Chapter 8

Squeezing Out Every Last Drop of Profit

In This Chapter

![]() Examining whether a firm is a profit maximizer

Examining whether a firm is a profit maximizer

![]() Looking at how a firm maximizes profits in the short and long run

Looking at how a firm maximizes profits in the short and long run

![]() Understanding how firms minimize costs

Understanding how firms minimize costs

Economists tend to begin their analysis of firms with the assumption that the firm is a profit maximizer — that is, the firm’s ultimate aim is making the most profit it can. Although microeconomics doesn’t stop there (and has produced a number of more in-depth analyses of managerial motivation and results that don’t rely on this assumption), the profit-maximizing firm is the basic building block of microeconomic analysis.

In this chapter we justify the idea that a firm is in practice a profit maximizer. We also look at profit maximization more closely, showing how it rests at the heart of economists’ conception of efficiency and how profit-maximizing firms choose the optimum amount of stuff to produce. In addition, we also discuss the opposite approach to achieving the same end: minimizing costs while maintaining the desired output.

Take a moment to catch your breath. You have quite a ride ahead!

Asking Whether Firms Really Maximize Profits

In most cases, economists assume that firms want to maximize their profits and that, as a result, they make their decisions on this basis.

Here’s a possible objection to this assumption: Economists are thinking about a firm as a very simple decision-making unit, quite unlike the complex entities that firms are in reality. All the following conditions characterize the standard approach to the firm in economics:

Here’s a possible objection to this assumption: Economists are thinking about a firm as a very simple decision-making unit, quite unlike the complex entities that firms are in reality. All the following conditions characterize the standard approach to the firm in economics:

- Managers act in the interest of shareholders whose goal is profit maximization.

- Management has unified interests.

- There are no internal issues between or inside internal divisions of the firm.

- People turn up on time and do the job for which they’re employed.

- There are no hidden incentives not to make profit in the tax system.

Suppose you know nothing about a company and you don’t know that all those things are the stuff of working life. How would you then make a representation of a firm? What goals, behaviors, or practices would you guess that this representative firm would engage in?

In this scenario, profit maximization is a reasonable assumption to make. Of course, if you know about particular reasons why a given entrepreneur has made a decision, you can guess at a lot more information about the firm. But if you know next to nothing about the individual case, the only assumption that makes sense is that the firm intends to maximize its profits.

In this scenario, profit maximization is a reasonable assumption to make. Of course, if you know about particular reasons why a given entrepreneur has made a decision, you can guess at a lot more information about the firm. But if you know next to nothing about the individual case, the only assumption that makes sense is that the firm intends to maximize its profits.

None of this, of course, means that profit maximization is always the goal of the organization. As a simple example, think of a company whose shareholders want to receive the highest possible level of returns, whereas the management of the company wants to hold on to their jobs or take as many of the potential returns for themselves. If the managers have sufficient bargaining power over the shareholders, they can affect the decisions of the firm in their own interests.

Talking about efficiency, in the long and short run

When a firm maximizes its profits effectively, it’s acting efficiently. Economists like efficiency and deplore waste. Whatever you do in business, they prefer that you make efficient use of your capital and other resources. If you take the lowest point of the average cost curve — where the marginal cost curve crosses the average cost curve — you’ve found the most efficient level of production. In addition, profit maximization occurs at the point where marginal revenue equals marginal cost (that is, MR = MC). See Chapter 7 for much more on this. Let’s take a moment now to explore — ahem, efficiently — why these two efficiency conditions are so important.

When economists discuss efficiency, they’re most likely talking about the following two conditions:

- Productive efficiency: Exists when output is being produced at a level that minimizes the average total cost of production.

- Allocative efficiency: Exists when making one party better off is impossible without making another party worse off (also called Pareto efficiency after celebrated Italian economist Vilfredo Pareto).

These two definitions are distinct, meaning that satisfying allocative efficiency without satisfying productive efficiency is possible. To see why, we look at the two concepts in a bit more detail.

