Chapter Fourteen

Topspin

Case Studies: Bruce Lee • General Sun Tzu • Frank Zhao, S&P • Uri Lopatin, Pardes Biosciences • Oscar Munoz, United Airlines • Marc Benioff, Salesforce • Dara Khosrowshahi, Uber • Reed Hastings, Netflix • Melanie Perkins, Canva • Jamie Dimon, JPMorgan Chase Ngozi Okonjo-Iweala, WTO • Werner Baumann, Bayer • Max Levchin, Affirm Holdings • Ben Silbermann, Pinterest • Albert Bourla, Pfizer • Mike Tuchen, Talend • David Zaccardelli, Verona Pharma • William Nash, CarMax • Apoorva Mehta, Instacart • Ronald Reagan

Absorb what is useful, Discard what is not, Add what is uniquely your own.1

Tao of Jeet Kune Do

Bruce Lee

Martial arts movie superstar Bruce Lee was also an avid scholar and reader. Among the more than 2,500 books in his library2 was Sun Tzu’s The Art of War. In respectful acknowledgement of the General’s inspiring words, “to subdue the enemy without fighting,” Lee had his character in his film Enter the Dragon say:

My style? You can call it the art of fighting without fighting.3

Lee also provided inspiration of his own in his philosophical writings. Just as the martial arts is metaphor for Buffering, Lee’s closing phrase in the quote above is a metaphor for Topspin:

Add what is uniquely your own.4

■ Topspin ■

Topspin is the polar opposite of spin. The latter has a negative connotation because of its pervasive use by politicians, spin doctors, communications counselors, media consultants, and public relations advisors who urge their clients to deliver their own messages. Unfortunately, many of those clients do so by following in the dysfunctional footsteps of Robert McNamara you read about in Chapter Eleven. His words serve as a perfect definition of Spin:

Never answer the question that is asked of you. Answer the question that you wish had been asked of you.5

You have every right to deliver your own message, your Point B, and accompany it with a boatload of WIIFYs to your audience, but only after you have answered your audience’s questions. McNamara’s misguidance is the “never” part. Replace that with “always” provide a quid pro quo answer or a valid reason for not answering. Earn the right to Topspin.

You’ll note that the icon in Figure 14.1 contains multiple upward swirls—to encourage you to add multiple variations of Topspin beyond your answers. Consider the multiple swirls as stretch goals—just as athletes do when they increase the difficulty of a drill in practice to heighten their execution in the actual event.

Figure 14.1 Topspin

The swirls are meant to address the tendency of presenters to neglect to ask for the order, or state their Point B, making the audience think “What’s the point?” or, as snarky teenagers put it, “And your point is?” Or the tendency of presenters to neglect to offer benefits, making the audience think, “Why should I care?”

Topspin to Point B and/or a WIIFY answers both of those questions affirmatively.

Culminating your answers with positive words produces persuasive results. Frank Zhao, a senior director of quantitative equity research at S&P, conducted a study on natural language processing, which found that:

Firms whose executives most frequently articulated references to growth- and expansion-related descriptors around I) revenue II) earnings or III) profitability topics outperformed their counterparts by 9.16%, 8.60% and 6.76% per year, respectively.6

At its most basic, Topspin adds value to your answer—which is particularly important when the answer is a deep technical or scientific dive.

Uri Lopatin, MD, is both a physician-scientist and a serial entrepreneur, and although he has spent much of his career successfully developing and building new biotech companies, he never loses sight of the science. As the CEO of Pardes Biosciences, a company that develops novel oral antiviral medicines, Uri worked with me to prepare for the company’s investor roadshow. In our sessions, Uri wanted to demonstrate the early potency data of a Pardes investigational drug with scientific evidence, and he did so with the slide in Figure 14.2.

Figure 14.2 Pardes Biosciences Slide

Because most investors do not have advanced degrees in chemistry or biology, I asked Uri to explain the slide. He began with this description:

What you see on the left is that this drug candidate is very potent on an absolute basis in lung-like cells—as we give more drug (x-axis), it suppresses virus replication (the y-axis) all the way to the limit of detection (maximal effect). On the right we see that effect mapped differently—as a percentage of maximum effect. It takes a very small amount of drug (x-axis) to achieve the maximal effect (y-axis), in the absence of any toxicity to cells (lower straight line).

