CHAPTER 2

Applications

While chapter 1 highlighted the principles of equity pricing from a rather theoretical point of view, we want to focus now on practical aspects: we will discuss a few commonly used stochastic volatility models and applications to Cliquet pricing; we will also address the pricing of payoffs that depend on the realized variance of an asset. In particular, “variance swaps” have become very liquid instruments and trading volumes are set to grow even further. The respective options on variance are an attractive new class of products on which to work.

2.1 CLASSIC EQUITY MODELS

In section 1.3.2, we discussed how we can construct martingales that fit a given initial option price surface, the most popular approach being Dupire's implied local volatility. We have already mentioned that in practice, it is rarely possible to obtain a continuum of option prices. Another problem with using an “implied” model is that it does not allow us to control the specific dynamics of the resulting actual stock price process. In this sense, we want to stress that a model that fits very well to some market does not at all guarantee that it produces acceptable prices: for example, consider a stock for which only forwards are traded, but no options. Then a “perfectly fitting” model would be given by a deterministic stock price process.1 In this case it is obvious that this “model” cannot be correct if we want to price options on the stock. This argument can be carried over to volatility models: The mere fit of a model to European option data does not imply that it gives sensible hedges or prices for exotic payoffs. For this reason, it makes sense to take a “structural” point of view and model the stock and its volatility directly, using a particular assumption on the SDE it satisfies. We will review here a few of such classical stochastic volatility models.

2.1.1 Heston

By far the most popular model is probably Heston's stochastic volatility model [19]. It is given as a solution to the SDE

![]()

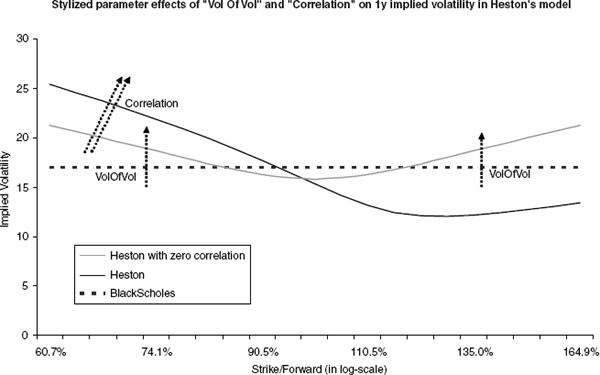

FIGURE 2.1 Stylized effects of changing vol of vol and correlation in Heston's model on the 1y implied volatility. The “Heston” parameters are ζ0 = 15%2, θ = 20%2, κ = 1, ρ = 70% and ν = 35%.

where W = (W1, W2) is a two-dimensional standard Brownian motion. We call κ the “speed of mean reversion” or “mean reversion speed,” ![]() the “long vol,” ν the “vol of vol,” ρ the “correlation,” and the initial value

the “long vol,” ν the “vol of vol,” ρ the “correlation,” and the initial value ![]() the “short vol.” We also refer to θ as “level of mean reversion.” The two parameters vol of vol and correlation can be thought of as being responsible for the skew. This is illustrated in figure 2.1: vol of vol controls the volume of the smile and correlation its “tilt.” A negative correlation produces the desired downward skew of implied volatility. The other three parameters control the term structure of the model:2 In figure 2.2, the impact of changing short vol, long vol, and mean reversion speed on the term structure of ATM implied volatility is illustrated. It can be seen that short vol lives up to its name and controls the level of the short dated implied volatilities, while long vol controls the long end. Reversion speed controls the skewness or “decay” of the curve from the short vol level to the long vol level.

the “short vol.” We also refer to θ as “level of mean reversion.” The two parameters vol of vol and correlation can be thought of as being responsible for the skew. This is illustrated in figure 2.1: vol of vol controls the volume of the smile and correlation its “tilt.” A negative correlation produces the desired downward skew of implied volatility. The other three parameters control the term structure of the model:2 In figure 2.2, the impact of changing short vol, long vol, and mean reversion speed on the term structure of ATM implied volatility is illustrated. It can be seen that short vol lives up to its name and controls the level of the short dated implied volatilities, while long vol controls the long end. Reversion speed controls the skewness or “decay” of the curve from the short vol level to the long vol level.

Note, however, that the distinction of the parameters by their effect on term structure and strike structure above was made for illustration purposes only: In particular, κ and ν are strongly interdependent if the model is used in the form (2.1). Indeed, κ is meant to be the “speed” of the process, but it does not feature in the volatility term of the variance. This is counterintuitive in the following sense:

FIGURE 2.2 The effects of changing short vol, long vol, and mean-reversion speed on the ATM term structure of implied volatilities. Each graph shows the volatility term structure for 12 years. The reference Heston parameters are ζ0 = 15%2, θ = 20%2, κ = 1, ρ = 70% and ν = 35%.

Consider the time change t′ := κt, such that

The process (ζt/κ)t can be seen as being in “unit speed,” κ = 1. From this point of view it would be more natural to parameterize the process ζ in (2.1) as

![]()

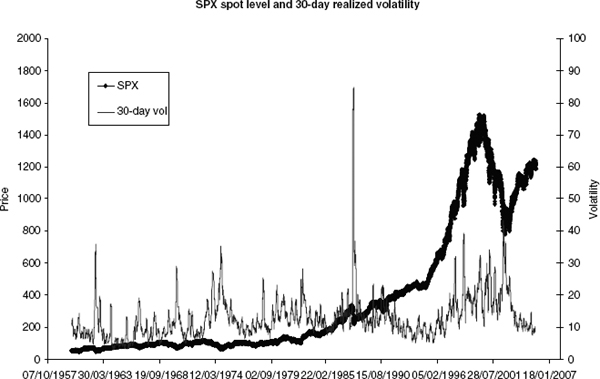

Properties of Heston's Model One of the most attractive features of Heston's model is the fact that its variance is mean reverting. Such a mean-reverting feature is commonly seen in real market data; see also figure 2.3. Moreover, its calibrated correlation of around −70% is quite stable over time and produces, as we will show, a relatively good fit to the market's implied volatilities, at least for maturities beyond three months. (Figures 2.6, 2.7, and 2.10 show examples of calibrating Heston and other models to market data.)

However, Heston's popularity is probably mainly derived from the fact that it is possible to price European options on X using a semiclosed-form Fourier transformation, which in turn allows rapid calibration of the model parameters to market data.

The underlying mathematical reason for the relative tractability of Heston's model is that ζ is a squared Bessel process, which is well understood and reasonably tractable (cf. Revuz/Yor [13]). In fact, a statistical estimation on SPX by Aït-Sahalia/Kimmel [20] of α ∈ [1/2, 2] in the extended model

![]()

FIGURE 2.3 Historic SPX quotes and estimated 30-day variance. Apart from occasional spikes we can identify the mean-reverting nature of the variance. It should be noted that the level of mean-reversion itself also varies over time.

has shown that, depending on the observation frequency, a value around 0.7 would probably be more adequate. What is more, the square-root volatility term means that unless

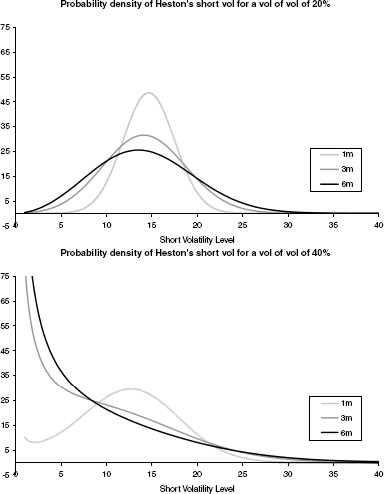

the process ζ can reach zero with nonzero probability. The crux is that this conditions is regularly violated if the model is calibrated freely to observed market data. While a vanishing short variance is not a problem in itself (after all, a variance of zero just implies that nobody trades), it makes numerical approximations more complicated. In a Monte Carlo simulation, for example, we have to take the event of ζ being negative into account. The same problem appears in a PDE solver: Heston's PDE becomes degenerate if the short vol hits zero (cf. section 9.4). A violation of (2.3) also implies that the distribution of short variance at some later time t is very wide (see figure 2.4).

Additionally, if (2.3) does not hold, then the stock price X may fail to have a second moment if the correlation is not negative enough in the sense detailed in proposition 3.1 in Andersen/Piterbarg [21]. Again, this is not a problem from a purely mathematical point of view, but it makes numerical schemes less efficient. In particular, Monte Carlo simulations perform much less well. Although an Euler scheme will still converge to the desired value, the speed of convergence deteriorates. Moreover, we cannot safely use control variates anymore if the payoff is not bounded.

Computing European Option Prices with Fourier Transforms To compute European option prices, we focus on the call price. Following Carr/Madan [22], we will price the call via Fourier inversion (see also Lewis [23] for a detailed overview of the subject). Let, as before,

FIGURE 2.4 This graphs shows the density of ζt for one, three, and six months for the case where condition (2.3) is satisfied (left side) or not (right side). Apart from the vol of vol, the parameters were ζ0 = 15%2, θ = 20%2, and κ = 1.

![]()

Since the call price itself is not an L2 function in k, we define a dampened call

![]()

for an α > 0 (see Carr/Madan [22] for a discussion on the choice of α). We also denote by φt the density and by φt the characteristic function of log Xt. Then,

We can then price a call on X using

![]()

The method also lends itself to Fast-Fourier transformation if a range of option prices for a single maturity is required.