Productive efficiency: Producing for the lowest possible cost

Productive efficiency is satisfied when a firm can’t possibly produce another unit of output without increasing proportionately more the quantity of inputs needed to produce that unit of output. It’s met when the firm is producing at the minimum of the average cost curve, where marginal cost (MC) equals average total cost (ATC). (Sometimes you will see ATC as just AC, or average cost. They mean the same thing.)

Productive efficiency is satisfied when a firm can’t possibly produce another unit of output without increasing proportionately more the quantity of inputs needed to produce that unit of output. It’s met when the firm is producing at the minimum of the average cost curve, where marginal cost (MC) equals average total cost (ATC). (Sometimes you will see ATC as just AC, or average cost. They mean the same thing.)

Why is that? At the minimum of the average total cost curve, economies of scale are exhausted, and production at this level yields the lowest per unit cost. The firm is producing an output level at the lowest possible cost. If a firm expands production beyond that point, it incurs a marginal cost higher than the average cost, and the per-unit cost of output increases. Recall the profit-maximizing conditions discussed in Chapters 3 and 7. A firm maximizes profits by producing where marginal revenue equals marginal cost, or MR = MC. If this occurs at the same output level where MC = ATC, then profit maximization leads to productive efficiency.

In Chapter 13, you can use the concept of productive efficiency to tell you a lot about how a market is operating. One application we mention here is in considering how society should treat natural monopolies — those companies that yield sufficient economies of scale relative to the size of the total market that they’re unlikely to ever face a direct competitor. One thing economists notice is that these companies tend to operate inefficiently; that is, that they don’t tend to operate at the lowest possible cost (and that consumers are consequently hurt by this, as inefficiencies get pushed on to the consumer in the form of lower quality or quantity and/or higher prices).

Figure 8-1 summarizes productive efficiency: The two shaded areas reveal how the firm can become better off by making itself more productive.

© John Wiley & Sons, Inc.

Figure 8-1: Productive efficiency.

Allocative efficiency: Can you make one party better off without making another worse off?

Allocative efficiency is related to the concept of Pareto efficiency that economists use to look at social welfare (see Chapter 12 for more on that), but it has important aspects that are driven by efficiency in production. Essentially, if something is allocatively efficient, one party can’t possibly be made better off without making another party worse off. Here’s a simple example to illustrate the point: Suppose Alice and Bob are allocated money from a central pot of $100, and you record the allocations twice:

- In the first round you allocate the whole $100, and Alice and Bob each get half, $50. Now within this framework, you can’t give either Alice or Bob more without making the other worse off, and so the distribution is allocatively efficient.

- But if you hold back $1 and distribute $99 to Alice and Bob, any distribution between the two isn’t allocatively efficient, because you can simply release the $1 and make either party better off, without making the other worse off!

In the context of production, when a firm is operating at lowest possible cost, it’s also allocating efficiently its budget for inputs between capital and labor. This occurs — you guessed it! — when the average cost of the firm is at a minimum.

Chapter 12 uses this concept of efficiency when it talks about welfare in general. For the moment, we just want to introduce the idea that when all firms operate at their minimum cost, welfare in society is maximized.

Checking the long and the short run

Economists distinguish between the long- and short-run positions of a firm. They do so because a firm can find itself, in the short run, in a number of positions where it is constrained. It can’t fully react to change immediately and therefore makes slightly different decisions than it would if there were no constraints — in other words, different than it would in the long run if it were fully capable of reacting to whatever change (pricing, technological, demand, and so on) was taking place.

Economists want to be more precise about what the terms long run and short run mean, without specifying a particular time interval (for example, a month) that will be different for firms in different industries. For example, finding an exploitable oil deposit may take longer than writing a couple lines of code. The definition economists use is conceptually simple: In the long run, the firm is able to change its use of all factors of production — labor, capital, and land. In the short run, the firm is not able to do that; it’s limited to imperfect adjustment, usually of only one factor, often labor.

