half-year to rectify the plan to ensure the completion of the shortterm plan. At the end of each year they should summarize the experiences and lessons in the implementation of the short-term plan and then formulate a short-term plan for the following year. At the same time, they should modify and improve the medium-term and long-term plan.

Analysis of system management for plan budget benefits

Enterprise makes investment with the purpose of achieving a targeted benefit (enterprise benefit and social benefit) by means of its management model. The management model of the enterprise determines the target benefit first, and then the budget of sales, cost, and expenditure is formulated while it is controlled by means of budget management, so the planning of enterprise investment and the scientific nature of the enterprise’s managements are greatly improved.

Further analysis on enterprise benefit budget management

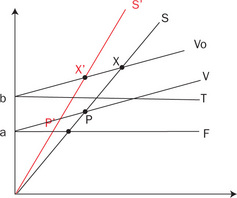

The study of the relationship between the enterprise’s sales revenue and the benefit from the perspective of management is called cost–volume–profit analysis. While determining the operation objective of an enterprise, the balance point between the enterprise revenue and consumption cost, the breakeven point, will be found first, which is the prime basis for the formulation of the enterprise’s objective. By designing a model, we can carry out monitoring and a decision-making analysis on the determinant variant among three varying factors. See Figure 15.2.

1. Confirm the rectangular coordinate system, with the horizontal axis representing sales volume and vertical axis representing cost.

2. Find the value of fixed cost a from the vertical axis and use horizontal axis o and point from vertical axis A as the starting point to portray a line of fixed cost F parallel with horizontal axis.

3. Use horizontal axis o and point from vertical axis A as the starting point and unit variable cost as ramp to portray overall cost line V.

4. Use the origin of the coordinate as the starting point and unit as the ramp to portray sales revenue line S.

5. The crossing point of the sales income line and the overall cost line is the breakeven point P, indicated as P in Figure 15.2; the upper right side of the breakeven point is the profit area while the lower left side is the loss area.

In this figure we find the balance point of enterprise income and overall cost. Profit is made when the sales income is above the balance; under the balance, loss is caused, which is the primary basis for formulating the enterprise goal. Certainly, there are many variable factors for enterprise profit, which are fundamental.

The management of enterprise benefit budgeting from the perspective of a profit and loss equation

Under the condition of ordinary relative market and regular enterprise operation, the enterprise’s profit and benefit are unknown. Then the existing resources of the enterprise will be utilized to reasonably arrange and develop the sales volume and revenue of consumption commodities, to control their cost, and to achieve profit benefit. When the objective is determined, scientific and systematic budget planning and profit management will be carried out.

The formula of sales volume required for achieving target profit is:

The formula of unit variable cost required for achieving target profit with established sales volume is:

The fixed formula required for achieving target profit under the condition of established sales volume is:

According to this profit and loss equation, the profit budget model can be displayed by cost–volume benefit diagram as shown in Figure 15.3.

1. Confirm the rectangular coordinate system, with the horizontal axis representing sales volume and vertical axis representing cost, sales income, and profit amount.

2. Find the value of fixed cost a from the vertical axis and use horizontal axis o and point from vertical axis a as starting point to portray a line of fixed cost F parallel with the horizontal axis.

3. Use horizontal axis o and point from vertical axis a as starting point and unit variable cost as a ramp to portray overall cost line V.

4. Use the origin of the coordinate as the starting point and unit as the ramp to portray sales revenue line S.

5. The fixed cost line uses target profit interest b as distance to portray target profit interest line T parallel with the fixed cost line.

6. Use target profit interest line as the basis and portray V line including target profit and overall cost parallel with V line. The crossing point X of VO line and sales income line S is the balance point to realize target profit benefit, called budget breakeven point.

According to the cost–volume profit interest diagram under profit budget management, we may see that under fixed cost, if the unit price rises, the slope of sales income will increase and the crossing point with VO line based on target profit will go down. Thus, the target profit will be realized in advance. The target profit can be realized with a relatively small amount of sales income. This is shown in Figure 15.4.

Under a fixed unit price, if the unit variable cost rises, the ramp of VO line based on the target profit interest will correspondingly drop and the crossing point with sales income, the breakeven point, will reduce too. Thus, the target profit interest will be realized in advance, as shown in Figure 15.5.

Under a fixed unit price and a unit variable cost, if the fixed cost reduces, the VO line based on target profit interest will move downwards parallel to it, as will the crossing point with sales income, and then the target profit of the enterprise will be realized under relatively low sales volume. If the sales volume continues to grow, the over-target profit will be acquired, as shown in Figure 15.6.

This analysis illustrates that the fundamental principle of the management mode of profit benefit budgeting is that sales volume and cost are worked out by demand budgeting to achieve target profit on the premise that the target profit is established, and the enterprise can obtain over-target profit by expanding the sales volume and reducing cost on the basis of determined sales volume and cost. If sales and cost budget, cash budget, research and development expenditure budget, and so on are considered from the perspective of long-term decision making, these budgets are connected to form enterprise benefit budget management.

Analysis of the budget balancing point of budget management with a focus on profit benefit

The crossing point of sales revenue and total cost under the budget management mode with a focus on profit benefit is called the budget balancing point. At X point shown in Figure 15.3, the budget balance point is the direct basis for investigating whether the target profit can be realized by profit benefit budget management.