When he finished, I said, “Now tell me why this slide should matter to investors.”

Uri replied:

The reason this is important to you as an investor is, to be successful, biotech companies want our drugs to be very potent against our target—in this case part of a virus, without hurting other things (toxicity) in cells. In general, the “stronger” or more “potent” a drug is—the less of it we need to show a desired effect. We use these numbers—which reflect effects in cells—to understand our target dose in humans. This [graph] suggests we have a potent drug candidate in cells, and we are optimistic that we can exceed these levels in humans, so what you are looking at is some of the data that support advancing into human clinical trials. If we are correct, we are very excited by the potential to see similar effects on virus in humans.7

By concluding the technical information with a WIIFY, Uri made the slide meaningful both to investment fund managers who are not scientists, as well as to analysts who are—and who must evaluate whether the science is sufficiently viable and stable to warrant an investment.

As a matter of course, I have the same exchange with every presenter who wants to deliver complex information—whether it is data analytics, genome sequencing, silicon circuitry, Artificial Intelligence, or software coding—to financial audiences. I ask that, following the description of technical material, the presenter adds a sentence that begins with:

The reason this is important to you as an investor is…

… and then concludes with Topspin to a WIIFY.

That same approach is applicable in every other direction—with financial pitches to scientific audiences and in every presentation to every audience. Your audience must fully understand your Call to Action and the reason for them to act.

While Topspin adds value to the answer to any question, it becomes even more valuable after the answers to the Seven Universal Issues because it counterbalances the challenges in the questions—particularly questions about serious problems.

![]()

(Video 43) WATCH LIVE: United Airlines CEO Oscar Munoz, Other Airline Executives Face House Committee https://youtu.be/WzmMXzq-w0I?t=8646

United Airlines suffered an infamous public relations black eye when, to accommodate airline employees traveling to meet their schedules, security officers forcibly removed a passenger from a sold-out flight and injured him in the process. Another passenger recorded the incident on a mobile phone, and the video went viral on social media. In the aftermath, United’s stock took a hit.8

The airline did its best to rectify the incident, but the subject came roaring back to the public forefront a month later in a televised congressional hearing on transportation and infrastructure. During the hearing, Representative Lloyd Smucker (R–PA) tore into United’s CEO Oscar Munoz:

I am very disappointed that you are not changing, or at least not mentioning a change to the policy of how you would select a passenger for removal. That is unbelievable to me, that, after that has occurred, you would not take, for instance, the very last passenger that shows up at the gate, rather than some other algorithm to choose an employee. So, I am very disappointed about your response, in that regard.

Munoz Buffered to the one neutral word in Smucker’s scolding:

Our policy…

Then he told Smucker what he wanted to know: how United planned to adjust their policy to avoid the problem in the future:

…our practice, our go forward sort of situation would be, as much as possible, to ameliorate the possibility of those actual events happening. And with regard to reducing our overbooking, making sure crews get there on time, and, most importantly, once you are on board one of our aircrafts, you will not be removed, and certainly law enforcement will not be allowed, other than for safety or security. So, I think we have covered most of those issues…

Having provided a quid pro quo answer, Munoz moved on to Topspin by offering a WIIFY to customers:

…and, of course, we will offer incentives and financial remuneration, along with alternative solutions to get to your destination…

And a WIIFY to Smucker:

So, it is a start, sir, and I think we will move forward. You will see us do that…

And a Point B to Smucker:

…and I hope I do earn your trust.9

Because he demonstrated transparency and accountability about a major problem as well as a plan to avoid its recurrence, Munoz was able to use Topspin to counterbalance the negativity. May all of your problems be minor, but when they occur—and they will occur—you can follow the steps Munoz took:

Buffer to neutralize.

Be transparent and accountable.

Provide a quid pro quo answer.

Topspin to Point B and/or a WIIFY.

Earn the Right

Let me culminate the value of Topspin by reinforcing an important requisite: you must earn the right to Topspin by first providing the quid pro quo answer. The politicians who characteristically slip, slide away from answers with Robert McNamara-instigated stonewalling or the equally unacceptable “whataboutism” and jump directly to Topspin—have not earned the right to do so.