As an example, imagine that a firm employs ten people to do a job working on ten machines. And suppose the wage it pays its workers has become more expensive, so that the firm would be better off employing only eight machines and eight people. But the lease for the machines is not up until the end of the year, whereas it can lay off workers at any time:

- In the short run: The firm adjusts its use of labor without adjusting its use of capital or machinery — having nine people operate the ten machines. Over this short-run period, the firm isn’t operating at its most effective use of resources.

- In the long run: After the firm negotiates a new lease, it can operate even more cheaply. Assuming profit maximization is its aim, it moves towards doing so.

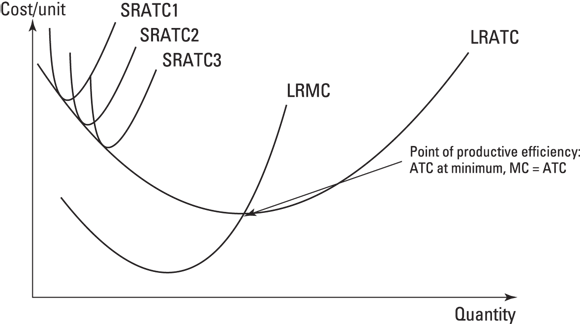

Microeconomists express this situation by looking at costs in the short and long run. To an economist, any short-run average total cost (SRATC) curve must be by definition less elastic — that is, less responsive to price — than a long-run average total cost (LRATC) curve. Therefore, in a diagram, a SRATC curve is steeper, reflecting the lower ability to adjust in the short run (as costs go up, output doesn’t change as much as in the long run). The LRATC is always less than or equal to the SRATC at any given output level, reflecting the fact that the firm can use its inputs more efficiently in the long run than in the short run.

Figure 8-2 illustrates this condition. Remember that a short-run marginal cost curve goes through the minimum of each of the SRATC curves, and the long-run marginal cost (LRMC) is more elastic — price and cost responsive — than in the short run.

© John Wiley & Sons, Inc.

Figure 8-2: Costs in the short and long run.

Going Large! The Goal of Profit Maximization

Now it’s time to find out a little more about the profit-maximizing process. To do so, we need to make a few little extensions to the model of the firm used in Chapter 7 to take account of how the firm changes its decisions when the costs of inputs change. And to do that, we’re going to express output in terms of two inputs — capital and labor — and their respective prices, the cost of capital and the wage rate.

Firms can use two methods to work out how to use their inputs to make outputs: the profit-maximizing approach of this section and the cost-minimizing approach (see the later section “Slimming Down: Minimizing Costs”). Although eventually they lead to the same place — assuming you do the relevant calculations right! — they arrive via slightly different journeys. Wherever you’re going, though, you need a place to start, and we begin with a production function.

Understanding a production function

A production function is a mathematical description of how a firm makes its output. For a simple firm with only one input, a production function may be expressed by the following:

![]()

Here, f is the firm’s production function, and x1 is the amount of an input — for example, labor. If you know the amount of the input x1 and the shape of the function f, then you know how much output the firm will produce. We now add the second input — holding it constant because we’re going to look at the short run first — and then use a little math to figure out the relationship between output and costs.

We call the production function f, the two inputs x1 and x2, and their respective costs w1 and w2. We begin by spelling out the production function:

![]()

That shows a relationship between inputs and outputs but not profit: The f part of the expression explains that there is a relationship between the amount of output produced and the level of inputs engaged in production, the x1 and the x2. For the moment, we’re not spelling out exactly what that relationship is mathematically. To know about the firm’s profits, we need to know about the revenue gained from selling the output and the cost of obtaining the inputs. The revenue side is very simple if the firm sells its output all at the same price p. Then if you know the output level, multiply it by price (p) and you have total revenue (TR):

![]()

And for total costs (TC):

![]()

Because we’re holding the second input constant in the short run, we call it x2. It won’t be changing, and so we can treat it as a constant.