Heston's Characteristic Function Let us now show how we can compute Heston's characteristic function,

![]()

We present here an approach that is mathematically not rigorous, but very intuitive. See Heston's original work for a more precise derivation of the characteristic function. We have

where ![]() is the complex measure associated with the density

is the complex measure associated with the density ![]() We have

We have ![]() du for a

du for a ![]() -Brownian motion Bz. This implies that under

-Brownian motion Bz. This implies that under ![]() , the process ζ satisfies

, the process ζ satisfies

![]()

Here, Wz is a ![]() -Brownian motion with a correlation of ρ with respect to Bz. We can therefore compute ψ using the more general function

-Brownian motion with a correlation of ρ with respect to Bz. We can therefore compute ψ using the more general function

![]()

for a process

![]()

To this end, note that because of the Markov property of x, the process ![]() (μ, h; xt) is a martingale on [0, T]. Hence, by using Ito and division by

(μ, h; xt) is a martingale on [0, T]. Hence, by using Ito and division by ![]() obtain the PDE

obtain the PDE

with boundary condition η0(μ, h; x) = e−μ x. Since x is affine, we guess that η is an exponential of an affine function,

By solving the above PDE for this function, we obtain

and

with the constants

For the case where m is time-dependent, see section 2.1.5 below.

Simulating Heston Once we have calibrated the model using the aforementioned semiclosed form solution for the European options, the question is how to evaluate complex products. At our disposal are PDEs and Monte Carlo schemes. We briefly comment on the Monte Carlo approach: we want to simulate the Heston process (2.1) in an interval [0, T]. Since the conditional transition density of the entire process is not known, we have to refrain from solving a discretization of the SDE (2.1). To this end, assume that we are given fixing dates 0 = t0 < … < tN = T and let Δti := ti+1 − ti for i = 0, …, N − 1. Moreover, we denote by ΔWi for i = 0, …, N − 1 a sequence of independent normal variables with variance Δi, and by ΔBi a corresponding sequence where ΔBi and ΔWi have correlation ρ.

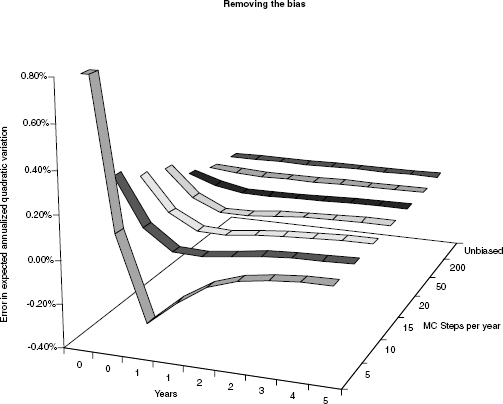

When using a straightforward Euler scheme, we will face the problem that ζ can become negative. It works well simply to reduce the volatility term of the variance to the positive part of the variance, that is, to simulate

![]()

A flaw of this scheme is that it is biased. This is overcome by using the moment-matching scheme

FIGURE 2.5 Plain Euler with various steps per year vs. the unbiased scheme. The model parameters were ζ0 = 30%2, θ = 20%2, κ = 2, ρ = −70%, ν = 35%. The graph shows the error between the true and the simulated value of ![]()

which works well in practice, see figure 2.5. Higher-order schemes such as Milstein cannot be used with this process since the square root is not differentiable at 0 (this is not such a big problem if we ensure that (2.3) is satisfied). A similar approach is used to compute the stock price: Here, we note that the integral over ζt in the interval [ti, ti+1] conditional on ζti is given as

![]()

hence, we set

![]()

A powerful tool to improve the convergence of the estimation of an expectation are control variates (for the case where (2.3) holds). The idea is as follows: Assume we want to compute the expectation of a random variable X (the payoff) and denote by ![]() the estimated value of X using n Monte Carlo paths. The standard deviation of the error in this estimate is given by

the estimated value of X using n Monte Carlo paths. The standard deviation of the error in this estimate is given by ![]() (i.e., it is worthwhile to try to reduce the variance of the variable we estimate). Now assume that there is a second random variable Y (the control variate) whose expectation

(i.e., it is worthwhile to try to reduce the variance of the variable we estimate). Now assume that there is a second random variable Y (the control variate) whose expectation ![]() we know analytically.

we know analytically.

The idea is that we estimate the value of X−hY and add back the value of hY. It is clear that this scheme is unbiased if our original Monte Carlo scheme was unbiased. To compute the ideal ρ, note X − hY has the variance Var[X] − 2hVar[X, Y] + h2Var[Y], which is minimized if we set

![]()

Since we usually do not know Var[X, Y] and Var[Y], we can replace the above quantities by the estimates on the nth path. Extension of this idea to a number of control variates is straightforward (a good reference on Monte Carlo in practice is Glasserman [17]).

An efficient control variate depends by construction on the actual payoff, but if no other variance reduction techniques are used, using the integrated variance and the stock price is usually a good choice. To this end, we track in addition to ζ and X also Vi+1 := Vi + ΔiV, which is an unbiased estimator of the integrated variance

![]()

2.1.2 SABR

The SABR model introduced by Hagan et al. [24] is given as

for ![]() and X0 = x and α0 > 0. It is a blend between the CEV model (cf. example 1) and a log-normal volatility model: the former is obtained from (2.8) by using ν = 0, while the latter corresponds to β = 1. This model is very popular in interest rate modeling due to the fact that it is possible to derive approximations for the implied volatility directly from the model parameters. These approximations can then be used to interpolate the implied volatility surface in an arbitrage-free way without the need to compute European option prices numerically with subsequent computation of implied volatilities. The implied volatility for a strike k at maturity T is approximated in [24] as

and X0 = x and α0 > 0. It is a blend between the CEV model (cf. example 1) and a log-normal volatility model: the former is obtained from (2.8) by using ν = 0, while the latter corresponds to β = 1. This model is very popular in interest rate modeling due to the fact that it is possible to derive approximations for the implied volatility directly from the model parameters. These approximations can then be used to interpolate the implied volatility surface in an arbitrage-free way without the need to compute European option prices numerically with subsequent computation of implied volatilities. The implied volatility for a strike k at maturity T is approximated in [24] as

with

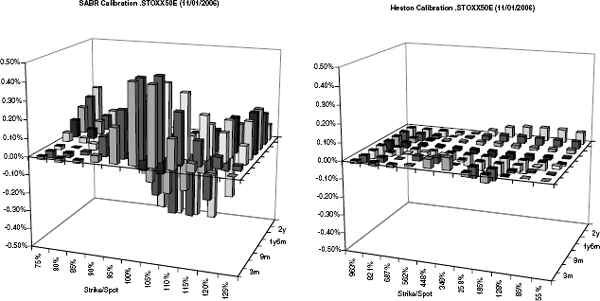

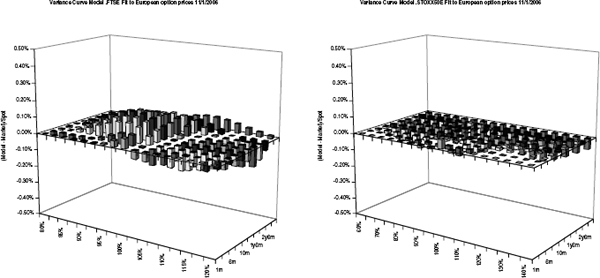

While this model is convenient for marking implied volatilities, it has a few drawbacks when used for pricing equity options. The first issue is that for the case β < 1, the stock price itself becomes zero with a nonzero probability just as the CEV process in example 1. While this might be acceptable for single stocks, this is rarely a desirable feature for index price processes. Another issue is that in the case β = 1 and ρ > 0, the stock price in this model is not a martingale, as Jourdain shows in [25]. He also shows that the model has moments up to order 1/(1 − ρ2); hence, the second moment does not exist for ![]() These problems stem from the fact that the model has a log-normal volatility, which implies that volatility can grow exponentially. However, most historic data indicate that an unbounded volatility process is rather unlikely, and that volatility should be mean-reverting in some sense (to this end, see figure 2.3 on page 38). Nonetheless, the model offers an alternative to the Heston model because it can be calibrated very quickly to observed European market prices using (2.9). At the moment, however, it does not seem to beat Heston in terms of fitting the market, as figure 2.6 shows.

These problems stem from the fact that the model has a log-normal volatility, which implies that volatility can grow exponentially. However, most historic data indicate that an unbounded volatility process is rather unlikely, and that volatility should be mean-reverting in some sense (to this end, see figure 2.3 on page 38). Nonetheless, the model offers an alternative to the Heston model because it can be calibrated very quickly to observed European market prices using (2.9). At the moment, however, it does not seem to beat Heston in terms of fitting the market, as figure 2.6 shows.

FIGURE 2.6 Calibration of SABR and unconstrained Heston to STOXX50E data for maturities from 3m to 2y. Heston appears to fit better to most indices at the time of writing. The calibrated values were α0 = 15.9%, ρ = −46.9%, ν = 78.0%, β = 0.58 and X0 = 0.75 for SABR and v0 = 15.7%2, θ = 40.2%2, κ = 0.30, ρ = −68.5% and ν = 38.3% for Heston. The SABR fit is only marginally worse for fixed β = 1 and X0 = 1, in which case the remaining parameters become α0 = 15.9%, ρ = −46.9% and ν = 78.0%.

