12

MANAGEMENT OF LIABILITIES

INTRODUCTION

It often has been said that the management, or planning and control, of the assets (excepting cash and temporary investments) of an enterprise rests largely in the hands of the operating executives but that management, or planning and control, of the liabilities and equity of the company is primarily the responsibility of the financial executives. In a certain sense this is true—up to a point—and the financial officers must exercise control over the liabilities of the entity to preserve its economic health.

The comments in this chapter relate to the practical or pragmatic considerations regarding liability planning and control, of which the controller must be intimately familiar. Remarks will relate to the traditional types of liabilities as well as new developments and concerns in this field of management.

LIABILITIES DEFINED

Although it is not the purpose of the chapter to deal at length with the accounting niceties regarding the recording of the liabilities of a company, the subject is defined for our purposes as:

Liabilities are the economic obligations of an enterprise that are recognized and measured in conformity with generally accepted accounting principles. Liabilities also include certain deferred credits that are not obligations (such as, for example, deferred credits from income tax allocations) but that are recognized and measured in conformity with generally accepted accounting principles.

Liabilities are measured at amounts established in the exchanges involved, usually the amounts to be paid but sometimes at discounted rates.

OBJECTIVES OF LIABILITY MANAGEMENT

In the basic sense, the purpose of liability management is to assure that the enterprise has “cash adequacy”—the ability to meet cash requirements for any purpose significant to the short- or long-term financial health of the company. It is not merely to avoid insolvency or bankruptcy. From the standpoint of the controller, the more specific objectives of liability management might include:

- The recording and disclosure in accordance with generally accepted accounting principles of the financial obligations of the company.

- The reporting in proper form, as required by indentures or credit agreements, of the corporate liabilities.

- Through effective planning and control, the maintenance of a sound financial structure, including the proper relationship of debt to equity capital.

- Continuance of the ability to secure necessary borrowed funds in a timely manner and at a cost that is competitive.

- To institute and maintain controls that restrict commitments within well-defined limits so that they do not result ultimately in excessive and burdensome liabilities.

- To enable the company to be so well regarded in the financial marketplace that its common (and preferred) stock will command respect far into the future with an acceptable price-earnings ratio, and that the stock will reflect a gradual increase in earnings per share and consequent long-term appreciation for the benefit of the owners.

- To permit the company to maintain a prudent dividend policy.

All of these objectives of liability management are interrelated.

DIRECT LIABILITIES

In an attempt to categorize the types of liabilities and to indicate some of the matters to be considered by the controller, a brief commentary follows.

Current Liabilities

Generally, liabilities classified as current are those due to be paid within the operating cycle—that ordinarily is within a period of one year. The importance of the proper segregation of current liabilities from other liabilities rests in the role played by various financial ratios, such as the current ratio, when funds are borrowed.

By another related definition, current liabilities include those obligations whose liquidation reasonably is expected to require the use of existing current assets or the creation of new current liabilities. Included in current liabilities are:

- Notes payable. Represent the obligations of the company under legal instruments in which there exists an explicit promise to pay a specified amount at a specified time.

- Accounts payable. Accounts payable usually are largely trade accounts payable and represent the obligations of the firm to its suppliers. Since these liabilities are recorded at the time the title passes to the goods or the services are received, the financial officers should be satisfied that clean cutoffs on the obligations exist. This is especially true in those instances where the working capital or current ratio requirement is critical in a credit agreement or the company is nearing the limits specified.

Additionally, credit balances in various asset accounts, such as accounts receivable, usually are reclassified to the accounts payable category—especially at year end—or when financial statements are published.

- Accrued expenses. When an obligation exists by reason of the benefits having been received but is not yet due and payable, it normally would be recorded as an accrued expense. Included would be such items as accruals for wages, salaries, commissions, rents, royalties, pension costs, and income and other taxes.

- Accrued income taxes. Special mention is made of this liability, since often it is composed of two segments. The normal tax due within a year would be recorded under current liabilities as “currently payable.” However, using the principle of matching costs with related revenues, yet recognizing that the tax laws permit the reporting of income in a different fiscal period than generally accepted accounting principles would either permit or require, there may be includable under current liabilities a “deferred” income tax obligation.

There are rather continuously numerous official releases by the Financial Accounting Standards Board (FASB), which provide new standards concerning income tax accounting. For example, in May 1992, the body issued Statement of Financial Accounting Standards No. 109—Accounting for Income Taxes. It supersedes FASB Statement No. 96, Accounting for Income Taxes and amends or supersedes a number of other accounting pronouncements. Statement No. 109 established financial accounting and reporting standards for the effects of income taxes that result from an enterprise's activities during the current and preceding years. It requires an asset and liability approach for financial accounting and reporting for income taxes. As the Standard says, “The objectives of accounting for income taxes are to recognize (a) the amount of taxes payable or refundable for the current year, and (b) deferred tax liabilities and assets for future tax consequences of events that have been recognized in an enterprise's financial statements or tax returns.”

It is assumed the controller will keep abreast of tax reporting requirements and will see that the tax liability is properly recognized.

This distinction becomes important in calculating cash flows and when considering acceptable terms in indentures or credit agreements.

Long-Term Liabilities

Long-term liabilities, by definition, represent those obligations due in more than one year or those to be paid out of noncurrent assets. Only three limited comments need be made.

- Long-term leases. If at its inception a lease meets one or more of the following criteria, it shall be classified as a capital lease by the lessee and placed on the balance sheet. Otherwise, it would be treated as an operating lease, with appropriate disclosure. The criteria for capitalization include:

- (a) The lease transfers ownership of the property to the lessee by the end of the lease term.

- (b) The lease contains a bargain purchase option.

- (c) The lease term is equal to 75% or more of the estimated economic life of the leased property (with certain exceptions).

- (d) The present value at the beginning of the lease term of the minimum lease payments—excluding certain costs—equals or exceeds 90% of the fair market value of the property over the related investment tax credit retained or expected to be used by the lessor.

For the specific criteria and the exceptions, reference should be made to the literature of the American Institute of Certified Public Accountants (AICPA).

- Bonds. Bonds are essentially long-term corporate notes issued under a formal legal procedure and secured either by the pledge of specific properties, or revenues, or the general credit of the issuer. Bonds differ from individual notes in that each represents a fractional interest of participation in a group contract, usually with a trustee acting as intermediary. The terms of the contract are set forth in the trust indenture.