The significance of the budget balance point is that the realization process of the target profit can be visualized, and the financial meaning of the balance point over budget can be explicitly portrayed. The triangle area under the budget balance point indicates the realization process of target profit. The VO line contains the target profit benefit and total cost. The crossing process of this line with the line of sales income S is also the process of the realization of the profit target. The crossing area of VO, S, and J vividly depicts this process. The upper right area of the budget balance point, the right area with the crossing of S and VO, indicates the over-budget profit benefit area or over-target profit benefit area.

The crossing point of sales revenue and total cost under the budget management mode with a focus on profit benefit is called the budget balancing point. This point is of great significance in budget profit benefit management. In additional to normal situations, it also manages estimated market sales volume and total cost and profit benefit. It is important to strive for technical reform or increase sales revenue or take measures to reduce cost to guarantee and develop the target of profit benefit. It is the basis for the system of enterprise leadership management.

Figure 15.7 shows the management system of enterprise profit benefit budgeting.

In the budget system of enterprise profit benefit, all budgets compose a complete and supporting budget system, which is the carrier of profit benefit budgeting. In the system of profit benefit budgeting, sub-budgets have close connection and a certain order. The close connection indicates every budget supports and depends on all the others. Target profit benefit is supported by every sub-subject, and every sub-budget attaches itself to the target profit benefit.

The target profit is subdivided into sub-budgets, the completion of which is a forceful guarantee for the realization of the target profit. Meanwhile, during the compilation of the budget, each competent department should communicate under the guidance of the budget compilation principle, which should be the reference of the budget formulation in each department to avoid the irrational phenomenon that a budget may be favorable to a specific department but not to the enterprise. Sub-budgets are interconnected and the order is irreversible.

Under a vertical organizational structure, the enterprise budget plan is subdivided into the budget responsibility of various cost centers. The person responsible for each cost center is responsible for the costs in the area. Having analyzed operation activities, the basic cost center regularly sends cost information to the superior cost center. Having summarized the subordinate cost information, the superior cost center will report to its superior, and this continues up to the investment center at the maximum level, or the cost control center, which regularly reports the plan to the budget plan management committee.

Under a horizontal organizational structure, the enterprise’s budget plan is also subdivided into budget responsibility of various centers. The basic cost center regularly submits the analysis report of actual cost to the superior cost center. Having summarized relevant information, the cost center at this level will submit it to the superior profit center. Having summarized the responsibility cost and income, the profit center will report it to the superior investment center, or the cost control center. Having summarized the budget completion situation, various centers will report the corresponding information to the corporation headquarters. The person responsible in each cost center is responsible for responsibility cost in its area.

Having analyzed operation activities, the basic cost center regularly sends cost information to the superior cost center, which summarizes the subordinate cost information and reports to its superior till the investment center at the maximum level, or the so-called cost control center, which regularly reports the plan to the budget plan management committee. Having submitted the budgeting management of operation profit benefits to special organs for disposal, the corporation reports to the budget plan management committee.

The organizational system is the basic environment for the fine operation of enterprise profit effectiveness and budget management mechanism. The realization of the target profit benefit should be established on the perfect organizational system, which mainly includes the budget management committee, special budget department, and budget responsibility network.

The budget management committee consists of the board chairman or general manager, and responsible persons of relevant departments. During the management process, they are in core leadership positions, whose main responsibility consists of organizing relevant personnel to decide target profit benefits, review, study, coordinate, and balance various budgeting items. It is the supreme management organ of profit benefit management. The special budget department is directly affiliated with the budget management committee, in charge of the management of the budget plan.

The budget responsibility network is the main body responsible for the budget, consisting of the investment center, profit center, and cost center. Different responsibility centers have different status in the profit budget management system with the investment center on top, the cost center on the bottom, and the profit benefit center in between. The investment center, profit benefit center, and cost center build the responsibility chain network, which is an all-round network including the responsibility of each department and employee. Depending on the organizational form of the enterprise, the organizational structure of the budget responsibility network is usually vertical and horizontal in form, as decided by enterprise leaders according to the conditions based on principles of convenience and strictness.

Budget variance analysis is the analysis of historical data, which does not guide production and operation (production consumption is viewed as operation) unless it is carried out sensibly and frequently (preferably once a week). The cause of budget variance mainly involves the internal working efficiency of the enterprise and the change of external elements. For the analysis and treatment of budget variance, different treatment measures are taken in accordance with the specific cause of the variance.

Ownership of responsibility for budget variance incurred by internal work efficiency should be clarified according to the controlling principle. Performance should be correctly evaluated. Combine actual performance of each budget executive body with its immediate interests through the reward and punishment system, confirm the resulting improvement measures according to reasons, and actively find new benefits growth point. If the change in factor variance incurred by external factors is a long-term trend, the operation strategy of the enterprise will be affected, which should be an investigation factor for the next phase of the budget compilation. We should properly adjust the budget goal of the next phase. On the contrary, the confirmation of the next phase of budget goal will not be influenced. Meanwhile, determining the responsibility for budget variance incurred by external factors, the principle of equal risk benefit should be followed, and risks caused by variance should be shared by various responsible organs, enterprise operators, and subscribers.

