10

PLANNING AND CONTROL OF INVENTORIES

INTRODUCTION

A controller who is not familiar with the intricacies of inventory management may have a difficult time determining whether a company has an inventory problem at all, the nature of the problem, and how to fix it. This chapter solves these problems by describing all key aspects of inventory that a controller should be concerned with, including the costs and benefits of having inventory on hand; the various materials management systems and how they impact inventory; types of reordering methodologies; the impact of obsolete inventory on overall valuations, accuracy, and turnover; and how to budget for projected inventories in future periods. Only a thorough grounding in all of these areas will allow a controller to master the art of keeping inventory levels to a minimum without upsetting a company's customer service levels or its ability to produce to a predetermined production schedule.

COSTS AND BENEFITS OF CARRYING INVENTORY

This chapter deals with a wide range of issues dealing with inventory, to an extent that is greater than in other chapters dealing with other parts of the balance sheet. Why the hoopla? This section notes the many critical factors surrounding inventory, all of which a controller should keep in mind before making a decision that will change the mix or amount of inventory kept on hand.

First, what are the benefits of keeping inventory on hand? One is that it covers up mistakes in the production area. For example, if the production process is damaging parts that are being assembled, it makes sense to keep a supply of extra parts on hand to fill in for any shortfalls caused by damage to parts. Similarly, it is useful to keep inventory on hand if the supply of parts from suppliers is questionable, which is a common occurrence if a supplier has a track record of not delivering on time or in the expected quantities. Of course, it is also possible to solve the root problem in both cases and fix the reason for damage to parts or replace a supplier. However, these options may require a considerable amount of time; in the meantime, it is useful to keep inventory on hand to cover any problems that may arise.

Another reason for keeping a healthy level of inventory on hand is to meet the demands of customers. In particular, if there is a seasonal demand for a company's products, it makes sense to keep a considerable quantity on hand for those periods when regular production capacity cannot keep up with surging demand. It may also be necessary to keep extra quantities available if demand is not predictable and fluctuates broadly. In these cases, it is difficult to shave inventory levels to reduce working capital requirements, because there is a risk of losing sales.

These are good reasons for keeping inventory in stock; however, there are powerful reasons for keeping inventory levels down as much as possible. Even though it is not always mandatory to adhere to the following reasons for reducing inventory, a controller should at least pay close attention to them before approving of a change in inventory strategy that will lead to more on-hand quantities. The following reasons for not keeping inventory on hand are all related to cost:

- Building cost. Most forms of inventory must be stored indoors, so one must factor in the cost of either owning or leasing building space, which includes building maintenance, utilities, and taxes.

- Carrying cost. When inventory is purchased, a company must expend working capital, which is not free. The best way to determine the cost of working capital is to assume that the money could otherwise have been invested or used to pay off debt, so the interest cost of doing so is the cost of carrying inventory.

- Change control cost. Of particular concern to a company that undergoes frequent product redesigns is the cost of moving from old to new component parts. When this happens, there must be a clearly defined breaking point when the new part is used, resulting in the immediate obsolescence of the old part. If a company wants to avoid this type of obsolescence, it must carefully track inventory levels and switch to new parts only when inventory levels of old parts are at a low point. However, this type of close management requires additional staff time. No matter how the issue is handled, change control when inventory is present is expensive.

- Counting cost. Most companies still conduct a year-end inventory count, while others prefer ongoing cycle counts to ensure record accuracy. In either case, there is a cost associated with paying employees to count the inventory, which can be exacerbated by sometimes having to shut down the production facility in order to ensure an accurate count.

- Damage cost. The problem with having piles of inventory is that one must move it around a lot in order to get at the inventory that is currently needed; when doing so, it is easy to damage inventory. In addition, every time something is moved in or out of the inventory, there is a risk that it will be damaged. The greater the number of moves, the greater the risk of damage.

- Handling cost. Moving inventory requires a staff to do the moving. If there is a large amount of inventory, there must be a large staff to do the moving, frequently armed with forklifts or similar equipment to assist the moves. A large warehouse staff adds no value to the product, and consequently is nothing more than a wasteful addition to overhead costs.

- Insurance cost. There is a risk that inventory can be destroyed, so there should be an insurance policy that covers damage to it. Though the cost of this policy can be reduced by increasing the deductible, the deductible becomes a cost in the event of an insurance claim.

- Obsolescence cost. Inventory may become unusable over time, which is a considerable risk when there is a large amount of inventory on hand, and especially if a company is in an industry with high product change rates, such as the personal computer industry. In these cases, a large proportion of inventory may have to be thrown away or disposed of at a substantial discount.

- Pilferage cost. If there is inventory, someone may want to steal it, especially if it is a consumer article that is readily used by employees, or an extremely valuable item that can be easily converted into cash, such as consumer electronics or computer parts. By reducing the amount of inventory, there is less need to incur expenses to guard it, while there is also proportionally less inventory available to be stolen.

- Racking cost. Most forms of inventory do not just sit in piles on the warehouse floor. Instead, they are stored in an orderly manner in storage racks, which can be exceedingly expensive, especially if they must be strong enough to support a large amount of storage weight.

The above list shows that the costs associated with inventory add up to a substantial amount, so much that a controller must hesitate to support any kind of increase in the amount of inventory kept on hand. Yet, there are good reasons for keeping inventory in specific situations. How does one reconcile these issues? The best solution is to keep inventory only until systems can be fixed that allow a company to reduce the need for the inventory. System changes that will allow this include switching to a just-in-time (JIT) manufacturing system, using express delivery to avoid storage fees, and using drop shipping straight from suppliers to customers to avoid any in-transit storage by the company. In short, inventory is needed by most companies in the short term, but there may be options over the long term that will allow the amount of inventory to be reduced or even eliminated.

ROLE OF THE CONTROLLER

One of the underlying functions of a controller is to report on the operations of other departments. Due to this staff function, a controller usually does not take direct responsibility for the operations of the materials management function, but rather reports on its operation by a line manager. This section notes the variety of tasks in which a controller can be involved that relate directly to inventory. The tasks are outlined as:

- Create overall inventory policy. Though the controller must create policy in concert with other members of the management team, he or she has an opportunity to forcefully state the advantages of keeping inventory levels as low as possible, thereby reducing the risk of inventory obsolescence, scrap costs, warehousing costs, and the size of a company's investment in working capital.

- Verify that inventory records are accurate. A large part of the typical company's assets reside in the warehouse. A controller must verify that the inventory listed in a company's general ledger is actually stored in the warehouse. All of the following inventory information is subject to audit:

- (a) Overall accuracy. To audit overall inventory accuracy, one must print an inventory report that sorts inventory by location, and compare a sample of items from the report to the actual inventory. However, there may be inventory that does not show up on the report at all, and will therefore never be counted, so one must also pick a number of items at random from the inventory and trace them back to the database. The total number of errors resulting from this audit can then be divided by the total number of items inspected to determine the percentage of inaccuracy for the inventory.

- (b) High-dollar accuracy. A small inaccuracy in the amount of the most expensive inventory can have a major impact of profits, so a separate audit can review the accuracy of a large proportion of the high-dollar items in stock. This can even be an audit of virtually all high-dollar items.