Nor has the presenter who reacts to a challenging question about formidable competition by replying:

Let me describe our competitive advantage.

Nor has the presenter who reacts to a challenging question about high prices by replying:

When you consider the total cost of ownership of our solution, you’ll see that it will save you money in the long run.

In both cases, the Topspin is leapfrogged into the Buffer without having provided an answer. You saw both of these defective cases in Chapter Eight and again with the Buffer and in Chapter Eleven with the answer. The tactic invalidates the questioner and the audience.

Never Topspin in the Buffer. Use the Buffer only to identify and neutralize the key issue. Move on to provide a quid pro quo answer to your audience’s question. Only then can you Topspin.

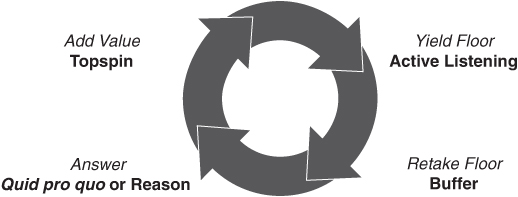

■ The Suasive Q&A Cycle ■

Topspin culminates all the skills you need to handle each step of the Q&A Cycle you first saw in Chapter Five, in Figure 5.1. I’ve repeated the image here as Figure 14.3, this time with the addition of the techniques you’ve learned in what is now the Suasive Q&A Cycle:

Figure 14.3 The Suasive Q&A Cycle

Yield the Floor: Use Active Listening and subvocalization to identify the Roman Column.

Retake the Floor: Buffer to the Roman Column to neutralize.

Answer: Provide a succinct quid pro quo answer or a valid reason for not answering.

Add Value: Topspin to Point B and/or WIIFY.

The Suasive Q&A Cycle and the Seven Universal Issues

Let’s now apply the full Suasive Q&A Cycle to each of the Seven Universal Issues.

1. Price/Cost

Question: Where do you get off charging so damned much?

Buffer: Our pricing rationale is…

Answer: Describe product capabilities, compatibility, added services, or the total cost of ownership.

Topspin: In the long run, you’ll actually pay less.

After the Buffer strips out the “so damned much” and the answer provides a rationale for the pricing, the Topspin then counterbalances the challenge by saying, essentially, that the product is worth the price.

![]()

(Video 44) Salesforce CEO Marc Benioff: Slack Deal Makes Salesforce “a Whole New Type of Company” https://youtu.be/4PCGu343LS8?t=6

Marc Benioff, the founder, chair, and CEO of Salesforce.com, the giant Customer Relationship Management (CRM) company, paid $27.7 billion to acquire Slack, a business communication platform.

Jim Cramer, the host of CNBC’s Mad Money, whose attempt to rattle Peter Rawlinson of Lucid Motors you read about in Chapter Twelve, tried the same aggressive tactic with Marc Benioff. When Marc appeared on the program, Cramer fired off a “Why did you pay so much?” question delivered with his characteristic strident edge:

OK, so look, I know—I know your deal style! And I’ve been listening to these different analysts and some are saying the deal’s too big! And some are saying he has to do it because he’s out of growth! And here’s one:

Cramer held up a fistful of papers and read from the top sheet:

“Salesforce Engagement, they gotta do it! The timing is curious…”

With a dramatic wave, Cramer flung the sheet in the air behind him and read from the next page as if he were a football announcer excitedly calling a touchdown:

…[Microsoft’s]“Teams has already won!” I mean this guy’s saying that all the time. I hear the deal’s too big! How are the last two too-big deals?

Marc neutralized the “big deal” by removing the loaded adverb “too” as well as the judgmental adjective “big” and Buffering with just the neutral “acquisition”:

Well, Jim, of course whenever you do an acquisition…

Then he pivoted to the purpose of the acquisition:

Customers are re-architecting how they are working. They’re building a 360-degree view of their customers. They’re building a 360-degree view of their employees. They have—they want the ability to work from anywhere and connect to their customers from anywhere.

Next, Marc added Topspin with a WIIFY to investors:

And you look at the opportunity today, incredible! Number one, selling from anywhere. I mean, there’s never been a more important point in history to have your B2B [Business-to-Business] sales force or even your B2C [Business-to-Customers] sales force to be able to connect directly with your customer or service from anywhere.