In the management model of profit benefit budgeting, budget variance analysis will begin with profit benefit variance analysis. Profit benefit variance will be gradually decreased and put into other elements related to target profit benefit, and these related elements will be analyzed one by one, so as systematically and fully to represent the cause of the actual profit benefit in budget period being above or below the target profit benefit. Figure 15.7 roughly shows the relations of various elements forming profit benefits variance. The main factors influencing the realization of the target profit benefit include sales income, sales and various variance costs, fixed costs, and management costs. During the disposal of the budget variance analysis, apply different treatment principles to different responsibility centers. Generally speaking, if a cost center can turn out products of the same quality at a cost lower than budgeted, it signifies better performance of the center.

Although management expenses belong to fixed cost, regarding the profit benefit budget, the reduction of management expenses will directly increase the profit benefits of an enterprise. Therefore, during variance analysis on management expenses, the enterprise should make reasonable judgments about work quality and service level with regard to other management systems (such as evaluation system of talents’ performance), cement this phase level, and actively seek an improvement principle to treat budget variance fairly and objectively. The profit benefit variance of the profit benefit center should be supplemented with non-currency measuring methods, including productivity, market positioning, product quality, employees’ attitude, social responsibility, balance of short-term and longterm goals, and so on.

Tables 14.1 to 14.7 illustrate the information required in budget plans.

Table 15.3

Information required in an operation profit benefits budget of service production enterprise plan (Yuan)

Table 15.7

Information required in a cash budgeting management plan (Yuan)

Note: cash flow management is the blood flow management of enterprise.

In case there are fluctuations in enterprise budget, profit, and effectiveness control and price positioning, the budget and profit plan should be adjusted.

These are some explanatory points:

1. The retail price of a full-competition product is the upward and downward price confirmed by market demand and supply relations. The enterprise fully realizes profit benefit with reduced cost.

2. The retail price of a semi-competitive product should be determined by the sales model, with reference to the retail price of a non-competitive product.

3. Price confirmation of a non-competitive product (including patent products and new-tech products) and a non-fully competitive product should consider risk expenses.

4. Self-marketing is the same as agent marketing. Both should ensure that there are sufficient expenses and operating profit in the operation process.

5. Product pricing is crucial. If the price is too high, the sales and operation results will be influenced. If the price is too low and can be raised in a timely manner, because of insufficient profit and expenses, the product cannot be developed and market of the product cannot be exploited, losing the enterprise’s double benefits.

There are many such examples. There are successful pricing experiences in Sansui Corporation, successful pricing of many products, including Sansui Oral Exposed Liquid; there is also failed product pricing (very good products, patent products, and so on), with experience and lessons very dear to the enterprise.

The enterprise takes as it focus profit benefit management, adopting budget profit benefit plan management, which is an integral systematic project. The table is a tool of the management process, but the tool can be improved or replaced. However, the profit benefit of the enterprise is not calculated, except through decision-making, balancing, and mobilizing all employees to participate in its management by giving full play to their creativity and wisdom in the operation management and enterprise development to create management benefit and development benefit in the process of plan management.

The budgeted profit and effectiveness is the goal of enterprise operation planning, which is a kind of power and motivation. The active distribution policy is the direct source of employee dynamics. To implement enterprise planning, budgeting and profit management, the employee rewarding mechanism should be implemented in the whole area of responsibilities, rights, and benefits, and should be made specific to individuals to mobilize the enthusiasm of all the employees. Meanwhile, we should pay adequate attention to quality training of all employees to let them participate in quality management, with work quality ensuring product quality to achieve impeccable quality goals. If the leader focuses attention on just accounting management while overlooking development, only the management is emphasized and the risk is intolerable, which will consequently adversely impact the development of enterprise. The management has a bottom line, but development is infinite.

The way out for an enterprise is the market. The enterprise should keep a close eye on direct consumers, and the commodity exchange channel is the bridge used to reach the target, direct consumers. The way out for the enterprise is satisfaction and favoring the product’s direct consumers and the shared goal of the manufacturer and the distributor is the direct consumer.

Various manufacturers and distributors direct consumers together, resulting in complications, and severe risks in market competition. The market changes so quickly some things cannot be planned. Therefore, managers will use planning and budgeting to strengthen accounting management and will study the competition in the market and the new demands from consumers, and improve their own policy and mode of sales service to satisfy the continual new demands of consumers. Then they can grasp the initiative in market competition; if they are passive, the targeted benefit of the operation plan cannot be realized.

The dynamic model of target operating profit

The control and management of planning and budgeting of target profit benefit of an enterprise begins with compressing costs.

Reducing the enterprise’s cost consumption is the internal work of enterprise management; talents are the source of enterprise wealth. Talents need a stage or opportunity to show the capabilities, while the stage needs talents for existence. Reducing enterprise costs begins with cutting personnel with low labor efficiency. When the number of employees of the enterprise decreases and labor efficiency rises, costs are reduced and enterprise profits are increased. Personnel costs can be reduced by:

• enhancing the comprehensive management capacity of managers and increasing labor efficiency through education and training

• applying more advanced management tools to increase management work efficiency and reducing the number of managers to the maximum extent, to improve labor efficiency and save management expenditure

• strengthening workers’ business technology knowledge and practice; in this way the enterprise improves workers’ proficiency levels on business technology, increases labor productivity and product qualification rates, and enhances the level of material management and use of raw materials and auxiliary materials; the number of backward employees will be reduced every year to increase labor productivity

• carrying out a piecework labor system for employees in the production line to calculate their salary by the piece; for operating posts to which the system cannot be applied, labor time should be checked to utilize the time relatively effectively and an overall rationing system and check by quality standard rationing, personnel rationing and salary rationing, and so on should be implemented, so as to eliminate employees with low labor productivity.