- (c)No locations. Despite the most extensive searches, it is probable that there will be inventory that cannot be located. If so, the controller should regularly review a report that lists all inventory in the database for which a location code has not been assigned and determine the company's monetary exposure if that inventory does not exist.

- (d) Low usage. Low usage parts take up valuable warehouse space, and should probably be disposed of rather than kept on hand. A controller can easily determine the amount of low usage items simply by printing a list of inventory for which there has been no or low activity for a prespecified number of months.

- (e) Unusual costs. Most controllers tend to focus an excessive amount of energy on achieving perfect quantity accuracy, to the detriment of achieving equal levels of cost accuracy. One can avoid this difficulty by reviewing inventory reports that list the lowest and highest dollar unit costs in the inventory. Such reviews can spot items that have incorrect costs, resulting in massively high or low inventory values. This is a common problem when a part is assigned a cost based on a specific unit of measure, but someone changes the unit of measure, resulting in a vastly different cost. For example, a roll of tape may have a cost in the database that is based on the number of rolls of tape, but the engineering department then changes the unit of measure to inches, so that it can more easily enter tape amounts into bills of material. The result is an inventory value that is several thousand times higher than it really should be.

- Audit inventory controls. A controller must ensure that all current inventory controls operate in their intended manner, which helps to keep inventory quantities from diverging from their intended levels. This function can also be performed by a company's internal audit department, assuming that it is large enough to have one.

- Install control points. A controller has a considerable amount of knowledge regarding how to create controls for a variety of systems and situations; this knowledge should be turned toward creating controls that will ensure that inventory is only used for its intended purpose, and not scrapped or diverted for other purposes. These controls should also make it extremely difficult for anyone to illicitly remove inventory from the company.

- Supervise the annual physical inventory count. If the perpetual inventory system is not accurate, the controller must conduct a physical inventory count, which involves setting up counting procedures and supervising the counting teams that check all inventory quantities.

- Report on inventory costs. A controller's prime responsibility is to ensure that the reported cost of inventory is accurate. If it is not, the amount of the cost of goods sold will be inaccurate, which can lead to major inaccuracies in a company's reported levels of profit.

- Know how inventory management systems work. A controller must know how a company's inventory management systems operate, because the type of system used has a direct impact on the control systems needed, as well as the inventory levels needed to feed a company's production systems.

- Measure warehouse functions. The results of any audits of the inventory should be posted in a place where the warehouse staff can see them. The measurements should include the overall accuracy of the inventory, the accuracy of high-dollar items, the total number of items in stock and their total cost (in case there is a push to reduce the overall amount of inventory), and also the percentage of jobs that were fully kitted on time (which is used only if the warehouse is supplying a job shop production operation). These measures give the warehouse staff a complete knowledge of the most important operating results of the warehouse.

- Create inventory management policies and procedures.

- (a) Low-cost, high-usage items policy. All high-usage, low-cost items shall be removed from the inventory database and maintained in bulk on the production floor, using visual reorder systems. Exceptions must be approved by management.

- (b) Inventory accuracy policy. Whatever actions necessary shall be taken to ensure that inventory accuracy is maintained at a level of at least 95%, with a level of 98% for high-dollar items.

- (c) Measurement policy. The controller shall provide warehouse performance and status measurements to the warehouse staff on a weekly basis.

- (d) Purchase quantity policy. Items shall be purchased only for immediate production needs. Blanket purchase orders shall be used whenever possible to assist in reducing the paperwork requirements of this policy.

- (e) Obsolescence review policy. The materials review board shall review the inventory database for obsolete items no less than once a week. All items that have not been used within the last 12 months shall be disposed of, unless approved by management.

- (f) Inventory disposition procedure. All items that have not been used in the last 12 months shall be considered obsolete. Of this group, all items with an extended cost of $50 or less shall be thrown out or donated, with no approval required. If the extended cost is between $50 and $500, the purchasing department shall first attempt to return it to a supplier, after which it may be thrown out or donated with no additional approval. Items with an extended cost exceeding $500 shall be disposed of only with the prior approval of the vice president of materials management.

Given the length and breadth of the discussion in this section, it is obvious that a controller can take a very large role in the management control and review of inventory. This sort of activity is normally welcomed by personnel in the materials management function, because the upshot of these activities is better control over inventory, which leads to reduced time by the materials management staff in looking for missing parts, making rush orders, and other unnecessary activities.

MATERIAL REQUIREMENTS PLANNING SYSTEMS

As noted in the “Role of the Controller” Section, a controller should be well grounded in materials management techniques, in order to know how to make recommendations to improve inventory tracking systems, as well as how to reduce inventory levels to save working capital and other costs. This section provides a brief overview of the most common materials management system, which is material requirements planning, or MRP.

There are two types of MRP. One is material requirements planning, and the other is manufacturing resource planning (MRP II). The first variety is concerned solely with inventory management, whereas MRP II is a more sophisticated version that also controls direct labor and machine usage. We will confine this discussion to MRP, since it is concerned only with the primary focus of this chapter—inventory. Material requirements planning uses several key databases in the manufacturing system to predict when inventory is needed for the production process. Its purpose is to form an orderly flow of parts to the production department, thereby ensuring that there will be no production stoppages due to parts shortages. When properly used, it can also keep inventory levels down, so that the working capital investment in inventory is minimized.

An MRP system works with three databases. The first is the production schedule. It takes the quantities and due dates on the production schedule for each product and multiplies it by the second database, which is the bill of materials for each product. The result is a list showing the quantities of parts needed for production, as well as their due dates. The system then compares the parts list to the on-hand inventory, to determine which parts are already in stock. Any parts that are not currently in stock or on order are then ordered, which can be done either manually or automatically by the MRP system, with the option of a manual review by the purchasing department. A final feature is that the purchase dates are based on the purchasing lead times required by each supplier, so that amounts ordered will arrive just when needed. In short, an MRP system combines the most common production databases to achieve timely delivery of a sufficient number of parts to complete the production schedule.

A controller should be aware of the various advantages and disadvantages of using an MRP system. One problem is that it is highly dependent on a large amount of computing power; the system must recalculate the purchasing schedule at least once a week, which can take many hours of processing time, even with today's super-fast computers. Another issue is that the system's results will be incorrect if the underlying databases contain incorrect data. For example, incorrect information in the bill of materials will result in parts overages or shortages on the production floor. Also, an MRP system allows for purchasing parts in economic order quantities, which means that not all parts ordered will be used at once. This opens the door to the possibility of having unused and obsolete inventory. However, MRP is an excellent way to gain control of a materials management process, ensuring reasonable inventory levels and the efficient marshaling of resources to ensure that products are produced on time.

By being aware of the inner workings of an MRP system, a controller can make recommendations to senior management regarding the need to have such a system, or to make modifications that will result in reduced inventory levels.

JIT MANUFACTURING SYSTEMS

Though JIT manufacturing is widely praised in the press for its ability to streamline entire organizations, improve delivery times, and shrink inventory levels, surprisingly few companies use any of its elements, let alone the entire range of JIT applications. Perhaps a greater understanding of JIT is needed to spur its deployment. Accordingly, this section gives a brief overview of the components of JIT and the impact it can have on inventory levels.