- Other long-term obligations, etc. Depending on circumstances, there may exist other obligations and like items that are classified either as long-term obligations or items carried in the long-term section of the balance sheet above the shareholders' equity. These may include such items as:

- Deferred income taxes

- Deferred compensation

- Accrued product warranty

- Employees pension, indemnity, retirement, and related provision

- Negative goodwill

- Minority interests

The reader is referred to the various publications of the AICPA about the generally accepted principles that govern the recording of the item.

ILLUSTRATIVE PROVISIONS OF CREDIT AGREEMENTS

To be sure, within limits, indentures or credit agreements will be tailored to fit the desires of both the lender and the borrower. However, a great number of standard provisions apply to many loan agreements. Before further discussing the recording of the liabilities and, indeed, before considering the planning of indebtedness, it may be helpful to be aware of some of these usual provisions that relate to indebtedness limits and certain uses of cash. Excerpts from the note agreement for a ten-year private placement loan from an insurance company to a manufacturing concern include:

6A.Current Ratio Requirement. The Company covenants that it will not permit Consolidated Current Assets at any time to be less than an amount equal to 150% of Consolidated Current Liabilities.

6B. Dividend Limitation. The Company covenants that it will not pay or declare any dividend on any class of its stock or make any other distribution on account of any class of its stock, or redeem, purchase or otherwise acquire, directly or indirectly, any shares of its stock (all of the foregoing being herein called “Restricted Payments”) except out of Consolidated Net Earnings Available For Restricted Payments; provided, however, that notwithstanding the foregoing limitations, the Company may make sinking fund and dividend payments on its outstanding preferred stock not in excess of $3,300,000 in the aggregate in any year, but provided further, that the amount of any such sinking fund payments and the amount of any such dividends paid or declared shall be included in any subsequent computation pursuant to this paragraph 6B. “Consolidated Net Earnings” shall mean consolidated gross revenues of the Company and its Subsidiaries less all operating and non-operating expenses of the Company and its Subsidiaries including all charges of a proper character (including current and deferred taxes on income, provision for taxes on unremitted foreign earnings which are included in gross revenues and current additions to reserves), but not including in gross revenues any gains (net of expenses and taxes applicable thereto) in excess of losses resulting from the sale, conversion or other disposition of capital assets (i.e., assets other than current assets), any gains resulting from the write-up of assets, any equity of the Company or any Subsidiary in the undistributed earnings of any corporation which is not a Subsidiary, any earnings of any corporation acquired by the Company or any Subsidiary through purchase, merger or consolidation or otherwise for any year prior to the year of acquisition, or any deferred credits representing the excess of the equity in any Subsidiary at the date of acquisition over the cost of the investment in such Subsidiary; all determined in accordance with generally accepted accounting principles including the making of appropriate deductions for minority interests in Subsidiaries. “Consolidated Net Earnings Available For Restricted Payments” shall mean an amount equal to (1) the sum of $10,000,000 plus 90% (or minus 100% in case of a deficit) of Consolidated Net Earnings for the period (taken as one accounting period) commencing on August 1, 20XX, and terminating at the end of the last fiscal quarter preceding the date of any proposed Restricted Payment, less (2) the sum of (a) the aggregate amount of all dividends and other distributions paid or declared by the Company on any class of its stock after July 31, 20XX, and (b) the excess of the aggregate amount expended, directly or indirectly, after July 31, 20XX, for the redemption, purchase or other acquisition of any shares of its stock, over the aggregate amount received after July 31, 20XX as the net cash proceeds of the sale of any shares of its stock. In the event that any shares of stock of the Company are issued upon conversion of convertible notes, bonds or debentures of the Company, the proceeds of the shares of stock so issued shall be deemed to be an amount equal to the principal amount of the obligations so converted. There shall not be included in Restricted Payments or in any computation of Consolidated Net Earnings Available For Restricted Payments: (x) dividends paid, or distributions made, in stock of the Company; or (y) exchanges of stock of one or more classes of the Company, except to the extent that cash or other value is involved in such exchange. The term “stock” as used in this paragraph 6B shall include warrants or options to purchase stock.

The company will not:

6C(2) Debt—Create, incur, assume, guarantee or in any way become liable for any Funded Debt in addition to the Funded Debt referred to in paragraph 8D, or create, incur, assume or suffer to exist any Current Debt, except

(i) Funded Debt of the Company or any Subsidiary provided that, after giving effect thereto and to the concurrent repayment of any other Funded Debt, Consolidated Net Tangible Assets shall be not less than an amount equal to (a) 250% of Consolidated Senior Funded Debt, and (b) 150% of Consolidated Funded Debt, and further provided that no Subsidiary shall create, incur, assume, guarantee or in any way become liable for any Funded Debt permitted by this clause (i) unless such Funded Debt shall be secured by a Lien on its property permitted by clauses (v), (vii) or (viii) of paragraph 6C(1), shall be of the type referred to in clause (iii) of paragraph 10G or shall constitute Funded Debt payable to the Company or another Subsidiary, and

(ii) Current Debt of the Company or any Subsidiary, provided that the aggregate Current Debt of the Company and its Subsidiaries permitted by this clause (ii) shall not be in excess of the Permitted Amount on any day after December 31, 20XX unless, during the fifteen months' period immediately preceding such day, the aggregate Current Debt of the Company and its Subsidiaries permitted by this clause (ii) shall not have been in excess of the Permitted Amount for at least 60 consecutive days, and further provided that no Subsidiary shall create, incur, assume or suffer to exist any Current Debt permitted by this clause (ii) unless such Current Debt shall be secured by a Lien on its property permitted by clauses (v), (vii) or (viii) of paragraph 6C(1) or shall constitute Current Debt payable to the Company or another Subsidiary:

6E. Subordinated Debt. The Company covenants that it will not (i) pay, prepay, redeem, purchase or otherwise acquire for value any Subordinated Debt except as required by the original provisions of the instruments evidencing Subordinated Debt or pursuant to which Subordinated Debt shall have been issued, (ii) amend the instruments evidencing Subordinated Debt or pursuant to which Subordinated Debt may have been issued in such manner as to terminate, impair or have adverse effect upon the subordination of the Subordinated Debt, or any part thereof, to the indebtedness evidenced by the Notes; or (iii) take or attempt to take any action whereby the subordination of the Subordinated Debt, or any part thereof, to the indebtedness evidenced by the Notes might be terminated, impaired or adversely affected. The term “Subordinated Debt” as used in this paragraph 6E shall mean any Funded Debt of the Company or any Subsidiary which does not constitute Senior Funded Debt.