In this way the number of enterprise employees is reduced, labor efficiency is enhanced, costs are lowered, and the enterprise’s profit is increased.

Table 15.8 shows an example of the annual target operating profit benefit of Enterprise A.

Table 15.8

Sample annual operating target plan

Note: per capita annual sales revenue generated: 200,000 Yuan, and benefit created for the enterprise: 20,000 Yuan.

When the total revenue of Enterprise A stays the same, the enterprise improves the level of business proficiency through strengthening personnel training and enhances the level of workers’ labor skills and improves the level of piecework labor; while the original management tool stays unchanged, the application of management by objectives and responsibilities improves the use of eight work hours to non-piecework posts (any unit or post to which piecework cannot be applied will be managed by post rationing), workload rationing, personnel rationing and work quality requirement rationing, salary rationing, bonus rationing, and target responsibility management rationing (excluding internal management of the enterprise). Therefore, the finished product rate is increased by 3% to 99%; 10% of cost – 270 million Yuan is saved; the increased benefit of 270 million Yuan caused by management is divided by the original basic benefit of 300 million Yuan to get 90%, or 270/300 = 0.9, and the management benefit rate is increased by 90%, and the labor benefit rate is increased to 19%. It can be seen that while sales revenue is not increased, only by strengthening the internal work of enterprise management is the annual profit of Enterprise A increased to 570 million Yuan from 300 million Yuan; the profit amount is increased by 90%, and the profit rate is increased to 19% from 10%.

Let us continue with Enterprise A, on the basis of 10% reduced cost consumption, management expenditure is reduced by 10% in the second year, travel expenses are reduced by 10%, environment expenses are reduced by 10%, and other consumptions are reduced by 10% and 5.832 million Yuan is saved. In the second year, the gross profit of Enterprise A is increased to 628.32 million Yuan from 570 million Yuan in the first year. Therefore, through two years’ internal management of the enterprise, while the annual sales revenue stays the same, 3 billion Yuan, the annual enterprise benefit is increased to 628.32 million Yuan from the original 300 million Yuan.

Let us continue with Enterprise A; in the third year, the annual cost of the company is reduced by 10% through managing and reducing raw and auxiliary materials – 37.2 million Yuan. Hence the direct cost consumption is reduced to 874.8 million Yuan from 0.972 billion Yuan, and the enterprise benefit is increased to 725.52 million Yuan in the third year.

It can be seen from the above analysis that under the condition of fierce competition in the market, especially full competition of products, when it is difficult to increase the total sales revenue of the enterprise, it is advisable, practical, and feasible to increase the operating benefit of the enterprise by practicing internal management and strengthening comprehensive enterprise management while the original sales revenue stays the same. Furthermore, the benefit can be doubled. However, the method has limitations, for product cost consumption is limited rather than limitless, and cannot be reduced any more when a certain level is reached. That is exactly the limitation of management benefit. An enterprise must develop, or it cannot have scale or enhance the double benefits – enterprise development benefit and management benefit (discussed otherwise) – to the largest extent. Now let us return to the market consumption competition of the enterprise.

Assume the product of Enterprise A is in a full-competition market during the process of sales market competition. The equilibrium profit rate in the market is 10%, and the original profit rate of Enterprise A is 10%, which is equal to the average profit value of comprehensive market competition.

During the process of fierce competition in the selling market, the average profit rate decreases to 5%, and some poorly operated enterprises with an original profit rate of only 4% are sure to be closed. When the enterprise profit rate is 5% or a little higher, the profit rate of Enterprise A is still 19.184, and the profit is 150 million Yuan, hence 725.52 million Yuan – 150 million Yuan = 575.5 million Yuan.

Assume in the fifth year (calculated from the first year in which Enterprise A is assumed), the average profit rate in the market decreases to 3%, and a large number of enterprises are closed. The profit of Enterprise A is reduced to 508 million Yuan from 575.5 million Yuan. In the fourth year, with the absolute advantage in fierce market competition, Enterprise A takes over a closed factory, and carries out production technology reform (because Enterprise A has huge capital) and improves advanced technical equipment. In addition, technicians and managers are assigned to operate Enterprise B, achieving sales revenue of Enterprise B of 2 billion Yuan. Enterprise A itself expands its factory and production, increasing the sales volume of 1 billion Yuan, increasing to 4 billion Yuan from the original 3 billion Yuan. Hence the sales volume is doubled during the process of fierce competition. Although the average profit rate in the market is only 3%, the profit of Enterprise is increased to above 1 billion Yuan because of its doubled sales volume and the merit of increased scale. Furthermore, in the sixth year, because of the fierce competition in the selling market, the selling price returned to 7% from the reduced price owing to supply exceeding demand, and the original level of supply–demand relations is restored in the sixth year. Suppose the retail price level under the supply–demand relations in the first year creates an average profit level of 10%.

Now Enterprise A has an annual sales revenue of 6 billion Yuan and a sales amount of 6 billion Yuan × 24.8% (profit rate) = 1.45104 billion Yuan (profit). We can see that its sales are doubled, and that its annual profit is 1.451 billion Yuan/300 million Yuan. Because of the development of the enterprise, the profit benefit is multiplied by 4.8 times.