Many of the basic factors involved in good inventory management have been briefly reviewed, but a key one yet to be discussed is the inventory and production system the management has chosen to use. None has drawn more attention recently than the just-in-time inventory system. The controllers may have little voice in which system is selected by the manufacturing executives. But they should be generally aware of the central philosophy—which basically is that all inventories are undesirable and should be eliminated or minimized—and the impact on purchasing and delivery systems, as well as the manufacturing system itself.

Adopting the just-in-time system requires major changes in purchasing and manufacturing strategies. In purchasing, the JIT system requires the manufacturers to select a few reliable suppliers who deliver, when needed, dependable materials and component parts with zero defects. The JIT manufacturing function is characterized by smaller lot sizes than traditional manufacturing, fixed production schedules for shorter periods, possible machine and process reconfiguration, as well as automation and a more flexible or multifunction workforce.

The objective of a JIT system is to produce and deliver:

- Finished goods just in time to be sold

- Subassemblies just in time to be assembled into finished goods

- Fabricated parts just in time to be made into subassemblies

- Raw materials and purchased parts just in time to be converted to fabricated parts

JIT has been described as a “pull” system of production control wherein the final assembly line production schedule triggers the withdrawal of materials or required parts at the needed time from the work centers that precede them in the manufacturing process. Workers secure the right quantity of parts to complete an order. Sequentially, each work center supplies parts to the next manufacturing operation and then manufactures parts to replace them. Thus, there is no stockpiling of work-in-process to offset lead times or to meet safety stock levels or the economic order quantities of subsequent production functions. (See the later discussion.) The results of this system are:

- Lower inventories and lower carrying costs

- Reduced rework and scrap

- Improved quality control

- Shorter production time and lead time, which assists the next result

- Increased productivity

JIT Purchasing

A successful JIT system depends, in the first instance, on a few reliable and dependable suppliers who maintain a very close buyer-vendor relationship. JIT manufacturers enter into long-term contracts with fewer suppliers. Moreover, the suppliers handle smaller lot sizes, and use statistical quality control techniques to improve the quality of their products (rather than after-the-fact inspection). The suppliers essentially become specialized makers to the manufacturers, with facilities close to the JIT manufacturer's plant, so as to make easier delivery of their products; and they are involved with the manufacturer in the product design and manufacturing process from the very outset.

The controller should be involved in the following special issues regarding JIT purchasing:

- Target Costing. The controller must include projected product costs in the budgeting process. Under the JIT concept, there is more opportunity to influence product costs during the design process than later, in the manufacturing process. Thus, the controller should be involved in setting a target product cost and assigning targeted subsidiary part costs to suppliers. Based on this targeted cost information, the controller can prepare the material cost budget.

- Collusion with Suppliers. Another accounting issue involving JIT purchasing is the possibility of collusion between buyers and suppliers. Since JIT precludes competitive bidding, it may be possible for buyers to select suppliers who will kickback profits to the buyers in exchange for the business. This problem is real, but is mitigated somewhat by the amount of interaction between company employees and the supplier. The product design function under JIT purchasing requires that the company's design engineers work closely with suppliers, so these people should recognize a sham supplier. A control that the controller can use is to compare supplier prices against those of the market on a spot basis. If prices seem excessive, then the controller should investigate further. Also, the controller can investigate whether or not previously agreed part price changes (usually downwards, for JIT suppliers) have taken place.

- Purchasing Paperwork. JIT purchases tend to occur frequently and involve small part quantities. Under a traditional accounting system, this would present an increased paperwork problem, for there would be more receiving documentation to match to more invoices, and more checks to cut. Consequently, the controller should consider recording receipts based on the number of parts used in production (based on bills of material), plus parts that were damaged at the fault of the buyer. This system would require very accurate bills of material.

- Supplier Rating Systems. Before JIT, suppliers ratings were based on the average unit price of parts sold to the company. Under the JIT philosophy, suppliers ratings should include ability to attain part cost targets, percentage of parts arriving on time (“on time” also means “not arriving too early,” for such materials must be moved and stored, creating problems for the buying company), part defect rates, and the percentage of shipments containing the exact amounts ordered. The controller should be involved not only in the design of these information gathering systems, but also in the auditing of them for accuracy.

- Buyer Measurement Systems. Before JIT, buyer ratings were based on the cost savings achieved from a standard cost for a part. JIT purchasing requires buyers to be facilitators rather than clerks, so that their new jobs require coordinating design teams from the two companies, assisting in qualifying suppliers, and shrinking the supplier base. Under JIT, continuing to judge a buyer based on the purchase price variance would be dysfunctional, since the buyer would be forced to put parts out to bid for the lowest price instead of working with one supplier to achieve a targeted cost. The controller should point out such dysfunctional performance measures to management, and recommend that they be eliminated. New performance measures for buyers are difficult to derive for individual buyers. Instead, the controller should consider formulating performance measures for groups, such as new product design teams that include buyers. A typical performance measure under this scenario would be achieving a product's cost that was originally targeted by management.

JIT Delivery

JIT manufacturers closely link their production schedules to the suppliers' delivery schedules. Hence, suppliers and manufacturers are not only relocating, they are also eliminating storage areas and loading docks where delivered material can accumulate. Suppliers may feed materials and parts directly to the assembly lines.

JIT Manufacturing

As would be expected, with the emphasis on small rather than large lot sizes, changes in manufacturing processes and machine arrangements usually are necessary. Under the typical U.S. production line, similar machines performing similar tasks are grouped together. This supposedly increases labor efficiency as well as the economy of large lot size production. Under the JIT system, “group technology” is used so that the small lot work moves rapidly through a common routing over several different types of machines. Hence there is little need for work-in-process inventory.

Moreover, rather than performing the task on only one machine, the worker is trained to operate all the machines of the work center. This leads to less boredom and assists in reducing defects, which, in the process, can be identified rather quickly.

For group technology to work, employees must be heavily cross-trained in the use of several pieces of equipment, since one employee will typically operate several machines. Also, since the company must invest in employee training, the cost of losing an employee is higher than would be the case in an assembly line environment, where less training is required. Finally, the employees must be willing to take responsibility for the quality of products produced; since an entire product can be produced by one employee or work group using group technology, part defects can be directly traced to individuals.

It is beyond the scope of this volume to discuss in detail the many operational aspects of just-in-time inventory planning and control. However, a review of one company's experience relative to purchased assemblies will give a good example of the pervasive impact that a JIT system can have on traditional financial controls. In this illustration, a high-cost subassembly is purchased from a single supplier with a long time association and under a long-term contract. There is one such assembly in each finished product. Each day all assemblies needed for that day's production are delivered at 8:00 A.M. A routine was established between the supplier and the manufacturer whereby the supplier was paid weekly based on the number of finished products shipped by the manufacturer that week.

This procedure eliminated the preparation and handling of purchase orders, receiving reports, inventory details (receipts and disbursements), and invoices—the new control being that if a product were manufactured, tested, and shipped, then the subassembly must have been delivered. This is a very different process from the usual matching of purchase orders, receiving report, and invoice in order to effect payment.

Just-in-time concepts strongly impact several accounting processes, reports, and performance measures. The controller should be aware of the following items:

- Product cost tracking. Under traditional assembly line production techniques, there were many opportunities to reduce product costs by closely examining the production process. However, with JIT, the glaring cost issues (e.g., excessive scrap and inventory levels) are eliminated from the production process. The controller may find that cost tracking systems on the production floor are not revealing cost savings. In fact, the tracking systems may cost more than the savings they generate. Consequently, the controller should consider cutting back on cost tracking systems on the shop floor and turn more attention to how well in-house and supplier design teams are achieving targeted cost goals when creating new products.