He added another upward swirl to the Point B of the acquisition:

Our customers are performing so well because that’s how our product was built from the beginning. Now with Slack it provides this incredible, incredible window into a collaborative interface onto all of our services…

And then he culminated with Topspin to a WIIFY for “the whole enterprise”:

…and the whole enterprise as well.10

Marc Benioff responded to Jim Cramer’s challenge—that he paid too much for Slack—by telling him that the purchase was worth the price. In Chapter Eight, you read how Uber CEO Dara Khosrowshahi faced the opposite charge—by Cramer’s CNBC colleague Andrew Ross Sorkin—that the company’s IPO was priced too low.

![]()

(Video 45) Watch CNBC’s Full Interview with Uber CEO Dara Khosrowshahi Ahead of Its IPO https://www.cnbc.com/video/2019/05/10/watch-cnbcs-full-interview-with-uber-ceo-dara-khosrowshahi-ahead-of-its-ipo.html

Let’s look at Khosrowshahi’s response that began with a Buffer:

Pricing a deal is an art not a science…

...and then continued on to position the price in relation to stock market conditions and the interests of shareholders:

…so, we will probably have had it imperfectly, but we thought at this price, it reflected the environment. And listen, the environment is uncertain right now. Anytime there is uncertainty in the market, investors are going to be a little hesitant to put eight billion of their dollars to work, and we wanted to put our stock with a group of funds who we know aren’t just going to hold for the next week, but they are going to hold for the next year and hopefully for the next five years.

Khosrowshahi then concluded his answer with Topspin to Uber’s Point B, the true value of the price:

So, when we looked at the environment and we balanced how we really think of this company long term, this was a great result. Eight billion is plenty for us to build and grow on top of.11

While one CEO was charged with paying too high a price and the other with pricing an offering too low, both responded to the charges with a positioning rationale and a strong reaffirmation that the price they settled on was right.

2. Compete/Differentiate

Question: What on Earth makes you think you can survive?

Buffer: The way we compete is...

Answer: Describe competitive strategy, product innovation, strategic partnerships, customer success, industry praise, or market share.

Topspin: I’m confident that not only can we compete effectively but that we will succeed in this market.

![]()

(Video 46) Netflix Q2 2018 Earnings Interview https://www.youtube.com/watch?v=xZN_PwZdsLA&feature=emb_logo

We return to Reed Hastings of Netflix for a third time in this book because every step of his response to an analyst’s question about the competitive threat posed by the powerful Walt Disney company serves as a perfect role model for every one of the techniques you’ve learned: Buffering, quid pro quo answer, and Topspin. Let’s revisit the entire sequence:

Analyst Question: Moving to the other elephant that was already in the room, just checking a bit on the competitive landscape. Obviously, a lot going on between Disney and Comcast and Fox and Sky, so need to check in and—and hear what you’re thinking in terms of what impact on Netflix, however that result turns out and there’s any particular result better or worse for your own competitive fortunes.

Buffer: There’s a lot of new and strengthening competition with Disney entering the market—HBO getting additional funding, the different French broadcasters coming together...

Answer: So that’s all normal and expected. So, it is what it is, we’re not going to be able to change it. Our focus is on doing the best content we’ve ever done, having the best user interface, the best recommendations, the best marketing—all the things that we’ve been doing for many years in the past…

Topspin: …and we’ll keep doing for many years in the future.12

![]()

(Video 47) E939 Canva CEO Melanie Perkins: On Growing Australian College Startup into Global Unicorn w/15m MAUs https://youtu.be/8TBSg79Gf0M?t=2081

Jason Calacanis is a successful entrepreneur and angel investor; as such, he always has the competitive landscape uppermost in mind. In an interview on his podcast with Melanie Perkins, the CEO of Canva, a graphic design platform, Calacanis asked her:

Did Adobe create a competing product, or are they threatened? You think they’re threatened by you guys, or they just think it’s like a different class of user?

Perkins was not about to be presumptuous enough to position Canva as David to the Adobe Goliath:

I don’t know, we just kind of stick to doing our thing—like we’ve got a really strong focus on serving our community, and that’s really where our team’s attention and focus is.