Thus, it can be seen that overall debt constraints are included in this agreement and usually are a part of most credit agreements.

With respect to securing short-term credit, certain other types of restrictions may apply. Excerpts from a loan and credit agreement for short-term borrowing under a revolving line of credit between a manufacturer and a group of commercial banks contain clauses that, under specified conditions, do:

- Restrict certain payments (such as cash dividends or purchases of company stock).

- Restrict the sale or lease of assets.

- Require the maintenance of a given ratio of shareholders' equity to senior indebtedness and a minimum amount of shareholders' equity.

- Place restraints on specific contingent liabilities.

- Place limitations on acquisitions of other companies.

- Place limitations both on certain specific debts and on overall consolidated indebtedness.

The specific wording of some of the clauses relating to covenants or restrictions may be of interest:

Minimum Working Capital. Maintain Consolidated Working Capital at a level whereby consolidated current assets are at least 175% of consolidated current liabilities of the Company and all Consolidated Subsidiaries and, in any event, of at least $200,000,000. In any calculation of Consolidated Working Capital, an amount equal to Covered Customer Advances shall be excluded from both consolidated current assets and consolidated current liabilities and deferred income taxes reported by the Company as a current liability in its consolidated balance sheet shall be excluded from consolidated current liabilities.

Negative Covenants. So long as credit shall remain available to the Company hereunder and until the payment in full of all Notes outstanding hereunder and the performance of all other obligations of the Company hereunder, the Company will not, and will not permit any Consolidated Subsidiary to, without the prior written consent of Banks holding at least 66 2/3% in aggregate unpaid principal amount of the Notes, or, if no Notes are then outstanding, Banks having at least 66 2/3% of the aggregate commitments to make loans hereunder:

Restrictive Payments. Declare, pay or authorize any Restricted Payment if (a) any such Restricted Payment is not paid out of Consolidated Net Earnings Available For Restricted Payments and (b) at the time of, and immediately after, the making of any such Restricted Payment (or the declaration of any such dividend except a stock dividend) no Event of Default specified in § 8 and no event which with notice or lapse of time or both would become such an Event of Default has occurred and (c) the making of any such Restricted Payment would reduce Consolidated Tangible Shareholders' Equity below $225,000,000.

Sale, Lease, etc. Sell, lease, assign, transfer or otherwise dispose of any of its assets, tangible and intangible (other than investments permitted by § 7B(7) and obsolete or worn-out property or real estate not used or useful in its business), whether now owned or hereafter acquired, excluding from the operation of this clause sales, leases, assignments, transfers and other dispositions (a) in the ordinary and normal operation of its business and for a full and adequate consideration, (b) between the Company and any Consolidated Subsidiary, and between Consolidated Subsidiaries and (c) by the Company not in the ordinary and normal operation of its business provided the value on the Company's books of assets so transferred shall not exceed 10% of Consolidated Tangible Shareholders' Equity in the aggregate in any calendar year.

Maintenance of Shareholder's Equity. Permit the amount of Consolidated Tangible Shareholders' Equity at any time to be less than 100% of the then aggregate outstanding amount of Consolidated Senior Indebtedness or less than $225,000,000.

Contingent Liabilities. Assume, guarantee (which for purposes of this clause (4) shall include agreements to purchase or to provide funds for the payment of obligations of, to maintain the net worth or working capital or other financial test of, or otherwise become liable upon the obligations of, any person, firm or corporation) or endorse any obligation of any other person, firm or corporation (except the Company or a Consolidated Subsidiary, or any captive insurance subsidiary, as the case may be, as permitted by this clause (4)) or permit to exist any assumption, guarantee or endorsement, excluding from the operation of this clause, (a) assumptions, guaranties and endorsements in the ordinary and normal operation of its business as presently conducted, it being understood that performance guaranty bonds, bank guaranties for foreign work, advance payment bonds, direct guarantees for performance, or other surety bonds will be so considered; (b) guarantees by the Company or any Consolidated Subsidiary or direct obligations of the Company or any Consolidated Subsidiary for the payment of money, whether domestic or foreign, so long as an amount equal to the aggregate amount of such guaranteed obligations is deemed to be (without duplication). Indebtedness and/or Consolidated Senior Indebtedness, as the case may be, for purposes of §§ 7b(8) and 7B(9); (c) guarantees of the Company or any Consolidated Subsidiary issued, or obligations assumed, in connection with acquisitions of assets permitted under § 7B(5), provided that obligations for borrowed money (whether guaranteed or assumed) shall be treated as provided in the next preceding clause (b); and (d) guaranties by the Company or any Consolidated Subsidiary of direct obligations of third parties for the payment of money, provided that if the then aggregate amount of such obligations shall exceed an amount equal to 15% of Consolidated Tangible Shareholders' Equity, the amount of such excess shall be deemed Consolidated Senior Indebtedness for purposes of this Agreement.

Acquisition of Assets. Acquire any assets of any other person through merger, consolidation or otherwise (including acquisition of capital stock of any other person if such acquisition is analogous in either purpose or effect to a consolidated or merger) except in the ordinary course of business, unless after giving effect to such acquisition (a) the Company shall be the surviving corporation, and (b) no Event of Default specified in § 8 or event which with notice or lapse of time or both would become such an Event of Default shall have occurred.