- Direct labor cost tracking. Traditionally, accountants have closely tracked all direct labor variances with the help of extensive shop floor labor reporting. However, in many companies, direct labor now accounts for less than 20 percent of a product's cost, so the cost expended to track direct labor may not be worth the benefit gained by reviewing labor variance reports. Therefore, the controller should consider eliminating direct labor reporting.

- Accounting reports. Most accounting reports are issued after the end of the month. Line managers review them and take action sometime well into the following month. With JIT operations, there is no work-in-process buffer to hide manufacturing problems, so line managers can spot most problems within minutes or hours of their occurrence. In short, JIT manufacturing personnel do not need monthly accounting reports as much as they used to. As JIT is implemented, the controller should periodically meet with line manager to ascertain their need for the information. The likely result will be fewer reports.

- Operational auditing. Under assembly line systems, operational audits focused on sources of waste from the system, such as pilferage, obsolete inventory, and scrap. With the greatly reduced inventory levels used by a JIT system, auditors must now shift their focus to issues that will slow down JIT, such as problems with setup time reductions, process flow and workstation designs, and product designs.

- JIT performance measures. Under assembly line systems, performance measures related to variances for direct labor and materials. With the assumptions under a JIT system that direct labor and materials costs are fixed and will have few variances, performance measures should shift to attaining targeted output and quality goals, the number of employee suggestions received, and the percentage implemented.

- Cost generators. Under assembly line systems, cost generators were viewed as direct labor and materials. With the assumptions under a JIT system that direct labor and materials costs are fixed, the controller should target other items. For example, close attention should be paid to:

- Engineering change orders, which can slow the product release process

- Space utilization, since excess space should be sublet for additional revenues

- Inventory levels, since less inventory leads to less space requirements, fewer obsolete items, less inventory tracking time, and reduced insurance costs

- Equipment downtime, since product ship dates cannot be achieved if production facilities are not functioning

Though this description of a JIT system may lead one to believe that it is entirely different from the previously described MRP system, it is possible to transition from MRP to JIT in an orderly manner. Because a JIT system requires a minuscule amount of inventory, the underlying management principle needed to bring about this transition is an alteration in purchasing policy. A traditional policy under the MRP system is for a company to purchase inventory in those quantities that minimize inventory carrying and ordering costs, which usually results in excess quantities of inventory on hand. The controller must convince management that the more appropriate technique is to purchase only the exact amounts required, which leaves no excess to be stored in inventory. By choking off the flow of incoming inventory, the warehouse and purchasing staffs can then concentrate on gradually reducing the remaining inventory stocks by a variety of means, such as donations, throwaways, and returns to suppliers. Over time, this approach will drastically reduce the inventory to the point where this aspect of a JIT system has been achieved.

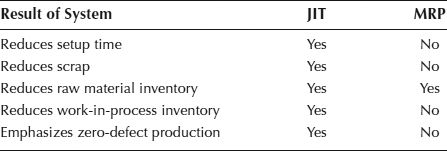

EXHIBIT 10.1 COMPARISON BETWEEN JIT AND MRP SYSTEMS

If management does not feel that there is any reason to transition from an MRP system to a JIT system, a controller can present them with the information in Exhibit 10.1.

Exhibit 10.1 shows that MRP is deficient in a number of areas, which may spur management into making a change away from MRP. However, if there is still some hesitation in moving away from an existing MRP system, it may be possible to effect a partial transition by slowly adding JIT features, such as cellular manufacturing groups and reduced setup times, which work well in either operating environment.

In short, JIT principles can effect a drastic reduction in the amount of inventory a controller must contend with, while also improving product quality and the reliability of delivery times to customers. It is a system well worth implementing, either totally or in part.

INVENTORY REORDERING SYSTEMS

The type of inventory reorder system should be of great concern to a controller, because the wrong method can greatly increase the amount of inventory on hand. This section presents a list of reordering methods, shown in declining order of desirability, with the first one resulting in the smallest amount of inventory on hand, and the last one the largest. The first method, JIT, requires the greatest attention to management systems, while the last is a simple approach that can be easily installed with minimal continuing supervision, which is perhaps why the last approach is the one most commonly used in practice. The reordering systems are:

- JIT. This method requires a company to issue a request for the immediate delivery of parts to a supplier as soon as it needs the parts in the production process, with the supplier immediately delivering the exact amount required to the production line. Although this appears to be an elegantly simple approach, it actually requires great attention to the accuracy of bills of material, as well as the selection of suppliers and the quality of incoming goods. It results in almost no on-hand inventory (with the exception of work-in-process), and is therefore the best reordering system from the perspective of reducing a company's investment in inventory.

- MRP. This method calculates the exact amount of inventory needed for scheduled production, based on bills of material, the production schedule, and existing inventory levels. The computer system then generates a recommended ordering level, which is executed by a purchasing person. This is an excellent ordering method, but can result in too much inventory if the ordering levels are supplemented by an economic order quantity, which may result in too much inventory being purchased.

- Visual check system. This method is a simple check of stocking levels, with reordering taking place based on the knowledge of the checker of the movement of each inventory item. A more modern variation is to mark lines on storage bins; reordering takes place as soon as inventory falls below the lines. Another variation is to have two storage bins for each item; reordering takes place when the larger, main storage bin is empty, while the smaller emergency bin is used until the reordered amount arrives. This is a good approach for the reordering of large-volume, low-cost items that are otherwise difficult to track, such as fittings and fasteners.

- Reservation method. This method recognizes the available stock as well as the physical stock. Available stock is defined as stock on order, plus physical stock, less the unfilled requirement. The reorder point is based on the available stock rather than the physical stock.

- Minimum–maximum. A very common means for reordering inventory is to use the “minimum–maximum” system, or “MinMax.” The minimum is the lowest acceptable amount of inventory that should be kept on hand, while the maximum is the highest acceptable amount. The minimum represents a margin of safety, while the maximum is usually the minimum level plus the standard ordering quantity. As a general rule, the use of a MinMax system is practical where the rate of sale or use of products is fairly stable and not subject to wide fluctuations or sporadic movements and where the order time is fairly short. However, it is based on a historical view of inventory data and can become inaccurate over time as usage rates vary. For this reason, it is generally inferior to a forward-looking system, such as material requirements planning.

The best way to still have an operational MinMax system while keeping the inventory investment low is to modify the “min/max” report so that it also shows the time period since a part was used, and its usage volume during the past 12-month period. If the computer system contains information from previous years, this can also be included, so that the report notes any trends in item usage. This additional information can be used by the purchasing staff to modify the minimum and maximum levels “on the fly,” so that the figures are constantly trimmed to match actual usage. Without this additional information, the minimum and maximum levels for each part will probably be adjusted only once every few years, which may lead to significant shortages or surpluses of parts. Thus, modifying the “min/max” report to include usage information allows buyers to change the preset ordering levels to match actual usage.