From the original production function, we can combine the two preceding equations to make a profit function that we want to maximize:

![]()

Meeting the isoprofit curve

We now substitute output, y, for the production function for a moment and use that to draw a picture. Again, we’ll use the Greek letter π for profit. The equation is now like this:

![]()

We want to use this equation to derive an isoprofit curve, which is a curve on which all points yield the same level of profit. In the preceding equation, profits could change if p, y, or one of the ws or one of the xs changes. On an isoprofit curve, we hold π, profits, constant for any point on the same curve, and we plot the relationship between inputs and outputs for a given level of profit. We rearrange the equation so that y is on the left-hand side:

![]()

This equation shows that the terms on the right-hand side and specifically all those terms that don’t include an x1, are constant. The intercept is where the curve intercepts the y axis. The expression on the right, referring to x1, gives the slope of the line, ![]() .

.

Looking at profit maximization using isoprofit curves

Now we turn to the concept of the marginal — the incremental change (see Chapter 7). In this case, the incremental change we’re interested in is the change in production at the margin. The slope of the production function is the measure of how production changes as x1 changes. In general, the marginal change in output is called marginal product, but here the relationship only exists between x1 and output, because we kept x2 constant.

Figure 8-3 illustrates maximization using the short-run production function f(x1,x2) with x2 held fixed, and three isoprofit curves. Only isoprofit 2 is possible and optimal. Why?

© John Wiley & Sons, Inc.

IP1 = isoprofit 1, IP2 = isoprofit 2, IP3 = isoprofit 3

Figure 8-3: Profit maximization for one factor using three isoprofit curves.

At isoprofit 2, the marginal product (MP, slope of the production function) is equal to the cost of the input used divided by the price received at market for your output. Or to put it more succinctly:

![]()

To discover what this means, we ask Jeph the Joiner, proprietor of Jeph’s Joinery. He has a job at the moment making chair legs for an interior designer. He wants to know, given that all his equipment is fixed in the short run, how many people to employ at a given wage in order to make as much profit as possible. His cousin Emma the Economist takes a look at his figures and says that he should employ up to the point where the contribution of the marginal worker is such that multiplying the output produced by the marginal worker by price equals the wage that Jeph will pay.

Jeph knows his hardwoods but not his margins and asks for the answer with less jargon. Emma says: “Suppose you’re making your chair legs and you know that the next one — the marginal one — is going to yield $10 in revenue. Now suppose you have to hire someone for a cost of $11 to make the leg. If the cost is greater than the marginal revenue, you make yourself better off by not producing that unit ($11 is greater than $10 and you’d lose $1 on the output). If the cost of hiring is only $9, though, you’d make a surplus of $1. You can make yourself better off still, assuming that you can sell the product, by hiring up until the cost of hiring equals the value of the marginal product — that is, the marginal revenue — you yield from selling the output.”

Microeconomics lays great stress on the concept of the margin for exactly this reason. The best that a firm can possibly do is when the marginal benefit it gets is equal to the marginal cost of achieving it.

Maximizing profit in the long run

Here’s a quick question for you: What’s the difference between the short and the long run to an economist? If you say that in the long run all factors are variable, you’re correct! If not, take a look at the earlier section “Talking about efficiency, in the long and short run” before reading on. When you’re clear on this issue, you can go on to the next section, safe in the knowledge that extending the model to two inputs isn’t so difficult.

I wonder if, after reading the preceding section, you want to say, “Hang on a minute; that situation’s unrealistic — only one factor changes!” You’re right, because in the example Jeph’s Joinery is considering only the short run. What happens in the long run?

An output level that minimizes average costs in the short run could lie on the long-run average cost curve (refer back to Figure 8-2) and be the best possible option in the long run too. We use that fact to point out that the only thing that has changed when moving to the long-run equilibrium is that now the last equation in the preceding section must apply to each input and not just one. Thus for two inputs x1 and x2 you get a pair of conditions:

![]()

![]()

Here, * denotes that these are the optimal levels of inputs given the cost of inputs.