According to the above-mentioned six years’ development process, Enterprise A stands firmly in the market competition by strengthening internal enterprise management and reducing cost consumption. Other enterprises are closed or operate with little profit. Owing to its management advantage, high product quality, high finished product rate, and low cost consumption, Enterprise A gains a profit rate higher than that of other enterprises in the industry and achieves further development and nearly 4.8 times of annual benefit. There are two lessons from this. First, we should practice the internal work of enterprise management, enhance product quality, and reduce the consumption cost of the enterprise to the largest extent. Second, we will develop the scale of the enterprise, winning by scale. The scientific development of an enterprise is a huge (but not limitless) prospect, which is the task of an entrepreneur. Enterprise A will be the most successful enterprise in the world. The entrepreneur is Jack Welch, who is a successful and great entrepreneur.

Section 5 Reinforce enterprise goals, and develop and initiate non-comprehensive market competition products to improve two enterprise efficiencies

The products of non-full market competition involve products with proprietary technology and new characteristics that are popular with direct consumers. The product for value innovation used in Blue Ocean Strategy, the traditional American wine industry, consists of seven elements:

• the price of each bottle of wine

• the elegant and high-taste logo attached on the packaging and the label on each bottle with the prize-winning declaration; the mystic winery is used to emphasize the artistic and scientific nature of the winery

• highly invested marketing; raise the popularity of the product in the fiercely competitive market and win the favor of distributors and retailers on a kind of wine

• the reputation and historical background of the winery (list names of manor and castles and historical era when the wine factory is established)

• the complexity and elegance of wine

• seven wines of different kinds ranging from chardonnay to merlot, made according to different brewery to satisfy the tastes of customers.

Some wines have been among the most competitive products worldwide. However, the US winery invented seven value elements of the commodity to make wine in this factory very popular with consumers. The wine has been successful in the full-competition sales market and US wine has the third leadership position in the global market. Competition in this industry, valued in US$20 billion, is very fierce. Wines from California dominate the domestic market, with two-thirds the sales volume of US wineries.

Casella Wines in Australia uses a four-step action framework for innovation (Figure 15.8), and has launched Yellow Tail Wine with great success.

In order to break the relationship of the tradeoff between differentiation and low cost and to create a new value curve, there are four problems of great significance for challenging existing strategic logic and business models:

1. The new value curve promotes the pursuit for differentiation and low cost in the enterprise, so as to break the relationship of the tradeoff between value and cost.

2. It can remind the enterprise that the enterprise should not increase its cost structure and over-design products and service only for growth and creation. Many enterprises are caught in such situations.

3. It is easy and can be understood by managers at various levels, so that it can be fully participated in and supported by the whole enterprise during strategy implementation.

4. It drives the enterprise to strictly consider every competition element in the industry, so as to find out the assumptions implied in the industry, which are usually unconsciously taken for granted by competing enterprises.

Figure 15.9 shows the strategic layout of Yellow Tail Wine.

With regard to high-level or affordable wines, we attach importance to other competitive elements, such as complex taste and the brewery quality of the process and oak fermenting. Wine insiders say that the sweetness of Yellow Tail Wine reduces the quality of the wine, which goes against the traditional taste, art, and wine-making process of superb wines. This may be unreasonable as some customers prefer Yellow Tail Wines.

This company breaks the traditional manufacturing mode and promotion means of wines, creates a new, unique manufacturing and promotion mode, and wins marketing success based on consumer preference.

Figure 15.10 shows the four step movement framework. The first step is to delete long-term competing elements in your industry. These elements are usually taken for granted, although they are valueless or their value is reduced. Sometimes, the value emphasized by the buyer experiences fundamental change, but the competing enterprises don’t take corresponding action to counter these changes, or even don’t detect such a change. This is a ‘habitual blind spot’, which cannot be detected.

The second step is to make a decision on whether current products or service are over-designed, just to match and beat competitors. Under such circumstances, offerings by the enterprises exceed the need of customers, or the cost of the enterprise suddenly increases, both of which yield no good results.

The third step is to explore and eliminate the reluctant compromises made by consumers.

The fourth step is to find new sources of buyers’ value and create new demand so that the strategic pricing standard can be changed.

Working through the first two steps (removal and reduction) can help you to understand how to reduce cost below your competitors. Research shows that enterprise managers seldom systematically remove and reduce investment in competing elements, resulting in increasing cost and a more complex business model. In contrast, the latter two issues teach us how to enhance the value of the buyer and create new demand. These two issues let us systematically explore how to provide new experience and reduce the cost of enterprises. What is most important is deletion and creation, which enable the enterprise to go beyond the level of competition to pursue the goal of maximizing values. They force enterprises to change competing elements and make current rules of competion insignificant.

The analysis of the innovation thinking in the wine industry by Yellow Tail Wine demonstrates that we should be good at detecting old and habitual thinking, and recreate the innovation in a product to inspire consumer desire for it, thus creating a new differentiated product with characteristics. The product is a non-full competition product with low relative cost. The retail price should be relatively high. In response to products needing promotion, transportation, advertisement, and marketing costs should be considered. The profit margin of distributors should be relatively high. Only in this way can distributors prefer to operate. Consumers are ready to purchase because of the differentiation and freshness of the product, bringing profit to the product manufacturer as well as the distributors, which is also the rule for creating new differentiated consumption products.