As companies place more and more emphasis on reducing their working capital investments in inventory, the reorder point system will come under more attack. This is because it is based on prior usage, not expected usage. Any reorder system based on what has happened in the past may very well result in orders for inventory items that have declining usage, resulting in excess inventory. The controller should regularly review the usage trends for those parts that are reordered with reorder points, and also correspond with the engineering department to see what parts are to be discontinued. Any part that is to be excluded from future products should immediately have its reorder point removed from the computer system, which will keep a company from ordering more of it when it is no longer needed.

In this section, the pros and cons of various inventory reordering systems, with a particular emphasis on their impact on inventory levels, were discussed. A controller who cares about a company's overall inventory investment would be wise to pay close attention to the types of reordering systems currently in use.

OBSOLETE INVENTORY

A controller should be deeply concerned with the extent and cost of obsolete inventory, because it can have a dramatic effect on a company's profits. Accounting rules state that the value of all obsolete inventory shall be written off as soon as it is identified, so a controller should always have current information on the state of this portion of the inventory. This section describes how to obtain information about obsolete inventory, as well as how to track down the causes of obsolescence and eliminate or at least reduce them.

The easiest way to determine whether a part is already obsolete or heading in that direction is to create a report that extracts the last usage date for a part from the production or inventory databases. This extracted information can then be sorted by date, with the oldest parts appearing at the top of the report. It is then a simple matter to review this list with the engineering staff to see which of the old parts are not going to be used again. These old parts can also be sorted by extended dollar value and totaled, providing an easy calculation of the total amount of obsolete inventory that a controller must write off on the financial statements.

An additional approach for determining whether a part is obsolete is reviewing engineering change orders. These documents note those parts being replaced by different ones, as well as when the changeover is scheduled to take place. One can then search the inventory database to see how many of the parts that are being replaced are still in stock, which can then be totaled, yielding another variation on the amount of obsolete inventory on hand.

A final method for determining the amount of obsolescence is to run a “where used” report, which is a common one when a computer system contains a bill of materials for each product a company produces. The report lists all of the products for which a part is used. If the report lists parts for which there are no product uses, then those parts can be considered obsolete (unless they are new parts being purchased for a new product that does not yet have a bill of materials in the system). To be absolutely certain of a part's status as being obsolete, it may be possible to use all three methods to derive three lists of obsolete parts, which can then be reviewed with the engineering staff periodically to determine which parts are truly obsolete. In truth, because of the overwhelming workload of the accounting and engineering departments, it is most common to simply run the first report, showing those parts with the longest period since use, and record those items as obsolete. The preferred approach, however, is to use all the methods, thereby avoiding the disposal of some inventory for which there may still be a use.

No matter what approach is used to identify obsolete inventory, it is uncommon to rely only on reports to verify that something is obsolete. Instead, the reports should be examined by a group of people who represent several departments and are authorized to throw out inventory. This group represents the engineering, accounting, production, and materials management departments, and is commonly known as the Materials Review Board (MRB). The group is tasked with not only throwing out obsolete inventory, but also examining parts that are suspected to be defective, and authorizing either rework, scrapping, or the delivery of parts back to suppliers for replacement or credit. The MRB must decide, based on visual inspection, if something is truly obsolete.

Although a controller may believe that it is only his or her responsibility to identify obsolete inventory, it is better to provide some value to the company by going a step further and tracking down the causes of obsolescence, so that they can be reduced or even eliminated. This extra step can eliminate a great deal of expense. The primary issues causing obsolescence are:

- Excessive purchasing volumes. The purchasing department may be purchasing in very large quantities, in order to save itself the trouble of issuing a multitude of purchase orders for smaller quantities, or because it can obtain lower prices by purchasing in large quantities. This problem can be avoided by attaching purchasing performance goals to minimal on-hand inventory, and can be verified by continuing reviews by the internal audit staff.

- Inadequate bills of material. A well-run purchasing department will use bills of material to determine the parts needed to build a product, and then order them in the correct quantities. If the bill of material is incorrect, then the items purchased will either be the wrong ones, or the correct ones but in the wrong quantities. To avoid this problem, the bills of material must be audited regularly for accuracy.

- Low inventory turnover. If there is too much inventory sitting in the warehouse, it will take so long to work through it that some of the inventory is bound to become obsolete before being used. This is partly the fault of the purchasing staff (see previous point), but may also be caused by a conservative production manager who wants to have enormous volumes of all parts kept on hand, so that there is no chance of a stock-out occurring that can interfere with the smooth completion of production goals. Attaching a high inventory turnover target to the goals of the production manager can reduce this problem.

- Poor engineering change control. If the engineering department does not verify that old parts are completely used up before installing a new part in a product, the remaining quantities of the old part will be rendered obsolete. This can be a major source of obsolescence. To avoid it, there should be tight control over using up old parts first, which can be verified by the internal audit staff and enforced by top management.

- Poor inventory tracking systems. It is easy for a part to become obsolete if no one knows where it is. If it is buried in an odd corner of the warehouse, there is not much chance that it will be used up. To avoid this problem, there should be location codes in the inventory database for every part, along with continual cycle counting to ensure that locations are correct. A periodic audit of location codes will give management a clear view of the accuracy of this information.

If a controller can identify any of the above problems as being the cause of obsolescence, quantify the cost of the problem, and aggressively push for changes, there can be a very significant cost savings.

Many companies that have not reviewed their inventories for a long time will find that obsolescence is a much larger problem than they would care to believe. It is not impossible for an older company to find that 80 percent of its inventory is obsolete. One can look upon such a problem as a major opportunity, because a company can write off a very large amount and reduce profits, thereby avoiding paying taxes. However, highly leveraged companies are probably using their inventories as collateral for loans and will face a reduction in the amount of debt that creditors are willing to lend if the amount of inventory is reduced; in these cases, it is best for a company to embark on an intensive campaign of inventory returns to suppliers, so that it can realize as much cash as possible from the disposition of inventory. Thus, obsolescence can have a major impact on a company's tax and debt situation.

REDUCING INVENTORY

A controller may be faced with suspected inaccuracies of unknown size in a company's inventories. If the number of items in stock is minor, then this problem is an easy one to correct—enroll a group of counters and descend on the warehouse for a few hours of counting. However, there are usually many parts, frequently scattered throughout the facility, which are improperly identified (if at all). In these cases, a controller is faced with a serious problem, since any significant inaccuracy has a direct impact on the cost of goods sold and profits. This section briefly describes the tasks a controller can complete in order to reduce the chore of counting inventory, which essentially means reducing the amount of inventory to count.

The best way to reduce the work associated with reviewing the accuracy of a perpetual inventory's cost is to reduce the size of the perpetual inventory. This can be done by using JIT manufacturing techniques. This involves moving goods straight from the supplier to the shop floor, thereby avoiding the warehouse entirely. To bypass the warehouse, these shipments must be in small enough quantities to avoid the storage of excess amounts in the warehouse, and they must arrive precisely on time to avoid storage until they are needed in the production process. If these two criteria can be met, the quantity of goods stored in the warehouse can be limited to those items that must be ordered in bulk and those items that are delivered too early to be immediately used by the production department. The result for the controller is a minimal inventory quantity to audit, cost, and report on.

Another important consideration in establishing sound inventory management is the standardization of materials and products and the simplification of the line. Simplification is merely the elimination of excess types and sizes. The elimination of those items that do not sell readily can contribute greatly to reducing the inventory which must be carried. Simplification is labor-intensive once inventory has been received, for considerable effort is needed to sell off excess inventory and ship it out of the warehouse. Less work is required if simplification is treated as a key step in designing new products, so that existing parts are used, rather than stocking new parts that may become obsolete.