Other Debt. Incur or have outstanding any Indebtedness or become or be liable with respect to any Indebtedness or sell any obligations of the Company or any Consolidated Subsidiary, excluding from the operation of this covenant,

(a) the Notes:

(b) indebtedness, other than for borrowed money, incurred in the ordinary course of business of the Company or a Consolidated Subsidiary, provided such indebtedness is not prohibited under § 78B(4) or 7B(5);

(c) liabilities in connection with capitalized leases;

(d) loans by the Company to Consolidated Subsidiaries, and loans by Consolidated Subsidiaries to the Company and other Consolidated Subsidiaries;

(e) indebtedness of the Company to Prudential, not exceeding $13,500,000, incurred pursuant to the Prudential Loan Agreement;

(f) commercial paper of the Company having a maturity of not more than nine months from its date, in amounts which in the aggregate do not exceed at any time outstanding the lesser of $75,000,000 or the sum of the unused Revolving Credit Commitments plus Bank lines of credit;

(g) existing indebtedness of Consolidated Subsidiaries not in excess of $2,075,000, provided that as said debt is paid or reduced it shall not be increased;

(h) a loan of X Company from a foreign bank in the amount of $2,075,000 (or the lira equivalent thereof), provided that as said debt is paid or reduced it shall not be increased;

(i) secured indebtedness permitted by § 7B(6)(g) in an aggregate amount not to exceed the $100,000,000 original principal amount, provided that as said debt is paid or reduced it shall not be increased;

(j) other Consolidated Senior Indebtedness of the Company and Consolidated Subsidiaries which does not exceed $30,000,000 in the aggregate at any time, provided that the maturity of all such indebtedness in excess of an aggregate of $5,000,000 has been consented to in writing by Banks holding at least 66 2/3% in aggregate unpaid principal amount of the Notes, or, if no Notes are then outstanding, Banks having at least 66 2/3% of the aggregate commitments to make loans hereunder;

(k) borrowings from foreign sources in amounts not exceeding the equivalent of $50,000,000, provided the maturity and terms of all such indebtedness in excess of an aggregate of $5,000,000 has been consented to in writing by Banks holding at least 66 2/3% in aggregate unpaid principal amount of the Notes, or, if no Notes are then outstanding, Banks having at least 66 2/3% of the aggregate commitments to make loans hereunder;

(l) Subordinated Debt of the Company; and

(m) other Consolidated Senior Indebtedness of the Company (but not of any Consolidated Subsidiary), whether domestic or foreign, so long as after incurrence thereof (i) the then aggregate outstanding amount of Consolidated Senior Indebtedness of the Company and all Consolidated Subsidiaries would not exceed 100% of Consolidated Tangible Shareholders' Equity and (ii) neither the Company nor any Consolidated Subsidiary would be in default under this Agreement.

Limitation on Consolidated Indebtedness. Permit the Consolidated Indebtedness of the Company and all Consolidated Subsidiaries at any time to be more than 200% of Consolidated Tangible Shareholders' Equity.

In the day-to-day administration of loan agreements, it is obvious that the controller should be aware of the terms and should report the financial condition and financial data as required in the contract. Of equal or more importance, however, should be the controller's review of proposed financial actions to determine whether they would violate any present agreements and then to take appropriate action.

Aside from the reporting requirements, the controller should be aware of management's obligation not only to the shareholders, but also to the suppliers of debt capital. The indenture agreement may still be the best way of protecting the interests of the senior long-term lender. However, given some recent experiences wherein investment-grade bonds have been converted essentially into junk bonds in a very short period, the credit agreement may require more restrictive measures, taking into account the creativity of some lawyers, and the use of technical devices to circumvent some protective clauses. Many entities are now demanding the “poison put” provision discussed in the section on developments in the fixed income market.

PLANNING THE CURRENT LIABILITIES

Having discussed in a general way the different types of liabilities, it is now in order to review the planning process first for the current liabilities and later for long-term debt.

Planning of any specificity for current liabilities for most concerns relates to the annual business plan, for the next year or so, or to an even shorter time span. Basically, the short-term planning involves these three steps:

- Determining, based on the operating requirements for each month and each month end, the level of each type of obligation expected (e.g., accounts payable, accrued expenses, accrued salaries and wages, accrued income taxes, notes payable, dividends payable).

- Ascertaining from the cash forecast (see Chapter 8) whether any borrowings are necessary to meet the payment requirements, and incorporating this need and the payments into the plan.

- Testing the consolidated plan at selected intervals, such as every reporting period or every quarter, to see if the terms of any or all credit agreements are being met—or if the indebtedness is within company norms or standards—and taking appropriate action if not (securing bank waivers, deferral of purchases, securing of special terms from suppliers, acceleration of cash receipts, etc.).

It may be observed that the level of most current liabilities, other than notes payable, will be the result of other operating segments of the annual plan. Thus, accounts payable will relate to purchases for inventory or obligations for current operating expenses; accrued salaries and wages will relate to the planned payrolls for the continuing operations, and so on. Any required short-term borrowings will derive from the cash planning.

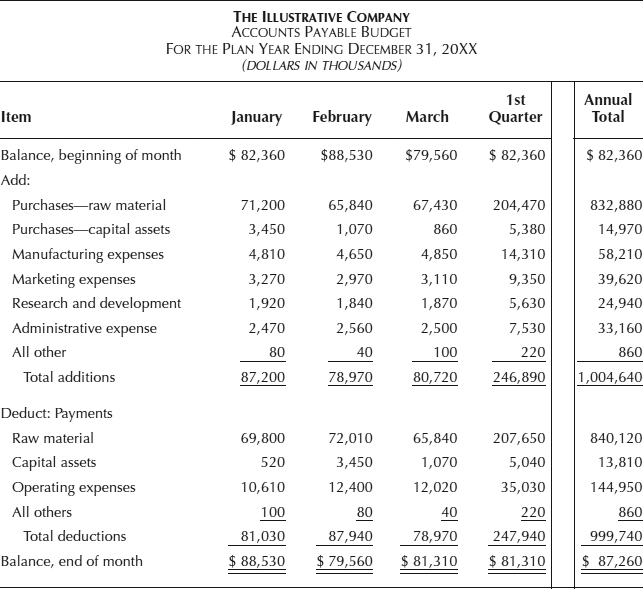

In planning any element of current payables, it is practical to accumulate the segment based on the normal grouping of costs and expenses needed for each type of transaction. Thus, as reflected in Exhibit 12.1, the aggregate liability for purchases of raw materials and purchased parts (probably one entry in planning material purchases) is recorded for each month. Perhaps all other current purchases of an expense nature are journalized for each month. Any significant “other transaction” is recorded separately for the plan, just as would be done for the actual expense. Payments would be estimated based on an average lag time as described in Chapter 8.