Improve the management of profit benefit budget and develop a patented product without competition

If the patented product can meet a market demand, it will be a consumer-preferred product. Since it is the consumption product solely produced by the enterprise, the product enjoys patent protection in the sales market, without competition from other products of the same type and quality (the competition from replaceable products is possible), therefore, we define a patented product as a product with relatively little competition. Patents, trademarks, copyrights, and other intangible protection-rights assets belong to the scope of enterprise management, which will be monopolized products at a certain time, space, and locations with certain technology since its price is far away from its value. With the expiration of a warranty period this technology will be pushed onto the market for the general public. Other enterprises can produce this product losing the protection of the patent. Sales of the product at the same quality will be popular, with prices rapidly declining to a relatively low level. The product enters the full-competition market.

The invented Sanzhu Oral Exposed Liquid I chaired is the first high-tech product of our company with a patent (patent number: ZL93115272.0, initiated in China and leading the world trend). When the product is launched on the market, it was popular with the broad masses. In 1994, sales revenue in the first year after launching was RMB 0.125 billion; the second year it was RMB 2.35 billion, the third year RMB 8.04 billion, the fourth year RMB 7.75 billion, with total taxes, RMB more than 2 billion. Both assets accumulation and social benefits are good. Another patented invention chaired by me is Fuxinkang Oral Exposed Liquid (patent number: ZL95112116.2). In the first year of its launching in 1995, sales revenue was RMB 0.5 billion, achieving many economic and social benefits. We are applying for international patent for this product and the invented ecological cosmetics I Chaired-Economic Beauty (patent number: ZL97112152.4). It earned sales revenue of RMB 0.5 billion in the first year after its launch in 1995.

At the beginning, the patent product of Sanzhu Corporation was relatively non-competitive. With the development of its competition in the market and rapid expansion of new-tech products and similar replaceable products, the price of the patent product gradually reduced to approach the optimal market rate, finally leading to full market competition.

Bill Gates from Microsoft invented the patented technology of computer chips, taking the monopoly position in the international sales market, with a product price far deviating from value rules. The enterprise made a good profit and developed fast to be listed in the global top 500.

Therefore, the prime task for the development of an enterprise is to build up new technical and differentiated products in the market and to create a new demand from consumers. Through enterprise activities of marketing and promotion (sales and management are discussed otherwise), consumers can know, accept, buy, and even prefer new technical products, realizing the social benefit value of new technical products and the operating value of the enterprise, which are necessary to realize the enterprise’s development benefit.

Taking an overview of the progress of global civilization, we may discover that its various historical stages were initiated and created by a new tech product for consumption. Therefore, new creations made by the enterprise should be the source of dynamics for its development.

Section 6 Consumption and enterprise decision management

During the whole development process of the enterprise, decision-making will always exist. Decision-making management includes industrial investment decision-making: who should buy the product produced by the enterprise; how should the information on the consumption market be investigated; how should raw and supplementary material and production tools be selected; and how should decisions on resource allocation, and short-term, medium-term, and long-term targets be made.

Since production process and tools decide the production mode, and the production mode decides the management mode, decision making regarding the management mode, management contents, enterprise culture, regulations, and discipline should be made according to the production mode, which should then be modified in the implementation process. We may say that the management and development process of double benefits is a process of decision making and modification on decision making, in particular, decision making on the development investment of enterprise, which is an important issue of the enterprise. As long as the decision-making is not wrong, issues caused during the development of an enterprise are easily solved. If the decision making of the enterprise is wrong, it will cause irrecoverable loss, which will be the maximum loss of the double benefits of the enterprise. We should transfer the arbitrary decision making of the enterprise leader to the assessment and decision making of the management group to avoid decision-making error.

The decision-making committee

An enterprise decision-making committee centering on the president and general manager, which is the supreme authority of the decision-making level of the enterprise, should be established. The committees should include the vice president for the market or the general manager, the financial director, and the person in charge of the market information department of the enterprise, and external consultants hired to take part in decision-making; Decision-making does not mean that the minority is subordinate to the majority, instead, it means scientifically evaluating the credibility of data, the feasibility of investment capital’s return cycle, and the potential and medium-term or long-term possibility of selling in the market. A positive decision can be made when the success rate is 70% and the risk is 30% while a negative decision should be made when the evaluated success rate is 60% while the risk is 40%. Why can a big decision allow 30% risk? The development of a sales market involves a dynamic social change process, with multiple variables and unanticipated factors. Any scientific evaluation report cannot contain all unanticipated factors. Therefore, even the best decision making contains risks, which just brings more development and investment impetus. That is the reason for the existence of venture capital. The decision-making process and the final decision-making plan display knowledge, wisdom, experience, education, and a cognitive level of understanding and inspiration.

The duty of a decision-making committee

The decision-making committee will not be in charge of the management of the double operating benefits of the enterprise but make significant decisions of the enterprise. Its duty is to evaluate and make decisions about the significant problems of the enterprise throughout the management process of double operating benefits. Once a decision is made, it will be carried into practice by the president and the organization’s business administration organization.

Monitor the process of implementation and management decision making

The implementation process will be monitored and evaluated regularly once or twice a year, and will be adjusted to reduce the loss caused by wrong decisions as much as possible. Therefore, enterprises must try to ensure that correct and scientific decisions are made, or serious and uncorrectable loss will occur.