Standardization is a more general term having to do with the establishment of standards. In the application to inventories, it has reference to the reduction of a line to fixed types, sizes, and characteristics that are considered to be standard. The object is to reduce the number of items, to establish interchangeability of manufactured parts and products, and to establish standards of quality in materials. With a reduction in the possible number of inventory items to be carried, the control problem is facilitated. Standardization extends even to such insignificant items as fasteners. If similar products can be designed to be assembled with a single bolt instead of ten slight variations on the same bolt size and material, then nine items can be eliminated, and no longer have to be tracked. Every time an item is removed from inventory, cost is reduced in the areas of cycle counting, obsolescence reserves, insurance, material moves, kitting, and receiving.

A more efficient inventory tracking system can be achieved if all obsolete inventory is removed from stock. The reason for improved efficiency when this happens is that a considerable amount of cycle counting is required to maintain a perpetual inventory. If some of the inventory is deleted, there is less inventory left to cycle count, resulting in a more accurate inventory with less counting effort by the staff. The controller should be aware, however, that overall inventory accuracy may initially decline if obsolete inventory is removed from stock; the reason for this decline is that obsolete inventory represents the most stable part of the inventory (since it is never used). By removing it, the usage level (and therefore the volatility) of the remaining inventory will increase, resulting in reduced initial levels of accuracy.

One of the major inventory-related problems for a controller is subtracting the value of consignment stock from inventory. This is inventory that is owned by another entity (e.g., a supplier or customer) and therefore cannot be included in the company's inventory valuation. Because this inventory may have the same appearance as inventory that is owned by the company, the best solution is to immediately store the consignment stock in a segregated area as soon as it is received. The other problem with consignment inventory is identifying it when it first arrives on the receiving dock. If the controller enforces the use of purchase orders for all receipts, then either the lack of a purchase order or its identification on a special purchase order should be sufficient to identify the consignment stock. If this separate storage requirement is enforced, the accuracy of the physical inventory's extended cost will be greatly improved.

A final method for reducing the amount of inventory to count is to shift as much inventory as possible to the shop floor and expense it as shop supplies. This approach works very well for fittings and fasteners, which are typically of low cost as well as being difficult to count. The approach has an added benefit of making it much easier for production personnel to access the parts, which not only improves employee morale, but also reduces the amount of materials handling, because there are fewer materials to move to the production facility.

There are a number of approaches for reducing the amount of inventory that must be counted. By segregating consignment stock, eliminating obsolete inventory, moving small parts to the shop floor, and using JIT systems, a controller can drastically reduce the inventory counting chore.

INVENTORY CUTOFF

One of the most common problems for a controller is not obtaining a proper period-end cutoff of inventory. The problem stems from receiving inventory while not recording a corresponding account payable. Without the payable amount being listed in the accounting records, inventory will be overstated, resulting in an understated cost-of-goods-sold figure, which yields an inordinately large profit number. The reverse problem of recording a payable before inventory is recorded is also possible but uncommon, because suppliers tend to send invoices after the shipment of goods, resulting in the inventory arriving first and being recorded first. If this cutoff problem is not properly dealt with at the end of each reporting period, a controller may end up reporting incorrect profit figures, which can lead to the hiring of a new controller.

How can a controller avoid the cutoff problem? The answer is a simple one, but the execution of the solution is not that simple, because it requires absolutely rigid adherence to an established receiving procedure, as well as the construction and implementation of a computerized matching system. If the procedure and computer system are not adhered to, there will continue to be cutoff problems, no matter what other solutions a controller may attempt to implement.

The solution to the cutoff problem is the proper maintenance and use of a receiving log. If the receiving staff religiously and accurately logs all incoming materials into the receiving log, the controller has an excellent tool for comparing accounts payable to receipts, which effectively solves the cutoff problem. For example, a controller can take all incoming invoices that have arrived near the end of the month and manually compare them to the receiving log, to see when items were actually received. If an item was not received until the beginning of the next reporting period, then the corresponding supplier invoice should also not be recorded until the following reporting period. The log can also be used to determine whether any supplier invoices have not been received at all, simply by matching every receipt in the log to an invoice. If there is no invoice, the controller can accrue for the expected amount of the supplier billing. One problem with using a receiving log is that it must be totally accurate—it must include the exact amount received, identify from whom it was sent, and note the correct date of the receipt. It is also important that the items noted as being received in the log are also recorded in the inventory database on the same date and in the correct quantities; otherwise, all of the work performed to match invoices to the receiving log will be in vain, because an inaccurate inventory database will still result in incorrect period-end inventory numbers. Given these problems, an accurate receiving log is still the best way to attain an accurate period-end inventory cutoff.

The trouble with manually matching supplier invoices to the receiving log is that it is manual—the controller must expend a respectable amount of accounting staff time on the matching process, which can interfere with the timely completion of financial statements (which are dependent on the completion of the cutoff analysis). However, it is possible to use automation to avoid nearly all of the matching work. To achieve this, the receiving log must be on-line, not a written document, so that the receiving staff enters information into a database that can then be compared to supplier invoices, which must also be entered into the database in a timely manner. If the receiving log includes a company purchase order number that was used to purchase materials, this number can be used as an index to compare receipts to invoices (which should also note the purchase order number). This automated cross-reference can be performed automatically by the computer, which can then print out a list of receipts for which there are no invoices, as well as a list of invoices for which there are no receipts. The only manual labor is to then review this list and determine whether the information is accurate. If it is, the accounting staff can make accruals that will result in a perfect match of receipts to invoices. Thus, the use of automation and the receiving log will give a controller excellent control over the period-end cutoff problem.

The solution to the cutoff problem seems simple; it is easy for it to fail, however, because there are always situations that will result in the incorrect recording of information, usually in the receiving log, that will alter the period-end inventory results. For example, a new receiving person who has not been properly trained may not enter information into the receiving log properly. Also, an overwhelmed receiving department may not enter receipts into the receiving log for several days, which may result in incorrect inventory balances. Also, there may be special situations, such as the receipt of consignment inventory that the company does not own, that are recorded improperly. For all of these situations, the best method of detection is to employ a company's internal audit staff to conduct an ongoing review of receiving procedures, to determine where problems are arising. Other types of fixes are to periodically retrain the receiving staff, provide extra receiving staffing during periods of high transaction volume, and produce clear procedures for the receipt of all possible items. Only by implementing all of these error checking and error prevention methods will a controller avoid period-end cutoff problems.

BUDGETING FOR RAW MATERIALS

There are basically two methods of developing the inventory budget of raw materials, purchased parts, and supplies:

- Budget each important item separately based on the production program.

- Budget materials as a whole or classes of materials, based on selected production factors.

Practically all concerns must employ both methods to some extent, although one or the other predominates. The former method is always preferable to the extent that it is practicable, since it allows quantities to be budgeted more precisely.

Budgeting Individual Items of Material

The following steps should be taken in budgeting the major individual items of materials and supplies:

- Determine the physical units of material required for each item of goods to be produced during the budget period.

- Accumulate these into total physical units of each material item required for the entire production program.