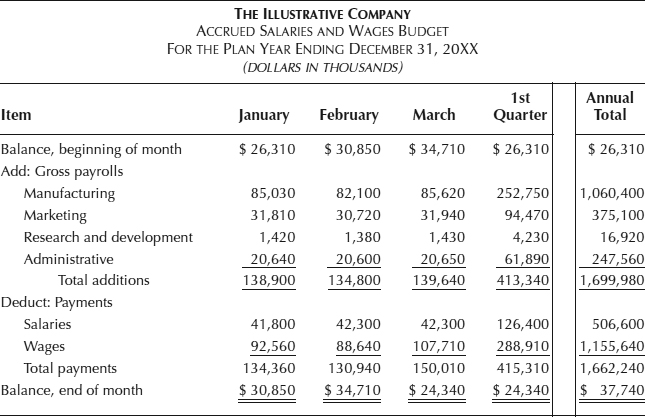

The estimate of accrued salaries and wages is shown in Exhibit 12.2. The additions to the accrual would be in those groupings used to determine manufacturing costs (inventory) or other logical accumulations.

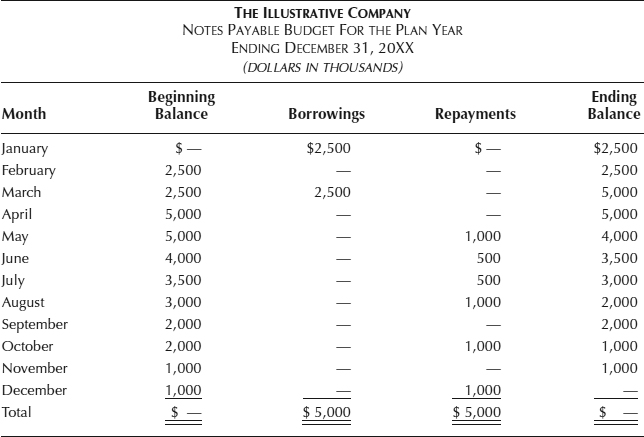

Based on the required borrowings and repayments as determined in the cash forecast, the plan for notes payable could be developed as in Exhibit 12.3.

The same procedure would be followed for each liability grouping deemed necessary and practical in the current liability planning cycle.

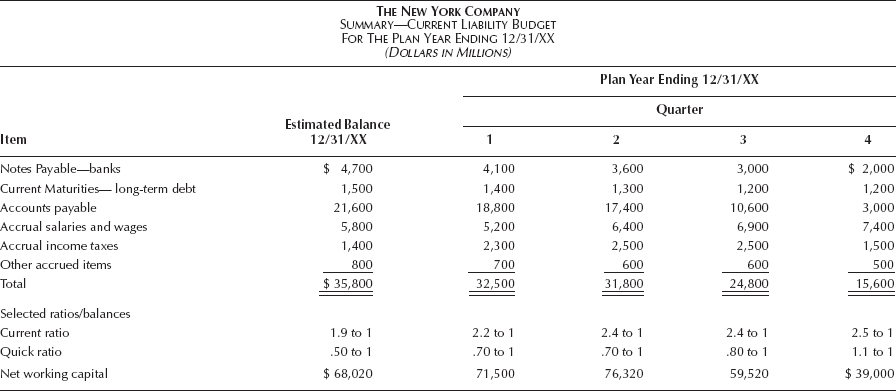

When all the current liabilities balances have been determined, they should be summarized as in Exhibit 12.4. As explained in the next section, the planned balances, as well as actual balances, should be measured against acceptable standards, as well as credit agreement requirements, and so on.

The above discussion of planning the current liabilities has been covered in the context of the annual business plan or any other short-term plan. The same principles would apply with respect to strategic planning or long-range planning (see Chapters 12 and 13), except that the time span usually can be by year and need not be by quarter or month. Moreover, the estimates may be arrived at on a ratio basis, and much less preciseness and detail usually are satisfactory.

EXHIBIT 12.1 ACCOUNTS PAYABLE PLAN

STANDARDS TO MEASURE AND CONTROL CURRENT LIABILITIES

The planning task of the controller does not consist merely of determining what the level of current liabilities will be at stipulated times, based on operating plans or capital budgets or other financial plans. Additionally, these planned levels should be tested for acceptability. The standards by which such acceptability is judged should include (a) any legal requirements, such as those in bank lending agreements or in bond indentures and so forth; (b) those developed by the company (probably by the financial officers) as deemed prudent to avoid undue financial exposure; or (c) those acceptable to knowledgeable persons in the industry. Dun … Bradstreet, for example, periodically issues selected ratios on each industry, showing the median and upper and lower quartile for certain operating ratios and financial conditions. The company could measure itself against these industry ratios or against performance of selected competitors or against standards developed or used by commercial bankers, investment bankers, or financial analysts. If these tests reveal unacceptable conditions, then corrective action should be taken, as discussed in the next section.

EXHIBIT 12.2 ACCRUED SALARIES AND WAGES BUDGET

EXHIBIT 12.3 NOTES PAYABLE BORROWING PLAN

Some suggested ratios used to measure the acceptability of current liabilities include:

- Current ratio

- Quick ratio

- Minimum net working capital

- Current debt to net worth

- Current debt to inventory

- Number of days' payables on hand (accounts payable turnover)

Current Ratio

The current ratio is calculated by dividing the current assets by the current liabilities. It measures the protection the creditors have, even if the current assets prove to be less valuable than anticipated. Years ago, a ratio deemed satisfactory was 2 to 1. However, with the advent of the computer and improved receivables and inventory control, a ratio of between 1 to 1 and 2 to 1 is usually acceptable.

Quick Ratio

The quick ratio measures the relationship of the highly liquid assets—cash, temporary investments, and accounts receivable—to current liabilities. This ratio, also known as the liquidity ratio or acid test, is an indicator of what very liquid assets are available to meet the demands of the short-term creditors.

EXHIBIT 12.4 SUMMARY OF CURRENT LIABILITIES PLAN

Minimum Net Working Capital

This is an absolute amount—the difference between current assets and current liabilities. Some loan and credit agreements, including the one illustrated earlier, require a minimum amount of working capital at all times. The net amount indicates the extent to which the current assets could shrink and yet be sufficient to meet the current liabilities.