Calacanis smiled at her diplomacy:

You got some media training!

But he still wanted her to address her competition:

What about all these other competitors? I know there were, like, a ton of them—Figma, Visually—all these ones but, none of them have hit any kind of scale. What—what do you think the differentiator has been for Canva?

This time, Perkins went right to the differentiator:

Right from the start, we really set out to solve a really significant pain point…

She proceeded to discuss how Canva’s online collaborative platform addressed the growing market demand—a requisite subject for investors—by providing graphic design at low cost.

Then Perkins concluded with validation that her company was succeeding— which was her Topspin to Canva’s Point B:

It’s been pretty powerful. I’ve been just blown away by our community. So, we’ve got 150,000 YouTube videos that have been made about Canva. People are tweeting about it. They’re having their own Facebook groups with, you know, tens of thousands of people. Just all over the place.13

Like investors, business reporters also have competition uppermost in their minds.

![]()

(Video 48) JPMorgan CEO Jamie Dimon on Markets, Economy, Returning to Office https://youtu.be/x8-eUse5hg8?t=14

In an interview with Jamie Dimon, chair and CEO of JPMorgan Chase, Bloomberg’s Ed Hammond made competition the point of his second question:

You recently told your bankers they should be scared expletive—about the threat posed by financial technology companies and others coming into the industry. Isn’t that a bit defeatist?

A survivor of many financial crises and a lion of the banking industry, Dimon was not about to admit defeat:

A little bit, but I didn’t mean it quite that way. So many years ago, we sent an airplane full of people to China to go over competition. So, JPMorgan itself is doing great…we just have to be prepared for intensified competition. We’re ready for it.

In dogged pursuit, Hammond wanted details:

But prepared how? What does that mean? Do you have to go and buy something?

Dimon was ready with details galore:

No. So, we already have 5,000 branches. We’re opening all—we’re opening another 400 next couple years in all 48 states.

And of course, Topspin to JPMorgan Chase’s Point B:

We’re very competitive, and we expect to win.14

3. Qualifications/Capabilities

Question: What makes you think you can be any good at being the CEO of a public company when you’ve never done it before?

Buffer: My qualifications include…

Answer: Describe prior experiences that map to the new role, such as having run a unit of a public company on a profit and loss basis, or having run the private company as if it was already public. Add that board members and other senior staff have had public company experience.

Topspin: Taken together, I’m confident that I can not only meet the challenge effectively but continue the success we’ve had as a private company as we become a public company.

![]()

(Video 49) WTO: I Am the Most Qualified for the Job—Okonjo-Iweala [FULL VIDEO] https://youtu.be/XZcVUPaMbnA?t=130

In Chapter Eight you read how Dr. Ngozi Okonjo-Iweala effectively Buffered a reporter’s challenging question about her qualifications to be Director-General of the WTO. Look at her response again and you’ll see that her Buffer went directly to the Topspin with her Point B:

I hope I’m the candidate that is chosen and is backed because I think I have the qualifications and the leadership characteristics to do the job and I’m sure Africa will come behind my candidacy.15

Dr. Ngozi was clearly so confident about her qualifications, she didn’t bother to rebut or offer counterevidence or proof points.

![]()

(Video 50) Bayer CEO Baumann: ‘Way Too Early’ to Say on Roundup-Related Cash Call https://www.bloomberg.com/news/videos/2020-02-27/bayer-ceo-way-too-early-to-say-on-roundup-related-cash-call-video

During the Bloomberg Television business program Surveillance, co-anchor Anna Edwards asked Werner Baumann, the CEO of the Bayer pharmaceutical company, about the qualifications of his company’s Supervisory Board:

Does the Supervisory Board, with the strengths that you’ve just described—is there a lack of expertise though in agriculture and in the U.S.—in the areas that you are experiencing these difficulties—do you, I mean, the new chairman comes with, I think, an accounting background—a German business background—do you think that you need more expertise in the supervisory board on agriculture in the U.S. business?

Rather than deal with “lack of expertise,” Baumann Buffered to neutralize by saying:

If you look at the composition of our board…

He then went directly into his proof points, detailing the credentials of individual members who had served on the boards of PwC, the United Nations, J&J, and Gilead Sciences and then concluded by countering the lack of expertise charge with Topspin to Bayer’s Point B.