- Determine for each item of material the quantity that should be on hand periodically to provide for the production program with a reasonable margin of safety.

- Deduct material inventories that are expected will be on hand at the beginning of the budget period to ascertain the total quantities to be purchased.

- Develop a purchasing program which will ensure that the quantities will be on hand at the time they are needed. The purchase program must give effect to such factors as economically sized orders, economy of transportation, and margin of safety against delays.

- Test the resulting budgeted inventories by standard turnover rates.

- Translate the inventory and purchase requirements into dollars by applying the expected prices of materials to budgeted quantities.

In many instances, it is the controller's staff that translates the unit requirements and balances into values, based on the data received from production control or purchasing, and so on. In some cooperative efforts, the accounting staff may undertake the entire task of determining quantities and values, based on computer programs agreed to by the manufacturing arm (the explosion of finished goods requirements into the raw material components, etc.).

In practice, many difficulties arise in executing the foregoing plan. In fact, it is practicable to apply the plan only to important items of material that are used regularly and in relatively large quantities. Most manufacturing concerns find that they must carry hundreds or even thousands of different items of materials and supplies to which this plan cannot be practically applied. Moreover, some concerns cannot express their production programs in units of specific products. This is true, for example, where goods are partially or entirely made to customers' specifications. In such cases, it is necessary to look to past experience to ascertain the rate and the regularity of movement of individual material items and to determine maximum and minimum quantities between which the quantities must be held. This necessitates a program of continuous review of material records as a basis for purchasing and frequent revision of maximum and minimum limits to keep the quantities adjusted to current needs.

Budget Based on Production Factors

For those items of materials and supplies that cannot be budgeted individually, the budget must be based on general factors of expected production activity, such as total budgeted labor hours, productive hours, standard allowed hours, cost of materials consumed, or cost of goods manufactured. To illustrate, assume that the cost of materials consumed (other than basic materials which are budgeted individually) is budgeted at $1,000,000 and that past experience demonstrates that these materials and supplies should be held to a rate of turnover of five times per year; then an average inventory of $200,000 should be budgeted. This would mean that individual items of material could be held in stock approximately 73 days (one fifth of 365 days). This could probably be accomplished by instructing the executives in charge to keep on hand an average of 60 days' supply. Although such a plan cannot be applied rigidly to each item, it serves as a useful guide in the control of individual items and prevents the accumulation of excessive inventories.

In the application of this plan, other factors must also be considered. The relationship between the inventory and the selected factor of production activity will vary with the degree of production activity. Thus a turnover of five times may be satisfactory when materials consumed are at the $1,000,000 level, but it may be necessary to reduce this to four times when the level goes to $750,000. Conversely, it may be desirable to hold it to six times when the level rises to $1,250,000. Moreover, some latitude may be necessitated by the seasonal factor, since it may be necessary to increase the quantities of materials and supplies in certain months in anticipation of seasonal demands. The ratio of inventory to selected production factors at various levels of production activity and in different seasons should be plotted and studied until standard relationships can be established. The entire process can be refined somewhat by establishing different standards for different sections of the materials and supplies inventory.

The plan, once in operation, must be closely checked by monthly comparisons of actual and standard ratios. When the rate of inventory movement falls below the standard, the records of individual items must be studied to detect the slow moving items.

Materials Purchasing Budget Illustrated

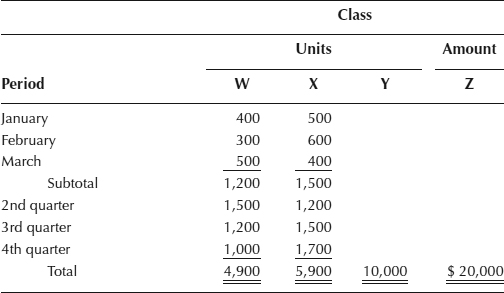

Some of the problems and methods of determining the total amount of expected purchases may be better understood by illustration. Assume, for example, that this information is made available regarding production requirements after a review of the production budget:

Solely for illustrative purposes, the following four groups of products have been assumed:

| Class W | Material of high unit value, for which a definite quantity and time program is established in advance-such as for stock items. Also, the material is controlled on a MinMax inventory basis for budget purposes. |

| Class X | Similar to item W, except that, for budget purposes, MinMax limits are not used. |

| Class Y | Material items for which definite quantities are established for the budget period but for which no definite time program is established, such as special orders on hand. |

| Class Z | Miscellaneous material items grouped together and budgeted only in terms of total dollar purchases for the budget period. |

In actual practice, of course, decisions about production time must be made regarding items using Y and Z classifications. However, the bases described later in this chapter are applicable in planning the production level.

Class W. Where the items are budgeted on a MinMax basis, it usually is necessary to determine the range within which purchases must fall to meet production needs and stay within inventory limits. A method of making such a calculation is shown next:

Within these limits, the quantity to be purchased will be influenced by such factors as unit transportation and handling costs, price considerations, storage space, availability of material, capital requirements, and so forth.

A similar determination would be made for each month for each such raw material, and a schedule of receipts and inventory might then be prepared, somewhat in this fashion:

Class X. It is assumed that the class X materials can be purchased as needed. Since other controls are practical on this type of item and since other procurement problems exist, purchases are determined by the production requirements. A simple extension is all that is required to determine the dollar value of expected purchases:

Class Y. The breakdown of the class Y items may be assumed to be:

A determination about the time of purchase must be made, even though no definite delivery schedules and the like have been set by the customer. In this instance, the distribution of the cost and units might be made on the basis of past experience or budgeted production factors, such as budgeted machine hours. The allocation to periods could be made on past experience, as:

The breakdown of units is for the benefit of the purchasing department only, inasmuch as the percentages can be applied against the total cost and need not apply to individual units. In practice, if the units are numerous regarding types and are of small value, the quantities of each might not be determined in connection with the forecast.

Class Z. Where the materials are grouped, past experience again may be the means of determining estimated expenditures by the period of time. Based on production hours, the distribution of class Z items may be assumed to be (cost of such materials assumed to be $2 per production hour):

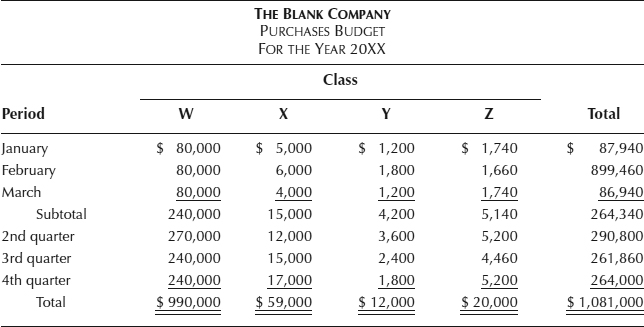

EXHIBIT 10.2 SAMPLE PURCHASES BUDGET

When all materials have been grouped and the requirements have been determined and translated to cost, the materials budget may be summarized as in Exhibit 10.2.

Exhibit 10.2 relates to raw materials. A similar approach would be taken with respect to manufacturing supplies. A few major items might be budgeted as the class W or X items just cited, but the bulk probably would be handled as Z items.

Once the requirements as measured by delivery dates have been made firm, it is necessary for the financial department to translate such data into cash disbursement needs through average lag time and so forth.