Current Debt to Net Worth

To the extent that assets are financed by the owners, there is more protection (more assets) for the creditors. A low current debt (or total debt) to net worth ratio is some measure of how the owners are supplying more relative funds.

Current Debt to Inventory

A high ratio of current debt as related to inventory would suggest that goods are purchased, processed, and sold without payments being made to suppliers. Depending on the relative ratio, as compared to the industry and trade practice, a high relationship would indicate inadequate financing.

Number of Days' Payables on Hand

The number of days' payables on hand is determined by dividing the accounts payable balance by the amount of purchases, and multiplying by the days in the period. For example, in Exhibit 12.1:

- The quarterly accounts payable balance planned is $81,310,000.

- Purchases for the period were planned at $246,890,000.

- Business days in the period are 65.

Such a result should be checked against industry standards, if available.

CORRECTIVE ACTION

If the annual plan reflects an unsatisfactory condition regarding current liabilities, or if actual results are not acceptable, what action can be taken? The controller might examine these alternatives with the appropriate line executive:

- Possibility of reducing inventory levels through different purchasing terms, inventory handling methods, or inventory control, for example, just-in-time (JIT) inventories

- Reducing accounts receivable by granting special terms or cash discounts and the like

- Making special arrangements with suppliers to receive goods on consignment or special payment terms

- As a last resort, if the conditions appear temporary, asking the lenders to waive or relax the restrictive terms for a limited period

If the condition appears more permanent, perhaps additional equity capital or long-term debt may be desirable. Less ambitious business plans may be considered for a time: less capital expenditures, lower sales volume, and so forth.

If actual unsatisfactory conditions emerge, then some of these same planning alternatives may need to be reviewed.

RISKS OF TOO MUCH DEBT

The subject of long-term debt is closely related to the capital structure of the entity—meaning the combination of shareholders' equity and long-term debt that should be used to provide for the financing needs over the span of several years. In considering this subject, the goal of the financial executive should be to so arrange the financing that the owners of the business will receive the maximum economic benefit over the longer run, through the increase in the share price and constantly rising dividend income.

It can be demonstrated over a period of time, assuming normal profitability and the deductibility of interest expense for tax purposes, that prudent borrowing will increase the return to the shareholder. Given this potential of gain, there exists a powerful deterrent that discourages using long-term debt to the maximum of its availability. That deterrent is the risk associated with servicing the debt. For debts and debt service must be paid when due regardless of the financial condition of the company to avoid unwelcome restraints or, worse, the loss of the enterprise.

SOME BENEFITS FROM DEBT INCURRENCE

While the prudent financial executive should be aware of the risks of excessive debt, it is also necessary to recognize some of the advantages of a reasonable debt load. Here are a few:

- Debt reduces tax payments. Because most interest cost is income tax deductible, tax payments are lower. This assists in reducing the cost of capital used in the business.

- Prudent borrowings can increase the return on capital to the owners. If the earnings from this borrowed capital exceed the cost net of taxes, then the return to the shareholder is higher. (See section 32-14 on leverage.)

- Debt imposes a discipline on management as to normal operations. Investors know that too much cash can encourage wasteful spending practices. They tend to watch performance more carefully if sizable debt exists. Additionally, the management is more sensitive to the need for frugality to repay the debt. So more careful spending results.

- Debt motivates managers and owners. Lowering the equity base with borrowed funds probably makes it easier for the management group to acquire a significant stake.

- Debt causes a more appropriate review of proposed capital expenditures and acquisitions. Rigid repayment schedules probably cause a closer look at the economics of proposed expenditures as well as those units that don't produce sufficient earnings.

In summary, as one executive stated, “Debt is a just-in-time financial system.”

SOURCES OF INFORMATION ON DEBT CAPACITY

For long-range financial planning, as well as judging the proposed terms or rating of contemplated new debt, what sources are available to secure guidance? In the final analysis, it must be management judgment that decides on acceptable limits for debt capacity. Some guidance in arriving at a decision may come from:

- Institutional lenders or intermediaries. Lenders, or commercial bankers, or investment bankers negotiate long-term loans at rather frequent intervals in contrast to the financial officer of an industrial enterprise. Consequently, they will be more familiar with the terms of recent agreements. Presumably, also, they are conservative and will tend to err in the conservative direction. They should be able to judge if proposed standards will be acceptable in the marketplace.

- Action of competitors. Ordinarily, the financial statements and loan agreements of comparable companies in the same industry are available. From such public information, individual companies and group norms can be obtained, together with ranges.

- Analysis of past practice. Finally, historical analysis of debt and income behavior in the particular company in times of adversity and normal conditions may provide some guide.

STANDARDS FOR DEBT CAPACITY

Conventionally, there are two types of standards by which to judge long-term debt capacity: a capitalization standard and an earnings coverage standard. In arriving at a debt policy for a particular company, each should be considered and interrelated. In working with internally generated data, the controller can make refinements ordinarily not possible with public data of other companies, thus guiding management about an acceptable relationship.

A widely used standard, often employed as a constraint in credit agreements, is the long-term debt-to-equity ratio. Thus long-term debt should not be more than, say, 25 percent of equity capital. It can also be expressed as a percent of total capitalization.

In using such a standard, several determinatives should be calculated, showing the impact, for example, of a 20 percent debt ratio versus a 25 percent ratio to judge the risk involved. Then, too, recognition must be given to the often wide variation between the principal of the debt and the annual debt service charge of interest and debt repayment. A loan may be paid off in 5 or 30 years. Whereas the ratio of debt to equity may be the same in each case in a given year, the debt service burden is substantially different. Conversely, whereas the debt ratio could improve dramatically with a shorter-term loan, the debt service drain remains the same until complete repayment.

The “earnings coverage standard” measures the total annual amount required for debt service to the net earnings available for servicing the debt. By relating the annual cash outflow for debt service (and perhaps other items) to the net earnings available for this purpose, it seeks to assure that even in times of adversity there are sufficient funds to meet the obligation. Obviously, the greater the probable change in cash flow, the higher the desired times-coverage ratio. The observed times coverage varies greatly by industry and by company. Typical well-financed companies may have a coverage of fifteen times or more.