So, I would say very, very strong balance of expertise at the board.16

We can’t know whether Baumann was familiar with the S&P study on positive language from earlier in this chapter, but he certainly spiced up his answer with four uses of the adverb “very” in his reply, concluding with a double “very” in his Topspin.

4. Timing

Question: What’s taken you so long?/Why don’t you wait?

Buffer: We chose this time because…

Answer: Describe readiness, timing, or trends.

Topspin: That’s why I’m confident that this is the right time.

![]()

(Video 51) Watch CNBC’s Full Interview with Affirm CEO Max Levchin https://youtu.be/Rkq8sf5NSBM?t=360

When Morgan Brennan, the co-anchor of CNBC’s Squawk on the Street, had an opportunity to interview Max Levchin, she knew that, as the co-founder of PayPal, the enormously successful payments company, as well as two other startups, Levchin would be priming his latest company, Affirm Holdings, for the public market. Following suit, Brennan asked him what was taking him so long:

I gotta ask about Affirm. Plans to go public?

Levchin laughed and explained the time factors:

You know, the company is eight years old. At some point, your investors start making hints and elbow gestures. So, at some point, yes. I’m not in the huge hurry. But I think that the biggest curse of a Silicon Valley company, or any technology company can do to itself is go public at a valuation that’s somewhere between two and five billion dollars. Once you clear that, your stock becomes a little bit more stable, but the volatility you take on as a two billion dollar stock, one billion dollar stock, you know, wake up the next morning and you’re suddenly half the evaluation.

Then, in his Topspin, Levchin reaffirmed Affirm’s Point B—that waiting to go public was the prudent choice:

So, the volatility is probably the primary reason companies like mine are hesitating.17

As interested as CNBC’s investor audiences are for new opportunities, the audience and attendees at the startup-focused TechCrunch Disrupt Conference are even more eager to rush to market, go public, and get rich as fast as possible.

![]()

(Video 52) Live from Disrupt SF 2017 Day 1 https://youtu.be/NhrIKJyWeus?t=17283

So, when Ben Silbermann, the co-founder and CEO of Pinterest, the social media network, sat down for a fireside chat with TechCrunch’s Matthew Lynley, the reporter promptly asked Silbermann what was taking Pinterest so long to go public:

It seems this year, especially after Snap went public, a lot of people were just racing to get out there. The window—IPO window—was opened. Why wait? Why, why continue to stay private?

Rather than racing to get out, Silbermann wanted to grow his company:

I still think that we’re working on building our core advertising systems. We’re working on growing our user base, and then the other reason is we’ve been really fortunate. We’ve been fortunate to have investors that are willing to kind of go with us on this journey.

Then, in his Topspin, Silbermann confirmed the rationale for waiting, Pinterest’s Point B.

So, we didn’t want to take on the overhead this moment of being a public company when we felt like there was a lot of stuff we could do and we had the capital, and the runway to do it.18

Waiting for the right time proved judicious for both Silbermann and Levchin. When Pinterest went public, its stock rose 28% on its first day of trading19; and Affirm Holdings jumped 98% on its first day.20

Waiting was not what Albert Bourla advised.

![]()

(Video 53) Pfizer’s CEO Hasn’t Gotten His Covid Vaccine Yet, Saying He Doesn’t Want to Cut in Line https://www.cnbc.com/2020/12/14/pfizers-ceo-hasnt-gotten-his-covid-vaccine-yet-saying-he-doesnt-want-to-cut-in-line.html

As the CEO of Pfizer, the global pharmaceutical company, Bourla appeared on CNBC’s Squawk Box at a very low point in the COVID-19 pandemic, when both the infection and death rates were soaring, and the unproven vaccines had yet to be released. Health and science reporter Meg Tirrell asked him a “Why not wait?” question:

What do you tell those folks who might be saying, “I am going to wait a few months before I get this one”?

In Bourla’s opinion, waiting was not a wise option:

I would tell them I wish the situation was not so critical so that they can have the luxury to think about it. But the situation is as deadly as it could be right now, with the amounts of deaths or new cases that we are facing. So, they need to think it wise[ly]…

Bourla concluded his answer with Topspin to a WIIFY for all humans:

The decision not to vaccinate will not only affect your health or your life unfortunately, it will affect the lives of others and likely the lives of the people you love the most…

Then, he added a universal Point B:

Trust science.21

5. Growth/Outlook

Question: How do you plan to increase your revenues?