The SABR model has been extended in several ways. In [26] Hagan et al. discuss the model with a more general local volatility function F,

for which they also present analytical approximations. Moreover, Henry-Labordère [27] discusses approximation formulas for much more general models than (2.8). In particular, he introduces a mean-reverting drift into the SDE for α and, additionally, shows how the local volatility function F in the above equations must be chosen to perfectly match the short-end skew. In a recent paper, Bourgade and Croissant [28] also work in this extended framework.

2.1.3 Scott's Exponential Ornstein-Uhlenbeck Model

Scott [29] has proposed a short-variance process, which is modeled as an exponential Ornstein-Uhlenbeck (OU) process,

This process has been investigated in depth by Fouque et al. in [30]. This model shares with the preceding SABR model the loss of the martingale property for ρ > 0 and the limitations if the second moment is to be retained (in fact, Jourdain discusses in [25] both models). From a practical point of view the problem with (2.10) is that no straightforward method is available that allows the efficient computation of European option prices or implied volatilities. It should be noted, however, that the process v itself is very easy to simulate. The complication is to simulate the stock price X, for which we have to revert to solving the SDE (2.10) via discretization. The use of control variates as discussed above improves the convergence of a Monte Carlo scheme, but again this limits us to the case where X has a second moment. However, if we want to price European options, we can make use of the following observation: let ζt := evt, then

with

![]()

Hence, we have reduced the computation of a European option to a one-factor problem. This obviously works for all “pure” stochastic volatility models where the volatility does not depend functionally on the stock price level.

2.1.4 Other Stochastic Volatility Models

The list of stochastic volatility models that have been proposed for option pricing is long. However, apart from Heston-type and SABR-type models, most stochastic volatility models do not admit an easy access to the pricing of European options or their implied volatilities.3 In contrast, for many Levy models proposed in the literature (see, for example, Overhaus et al. [31] and Shoutens [32]), the characteristic function is available, such that the approach discussed on page 38 can be used to price Europeans. Numerical methods for such models tend to be more involved than for diffusion-based models; see Cont/Tankov [33] for a good account on using Levy models in finance.

2.1.5 Extensions of Heston's Model

Using Heston's model (2.1) as a basis, we can develop a range of related models that still admit a characteristic function that can be computed more or less quickly. The first extension is a model in which the level of mean reversion is time dependent: assume that θ = (θt)t≥0 is a non-negative function and set

A good example, which we will pick up again in section 2.3.3, is θt := m + (θ0 − m)e−ct. Following the computations for Heston's model, we find that we can still write the characteristic function of log X as an exponential of an affine function as in (2.4). Indeed, the only change is that now, instead of (2.6),

![]()

If time dependency of the other parameters of Heston's model is required, we can revert to the case of piecewise constant parameters. Indeed, let us set

with functions κ, θ, ν and ρ, which are piecewise constant on 0 = t0 < … < tn. Assume that tk < T ≤ tk+1. The characteristic function of log XT is then given as

![]()

for some constants ![]() and

and ![]() By iteration, we obtain once again an exponential affine characteristic function of log XT.

By iteration, we obtain once again an exponential affine characteristic function of log XT.

In a different direction, Heston's model can be extended by adding jumps to the return process. A popular example is Bates's “Heston Jump Diffusion” [35], which is a combination of Heston's model and the jump diffusion model with normal jumps in the return as in example 2 on page 20. Since the characteristic function of the jump diffusion part can be computed easily and since the jumps and the Brownian motions are independent, the characteristic function of Bates's model is just the product of the characteristic functions of Heston's model and the Jump Diffusion model with zero short volatility (i.e., σ = 0 in (1.28)). The parameters of this model can also be made time dependent with piecewise constant values.

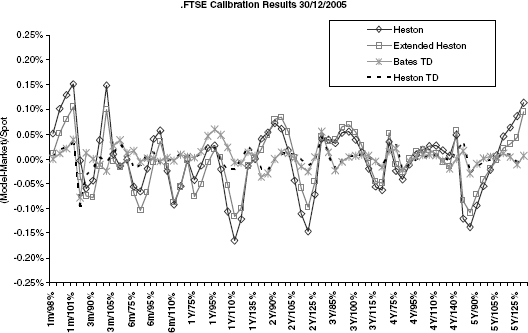

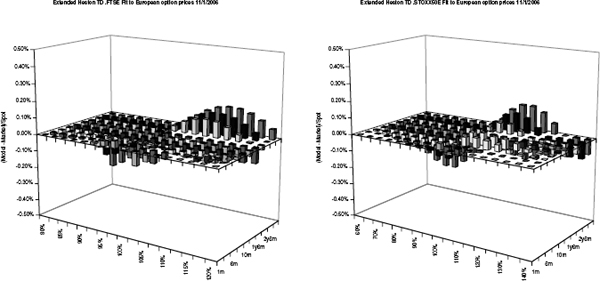

FIGURE 2.7 Various models fitted to STOXX50E for maturities from 1m to 5y. The introduction of time dependency clearly improves the fit. Figure 2.8 on page 48 shows a summary of the calibration for STOXX50 while figure 2.9 on page 48 and figure 2.10 on page 49 show the summaries for SPX and FTSE, respectively.

When the number of parameters in a model increases, it will usually also fit better to the implied volatility. In particular, the extension (2.11) is a good way of improving the short-end fit of Heston's model to the implied volatility market. If a much better fit is required, the piecewise constant time-dependent Heston model with or without jumps can be used, as is illustrated in figures 2.7 through 2.10.

However, it should be noted that by introducing piecewise constant time-dependent data, we lose much of a model's structure. It is turned from a time-homogeneous model that “takes a view” on the actual evolution of the volatility via its SDE into a kind of an arbitrage-free interpolation of market data: If calibrated without additional constraints to ensure smoothness of the parameters over time, this is reflected in large discrepancies of the parameter values for distinct periods.

FIGURE 2.8 A summary view of the calibration for STOXX50E. The extension of Heston via (2.11) in particular improves the fit of Heston's model to the short end, which is a common problem of the original model.

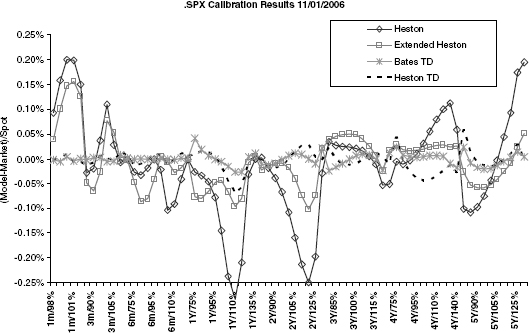

FIGURE 2.9 Calibration results for SPX. The naïve calibration for Heston gives a very bad fit that exceeds the desired 0.10% error threshold frequently.

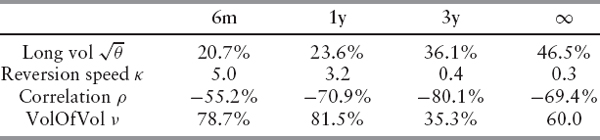

For example, the excellent fit of the time-dependent Heston model in figure 2.8 is achieved with the following parameter values (short volatility ![]() was 15.0%):

was 15.0%):

FIGURE 2.10 Calibration results for FTSE.

Moreover, the increased number of parameters makes it more difficult to hedge in such a model in practice. Even though both Heston and the time-dependent Heston models create complete markets, as discussed in section 1.4.1, we will always need to additionally protect our position against moves in the parameters values of our model. Just as for vega in Black and Scholes, this is typically done by computing “parameter greeks” and neutralizing the respective sensitivities. Clearly, the more parameters are involved, and the less stable these are, this “parameter hedge” becomes less and less reliable.

2.1.6 Cliquets

A classic group of “volatility products” in equity markets is called Cliquets. The term generally refers to contracts whose payoff depends one way or the other on the performance of an asset over a future period of time. For example, a globally floored Cliquet with a local floor of 2.5% and a cap of 5% over the reset dates 0 = t0 < … < tn = T pays

where we used the notation ![]() and

and ![]() Other, more exotic payoffs include:

Other, more exotic payoffs include:

The evaluation of such products is by far not trivial and the market has not yet settled for an agreed reference model. In fact, at least for single underlying products, a big step forward would be if it were possible to price and, more importantly, actually hedge plain forward-started options consistently. For example, a forward-started call has the payoff

Puts are defined accordingly.4

If we want to price a forward-started option of the type above, it is clear that at the reset date t1, the contract turns into a plain European option. Since such options are liquidly traded, this price must be very accurate. In other words, any model we may propose should internally be able to produce future implied volatility shapes (i.e., European option prices) that are consistent with historic behavior: we have already discussed in section 1.2.1 that the general shape of the implied volatility surface is similar over time. However, we do not necessarily need to fit the entire implied volatility surface perfectly. Intuitively, the main importance is to fit and explain well those implied volatilities at time-to-maturity of the length of the period τ := ti − ti−1, so typically one month, three months, six months, or one year.