In making analyses of the company, the controller can apply a great deal of sophistication in changing anticipated cash outflows to judge the impact. Thus it may be desirable to measure not only times coverage of net income to debt service but also other cash requirements that should not be disturbed, that is, dividends for shareholders, or certain research and development expenditures, or expected inventory build-up, or minimum capital expenditures. Each major cash outflow should be considered and reasonable sums provided even in times of adversity. An example of an analysis that might be made is shown in Exhibit 12.5. In this illustration, actual and planned cash sources and uses are satisfactory in the planning period.

EXHIBIT 12.5 ANALYSIS OF CASH AVAILABILITY AND SELECTED DEBT COVERAGE

The debt coverage ratios are very good. However, with a major drop in sales, even planned cutbacks in receivables, inventory, and capital expenditures result in coverage ratios that although adequate are substantially below the levels the financial management considers desirable in a cyclical type of business. The need for a new debt issue in 20X5 should be reexamined in terms of the probability or danger of a sales decline. However, a long-term debt has been continually declining from 16 percent of capitalization in 20XX to 11 percent in 20X4; and even with the planned $70 million new debt issue in 20X5 it reaches only 17 percent. Hence, the critical point in this example is earnings coverage, not capitalization.

The magnitude of the probable downturn in earnings and changes in various cash out-flows under such circumstances should be considered. A range of the most probable contraction in sales volume and, therefore, in net income should be determined and resulting times coverage determined.

In the final analysis, debt policy or appropriate capital structure can be determined only by an examination of the factors in the company and in the industry that influence the ability to repay debt. It is a matter of judgment and foresight regarding likely conditions, conservatively arrived at—and not mathematics.

BOND RATINGS

There exists a significant difference in interest cost, depending on the quality rating assigned to debt securities by the three rating agencies, and this is an important consideration in selecting aggregate debt limits. Standard and Poor's (S…P), Moody's Investor Service, and Fitch Investor's Service—the three debt rating agencies—assign ratings that characterize judgment about the quality or inherent risk in any given security. The rating will depend, among many other factors, on the debt coverage relationship.

The symbols Moody's uses for the highest four ratings may be summarized or characterized as:

- Aaa. The best quality; smallest degree of investment risk and generally considered “gilt edge.”

- Aa. Judged to be of high quality by all standards.

- A. Higher medium grade obligations, with some elements that may be present to suggest a susceptibility to impairment at some time in the future.

- Baa. Lower medium grade. Lack outstanding investment characteristics and, in fact, have speculative characteristics as well.

The objective of many well-financed companies is to secure at least an Aa rating for its bonds.

Presentations to secure the bond ratings should be carefully prepared, because poor ratings are not easily overcome.

In determining a debt rating, the agencies need adequate financial data, such as:

- Consolidated balance sheets—perhaps five historical years and five projected years.

- Consolidated statements of income and retained earnings for five years historical and five years projected. Included would be dividends paid and per share data, including earnings, dividends, and book value.

- Consolidated statement of cash flows—again five historical years and five prospective years.

- Product group statements for historical and projected data regarding sales, operating margin, and margin rate.

The ratio analysis, including the coverage ratios, found helpful to the rating agencies is shown in Exhibit 12.6.

EXHIBIT 12.6 RATIO ANALYSIS FOR USE BY RATING AGENCY

LEVERAGE

In considering capital structure, the financial officers necessarily must recognize and study the impact of leverage. Essentially, leverage consists of financing an enterprise with senior obligations to increase the rate of return on the common equity. The action is known also as “trading on the equity.”

An application of leverage is shown in Exhibit 12.7. Assume that the management has been earning, before income taxes, 37% on capitalization; that it believes it can continue to achieve this same return; and that the company can borrow at an 11% rate. If it borrows 20% of equity and continues the rate of return on assets, the earnings per share, with favorable leverage, increase from $5.00 to $5.70 and the return on equity rises from 19.98 to 22.79%.

However, if, under unfavorable leverage conditions, management were too optimistic and the earnings rate less than the bond interest rate, the results can be unsatisfactory—as illustrated in Exhibit 12.8. Here, the rate of return on capitalization was less than the bond interest rate.

From an investor standpoint, in good times, the leverage increases the earnings per share and the price of the stock. However, in adverse times, the reverse condition exists, and the stock of a leveraged company becomes less attractive.

CONTINGENCIES

To this point in this chapter, the discussion has been related to direct liabilities of the enterprise. However, the management of liabilities must extend to contingent liabilities, including proper accounting for the items and proper disclosure. Aside from the matters covered herein, the controller should recognize that contingent liabilities of certain types may be weighted by a lending institution in agreeing to amounts and terms and conditions in a proposed loan agreement.

EXHIBIT 12.7 FAVORABLE LEVERAGE

EXHIBIT 12.8 UNFAVORABLE LEVERAGE

Moreover, in planning for the direct liabilities of the enterprise, the controller may find it necessary to estimate the timing and amount of contingent liabilities that should be treated as direct debt on a probability basis.

Treatment of Long-Term Liabilities in the Annual Business Plan

Planning the long-term debt status for the coming year is one segment of the annual business plan. This phase of the business may be reported only as presented in the statement of financial position, with the beginning-of-the-year status and the end-of-the-year status indicated. However, if the items are numerous enough, or if the attention of the management and the board of directors should be directed to this matter, then the plan for long-term debt may be summarized and presented on an exhibit as in Exhibit 12.9. It should be noted that the proposed transactions are disclosed, as well as key ratios. In all published financial statements, the controller has the responsibility to properly value and properly disclose the significant long-term obligations in accordance with generally accepted accounting principles (GAAP). It is suggested that in most instances the same basis be used in the planning statements. Obligations and contingent obligations that are covered by footnote in the annual report to shareholders can be disclosed by oral or written commentary in reviewing the annual plan (or long-range plan) with management or the board of directors.

LONG-RANGE FINANCIAL PLAN

The strategic plans and long-range financial plans are much less detailed than the annual business plan. Accordingly, summarized data may be the only information formulated and provided to the management and the board of directors—unless, of course, they desire more detail, or if, because of great risks and the like, it is imperative these groups fully understand the debt status. In arriving at the planned indebtedness levels for the long-range plan, the process is much as implied in Exhibit 12.5; that is, the plans are summarized year by year in sequence. If more capital is required to meet cash outflow or to correct an unsatisfactory current debt picture, then long-term capital is planned. If it appears the marketplace will accept indebtedness under suitable terms, then borrowings can be assumed. If the long-term debt percentage would be too high or if service coverage would be insufficient, then the sale of equity may be the route necessary. Again, the objective of the financial officers should be to maintain the company in such good financial health that, under most circumstances (good times or poor), it should be able to secure any needed capital under reasonably acceptable terms.