Correct decisions of Sanzhu Corporation bring huge success while important decision-making mistakes cause big losses (due to incorrect information). Therefore, enterprises should seriously summarize experience and lessons, which are important for the enterprise leaders and the enterprise.

Section 7 Consumption and organization management

Organization management is a very important element of enterprise management. Management functions of enterprises are realized by the work of the organization. The organization is power. When the enterprise has a scientific target plan and wants to realize this target plan, the first priority is to organize all resources allocation and implement them according to functional elements to realize the final target plan of the enterprise. However, the organizational development process is a test of the organization itself. It is a guarantee of the organization if the structure is strict, discipline clear, requirement severe, and attitude serious. Organizational work can enhance and develop consumption productivity of society at the maximum level, reduce cost consumption of the enterprise at the maximum level to raise double-benefits goal of enterprises.

Organizational management is the first priority of enterprise management, and does not only apply to enterprise management. Any kind of group activities needs organization. Without organization, anything will be in a mess, with no power. No targeted task can be realized (whether big or small) without organization. Individual heroism sometimes exerts great power; without organization, it is very insignificant. The hero has to be combined with the broad masses to strive to realize the plan’s target. Only then, can a hero become a true hero.

Enterprise form of organizing

The configuration of the enterprise management mode is the behavior model of the organization’s structure set in accordance with the enterprise’s production purpose, production mode, subject of labor, and the need of all the enterprise’s resources allocation. It should be established according to the size of the enterprise itself, such as flat mode, matrix mode, layer mode, and so on.

Organization structure should be simple and scientific

Organization structure should be simple and scientific. In order to set the organization structure scientifically, tight links and cross-linkage functions should be provided in it, which is guaranteed by strict discipline. The requirement for the execution of discipline should be severe; the treatment of problems should be serious, or else the organization’s power and characteristics will be lost. Management leaders at various levels should discover whether management is proper. For example, if the organization establishes a center, department and divisions, with one leader managing three or four units, or even as many as six units, bureaucratic mistakes will emerge if there are too many employees under one leader, which will affect their work. For example, the organization of the army usually adopts the system of three above three, or four above four. It will no longer be scientific with five above five system.

Bureaucratic organization will be strictly controlled

Bureaucracy is when leaders command and make decisions without considering the actual situation for a period of time. Bureaucracy is behavior that doesn’t conform to actual conditions, which is a frequent mistake made by leaders. Therefore, bureaucratic organization is a formidable enemy for management, the source of every fault during the management process and the source of wasteful consumption. Bureaucracy brings the enterprise’s management organization into failure.

To overcome bureaucracy, organization overlapping should be strictly avoided.

Reduce the number of assistants. Too many assistants are the root cause of bureaucracy. Due to too many assistants, the first leader will work by depending on assistants, who won’t go further and listen to reports. The first leader will just make decisions and command relying on reported information. Personnel will not truly report pros and cons of an issue since all this is connected to their responsibility, power, obligation, and interests so as to cause major leaders to make bureaucratic mistakes.

Overstaffing in an organization is the root cause of bureaucracy. It keeps major leaders away from practice, causing bureaucracy, which cannot be controlled by people’s will. Overstaffing in an organization is sure to cause excess employees, low work efficiency and productivity, and serious wasteful consumption.

Organizational power is generated when humans exploit and create consumption materials from nature; this encourages the fight between humans and nature, among human groups, and even among nations. Therefore, enterprise management should regard organizational management as the first priority of leaders.

Section 8 Consumption and consumption object management

The target consumer group of products will be managed

Before investing in production, the object of consumption for a product must be positioned. At the same time, the positioned object of consumption will be studied, with or without competitors, full competitors or non-full competitors, and then a study should be carried out to exploit or gain some direct consumers who are ready to consume the product. Meanwhile, you should study competition on the same type of products from other enterprises or replaceable consumption products. During the fierce competition process in the sales market, use consumer management to increase the loyalty of consumers for your products to enhance the sales volume and double the benefits of the enterprise’s consumption products.

Object of consumption during production process

All consumptions of the enterprise in creating new consumption commodities are included in the production process of the object of consumption. Only when all consumptions in the production process are transferred to a certain product, which is becoming a new commodity consumed by the direct consumer, can the value of production purpose be realized.

Consumptions during the production process include the consumption of subject of labor, the consumption of tool depreciation, the consumption of management expense, the consumption of labor expense, and the consumption of social environment expense. The selection of the object of consumption is important to determine consumption cost and product quality.

The selection of targeted consumers determines the consumption cost and quality of products. Disqualified raw materials, poor production instruments, and unskilled laborers would result in high consumption costs, poor products, and even poor operation, loss, or closedown of the enterprise.

Section 9 Enterprise object management

An objective has the power of appealing, attracting, and generating cohesion. It can mobilize every group related to the targeted interest. Therefore, any scientifically feasible target can generate the power of appealing, attracting, and generating cohesion (three forces). However, it will be guaranteed by strong and powerful organization.

Based on its operation targets, the enterprise decides its objectives in the near, medium, and long term, which are divided into high, middle, and low level objects. In this way, fulfillment of the objectives can be guaranteed and arrogance can be avoided. The meaning of designing the objectives of three stages: the first objective should be based on the current foundation, a higher objective that the team is confident to realize through hard work. Based on the first objective, the second objective task ascends to a higher level, which is possible to realize with hard work while the third objective task has an expectation value, with hope to realize.