BUDGETING FOR WORK-IN-PROCESS

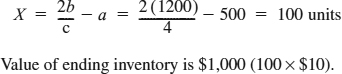

The inventory of goods actually in process of production between stocking points can be best estimated by applying standard turnover rates to budgeted production. This may be expressed either in units of production or dollars and may be calculated for individual processes and departments or for the factory as a whole. The former is more accurate. To illustrate this procedure, assume the following inventory and production data for a particular process or department:

With a standard turnover rate of four times per month, the average inventory should be 300 units (1,200 + 4). To produce an average inventory of 300 units, the ending inventory should be 100 units:

![]()

Using the symbol X to denote the quantity to be budgeted as ending inventory, the following formula can be applied:

Where the formula produces a minus quantity (as it will if beginning inventory is excessive), the case should be studied as an individual problem and a specific estimate made for the process or department in question.

Control over the work-in-process inventories can be exercised by a continuous check of turnover rates. Where the individual processes, departments, or plants are revealed to be excessive they should then be subjected to individual investigation.

The control of work-in-process inventories has been sorely neglected in many concerns. The time between which material enters the factory and emerges as the finished product is frequently much longer than necessary for efficient production. An extensive study of the automobile tire industry revealed an amazing spread of time between five leading manufacturers, one company having an inventory float six times that of another. This study indicated also, by an analysis of the causes of the float time, that substantial reductions could be made in all five of the companies without interference with production efficiency.

Although it is desirable to reduce the investment in goods actually being processed to a minimum consistent with efficient production, it is frequently desirable to maintain substantial inventories of parts and partially finished goods as a means of reducing finished inventories.

Parts, partial assemblies, processed stock, or any type of work-in-process that is stocked at certain points should be budgeted and controlled in the same manner as materials. That is, inventory quantities should be set for each individual item, based on the production program; or inventory limits should be set that will conform to standard rates of turnover. In the former case, control must be exercised through the enforcement of the production program; in the latter case, maximum and minimum quantities must be established and enforced for each individual item.

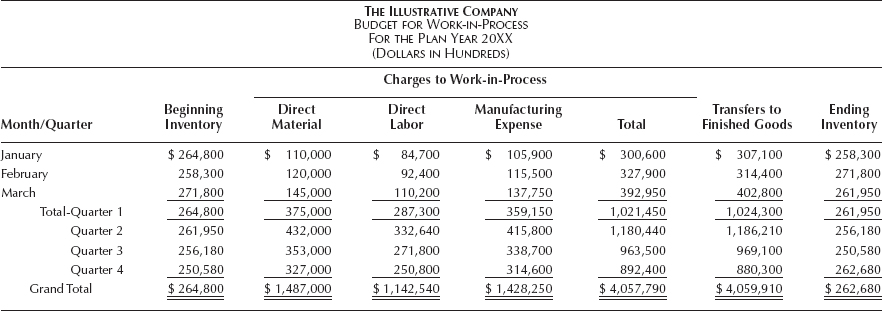

With the planned cost input to work-in-process known from the materials usage budget, the direct labor budget, and the manufacturing expense budget (see Chapters 4 and 5), and the quantities of planned completed goods furnished by manufacturing, the controller may develop the planned work-in-process, time-phased (condensed), as shown in Exhibit 10.3. The reasonableness of the budgeted inventory level should be tested by one of the several methods suggested in this chapter (turnover, etc.).

BUDGETING FOR FINISHED GOODS

The budget of finished goods inventory (or merchandise in the case of trading concerns) must be based on the sales budget. If, for example, it is expected that 500 units of item A will be sold during the budget period, it must be ascertained what number of units must be kept in stock to support such a sales program. It is seldom possible to predetermine the exact quantity that will be demanded by customers day by day. Some margin of safety must be maintained by means of the finished goods inventory so that satisfactory deliveries can be made. With this margin established, it is possible to develop a program of production or purchases whereby the stock will be replenished as needed.

EXHIBIT 10.3 BUDGET FOR WORK-IN-PROCESS

Budgeting Finished Goods by Individual Items

Two general methods may be employed in budgeting the finished goods inventory. Under the first method, a budget is established for each item separately. This is done by studying the past sales record and the sales program of each item and determining the quantity that should be on hand at various dates (usually, the close of each month) throughout the budget period. The detailed production or purchase program can then be developed to provide such quantities over and above current sales requirements. The total budget is merely the sum of the budgets of individual items. This total budget can then be tested by the rate of turnover desired as proof that a satisfactory relationship will be maintained between inventory and sales and that it harmonizes with the general financial program. If it fails in either respect, revision must be made in the program of sales, production, or finance until a proper coordination is effected.

Under this plan, control over the inventory is effected by means of enforcement of the sales and production programs. If either varies to any important degree from the budget, the other must be revised to a compensating degree and the inventory budget revised accordingly.

Where the sales and production programs can be enforced with reasonable certainty, this is the preferable method. It is particularly suitable for those concerns that manufacture a comparatively small number of items in large quantities. The application is similar in principle to that illustrated in connection with raw materials controlled budget-wise by minimums and maximums.

Budgeting Total Finished Quantities and Values

Where the sales of individual items fluctuate considerably and where such fluctuations must be watched for hundreds or even thousands of items, a second plan is preferable. Here basic policies are adopted relative to the relationship that must be maintained between finished inventory and sales. This may be done by establishing standard rates of turnover for the inventory as a whole or for different sections of the inventory. For example, it may be decided that a unit turnover rate of three times per year should be maintained for a certain class of goods or that the dollar inventory or another class must not average more than one fourth of the annual dollar cost of sales. The budget is then based on such relationships, and the proper executives are charged with the responsibility of controlling the quantities of individual items in such a manner that the resulting total inventories will conform to the basic standards of turnover.

With such standard turnover rates as basic guides, those in charge of inventory control must then examine each item in the inventory; collect information about its past rate of movement, irregularity of demand, expected future demand, and economical production quantity; and establish maximum and minimum quantities, and quantities to order. Once the governing quantities are established, they must be closely watched and frequently revised if the inventory is to be properly controlled.

The establishment and use of maximum, minimum, and order quantities can never be resolved into a purely clerical routine if it is to be effective as an inventory control device. A certain element of executive judgment is necessary in the application of the plan. If, for example, the quantities are based on past sales, they must be revised as the current sales trend indicates a change in sales demand. Moreover, allowance must be made for seasonal demands. This is sometimes accomplished by setting different limits for different seasons.

The most frequent cause of the failure of such inventory control plans is the assignment of unqualified personnel to the task of operating the plan and the failure to maintain a continuous review of sales experience relative to individual items. The tendency in far too many cases is to resolve the matter into a purely clerical routine and assign to it clerks capable only of routine execution. The danger is particularly great in concerns carrying thousands of items in finished stock, with the result that many quantities are excessive and many obsolete and slow-moving items accumulate in stock. The successful execution of an inventory control plan requires continuous study and research, meticulous records of individual items and their movement, and a considerable amount of individual judgment.

The plan, once in operation, should be continually tested by comparing the actual rates of turnover with those prescribed by the general budget program. If this test is applied to individual sections of the finished inventory, it will reveal the particular divisions that fail to meet the prescribed rates of movement. The work of correction can then be localized to these divisions.

Whenever possible, the plan of finished inventory control should be exercised in terms of units. When this is not practicable, it must be based on dollar amounts.