EXHIBIT 12.9 SUMMARY OF PLANNED LONG-TERM DEBT

MANAGING LIABILITIES: SOME PRACTICAL STEPS

We have reviewed the objectives of liability management, planning the liabilities, and, among other things, provided some of the standards to measure the amount of current debt as well as long-term debt. While the concerns of the controller and other financial executives have been addressed, perhaps it will be helpful to summarize some of the desirable steps in properly managing liabilities. Because of the differing nature of the various types of liabilities, it is practical in the accounting, planning, and control activities to treat each group separately. Here, then, are some suggestions as to what the controller might do to assist in properly managing the liabilities:

- Current Liabilities

- Plan the liabilities by month or quarter or year as may be applicable (as in the annual business plan or longer-term strategic plan). This can be accomplished after the various assets levels (cash, receivables, inventories, plant, and equipment) are planned and when the operational plans (sales, manufacturing expenses, direct labor, direct material, selling expense, general and administrative) are completed.

It is practical to group the current liabilities according to the categories to be identified in the Statement of Estimated Financial Position, such as accounts payable, accrued salaries and wages, accrued expenses, accrued income taxes, notes payable.

The accounts payable plan or budget, when finalized, for the annual plan might appear as in Exhibit 12.10. The budget or plan for all current liabilities, by quarter, for the annual plan could be somewhat as in Exhibit 12.11. Note that certain pertinent ratios are shown.

- Test the plan for compliance with credit agreements or other internally developed standards such as current ratio, inventory turns, net working capital, and industry average or competitor performance. If necessary, modify the plan.

- Analyze each line item for ways to reduce the obligation, for example, use of JIT inventories to reduce accounts payable or notes payable. “What if' analyses of actions on other assets (terms of sale, etc.) or liabilities can be made to improve the status, if warranted. Take any appropriate action.

- Monitor the monthly or quarterly balances for any unfavorable developing trends, and take appropriate action.

- Issue the appropriate control or informational reports, such as to the supervisor of accounts payable, board of directors, or creditors. This might include updating the projected debt status to the year end.

- When appropriate, as in major developments, revise the financial plan.

EXHIBIT 12.10 ACCOUNTS PAYABLE BUDGET

EXHIBIT 12.11 SUMMARY—CURRENT LIABILITY PLAN

- Plan the liabilities by month or quarter or year as may be applicable (as in the annual business plan or longer-term strategic plan). This can be accomplished after the various assets levels (cash, receivables, inventories, plant, and equipment) are planned and when the operational plans (sales, manufacturing expenses, direct labor, direct material, selling expense, general and administrative) are completed.

- Long-Term Liabilities

- Plan the long-term debt, by appropriate category, as in Exhibit 12.9, for the annual plan, or strategic plan, based on the commentary or factors reviewed in the chapter.

- Test the plan, before finalizing, against credit agreement requirements, or standards for debt capacity, including that which might exist under the least favorable business conditions which are likely to prevail in the planning period. Adjust the plan, if required.

- Monitor actual performance or condition periodically during the plan term for unfavorable developments, and take appropriate action.

- Report on the financial condition and outlook to the appropriate interests (bankers, bondholders, board of directors, etc.).

- As to All Indebtedness Items

- Review the accounting to ascertain that GAAP are followed, to the extent practical.

- Periodically have the internal controls checked to assure the system is functioning properly.

- Keep reasonably informed on the status and probable trend of the debt market, and the new debt instruments, both short and long term. If appropriate, this includes foreign markets. Such information may be gained from informal discussions with commercial bankers as well as investment bankers. Perusal of financial and business literature or periodicals also may be helpful.

Additionally, the controller and other financial executives should be sensitive as to the impact of new debt issues on the holders of existing debt.

By following these few commonsense practices, there should be no unpleasant surprises regarding the management of liabilities.

ACCOUNTING REPORTS ON LIABILITIES

Reports with respect to the status and management of liabilities will depend on the business needs. A limited number are necessary for monitoring the actual status and to disclose the results of short- and long-term planning. A suggested list includes:

- Usual monthly statement of financial condition perhaps by organization segment, comparing actual and planned status

- Monthly or quarterly comparison of actual liabilities with amounts, by detailed category, as compared with permitted amounts under credit agreements

- Planning reports comparing required indebtedness as compared to credit agreements and debt capacity

- Periodic analysis of special liabilities, whether actual or contingent:

- Long-term leases

- Unfunded pension plan liabilities

- Exposures of various health care plan trusts and so forth

- Foreign currency exposure

- Aging of payables

- Comparison of actual and budgeted obligations

- Detailed liability reports as required by credit agreements

- Periodic summaries of contingent liabilities and likely actual liability

The controller should prepare those reports for financial management, or general management, as appropriate, to guide the business, with suitable oral or written commentary.

INTERNAL CONTROLS

Internal control of liabilities runs the gamut from routine accounts payable and payroll disbursements to the periodic payment of notes payable under the various indenture terms and the like.

A fundamentally sound routine for the recording of liabilities is basic to a well-founded disbursements procedure. The essence of the problem is to make certain that no improper liabilities are placed in line for payment. Routines must be instituted to see that all liabilities are properly certified or approved by designated authority. The proper comparison of receiving reports, purchase orders, and invoices by those handling the detail disbursement procedure eliminates many duties by the officers; but the liabilities not covered by these channels must have the necessary review. The controller or treasurer, for example, must approve the payrolls before payment. The chief purchasing agent, or chief engineer, or treasurer, or some official must approve invoices for services, because no receiving report is issued. Certain special transactions may require the approval of the president. Again, invoices for such items should be checked against the voucher file for duplicate payments. In summary, the controller should consider the system of recording payables somewhat independently of the disbursements procedure to give added assurance that the necessary controls exist.

Moreover, if computers play a large part in processing liabilities, much acceptable software is available. However, the existence and extent of internal controls should be checked.