Stochastic Implied Volatility Under these circumstances, the most natural modeling approach is to model directly the implied volatility surface (or, equivalently, the implied forward distribution or the European option prices). The first such stochastic implied volatility model (to our knowledge) was proposed by Brace et al. in [36].5 It has also been discussed by Cont et al. [38] and Haffner [39]. The idea is relatively straightforward: Let us denote by σt(T, k) the implied volatility in our model at time t for a strike k and a maturity T. We now want to model this quantity directly as a stochastic process. While it is possible to formulate this idea in terms of stochastic functions in the spirit of Brace et al. [36], we consider here the more direct approach of writing σ in terms of a sufficiently well-behaved function G and an m-dimensional parameter process Z = (Zt)t≥0 as

![]()

For example, we use a d-dimensional Brownian motion W = (W1, …, Wd) and assume that the m-dimensional process Z is the unique strong solution to an SDE

for vectors ![]()

The function G is chosen such that it gives a reasonable shape of the implied volatility for all possible parameter values ![]() This is why we have written G(z; x, c) as a function of the natural coordinates’ time-to-maturity x = T − t and relative strike c = k/Xt instead of fixed maturities and cash strikes. Ideally, the parameters of the process Z would have a direct interpretation such as level, skew, kurtosis, and term structure of the implied volatility surface. However, it should be clear that the specification of such a function and the dynamics of Z are constrained by no-arbitrage conditions: In particular, the price process of each European option should be a local martingale.6

This is why we have written G(z; x, c) as a function of the natural coordinates’ time-to-maturity x = T − t and relative strike c = k/Xt instead of fixed maturities and cash strikes. Ideally, the parameters of the process Z would have a direct interpretation such as level, skew, kurtosis, and term structure of the implied volatility surface. However, it should be clear that the specification of such a function and the dynamics of Z are constrained by no-arbitrage conditions: In particular, the price process of each European option should be a local martingale.6

The price of a call with cash strike k and maturity T at time t is given by

![]()

If the implied volatility surface is well defined, then it follows from the continuity of the stock price process that X is given in the form ![]() for some Brownian motion B and with a short variance process ζ, which is the square of the instantaneously maturing implied volatility, ζt = σt(0; Xt)2.7 In other words, the call price is a function of X and Z, and as such we can apply Ito. As a result, we obtain a regularity condition on the interplay between

for some Brownian motion B and with a short variance process ζ, which is the square of the instantaneously maturing implied volatility, ζt = σt(0; Xt)2.7 In other words, the call price is a function of X and Z, and as such we can apply Ito. As a result, we obtain a regularity condition on the interplay between ![]() , μ, ζ and ζ.

, μ, ζ and ζ.

This expression can be expanded using the standard derivatives for the Black & Scholes formula, which results in a complex PDE for ζ and μ (see Brace et al. [36] for details). While this approach is very appealing, it has the unfortunate drawback simply that no “stochastic implied volatility” model has yet been published that is not from the start a stochastic volatility model. The main problem of the entire approach is that it is very difficult to find a function G that actually ensures that the European option prices at any time t are strongly arbitrage free in the sense of definition 1.3.1 on page 16; if a model produces arbitrage situations in itself, then the “price” of a derivative computed with this model is meaningless. Indeed, it seems that the only functional forms for G so far known are those that stem from starting with price process X in the first place: this is one of the motivations of using the SABR model discussed above, for which we have approximative formulas for the implied volatilities. However, even if we use the implied volatility surface function given by, say, a Heston model (2.1) and simply see it as a function

![]()

which maps the parameters of the model to an implied volatility surface, the restrictions imposed by the no-arbitrage equation derived above are severe (also see the comments in example 5 on page 75).

REMARK 2.1.1 Instead of modeling implied volatility, we could also consider alternatives such as the call prices on the stock, its implied distribution, or the implied local volatility. The latter has been discussed by Derman/Kani in the related context of their implied trees [40].

2.1.7 Forward-Skew Propagation

To price Cliquets, we have to revert to less ambitious approaches. Note that it is, of course, possible to price a forward-started option using the Black-Scholes formula. For a given flat volatility σ, the price of such a call (2.14) on X is given as

![]()

Just as before, this allows us to define what is called the forward implied volatility of a given market price ![]() (t1, t2, k) for the call as

(t1, t2, k) for the call as

![]()

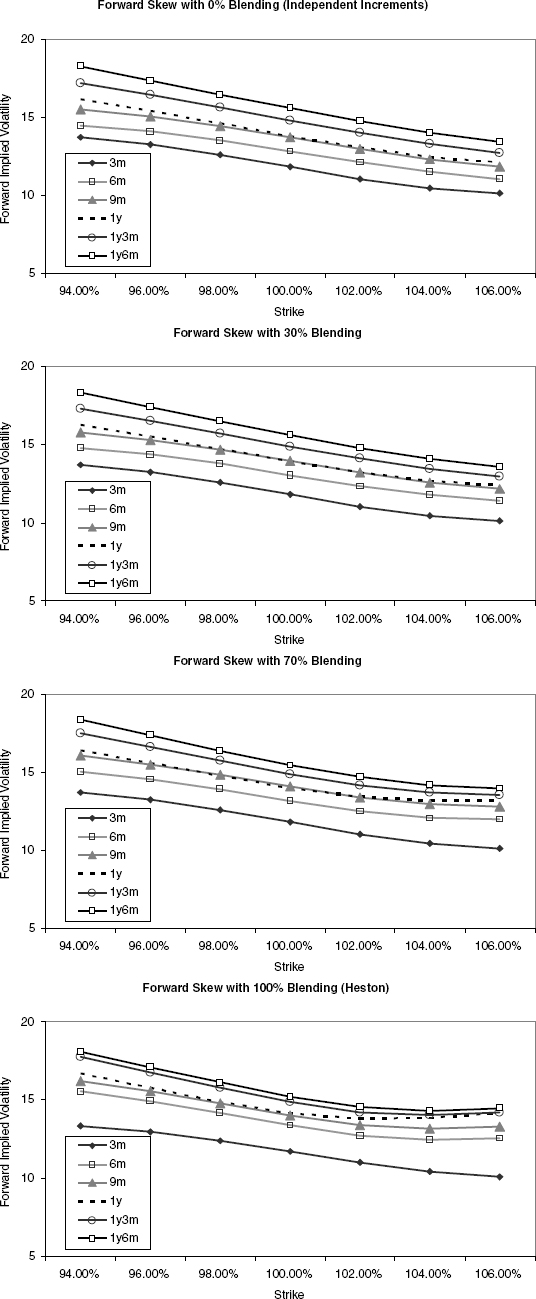

This quantity is often used as a way to quote the price of a forward-started option. For example, we call ![]() the forward skew at t1 for the period τ := t2 − t1. Given a particular model, this forward skew can be used to compare the prices of forward-started options with the same reset period τ but with different starting dates: see, for example, the fourth graph in figure 2.12 on page 82, which shows how the forward skew for τ is equal to three-month changes with the start date in a Heston model. We can clearly see that the skew becomes more and more U-shaped.

the forward skew at t1 for the period τ := t2 − t1. Given a particular model, this forward skew can be used to compare the prices of forward-started options with the same reset period τ but with different starting dates: see, for example, the fourth graph in figure 2.12 on page 82, which shows how the forward skew for τ is equal to three-month changes with the start date in a Heston model. We can clearly see that the skew becomes more and more U-shaped.

Sometimes it is required that a model “propagates the skew,” that is, that the forward skew matches the current skew for the same time-to-maturity as closely as possible. One way to achieve this works as follows: As before, denote by τ the period between two reset dates, and we assume that we can extract the distribution of St1 from the market using the second derivative in strike of standard spot-started European options. The idea is now to assume that

![]()

is independent of Yj, j = i − 1, …, 1 and that it has exactly the same distribution as Y1. This implies that the discrete stock price is given as a product of independent variables,

Such a model is called an independent increment model and by construction it will perfectly “preserve the skew.”8 Apart from the unrealistic assumption that the increment of a stock price does not depend on its past behavior in any way, this model also has the drawback that the prices of spot-started European options with maturities t2, …, tn are completely determined by the initial distribution of Y1. Consequently, the ATM spot-started options will usually not fit to the market prices. To alleviate this obvious drawback, it has been proposed to maintain the ATM implied volatility for the forward-started options in Black and Scholes and to apply a certain skew to them. These forward starts are then used to back out the assumed distribution of Yi, which is possible because of the assumption of independent increments: If all forward-started call prices are known, the forward distribution is as usual given by the second derivative of these prices in strike. Hence, a simple model of this type can be realized by jumping independently between the reset dates ti according to the forward distributions implied by the forward-started call prices.9

Blending the Skew Instead of using purely independent increments, it is often desirable to introduce some interdependency between the increments while retaining the possibility of controlling closely the shape of the forward distribution. In fact, what is needed is a model where each Yi is distributed according to some distribution μ, which is parameterized by a parameter-vector χ. If these parameters are the same for all i = 1, …, n, then the model is an independent increment model.