Profit-maximization problems tend to follow these forms, though they can get more complicated than this simple presentation. Sometimes economists are interested in a different (though related) type of question, such as what to do if the price of one input changes but not the other, or what happens when firm technology changes. The next section discusses an adaptation of the model for that — the cost-minimization model.

Slimming Down: Minimizing Costs

The preceding section discusses a firm maximizing its profit by choosing a level of inputs that allows it to produce a given level of profit. Now we rearrange the problem slightly and assume that the firm wants to reduce its costs to the minimum level while producing a desired level of output. To do so, the firm chooses how much to use of two inputs, called x1 and x2, as defined in the earlier section “Understanding a production function.” But unlike in that section, we want to choose a way of minimizing the cost.

Economists write this problem in a new way, using two equations to represent it:

The min means choose values of x1 and x2 that make everything in the equation (w1x1 + w2x2) as small as possible. The values we’re choosing for the inputs are optimal values, and we call those x*1 and x*2, with the * meaning an optimal value.

The second equation, which uses the production function, shows all the feasible combinations of inputs that produce a desired level of output. This is called an isoquant — meaning that all points or input combinations on an isoquant yield the same level of output, in this case y. Now we alter the first equation to see another facet of the equation: We look for a given level of cost, which we denote C. We do so by rearranging a little:

![]()

Rearrange this so that you can put the input x2 on the vertical axis in the graphs (see Figure 8-4), and you get this:

![]()

© John Wiley & Sons, Inc.

Figure 8-4: Isocosts for the cost-minimizing firm.

In this rearrangement of the equation, the quantity of x2 used is a function of constant level of cost and the relative price of x1. Given that the price of x1 is w1, the relative price of x1 is w1/w2. Now, when plotted on a graph, it becomes a straight line with a slope of –w1/w2 and an intercept on the vertical axis of C/w2.

We allow C to change to create a set of lines, each of which has the same total cost, and has the same slope of –w1/w2. Called isocosts (see Figure 8-4), these are all downward-sloping parallel lines. Every point on an isocost has the same cost and higher isocost lines have higher costs.

The final step is to put the isoquant and isocost together. We restate the problem as finding a point on an isoquant line with the lowest possible isocost associated with it. This happens at a point of tangency between the isoquant and isocost, which is a more mathematical way of saying that at the optimal point or input combination, the slopes of the isocost and the isoquant are equal (see Figure 8-5).

© John Wiley & Sons, Inc.

Figure 8-5: Cost minimization using isocosts and isoquants.

The only input combination that can be optimal to use is the point where the two curves are tangent. Taking a look at the isoquant, you can see that an infinite number of combinations of inputs can make up that fixed desired level of output. However, point A for example is on a higher isocost than the optimal and therefore wouldn’t be chosen, because the same output can be produced for a lower cost, and the firm wants to minimize those costs.

You can derive a cool further condition from knowing about the slopes of the isoquant and isocost and how they must match. Remember that the slope of something is generally an indication of how much it’s changing at a given point. Economists are interested in what the changes along the isoquant reveal about the marginal product (MP) of the two inputs x1 and x2, and what the ratio of the marginal products says about the technology a firm is using.

The slope of the isocost must match the slope of the isoquant. You already know the slope of the isocost: –w1/w2. You also know that the slope of the isoquant matches the ratio between the prices of the inputs. Now the slope of the isoquant is the ratio of the marginal product of each of the inputs, and so at the optimum point:

![]()

The bit on the left side is the ratio between the marginal products of the two inputs at the optimum. It’s also known as the technical rate of substitution, because it describes the rate at which a firm gives up one input in order to add increasing units of another input while keeping output constant. Because economists generally assume diminishing productivity when substituting, the isoquant must slope continuously downwards when production technologies are what economists call well behaved — this captures diminishing returns to substituting one unit of one input for one unit of another.