Buffer: Our growth strategy is…

Answer: Describe new products, new markets, or new partnerships.

Topspin: That’s why I’m confident that we can continue to attract new customers and enter new markets to generate new revenues.

As the CEO of Talend, a cloud integration company, Mike Tuchen took the company public and then led it on an ascending path of hockey stick growth. He shared that story in his presentation at the JMP Securities Technology Conference. After his presentation, Mike sat down for a fireside chat with Greg McDowell, JMP’s Managing Director, who asked how Talend intended to continue its streak:

I think one of the most impressive components of this story, as you mentioned, is the eight quarters in a row of accelerating growth, and I guess I just wanted to start with sort of what gives you the confidence that, you know, the tailwinds you have in this market are—are going to continue?

Mike began his response by Buffering with a synonym for “tailwinds”:

Right now, those big trends…

Then he gave Greg substantive details and evidence:

…big data and cloud are just like a freight train, and those things are not slowing down. And so really for us, as we become the best in the market in those areas, our win rates are going up, our deal latencies are decreasing. So, we’re selling more, and we’re selling it faster. And as a result, our sales productivity is going up.

Next, Mike went on to Topspin with a WIIFY for investors:

So, everything is telling us right now that these, not just these huge trends are gonna continue…

And another swirl of Topspin to a Point B for Talend:

…but our position with them is looking very secure.22

Greg McDowell’s question about whether the tailwinds are going to continue was about the outlook for Talend being able to maintain a positive momentum. A negative variant of the Growth/Outlook question arises out of a problem and is usually phrased as “What are you planning to do to keep the problem from happening again?” or “How do you plan to fix the problem?”

Question: Your last product missed the release date by a month. How do I know that that it won’t happen again with the next product?

Buffer: Our new product production plan is…

Answer: Describe new checklists, personnel, monitors, tools, or systems.

Topspin: I’m confident that not only will we release the product on time, but it will be error-free and fully functional.

In Chapter Nine you read about how Adam Kiciński, the joint CEO of CD PROJEKT, was able to handle a long three-part question from an investor. The first was about a three-week delay in releasing the company’s latest game and culminated with a “How do I know this this won’t happen again?” question.

Question: Going back to what you said in the middle of June when you last delayed the game — I think you specifically ruled out delaying it again beyond November 19. My question is why is it different this time; why you’re confident that you can get this game out on December 10?

Buffer: We are in a very different situation now…

Answer: …releasing on the 19th was possible as well, but we believe that having these extra three weeks will enable us to get more things ready to our satisfaction.…we’re glad to have more time and believe this is the right move. I know three weeks doesn’t seem like a long period…

Topspin: …but it actually doubles our available time starting from the moment the decision was made; this can greatly help us with those technical matters regarding current-gen.23

6. Contingencies

In Chapter Two, I compared business audiences to customers considering an automobile purchase: both kick the tires. Business audiences want to know whether potential problems have been anticipated and they usually phrase such questions as “What are you going to do if…?”—also known as a Contingency question.

Question: What are you going to do if one of your leading customers goes with one of your competitors?

Buffer: Our contingency plan is…

Answer: Describe customer concentration, new products, or new markets.

Topspin: I’m confident that we can continue to maintain and even grow our revenue stream.

In an earnings call, Verona Pharma, a public company that develops treatments for respiratory diseases, announced positive results for their Ensifentrine drug in a Phase 2 trial called ENHANCE. But Jefferies Financial Group analyst Suji Jeong questioned the results with a “What are you going to do if?” question:

[If the] ENHANCE program doesn’t show benefit in exacerbation rate, do you plan to run additional studies to show exacerbation benefits?

Verona CEO David Zaccardelli, knowing full well that investors do not like to hear about additional studies because they cost more money and take more time, promptly diffused the risk potential by putting the exacerbation factor into context:

As you know, the ENHANCE trials are not specifically designed to be exacerbation endpoint studies, both by numbers of patients as well as duration.…We will look at that after the studies are completed and determine if that is something that we’d want to do.