We want to discuss such a model now: It allows us to blend between a pure independent increment model and a real stochastic volatility model. The idea is to use the distribution in Heston's model for the forward distribution. Using previous results, we can combine the various forward distributions such that it is possible to blend between a pure Heston model and an independent increment model. Let us therefore define for the first interval t ∈ [0, t1] the initial process

The distribution of Xt1 is then controlled by the parameters ![]() To model the next increment, we again want to use Heston's model. Hence, set for t ∈ (t1, t2]

To model the next increment, we again want to use Heston's model. Hence, set for t ∈ (t1, t2]

The key is that we can introduce a dependency on the values of the previous process by letting

![]()

where we usually set ![]() to avoid jumps in the forward variance curve of the model. The blending parameter α2 allows us to blend from the independent increment case (α2 = 1) to the pure (piecewise time-dependent) Heston case (α2 = 0). The parameters for the second maturity are χ2 = (θ2, κ2, ρ2, ν2; α2). This process can then be iterated to yield a sequence of semidependent short volatilities for each interval. Additionally, the sequence θ1, …, θn can be used to fit the model to the ATM spot options.

to avoid jumps in the forward variance curve of the model. The blending parameter α2 allows us to blend from the independent increment case (α2 = 1) to the pure (piecewise time-dependent) Heston case (α2 = 0). The parameters for the second maturity are χ2 = (θ2, κ2, ρ2, ν2; α2). This process can then be iterated to yield a sequence of semidependent short volatilities for each interval. Additionally, the sequence θ1, …, θn can be used to fit the model to the ATM spot options.

While the other parameters could be chosen freely, it is in the spirit of the approach—propagating the skew—to keep κ, ρ and ν constant, because this implies that the forward distribution of Xti for i = 2, …, n has the general properties of the initial distribution for Xt1. The parameter α can be varied to assess the impact of co-correlation between the increments. Indeed, if α = 0 and if θ and the start values for each interval, ![]() are kept constant, then the model simply is an independent increment model with identically distributed increments.

are kept constant, then the model simply is an independent increment model with identically distributed increments.

FIGURE 2.11 The fit of the Heston model to the 3m skew. The calibrated parameters are ζ0 = 11.25%2, θ = 17.39%2, κ = 2.75, ρ = −65%, and ν = −51.69% (note that condition (2.3) is violated).

Of course, the general idea of randomizing the parameters of the distribution can be applied to any stock price model, but the “blended Heston skew” model described here has the advantage that the characteristic function of the logarithm of the stock price can be computed easily: in each interval, a formula of the type (2.4) holds. For i = 1, …, n we can find constants Ai and Bi such that

![]()

Iteration yields a closed form for the characteristic function. To match the very short-term options better it is possible to add a jump diffusion component along the lines of Bates [35].10

Example As an example, assume we want to price a Cliquet structure with three monthly reset periods. We have calibrated a Heston model to the following options: 3m calls on 100%, 102.5%, and 105%; 3m puts on 95% and 97.5%; and 1m and 2m calls on 100%. Since the reset period of the Cliquet we want to price is three months, we have given the 3m options twice as much weight as the other two options.

The resulting Heston model fits very well to the calibration instruments, as shown in figure 2.11.

As a next step, we have set up the above model with θi := θ, νi = ν, ρi = ρ and ![]() for i = 1, …, n. As a result, the model is just the calibrated Heston model as long as αi = 0, while it is an independent increment model if we set αi = 1; note that the increments are not exactly identically distributed because the short vol parameters

for i = 1, …, n. As a result, the model is just the calibrated Heston model as long as αi = 0, while it is an independent increment model if we set αi = 1; note that the increments are not exactly identically distributed because the short vol parameters ![]() vary. The interesting point is now the impact on the forward skew of changing α between these extreme values: Figure 2.12 shows how α blends between a skew-preserving model and a true homogeneous Markovian model.

vary. The interesting point is now the impact on the forward skew of changing α between these extreme values: Figure 2.12 shows how α blends between a skew-preserving model and a true homogeneous Markovian model.

Finally, we can assess the impact of the blending of the skew when pricing a Cliquet structure. As an example, we show in figure 2.13 what happens when we price the globally floored Cliquet (2.13).

REMARK 2.1.2 The last graph of figure 2.12 shows the usual effect that in stochastic volatility models the forward skew for start dates that are farther away tends to become more “U-shaped.” The reason for this behavior can be explained as follows: For a time-homogeneous stochastic volatility model such as Heston, the price of a forward-started call on X with reset date t1, maturity t2, and strike k is given as

with

At time t1, the implied volatility for the relative strike k and time-to-maturity τ := t2 − t1 is according to (1.22) given as

![]()

that is, it is a function of the random short variance ζt1. Due to the homogeneity of the model, the skew ![]() will be very similar in shape to

will be very similar in shape to ![]() for all reasonable values of ζt1. In particular, the “expected future skew”

for all reasonable values of ζt1. In particular, the “expected future skew” ![]() is nearly the same as

is nearly the same as ![]() (see figure 2.14). The quantity “forward skew,” on the other hand, is given as

(see figure 2.14). The quantity “forward skew,” on the other hand, is given as

![]()

Since ![]() is concave for out-of-the-money options, it follows from Jensen that we obtain the observed U-shape. It seems theoretically more natural to preserve the expected future skew instead of the forward skew. The former is a genuine property of all homogeneous stochastic volatility models.

is concave for out-of-the-money options, it follows from Jensen that we obtain the observed U-shape. It seems theoretically more natural to preserve the expected future skew instead of the forward skew. The former is a genuine property of all homogeneous stochastic volatility models.

2.2 VARIANCE SWAPS, ENTROPY SWAPS, GAMMA SWAPS

We have seen that under the assumption that sufficiently many European options on the underlying S, or X, are traded, we can price European payoffs uniquely using (1.29) or its discrete version (1.30). A particularly popular application of (1.29) is the pricing of variance swaps, suggested first by Neuberger. We also present two relatively new products, entropy swaps and gamma swaps.

FIGURE 2.12 The impact of changing the blending parameter α on the forward skew. We can clearly see the usual increasingly upward-sloping forward skew in the classic Heston model.

FIGURE 2.13 The price of the globally floored Cliquet (2.13) with maturity in two years along with the values of the prices of the involved forward-started call spreads. The price differences stem mostly from the difference in the prices of the forward-started options, rather than the global floor.

FIGURE 2.14 Forward skew and expected future skew in the Heston model.

2.2.1 Variance Swaps

A variance swap with maturity T is a contract that pays the realized variance of the return of the stock over the period [0, T] in exchange for a previously agreed strike, K2 (the strike is usually quoted in “volatility,” K). In the absence of any proportional or fixed dividends, and no risk of default, the realized variance is commonly defined as

where 0 = t0 < … < tn := T are the business days in the period [0, T]. The scaling factor

![]()

“annualizes” the returned variance: the number 252 is the standardized number of business days per year; we can think of [T] as being approximately T. If the stock price pays dividends and is subject to default risk, then we use here

where ![]() denotes the discrete cash dividend paid at tk and where

denotes the discrete cash dividend paid at tk and where ![]() proportional dividend for this date, cf. (1.10). The idea of this convention is that we do not want to count movements of the stock price that are due to (previously known) dividend payments. Indeed, if no further dividends are paid in (tk−1, tk), we obtain (cf. equation (1.6) on page 7):

proportional dividend for this date, cf. (1.10). The idea of this convention is that we do not want to count movements of the stock price that are due to (previously known) dividend payments. Indeed, if no further dividends are paid in (tk−1, tk), we obtain (cf. equation (1.6) on page 7):

In practice, default risk is not excluded as in (2.16), but by imposing a cap on the overall realized variance (discussed on page 64 ff). Moreover, dividends are in practice taken out only for single stocks; for indices, (2.15) is used. See remark 2.2.1 for the impact of dividends. Let us first consider the case where dividends are taken out (i.e., (2.16)).

Given dividend dates 0 = τ0 < … < τm = T, we have

We will assume that the right-hand side is in fact the definition of realized variance (cf. remark 2.2.1 below). A variance swap pays the actual realized variance up to its maturity T in exchange for a previously agreed strike K2. Its payoff is therefore

![]()

We will denote by ![]() the value at time t of a variance swap with strike K and maturity T. Since both

the value at time t of a variance swap with strike K and maturity T. Since both ![]() and K are constants, it is sufficient to compute the expectation (2.17) for the purpose of evaluating a variance swap, which is given by

and K are constants, it is sufficient to compute the expectation (2.17) for the purpose of evaluating a variance swap, which is given by

![]()

If ![]() is a pricing measure, and if there are no cash dividends, this means that

is a pricing measure, and if there are no cash dividends, this means that

![]()

The fair strike K*(T) for this maturity, which renders the initial value of the trade zero, is therefore

REMARK 2.2.1 Note that approximation (2.17) works well if we want to price variance swaps. However, the pathwise approximation of realized variance by quadratic variation is not perfect, as is illustrated in figure 2.15. This is particularly important if we price nonaffine payoffs of realized variance; see Barnorff-Nielsen et al. [41] for a discussion on the properties of the error.

FIGURE 2.15 The quality of the approximation of realized variance by quadratic variation. The graph shows an example path of each of the two quantities for Heston's model with the calibrated parameters from figure 2.6.