In the process of ensuring the realization of the first objective, all employees are fully confident to realize the objective with hard effort. Without the power of appealing, attraction and cohesion, arrogance will appear and negative factors will be induced, which is unfavorable to enterprise development and interests and the development of employees. Besides, this arrogance is an intrinsic ideological activity. When the objective at this stage is completed, leaders can smoothly shift the fighting force and collective enthusiasm to the second objective. In this juncture, the spiritual power of the team will smoothly transfer into huge material power to possibly realize the second goal if it is within the target period and there is time for forward development. Then leaders can channel team power to the third objective to strive for the realization of the third objective.

At the end of the season and year, we need to organize to summarize seasonal or yearly experiences and lessons and carry out relevant rewards to encourage advanced groups and individuals. However, the rewarding should be fair and justified. For this, excellent models should be fairly selected. We then reward these models to make them display exemplary force for moving everyone towards the new objectives. We should be careful to prevent unfair and unjustified praise and reward. The standard for rewarding should be performance based and these rewards will encourage everyone to follow. Or else, the realization of new objectives will be severely influenced.

Section 10 Consumption and the management of resource allocation

The enterprise production and operation management process are also a consumption process of resource allocation. Resource is an important objective used in enterprise management, which is also an integral element of the productivity of the consumption society. It includes laborers, capital, land, raw and supplementary materials, tools, technical processes, machinery equipment, product sales, models, time, information, solar power, air, wind, living environment, and other important resources.

The level of consumption and resources allocation management is closely related to the double benefits of the enterprise’s operational management, which is an integral indication of leadership capacity, leadership method, and the art of core leaders. While studying the development of the enterprise productivity in a consumption society, the enterprise leaders will first study enterprise resource, analyze its advantages and disadvantages, make the most of integrated advantages and overcome disadvantages, unleash the power of the organization, and organically create the best double benefits of the enterprise through systematic and integral management.

Section 11 Consumption and enterprise management mode

Consumption and management mode of productive enterprises

The management of a productive enterprise will be determined by the production mode, which is determined by the production purpose, production technology, and process and production tools. Since production purpose, production technology, and process constantly develop, and new production tools are constantly invented, the production mode should change constantly. Because of the constant change of the production mode, the management mode must change with the change of the production mode to adapt the development of productivity, or the development of productivity of the consumption society will be impacted and hindered. This is one of the important reasons why enterprise management is a topic of study.

For example, the management of the production mode of the family workshop is totally different from that of the intensive production mode of steam engine industrialization; the management mode of a labor-intensive production mode is different from that of a new high-tech intensive production mode; and the management mode of a general laborintensive production mode is different from that of an intelligent and automatic production mode.

Therefore, the management mode should be determined based on the actual production mode to make the management mode adapt to the production mode so that the maximum productivity of the consumption society can be displayed.

Sales management mode (including operating and selling enterprises)

Sales of the consumption commodity produced by enterprises

The management model of enterprise product sales will be determined by the objects of consumption of their consumption commodities and the supply–demand relations in the market.

When supply falls short of demand, the spot cash sales management model of a manufacturer’s via direct authorizations to the retail stores (supermarkets) or wholesalers is relatively simple, but the manufacturer will have close and friendly relationship with distributors since they replace the manufacturer to serve consumers directly. They serve and manage consumers – they complete sales on behalf of the manufacturer (under the pretext of guaranteeing their own interests).

The enterprise organizes sales itself. A large enterprise carries out the integration of research, development, production, and sales, and the internal operation of the enterprise during the selling process. Totally different from the first management mode, the management mode involves a group. Scientific research and the manufacturer adopt a workshop-style management. The overall management structure of the enterprise contains the front house (market) and back house (research and production) with the latter guaranteeing the supply–demand relations of the former. The sales market adopts a system of independent legal subsidiary. The group establishes head office for each sales market (sales department of group) to command enterprise planning and manage sales of various subsidiaries. Various provinces establish provincial offices to substitute for the corporation to be in charge of running the management of sales in each province and region, each subsidiary is in charge of management of regional and town offices. This is the leveled management system.

Sales management is the direct handing over of the product produced by the factory to the sales company for sale. Accounting disposal should be carried out first inside the group. The group company also adopts the accounting treatment for financial management of independent subsidiaries. Group enterprise should encourage internal trade among independent subsidiaries as a way to manage operations and sales. That is the marketing management mode of direct sales to consumers by subsidiaries and workshops.

The financial center of the group directly rules the financial management of subsidiaries all over China; product sales, collection and labor expenses should be managed by a central financial center. The deposit volume of various subsidiaries should be limited and the excess should all be remitted to the financial center of the group, adopting a centralized management mode. The finished product warehouse of the production factory establishes a second level warehouse management model, with the primary finished product warehouse established in the factory while the secondary product warehouses are kept in various provinces and regions. Direct management of the factory ensures the supply in the sales market. Sales cash from various offices and workstations should be deposited in the corporation’s designated accounts (only deposits are allowed; withdrawal is prohibited).

The aforesaid management ensures that the cash flow of 2,200 offices and 13,500 workstations of Sanzhu Corporation around China can enter the subsidiaries’ account at the right time, with cash turnaround as fast as 27 days. Meanwhile, the smooth development of the sales market and sales channel of the consumption commodity should be ensured. Rapid development of the promotion process greatly encourages productivity in the consumption society.

The management mode of product sales agents of productive enterprises