And then he concluded with Topspin to Verona’s Point B:

But we—at this time, don’t believe it’s essential for the success of Ensifentrine.24

A variation of the “What are you going to do if…?” question is the “What are you doing to do when…?” question. During an earnings call for CarMax, the large used-car retailer, CEO William Nash was asked such a question by Exane BNP Paribas analyst Chris Bottiglieri:

Once we exit this bizarre credit world that we’re in, where losses are lower, right, but higher unemployment, if things go back to kind of pre-COVID trends. Do you expect the change in fee structure to stick?

Nash Buffered:

It’s hard to say if it’s going to stick.

Then he answered:

This is a very fluid environment. We’re always looking to optimize the platform clearly. Clearly, it’s a very positive credit environment in which we’re operating right now.…One thing I want to drive home is, again, our structures with our partners; we have many partners in place. They provide the quality offers that we are able to give our customers in all the economic times, bizarre economic times and good times as well…

And then he concluded with Topspin to CarMax’s Point B:

We’re poised for growth. So, we feel real good about our platform right now.25

7. Problems

Question: What keeps you up at night?

Buffer: What is top of mind for me is meeting our production schedule…

Answer: Describe adding more capacity, personnel, or check points.

Topspin: By doing so, I’m confident that we can fulfill our customers’ expectations on time.

![]()

(Video 54) Instacart CEO on Scaling the Business to Meet Covid-19 Pandemic Demand https://youtu.be/a9dAvY_nX_U?t=165

In an appearance on a CNBC financial program, Apoorva Mehta, the CEO of Instacart, an online grocery delivery service, proactively posed the “What keeps you up at night?” question as a rhetorical question and provided his own answer:

You know, a lot of times people will ask me what keeps me up at night. Well, what would keep me up at night is when one of our groceries is not growing fast enough, and you’re not able to be there for the customers enough.

He then described what his company was doing to help groceries grow faster:

At Instacart, we provide not only all the picking technology, all the delivery technology, we also give the retailer the ability to be there for their customer, whether it’s on their apps or on the e-commerce platform…

Mehta then added Topspin with a WIIFY for the retailer’s customers (Instacart’s customers)—consumers:

…the ability to really merchandise and create the same wonderful experiences that they had in the offline world…

And then concluded with Topspin to Instacart’s Point B:

…and to do that online.26

The Suasive Q&A Cycle Summary

You can counter any charge—that accuses your company, product, or service of being too expensive, too cheap, too small, too big, too late, too early, too light, too heavy, too narrow, too broad, too anything—with Topspin. But you must first neutralize the negativity with a Buffer and provide a substantive answer directly related to the Roman Column in the question before you Topspin.

As good as are all the preceding Topspin exemplars, there is still one better: a Topspin delivered by the Great Communicator.

Topspin Coda

![]()

(Video 55) Reagan–Mondale Debate: The Age Issue https://youtu.be/LoPu1UIBkBc

Ronald Reagan was 73 years old when he ran for a second term as president. His opponent, Walter Mondale, a senator from Minnesota, was 56 years old. When the two candidates met for a debate at the Municipal Auditorium in Kansas City, a panel of journalists posed questions. One was Henry Trewhitt, the diplomatic correspondent for The Baltimore Sun, who asked President Reagan:

You already are the oldest president in history, and some of your staff say you were tired after your most recent encounter with Mr. Mondale. I recall yet that President Kennedy had to go days on end with very little sleep during the Cuba missile crisis. Is there any doubt in your mind that you would be able to function in such circumstances?

Reagan replied promptly with a crisp three-word answer:

Not at all.

And then he delivered a Topspin for all time:

And, Mr. Trewhitt, I want you to know also I will not make age an issue of this campaign. I am not going to exploit for political purposes my opponent’s youth and inexperience.27

The audience broke into peals of laughter and so did Mondale, who knew he was in the presence of a master of the game.

You can follow the examples of positive role models above by listening, Buffering, answering, and then pivoting to Topspin—your own cause with Point B and/or the benefits to your audience, their WIIFYs.

In your practice, prompt yourself and/or your colleagues by using the gesture that I use when I coach my clients: Point your forefinger skyward and twirl it: Topspin.