Pricing and Hedging Following Demeterfi et al. [42], we henceforth assume that the pure stock price X is continuous, and that ![]() is absolutely continuous with respect to the Lebesgue measure. We have mentioned already in section 1.1.2 that this implies that there exists a stochastic short variance process ζ = (ζt)t≥0 and a Brownian motion B such that

is absolutely continuous with respect to the Lebesgue measure. We have mentioned already in section 1.1.2 that this implies that there exists a stochastic short variance process ζ = (ζt)t≥0 and a Brownian motion B such that

![]()

where ![]() denotes again the Doleans-Dade-exponential. Accordingly, the quadratic variation of the returns of X is given as

denotes again the Doleans-Dade-exponential. Accordingly, the quadratic variation of the returns of X is given as

![]()

On [τj−1, τj) with τ > τj, we have ![]() Hence,11

Hence,11

Hence,

Let us focus for a moment on the case when there are no discrete cash dividends. We obtain

![]()

and, using ![]()

This means that we can replicate realized variance by holding a static position in a log-contract with payoff −2 log ST and by dynamic delta-hedging with a delta of Δt := 2/St− (for clarity of exposure we ignore discounting here). One particular point is that the cash-delta ![]() (2.19) is constant: we hold at all times the value 2 in the stock. Similarly, the gamma

(2.19) is constant: we hold at all times the value 2 in the stock. Similarly, the gamma ![]() implies that our cash gamma of

implies that our cash gamma of ![]() is constant, too. (In the light of the discussion below this makes a variance swap particularly suited to “trade volatility.”) For (2.18), the expression is slightly more complicated, but it is still of the same basic structure. (Note that additional terms are European-type payoffs on S, whose value can be computed using formula (1.29).)

is constant, too. (In the light of the discussion below this makes a variance swap particularly suited to “trade volatility.”) For (2.18), the expression is slightly more complicated, but it is still of the same basic structure. (Note that additional terms are European-type payoffs on S, whose value can be computed using formula (1.29).)

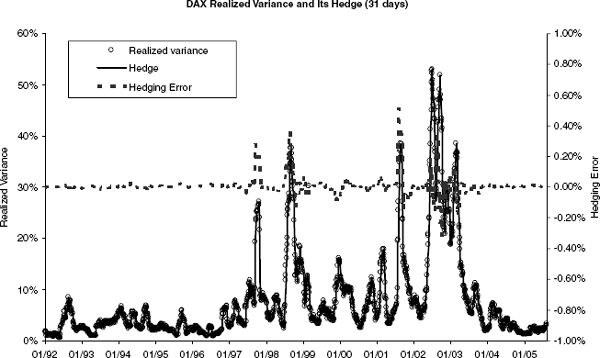

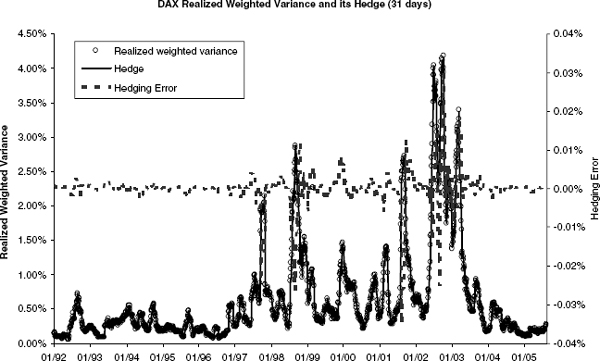

FIGURE 2.16 The quality of hedging variance swaps with (2.19). The graph shows daily the realized variance over 31 business days, the return from the hedging strategy (2.19), and the hedging error.

To assess the quality of the hedging strategy implied by this equation, we have used historic DAX returns and priced a variance swap against two log-contracts plus their daily delta-hedge. Figure 2.16 shows the impressive performance of this hedge.

To calculate the cost of exercising this strategy, note that under any equivalent matringale ![]() , the expectation of the right hand side of (2.19) is given as

, the expectation of the right hand side of (2.19) is given as

To compute ![]() , note that this value is equal to

, note that this value is equal to ![]() with H (x) = x − 1 − log x, the function shown in figure 1.6 on page 23.

with H (x) = x − 1 − log x, the function shown in figure 1.6 on page 23.

This function can also be used to center the strip of options around some “reference strike” ![]() To this end, note that

To this end, note that ![]() has a minimum of zero in

has a minimum of zero in ![]() We have

We have

that is,

Following this strategy, that is, taking a static position in ![]() instead of − log ST, requires an additional position in a future. See Demeterfi et al. [42] for an extensive discussion of this subject. Also, Carr/Madan discuss various extensions of the idea of pricing volatility-sensitive options via hedging arguments similar to (2.21) in [43]. For example, it can be shown that pricing H via (1.31) means that in actual fact, a corridor variance swap is priced, that is, the returns in the sum (2.16) will be counted only if the stock price is between the lowest and highest strike of (2.21). Therefore, a sufficiently wide strike range should be used. Corridor variance swaps and their hedging are discussed in Carr/Lewis [44].

instead of − log ST, requires an additional position in a future. See Demeterfi et al. [42] for an extensive discussion of this subject. Also, Carr/Madan discuss various extensions of the idea of pricing volatility-sensitive options via hedging arguments similar to (2.21) in [43]. For example, it can be shown that pricing H via (1.31) means that in actual fact, a corridor variance swap is priced, that is, the returns in the sum (2.16) will be counted only if the stock price is between the lowest and highest strike of (2.21). Therefore, a sufficiently wide strike range should be used. Corridor variance swaps and their hedging are discussed in Carr/Lewis [44].

REMARK 2.2.2 In some contracts, in particular for indices, realized variance is defined using equation (2.15), even if dividends are present. In that case, we have to evaluate

The additional terms ![]() (of which there are only finitely many) can be hedged and priced with European options using formula (1.29).

(of which there are only finitely many) can be hedged and priced with European options using formula (1.29).

Trading Volatility Apart from the fact that variance swaps can be hedged and priced using European options and a clearly defined delta-hedging strategy, what are the reasons to trade this product?

One motivation to trade in volatility is that apart from the stock, the price of an equity derivative is massively dependent on the volatility of the stock price. Practitioners therefore seek to protect themselves against moves in volatility. A very common method works as follows (assume that X = S): To price an option with payoff H(XT), we use the Black-Scholes model with a constant volatility σ,

where we estimate a reasonable σ from European options traded at maturity T. For example, we might decide that the payoff H is sufficiently close to a call with maturity T and strike k with a market price of ![]() 0(T, k) at time zero. Its implied volatility (cf. definition 1.2.1) is denoted by

0(T, k) at time zero. Its implied volatility (cf. definition 1.2.1) is denoted by ![]() , and we choose to use this implied volatility for our Black-Scholes model (2.22) by setting

, and we choose to use this implied volatility for our Black-Scholes model (2.22) by setting ![]() Let us

Let us ![]() to denote the real market price process.

to denote the real market price process.

Then, our price for H is given as

![]()

At some later time t, the value of H given the observed spot ![]() is then computed as

is then computed as

That works well if the real price process ![]() is a Black-Scholes diffusion with volatility σ. In reality, though, that is unlikely. Assume, for example, that in fact

is a Black-Scholes diffusion with volatility σ. In reality, though, that is unlikely. Assume, for example, that in fact

for some stochastic short variance ζ = (ζt)t≥0. Then, our price (2.23) evolves as

Using the fact that h is a Black-Scholes price for H and that it therefore satisfies the Black-Scholes PDE

![]()

we have

(See also the results from El Karoui, Jeanblanc-Picquè and Shreve [45].) The cost of our strategy to replicate H(XT) via its Black-Scholes hedge is therefore not covered by the initial price ![]() The term

The term

shows that we will have an additional contribution from the mismatch in volatility weighted by cash gamma ![]() 12 For convex payoffs, cash gamma will be positive, so we see that we lose money if the real variance ζ stays above σ, and we will gain if our initial guess was larger than the real variance. Equation (2.25) also reveals that it is not sufficient for a perfect hedge that the realized variance,

12 For convex payoffs, cash gamma will be positive, so we see that we lose money if the real variance ζ stays above σ, and we will gain if our initial guess was larger than the real variance. Equation (2.25) also reveals that it is not sufficient for a perfect hedge that the realized variance, ![]() equals σ2T.

equals σ2T.

Vega Hedging To protect ourselves against the profit and loss swings arising from a wrong volatility assumption in (2.25), it is natural to readjust the Black-Scholes volatility during the life of the product. After all, if we price the call (T, k) itself, we will not match the market as soon as its implied volatility changes.

Assume therefore that at some later time t, the call trades at some ![]() t ≡

t ≡ ![]() t(T, K). We can then infer its implied volatility

t(T, K). We can then infer its implied volatility ![]() by inverting the Black-Scholes price for the call,13

by inverting the Black-Scholes price for the call,13

![]()

Hence, the our price process for H is now given as

![]()

A common practice is to protect the position against the change in volatility by vega hedging. The idea is to buy as many calls ![]() t such that the overall sensitivity of the position to changes in both

t such that the overall sensitivity of the position to changes in both ![]() and

and ![]() is zero (recall that the derivative of a price with respect to volatility is called vega; hence the name vega hedging). In our case, this means first to define the Black-Scholes delta-neutral portfolio

is zero (recall that the derivative of a price with respect to volatility is called vega; hence the name vega hedging). In our case, this means first to define the Black-Scholes delta-neutral portfolio

![]()

and then build a hedging position

![]()

The first observation is that this strategy applied to the payoff H(XT) := (XT − k)+ will yield a perfect hedge: we simply hold ![]() . This is an advantage over the pure delta-hedging strategy discussed initially.

. This is an advantage over the pure delta-hedging strategy discussed initially.

However, it is clear that we still do not cover the cost of this hedge with our initial price, ![]() . Heuristically, we expect that the hedge above works better, but it is not clear that this is actually true in practice. Another problem with this approach is that it requires us, at least in this pure form, to select a reference option that can be used for vega hedging. In light of today's strong volatility skews, the choice of a strike is a tricky problem and requires a good knowledge of the product that we want to risk manage.14

. Heuristically, we expect that the hedge above works better, but it is not clear that this is actually true in practice. Another problem with this approach is that it requires us, at least in this pure form, to select a reference option that can be used for vega hedging. In light of today's strong volatility skews, the choice of a strike is a tricky problem and requires a good knowledge of the product that we want to risk manage.14

Here is where the variance swaps come in: Their price does not depend on a strike. Moreover, their payoff is directly the realized variance; hence, variance swaps are a more natural instrument to hedge against changes in volatility. Indeed, variance swap trades are in practice quoted in units of vega.

The idea behind trading vega is as follows: In terms of the variance swap volatility σ := K*(T), a variance swap with maturity T pays out the quantity σ2.

This payoff has a vega of

![]()

If we now assume that we have an overall vega exposure ν in our trading book, we can neutralize this exposure by buying

units of variance swaps (the quantity N is the “notional” of a trade of ν). This approach is consistent with the idea of hedging volatility exposure with variance swaps. (For a thorough account on this approach, see section 2.3). However, it requires that the vega of the portfolio is the sensitivity of the portfolio with respect to changes in the fair strike of the variance swap. In particular, it requires us to compute all option payoffs with a model that at least reprices the Europeans in (1.30) and therefore the variance swap itself.

More commonly, though, the vega of a book is an accumulated sum of Black-Scholes vegas across strikes (and possibly maturities), as discussed above. In this case, it seems sensible to assign the Black-Scholes vegas per strike weights according to (1.30). Of course, such an approach does not generally produce a perfect hedge, and it also disrespects changes in skew and kurtosis of the implied volatility surface.

Volatility as an Asset Class Apart from the potential use of variance swaps for vega hedging, they also offer the investor a way to invest in volatility. This can be attractive for many reasons. One of the most interesting properties is that volatility tends to be anticorrelated to movements of the market. Volatility increases if the market is falling and often decreases if the market rallies. (Note, though, that during the dotcom boom both price levels and volatility rose; cf. figure 2.3.) Now, most market participants would probably prefer to trade implied volatility in some way.

The drawback of using plain implied volatility as an underlying, however, is that once a strike of the respective option, to which the implied volatility refers, is fixed (for example at-the-money), this strike can entirely change its characteristics depending on the movements of the stock price. For example, if we start off with a strike at-the-money and the market starts to fall, we end up with an out-of-the money strike above current spot level. Implied volatility in this region often appears to be “cheap.” (For most indices, upside implied volatility is lower than at-the-money implied volatility.) Moreover, the farther out the strike, the less liquid the corresponding option becomes, with the effect of increasing transaction costs.

Here, variance swaps are a good and relatively inexpensive alternative (in terms of transaction costs). They offer exposure to volatility in a way that does not depend on the level of the market in the sense above. Indeed, cash gamma of a variance swap is simply constant 2, if we use the static replication strategy (2.21). In fact, we could also define the variance as the contract that has a constant cash gamma, that is, as the contract that always has the same sensitivity to changes in realized variance, regardless of the level of the stock. See Demeterfi et al. [42] for this approach. A linear cash gamma can be realized using gamma swaps, which are discussed below.

REMARK 2.2.3 The market's interest in trading volatility has led to the introduction of “variance indices,” notably VIX for SPX and VDAX for the GDAXI. These indices can be seen as rolling the square-root of variance swaps with a fixed maturity, a property that makes them very costly to replicate.

It is also noteworthy that trading in options on VIX futures started on CBOE in February 2006.

As soon as trading in variance swaps began, it became clear that variance swaps on single names are very sensitive to large price moves in the underlying asset, as can be seen easily from equation (2.15). In particular, the payout will be infinite if the asset defaults (recall that in practice, the case of default is not excluded by using definition (2.16)). For this reason, investors who sold variance swaps have requested to impose a cap on the potential payout of a variance swap. Typically, this cap is around 250% of K2; that is, the payoff of such a capped variance swap is, in the absence of dividends,

![]()

This is equivalent to

![]()

The latter payoff is also valid in the presence of dividends if (2.16) is used plus the additional payoff of 250%K2 in the event of default.

By requesting protection against extreme stock price movements, investors who sold the capped variance swaps essentially bought out-of-the-money calls on variance. The availability of such products then spurred the development of more standard options: common options on variance that are available today are simple calls

and puts

but also volatility swaps with payoff

![]()

(Note that value of a zero-strike volatility swap is always less than the value of a zero-strike variance swap.) More recently, options on forward variance swaps have emerged. For example, a call on forward variance between T1 and T2 has at time T1 the payoff

![]()

where Vt(T1, T2) is the price at time t of the variance between T1 and T2, that is,

![]()

It should be noted that this contract has a different nature than a forward starting call on variance swap, which pays at T2 the quantity

![]()

where k is now a relative strike.

REMARK 2.2.4 (Quoting Conventions) European options on variance such as (2.27) and (2.28) are usually quoted in terms of “vol points,”

![]()

As before, K*(T) denotes the variance swap volatility.

2.2.2 Entropy Swaps

Since variance swaps offer exposure to the realized volatility of the returns of the stock X, they are relatively insensitive to the level of the stock price.15 As an alternative measure of variance, it is possible to define the payoff of what we will call an entropy swap as

Intuitively, this “entropy variance” has the convenient property that if stock price and short variance are negatively correlated, then rises in one quantity are offset by falls of the other. Moreover, if the market drifts sidewards (i.e., the level of X does not change much), then the payoff behaves roughly like a variance swap: If the instantaneous correlation between X and ζ is zero, then the value of weighted variance and standard variance are equal. Price and hedging strategy of such a swap can be computed using the same ideas as above. To this end, note that

Hence, pricing an entropy swap boils down to approximate the convex and bounded function H(x) := x log x − x + 1 via (1.29); while the weights for evaluating a variance swap via (1.29) are given as 1/k2, they are 1/k in the case of an entropy swap. Since X is a martingale with X0 = 1, we can compute the value of an entropy swap with maturity T at time 0 as

![]()

Let us define the stock price measure ![]() by setting

by setting ![]() for all A ∈ FT and all T < ∞. This measure is given by using X itself as a numeraire, and the above expression shows that

for all A ∈ FT and all T < ∞. This measure is given by using X itself as a numeraire, and the above expression shows that ![]() is simply the relative entropy of

is simply the relative entropy of ![]() with respect to

with respect to ![]() , hence the name entropy swap.

, hence the name entropy swap.

Shadow Options The connection between an entropy swap and the measure ![]() goes further: we have

goes further: we have

In other words, the price of an entropy swap is the value of a variance swap under ![]() . With regard to this measure, recall that we used U(T, k) to denote a put on X with strike k and maturity T. Hence,

. With regard to this measure, recall that we used U(T, k) to denote a put on X with strike k and maturity T. Hence,

where we call CX following Lewis [23] the “shadow call” on X. It is the call on ![]() under the numeraire X. The shadow put uX is defined similarly; together we have

under the numeraire X. The shadow put uX is defined similarly; together we have

Hence, the shadow option prices can be read from the market. So, in principle, we could compute the value of an entropy swap, ![]() using (1.29) in terms of shadow options.

using (1.29) in terms of shadow options.

2.2.3 Gamma Swaps

While entropy swaps are an interesting alternative to variance swaps, they are not particularly well suited for real-life investments, because they require us to strip dividends, repo, and interest rates from the traded stock price, S, in order to obtain X. This is very unnatural from an economic point of view and inconveniences the investor. This drawback can be overcome by using what are called gamma swaps or weighted variance swaps: A gamma swap pays at maturity the weighted variance of the stock price,

Assuming that there are no cash dividends, we approximate (2.30) as

![]()

A gamma swap has the same attractive property as the entropy swap of being exposed to correlation between stock price and volatility. See figure 2.17 for past performance of gamma swaps. Under the assumption of continuity of X, the price of a gamma swap is

FIGURE 2.17 Past performance of 1y variance and gamma swaps on STOXX50E. We have also plotted the return performance of the index.

(recall the symbols ![]() and At from page 7). In other words, a gamma swap is a sequence of forward variance swaps and forward entropy swaps. We can approximate its price as

and At from page 7). In other words, a gamma swap is a sequence of forward variance swaps and forward entropy swaps. We can approximate its price as

When it comes to hedging a gamma swap, let h ≡ 0 and define H(x) := x log x − x + 1 as above. Let us also recall equation (1.12) and Ito's formula (1.13). They give us again a hedging program,

similar to (2.19). Here, we can see why the product is called gamma swap: The cash gamma ![]() for this product is

for this product is ![]() (i.e., linear in spot). The performance of this hedge for real-life gamma swaps is as good as it is for variance swaps, as figure 2.18 shows.

(i.e., linear in spot). The performance of this hedge for real-life gamma swaps is as good as it is for variance swaps, as figure 2.18 shows.

FIGURE 2.18 The quality of hedging weighted variance swaps with (2.31). The graph shows the daily realized weighted variance over 31 business days, the return from the hedging strategy (2.19), and the hedging error.

2.3 VARIANCE SWAP MARKET MODELS

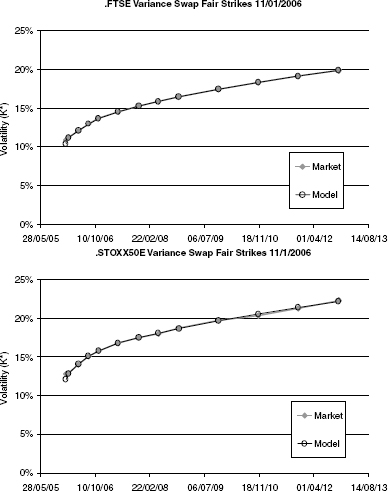

While the evaluation of variance swaps, entropy swaps and gamma swaps is relatively model independent, such formulas are not known for options on realized variance, as introduced in section 2.2.1.16 To price and hedge a call (2.27) on realized variance on a stock where only European options are traded, we have to use a particular stock price model. In this section we will discuss a general modeling approach that is based on the idea to hedge options on variance with variance swaps. As an illustration, figure 2.19 shows the term structure of variance swap fair strikes K* for a few major indices. The aim is to model the entire curve of variance swaps as a random variable and then derive in a second step the dynamics of a stock price process that realizes the modeled variance. (We do not attempt to develop a model that prices variance swaps; rather, their prices are input parameters for the model.) Of course, a model that describes well the evolution of variance swap price curves cannot only be used to hedge options on realized variance. Since we will also provide an “associated stock price process” in the model (and an intuitive meaning of correlation), we can use such a model to price and hedge any exotic derivative. For example, it is natural to hedge Cliquet-type products as discussed in section 2.1.6 using forward started variance swaps.17 This approach is particularly appealing in the light of recent trading volumes in variance swaps.

FIGURE 2.19 Variance swap fair strikes for major stock price markets.

The entire approach is very similar to the Heath-Jarrow-Merton (HJM) approach [47] in interest rates. There, the dynamics of the forward interest rates are modeled as stochastic variables; we will consider forward variance. The basic assumption is that alongside the “pure” stock X, at any time t, (zero-strike) variance swaps for all finite maturities with prices

![]()

are liquidly traded. Under the assumption of “no free lunch with vanishing risk,” there exists an equivalent measure ![]() under which both X and all variance swap price processes and therefore V = (VT))T≥0 are local martingales (for ease of exposure we will frequently refer to V(T) as the price process of a variance swap even though, strictly speaking, the price process is V(T)/[T]). While variance swap prices V are readily available in the market, they are slightly difficult to model directly: Since the prices Vt = (Vt(T))T≥t of variance swaps have to be increasing in T at any time t, it is more natural to work instead with the forward variances

under which both X and all variance swap price processes and therefore V = (VT))T≥0 are local martingales (for ease of exposure we will frequently refer to V(T) as the price process of a variance swap even though, strictly speaking, the price process is V(T)/[T]). While variance swap prices V are readily available in the market, they are slightly difficult to model directly: Since the prices Vt = (Vt(T))T≥t of variance swaps have to be increasing in T at any time t, it is more natural to work instead with the forward variances

Forward variance is “the market's expectation” at time t of the variance at time T, just as the forward rate in interest rates is the expectation of the short interest rate under the forward measure. (Note that in contrast to a forward rate, a forward variance of zero is a natural state, for example, on weekends.) The main point is that due to its definition (2.32), forward variance itself is tradable and must therefore be a local martingale under a pricing measure, if such a measure exists.

As with interest rates, it is much more natural to look at the evolution of the forward variance curve over time in “fixed time-to-maturity,” rather than a fixed maturity. We expect the properties of forward variance vt(T) to change markedly during the remaining time to maturity T − t: for example, very long-term forward variance should not be as volatile as short-term forward variance. It is therefore more convenient to use the Musiela parametrization18 of forward variance,

Accordingly, the price of a variance swap (modulo scaling by the inverse of time-to-maturity) in Musiela-parametrization is

![]()

HJM Theory for Variance Swaps The idea of “variance curve models” as introduced by Buehler [49] is now to start by specifying the dynamics of the family u = (u(x))x≥0 itself, just as HJM-type interest rate models are specified by starting with the forward rate dynamics. The additional complication in the case of forward variance is that we do not only want to model the variance swap prices in this way, but we also need to model a consistent stock price process whose expected realized variance is the price of the respective variance swap. We ignore the effects of dividends in this section.

To formalize our setup, assume that we have a d-dimensional Brownian motion W = (W1, …, Wd) under a measure ![]() , which creates the filtration

, which creates the filtration ![]() We will model the variance curves directly under their martingale measure; the ideas from section 1.4 will then be used to derive conditions on market completeness. Assume that u = (u(x))x≥0 is a family of non-negative processes u(x) = (ut(x))t≥0 given by

We will model the variance curves directly under their martingale measure; the ideas from section 1.4 will then be used to derive conditions on market completeness. Assume that u = (u(x))x≥0 is a family of non-negative processes u(x) = (ut(x))t≥0 given by

for some integrable predictable processes α and β = (β1, …, βd). Reversing the construction above, we can then define the forward variance processes v = (v(T))T≥0 by setting

(note that vt(T) is well-defined for t > T). Equivalently, the variance swap price processes for finite maturities T are defined as

![]()

DEFINITION 2.3.1 We call u given by (2.34) a variance curve model if v(T) given by (2.35) is a local martingale for all T < ∞ and if there exists a local martingale X for the stock price such that

![]()

for all t and all T < ∞.

Let us assess when a curve u is indeed a variance curve model.19 First of all, it is natural to assume that all initial variance swap prices are finite, that is,

![]()

for all x < ∞. Indeed, if this does not hold, the expected value of the logarithm of X cannot exist. Second, we have to ensure that for each T < ∞, the process v(T) is a local martingale. To this end, we require that β is in C1 and its derivative ∂xβ(x) is integrable with respect to Brownian motion. Then,

which implies that the following HJM drift condition for forward variance must hold:

![]()

As a next step, note that the process

is an adapted non-negative process. Since ![]() its square root

its square root ![]() is integrable with respect to any Brownian motion B. Each such Brownian motion B can be written in terms of W as

is integrable with respect to any Brownian motion B. Each such Brownian motion B can be written in terms of W as

where ρ = (ρ1, …, ρd) is some potentially stochastic “correlation vector” with values in [−1, +1]d, which always has unit norm, ![]() This means that

This means that

![]()

is a well-defined local martingale with the property that

just as required. We call X an associated stock price process to u.

The Brownian motion B or, alternatively, the correlation vector ρ was arbitrary in the construction of X. Indeed, B plays the role of a “correlation” or “skew” parameter: If the dynamics of u in the form of β are given, then the specification of ρ links the movement of the variance curve with the stock price movement. In particular, this implies that volatility structure of the variance curve and its correlation with the stock price movement can be estimated one after the other.

However, the general formulation of a variance curve above in terms of equation (2.34) plus the requirement of non-negativity is more subtle than it may appear in the first place. Indeed, it is very difficult to assess whether a general stochastic integral (2.34) will remain non-negative. In particular it means that we cannot—as in the HJM-framework for interest rates—specify the volatility structure β independently of the initially observed forward variance curve u0.

A natural approach to this problem is to model u as an exponential,

![]()

where w satisfies the integral equation

Applying our previous results implies the HJM-type drift condition

This approach is well suited for statistical estimation of a volatility structure independent of the initial state u0 of the variance curve, for example, via a PCA-type estimation of the factors driving the curve. However, it should be noted that this approach also excludes all those classical stochastic volatility models that allow the volatility to reach zero, such as Heston's. Moreover, it is usually more complicated to ensure a true martingale property for the process X if u is given in the form above: recall in particular Jourdain's results [25] for the SABR model and for Scott's model, which we discussed in sections 2.1.2 and 2.1.3, respectively. Nonetheless, given a “volatility structure” w that ensures the martingale property for all initial values u, the above formulation can be used to “fit the market.” This will be discussed in section 2.3.3.

2.3.1 Finite Dimensional Parametrizations

One drawback of our approach so far is that we formulated the dynamics for u in a very general way. But in practice, the formulation of u in terms of a predictable integral equation (2.34) is inconvenient for numerical purposes. Moreover, this formulation implies that the entire curve u is the state of the process, an object difficult to handle on a computer. What we are really interested in is a finite-dimensional representation of the curve u. Indeed, in real life, a finite number of variance swap market quotes is usually interpolated or approximated by some nonnegative increasing functional ![]() , which itself depends on only a finite number of parameters

, which itself depends on only a finite number of parameters ![]() If Zt is the parameter vector at time t, this means that the price at time t of a variance swap starting in t with time-to-maturity x is given as

If Zt is the parameter vector at time t, this means that the price at time t of a variance swap starting in t with time-to-maturity x is given as

![]()

Since the function ![]() must be increasing in x, we can set